false 0000763901 0000763901 2024-01-25 2024-01-25 0000763901 us-gaap:CommonStockMember 2024-01-25 2024-01-25 0000763901 us-gaap:CumulativePreferredStockMember 2024-01-25 2024-01-25

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 8-K

CURRENT REPORT

Pursuant to Section 13 OR 15(d)

of the Securities Exchange Act of 1934

Date of Report (Date of earliest event reported): January 25, 2024

POPULAR, INC.

(Exact name of registrant as specified in its charter)

|

|

|

|

|

| Puerto Rico |

|

001-34084 |

|

66-0667416 |

| (State or other jurisdiction of incorporation or organization) |

|

(Commission File Number) |

|

(IRS Employer Identification Number) |

|

|

|

| 209 Muñoz Rivera Avenue Hato Rey, Puerto Rico |

|

00918 |

| (Address of principal executive offices) |

|

(Zip code) |

(787) 765-9800

(Registrant’s telephone number, including area code)

NOT APPLICABLE

(Former name, former address and former fiscal year, if changed since last report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General Instruction A.2. below):

| |

☐ |

Written communication pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| |

☐ |

Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| |

☐ |

Pre-commencement communication pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| |

☐ |

Pre-commencement communication pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Securities registered pursuant to Section 12(b) of the Act:

|

|

|

|

|

| Title of each class |

|

Trading Symbol(s) |

|

Name of each exchange on which registered |

| Common Stock ($0.01 par value) |

|

BPOP |

|

The NASDAQ Stock Market |

| 6.125% Cumulative Monthly Income Trust Preferred Securities |

|

BPOPM |

|

The NASDAQ Stock Market |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

| Item 2.02. |

Results of Operations and Financial Condition. |

On January 25, 2024, Popular, Inc. (the “Corporation”) issued a press release announcing its unaudited financial results for the quarter ended December 31, 2023, a copy of which is attached as Exhibit 99.1 to this Current Report on Form 8-K.

The information furnished pursuant to this Item 2.02 of this Current Report on Form 8-K, including Exhibit 99.1, shall not be deemed “filed” for purposes of the Securities Exchange Act of 1934, as amended, nor shall it be incorporated by reference into any of the Corporation’s filings under the Securities Act of 1933, as amended, unless otherwise expressly stated in such filing.

| Item 7.01. |

Regulation FD Disclosure. |

The Corporation is furnishing information regarding its conference call to discuss its financial results for the quarter ended December 31, 2023. A copy of the presentation to be used by the Corporation on the conference call is attached hereto as Exhibit 99.2.

The information furnished pursuant to this Item 7.01 of this Current Report on Form 8-K, including Exhibit 99.2, shall not be deemed “filed” for purposes of the Securities Exchange Act of 1934, as amended, nor shall it be incorporated by reference into any of the Corporation’s filings under the Securities Act of 1933, as amended, unless otherwise expressly stated in such filing.

| Item 9.01. |

Financial Statements and Exhibits. |

Exhibits 99.1 and 99.2 shall not be deemed to be “filed” for purposes of the Securities Exchange Act of 1934, as amended.

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, as amended, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

|

|

|

|

|

|

|

| |

|

|

|

POPULAR, INC. (Registrant) |

|

|

|

|

| Date: January 25, 2024 |

|

|

|

By: |

|

/s/ Jorge J. García |

|

|

|

|

|

|

Jorge J. García |

|

|

|

|

|

|

Senior Vice President and Corporate Comptroller |

Exhibit 99.1

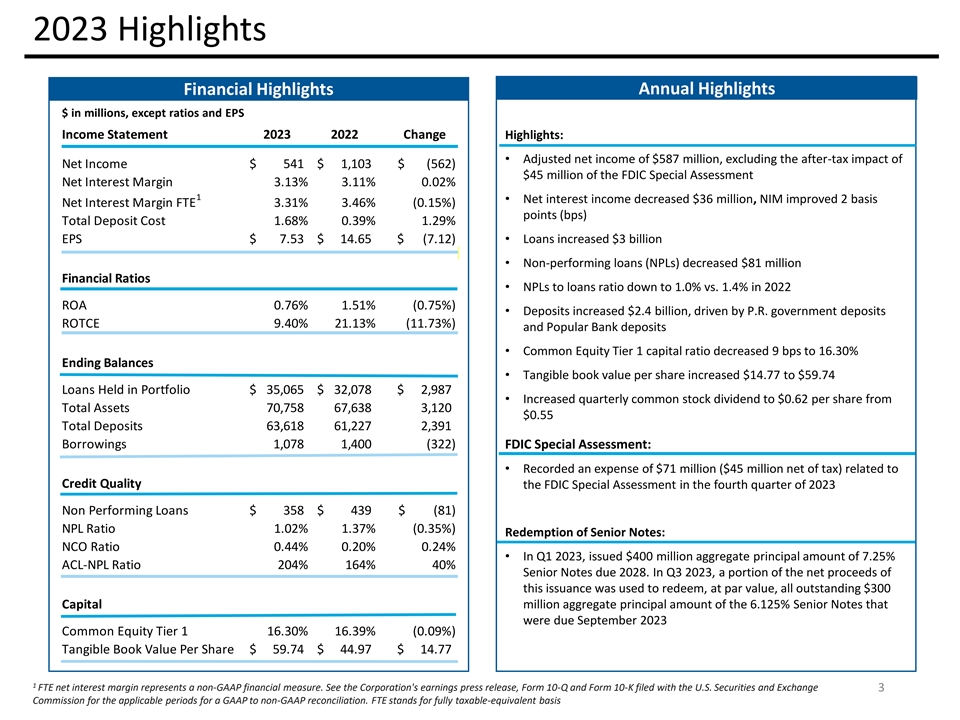

Popular, Inc. Announces Fourth Quarter 2023 Financial Results

| |

• |

|

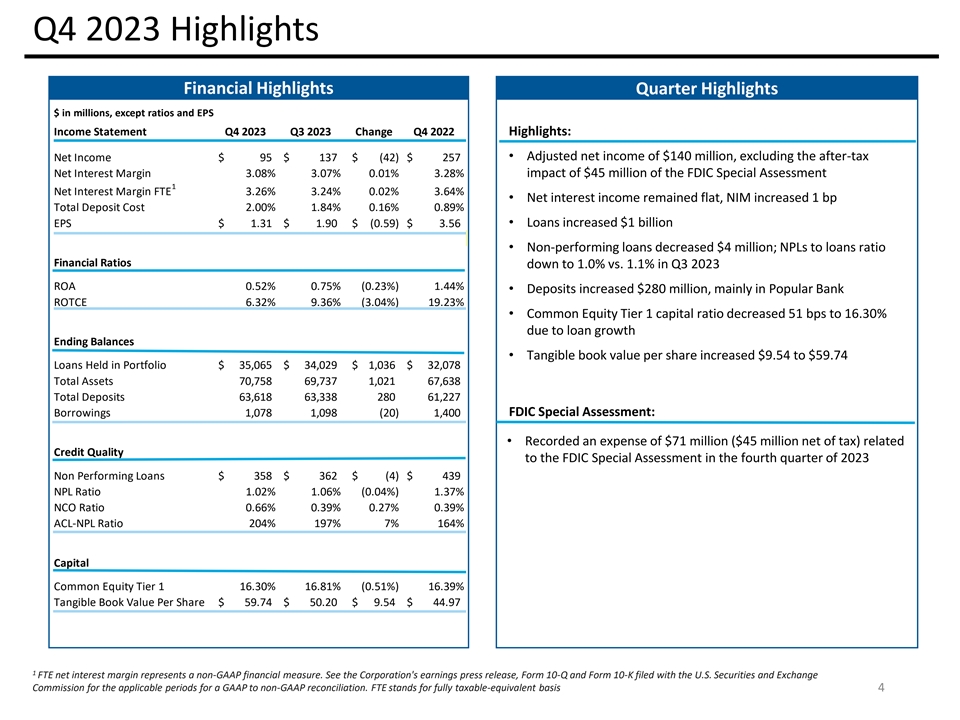

Net income of $94.6 million in Q4 2023, compared to net income of $136.6 million in Q3 2023;

excluding the $45.3 million after-tax impact during the fourth quarter of the FDIC Special Assessment (defined below), adjusted net income was $139.9 million. |

| |

• |

|

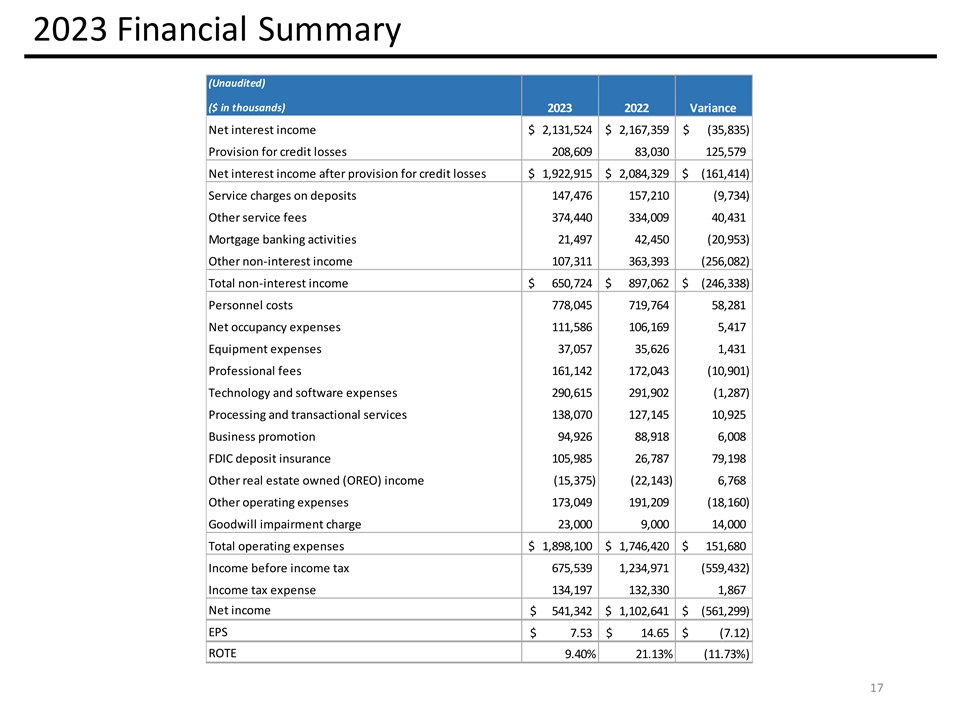

Net income of $541.3 million for the year 2023, compared to net income of $1.1 billion for the year

2022. Excluding the effects of the FDIC Special Assessment, the adjusted net income for the year 2023 was $586.6 million, compared to an adjusted net income of $807.8 million for the year 2022, excluding the effects of the partial release

of $68.2 million of the deferred tax asset valuation allowance and the $226.6 million impact of the completed Evertec Transactions and related accounting adjustments, in which the Corporation acquired certain critical channels from

