UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act File Number 811-22551

MAINSTAY MACKAY DEFINEDTERM

MUNICIPAL OPPORTUNITIES FUND

(Exact name of Registrant as specified in charter)

51 Madison Avenue, New York, NY 10010

(Address of principal executive offices) (Zip code)

J. Kevin Gao, Esq.

30 Hudson

Street

Jersey City, New Jersey 07302

(Name and address of agent for service)

Registrant’s telephone number, including area code: (212) 576-7000

Date of fiscal year end: May 31

Date of reporting period:

May 31, 2023

| Item 1. |

Reports to Stockholders. |

MainStay MacKay DefinedTerm Municipal Opportunities Fund

Message from the President and

Annual Report May 31, 2023 | NYSE Symbol MMD

Sign up for e-delivery of your shareholder reports. For full details on e-delivery, including who can participate and what you can receive via e-delivery,

please log in to www.computershare.com/investor.

| |

|

|

|

Not Insured by Any Government Agency |

This page

intentionally left blank

Message

from the President

Despite elevated market volatility driven by high levels of inflation and rising interest rates, broadly based bond

indices saw modest overall changes during the 12-month reporting period ended May 31, 2023. Declines during

the first four-and-a-half months, driven by increasing inflationary pressures and aggressive monetary

efforts to curb them, were largely balanced by gains during the latter months, as inflation began responding to central bank interest rate increases, and the pace of the increases moderated.

In May 2022, before the start of the reporting period, U.S. inflation stood at an annualized rate of 8.58%, up from 4.99% in May 2021 and 0.12% in May 2020. In an effort to rein in

inflation, the U.S. Federal Reserve (the “Fed”) raised the federal funds rate eight times

during the reporting period, hiking the benchmark federal funds rate from 0.75%–1.00% at the beginning of June 2022 to 5.00%–5.25% in May 2023—the Fed’s most aggressive series of rate increases since the

1980’s. Inflation appeared to respond, easing steadily from a peak of 9.06% in June 2022 to 4.05% in

May 2023. Although the Fed projected additional rate rises in 2023, by the end of the reporting period the current rate-hike cycle appeared near its end. Economic growth, although slower, remained positive, supported by historically

high levels of employment and strong consumer spending.

Fixed-income market behavior during the reporting period reflected the arc of monetary policy and economic developments.

Bond prices trended lower early in the period, as yields rose along with interest rates. Short-term yields

rose faster than long-term yields, producing a yield curve inversion—with long-term rates lower than

short-term rates—that persisted from July 2022 through the end of the reporting period. However, market

sentiment improved in the second half of the period when inflationary pressures eased. As the Fed decreased

the level of rate increases, focus turned toward the possibility of eventual rate reductions and a

potential “soft landing” for the economy. On a more negative note, a small number of high-profile, regional U.S.

bank failures in March and April 2023 raised

fears of a possible wider banking industry contagion and future credit constraints. In general, although

most bond classes lost modest ground during the reporting period, municipal issues produced mild gains,

bolstered by favorable supply/demand dynamics and the sector’s historically low default

rates.

While many market observers believe the Fed has neared the end of the current cycle of rate increases, the Fed remains sharply focused on its inflation target of 2%, warning that

further increases are likely. Only time will tell if the market’s favorable expectations prove

well-founded, and if economic growth can stay positive despite the impact of relatively high interest rates.

However, the uncertainties implicit in the current economic environment appear to bode well for the

municipal bond market, due to the sector’s relative stability compared to taxable equivalents,

fundamental credit strength, and tax-advantaged characteristics.

MainStay MacKay DefinedTerm Municipal Opportunities Fund provides an opportunistic investment approach to the municipal

bond market through an active, relative-value strategy managed by MacKay Shields, a team with decades of

municipal bond experience. As such, the Fund exemplifies the one-on-one philosophy and diversified,

multi-boutique investment resources that set New York Life Investments apart.

Thank you for trusting us to help meet your investment needs.

Sincerely,

Kirk C. Lehneis

President

The opinions expressed are as of the date of this report and are

subject to change. There is no guarantee that any forecast made will come to pass. This material does not constitute investment advice and is not intended as an endorsement of

any specific investment. Past performance is no guarantee of future results.

Not part of the Annual Report

Certain material in this report

may include statements that constitute “forward-looking statements” under the U.S. securities laws. Forward-looking statements include, among other

things, projections, estimates and information about possible or future results or events related to the Fund, market or regulatory developments. The views

expressed herein are not guarantees of future performance or economic results and involve certain risks, uncertainties and assumptions that could cause actual

outcomes and results to differ materially from the views expressed herein. The views expressed herein are subject to change at any time based upon economic,

market, or other conditions and the Fund undertakes no obligation to update the views expressed herein.

Fund

Performance and Statistics (Unaudited)

Performance data quoted

represents past performance of Common shares of the Fund. Past performance is no guarantee of future results. Because of market volatility and other factors,

current performance may be lower or higher than the figures shown. Investment return and principal value will fluctuate. For performance information current to the most recent month-end, please

visit newyorklifeinvestments.com/mmd.

The performance table and graph do not reflect the deduction of taxes that a shareholder would pay on distributions or the sale of Fund shares.

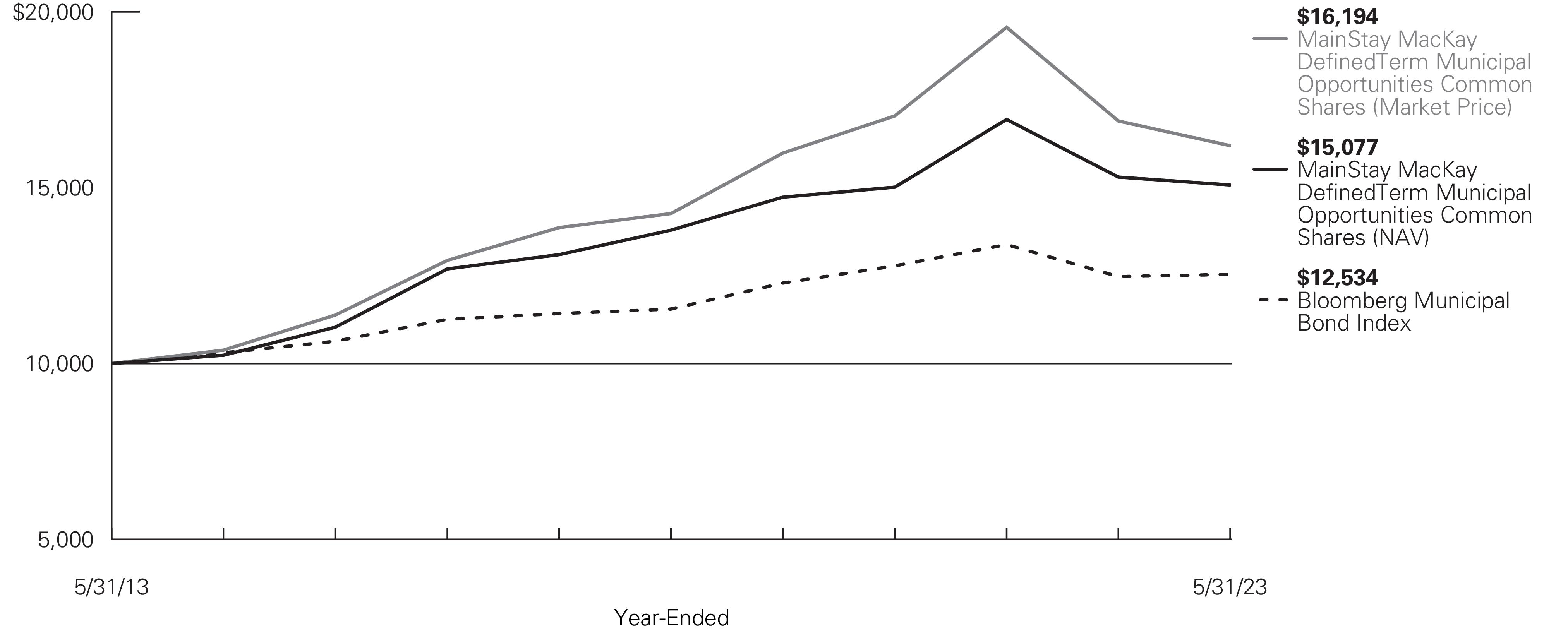

Average Annual Total Returns for the Year-Ended May 31, 2023* |

| |

|

|

|

| |

|

|

|

| |

|

|

|

Bloomberg Municipal Bond Index2

|

|

|

|

Morningstar Muni National Long Category

Average3 |

|

|

|

| |

Returns for indices reflect no deductions for fees, expenses or taxes, except for foreign withholding taxes where applicable. Results assume reinvestment of all dividends

and capital gains. An investment cannot be made directly in an index.

