Filed Pursuant to Rule 424(b)(5)

Registration

No. 333-261229

Prospectus Supplement

(To Prospectus dated June 10, 2022)

Up to $1,440,000 of Shares of Common Stock

of

Shineco, Inc.

Shineco,

Inc. (the “Company” or “we”) is offering up to $1,440,000 in shares (“Shares”) of our common stock

to certain investors under a purchase agreement entered into on December 22, 2023 (the “Purchase Agreement”) at a per share

purchase price of $0.12. Delivery of the common stock offered hereby and receipt of the gross proceeds from the sale of the Shares

is expected to occur on or about December 22, 2023 subject to the satisfaction of certain closing conditions. See “Purchase Agreement”

beginning on page S-17 of this prospectus supplement for more information regarding these arrangements.

Our

common stock is listed on the Nasdaq Capital Market under the symbol “SISI.” On December 21, 2023, the closing price of

our common stock was $0.0941 per share.

The

securities offered by this prospectus involve a high degree of risks. Shineco is a holding company incorporated in Delaware. As a holding company with no material operations of our own, we conduct

our operations through our subsidiaries and in the two years ended June 30, 2022 and 2023, through the variable interest entities (the

“VIEs”) and subsidiaries.

Because of Shineco’s corporate

structure, the Company is subject to the risks due to uncertainty of the interpretation and the application of the PRC laws and regulations.

As of the date of this prospectus, there is no laws, regulations or other rules that require the China based operating entities

to obtain permission or approvals from any Chinese authorities to list or continue listing Shineco or its affiliate’s securities

on U.S. stock exchanges, and nor does Shineco have received or was denied such permission. However, there is no guarantee that Shineco

will receive or not be denied permission from Chinese authorities to continue listing on U.S. exchanges in the future.

Shineco

is also subject to the legal and operational risks associated with being based in and having the majority of its operations in China.

These risks could result in material changes in operations, or a complete hindrance of Shineco’s ability to offer or continue to

offer its securities to investors, and could cause the value of Shineco’s securities to significantly decline or become worthless.

Recently, the PRC government initiated a series of regulatory actions and statements to regulate business operations in China with little

advance notice, including cracking down on illegal activities in the securities market, enhancing supervision over China-based companies

listed overseas using variable interest entity structure, adopting new measures to extend the scope of cybersecurity reviews, and expanding

the efforts in anti-monopoly enforcement. On July 6, 2021, the General Office of the Communist Party of China Central Committee and the

General Office of the State Council jointly issued an announcement to crack down on illegal activities in the securities market and promote

the high-quality development of the capital market, which, among other things, requires the relevant governmental authorities to strengthen

cross-border oversight of law-enforcement and judicial cooperation, to enhance supervision over China-based companies listed overseas,

and to establish and improve the system of extraterritorial application of the PRC securities laws. On July 10, 2021, the PRC State Internet

Information Office issued the Measures of Cybersecurity Review, which requires cyberspace companies with personal information of more

than one (1) million users that want to list their securities on a non-Chinese stock exchange to file a cybersecurity review with the

Office of Cybersecurity Review of China. On December 28, 2021, a total of thirteen governmental departments of the PRC, including the

Cyberspace Administration of China (the “CAC”), issued the Measures of Cybersecurity Review, which became effective on February

15, 2022. The Cybersecurity Review Measures provide that an online platform operator, which possesses personal information of at least

one million users, must apply for a cybersecurity review by the CAC if it intends to be listed in foreign countries. Because our current

operations do not possess personal information from more than one million users at this moment, Shineco does not believe that it is subject

to the cybersecurity review by the CAC.

As

of the date of this prospectus, neither the Measures of Cybersecurity Review nor the anti-monopoly regulatory actions has impacted Shineco’s

ability to conduct its business, accept foreign investments, or continue its listing on Nasdaq or on another non-Chinese stock exchange;

however, there are uncertainties in the interpretation and enforcement of these new laws and guidelines, which could materially and adversely

impact the Company’s overall business and financial outlook. In summary, the recent statements and regulatory actions by China’s

government related to the use of variable interest entities and data security or antimonopoly concerns have not affected our ability

to conduct our business, accept foreign investments, or list on a U.S. or other foreign exchange. However, since these statements and

regulatory actions by the PRC government are newly published and official guidance and related implementation rules have not been issued,

it is highly uncertain what the potential impact such modified or new laws and regulations will have on Shineco’s daily business

operation, the ability to accept foreign investments and list on a U.S. or non-Chinese exchange. The Standing Committee of the National

People’s Congress (the “SCNPC”) or other PRC regulatory authorities may in the future promulgate laws, regulations

or implementing rules that would require Shineco or any of its subsidiaries to obtain regulatory approval from Chinese authorities before

listing in the U.S. See “Risk Factors - Risks Associated With Doing Business in China” on page S-21.

On

May 20, 2020, the U.S. Senate passed the Holding Foreign Companies Accountable Act (“HFCAA”) requiring a foreign company

to certify it is not owned or controlled by a foreign government if the PCAOB is unable to audit specified reports because the company

uses a foreign auditor not subject to PCAOB inspection. On December 18, 2020, the Holding Foreign Companies Accountable Act or HFCAA

was signed into law. On September 22, 2021, the PCAOB adopted a final rule implementing the HFCAA, which prohibits foreign companies

from listing their securities on U.S. exchanges if the company has been unavailable for PCAOB inspection or investigation for three consecutive

years.

Our

common stock may be prohibited from trading on a national exchange or “over-the-counter” markets under the HFCAA if the Public

Company Accounting Oversight Board (“PCAOB”) determines that it is unable to inspect or fully investigate our auditor and

as a result the exchange where our securities are traded may delist our securities. Furthermore, on June 22, 2021, the U.S. Senate passed

the Accelerating Holding Foreign Companies Accountable Act (the “AHFCAA”), which was signed into law on December 29, 2022,

amending the HFCAA and requiring the SEC to prohibit an issuer’s securities from trading on any U.S. stock exchange if its auditor

is not subject to PCAOB inspections for two consecutive years instead of three consecutive years. Pursuant to the HFCAA, the PCAOB issued

a Determination Report on December 16, 2021, which found that the PCAOB was unable to inspect or investigate completely certain named

registered public accounting firms headquartered in mainland China and Hong Kong. On December 15, 2022, the PCAOB issued a report that

vacated its December 16, 2021 determination and removed mainland China and Hong Kong from the list of jurisdictions where it is unable

to inspect or investigate completely registered public accounting firms.

Our independent registered public accounting firm is headquartered in Singapore and has

been inspected by the PCAOB on a regular basis and as such, it is not affected by or subject to the PCAOB’s Determination Report.

Notwithstanding the foregoing, in the future, if there is any regulatory change or step taken by PRC regulators that does not permit our

auditor to provide audit documentations located in China or Hong Kong to the PCAOB for inspection or investigation, you may be deprived

of the benefits of such inspection which could result in limitation on or restriction to our access to the U.S. capital markets and trading

of our securities, including trading on the national exchange and trading on “over-the-counter” markets.

Instead

of a Chinese operating company, Shineco is a holding company incorporated in the State of Delaware. You will be purchasing the shares

of common stock of Shineco, the domestic holding company with offshore subsidiaries and affiliates pursuant to this registration statement.

You are not directly investing in any of our affiliated entities.

Shineco’s

operating subsidiaries receive substantially all of the Company’s revenue in RMB. As of the date of this prospectus supplement, none of

Shineco, our subsidiaries have the intention to distribute earnings on any corporate level in the near future. We intend to keep any future earnings to finance the expansion of our business, and we

do not anticipate that any cash dividends will be paid in the foreseeable future. As of the date of this prospectus supplement, none of the

consolidated subsidiaries have made any transfers of cash, dividends or distributions to Shineco or shareholders of

Shineco.

Neither

the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined

if this prospectus supplement is truthful or complete. Any representation to the contrary is a criminal offense.