Evertec, Inc. (“Evertec”) and completed the sale of its shares of Evertec. |

| |

• |

|

Net interest income amounted to $534.2 million, flat compared to Q3 2023. |

| |

• |

|

Net interest margin of 3.08% in Q4 2023, compared to 3.07% in Q3 2023; net interest margin on a taxable

equivalent basis of 3.26% in Q4 2023, compared to 3.24% in Q3 2023. |

| |

• |

|

Non-interest income of $168.7 million, an increase of

$9.2 million compared to Q3 2023. |

| |

• |

|

Operating expenses amounted to $531.1 million, including the

before-tax $71.4 million FDIC Special Assessment; an increase of $65.2 million compared to Q3 2023. Excluding the FDIC Special Assessment, operating expenses decreased by $6.2 million.

|

| |

• |

|

Non-performing loans held-in-portfolio (“NPLs”) decreased by $3.9 million from Q3 2023; NPLs to loans ratio at 1.0% vs. 1.1% in Q3 2023; |

| |

• |

|

Net charge-offs (“NCOs”) increased by $24.3 million from Q3 2023; annualized NCOs at 0.66% of

average loans held-in-portfolio vs. 0.39% in Q3 2023; |

| |

• |

|

Allowance for credit losses (“ACL”) to loans held-in-portfolio at 2.08% vs. 2.09% in Q3 2023; and |

| |

• |

|

ACL to NPLs at 204.0% vs. 196.7% in Q3 2023. |

| |

• |

|

Loans ending balances increased by $1.0 billion and by $1.0 billion in average quarterly balances,

from Q3 2023. |

| |

• |

|

Ending deposit balances increased by $280.6 million while average quarterly balances increased by

$285.9 million, from Q3 2023. |

| |

• |

|

Common Equity Tier 1 ratio of 16.30%, Common Equity per Share of $71.03 and Tangible Book Value per Share of

$59.74 at December 31, 2023. |

SAN JUAN, Puerto Rico – (BUSINESS WIRE) – Popular, Inc. (the “Corporation,”

“Popular,” “we,” “us,” “our”) (NASDAQ:BPOP) reported net income of $94.6 million for the quarter ended December 31, 2023, compared to net income of $136.6 million for the quarter ended

September 30, 2023. Excluding the impact during the fourth quarter of the FDIC Special Assessment, adjusted net income was $139.9 million.

Ignacio Alvarez, President and Chief Executive Officer, said: “We delivered solid fourth quarter and year-end results and entered 2024 with strong

momentum. Notwithstanding the interest rate environment and the disruptions in the banking market early in the year, we were able to maintain stable net interest income as we grew loans by approximately $1 billion during the quarter and a total

of $3 billion for the full year.

We continued to experience strong client activity during the year, growing our customer base in

Puerto Rico by 34,000 reflecting the continued strength of the local economy and our diversified product offerings. Excluding the gain from the Evertec transaction in 2022, we grew non-interest income by $11 million. While we saw some credit

normalization in our consumer portfolios, credit quality remained strong. We were also able to manage our operating expenses at the same time we continued to invest in our transformation efforts.

Our CET1 ratio at year-end was 16.3% and our tangible equity increased by 33%, or $14.77 per share. Our strong liquidity and capital

ratios position us well to continue to support responsible growth in 2024.

I would like to express my gratitude and appreciation to our

employees for all their hard work and dedication during the year. While conscious that we are living in a period of great uncertainty, the outlook for the macroenvironment in Puerto Rico remains positive and we look forward to 2024 with

optimism.”

1

Significant Events

FDIC Special Assessment

On

November 16, 2023, the Federal Deposit Insurance Corporation (“FDIC”) approved a final rule that imposes a special assessment (the “FDIC Special Assessment”) to recover the losses to the deposit insurance fund

(“DIF”) resulting from the FDIC’s use, in March 2023, of the systemic risk exception to the least-cost resolution test under the Federal Deposit Insurance Act in connection with the receiverships of several failed banks.

Under the final rule, the assessment base for the special assessment is equal to an insured depository institution’s (“IDI”) estimated

uninsured deposits, as reported in the IDI’s December 31, 2022 Call Report, excluding the first $5 billion in estimated uninsured deposits. For a holding company that has more than one IDI subsidiary, such as Popular, the

$5 billion exclusion is allocated among the company’s IDI subsidiaries in proportion to each IDI’s estimated uninsured deposits. The special assessments would be collected at an annual rate of approximately 13.4 basis points per year

(3.35 basis points per quarter) over eight quarters in 2024 and 2025, with the first assessment period beginning January 1, 2024. In their December 31, 2022 Call Reports, Banco Popular de Puerto Rico (“BPPR”) and Popular Bank

(“PB”) reported estimated uninsured deposits of approximately $28.1 billion, including $16.2 billion in fully collateralized public sector deposits, and $3.5 billion, respectively. The Corporation recorded an expense of

$71.4 million, $45.3 million net of tax, in the fourth quarter of 2023, representing the full amount of the assessment.

Increase in

quarterly common stock dividends

During the fourth quarter of 2023, the Corporation declared a quarterly common stock cash dividend of $0.62

per share, an increase of $0.07, or 13%, compared to the $0.55 per share declared by the Corporation in the third quarter of 2023.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Earnings Highlights |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| (Unaudited) |

|

Quarters ended |

|

|

Years ended |

|

| (Dollars in thousands, except per share information) |

|

31-Dec-23 |

|

|

30-Sep-23 |

|

|

31-Dec-22 |

|

|

31-Dec-23 |

|

|

31-Dec-22 |

|

| Net interest income |

|

$ |

534,180 |

|

|

$ |

534,020 |

|

|

$ |

559,566 |

|

|

$ |

2,131,524 |

|

|

$ |

2,167,359 |

|

| Provision for credit losses |

|

|

78,663 |

|

|

|

45,117 |

|

|

|

49,531 |

|

|

|

208,609 |

|

|

|

83,030 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net interest income after provision for credit losses |

|

|

455,517 |

|

|

|

488,903 |

|

|

|

510,035 |

|

|

|

1,922,915 |

|

|

|

2,084,329 |

|

| Other non-interest income |

|

|

168,743 |

|

|

|

159,549 |

|

|

|

158,465 |

|

|

|

650,724 |

|

|

|

897,062 |

|

| Operating expenses |

|

|

531,145 |

|

|

|

465,984 |

|

|

|

461,708 |

|

|

|

1,898,100 |

|

|

|

1,746,420 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Income before income tax |

|

|

93,115 |

|

|

|

182,468 |

|

|

|

206,792 |

|

|

|

675,539 |

|

|

|

1,234,971 |

|

| Income tax (benefit) expense |

|

|

(1,479 |

) |

|

|

45,859 |

|

|

|

(50,347 |

) |

|

|

134,197 |

|

|

|

132,330 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net income |

|

$ |

94,594 |

|

|

$ |

136,609 |

|

|

$ |

257,139 |

|

|

$ |

541,342 |

|

|

$ |

1,102,641 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net income applicable to common stock |

|

$ |

94,241 |

|

|

$ |

136,256 |

|

|

$ |

256,786 |

|

|

$ |

539,930 |

|

|

$ |

1,101,229 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net income per common share-basic |

|

$ |

1.31 |

|

|

$ |

1.90 |

|

|

$ |

3.56 |

|

|

$ |

7.53 |

|

|

$ |

14.65 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net income per common share-diluted |

|

$ |

1.31 |

|

|

$ |

1.90 |

|

|

$ |

3.56 |

|

|

$ |

7.52 |

|

|

$ |

14.63 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net interest income on a taxable equivalent basis – Non-GAAP financial

measure

Net interest income, on a taxable equivalent basis, is presented with its different components in Tables D and E for the quarter ended

December 31, 2023 and comparable quarters September 30, 2023 and December 31, 2022, respectively, and Table F for the year ended December 31, 2023 and 2022. Net interest income on a taxable equivalent basis is a non-GAAP financial measure. Management believes that this presentation provides meaningful information since it facilitates the comparison of revenues arising from taxable and

tax-exempt sources.

Non-GAAP financial measures used by the Corporation

may not be comparable to similarly named non-GAAP financial measures used by other companies.