|

| |

Total returns assume dividends and capital gains distributions are reinvested. |

| |

The Bloomberg Municipal Bond Index is considered representative of the broad market for investment-grade, tax-exempt bonds with a maturity of at least one year.

Bonds subject to the alternative minimum tax or with floating or zero coupons are

excluded. |

| |

The Morningstar Muni National Long Category Average is representative of funds that invest in bonds issued by various state and local governments to fund public

projects. The income from these bonds is generally free from federal taxes. These funds

have durations of more than 7 years. Results are based on average total returns of

similar funds with all dividends and capital gain distributions reinvested. |

Fund Statistics as of May 31,

2023

| |

|

|

|

| |

|

Total Net Assets (millions) |

|

| |

|

Total Managed Assets (millions)2 |

|

| |

|

|

|

| |

|

|

|

| |

Premium/Discount is the percentage (%) difference between the market price and the NAV. When the market price exceeds the NAV, the Fund is trading at a premium.

When the market price is less than the NAV, the Fund is trading at a

discount. |

| |

“Managed Assets” is defined as the Fund’s total assets, minus the sum of its accrued liabilities (other than Fund liabilities incurred for the purpose of

creating effective leverage (i.e. tender option bonds) or Fund liabilities related to

liquidation preference of any Preferred shares issued). |

| |

Leverage is based on the use of proceeds received from tender option bond transactions, issuance of Preferred shares, funds borrowed from banks or other institutions

or derivative transactions, expressed as a percentage of Managed Assets.

|

| |

Alternative Minimum Tax (“AMT”) is a separate tax computation under the Internal Revenue Code that, in effect, eliminates many deductions and credits and creates

a tax liability for an individual who would otherwise pay little or no tax, expressed as

a percentage of Managed Assets. |

Portfolio

Composition as of May 31,

2023†(Unaudited)

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

Other Assets, Less Liabilities |

|

| |

|

| |

As a percentage of Managed Assets. |

| |

As of May 31, 2023, 58.3% of the Puerto Rico municipal securities held by the Fund were insured and all bonds continue to pay full principal and interest.

|

See Portfolio of Investments beginning on page10 for specific holdings within these categories. The Fund's holdings are subject to change.

| |

MainStay MacKay DefinedTerm Municipal Opportunities Fund

|

Top Ten Holdings and/or Issuers

Held as of May 31, 2023 (excluding short-term investments)# (Unaudited)

| |

Chicago O'Hare International Airport, 5.25%-5.75%, due 1/1/38–1/1/45 (a) |

| |

State of Illinois, 5.25%-5.50%, due 5/1/30–5/1/39

|

| |

Los Angeles Department of Water & Power, 5.00%, due 7/1/42

|

| |

Metropolitan Transportation Authority, 5.00%-5.25%, due 11/15/45–11/15/56 |

| |

Pennsylvania Economic Development Financing Authority, 5.75%-6.00%, due 7/1/53–12/31/62 (a) |

| |

Orange County Convention Center, 4.00%, due 10/1/33

|

| |

City of Chicago, 5.00%-6.00%, due 1/1/27–1/1/49

|

| |

Puerto Rico Sales Tax Financing Corp., 4.55%-5.00%, due 7/1/40–7/1/58 |

| |

City of Salt Lake, 5.00%, due 7/1/47 |

| |

County of Broward, 4.00%-5.50%, due

9/1/51–1/1/55 (a)

|

| |

Some of these holdings have been transferred to a Tender Option Bond (“TOB”) Issuer in exchange for TOB Residuals and cash. |

| |

Municipal security may feature credit enhancements, such as bond insurance. |

Credit Quality as of May 31, 2023^ (Unaudited)

^ As a percentage of total investments.

Ratings apply to the underlying portfolio of bonds held by the Fund and are rated by an independent rating

agency, such as Standard & Poor’s (“S&P”), Moody’s Investors Service, Inc. and/or Fitch Ratings, Inc. If the ratings provided by the ratings

agencies differ, the higher rating will be utilized. If only one rating is provided, the available rating will be utilized. Securities that are unrated by the rating agencies

are reflected as such in the breakdown. Unrated securities do not necessarily indicate low quality. S&P rates borrowers on a scale from AAA to D. AAA through BBB-

represent investment grade, while BB+ through D represent non-investment grade.

Portfolio

Management Discussion and Analysis (Unaudited)

Questions answered by

portfolio managers John Loffredo, CFA, Robert DiMella, CFA, Michael Petty, David Dowden, Scott Sprauer, John Lawlor and Michael Denlinger, CFA, of MacKay

Shields LLC, the Fund’s Subadvisor.

How did MainStay MacKay DefinedTerm Municipal

Opportunities Fund perform relative to its benchmark and peer

group during the 12 months ended May 31, 2023?

For the 12 months ended May 31, 2023, MainStay MacKay

DefinedTerm Municipal Opportunities Fund returned −1.49% based on net asset value applicable to

Common shares and −4.16% based on market price. At net asset value and at market price, the Fund

underperformed the 0.49% return of its benchmark, the Bloomberg Municipal Bond Index (the “Index”). At net asset value the Fund outperformed, and at market price the Fund underperformed, the −3.15% return of the

Morningstar Muni National Long Category Average.1

What factors affected the Fund’s relative performance during the reporting period?

During the first half of the reporting period, both municipal rates and U.S. Treasury rates rose, with the municipal

yield curve2 steepening as outflows persisted. As a result, ratios cheapened across the curve, most notably on the long-end. The

Fund’s overweight exposure to this segment of the market compared to the Index was a driver of

relative underperformance. Across the credit spectrum, underweight exposure to AAA/AA-rated3 credits

detracted from relative performance, while security selection among the non-rated credits helped to offset

some of the losses. From a geographic perspective, an overweight allocation to Florida bonds detracted from

relative performance, whereas security selection among Illinois bonds made positive contributions to

relative returns. (Contributions take weightings and total returns into account.) Finally, the Fund’s

overweight exposure to bonds with coupons of 6% detracted on a relative basis.

How was the Fund’s leverage strategy implemented during the reporting

period?

During the reporting period, we reduced the Fund’s leverage modestly to 36.7% of the Fund’s managed assets. The Fund continued to exit positions in names that no longer

represented spread-tightening4 opportunities. The Fund also continued to execute tax loss swaps and reinvest in higher-yielding bonds and structures with potential spread-tightening characteristics.

What was the Fund’s duration5 strategy during the reporting period?