This prospectus supplement is dated December

22, 2023

Table

of Contents

PROSPECTUS

SUPPLEMENT

PROSPECTUS

You

should rely only on the information incorporated by reference or provided in this prospectus supplement and the accompanying prospectus.

We have not authorized anyone to provide you with different information. If anyone provides you with different or inconsistent information,

you should not rely on it. This prospectus supplement and the accompanying prospectus do not constitute an offer to sell, or a solicitation

of an offer to purchase, the securities offered by this prospectus supplement and the accompanying prospectus in any jurisdiction where

it is unlawful to make such offer or solicitation. You should assume that the information contained in this prospectus supplement or

the accompanying prospectus, or any document incorporated by reference in this prospectus supplement or the accompanying prospectus,

is accurate only as of the date of those respective documents. Neither the delivery of this prospectus supplement nor any distribution

of securities pursuant to this prospectus supplement shall, under any circumstances, create any implication that there has been no change

in the information set forth or incorporated by reference into this prospectus supplement or in our affairs since the date of this prospectus

supplement. Our business, financial condition, results of operations and prospects may have changed since that date.

ABOUT THIS PROSPECTUS SUPPLEMENT

This document is in two parts.

The first part is this prospectus supplement, which describes the specific terms of this offering of securities hereunder and also adds

to and updates information contained in the accompanying prospectus and the documents incorporated by reference into this prospectus

supplement and the accompanying prospectus. The second part, the accompanying prospectus dated June 10, 2022 included in the registration

statement on Form S-3 (No. 333-261229), including the documents incorporated by reference therein, provides more general information.

Generally, when we refer to this prospectus supplement, we are referring to both parts of this document combined.

To the extent there is a conflict

between the information contained in this prospectus supplement, on the one hand, and the information contained in the accompanying prospectus

or in any document incorporated by reference that was filed with the SEC, before the date of this prospectus supplement, on the other

hand, you should rely on the information in this prospectus supplement. If any statement in one of these documents is inconsistent with

a statement in another document having a later date—for example, a document incorporated by reference in the accompanying prospectus—the

statement in the document having the later date modifies or supersedes the earlier statement.

In this prospectus supplement,

unless otherwise indicated or unless the context otherwise requires,

| |

● |

“China”

or the “PRC” refers to the People’s Republic of China, excluding, for the purpose of this prospectus only, Hong

Kong, Macau and Taiwan; |

| |

|

|

| |

● |

“common

stock” refers to our common stock, par value US$0.001 per share; |

| |

|

|

| |

● |

“RMB”

refers to the legal currency of China; |

| |

|

|

| |

● |

“U.S.

dollars,” “US$” and “dollars” refers to the legal currency of the United States; and |

| |

|

|

| |

● |

“we,”

“us,” “our company” or “our” refers to Shineco, Inc., its subsidiaries. |

WHERE YOU CAN FIND MORE

INFORMATION ABOUT US

We are currently subject to

periodic reporting and other informational requirements of the Securities Exchange Act of 1934, as amended, or the Exchange Act, as applicable

to domestic issuers. Accordingly, we are required to file reports, including annual reports on Form 10-K and other information with the

SEC pursuant to the rules and regulations of the SEC that apply to foreign private issuers.

Documents that we file with,

or furnish to, the SEC are also available on the website maintained by the SEC (www.sec.gov). Our common stock is listed on the

Nasdaq Capital Market. You can consult reports and other information about us that we filed pursuant to the rules.

This prospectus supplement

is part of a registration statement we have filed with the SEC on Form S-3 which was declared effective on June 10, 2022. This prospectus supplement does not contain

all the information set forth in the registration statement and the exhibits to the registration statement. For further information,

we refer you to the registration statement and the exhibits and documents filed as part of the registration statement. If a document

has been filed as an exhibit to the registration statement, we refer you to the copy of the document that has been filed. Each statement

in this prospectus supplement relating to a document filed as an exhibit is qualified in all respects by the filed exhibit.

INCORPORATION OF CERTAIN

INFORMATION BY REFERENCE

The SEC allows us to “incorporate

by reference” the information we file with them. This means that we can disclose important information to you by referring you

to those documents. Each document incorporated by reference is current only as of the date of such document, and the incorporation by

reference of such documents shall not create any implication that there has been no change in our affairs since the date thereof or that

the information contained therein is current as of any time subsequent to its date. The information incorporated by reference is considered

to be a part of this prospectus supplement and should be read with the same care. When we update the information contained in documents

that have been incorporated by reference by making future filings with the SEC, the information incorporated by reference in this prospectus

supplement is considered to be automatically updated and superseded. In other words, in the case of a conflict or inconsistency between

information contained in this prospectus supplement and information incorporated by reference in this prospectus supplement, you should

rely on the information contained in the document that was filed later.

We incorporate by reference

the documents listed below:

| |

(a) |

our

Annual Report on Form

10-K for the year ended June 30, 2023 filed with the SEC on September 28, 2023; |

| |

|

|

| |

(b) |

our

Quarterly Report on Form

10-Q for the quarterly period ended September 30, 2023 filed with the SEC on November 14, 2023; |

| |

|

|

| |

(c) |

our

Current Reports on Form 8-K filed with the SEC on November

17, 2023, December

1, 2023, and December 21, 2023; and |

| |

|

|

| |

(d) |

the

description of the common stock, $0.001 par value per share, contained in our registration statement on Form

8-A filed with the SEC on May 13, 2016 pursuant to Section 12(b) of the Exchange Act and all amendments or reports filed by us

for the purpose of updating those descriptions. |

Copies of all documents incorporated

by reference in this prospectus supplement, other than exhibits to those documents unless such exhibits are specially incorporated by

reference in this prospectus supplement, will be provided at no cost to each person, including any beneficial owner, who receives a copy

of this prospectus supplement on the written or oral request of that person made to:

SHINECO, INC.

T1, South Tower, Jiazhaoye Square

Chaoyang District,

Beijing, People’s Republic of China

Tel: (+86) 10-87227366

SPECIAL NOTE REGARDING

FORWARD-LOOKING STATEMENTS

This prospectus supplement,

the accompanying prospectus and the documents incorporated by reference herein and therein contain forward-looking statements that reflect

our current expectations and views of future events. These statements are made under the “safe harbor” provisions of the

U.S. Private Securities Litigation Reform Act of 1995. You can identify these forward-looking statements by terminology such as “may,”

“could,” “will,” “should,” “would,” “expect,” “plan,” “intend,”

“anticipate,” “believe,” “estimate,” “predict,” “potential,” “future,”

“is/are likely to,” “project” or “continue” or other similar expressions. We have based these forward-looking

statements largely on our current expectations and projections about future events and financial trends that we believe may affect our

financial condition, results of operations, business strategy and financial needs.

The forward-looking statements

included in this prospectus supplement, in the documents incorporated by reference herein and in any amendments to this prospectus supplement

are subject to risks, uncertainties and assumptions about our company which are, in some cases, beyond our control and which could materially

affect our results. Our actual results of operations may differ materially from the forward-looking statements as a result of the risk

factors disclosed in this prospectus supplement, in the documents incorporated by reference herein or in any accompanying prospectus

supplement.

We would like to caution you

not to place undue reliance on these forward-looking statements, and you should read these statements in conjunction with the risk factors

disclosed herein, in the documents incorporated by reference herein or in any accompanying prospectus supplement for a more complete

discussion of the risks of an investment in our securities. We operate in a rapidly evolving environment. New risks emerge from time

to time and it is impossible for our management to predict all risk factors, nor can we assess the impact of all factors on our business

or the extent to which any factor, or combination of factors, may cause actual results to differ from those contained in any forward-looking

statement. We do not undertake any obligation to update or revise the forward-looking statements except as required under applicable

law.