2

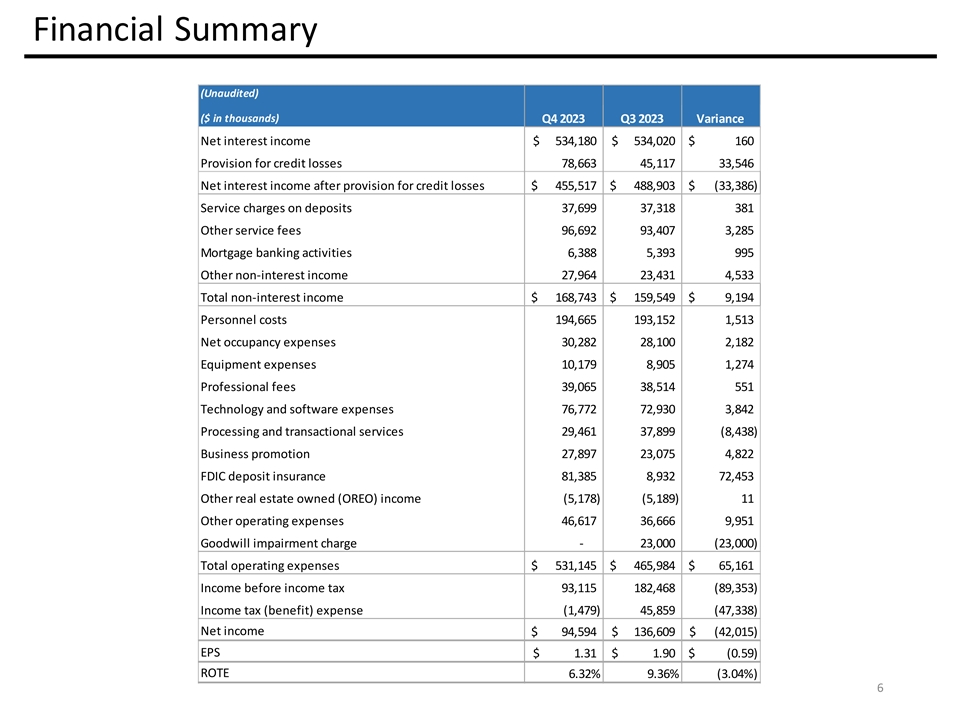

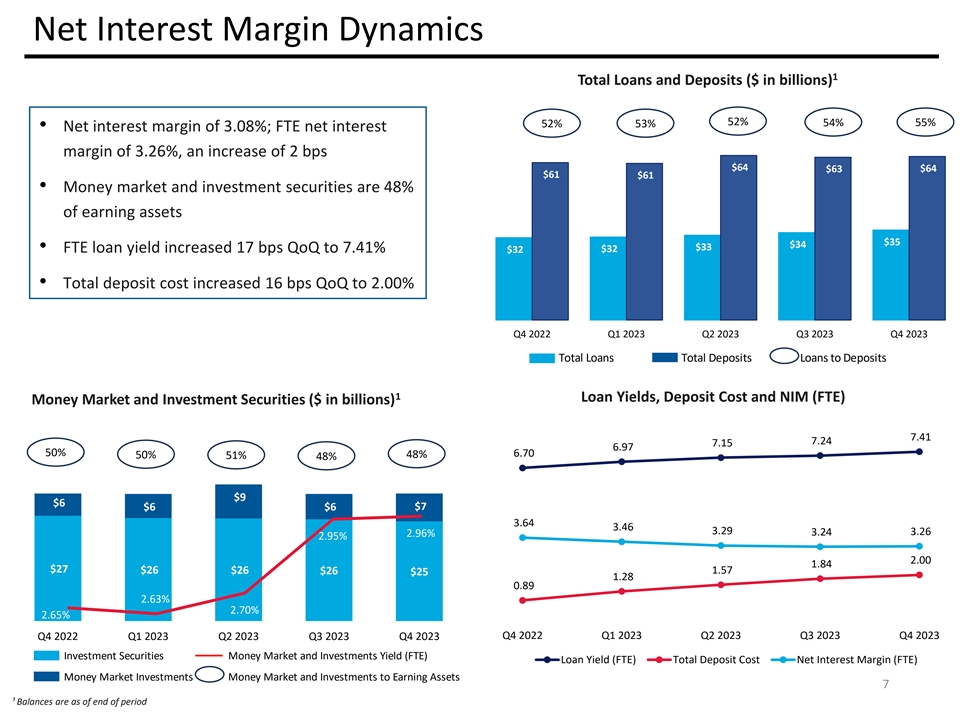

Net interest income for the quarter ended December 31, 2023 was $534.2 million, flat when compared

to $534.0 million in the previous quarter. Net interest income on a taxable equivalent basis for the fourth quarter of 2023 was $564.8 million, compared to $563.7 million in the previous quarter, an increase of $1.1 million.

Net interest margin for the fourth quarter of 2023 was 3.08% compared with 3.07% in the prior quarter. On a taxable equivalent basis, net interest margin for

the fourth quarter of 2023 was 3.26%, compared to 3.24% for the prior quarter. The main quarter over quarter variances in net interest income on a taxable equivalent basis were:

| |

• |

|

Higher interest income from loans by $32.4 million resulting from an increase in average loans by

$995 million, reflecting increases in BPPR and PB of $729 million and $266 million, respectively. All major loan categories in BPPR increased, while at PB the increase was mainly in the commercial and construction portfolios. Loan

originations in a higher interest rate environment and the repricing of adjustable-rate loans resulted in a higher yield on loans by 17 basis points. All loan categories resulted in a higher yield quarter over quarter; |

partially offset by:

| |

• |

|

Lower interest income from investment securities, trading and money market investments by $8.7 million

driven mainly by lower volume of U.S. Treasury Securities, partially offset by stable volume of money market investments at a higher yield by seven basis points. The increase in the yield of money market investments is driven by the full quarter

effect of the 25 basis points increase in market rates that occurred at the end of July; and |

| |

• |

|

Higher interest expense on deposits by $25.1 million, mainly from the increase in cost of Puerto Rico

government deposits by 34 basis points, or $10.3 million, and a higher volume and cost of PB interest bearing deposits by $555 million and 34 basis points, respectively, or $12.6 million. |

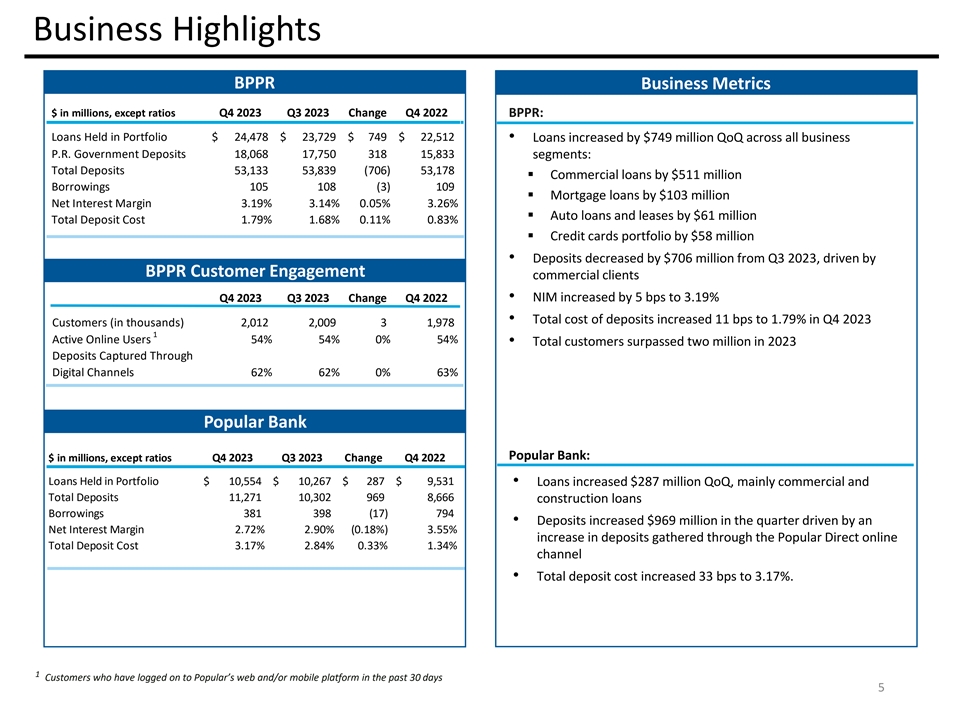

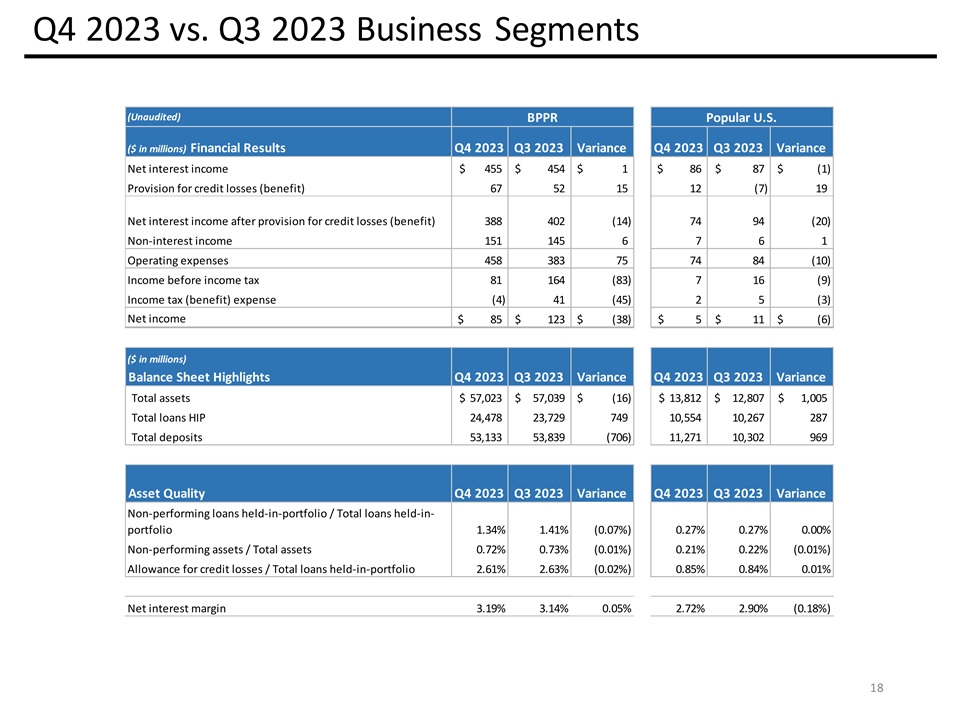

Net interest income for the BPPR segment amounted to $454.9 million for the fourth quarter of 2023, an increase of $1.0 million when compared to

$453.9 million in net interest income during the third quarter of 2023. Net interest margin for the BPPR segment increased five basis points to 3.19% compared to 3.14% in the third quarter of 2023. The increase in net interest margin reflects a

higher volume of loans by $729 million across all loan categories, except construction loans, partially offset by a lower volume of investment securities, trading and money market investments by $1.6 billion driven by a decrease in

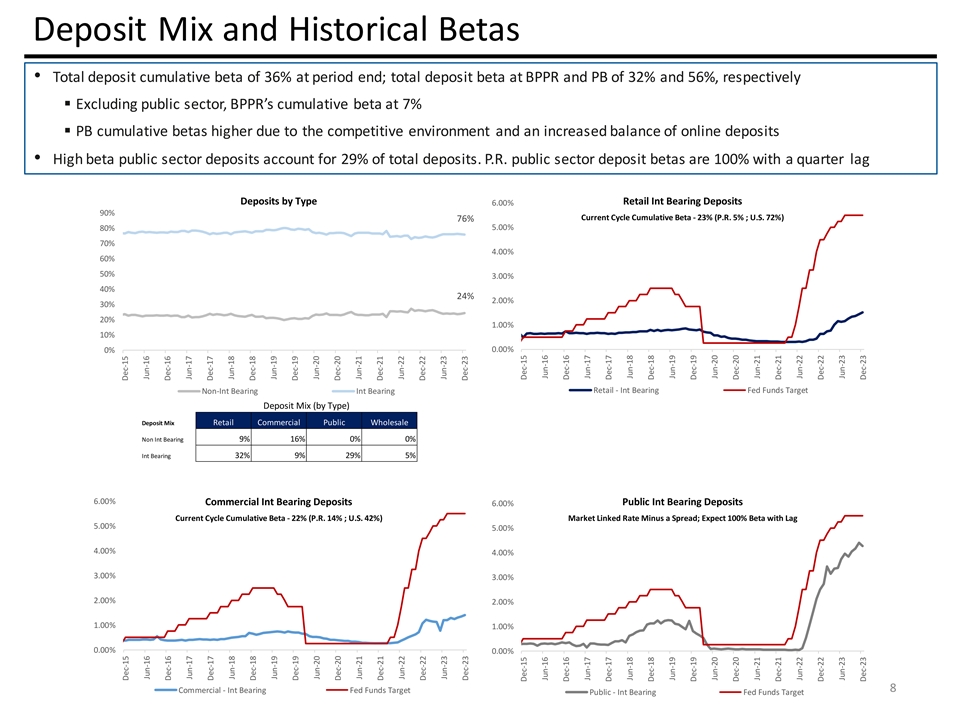

deposits of $1.0 billion and a higher cost of deposits, mainly Puerto Rico government deposits. Earning assets yield improved 14 basis points from 4.74% to 4.88% in Q4 2023. The cost of interest-bearing deposits increased by 16 basis points to

2.41% from 2.25% the previous quarter. The increase in the cost of deposits mainly resulted from the repricing of public funds. Total deposit cost in the fourth quarter of 2023 was 1.79%, compared to 1.68% in the third quarter of 2023, an increase

of 11 basis points.