We do

not make interest rate forecasts or duration bets. Rather, we aim to take a duration-neutral posture in the Fund relative to the Index. As of the end of the reporting period, the Fund's modified duration to worst6 was 5.89 years compared to 6.02 years for the Index.

During the reporting period, which sectors were the strongest positive contributors to the Fund’s relative performance and

which sectors were particularly weak?

During the reporting period, the Fund’s security selection

among electric holdings contributed positively to relative performance, as did underweight exposure to the

leasing sector. Conversely, underweight exposure to, and security selection in, the transportation and

hospital sectors detracted most significantly.

How did the Fund’s market

segments change during the reporting period?

During the reporting period, there were no material changes to the weightings in the Fund. At the margin, we increased

the Fund’s exposure to the electric and state general obligation sectors during the reporting period.

In the coming year, we anticipate greater demand for traditional municipal bonds—including bonds

backed by the taxing power of general obligation issuers or secured by the revenues of essential service

providers. In addition, we increased the Fund’s credit exposure to AAA-rated bonds, given their

relatively strong financial condition and the fact that they were available at much higher yields.

Furthermore, we increased the Fund’s state exposure to Illinois. Conversely, we decreased the

Fund’s exposure to the hospital and prerefunded/ETM (escrowed to maturity) sectors, as well as credit

exposure to non-investment-grade bonds and state exposure to Michigan.

How was the Fund positioned at the end of the reporting period?

As of May 31,

2023, the Fund remained overweight to the long end of the curve, where municipal yields were more attractive. In addition, the Fund held overweight exposure to the special tax and

1.

See "Fund Performance and Statistics" for more information on Fund returns.

2.

The yield curve is a line that plots the yields of various securities of similar

quality—typically U.S. Treasury issues—across a range of maturities. The U.S. Treasury yield curve serves as a benchmark for other debt and is used in economic

forecasting.

3.

An obligation

rated ‘AAA’ has the highest rating assigned by Standard & Poor’s (“S&P”), and in the opinion of S&P, the obligor’s capacity to meet its financial commitment on the obligation is extremely strong. An obligation rated ‘AA’ by S&P is deemed by S&P to differ from the highest-rated obligations only to a small degree.

In the opinion of S&P, the obligor's capacity to meet its financial commitment on the obligation is very strong. When applied to Fund holdings, ratings are based solely on

the creditworthiness of the bonds in the portfolio and are not meant to represent the security or safety of the Fund.

4.

The terms

“spread” and “yield spread” may refer to the difference in yield between a security or type of security and comparable U.S. Treasury issues. The terms may

also refer to the difference in yield between two specific securities or types of securities at a given time.

5.

Duration is a measure of the price sensitivity of a fixed-income investment to changes in

interest rates. Duration is expressed as a number of years and is considered a more accurate sensitivity gauge than average maturity.

6.

Modified duration

is inversely related to the approximate percentage change in price for a given change in yield. Duration to worst is the duration of a bond computed using the bond’s

nearest call date or maturity, whichever comes first. This measure ignores future cash flow fluctuations due to embedded optionality.

| |

MainStay MacKay DefinedTerm Municipal Opportunities Fund

|

electric sectors. Across states and

territories, the Fund held overweight exposure to bonds from Illinois and Puerto Rico. From a credit

perspective, the Fund held overweight exposure to non-rated bonds not held in the Index. As of the same date, the Fund held underweight exposure to the state general obligation, local general obligation and hospital sectors, as well

as AAA-rated credits and holdings from the state of California.

The opinions expressed are those of the portfolio managers as of the date of this report and are subject to change. There is no guarantee that any forecasts will come to pass. This material does not constitute investment advice and is not intended as an endorsement of any specific investment.

Portfolio

of Investments May 31, 2023†

| |

|

|

| |

Arizona 0.3%

(0.2% of Managed Assets) |

Industrial Development Authority of the City of Phoenix (The), Espiritu Community Development Corp., Revenue Bonds |

|

|

| |

|

|

| |

|

|

California 15.7%

(10.0% of Managed Assets) |

Calexico Unified School District, Election of 2020, Unlimited General Obligation |

|

|

| |

|

|

| |

|

|

California Municipal Finance Authority, LAX Integrated Express Solutions LLC, Revenue Bonds, Senior Lien |

|

|

| |

|

|

| |

|

|

California Municipal Finance Authority, United Airlines, Inc. Project, Revenue Bonds |

|

|

| |

|

|

Los Angeles Department of Water & Power, Power System, Revenue Bonds |

|

|

| |

|

|

| |

|

|

Regents of the University of California Medical Center Pooled, Revenue Bonds |

|

|

| |

|

|

| |

|

|

Sacramento City Unified School District, Election of 2020, Unlimited General Obligation |

|

|

| |

|

|

| |

|

|

San Diego County Regional Airport Authority, Revenue Bonds (a) |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

San Francisco City & County Airport Commission, International Airport, Revenue Bonds |

|

|

| |

|

|

| |

|

|

| |

|

|

Colorado 1.7%

(1.1% of Managed Assets) |

City & County of Denver, Airport System, Revenue Bonds |

|

|

| |

|

|

| |

|

|

Copper Ridge Metropolitan District, Revenue Bonds |

|

|

| |

|

|

Sterling Ranch Community Authority Board, Metropolitan District No. 2, Revenue

Bonds |

|

|

| |

|

|

| |

|

|

| |

|

|

District of Columbia 0.6%

(0.4% of Managed Assets) |

Metropolitan Washington Airports Authority, Dulles Toll Road, Revenue Bonds, Second Lien |

|

|

| |

|

|

| |

|

|

Florida 16.8%

(10.8% of Managed Assets) |

City of Miami Beach, Unlimited General Obligation |

|

|

| |

|

|

| |

|

|

County of Broward, Convention Center Expansion Project, Revenue Bonds |

|

|

| |

|

|

| |

|

|

| |

|

|

County of Broward, Convention Center Hotel, Revenue Bonds, First Tier |

|

|

| |

|

|

County of Miami-Dade, Transit System, Revenue Bonds |

|

|

| |

|

|

| |

|

|

The notes to the financial statements are an integral part of, and should be read

in conjunction with, the financial statements.

| |

MainStay MacKay DefinedTerm Municipal Opportunities Fund

|

| |

|

|

|

|

JEA Electric System, Revenue Bonds |

|

|

| |

|

|

| |

|

|

Orange County Convention Center, Revenue Bonds |

|

|

| |

|

|

| |

|

|

| |

|

|

Georgia 0.5%

(0.3% of Managed Assets) |

Municipal Electric Authority of Georgia, Plant Vogtle Units 3&4 Project, Revenue Bonds |

|

|

| |

|

|

| |

|

|

Guam 2.2%

(1.4% of Managed Assets) |

Antonio B Won Pat International Airport Authority, Revenue Bonds |

|

|

| |

|

|

| |

|

|

Guam Government Waterworks Authority, Water and Wastewater System, Revenue Bonds |

|

|

| |

|

|

| |

|

|

Illinois 29.7%

(19.0% of Managed Assets) |

Chicago Board of Education, Unlimited General Obligation |

|

|

| |

|

|

| |

|

|

Chicago Board of Education, Dedicated Capital Improvement, Revenue Bonds |

|

|

| |

|

|

Chicago Board of Education, Dedicated Capital Improvement, Unlimited General Obligation (d) |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

Chicago O'Hare International Airport, Revenue Bonds, Senior lien |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

Chicago O'Hare International Airport, Customer Facility Charge, Revenue Bonds, Senior Lien |

|

|

| |

|

|

| |

|

|

City of Chicago, Unlimited General Obligation |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

City of Chicago, Wastewater Transmission, Revenue Bonds, Second Lien |

|

|

| |

|

|

| |

|

|

Metropolitan Pier & Exposition Authority, McCormick Place Expansion Project, Revenue Bonds |

|

|

| |

|

|

| |

|

|

| |

|

|

(zero coupon), due 6/15/43 |

|

|

Sales Tax Securitization Corp., Revenue Bonds |

|

|

| |

|

|

| |

|

|

State of Illinois, Unlimited General Obligation |

|

|

| |

|

|

| |

|

|

| |

|

|

Will County School District No. 114

Manhattan, Unlimited General

Obligation |

|

|

| |

|

|

| |

|

|

| |

|

|

Massachusetts 4.3%

(2.8% of Managed Assets) |

Commonwealth of Massachusetts, Unlimited General Obligation |

|

|

| |

|

|

| |

|

|

The notes to the financial statements are an integral part of, and should be read

in conjunction with, the financial statements.