PROSPECTUS SUPPLEMENT SUMMARY

This summary highlights certain information

contained elsewhere in or incorporated by reference into this prospectus supplement. This summary is not complete and does not contain

all of the information that you should consider before deciding whether to invest in our common stock. You should read the entire prospectus

supplement, the accompanying prospectus and the documents incorporated by reference carefully, including the section titled “Risk

Factors” and our financial statements and the notes to those financial statements, which are incorporated by reference, and the

other financial information appearing elsewhere in or incorporated by reference in this prospectus supplement, before making an investment

decision.

Overview

Shineco, Inc. is a holding

company incorporated in Delaware. As a holding company with no material operations of our own, we conduct our operations through our

subsidiaries and in the two years ended June 30, 2022 and 2023, through the variable interest entities (the “VIEs”) and subsidiaries.

Our shares of common stock currently listed on the Nasdaq Capital Markets are shares of our Delaware holding company. The Chinese regulatory

authorities could disallow our structure, which could result in a material change in our operations and the value of our securities could

decline or become worthless.

Current Business

On September 19, 2023, the

Company and Shineco Life Science Group Hong Kong Co., Limited (“Shineco Life”), a company established under the laws of Hong

Kong and a wholly owned subsidiary of the Company (together as the “Buying Parties”) closed the acquisition of 71.42% equity

interest (the “Acquisition”) in Dream Partner Limited, a BVI corporation (“Dream Partner”), pursuant to the stock

purchase agreement (the “Agreement”) dated May 29, 2023, entered into by and among the Buying Parties, Dream Partner, Chongqing

Wintus Group, a corporation incorporated under the laws of mainland China (“Wintus”) and certain shareholders of Dream Partner

(the “Sellers,” together with Dream Partner and Wintus as the “Selling Parties”).

As the consideration for

the Acquisition, the Company (a) paid the Sellers an aggregate cash consideration of $2,000,000 (the “Cash Consideration”);

(b) issued certain shareholders, as listed in the Agreement, an aggregate of 10,000,000 shares of the Company’s restricted Common

Stock (the “Shares”); and (c) transferred and sold to the Sellers 100% of the Company’s equity interest in Beijing

Tenet-Jove Technological Development Co., Ltd. (the “Tenet-Jove Shares”).

Following the closing of

the Acquisition and the sale of the Tenet-Jove Shares, the Company divested its equity interest in its operating subsidiary Beijing Tenet-Jove

Technological Development Co., Ltd. (“Tenet-Jove”) and thereby terminated its VIE Structure.

Dream Partner is a holding

company incorporated in British Virgin Islands. As a holding company with no material operations of its own, it conducts a substantial

majority of its operations through the operating entities established in the People’s Republic of China, or the PRC.

Dream Partner, via its subsidiaries,

integrates the production, processing, export and domestic trade of cocoon silk products in the silk manufacturing industrial chain,

established for more than 20 years, committed to the research and development, production and sales of functional silk fabrics. Dream

Partner owns several large-scale sericulture bases in mainland China, where it can use them to cultivate silkworm cocoons, which is the

raw material for silk production. Dream Partner also has production plant equipped with advanced machinery, such as Italian rapier looms

to produce silk fabric. Dream Partner’s products are sold domestically and globally, mainly in India. Dream Partner cooperates

with a number of scientific research institutions conducting silk fabric innovative research and development and market applications,

and launching a variety of new functional silk fabrics, which possess various qualities, such as waterproof, oilproof, antibacterial,

antiviral and other characters, in response to market demand. Dream Partner advocates a healthy, comfortable and tasteful lifestyle,

creates economic and social benefits with high value-added products, and enhances the core competitiveness of enterprises. Dream Partner

generates revenue from the following three streams:

Processing and distributing

agricultural produce as well as growing and cultivating mulberry trees and silkworm cocoons - Dream Partner currently breeds

silkworms and produces related agricultural products, and continues to develop the sericulture base. Dream Partner works closely with

domestic scientific research institutions to promote mulberry seeds, silkworm seeds and advanced production modes according to local

conditions, reduce the risk of sericulture planting, reduce labor intensity and increase farmers’ income. The adequate output and

high quality of silkworm cocoons in our own sericulture base not only can ensure our own fabric production and manufacturing, but also

can satisfy the outside customers. Dream Partner also carries out fruit distribution business through collaboration with many domestic

fruit traders, and continuously expands the domestic market with high quality imported fruits. Dream Partner imports high quality fruits

mainly from Southeast Asian countries, such as Thailand and Malaysia.

Processing and distributing

silk and silk fabrics as well as other by-products - Processing and distributing silk and silk fabrics is our major business.

We conduct this segment of our business relying on our own bases and factory. Through the integrated operation system of trade, industry

and agriculture, it can achieve real and controllable raw materials, control the production costs and production cycles. In the last

20 years of development, Dream Partner has continued to innovate and upgrade, introduced advanced intelligent manufacturing equipment,

improved production efficiency and product quality, developed innovative varieties, and had strong market competitiveness and won the

recognition of new and old customers. Our silk textiles are sold domestically and globally, mainly in India.

Distributing automotive batteries

for production of electric automotive - In 2020, Dream Partner began to export automotive batteries to U.S. automakers for manufacturing

electric automotives. Due to the new policy requirements of “manufacturing returning to the United States” introduced in

the second half of 2022, American automobile manufacturers have adjusted their procurement strategies accordingly and selected more products

produced and assembled in the United States. After this, our revenue from sales of automotive batteries declined significantly.

Factors Affecting Financial

Performance

Dream Partner believes that

the following factors will affect its financial performance:

Increasing demand for our

products - Dream Partner believes that the increasing demand for its agricultural products will have a positive impact on its financial

position. Dream Partner plans to develop new products and expand its distribution network as well as to grow its business through product

innovation, aiming at increasing its brand awareness, developing customer loyalty, meeting customer demands in various markets and providing

solid foundations for its growth.

Maintaining effective control

of our costs and expenses - Successful cost control depends upon our ability to obtain and maintain adequate material supplies as

required by our operations at competitive prices. Dream Partner will focus on improving its long-term cost control strategies, including

establishing long-term alliances with certain suppliers to ensure adequate supply. Dream Partner currently enjoys the economies of scale

and advantages from the nationwide distribution network and diversified offerings.

Economic and Political

Risks

Dream Partner’s operations

are conducted primarily in the PRC and subject to special considerations and significant risks associated with suppliers and customers

in Southeast Asia and North America. These risks include the political, economic and legal environment and foreign currency exchange

risks. Our financial results may be adversely affected by changes in the political and social conditions in the PRC, and PRC governmental

policies with respect to laws and regulations, anti-inflationary measures, currency conversions, remittances abroad, and rates and methods

of taxation, among other things.

Discontinued Business

Prior to the Acquisition

we conducted a majority of our operations through the operating entities established in the People’s Republic of China, or the

PRC, through the variable interest entities (the “VIEs”), which were then terminated in September 2023, following the Acquisition.

We did not have any equity ownership of the VIEs, instead we received the economic benefits of the VIEs’ business operations through

certain contractual arrangements. We used our subsidiaries and the VIEs’ vertically and horizontally integrated production, distribution,

and sales channels to provide plant-based health and well-being focused products. The health and well-being focused plant-based products

previously sold by the Company are divided into the following three major segments:

Processing and distributing

traditional Chinese herbal medicine products as well as other pharmaceutical products - This segment was conducted through Ankang

Longevity Pharmaceutical (Group) Co., Ltd. (“Ankang Longevity Group”), a Chinese company formerly under contractual arrangement

with the Company which operated 66 cooperative retail pharmacies throughout Ankang Longevity Group, a city in southern Shaanxi province,

China, through which we sold directly to individual customers traditional Chinese medicinal products produced by us as well as by third

parties. Ankang Longevity Group also owned a factory specializing in decoction, which was the process by which solid materials are heated

or boiled in order to extract liquids, and distributed decoction products to wholesalers and pharmaceutical companies around China.