Net interest income for PB was $85.6 million for the quarter ended December 31, 2023, a decrease of $1.8 million when

compared to $87.4 million during the previous quarter. Net interest margin decreased by 18 basis points in the quarter to 2.72%, compared to 2.90% in the third quarter of 2023. The decrease in net interest margin was mostly driven by a higher

cost of deposits, partially offset by a higher volume of loans and the repricing of adjustable-rate loans in the current interest rate environment. The cost of interest-bearing deposits was 3.66%, compared to 3.31% for the third quarter, or an

increase of 34 basis points, while total deposit cost was 3.17%, compared to 2.84% in the previous quarter.

Non-interest income

Non-interest income amounted to $168.7 million for the fourth quarter of 2023, an increase of $9.2 million

when compared to $159.5 million for the quarter ended September 30, 2023. The variance in non-interest income was driven primarily by:

| |

• |

|

a favorable variance in the fair value adjustment of equity securities by $3.6 million, mainly related to

securities held for deferred benefit plans, which have an offsetting effect in personnel costs; |

| |

• |

|

higher other service fees by $3.3 million due to an increase in contingent insurance commissions that are

typically received during the fourth quarter and higher debit and credit card fees due to higher transactional volumes; and |

| |

• |

|

a favorable variance in the adjustment for indemnity reserve on loans previously sold of $2.5 million.

|

Refer to Table B for further details.

3

Operating expenses

Operating expenses for the fourth quarter of 2023 totaled $531.1 million, including higher FDIC deposit insurance expense by $72.5 million due to the

impact of the FDIC Special Assessment, an increase of $65.2 million when compared to the third quarter of 2023. Excluding the effect of the FDIC Special Assessment, total expenses for the fourth quarter of 2023 were $459.7 million,

compared to $466.0 million in the previous quarter. During the fourth quarter of 2023, the Corporation incurred approximately $4.8 million in costs related to its technological and business process transformation initiative, compared to

$3.8 million in the previous quarter, mainly in professional services and personnel costs. During the year 2023, the Corporation incurred approximately $21.5 million in transformation related costs, compared to $24.6 million incurred

during the second half of the year 2022. The other variances in operating expenses for the quarter were driven primarily by:

| |

• |

|

higher other taxes expense by $6.0 million mainly due to an accrual reversal of $8.2 million during the

third quarter of 2023 related to regulatory examination fees in BPPR; |

| |

• |

|

higher business promotion expense by $4.8 million mainly due to $5.4 million of seasonal projects and

higher donations granted during the quarter; partially offset by lower customer rewards programs expense in our credit card business by $2.0 million; |

| |

• |

|

higher other operating expenses by $3.9 million mainly due to $1.4 million in higher sundry losses and

an unfavorable variance of $1.1 million in net gains/losses recognized on the sale of foreclosed auto units; |

| |

• |

|

higher technology and software expenses by $3.8 million mainly due to higher IT professional fees and

network management expenses due to various ongoing technology projects; and |

| |

• |

|

higher net occupancy expense by $2.2 million mainly due to an increase in buildings’ repairs and

maintenance costs; |

partially offset by:

| |

• |

|

a non-cash goodwill impairment of $23.0 million recorded during the

previous quarter in our U.S. based equipment leasing subsidiary due to lower forecasted cash flows and an increase in the rate used to discount cash flows; and |

| |

• |

|

lower processing and transactional services expense by $8.4 million mainly due to lower credit card

processing expenses by $7.1 million as a result of annual volume growth incentives recognized during the quarter; |

Full-time

equivalent employees were 9,088 as of December 31, 2023, compared to 9,063 as of September 30, 2023.

For a breakdown of operating expenses

by category refer to Table B.

4

Income taxes

For the quarter ended December 31, 2023, the Corporation recorded an income tax benefit of $1.5 million, compared to an income tax expense of

$45.9 million for the previous quarter. The positive variance of $47.4 million is mostly attributed to a lower income before tax of $89.4 million, primarily due to the FDIC Special Assessment; the remaining variance is related to tax

credits, higher exempt income, and other adjustments recorded during this quarter. The effective tax rate (“ETR”) for the 2023 fourth quarter was (1.6)%, compared to 25.1% for the third quarter. Excluding the impact of the FDIC Special

Assessment, the ETR for the fourth quarter was 15.0%, compared to 25.1% for the third quarter.

The Corporation’s ETR for the year 2023 was 19.9%;

excluding the FDIC Special Assessment, the ETR was 21.5%. The ETR of the Corporation is impacted by the composition and source of its taxable income. The Corporation expects its ETR for the year 2024 to be within a range from 19% to 23%.

Credit Quality

During the fourth quarter of 2023,

the Corporation continued to reflect credit quality normalization. Non-performing loans (“NPLs”) and net charge offs (“NCOs”) continued below historical

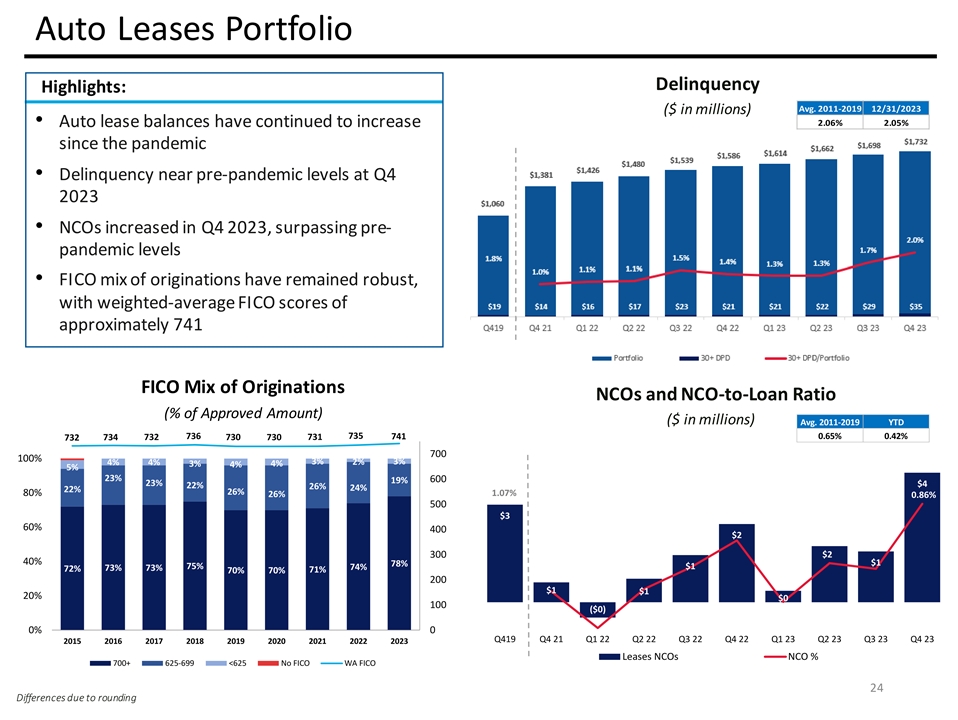

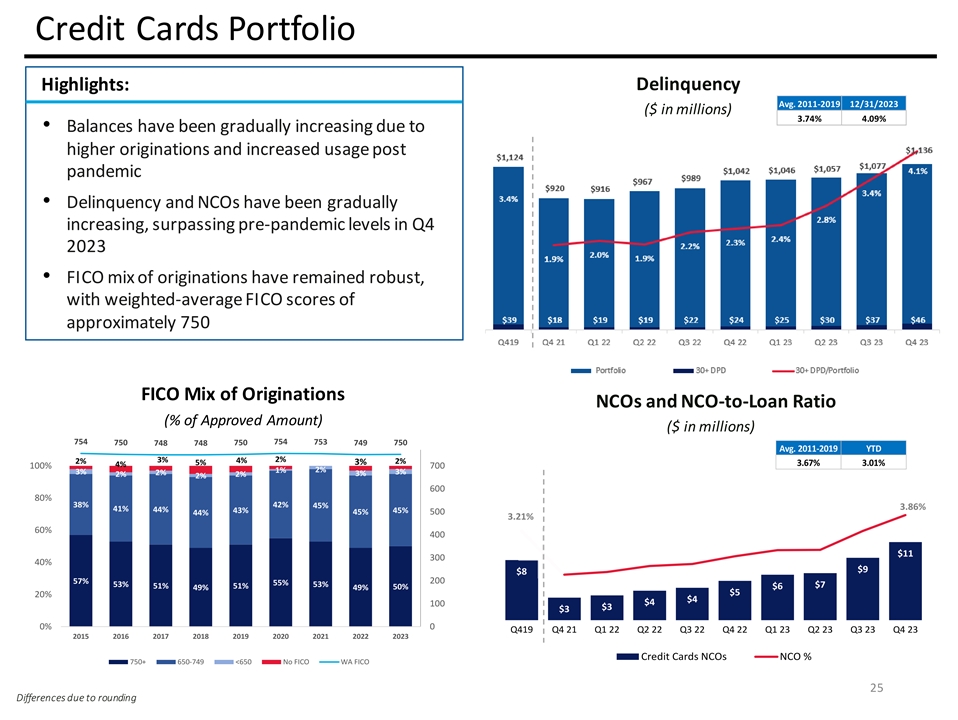

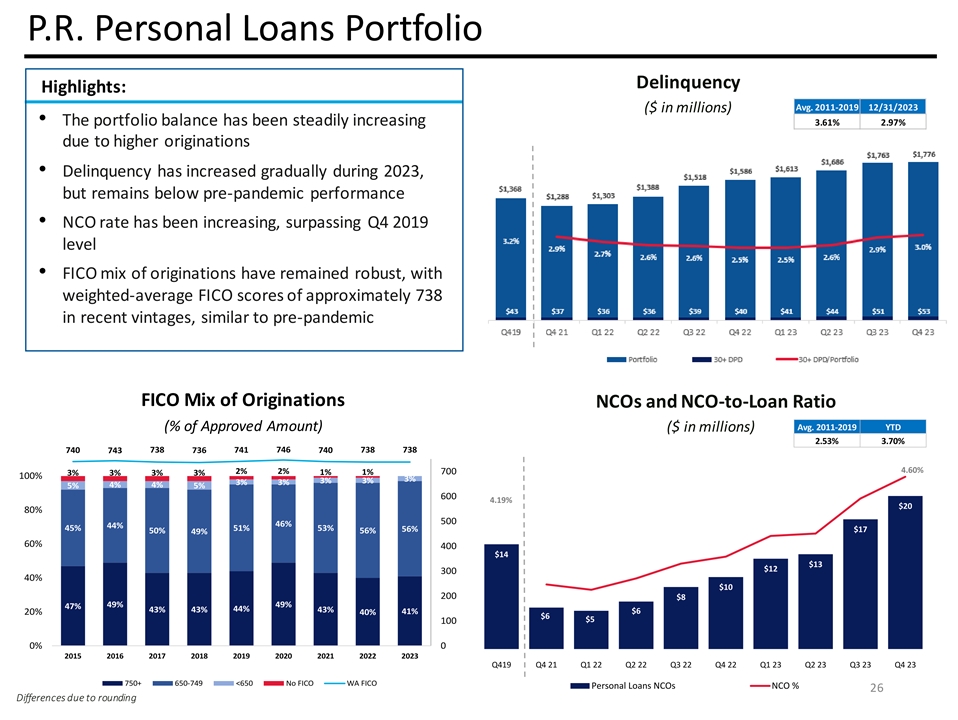

pre-pandemic averages. Consumer portfolios, however, reflected certain credit quality deterioration, particularly the personal loans and credit cards portfolios, with delinquencies and NCOs near or exceeding pre-pandemic levels. The auto loans portfolio also showed credit normalization, however, metrics remained below pre-pandemic levels. The commercial and mortgage