Portfolio

of Investments May 31, 2023†

(continued)

| |

|

|

Massachusetts (continued)

|

Massachusetts Development Finance Agency, North Eastern University Issue, Revenue Bonds |

|

|

| |

|

|

| |

|

|

Massachusetts School Building Authority, Revenue Bonds |

|

|

| |

|

|

| |

|

|

| |

|

|

Michigan 2.2%

(1.4% of Managed Assets) |

Great Lakes Water Authority Sewage Disposal System, Revenue Bonds, Senior Lien |

|

|

Series B, Insured: AGM-CR |

|

|

| |

|

|

Nebraska 0.5%

(0.3% of Managed Assets) |

Omaha Public Power District, Electric System, Revenue Bonds |

|

|

| |

|

|

| |

|

|

Nevada 5.1%

(3.3% of Managed Assets) |

County of Clark, Regional Transportation Commission of Southern Nevada Motor Fuel Tax, Revenue Bonds |

|

|

| |

|

|

Las Vegas Convention & Visitors Authority, Convention Center Expansion, Revenue Bonds |

|

|

| |

|

|

| |

|

|

| |

|

|

New Hampshire 1.0%

(0.6% of Managed Assets) |

Manchester Housing and Redevelopment Authority, Inc., Meals & Rooms Tax, Revenue Bonds |

|

|

| |

|

|

(zero coupon), due 1/1/24 |

|

|

New Jersey 4.7%

(3.0% of Managed Assets) |

New Jersey Economic Development Authority, Continental Airlines, Inc. Project, Revenue Bonds |

|

|

| |

|

|

| |

|

|

| |

New Jersey Economic Development Authority, New Jersey Transit Transportation Project, Revenue Bonds |

|

|

| |

|

|

| |

|

|

New Jersey Transportation Trust Fund Authority, Transportation Program, Revenue Bonds |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

State of New Jersey, COVID-19 General Obligation Emergency Bonds, Unlimited General Obligation |

|

|

| |

|

|

| |

|

|

Tobacco Settlement Financing Corp., Revenue Bonds |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

New York 21.0%

(13.4% of Managed Assets) |

Metropolitan Transportation Authority, Revenue Bonds |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

New York City Transitional Finance Authority, Future Tax Secured, Revenue Bonds |

|

|

| |

|

|

| |

|

|

New York State Dormitory Authority, State Personal Income Tax, Revenue Bonds |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

The notes to the financial statements are an integral part of, and should be read

in conjunction with, the financial statements.

| |

MainStay MacKay DefinedTerm Municipal Opportunities Fund

|

| |

|

|

|

|

New York State Housing Finance Agency, Revenue Bonds |

|

|

| |

|

|

| |

|

|

New York Transportation Development Corp., LaGuardia Airport Terminal B Redevelopment Project, Revenue Bonds |

|

|

| |

|

|

| |

|

|

Onondaga County Trust for Cultural Resources, Syracuse University Project, Revenue Bonds |

|

|

| |

|

|

Port Authority of New York & New Jersey, Revenue Bonds |

|

|

| |

|

|

Riverhead Industrial Development Agency, Riverhead Charter School, Revenue Bonds |

|

|

| |

|

|

| |

|

|

Triborough Bridge & Tunnel Authority, Payroll Mobility Tax, Revenue Bonds, Senior Lien |

|

|

| |

|

|

| |

|

|

Triborough Bridge & Tunnel Authority, Sales Tax, Revenue Bonds |

|

|

| |

|

|

| |

|

|

| |

|

|

North Carolina 0.6%

(0.4% of Managed Assets) |

Charlotte-Mecklenburg Hospital Authority (The), Atrium Health Obligated Group, Revenue Bonds |

|

|

| |

|

|

| |

|

|

Pennsylvania 9.6%

(6.2% of Managed Assets) |

Allentown Neighborhood Improvement Zone Development Authority, City Center Project, Revenue Bonds |

|

|

| |

|

|

| |

|

|

| |

Commonwealth Financing Authority, Tobacco Master Settlement Payment, Revenue Bonds |

|

|

| |

|

|

| |

|

|

Pennsylvania Economic Development Financing Authority, Capital Region Parking System, Revenue Bonds |

|

|

Series B, Insured: County Guaranteed |

|

|

| |

|

|

Pennsylvania Economic Development Financing Authority, The Penndot Major Bridges Package One Project, Revenue Bonds |

|

|

| |

|

|

5.75%, due 12/31/62 (a)(b) |

|

|

Pennsylvania Turnpike Commission, Revenue Bonds |

|

|

| |

|

|

| |

|

|

Southeastern Pennsylvania Transportation Authority, Asset Improvement Program, Revenue Bonds |

|

|

| |

|

|

| |

|

|

Puerto Rico 11.7%

(7.5% of Managed Assets) |

Children's Trust Fund, Asset-Backed, Revenue Bonds |

|

|

| |

|

|

Commonwealth of Puerto Rico, Restructured, Unlimited General Obligation |

|

|

| |

|

|

| |

|

|

Puerto Rico Commonwealth Aqueduct & Sewer Authority, Revenue Bonds, Senior Lien |

|

|

| |

|

|

| |

|

|

Puerto Rico Electric Power Authority, Revenue Bonds (f) |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

The notes to the financial statements are an integral part of, and should be read

in conjunction with, the financial statements.

Portfolio

of Investments May 31, 2023†

(continued)

| |

|

|

|

|

Puerto Rico Electric Power Authority, Revenue Bonds (f) (continued) |

|

|

Series PP, Insured: NATL-RE |

|

|

| |

|

|

Series PP, Insured: NATL-RE |

|

|

| |

|

|

Series TT, Insured: AGM-CR |

|

|

| |

|

|

Puerto Rico Municipal Finance Agency, Revenue Bonds |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

Puerto Rico Sales Tax Financing Corp., Revenue Bonds |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

South Carolina 3.0%

(1.9% of Managed Assets) |

South Carolina Public Service Authority, Santee Cooper, Revenue Bonds |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

Texas 6.2%

(4.0% of Managed Assets) |

City of Georgetown, Utility System, Revenue Bonds |

|

|

| |

|

|

| |

|

|

City of Lubbock, Electric Light & Power System, Revenue Bonds |

|

|

| |

|

|

| |

|

|

Harris County-Houston Sports Authority, Revenue Bonds, Senior Lien |

|

|

Series A, Insured: AGM, NATL-RE |

|

|

(zero coupon), due 11/15/38 |

|

|

Harris County-Houston Sports Authority, Revenue Bonds, Junior Lien |

|

|

Series H, Insured: NATL-RE |

|

|

(zero coupon), due 11/15/28 |

|

|

| |

|

|

| |

Harris County-Houston Sports Authority, Revenue Bonds, Junior Lien (continued) |

|

|

Series H, Insured: NATL-RE |

|

|

(zero coupon), due 11/15/38 |

|

|

San Antonio Water System, Water System, Revenue Bonds, Junior Lien |

|

|

| |

|

|

| |

|

|

Texas Water Development Board, State Water Implementation, Revenue Bonds |

|

|

| |

|

|

| |

|

|

| |

|

|

U.S. Virgin Islands 3.4%

(2.2% of Managed Assets) |

Matching Fund Special Purpose Securitization Corp., United States Virgin Islands Federal Excise Tax, Revenue Bonds |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