On June 8, 2021, Tenet-Jove

entered into a Restructuring Agreement with various parties. Pursuant to the terms of the Restructuring Agreement, (i) the Company transferred

all of its rights and interests in Ankang Longevity Group to Yushe County Guangyuan Forest Development Co., Ltd. (“Guangyuan”)’s

Shareholders in exchange for Guangyuan Shareholders entering into VIE agreements with Tenet-Jove, which composed of one group of similar

identifiable assets; (ii) Tenet-Jove entered a Termination Agreement with Ankang Longevity Group and the Ankang Longevity Group Shareholders;

(iii) as a consideration to the Restructuring Agreement and based on a valuation report on the equity interests of Guangyuan issued by

an independent third party, Tenet-Jove relinquished all of its rights and interests in Ankang Longevity Group and transferred those rights

and interests to the Guangyuan Shareholders; and (iv) Guangyuan and the Guangyuan Shareholders entered into a series of variable interest

entity agreements with Tenet-Jove. After signing of the Restructuring Agreement, the Company and the shareholders of Ankang Longevity

Group and Guangyuan actively carried out the transferring of rights and interests in Ankang Longevity Group and Guangyuan, and the transferring

was completed subsequently on July 5, 2021. Afterwards, with the completion of all other follow-ups works, on August 16, 2021, the Company,

through its subsidiary Tenet-Jove, completed the previously announced acquisition pursuant to the Restructuring Agreement dated June

8, 2021. The management determined that July 5, 2021 was the disposal date of Ankang Longevity Group.

Processing and distributing

green and organic agricultural produce as well as growing and cultivating yew trees (taxus media) - We cultivated and soled yew

mainly to group and corporate customers, but did not process yew into Chinese or Western medicines. This segment was conducted through

the following VIEs: Qingdao Zhihesheng Agricultural Produce Services, Ltd (“Qingdao Zhihesheng”). Meanwhile, we planted fast-growing

bamboo willows and scenic greening trees through Guangyuan. The operations of this segment were located in the North regions of Mainland

China, mostly carried out in Shanxi Province.

Providing domestic

air and overland freight forwarding services - We provided domestic air and overland freight forwarding services by outsourcing

these services to a third party. This segment was conducted through the Zhisheng VIE, Yantai Zhisheng International Freight Forwarding

Co., Ltd (“Zhisheng Freight”).

Developing and distributing

specialized fabrics, textiles, and other byproducts derived from an indigenous Chinese plant Apocynum Venetum, grown in the Xinjiang

region of China, and known in Chinese as “Luobuma” or “bluish dogbane” - The Luobuma products are specialized

textile and health supplement products designed to incorporate traditional Eastern medicines with modern scientific methods. These products

are predicated on centuries-old traditions of Eastern herbal remedies derived from the Luobuma raw material. This segment is channeled

through our directly-owned subsidiary, Beijing Tenet-Jove Technological Development Co., Ltd. (“Tenet-Jove”), and its 90%

subsidiary Tianjin Tenet Huatai Technological Development Co., Ltd. (“Tenet Huatai”).

Contractual Arrangements with Each VIE

Shineco conducted its business

through a combination of contractual arrangements with PRC operating companies and equity ownership of PRC subsidiaries. The contractual

arrangements with respect to the VIEs were not equivalent to an equity ownership in the business of the VIEs but were used to replicate

foreign investments in China-based companies where Chinese law prohibit or limit direct foreign investment in Chinese companies belonging

to certain categories. Where Shineco operated its business through such contractual relationships, it was subject to risks related to

such operation. As of June 30, 2023, any references to control or benefits that accrued to Shineco because of the VIEs are limited to,

and subject to conditions we have satisfied for consolidation of the VIEs under U.S. GAAP. As of June 30, 2023, the VIEs are consolidated

for accounting purposes but none of them is an entity in which Shineco owned equity. Shineco did not conduct any active operations and

was the primary beneficiary of the VIEs for accounting purposes. Our shareholders did not own any equity in any of Shineco’s subsidiaries

or the VIEs.

The principal regulation

governing foreign ownership of businesses in the PRC is the Foreign Investment Industrial Guidance Catalogue, effective as of April 10,

2015 (the “Catalogue”). The Catalogue classifies various industries into three categories: encouraged, restricted and prohibited.

Shineco was engaged in businesses and industries where direct foreign investment is expressly prohibited: the preparation of traditional

Chinese medicines in small pieces ready for decoction.

Due, in part, to the regulations

on foreign ownership of PRC businesses, neither Shineco neither our subsidiaries owned any equity interest in the Zhisheng Group, with

which Beijing Tenet-Jove Technological Development Co., Ltd., a Chinese company and wholly-owned subsidiary of Shineco (“WFOE”)

had entered into one set of VIE agreements respectively with each following Chinese operating companies: Zhisheng Biotech, Yantai Zhisheng

and Zhihesheng. In addition, as a result of the Restructuring Agreement dated June 8, 2021, WFOE entered into the series of VIE agreements

with Guangyuan Forest and its shareholders on the same date. Instead of direct ownership, Shineco received the economic benefits of each

VIEs’ business operations through a series of contractual arrangements. WFOE, each of the four VIEs and their shareholders had

entered into a series of contractual arrangements, also known as VIE Agreements.

Each set of the VIE Agreements

is described below and consisted of, for each of the Zhisheng Group and Guangyuan, (a) exclusive business cooperation agreements, (b)

equity interest pledge agreements, (c) exclusive option agreements, and (d) powers of attorney. As an overview, these agreements taken

together were designed to allow Shineco to manage the operations of each of the VIEs and to receive all of the net income of such VIEs

in return therefor. To secure WFOE’s interest in the VIEs, the equity interest pledges and option agreements and the powers of

attorney were designed to allow WFOE to step in and convert its contractual interest into an equity interest in the event we determined

that doing so is warranted.

The following is a summary

of the common contractual arrangements that enabled us to receive substantially all of the economic benefits from the four VIEs’

operations for accounting purposes under U.S. GAAP in the years ended June 30, 2022 and 2023.

Exclusive Business Cooperation Agreements

WFOE entered into an Exclusive

Business Cooperation Agreement with Zhisheng Biotech, Yantai Zhisheng, Zhihesheng, and Guangyuan Forest on February 24, 2014, June 16,

2011, May 24, 2012, and June 8, 2021, respectively. WFOE managed each VIE pursuant to the terms of each of the four Exclusive Business

Cooperation Agreements.

Pursuant to substantially

identical Exclusive Business Cooperation Agreements between each VIE and WFOE, WFOE provided each VIE with technical support, consulting

services and other management services relating to its day-to-day business operations and management, on an exclusive basis, utilizing

its advantages in technology, human resources, and information. Additionally, each VIE had granted an irrevocable and exclusive option

to WFOE to purchase from such VIE, any or all of its assets, to the extent permitted under applicable PRC law. WFOE also could exercise,

at its sole discretion, the option to purchase from each VIE any or all of such VIE’s assets at the lowest purchase price permitted

by PRC law. If WFOE exercised such option, the parties had to enter into a separate asset transfer or similar agreement. WFOE owned all

intellectual property rights that are developed during the course of each Exclusive Business Cooperation Agreement. For services rendered

to each VIE by WFOE under the agreement to which such VIE is a party, WFOE was entitled to collect a service fee calculated based on

the time of services rendered multiplied by the corresponding rate, which were approximately equal to the net income of such VIE.

Each Exclusive Business Cooperation

Agreement remained in effect for ten years until it was extended or terminated by WFOE, which could have be done unilaterally, except

in the case of gross negligence or fraud, in which case the VIE could terminate the agreements. Pursuant to each such agreement, WFOE

had absolute authority relating to the management of each VIE, including but not limited to decisions with regard to expenses, salary

raises and bonuses, hiring, firing and other operational functions. Although the Exclusive Business Cooperation Agreements did not prohibit

related party transactions, the audit committee of Shineco was required to review and approve in advance any related party transactions,

including transactions involving WFOE or any VIE. To continue the contractual relationship with Zhihesheng, WFOE entered into an amendment

dated April 24, 2022 to the Exclusive Business Cooperation Agreement with Zhihesheng to extend the term of such Agreement for additional

twenty (20) years from May 23, 2022. Similarly, to continue the contractual relationship with Yantai Zhisheng, WFOE entered into an amendment

dated June 1, 2021 to the Exclusive Business Cooperation Agreement with Yantai Zhisheng to extend the term of such Agreement for additional

twenty (20) years from June 15, 2021.