portfolios continue to operate with historically low levels of NCOs and NPLs. We continue to closely monitor changes in the macroeconomic environment and on borrower performance given higher interest rates and inflationary pressures. However,

management believes that the improvements over recent years in risk management practices and the risk profile of the Corporation’s loan portfolios position Popular to continue to operate successfully under the current environment.

The following presents credit quality results for the fourth quarter of 2023:

| |

• |

|

At December 31, 2023, total NPLs

held-in-portfolio decreased by $3.9 million from September 30, 2023. BPPR’s NPLs decreased by $5.1 million, mostly driven by lower mortgage NPLs by

$12.3 million, in part offset by higher consumer NPLs by $4.9 million. The commercial NPLs remained flat quarter-over-quarter, the result of an $17.9 million relationship inflow, offset by a $5.3 million collateral dependent loan

transferred to OREO, $6.4 million in loans returning to accrual status and $5.1 million in charge-offs. PB’s NPLs remained flat quarter-over-quarter. At December 31, 2023, the ratio of NPLs to total loans held-in-portfolio was 1.0%, compared to 1.1% in the third quarter of 2023. |

| |

• |

|

Inflows of NPLs

held-in-portfolio, excluding consumer loans, increased by $17.7 million quarter-over-quarter. In BPPR, total inflows increased by $15.0 million due to higher

commercial inflows by $19.3 million driven by the abovementioned $17.9 million single relationship, in part offset by lower mortgage inflows by $4.3 million. PB inflows increased by $2.7 million, driven by higher commercial

inflows. |

| |

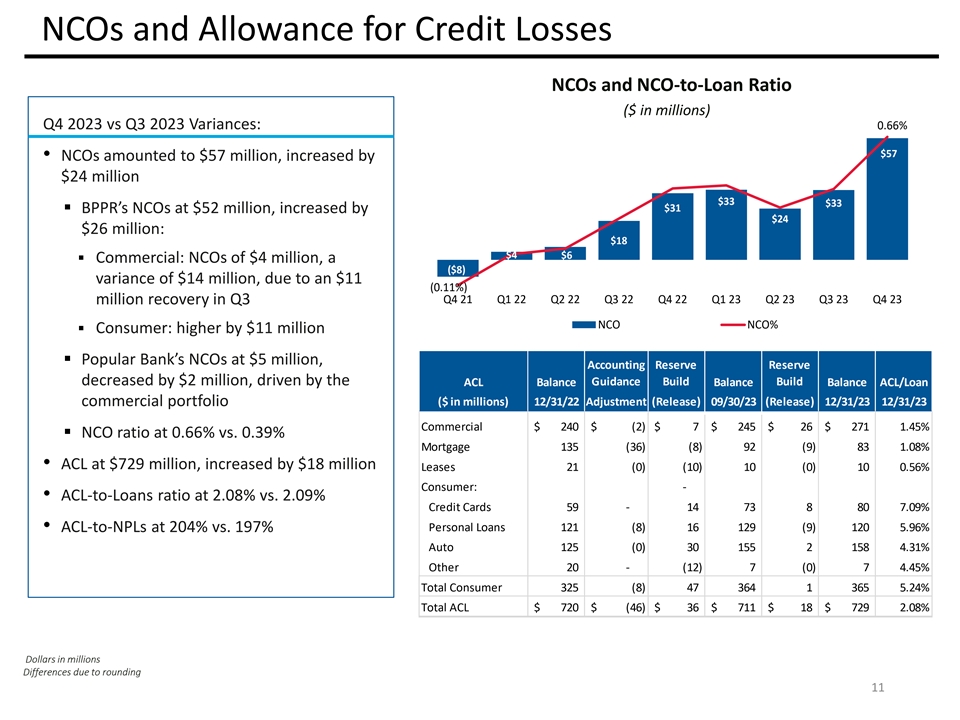

• |

|

NCOs amounted to $56.9 million, increasing by $24.3 million when compared to the third quarter of 2023.

BPPR’s NCOs increased by $26.3 million quarter-over-quarter, mainly driven by higher commercial and consumer NCOs by $14.4 million and $11.2 million, respectively. The commercial NCO increase was mainly the result of a

$10.8 million recovery from a loan pay-off in the previous quarter, coupled with charge-offs on valuations of collateral dependent loans during the fourth quarter of 2023. The consumer NCO increase was

mainly driven by higher auto loans, personal loans and credit cards NCOs by $5.9 million, $3.1 million and $2.2 million, respectively. PB’s NCOs decreased by $2.0 million quarter-over-quarter, mainly driven by lower

commercial NCOs. During the fourth quarter of 2023, the Corporation’s ratio of annualized NCOs to average loans held-in-portfolio was 0.66%, compared to 0.39% in

the third quarter of 2023. Refer to Table N for further information on NCOs and related ratios. |

| |

• |

|

At December 31, 2023, the allowance for credit losses (“ACL”) increased by $18.3 million from

the third quarter of 2023 to $729.3 million. In BPPR the ACL increased by $15.3 million, primarily driven by a $10.0 million specific reserve for the $17.9 million new NPL mentioned above, loan growth and higher reserves for the

consumer portfolios attributable to changing credit quality. In PB the ACL increased by $2.9 million from the previous quarter, mainly driven by higher reserves for the commercial portfolio due to changes in ratings. |

| |

• |

|

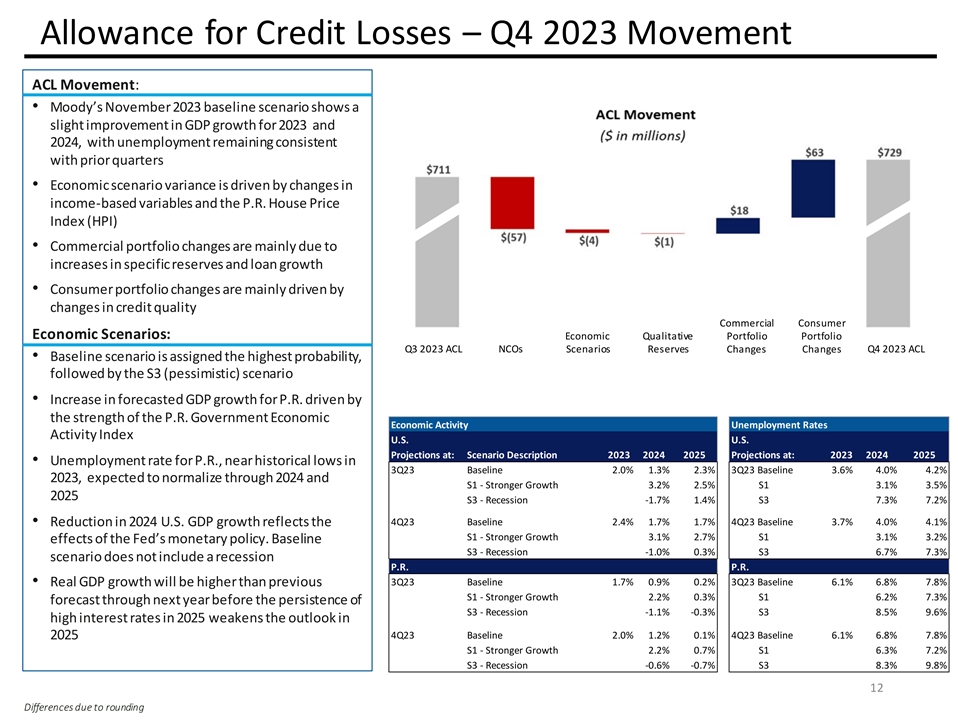

The ACL incorporated updated macroeconomic scenarios for Puerto Rico and the United States. Given that any one

economic outlook is inherently uncertain, the Corporation leverages multiple scenarios to estimate its ACL. The baseline scenario continues to be assigned the highest probability, followed by the pessimistic scenario, and then the optimistic

scenario. |

5

| |

• |

|

The 2023 annualized GDP growth in the baseline scenario improved to 2.0% and 2.4% for Puerto Rico and the United

States, respectively, compared to 1.7% and 2.0% in the previous quarter. The 2023 forecasted average unemployment rate for Puerto Rico remained at 6.1% from previous forecast, while in the United States unemployment levels remained stable at 3.7%,

compared to 3.6% in the previous forecast. |

| |

• |

|

GDP growth is expected to slow down during 2024 for both regions, when compared to 2023, as a result of the

Fed’s monetary policy. The 2024 GDP growth is expected to be 1.21% for Puerto Rico and 1.65% for the United States. The average 2024 unemployment rate is expected to increase to 6.79% in Puerto Rico and 3.95% in the United States.

|

| |

• |

|

The Corporation’s ratio of the ACL to loans

held-in-portfolio was 2.08% in the fourth quarter of 2023, compared to 2.09% in the previous quarter. The ratio of the ACL to NPLs held-in-portfolio stood at 204.0%, compared to 196.7% in the previous quarter. |

| |

• |

|

The provision for credit losses for the loan portfolios for the fourth quarter of 2023 was $75.2 million,

compared to $43.5 million in the previous quarter, reflecting the previously mentioned changes in the allowance for credit losses. The provision for the BPPR segment was $67.2 million, compared to $54.0 million in the previous

quarter, while the provision for PB was $8.0 million, compared to a benefit of $10.5 million in the previous quarter. In the third quarter, the Corporation implemented a new model for the U.S. commercial real estate portfolio. The

implementation of this new model generated a $15.0 million reduction in reserves, which contributed to PB’s net benefit recorded in the third quarter. |

| |

• |

|

The provision for credit losses on our loan and lease portfolios, provision for unfunded loan commitments of