Virgin Islands Public Finance Authority, Gross Receipts Taxes Loan, Revenue Bonds |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

Series A, Insured: AGM-CR |

|

|

| |

|

|

| |

|

|

Utah 7.5%

(4.8% of Managed Assets) |

City of Salt Lake, International Airport, Revenue Bonds |

|

|

| |

|

|

| |

|

|

Intermountain Power Agency, Revenue Bonds |

|

|

| |

|

|

| |

|

|

| |

|

|

The notes to the financial

statements are an integral part of, and should be read in conjunction with, the financial statements.

| |

MainStay MacKay DefinedTerm Municipal Opportunities Fund

|

| |

|

|

Virginia 1.0%

(0.6% of Managed Assets) |

Tobacco Settlement Financing Corp., Asset-Backed, Revenue Bonds, Senior Lien |

|

|

| |

|

|

| |

|

|

Washington 1.5%

(1.0% of Managed Assets) |

State of Washington, Various Purpose, Unlimited General Obligation |

|

|

| |

|

|

| |

|

|

Washington State Housing Finance Commission, Single Family Program, Revenue Bonds |

|

|

| |

|

|

| |

|

|

| |

|

|

Wisconsin 1.3%

(0.8% of Managed Assets) |

Public Finance Authority, Bancroft NeuroHealth Project, Revenue Bonds |

|

|

| |

|

|

| |

|

|

Public Finance Authority, Ultimate Medical Academy Project, Revenue Bonds |

|

|

| |

|

|

| |

|

|

| |

|

|

Total Investments

(Cost $710,692,670) |

|

|

Floating Rate Note Obligations (g) |

|

|

Other Assets, Less Liabilities |

|

|

Net Assets Applicable to Common

Shares |

|

|

| |

Percentages indicated are based on Fund net assets applicable to Common shares. |

| |

Interest on these securities was subject to alternative minimum tax. |

| |

All or portion of principal amount transferred to a Tender Option Bond (“TOB”) Issuer in exchange for TOB Residuals and cash. |

| |

Step coupon—Rate shown was the rate in effect as of May 31, 2023. |

| |

May be sold to institutional investors only under Rule 144A or securities offered pursuant to Section 4(a)(2) of the Securities Act of 1933, as amended. |

| |

Variable-rate demand notes (VRDNs)—Provide the right to sell the security at face value on either that day or within the rate-reset period. VRDNs will normally trade as if the maturity is the earlier put date, even though stated maturity is longer. The interest rate is reset on the put date at a stipulated daily, weekly, monthly, quarterly, or other specified time interval to reflect current market conditions. These securities do not indicate a reference rate and spread in their description. The maturity date shown is the final maturity. |

| |

Bond insurance is paying principal and interest, since the issuer is in default. |

| |

Face value of Floating Rate Notes issued in TOB transactions. |

"Managed Assets" is defined as the Fund’s total assets,

minus the sum of its accrued liabilities (other than Fund liabilities incurred for the purpose of creating

effective leverage (i.e. tender option bonds) or Fund liabilities related to liquidation preference of any

preferred shares issued), which was $739,491,367 as of May 31, 2023.

| |

AGC—Assured Guaranty Corp. |

AGM—Assured Guaranty Municipal Corp. |

BAM—Build America Mutual Assurance Co. |

| |

NATL-RE—National Public Finance Guarantee Corp. |

The notes to

the financial statements are an integral part of, and should be read in conjunction with, the financial statements.

Portfolio

of Investments May 31, 2023†

(continued)

The following is a summary of the fair valuations according to the inputs used as of May 31, 2023, for valuing the Fund’s

assets:

| |

Quoted

Prices in

Active

Markets for

Identical

Assets

(Level 1) |

Significant

Other

Observable

Inputs

(Level 2) |

Significant

Unobservable

Inputs

(Level 3) |

|

| |

|

|

|

|

Investments in Securities (a) |

|

|

|

|

| |

|

|

|

|

| |

For a complete listing of investments and their industries, see the Portfolio of Investments. |

The notes to the financial statements are an integral part of, and should be read

in conjunction with, the financial statements.

| |

MainStay MacKay DefinedTerm Municipal Opportunities Fund

|

Statement

of Assets and Liabilities as of May 31, 2023

| |

Investment in securities, at value

(identified cost $710,692,670) |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

Payable for Floating Rate Note Obligations |

|

| |

|

| |

|

| |

|

Shareholder communication |

|

| |

|

| |

|

| |

|

| |

|

Interest expense and fees payable |

|

| |

|

Net assets applicable to Common shares |

|

Common shares outstanding |

|

Net asset value per Common share (Net assets applicable to Common shares divided by Common shares outstanding) |

|

Net Assets Applicable to Common Shares Consist of |

Common shares, $0.001 par value per share, unlimited number of shares authorized |

|

Additional paid-in-capital |

|

| |

|

Total distributable earnings (loss) |

|

Net assets applicable to Common shares |

|

The notes to the financial statements are an integral part of, and should be read

in conjunction with, the financial statements.

Statement

of Operations for the year ended May 31, 2023

| |

| |

|

| |

|

| |

|

| |

|

Interest expense and fees |

|

| |

|

Shareholder communication |

|

| |

|

| |

|

| |

|

| |

|

Total expenses before waiver/reimbursement |

|

Reimbursement from prior custodian(a)

|

|

| |

|

Net investment income (loss) |

|

Realized and Unrealized Gain (Loss) |

Net realized gain (loss) on investments |

|

Net change in unrealized appreciation (depreciation)

on investments |

|

Net realized and unrealized gain (loss) |

|

Net increase (decrease) in net assets to Common shares

resulting from operations |

|

| |

Represents a refund for overbilling of custody fees. |

The notes to the financial statements are an integral part of, and should be read

in conjunction with, the financial statements.

| |

MainStay MacKay DefinedTerm Municipal Opportunities Fund

|

Statements of Changes in Net Assets

for the years ended May 31, 2023 and May 31, 2022

| |

|

|

Increase (Decrease) in Net Assets Applicable to

Common Shares |

| |

|

|

Net investment income (loss) |

|

|

| |

|

|

Net change in unrealized appreciation (depreciation) |

|

|

Net increase (decrease) in net assets applicable to Common shares resulting from operations |

|

|

Distributions to Common shareholders |

|

|

Capital share transactions

(Common shares): |

|

|

Net proceeds issued to shareholders resulting from reinvestment of dividends |

|

|

Net increase (decrease) in net assets applicable to Common shares |

|

|

Net Assets Applicable to Common Shares |

| |

|

|

| |

|

|

The notes to the financial

statements are an integral part of, and should be read in conjunction with, the financial statements.