Equity Interest Pledge Agreements

Under the Equity Interest

Pledge Agreements among the WFOE, each VIE and each group of shareholders of the VIE, the shareholders pledged all of their equity interests

in each such VIE to WFOE to guarantee the performance of such VIE’s obligations under the respective Exclusive Business Cooperation

Agreement. Under the terms of each agreement, in the event that the VIE or its shareholders breached their respective contractual obligations

under the Exclusive Business Cooperation Agreement to which they are a party, WFOE, as pledgee, was entitled to certain rights, including,

but not limited to, the right to collect dividends generated by the pledged equity interests. Each VIE’s shareholders also agreed

that upon occurrence of any event of default, as set forth in the applicable Equity Interest Pledge Agreement, WFOE was entitled to dispose

of the pledged equity interest in accordance with applicable PRC laws. Each VIE’s shareholders further agreed not to dispose of

the pledged equity interests or take any actions that would prejudice WFOE’s interest in the applicable VIE.

Each Equity Interest Pledge

Agreement was effective until all payments due under the related Exclusive Business Cooperation Agreement were paid by the VIE party

thereto. WFOE could cancel or terminate an Equity Interest Pledge Agreement upon a VIE’s full payment of fees payable under its

applicable Exclusive Business Cooperation Agreement.

Exclusive Option Agreements

Under the Exclusive Option

Agreements, shareholders of each VIE irrevocably granted WFOE (or its designee) an exclusive option to purchase, to the extent permitted

under PRC law, once or at multiple times, at any time, part or all of their equity interests in each VIE. The option price was equal

to the capital paid in by the applicable VIE shareholders subject to any appraisal or restrictions required by applicable PRC laws and

regulations. The option purchase price could be increased in case the applicable VIE shareholders make additional capital contributions

to such VIE.

Each agreement remained effective

for a term of ten years and could be unilaterally renewed at WFOE’s election. WFOE, Zhihesheng and all of the shareholders of Zhihesheng

entered into an amendment dated April 25, 2022 to the Exclusive Option Agreement to extend the term of such Agreement for additional

twenty (20) years from May 23, 2022. Yantai Zhisheng, WFOE and all of the shareholders of Yantai Zhisheng entered into an amendment dated

June 1, 2021 to the Exclusive Option Agreement with Yantai Zhisheng to extend the term of such Agreement for additional twenty (20) years

from June 15, 2021.

Powers of Attorney

Under the Powers of Attorney,

the shareholders of each VIE authorized WFOE to act on their behalf as their exclusive agent and attorney with respect to all rights

as shareholders of the respective VIEs, including but not limited to: (a) attending shareholders’ meetings; (b) exercising all

the shareholder’s rights, including voting, that shareholders are entitled to under the laws of China and the Articles of Association,

including but not limited to the sale or transfer or pledge or disposition of shares in part or in whole; and (c) designating and appointing

on behalf of shareholders the legal representative, the executive director, supervisor, the chief executive officer and other senior

management members of the respective VIEs.

Summary of challenges and risks involved

in the VIE Arrangements and enforcing the VIE Agreements

Prior to the Acquisition

and the termination of the VIE structure, Shineco was also subject to the legal and operational risks associated with being based in

and having the majority of its operations in China and operating through VIEs. These risks could result in material changes in operations,

or a complete hindrance of Shineco’s ability to offer or continue to offer its securities to investors, and could cause the value

of Shineco’s securities to significantly decline or become worthless. Recently, the PRC government initiated a series of regulatory

actions and statements to regulate business operations in China with little advance notice, including cracking down on illegal activities

in the securities market, enhancing supervision over China-based companies listed overseas using variable interest entity structure,

adopting new measures to extend the scope of cybersecurity reviews, and expanding the efforts in anti-monopoly enforcement. On July 6,

2021, the General Office of the Communist Party of China Central Committee and the General Office of the State Council jointly issued

an announcement to crack down on illegal activities in the securities market and promote the high-quality development of the capital

market, which, among other things, requires the relevant governmental authorities to strengthen cross-border oversight of law-enforcement

and judicial cooperation, to enhance supervision over China-based companies listed overseas, and to establish and improve the system

of extraterritorial application of the PRC securities laws. On July 10, 2021, the PRC State Internet Information Office issued the Measures

of Cybersecurity Review, which requires cyberspace companies with personal information of more than one (1) million users that want to

list their securities on a non-Chinese stock exchange to file a cybersecurity review with the Office of Cybersecurity Review of China.

On December 28, 2021, a total of thirteen governmental departments of the PRC, including the Cyberspace Administration of China (the

“CAC”), issued the Measures of Cybersecurity Review, which became effective on February 15, 2022. The Cybersecurity Review

Measures provide that an online platform operator, which possesses personal information of at least one million users, must apply for

a cybersecurity review by the CAC if it intends to be listed in foreign countries. Because our previous operations doid not possess personal

information from more than one million users at this moment, Shineco did not believe that it is subject to the cybersecurity review by

the CAC.

As of June 30, 2023, neither

the Measures of Cybersecurity Review nor the anti-monopoly regulatory actions had impacted Shineco’s ability to conduct its business,

accept foreign investments, or continue its listing on Nasdaq or on another non-Chinese stock exchange; however, there are uncertainties

in the interpretation and enforcement of these new laws and guidelines, which could materially and adversely impact the Company’s

overall business and financial outlook. In summary, as of June 30, 2023, the recent statements and regulatory actions by China’s

government related to the use of variable interest entities and data security or antimonopoly concerns had not affected the Company’s

ability to conduct its business, accept foreign investments, or list on a U.S. or other foreign exchange. However, since these statements

and regulatory actions by the PRC government are newly published and official guidance and related implementation rules have not been

issued, it is highly uncertain what the potential impact such modified or new laws and regulations will have on Shineco’s daily

business operation, the ability to accept foreign investments and list on a U.S. or non-Chinese exchange. The Standing Committee of the

National People’s Congress (the “SCNPC”) or other PRC regulatory authorities may in the future promulgate laws, regulations

or implementing rules that would require Shineco or any of its subsidiaries to obtain regulatory approval from Chinese authorities before

listing in the U.S.

Prior to the Acquisition and

the termination of the VIE structure, because Shineco did not hold equity interests in the VIEs, we were subject to risks due to the

uncertainty of the interpretation and application of the PRC laws and regulations, including but not limited to regulatory review of

oversea listing of PRC companies through a special purpose vehicle, and the validity and enforcement of the contractual arrangement with

the VIEs. We were also subject to the risks of the uncertainty that the PRC government could disallow the VIE structure, which could

have likely resulted in a material change in our operations, or a complete hindrance of our ability to offer or continue to offer our

securities to investors, and the value of our shares of common stock may had depreciated significantly. The arrangements of VIE Agreements

are less effective than direct ownership due to the inherent risks of the VIE structure and that Shineco could have had difficulty in

enforcing any rights it had under the VIE agreements with the VIEs, its founders and shareholders in the PRC because all of the VIE agreements

are governed by the PRC laws and provide for the resolution of disputes through arbitration in the PRC, where the legal environment is

uncertain and not as developed as in the United States, and where the Chinese government has significant oversight and discretion over

the conduct of Shineco’s business and may intervene or influence Shineco’s operations at any time with little advance notice,

which could result in a material change in our operations and/or the value of your common stock. In addition, the contractual agreements

with the VIEs have not been tested in court in China and this structure involves unique risks to investors. Furthermore, these VIE agreements

may not be enforceable in China if the PRC authorities or courts take a view that such VIE agreements contravene with the PRC laws and

regulations or are otherwise not enforceable for public policy reasons. In the event we were unable to enforce these VIE Agreements,

Shineco would have not been able to derive economic benefits from the VIEs and Shineco’s ability to conduct its business could

have been materially and adversely affected. As of June 30, 2023, any references to economic benefits that accrued to Shineco because

of the VIEs are limited to, and subject to conditions we had satisfied for consolidation of the VIEs under U.S. GAAP. The VIEs are consolidated

for accounting purposes but none of them is an entity in which Shinceco owned equity. Shineco did not conduct any active operations and

ws the primary beneficiary of the VIEs for accounting purposes. See “Risk Factors - Risks Relating to Our Corporate Structure”,

“Risk Factors - Risks Associated With Doing Business in China” and “Risk Factors - Risks Relating to Investment in

Our Common Stock” for more information.