$3.7 million, and release for credit losses on our investment portfolio of $0.2 million for the fourth quarter are aggregated and presented in the provision for credit losses caption in our Consolidated Statement of Operations. For the

fourth quarter, these combined concepts resulted in a provision expense of $78.7 million, compared to $45.1 million in the previous quarter. |

Non-Performing Assets

|

|

|

|

|

|

|

|

|

|

|

|

|

| (Unaudited) |

|

|

|

|

|

|

|

|

|

| (In thousands) |

|

31-Dec-23 |

|

|

30-Sep-23 |

|

|

31-Dec-22 |

|

| Non-performing loans held-in-portfolio |

|

$ |

357,611 |

|

|

$ |

361,523 |

|

|

$ |

439,441 |

|

| Other real estate owned (“OREO”) |

|

|

80,416 |

|

|

|

82,322 |

|

|

|

89,126 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total non-performing assets |

|

$ |

438,027 |

|

|

$ |

443,845 |

|

|

$ |

528,567 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net charge-offs (recoveries) for the quarter |

|

$ |

56,947 |

|

|

$ |

32,655 |

|

|

$ |

31,200 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Ratios: |

|

|

|

|

|

|

|

|

|

|

|

|

| Loans

held-in-portfolio |

|

$ |

35,064,971 |

|

|

$ |

34,029,313 |

|

|

$ |

32,077,769 |

|

| Non-performing loans held-in-portfolio to loans held-in-portfolio |

|

|

1.02 |

% |

|

|

1.06 |

% |

|

|

1.37 |

% |

| Allowance for credit losses to loans held-in-portfolio |

|

|

2.08 |

|

|

|

2.09 |

|

|

|

2.25 |

|

| Allowance for credit losses to non-performing loans,

excluding loans held-for-sale |

|

|

203.95 |

|

|

|

196.69 |

|

|

|

163.91 |

|

Refer to Table L for additional information.

6

Provision for Credit Losses (Benefit) - Loan Portfolios

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| (Unaudited) |

|

Quarters ended |

|

|

Years ended |

|

| (In thousands) |

|

31-Dec-23 |

|

|

30-Sep-23 |

|

|

31-Dec-22 |

|

|

31-Dec-23 |

|

|

31-Dec-22 |

|

| Provision for credit losses (benefit) - loan portfolios: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| BPPR |

|

$ |

67,235 |

|

|

$ |

54,017 |

|

|

$ |

44,383 |

|

|

$ |

194,834 |

|

|

$ |

69,544 |

|

| Popular U.S. |

|

|

7,983 |

|

|

|

(10,503 |

) |

|

|

3,949 |

|

|

|

6,705 |

|

|

|

13,763 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total provision for credit losses (benefit) - loan portfolios |

|

$ |

75,218 |

|

|

$ |

43,514 |

|

|

$ |

48,332 |

|

|

$ |

201,539 |

|

|

$ |

83,307 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Credit Quality by Segment

|

|

|

|

|

|

|

|

|

|

|

|

|

| (Unaudited)

(In thousands) |

|

Quarters ended |

|

| BPPR |

|

31-Dec-23 |

|

|

30-Sep-23 |

|

|

31-Dec-22 |

|

| Provision for credit losses - loan portfolios |

|

$ |

67,235 |

|

|

$ |

54,017 |

|

|

$ |

44,383 |

|

| Net charge-offs |

|

|

51,913 |

|

|

|

25,600 |

|

|

|

19,846 |

|

| Total non-performing loans

held-in-portfolio |

|

|

328,718 |

|

|

|

333,825 |

|

|

|

402,009 |

|

| Annualized net charge-offs (recoveries) to average loans held-in-portfolio |

|

|

0.86 |

% |

|

|

0.44 |

% |

|

|

0.35 |

% |

| Allowance / loans

held-in-portfolio |

|

|

2.61 |

% |

|

|

2.63 |

% |

|

|

2.73 |

% |

| Allowance / non-performing loans held-in-portfolio |

|

|

194.65 |

% |

|

|

187.08 |

% |

|

|

153.12 |

% |

|

|

| |

|

Quarters ended |

|

| Popular U.S. |

|

31-Dec-23 |

|

|

30-Sep-23 |

|

|

31-Dec-22 |

|

| Provision for credit losses - loan portfolios |

|

$ |

7,983 |

|

|

$ |

(10,503 |

) |

|

$ |

3,949 |

|

| Net charge-offs |

|

|

5,034 |

|

|

|

7,055 |

|

|

|

11,354 |

|

| Total non-performing loans

held-in-portfolio |

|

|

28,893 |

|

|

|

27,698 |

|

|

|

37,432 |

|

| Annualized net charge-offs (recoveries) to average loans held-in-portfolio |

|

|

0.19 |

% |

|

|

0.28 |

% |

|

|

0.49 |

|

| Allowance / loans

held-in-portfolio |

|

|

0.85 |

% |

|

|

0.84 |

% |

|

|

1.10 |

% |

| Allowance / non-performing loans held-in-portfolio |

|

|

309.70 |

% |

|

|

312.42 |

% |

|

|

279.86 |

% |

Financial Condition Highlights

|

|

|

|

|

|

|

|

|

|

|

|

|

| (Unaudited) |

|

|

|

|

|

|

|

|

|

| (In thousands) |

|

31-Dec-23 |

|

|

30-Sep-23 |

|

|

31-Dec-22 |

|

| Cash and money market investments |

|

$ |

7,419,333 |

|

|

$ |

6,924,772 |

|

|

$ |

6,084,096 |

|

| Investment securities |

|

|

25,148,673 |

|

|

|

25,653,616 |

|

|

|

26,553,317 |

|

| Loans |

|

|

35,064,971 |

|

|

|

34,029,313 |

|

|

|

32,077,769 |

|

| Total assets |

|

|

70,758,155 |

|

|

|

69,736,936 |

|

|

|

67,637,917 |

|

| Deposits |

|

|

63,618,243 |

|

|

|

63,337,600 |

|

|

|

61,227,227 |

|

| Borrowings |

|

|

1,078,332 |

|

|

|

1,097,720 |

|

|

|

1,400,319 |

|

| Total liabilities |

|

|

65,611,202 |

|

|

|

65,279,328 |

|

|

|

63,544,492 |

|

| Stockholders’ equity |

|

|

5,146,953 |

|

|

|

4,457,608 |

|

|

|

4,093,425 |

|

7

Total assets amounted to $70.8 billion at December 31, 2023, an increase of $1.0 billion from

the third quarter of 2023, driven by:

| |

• |

|

an increase in loans

held-in-portfolio of $1.0 billion driven by an increase of $748.4 million at BPPR, mainly in the commercial portfolio as well as in mortgage and consumer

loans, and an increase of $287.3 million at PB mainly from commercial and construction loans; and |

| |

• |

|

a net increase in cash and money market investments of $494.6 million due to higher deposits and repayments

from the investment portfolio; |

partially offset by:

| |

• |

|

a decrease in securities

available-for-sale (“AFS”) of $400.8 million, mainly due to repayments and maturities, offset in part by favorable changes in the fair value of debt

securities; and |

| |

• |

|

a decrease in securities

held-to-maturity (“HTM”) of $107.5 million driven by maturities of U.S. Treasury securities, partially offset by the amortization of $44.2 million of

the discount related to U.S. Treasury securities previously reclassified from the AFS to HTM, which has an offsetting unrealized loss included within other comprehensive income that is also being accreted, resulting in a neutral effect to earnings.

|

Total liabilities increased by $331.9 million from the third quarter of 2023, driven by:

| |

• |

|

an increase of $280.6 million in deposits, mainly in time deposits and savings accounts at PB and demand

deposits and P.R. public sector accounts at BPPR, partially offset by a decrease in savings accounts at BPPR; and |

| |

• |

|

an increase of $70.6 million in other liabilities mainly due to the $71.4 million FDIC Special

Assessment recognized during the fourth quarter. |

Stockholders’ equity increased by $689.3 million from the third quarter of

2023, mainly due to the after-tax impact of the decrease in net unrealized losses in the portfolio of AFS securities of $593.2 million, the net income for the quarter of $94.6 million and the

amortization of unrealized losses from securities previously reclassified to HTM of $35.3 million, net of taxes, partially offset by common and preferred dividends declared during the quarter.

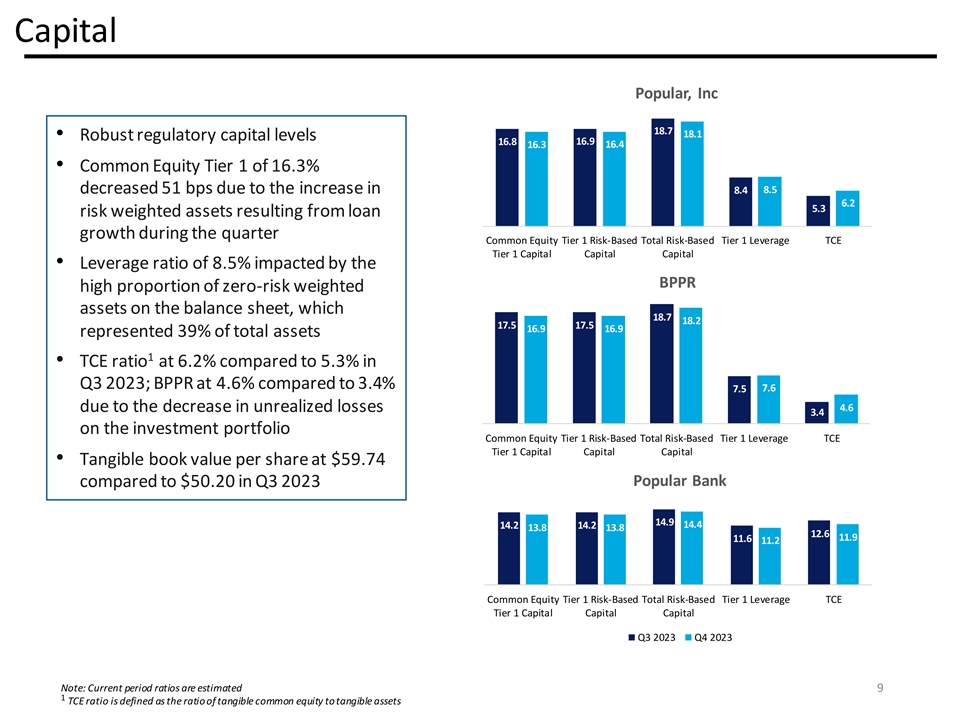

Common Equity Tier 1 ratio (“CET1”), common equity per share and tangible book value per share were 16.30%, $71.03 and $59.74, respectively, at

December 31, 2023, compared to 16.81%, $61.49 and $50.20, respectively, at September 30, 2023. Refer to Table A for capital ratios.