Statement of Cash Flows

for

the year ended May 31, 2023

Cash Flows From (Used in) Operating Activities: |

Net decrease in net assets resulting from operations |

|

Adjustments to reconcile net decrease in net assets resulting from operations to net cash used in operating activities: |

|

| |

|

| |

|

Amortization (accretion) of discount and premium, net |

|

Decrease in interest receivable |

|

| |

|

Decrease in due to custodian |

|

Decrease in professional fees payable |

|

Decrease in custodian payable |

|

Decrease in shareholder communication payable |

|

Increase in due to Trustees |

|

Decrease in due to manager |

|

Increase in due to transfer agent |

|

Decrease in accrued expenses |

|

Increase in interest expense and fees payable |

|

Net realized loss from investments |

|

Net change in unrealized (appreciation) depreciation on unaffiliated investments |

|

Net cash from operating activities |

|

Cash Flows From (Used in) Financing Activities: |

Net proceeds resulting from reinvestment of dividends |

|

Proceeds from floating rate note obligations |

|

Payments on floating rate note obligations |

|

Cash distributions paid, net of change in Common share dividend payable |

|

Net cash used in financing activities |

|

| |

|

Cash at beginning of year |

|

| |

|

The notes to the financial statements are an integral part of, and should be read

in conjunction with, the financial statements.

| |

MainStay MacKay DefinedTerm Municipal Opportunities Fund

|

Financial

Highlights selected per share data and ratios

| |

|

| |

|

|

|

|

|

Net asset value at beginning of year applicable to Common shares |

|

|

|

|

|

Net investment income (loss) |

|

|

|

|

|

Net realized and unrealized gain (loss) |

|

|

|

|

|

Total from investment operations |

|

|

|

|

|

Dividends and distributions to Common shareholders |

|

|

|

|

|

Net asset value at end of year applicable to Common shares |

|

|

|

|

|

Market price at end of year applicable to Common shares |

|

|

|

|

|

Total investment return on market price (a) |

|

|

|

|

|

Total investment return on net asset value (a) |

|

|

|

|

|

Ratios (to average net assets of Common shareholders)/

Supplemental Data: |

|

|

|

|

|

Net investment income (loss) |

|

|

|

|

|

Net expenses (including interest expense and fees) |

|

|

|

|

|

Interest expense and fees (b) |

|

|

|

|

|

| |

|

|

|

|

|

Net assets applicable to Common shareholders at end of year (in 000’s) |

|

|

|

|

|

Preferred shares outstanding at $100,000 liquidation preference,

end of year (in 000’s) (d)(e) |

|

|

|

|

|

Assets coverage per Preferred share, end of year (d)(e) |

|

|

|

|

|

Average market value per Preferred share: |

|

|

|

|

|

| |

|

|

|

|

|

| |

|

|

|

|

|

| |

Total investment return on market price is calculated assuming a purchase of a Common share at the market price on the first day and a sale on the last day business day of each

month. Dividends and distributions are assumed to be reinvested at prices obtained under

the Fund’s dividend reinvestment plan. Total investment return on net asset value reflects the changes in net asset value during each period and assumes the reinvestment of dividends and distributions at net asset value on the last business day of each month. This percentage may be

different from the total investment return on market price, due to differences between the

market price and the net asset value. For periods less than one year, total investment return is not annualized. |

| |

Interest expense and fees relate to the costs of tender option bond transactions (See Note 2(G)) and the issuance of fixed rate municipal term preferred shares, where

applicable, for the years ended May 31, 2023, 2022, 2021, 2020 and 2019,

respectively. |

| |

The portfolio turnover rate includes variable rate demand notes. |

| |

Redeemed on June 15, 2020. |

| |

Redeemed on December 15, 2020. |

| |

Calculated by subtracting the Fund’s total liabilities (not including the Preferred shares) from the Fund’s total assets, and dividing the result by the number of

Preferred shares outstanding. |

The notes to the financial

statements are an integral part of, and should be read in conjunction with, the financial statements.

Notes to

Financial Statements

Note 1-Organization and Business

MainStay MacKay DefinedTerm Municipal Opportunities Fund (the “Fund”) was organized as a Delaware statutory trust on April 20, 2011, pursuant to an agreement and declaration of trust, which

was most recently amended and restated on June 10, 2022 (“Declaration of Trust’’). The

Fund is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as a

“diversified”, closed-end management investment company, as those terms are defined in the 1940 Act, as interpreted or modified by regulatory authorities having jurisdiction, from time to time. The Fund first offered Common

shares through an initial public offering on June 26, 2012.

Pursuant to the terms of the Declaration of Trust, the Fund will commence the process of liquidation and dissolution at

the close of business on December 31, 2024 (the “Termination Date”) unless otherwise extended

by a majority of the Board of Trustees (the “Board”) (as discussed in further detail below).

During the six-month period preceding the Termination Date or Extended Termination Date (as defined below), the Board may, without shareholder approval unless such approval is required by the 1940 Act, determine to (i) merge or

consolidate the Fund so long as the surviving or resulting entity is an open-end registered investment

company that is managed by the same investment adviser which serves as the investment adviser to the Fund

at that time or is an affiliate of such investment adviser; or (ii) convert the Fund from a closed-end fund into an open-end registered investment company. Upon liquidation and termination of the Fund, shareholders will receive an

amount equal to the Fund’s net asset value (“NAV”) at that time, which may be greater or less than the price at which Common shares were issued. The Fund’s investment objectives and policies are not designed

to return to investors who purchased Common shares in the initial offering of such shares their initial

investment on the Termination Date and such initial investors may receive more or less than their original investment upon termination.

Prior to the commencement of the six-month period preceding the Termination Date, a majority of the Board may extend the Termination Date for a period of not more than two years or

such shorter time as may be determined (the “Extended Termination Date”), upon a determination

that taking such actions as described in (i) or (ii) above would not, given prevailing market conditions,

be in the best interests of the Fund’s shareholders. The Termination Date may be extended one or more times by the Board prior to the first business day of the sixth month before the next occurring Extended Termination

Date.

Pursuant to the June 10, 2022 amendment, if the Fund completes an Eligible Tender Offer (as defined below), a majority of the Board may, without shareholder approval unless such approval

is required by the 1940 Act, eliminate the Termination Date and cause the Fund to have a perpetual

existence as a closed-end fund. An “Eligible Tender Offer” is defined as a tender offer by the Fund to purchase 100% of the then outstanding Common shares of the Fund at a price equal to the NAV per Common share calculated in accordance with the

Fund’s valuation procedures as of the date specified in the tender offer, with the expiration

date of the tender offer being as of a date within twelve months

preceding the Termination Date.

If

the payment for properly tendered Common shares would result in the Fund’s net assets totaling less than $200 million (the “Termination Threshold”), the Eligible Tender Offer shall be canceled, no Common shares will be repurchased pursuant to the

Eligible Tender Offer, and the Fund would dissolve as set forth above. If an Eligible Tender Offer is

conducted and the payment for properly tendered Common shares would result in the Fund’s net assets

totaling greater than or equal to the Termination Threshold, all Common shares properly tendered and not

withdrawn will be purchased by the Fund pursuant to the terms of the Eligible Tender Offer. The Fund may

conduct an Eligible Tender Offer upon the affirmative vote of a majority of the Board - or by an instrument

signed by a majority of the Board - without a vote of the shareholders.

The Fund's primary investment objective is to seek current income exempt from regular U.S. Federal income taxes (but

which may be includable in taxable income for the purpose of the Federal alternative minimum tax). Total

return is a secondary objective.

Note 2–Significant Accounting Policies

The Fund is an investment company and accordingly follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board (“FASB”)

Accounting Standards Codification Topic 946 Financial Services—Investment

Companies.The Fund prepares its financial statements in accordance with generally accepted accounting principles (“GAAP”) in the United States of America and follows the significant accounting

policies described below.

(A) Securities Valuation. Investments are usually valued as of the close of regular trading on the New York Stock Exchange (the "Exchange") (usually 4:00 p.m. Eastern time) on each day

the Fund is open for business ("valuation date").