Asset Transfer and Dividend Distribution

Among Shineco, its Subsidiaries and the VIEs

As of the date of this prospectus supplement,

Shineco, any of its subsidiaries or any of the VIEs have not distributed any earnings or settled any amounts owed under the VIE Agreements.

We intend to keep any future earnings to finance the expansion of our business, and we do not anticipate that any cash dividends will

be paid in the foreseeable future.

As of June 30, 2023, Shineco’s

operating subsidiaries and the VIEs received substantially all of the Company’s revenue in RMB. Under our previous corporate structure

of mixed ownership and VIE arrangement, the WFOE had paid some of Shineco’s expenses and Shineco had from time to time transferred

cash to WFOE to fund WFOE and other subsidiaries’ or VIEs’ operations. For the year ended June 30, 2023, Shineco transferred

cash in the total amount of $200,000 to WFOE and WFOE paid expense approximately $23,746 on behalf of Shineco. For the year ended June

30, 2022, Shineco transferred cash in the aggregate amount of $15,349,077 to the WFOE and WFOE paid $978,979 to Shineco’s creditors

on behalf of Shineco. The assets transfer was for business operation purposes. There was no distribution of earnings by the PRC operating

subsidiaries to Shineco during the years ended June 30, 2023 and 2022, respectively.

Under the existing PRC foreign

exchange regulations, payments of current account items, such as profit distributions and trade and service-related foreign exchange

transactions, can be made in foreign currencies without prior approval from the State Administration of Foreign Exchange (the “SAFE”)

by complying with certain procedural requirements. Approval from or registration with appropriate government authorities is, however,

required where RMB is to be converted into a foreign currency and remitted out of China to pay capital expenses, such as the repayment

of loans denominated in foreign currencies. The PRC government may also, at its discretion, restrict access in the future to foreign

currencies for Shineco’s accounts with little advance notice.

Product Description

Yew Trees, fast-growing bamboo

willows and scenic greening trees

Prior to the Acquisition

and the termination of the VIE structure, through Zhisheng Group VIEs, we sold ornamental yew trees and yew cuttings to third parties.

We also rented ornamental yew trees to companies who desired the environmental benefits of natural plants in their workplaces. Before

engaging in the business of selling yew trees and yew cuttings, we were primarily engaged in the production, distribution and sale of

agricultural products, including the planting and processing of organic fruits and vegetables, such as tomatoes, eggplants, string beans,

peppers as well as certain popular fruits in China like blueberries and wine grapes, but those operations were temporarily scaled back

due to stiff competition and a change of our internal policy in favor of the expansion of the yew tree business.

As our inventories of young

yew trees matured, our long-term goals were particularly focused on the extraction of paclitaxel or taxol, which is derived from certain

species of yew trees including those we grew. Taxol, a broad-spectrum mitotic inhibitor used in cancer chemotherapy, can be extracted

from mature yew trees. As a mitotic inhibitor, taxol adheres to rapidly dividing cancerous cells during mitosis (cell division) and interferes

with the division process. It may suppress tumor growth through regulating microtubule stabilization, inducing apoptosis and adjusting

immunologic mechanism. Taxol is also used for the prevention of restenosis, which is the narrowing of blood vessels. In the treatment

of certain soft tissue cancers, such as breast cancer, taxol is given for early stage and metastatic breast cancer after combination

anthracycline and cytoxan therapy and is also given as treatment to shrink a tumor before surgery. It can also be used together with

a drug called Cisplatin to treat advanced ovarian cancer and non-small cell lung cancer, or “NSCLC.” The U.S. Food and Drug

Administration approved taxol as the primary and secondary treatment for NSCLC. There are other generally accepted protocols for the

use of taxol as a cancer drug alone or in combination with other drugs depending upon the diagnosis, staging and type of cancer, as well

as a patient’s medical history, tolerances and allergies, among other relevant factors. Taxol is usually sold to large pharmaceutical

companies to be used in their products, which can be used to treat patients with lung, ovarian, breast, head and neck cancer, and advanced

forms of Kaposi’s sarcoma.

Following the acquisition

of Guangyuan, we entered the market of planting fast-growing bamboo willows and scenic greening trees. The operations of this segment

were located in the North regions of Mainland China, mostly carried out in Shanxi Province.

Tenet-Jove Textiles

Various scientists and other

Chinese researchers have brought modern scientific methods to the study of Luobuma, and have determined that Luobuma fibers have an increased

tendency to radiate light at the “far infrared” end of the light spectrum, with wavelengths measuring between 8-15 microns

(referred to as “FIR”). Based on Chinese scientific studies some believe that Luobuma’s FIR-radiating qualities exert

a positive effect on various functions of the human body, including cellular metabolism. For this reason, we had marketed and sold these

products utilizing such technology. These products are popular with Chinese customers seeking the perceived benefits of traditional Chinese

medicine.

For example, according to

a report by the College of Science of Tianjin University, tests conducted by the PRC’s National Institute of Metrology have reported

that the radiance rate of far infrared light from Luobuma fiber is 84%, 2 to 4 times higher than that from cotton and other natural fibers.

The same tests found that the FIR radiance rate from our proprietary bio-ceramic powder reaches 91%. Healthful benefits have been observed

at radiance rate levels above 70%. Based on these observations about FIR radiance, we had developed textiles that our customers can wear

and from which we believe they can receive those health benefits commonly associated with Chinese herbal remedies.

Tenet-Jove first commercially

developed the natural FIR-radiant properties of the Luobuma plant in 1997. We referred to this natural Luobuma fiber as a “Second

Generation” FIR textile. The “First Generation” of FIR-radiant textiles initially became popular in China around 1989,

when manufacturers learned to add 3% of a FIR-radiant inorganic material to synthetic fibers comparable to nylon or polyester. This “First

Generation” FIR material employs a relatively low level of technology and has relatively few perceived or measurable health benefits.

The “Second Generation” FIR textiles we had developed are softer, smoother and more breathable natural fibers that are not

as prone to static electricity as the low technology “First Generation” FIR-radiant textiles.

The Luobuma fabrics had been

a success in the Chinese domestic market and had also received numerous awards. The technology applied to the Luobuma-based FIR Therapeutic

Clothing and Textile Products had received a “Special Golden Award” from the China National Intellectual Property Bureau

at China’s National Patent and Brand Expo. The products under the brand name of “Tenethealth” had also been honored

with the title of “Consumer’s Favorite Products” by the Chinese Consumer Association.

The fibers of natural Luobuma

FIR materials can contain up to 32 medicinal compounds, many of which are familiar to practitioners of traditional Chinese medicine.

In addition, the processes for manufacturing Luobuma textiles produced a fabric that is smooth, air-permeable, and soft. By combining

a product that is familiar to PRC consumers seeking the benefits of traditional Chinese medicine with quality and comfort, we believes

we were innovative and had chosen a product that had great commercial potential in the Chinese textile market.