Refer to

Table C for the Statements of Financial Condition.

8

Cautionary Note Regarding Forward-Looking Statements

This press release contains “forward-looking statements” within the meaning of the U.S. Private Securities Litigation Reform Act of 1995, including

without limitation those regarding Popular’s business, financial condition, results of operations, plans, objectives and future performance. These statements are not guarantees of future performance, are based on management’s current

expectations and, by their nature, involve risks, uncertainties, estimates and assumptions. Potential factors, some of which are beyond the Corporation’s control, could cause actual results to differ materially from those expressed in, or

implied by, such forward-looking statements. Risks and uncertainties include, without limitation, the effect of competitive and economic factors, and our reaction to those factors, the adequacy of the allowance for loan losses, delinquency trends,

market risk and the impact of interest rate changes (including on our cost of deposits), our ability to attract deposits and grow our loan portfolio, capital market conditions, capital adequacy and liquidity, the effect of legal and regulatory

proceedings, new regulatory requirements or accounting standards on the Corporation’s financial condition and results of operations, the occurrence of unforeseen or catastrophic events, including extreme weather events, pandemics, man-made

disasters or acts of violence or war, as well as actions taken by governmental authorities in response thereto, and the direct and indirect impact of such events on Popular, our customers, service providers and third parties. Other potential factors

include Popular’s ability to successfully execute its transformation initiative, including, but not limited to, achieving projected earnings, efficiencies and return on tangible common equity and accurately anticipating costs and expenses

associated therewith, imposition of additional or special FDIC assessments, changes to regulatory capital, liquidity and resolution-related requirements applicable to financial institutions in response to recent developments affecting the banking

sector and the impact of bank failures or adverse developments at other banks and related negative media coverage of the banking industry in general on investor and depositor sentiment regarding the stability and liquidity of banks. All statements

contained herein that are not clearly historical in nature, are forward-looking, and the words “anticipate,” “believe,” “continues,” “expect,” “estimate,” “intend,” “project” and

similar expressions, and future or conditional verbs such as “will,” “would,” “should,” “could,” “might,” “can,” “may” or similar expressions, are generally intended to identify

forward-looking statements.

More information on the risks and important factors that could affect the Corporation’s future results and financial

condition is included in our Form 10-K for the year ended December 31, 2022, in our Form 10-Q for the quarters ended March 31, 2023, June 30, 2023, and

September 30, 2023 and in our Form 10-K for the year ended December 31, 2023 to be filed with the Securities and Exchange Commission. Our filings are available on the Corporation’s website

(www.popular.com) and on the Securities and Exchange Commission website (www.sec.gov). The Corporation assumes no obligation to update or revise any forward-looking statements or information which speak as of their respective dates.

About Popular, Inc.

Popular, Inc. (NASDAQ:

BPOP) is the leading financial institution in Puerto Rico, by both assets and deposits, and ranks among the top 50 U.S. bank holding companies by assets. Founded in 1893, Banco Popular de Puerto Rico, Popular’s principal subsidiary, provides

retail, mortgage and commercial banking services in Puerto Rico and the U.S. Virgin Islands. Popular also offers in Puerto Rico auto and equipment leasing and financing, investment banking, broker-dealer and insurance services through

specialized subsidiaries. In the mainland United States, Popular provides retail, mortgage and commercial banking services through its New York-chartered banking subsidiary, Popular Bank, which has branches located in New York, New Jersey and

Florida.

Conference Call

Popular will hold a

conference call to discuss its financial results today, Thursday, January 25, 2024 at 10:00 a.m. Eastern Time. The call will be broadcast live over the Internet and can be accessed through the Investor Relations section of the

Corporation’s website: www.popular.com.

Listeners are recommended to go to the website at least 15 minutes prior to the call to download and install

any necessary audio software. The call may also be accessed through a dial-in telephone number

1-833-470-1428 (Toll Free) or

1-404-975-4839 (Local). The dial-in access code is 803461.

A replay of the webcast will be archived in Popular’s website. A telephone replay will be available one hour after the end of the conference call through

Friday, February 23, 2024. The replay dial in is: 1-866-813-9403 or 1-929-458-6194. The replay passcode is 212082.

An electronic version of

this press release can be found at the Corporation’s website: www.popular.com.

9

Popular, Inc.

Financial Supplement to Fourth Quarter 2023 Earnings Release

Table A - Selected Ratios and Other Information

Table B -

Consolidated Statement of Operations

Table C - Consolidated Statement of Financial Condition

Table D - Analysis of Levels and Yields on a Taxable Equivalent Basis (Non-GAAP) - QUARTER

Table E - Analysis of Levels and Yields on a Taxable Equivalent Basis (Non-GAAP) - QUARTER

Table F - Analysis of Levels and Yields on a Taxable Equivalent Basis (Non-GAAP) - YEAR-TO-DATE

Table G - Mortgage Banking Activities and Other Service Fees

Table H - Loans and Deposits

Table I - Loan Delinquency - BPPR

Operations

Table J - Loan Delinquency - Popular U.S. Operations

Table K - Loan Delinquency - Consolidated

Table L - Non-Performing Assets

Table M - Activity in Non-Performing Loans

Table N - Allowance for Credit Losses, Net Charge-offs and Related Ratios

Table O - Allowance for Credit Losses ‘‘ACL’’ - Loan Portfolios - Consolidated

Table P - Allowance for Credit Losses ‘‘ACL’’ - Loan Portfolios - BPPR Operations

Table Q - Allowance for Credit Losses ‘‘ACL’’ - Loan Portfolios - Popular U.S. Operations

Table R - Reconciliation to GAAP Financial Measures

10

POPULAR, INC.

Financial Supplement to Fourth Quarter 2023 Earnings Release

Table A - Selected Ratios and Other Information

(Unaudited)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Quarters ended |

|

|

Years ended |

|

| |

|

31-Dec-23 |

|

|

30-Sep-23 |

|

|

31-Dec-22 |

|

|

31-Dec-23 |

|

|

31-Dec-22 |

|

| Basic EPS |

|

$ |

1.31 |

|

|

$ |

1.90 |

|

|

$ |

3.56 |

|

|

$ |

7.53 |

|

|

$ |

14.65 |

|

| Diluted EPS |

|

$ |

1.31 |

|

|

$ |

1.90 |

|

|

$ |

3.56 |

|

|

$ |

7.52 |

|

|

$ |

14.63 |

|

| Average common shares outstanding |

|

|

71,810,073 |

|

|

|

71,794,934 |

|

|

|

72,101,177 |

|

|

|

71,710,265 |

|

|

|

75,147,263 |

|

| Average common shares outstanding - assuming dilution |

|

|

71,881,020 |

|

|

|

71,818,102 |

|

|

|

72,192,680 |

|

|

|

71,791,692 |

|

|

|

75,274,003 |

|

| Common shares outstanding at end of period |

|

|

72,153,621 |

|

|

|

72,127,595 |

|

|

|

71,853,720 |

|

|

|

72,153,621 |

|

|

|

71,853,720 |

|

| Market value per common share |

|

$ |

82.07 |

|

|

$ |

63.01 |

|

|

$ |

66.32 |

|

|

$ |

82.07 |

|

|

$ |

66.32 |

|

| Market capitalization - (In millions) |

|

$ |

5,922 |

|

|

$ |

4,545 |

|

|

$ |

4,765 |

|

|

$ |

5,922 |

|

|

$ |

4,765 |

|

| Return on average assets |

|

|

0.52 |

% |

|

|

0.75 |

% |

|

|

1.44 |

% |

|

|

0.76 |

% |

|

|

1.51 |

% |

| Return on average common equity |

|

|

5.55 |

% |

|

|

8.17 |

% |

|

|

16.59 |

% |

|

|

8.21 |

% |

|

|

18.39 |

% |

| Net interest margin (non-taxable equivalent

basis) |

|

|

3.08 |

% |

|

|

3.07 |

% |

|

|

3.28 |

% |

|

|

3.13 |

% |

|

|

3.11 |

% |

| Net interest margin (taxable equivalent basis) -non-GAAP |

|

|

3.26 |

% |

|

|

3.24 |

% |

|

|

3.64 |

% |

|

|

3.31 |

% |

|

|

3.46 |

% |

| Common equity per share |

|

$ |

71.03 |

|

|

$ |

61.49 |

|

|

$ |

56.66 |

|

|

$ |

71.03 |

|

|

$ |

56.66 |

|

| Tangible common book value per common share (non-GAAP)

[1] |

|

$ |

59.74 |

|

|

$ |

50.20 |

|

|

$ |

44.97 |

|

|

$ |

59.74 |

|

|

$ |

44.97 |

|

| Tangible common equity to tangible assets (non-GAAP)

[1] |

|

|

6.16 |

% |

|

|

5.25 |

% |

|

|

4.84 |

% |

|

|

6.16 |

% |

|

|

4.84 |

% |

| Return on average tangible common equity [1] |

|

|

6.32 |

% |

|

|

9.36 |

% |

|

|

19.23 |

% |

|

|

9.40 |

% |

|

|

21.13 |

% |

| Tier 1 capital |

|

|

16.36 |

% |

|

|

16.88 |

% |

|

|

16.45 |

% |

|

|

16.36 |

% |

|

|

16.45 |

% |

| Total capital |

|

|

18.13 |

% |

|

|

18.67 |

% |

|

|

18.26 |

% |

|

|

18.13 |

% |

|

|

18.26 |

% |

| Tier 1 leverage |

|

|

8.51 |

% |

|

|

8.41 |

% |

|

|

8.06 |

% |

|

|

8.51 |

% |

|

|

8.06 |

% |

| Common Equity Tier 1 capital |

|

|

16.30 |

% |

|

|

16.81 |

% |

|

|

16.39 |

% |

|

|

16.30 |

% |

|

|

16.39 |

% |

| [1] |

Refer to Table R for reconciliation to GAAP financial measures. |

11

POPULAR, INC.