Pursuant to Rule 2a-5 under the 1940 Act, the Board has designated New York Life Investment Management LLC (“New

York Life Investments” or the "Manager")as its Valuation Designee (the "Valuation Designee"). The

Valuation Designee is responsible for performing fair valuations relating to all investments in the Fund’s portfolio for which market quotations are not readily available; periodically assessing and managing material valuation risks; establishing and

applying fair value methodologies; testing fair valuation methodologies; evaluating and overseeing pricing

services; ensuring appropriate segregation of valuation and portfolio management functions; providing quarterly, annual and prompt reporting to the Board, as appropriate; identifying potential conflicts of interest; and maintaining appropriate

records. The Valuation Designee has established a valuation committee ("Valuation Committee") to assist in

carrying out the Valuation Designee’s responsibilities and establish prices of securities for which market quotations are not readily available. The Fund’s and the Valuation Designee's policies and procedures ("Valuation Procedures") govern the

Valuation Designee’s selection and application of methodologies for determining and

| |

MainStay MacKay DefinedTerm Municipal Opportunities Fund

|

calculating the fair value of Fund investments.

The Valuation Designee may value the Fund's portfolio securities for which market quotations are not

readily available and other Fund assets utilizing inputs from pricing services and other third-party sources. The Valuation Committee meets (in person, via electronic mail or via teleconference) on an ad-hoc basis to determine fair valuations and on a

quarterly basis to review fair value events with respect to certain securities for which market quotations are not readily available, including valuation risks and back-testing results, and to preview reports to the

Board.

The Valuation Committee establishes prices of securities for which market quotations are not readily available based on such methodologies and measurements on a regular basis after considering

information that is reasonably available and deemed relevant by the Valuation Committee. The Board shall

oversee the Valuation Designee and review fair valuation materials on a prompt, quarterly and annual basis and approve proposed revisions to the Valuation Procedures.

Investments for which market quotations are not readily available are valued at fair value as determined in good faith pursuant to the Valuation Procedures. A market quotation is readily

available only when that quotation is a quoted price (unadjusted) in active markets for identical

investments that the Fund can access at the measurement date, provided that a quotation will not be readily

available if it is not reliable. "Fair value" is defined as the price the Fund would reasonably expect to receive upon selling an asset or liability in an orderly transaction to an independent buyer in the principal or most advantageous

market for the asset or liability. Fair value measurements are determined within a framework that

establishes a three-tier hierarchy that maximizes the use of observable market data and minimizes the use

of unobservable inputs to establish a classification of fair value measurements for disclosure purposes.

"Inputs" refer broadly to the assumptions that market participants would use in pricing the asset or

liability, including assumptions about risk, such as the risk inherent in a particular valuation technique used to measure fair value using a pricing model and/or the risk inherent in the inputs for the valuation technique. Inputs may be

observable or unobservable. Observable inputs reflect the assumptions market participants would use in

pricing the asset or liability based on market data obtained from sources independent of the Fund. Unobservable inputs reflect the Fund’s own assumptions about the assumptions market participants would use in pricing the asset or liability based on the

information available. The inputs or methodology used for valuing assets or liabilities may not be an

indication of the risks associated with investing in those assets or liabilities. The three-tier hierarchy

of inputs is summarized below.

• Level

1—quoted prices (unadjusted) in active markets for an identical asset or liability

• Level 2—other significant observable inputs (including quoted prices for a similar asset or liability in active markets, interest rates and yield curves, prepayment speeds, credit risk,

etc.)

• Level 3—significant unobservable inputs (including the Fund's own assumptions about the assumptions that market participants would use in measuring fair value of an asset or

liability)

The level of an asset or liability within the fair value hierarchy is based on the lowest level of an input, both individually and in the aggregate, that is significant to the fair value measurement.

The aggregate value by input level of the Fund’s assets and liabilities as of May 31, 2023, is included

at the end of the Portfolio of Investments.

The Fund may use third-party vendor evaluations, whose prices may be derived from one or more of the following standard

inputs, among others:

| |

|

| |

|

| |

|

| |

• Reference data (corporate actions or

material event notices) |

• Industry and economic events |

|

• Monthly payment information |

|

An asset or liability for which a market quotation is not readily available is valued by methods deemed reasonable in good faith by the Valuation Committee, following the Valuation Procedures to

represent fair value. Under these procedures, the Valuation Designee generally uses a market-based approach

which may use related or comparable assets or liabilities, recent transactions, market multiples, book values and other relevant information. The Valuation Designee may also use an income-based valuation approach in which the anticipated

future cash flows of the asset or liability are discounted to calculate fair value. Discounts may also be

applied due to the nature and/or duration of any restrictions on the disposition of the asset or liability. Fair value represents a good faith approximation of the value of a security. Fair value determinations involve the consideration of a number

of subjective factors, an analysis of applicable facts and circumstances and the exercise of judgment. As a

result, it is possible that the fair value for a security determined in good faith in accordance with the Valuation Procedures may differ from valuations for the same security determined for other funds using their own valuation

procedures. Although the Valuation Procedures are designed to value a security at the price the Fund may

reasonably expect to receive upon the security's sale in an orderly transaction, there can be no assurance that any fair value determination thereunder would, in fact, approximate the amount that the Fund would actually realize upon the sale of

the security or the price at which the security would trade if a reliable market price were readily

available. During the year ended May 31, 2023, there were no material changes to the fair value

methodologies.

Securities which may be valued in this manner include, but are not limited to: (i) a security for which trading has been halted or suspended or otherwise does not have a readily available market

quotation on a given day; (ii) a debt security that has recently gone into default and for which there is

not a current market quotation; (iii) a security of an issuer that has entered into a restructuring; (iv) a security that has been delisted from a national exchange; (v) a security subject to trading collars for which no or limited trading takes place; and

(vi) a security whose principal market has been temporarily closed at a time when, under normal

Notes to

Financial Statements (continued)

conditions, it would be open. Securities valued in this manner

are generally categorized as Level 2 or 3 in the hierarchy.

Municipal debt securities are valued at the evaluated mean prices supplied by a pricing agent or broker selected by the

Valuation Designee, in consultation with the Subadvisor. The evaluations are market-based measurements

processed through a pricing application and represents the pricing agent's good faith determination as to what a holder may receive in an orderly transaction under market conditions. The rules-based logic utilizes valuation techniques that

reflect participants' assumptions and vary by asset class and per methodology, maximizing the use of

relevant observable data including quoted prices for similar assets, benchmark yield curves and market corroborated inputs. The evaluated bid or mean prices are deemed by the Valuation Designee, in consultation with the Subadvisor, to be

representative of market values, at the regular close of trading of the Exchange on each valuation date.

Municipal debt securities purchased on a delayed delivery basis are marked to market daily until settlement

at the forward settlement date. Municipal debt securities are generally categorized as Level 2 in the

hierarchy.

The information above

is not intended to reflect an exhaustive list of the methodologies that may be used to value portfolio investments. The Valuation Procedures permit the use of a variety of valuation methodologies in connection with valuing portfolio

investments. The methodology used for a specific type of investment may vary based on the market data

available or other considerations. The methodologies summarized above may not represent the specific means by which portfolio investments are valued on any particular business day.

(B) Income Taxes. The Fund's policy is to comply with the requirements of the Internal Revenue Code of 1986, as amended (the “Internal Revenue Code”), applicable to

regulated investment companies and to distribute all of its taxable income to the shareholders of the Fund

within the allowable time limits.