Tenet-Jove Product Development

We had developed what we

term a “Third Generation” of FIR textiles under a contract with the Institute of Process Engineering at the Chinese Academy

of Sciences, one of the leading scientific institutions in China. Our research and development had focused on adding nanotechnology enhancements

to the Luobuma textile products, in which we used small-scale nanotechnology to be embed or impregnate our Luobuma-fiber textiles with

other FIR-radiant materials, bio-ceramic materials, or other Chinese herbal remedies. Using these nanotechnology methods, we had developed

and marketed health-promoting textile goods that are impregnated with FIR-radiant materials or other Chinese herbal remedies, which are

then absorbed through the wearer’s skin. We believed that these “Third Generation” FIR textiles will better combine

the health benefits of Luobuma with an even softer, more natural cotton-like fabric that will be popular with Chinese consumers.

Prior to the Acquisition

and the termination of the VIE structure, the Company produced approximately 100 “Third Generation” FIR textile products.

These textile products included:

| |

● |

Far Infrared bedding sets (including various pillows, comforters,

and sheets); |

| |

|

|

| |

● |

Far Infrared underwear, T-shirts, and socks; |

| |

|

|

| |

● |

Far Infrared knee and shin pads, waist supports and other protective

clothing; and |

| |

|

|

| |

● |

Far Infrared body wraps or protectors (for the ankle, elbow, wrist,

and knee). |

All our textile products

were made of Luobuma-based fibers and were impregnated with bio-ceramic powder, which contains various minerals such as halloysite. Both

the fiber and the bio-ceramic powder were developed with the Company’s patented, proprietary techniques.

Manufacturing and Production Facilities

Prior to the Acquisition

and the termination of the VIE structure, we had formed strategic alliances with several certified knitting and clothing manufacturers

throughout China in order to produce the Luobuma products. We assigned them limited manufacturing jobs and require certain conditions,

including protecting our proprietary techniques and meeting our rigid quality standards.

Strategy for Research and Development

| |

● |

To

keep the products proprietary and patented; |

| |

|

|

| |

● |

To

commit to further development of the Luobuma byproducts, houpu magnolia products, and selenium-enriched herbs and plants; and |

| |

|

|

| |

● |

To

build strategic alliances with universities and scientific institutions, which allowed us exposure to advanced technologies, excellent

researchers and scientists and we believed that it will lower the costs and timing of the development of new products. |

Tenet-Jove specialized in

developing Luobuma products and combining FIR technology with natural herbal medicines. We estimated that there are large supplies of

Luobuma in China, especially Xinjiang Province. In China, Luobuma can grow as high as 3.6 meters. In the first year after planting, Luobuma

can be harvested once during that year; thereafter, it can be harvested twice per year before or at the beginning of the flowering period

in June and a second time around September.

Intellectual Property

Trademarks

Tenet-Jove had obtained 18

trademark registrations at the China Trademark Office. As of June 30, 2023, we are not aware of any valid claim or challenges to our

right to use the registered trademark or any counterfeit or other infringement to the registered trademark.

Distribution Network

Prior to the Acquisition

and the termination of the VIE structure, we sold the products through various distribution networks.

The Luobuma product distribution

networks consisted of four distributors who distribute the products to approximately 21 outlets, including flagship stores, retail stores

and sales counters. These distributors sold the products throughout mainland China, under the proprietary brand name and “Tenethealth®”

trademark. We also sold the Luobuma textile products online through third party e-commerce websites, such as Taobao, Tmall and JD. The

yew trees and agricultural products were primarily sold through our sales personnel and group and institutional sales.

Our sales and distribution

strategy for the products focused on expanding our distribution network of retail stores and sales counters into all major provinces

and cities of China. We also planned to use our then distribution network to introduce the newly developed products into target markets

more efficiently and effectively.

Sales and Marketing

Prior to the Acquisition

and the termination of the VIE structure, we marketed Luobuma to consumers primarily by highlighting its unique characteristics- the

material is soft like cotton, breathable like hemp and is smooth to the touch like silk, and its FIR-radiating qualities are believed

by some to exert a positive effect on various functions of the human body. Very few other companies in China were involved with Luobuma

fiber production, so we were chiefly able to market the products against products of natural and man-made fibers that do not have the

perceived advantages of Luobuma. The small number of companies that were involved in Luobuma fiber production were still using the traditional,

outdated methods of producing Luobuma. We were the only company using advanced technologies. Tenet-Jove’s overall marketing strategy

included:

| |

● |

Brand marketing strategy, primarily through media publicity, product-

and market-oriented strategy; |

| |

|

|

| |

● |

Distinguishing Luobuma as a high-end, technologically advanced native

Chinese product; and |

| |

|

|

| |

● |

Online advertising, which included online advertisements appearing

on the sites where we sold our products, as well as social media advertising, including Wechat, and direct e-mail solicitations. |

The Zhisheng Group emphasized

the following marketing strategies:

| |

● |

Focusing on the advanced growing conditions provided by the modern

greenhouse operations and the potential pharmaceutical byproducts of yew, especially paclitaxel or taxol; and |

| |

|

|

| |

● |

Brand marketing to focus on the yew’s brand positioning. |

Prior to the discontinuation

and the Acquisition, the Company’s sales were generated through the following five major channels:

| |

1. |

Retail stores and sales counters. We mainly sold the Luobuma related

products through sales counters and medicine through the pharmacy chain stores. |

| |

|

|

| |

2. |

Sales to group or institutional customers. We mainly sold the organic

agricultural products and yew trees to group or corporate customers. |

| |

|

|

| |

3. |

Seminars and conferences. Because a majority of new consumers need

to learn about our new products before buying them, it was very important and effective for us to organize or sponsor seminars and

events to present healthcare knowledge while introducing and selling the products to new users. |

| |

|

|

| |

4. |

E-commerce. We mainly sold the Luobuma related products through

Tmall and Taobao to underdeveloped regions in China, Taiwan and Macau. We were one of only three certified online sellers of Luobuma

textile products on China’s largest online sales platform, Tmall run by Alibaba. Selling through the Internet had become increasingly

important to our sales in undeveloped regions and developed cities. |

The Market

Prior to the Acquisition

and the termination of the VIE structure, we primarily marketed our health and wellbeing-focused products in China. We did not sell any

of our products in the United States or Canada. On the demand side, we believed that the following four forces drove market growth in

all three of the business segments:

| |

1. |

The rapid growth of China’s economy, which has produced one

of the largest groups of middle-class families in the world, with the largest collective purchasing power in the world. The Brookings

Institution estimates that by 2030, over 70 percent of China’s population could be middle class, consuming approximately $10

trillion in goods and services. |

| |

|

|

| |

2. |

The increase of China’s aging population. The China Census

Bureau predicts that the majority of the China “baby boom” population (representing 40% of China’s total population)

will be 66 or older by 2021, which represents over 500 million potential consumers of our pharmaceutical and healthcare products,

the majority of which are sold to older customers. |

| |

|

|

| |

3. |

Chinese people’s increasing attention and awareness to healthy

and active lifestyles, especially in urban areas. |

| |

|

|

| |

4. |

Chinese healthcare reforms. |

Competition

We competed with other top-tier

healthcare companies in China. Many of them were more established than we were and had significantly greater financial, technical, marketing

and other resources than we possessed. Some of our competitors had greater name recognition and a larger customer base. Those competitors

could have responded more quickly to new or changing opportunities and customer requirements and could have undertaken more extensive

promotional activities, offer more attractive terms to customers, and adopt more aggressive pricing policies. Some of our competitors

had also developed similar products that compete with ours.

Our most prominent competitors

in China’s textile products market were primarily large-scale textile companies, such as Luolai Home Textile Co., Fuanna Bedding

and Furnishing Co., Ltd., Violet Home Textile Co., and Shuixing Home Textile Co., Ltd, as well as Bauerfeind Sports and Albert Medical,

makers of protective clothing products similar to our protective clothing products. Our most prominent competitors in China’s agricultural

market were Beijing Jinfu Yinong Agricultural Technology Group Co., Ltd. for vegetables and other produce and Shenyang Xincheng Garden

Engineering Co., Ltd. for yew trees.