Financial Supplement to Fourth Quarter 2023 Earnings Release

Table B - Consolidated Statement of Operations

(Unaudited)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Quarters ended |

|

|

Variance |

|

|

Quarter ended |

|

|

Variance |

|

|

Years ended |

|

| |

|

|

|

|

|

|

|

Q4 2023 |

|

|

|

|

|

Q4 2023 |

|

|

|

|

|

|

|

| (In thousands, except per share information) |

|

31-Dec-23 |

|

|

30-Sep-23 |

|

|

vs. Q3 2023 |

|

|

31-Dec-22 |

|

|

vs. Q4 2022 |

|

|

31-Dec-23 |

|

|

31-Dec-22 |

|

| Interest income: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Loans |

|

$ |

623,438 |

|

|

$ |

596,886 |

|

|

$ |

26,552 |

|

|

$ |

522,042 |

|

|

$ |

101,396 |

|

|

$ |

2,331,654 |

|

|

$ |

1,876,166 |

|

| Money market investments |

|

|

100,840 |

|

|

|

99,286 |

|

|

|

1,554 |

|

|

|

50,908 |

|

|

|

49,932 |

|

|

|

366,625 |

|

|

|

118,080 |

|

| Investment securities |

|

|

143,214 |

|

|

|

148,614 |

|

|

|

(5,400 |

) |

|

|

140,244 |

|

|

|

2,970 |

|

|

|

547,028 |

|

|

|

471,665 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total interest income |

|

|

867,492 |

|

|

|

844,786 |

|

|

|

22,706 |

|

|

|

713,194 |

|

|

|

154,298 |

|

|

|

3,245,307 |

|

|

|

2,465,911 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Interest expense: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Deposits |

|

|

319,200 |

|

|

|

294,121 |

|

|

|

25,079 |

|

|

|

139,338 |

|

|

|

179,862 |

|

|

|

1,050,024 |

|

|

|

252,845 |

|

| Short-term borrowings |

|

|

1,342 |

|

|

|

1,478 |

|

|

|

(136 |

) |

|

|

4,488 |

|

|

|

(3,146 |

) |

|

|

7,329 |

|

|

|

5,737 |

|

| Long-term debt |

|

|

12,770 |

|

|

|

15,167 |

|

|

|

(2,397 |

) |

|

|

9,802 |

|

|

|

2,968 |

|

|

|

56,430 |

|

|

|

39,970 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total interest expense |

|

|

333,312 |

|

|

|

310,766 |

|

|

|

22,546 |

|

|

|

153,628 |

|

|

|

179,684 |

|

|

|

1,113,783 |

|

|

|

298,552 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net interest income |

|

|

534,180 |

|

|

|

534,020 |

|

|

|

160 |

|

|

|

559,566 |

|

|

|

(25,386 |

) |

|

|

2,131,524 |

|

|

|

2,167,359 |

|

| Provision for credit losses |

|

|

78,663 |

|

|

|

45,117 |

|

|

|

33,546 |

|

|

|

49,531 |

|

|

|

29,132 |

|

|

|

208,609 |

|

|

|

83,030 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net interest income after provision for credit losses |

|

|

455,517 |

|

|

|

488,903 |

|

|

|

(33,386 |

) |

|

|

510,035 |

|

|

|

(54,518 |

) |

|

|

1,922,915 |

|

|

|

2,084,329 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Service charges on deposit accounts |

|

|

37,699 |

|

|

|

37,318 |

|

|

|

381 |

|

|

|

34,682 |

|

|

|

3,017 |

|

|

|

147,476 |

|

|

|

157,210 |

|

| Other service fees |

|

|

96,692 |

|

|

|

93,407 |

|

|

|

3,285 |

|

|

|

89,022 |

|

|

|

7,670 |

|

|

|

374,440 |

|

|

|

334,009 |

|

| Mortgage banking activities |

|

|

6,388 |

|

|

|

5,393 |

|

|

|

995 |

|

|

|

6,562 |

|

|

|

(174 |

) |

|

|

21,497 |

|

|

|

42,450 |

|

| Net gain (loss), including impairment, on equity securities |

|

|

2,317 |

|

|

|

(1,319 |

) |

|

|

3,636 |

|

|

|

317 |

|

|

|

2,000 |

|

|

|

3,482 |

|

|

|

(7,334 |

) |

| Net gain (loss) on trading account debt securities |

|

|

750 |

|

|

|

219 |

|

|

|

531 |

|

|

|

162 |

|

|

|

588 |

|

|

|

1,382 |

|

|

|

(784 |

) |

| Net loss on sale of loans, including valuation adjustments on loans

held-for-sale |

|

|

(71 |

) |

|

|

(44 |

) |

|

|

(27 |

) |

|

|

— |

|

|

|

(71 |

) |

|

|

(115 |

) |

|

|

— |

|

| Adjustments to indemnity reserves on loans sold |

|

|

2,350 |

|

|

|

(187 |

) |

|

|

2,537 |

|

|

|

(221 |

) |

|

|

2,571 |

|

|

|

2,319 |

|

|

|

919 |

|

| Other operating income |

|

|

22,618 |

|

|

|

24,762 |

|

|

|

(2,144 |

) |

|

|

27,941 |

|

|

|

(5,323 |

) |

|

|

100,243 |

|

|

|

370,592 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total non-interest income |

|

|

168,743 |

|

|

|

159,549 |

|

|

|

9,194 |

|

|

|

158,465 |

|

|

|

10,278 |

|

|

|

650,724 |

|

|

|

897,062 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Operating expenses: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Personnel costs |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Salaries |

|

|

127,809 |

|

|

|

127,832 |

|

|

|

(23 |

) |

|

|

116,503 |

|

|

|

11,306 |

|

|

|

505,935 |

|

|

|

432,910 |

|

| Commissions, incentives and other bonuses |

|

|

26,632 |

|

|

|

27,670 |

|

|

|

(1,038 |

) |

|

|

39,570 |

|

|

|

(12,938 |

) |

|

|

112,657 |

|

|

|

155,889 |

|

| Pension, postretirement and medical insurance |

|

|

17,598 |

|

|

|

16,985 |

|

|

|

613 |

|

|

|

12,452 |

|

|

|

5,146 |

|

|

|

67,469 |

|

|

|

56,085 |

|

| Other personnel costs, including payroll taxes |

|

|

22,626 |

|

|

|

20,665 |

|

|

|

1,961 |

|

|

|

21,612 |

|

|

|

1,014 |

|

|

|

91,984 |

|

|

|

74,880 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total personnel costs |

|

|

194,665 |

|

|

|

193,152 |

|

|

|

1,513 |

|

|

|

190,137 |

|

|

|

4,528 |

|

|

|

778,045 |

|

|

|

719,764 |

|

| Net occupancy expenses |

|

|

30,282 |

|

|

|

28,100 |

|

|

|

2,182 |

|

|

|

27,812 |

|

|

|

2,470 |

|

|

|

111,586 |

|

|

|

106,169 |

|

| Equipment expenses |

|

|

10,179 |

|

|

|

8,905 |

|

|

|

1,274 |

|

|

|

9,828 |

|

|

|

351 |

|

|

|

37,057 |

|

|

|

35,626 |

|

| Other taxes |

|

|

14,636 |

|

|

|

8,590 |

|

|

|

6,046 |

|

|

|

16,142 |

|

|

|

(1,506 |

) |

|

|

55,926 |

|

|

|

63,603 |

|

| Professional fees |

|

|

39,065 |

|

|

|

38,514 |

|

|

|

551 |

|

|

|

49,159 |

|

|

|

(10,094 |

) |

|

|

161,142 |

|

|

|

172,043 |

|

| Technology and software expenses |

|

|

76,772 |

|

|

|

72,930 |

|

|

|

3,842 |

|

|

|

78,264 |

|

|

|

(1,492 |

) |

|

|

290,615 |

|

|

|

291,902 |

|

| Processing and transactional services |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Credit and debit cards |

|

|

6,682 |

|

|

|

13,762 |

|

|

|

(7,080 |

) |

|

|

10,278 |

|

|

|

(3,596 |

) |

|

|

44,578 |

|

|

|

45,455 |

|

| Other processing and transactional services |

|

|

22,779 |

|

|

|

24,137 |

|

|

|

(1,358 |

) |

|

|

22,509 |

|

|

|

270 |

|

|

|

93,492 |

|

|

|

81,690 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total processing and transactional services |

|

|

29,461 |

|

|

|

37,899 |

|

|

|

(8,438 |

) |

|

|

32,787 |

|

|

|

(3,326 |

) |

|

|

138,070 |

|

|

|

127,145 |

|

| Communications |

|

|

4,181 |

|

|

|

4,220 |

|

|

|

(39 |

) |

|

|

3,857 |

|

|

|

324 |

|

|

|

16,664 |

|

|

|

14,885 |

|

| Business promotion |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Rewards and customer loyalty programs |

|

|

14,130 |

|

|

|

15,988 |

|

|

|

(1,858 |

) |

|

|

13,538 |

|

|

|

592 |

|

|

|

59,092 |

|

|

|

51,832 |

|

| Other business promotion |

|

|

13,767 |

|

|

|

7,087 |

|

|

|

6,680 |

|

|

|

14,596 |

|

|

|

(829 |

) |

|

|

35,834 |

|

|

|

37,086 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total business promotion |

|

|

27,897 |

|

|

|

23,075 |

|

|

|

4,822 |

|

|

|

28,134 |

|

|

|

(237 |

) |

|

|

94,926 |

|

|

|

88,918 |

|

| FDIC deposit insurance |

|

|

81,385 |

|

|

|

8,932 |

|

|

|

72,453 |

|

|

|

6,342 |

|

|

|

75,043 |

|

|

|

105,985 |

|

|

|

26,787 |

|

| Other real estate owned (OREO) income |

|

|

(5,178 |

) |

|

|

(5,189 |

) |

|

|

11 |

|

|

|

(9,180 |

) |

|

|

4,002 |

|

|

|

(15,375 |

) |

|

|

(22,143 |

) |

| Other operating expenses |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Operational losses |

|

|

6,921 |

|

|

|

5,504 |

|

|

|

1,417 |

|

|

|

9,018 |

|

|

|

(2,097 |

) |

|

|

23,505 |

|

|

|

32,049 |

|

| All other |

|

|

20,084 |

|

|

|

17,557 |

|

|

|

2,527 |

|

|

|

18,614 |

|

|

|

1,470 |

|

|

|

73,774 |

|

|

|

77,397 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total other operating expenses |

|

|

27,005 |

|

|

|

23,061 |

|

|

|

3,944 |

|

|

|

27,632 |

|

|

|

(627 |

) |

|

|

97,279 |

|

|

|

109,446 |

|

| Amortization of intangibles |

|

|

795 |

|

|

|

795 |

|

|

|

— |

|

|

|

794 |

|

|

|

1 |

|

|

|

3,180 |

|

|

|

3,275 |

|

| Goodwill impairment charge |

|

|

— |

|

|

|

23,000 |

|

|

|

(23,000 |

) |

|

|

— |

|

|

|

— |

|

|

|

23,000 |

|

|

|

9,000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total operating expenses |

|

|

531,145 |

|

|

|

465,984 |

|

|

|

65,161 |

|

|

|

461,708 |

|

|

|

69,437 |

|

|

|

1,898,100 |

|

|

|

1,746,420 |

|

| Income before income tax |

|

|

93,115 |

|

|

|

182,468 |

|

|

|

(89,353 |

) |

|

|

206,792 |

|

|

|

(113,677 |

) |

|

|

675,539 |

|

|

|

1,234,971 |

|

| Income tax (benefit) expense |

|

|

(1,479 |

) |

|

|

45,859 |

|

|

|

(47,338 |

) |

|

|

(50,347 |