Zhisheng Group

There were dozens of companies

planting and cultivating yew trees in China, some of which were large-scale companies. Shenyang Xincheng Garden Engineering Co., Ltd.

was a large agricultural competitor whose main product is yew. Their nurseries had the most mature yew trees in northeast China, and

the average age of their yew trees is more than eleven years old. Another competitor, Chongqing Jiangjin District Mansheng Agricultural

Development Co., Ltd., had the biggest nursery for young plants in Southwest China. And Jingyin City Hengtu Town Green Industry Yew Base

specializes in cultivating, planting, gardening, and technological development of yew trees. They were the first company to introduce

taxus media yew trees in China.

Tenet-Jove

There were few viable competitors

producing advanced technology textile products with health benefits like our Luobuma textile products. Principally, our competitors were

those that market and sold traditional textile products, such as Luolai Home Textile Co., Fuanna Bedding and Furnishing Co., Ltd., Violet

Home Textile Co., and Shuixing Home Textile Co., Ltd, as well as those companies that marketed and sold protective clothing, like Bauerfeind

Sports and Albert Medical. Luobuma is native to China, thus our ability to source raw materials locally greatly enhanced our competitive

position in the Chinese market for high quality textile products with perceived health benefits.

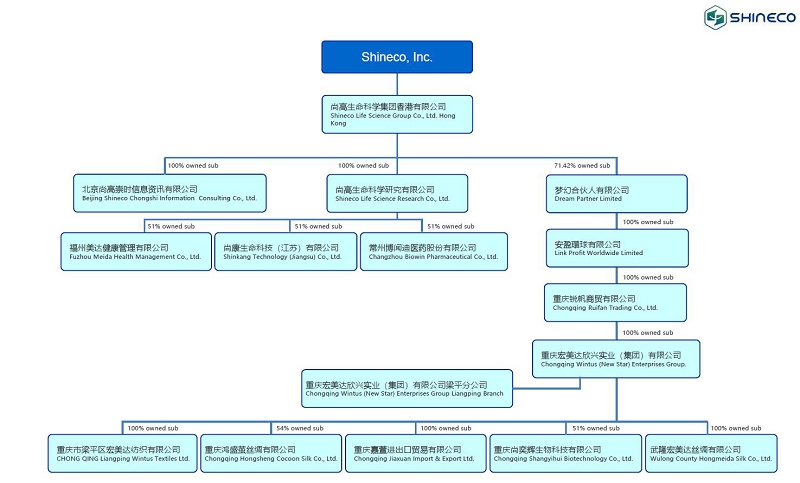

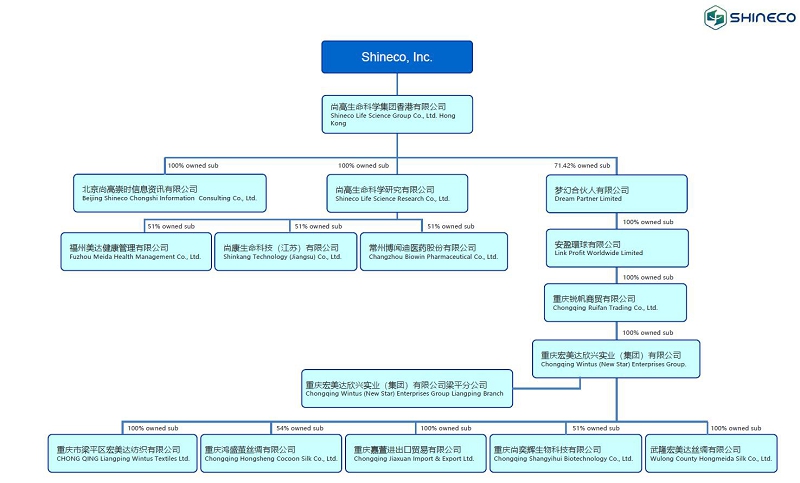

Corporate Structure

The chart below depicts the

corporate structure of the Company as of the date of this prospectus supplement.

Relevant PRC Regulations

Permissions from the PRC Authorities to

Issue Our Common Stock to Foreign Investors

As of June 30, 2023, Shineco,

our subsidiaries and the VIEs, (1) were not required to obtain any permission from any PRC authorities to offer, sell or issue our common

stock to non-Chinese investors, (2) were not covered by the permission requirements from the China Securities Regulatory Commission (the

“CSRC”), Cyberspace Administration of China (the “CAC”), or any other regulatory agency that is required to approve

of the VIEs’ operations, and (3) had not received nor been denied such permissions by any PRC authorities. Nevertheless, the General

Office of the Central Committee of the Communist Party of China and the General Office of the State Council jointly issued the “Opinions

on Severely Cracking Down on Illegal Securities Activities According to Law,” or the July 6, 2021 Opinions, which were made available

to the public on July 6, 2021. The July 6, 2021 Opinions emphasized the need to strengthen the administration over illegal securities

activities, and the need to strengthen the supervision over overseas listings by Chinese companies. Given the current PRC regulatory

environment, it is uncertain whether and when we or any of our subsidiaries, will be required to obtain any permission from the PRC government

to list or continue listing on a U.S. stock exchange in the future, and even when we obtain such permission, whether it will be denied

or rescinded. We have been closely monitoring regulatory developments in China regarding any necessary approvals from the CSRC, CAC or

other PRC governmental authorities required for overseas listings.

If (i) we, our subsidiaries

inadvertently conclude that any of such permission was not required or (ii) it is determined in the future that the approval of the CSRC,

CAC or any other regulatory authority is required for maintaining listing of our securities on Nasdaq, we will actively seek such permissions

or approvals but may face sanctions by the CSRC, CAC or other PRC regulatory agencies. These regulatory agencies may impose fines and

penalties on our operations in China, limit our ability to pay dividends outside of China, limit our operations in China, delay or restrict

the repatriation of the proceeds from offerings into China or take other actions that could have a material adverse effect on our business,

financial condition, results of operations and prospects, as well as the trading price of our securities. The CSRC, CAC or other PRC

regulatory agencies also may take actions requiring us, or making it advisable for us, to halt offerings before settlement and delivery

of our securities. Any uncertainties and/or negative publicity regarding such an approval requirement could have a material adverse effect

on the trading price of our securities. In the event that we failed to obtain such required approvals or permissions, it would be likely

that our securities would be delisted from the Nasdaq or any other foreign exchange our securities are listed then.

The Holding Foreign Companies Accountable

Act

On May 20, 2020, the U.S.

Senate passed the Holding Foreign Companies Accountable Act (“HFCAA”) requiring a foreign company to certify it is not owned

or controlled by a foreign government if the PCAOB is unable to audit specified reports because the company uses a foreign auditor not

subject to PCAOB inspection. On December 18, 2020, the Holding Foreign Companies Accountable Act or HFCAA was signed into law. On September

22, 2021, the PCAOB adopted a final rule implementing the HFCAA, which prohibits foreign companies from listing their securities on U.S.

exchanges if the company has been unavailable for PCAOB inspection or investigation for three consecutive years.

Our common stock may be prohibited

from trading on a national exchange or “over-the-counter” markets under the HFCAA if the Public Company Accounting Oversight

Board (“PCAOB”) determines that it is unable to inspect or fully investigate our auditor and as a result the exchange where

our securities are traded may delist our securities. Furthermore, on June 22, 2021, the U.S. Senate passed the Accelerating Holding Foreign

Companies Accountable Act (the “AHFCAA”), which was signed into law on December 29, 2022, amending the HFCAA and requiring

the SEC to prohibit an issuer’s securities from trading on any U.S. stock exchange if its auditor is not subject to PCAOB inspections

for two consecutive years instead of three consecutive years. Pursuant to the HFCAA, the PCAOB issued a Determination Report on December

16, 2021, which found that the PCAOB was unable to inspect or investigate completely certain named registered public accounting firms

headquartered in mainland China and Hong Kong. On December 15, 2022, the PCAOB issued a report that vacated its December 16, 2021 determination