The Manager evaluates the Fund’s tax positions to determine if the tax positions taken meet the minimum recognition threshold in connection with accounting for uncertainties in income tax

positions taken or expected to be taken for the purposes of measuring and recognizing tax liabilities in

the financial statements. Recognition of tax benefits of an uncertain tax position is permitted only to the extent the position is “more likely than not” to be sustained assuming examination by taxing authorities. The Manager analyzed the Fund's tax

positions taken on federal, state and local income tax returns for all open tax years (for up to three tax

years) and has concluded that no provisions for federal, state and local income tax are required in the Fund's financial statements. The Fund's federal, state and local income tax and federal excise tax returns for tax years for which the applicable

statutes of limitations have not expired are subject to examination by the Internal Revenue Service and

state and local departments of revenue.

(C) Dividends and

Distributions to Common Shareholders. Dividends and

distributions are recorded on the ex-dividend date. The Fund intends to declare dividends from net investment income at least monthly and declares and pays distributions from net realized capital gains, if any, at least annually. Dividends

and distributions are determined in accordance with federal income tax regulations and may differ from

determinations using GAAP. For information on the Fund’s dividend reinvestment plan, please see

page35.

(D) Security Transactions and Investment Income. The Fund records security transactions on the trade date. Realized gains and losses on security transactions are determined using

the identified cost method. Interest income is accrued as earned using the effective interest rate method.

Discounts and premiums on securities purchased by the Fund, other than temporary cash investments that mature in 60 days or less at the time of purchase, are accreted and amortized, respectively, using the effective interest rate method.

The Fund may place a debt security on non-accrual status and reduce related interest income by ceasing current accruals and writing off all or a portion of any interest receivables when

the collection of all or a portion of such interest has become doubtful. A debt security is removed from

non-accrual status when the issuer resumes interest payments or when collectability of interest is

reasonably assured.

(E) Expenses. Expenses of the Fund are recorded on the date the expenses are incurred. The expenses borne by the Fund, including those

of related parties to the Fund, are shown in the Statement of Operations. Certain expenses of the Fund are

allocated in proportion to other funds within the MainStay Group of Funds.

(F) Use of Estimates. In preparing financial statements in conformity with GAAP, the Manager makes estimates and assumptions that affect the reported amounts and disclosures in the financial

statements. Actual results could differ from those estimates and assumptions.

(G) Tender Option Bonds. The Fund may leverage its assets through the use of proceeds received from tender option bond (“TOB”) transactions. In a TOB transaction, a tender

option bond trust (a “TOB Issuer”) is typically established, which forms a special purpose trust into which the Fund, or an agent on behalf of the Fund, transfers municipal bonds or other municipal securities

(“Underlying Securities”). A TOB Issuer typically issues two classes of beneficial interests: short-term floating rate notes (“TOB Floaters”) with a fixed principal amount representing a senior interest in the

Underlying Securities, and which are sold to third party investors, and residual interest municipal tender option bonds (“TOB Residuals”) representing a subordinate interest in the Underlying Securities, and which are

generally issued to the Fund. The interest rate on the TOB Floaters resets periodically, usually weekly, to a

prevailing market rate, and holders of the TOB Floaters are granted the option to tender their TOB Floaters

back to the TOB Issuer for repurchase at their principal amount plus accrued interest thereon periodically,

usually daily or weekly. The Fund may invest in both TOB Floaters and TOB Residuals. The Fund may not

invest more than 5% of its Managed

| |

MainStay MacKay DefinedTerm Municipal Opportunities Fund

|

Assets (as defined in Note 3(A)) in any single

TOB Issuer. The Fund may invest in both TOB Floaters and TOB Residuals issued by the same TOB

Issuer.

Typically, a fund serves

as the sponsor of the TOB issuer (“Fund-sponsored TOB”). Under this structure, a fund establishes, structures and “sponsors” the TOB Issuer in which it holds TOB Residuals. The Fund uses this or a similar

structure for any TOB in which it invests. In connection with Fund-sponsored TOBs, the fund sponsoring the

Fund-sponsored TOB (“Fund Sponsor”) may contract with a third-party to perform some or all of

the Fund Sponsor’s duties as sponsor. Regardless of whether the Fund Sponsor delegates any of its sponsorship duties to a third party, the Fund Sponsor’s expanded role under the Fund-sponsored TOB structure may increase the Fund

Sponsor’s operational and regulatory risk. If the third-party is unable to perform its obligations as an administrative agent, the Fund Sponsor itself would be subject to such obligations or would need to secure a replacement

agent. The obligations that the Fund Sponsor may be required to undertake could include reporting and

recordkeeping obligations under the Internal Revenue Code and federal securities laws and contractual obligations with other TOB service providers. The Fund may serve as a Fund Sponsor to a Fund-sponsored TOB. If the Fund serves as a Fund Sponsor,

it would be subject to the obligations discussed above and the risks attendant to such

obligations.

Under the

Fund-sponsored TOB structure, the TOB Issuer receives Underlying Securities from the Fund through (or as) the Fund Sponsor and then issues TOB Floaters to third party investors and TOB Residuals to the Fund. The Fund is paid the cash (less

transaction expenses, which are borne by the Fund) received by the TOB Issuer from the sale of TOB Floaters

and typically will invest the cash in additional municipal bonds or other investments permitted by its investment policies. TOB Floaters may have first priority on the cash flow from the securities held by the TOB Issuer and are enhanced with a liquidity

support arrangement from a bank or an affiliate of the sponsor (the “liquidity provider”), which allows holders to tender their position back to the TOB Issuer at par (plus accrued interest). The Fund, in addition to

receiving cash from the sale of TOB Floaters, also receives TOB Residuals. TOB Residuals provide the Fund

with the right to (1) cause the holders of TOB Floaters to tender their notes to the TOB Issuer at par (plus accrued interest), and (2) acquire the Underlying Securities from the TOB Issuer. In addition, all voting rights and decisions to be made with respect to any

other rights relating to the Underlying Securities deposited in the TOB Issuer are passed through to the

Fund, as the holder of TOB Residuals. Such a transaction, in effect, creates exposure for the Fund to the entire return of the Underlying Securities deposited in the TOB Issuer, with a net cash investment by the Fund that is less than the value of the

Underlying Securities deposited in the TOB Issuer. This multiplies the positive or negative impact of the

Underlying Securities’ return within the Fund (thereby creating leverage). Income received from TOB

Residuals will vary inversely with the short-term rate paid to holders of TOB Floaters and in most

circumstances, TOB Residuals represent substantially all of the Underlying Securities’ downside

investment risk and also benefits disproportionately

from any potential appreciation of the Underlying Securities’ value. The amount of such increase or decrease is a

function, in part, of the amount of TOB Floaters sold by the TOB Issuer of these securities relative to the

amount of TOB Residuals that it sells. The greater the amount of TOB Floaters sold relative to TOB

Residuals, the more volatile the income paid on TOB Residuals will be. The price of TOB Residuals will be more volatile than that of the Underlying Securities because the interest rate is dependent on not only the fixed coupon rate of the

Underlying Securities, but also on the short-term interest rate paid on TOB Floaters.

For TOB Floaters, generally, the interest rate earned will be based upon the market rates for municipal securities with

maturities or remarketing provisions that are comparable in duration to the periodic interval of the tender

option, which may vary from weekly, to monthly, to extended periods of one year or multiple years. Since the option feature has a shorter term than the final maturity or first call date of the Underlying Securities deposited in the TOB Issuer, the

Fund, if it is the holder of the TOB Floaters, relies upon the terms of the agreement with the financial

institution furnishing the option as well as the credit strength of that institution. As further assurance

of liquidity, the terms of the TOB Issuer provide for a liquidation of the Underlying Security deposited in the TOB Issuer and the application of the proceeds to pay off the TOB Floaters.

The TOB Issuer may be terminated without the consent of the Fund upon the occurrence of certain events, such as the

bankruptcy or default of the issuer of the Underlying Securities deposited in the TOB Issuer, a substantial

downgrade in the credit quality of the issuer of the securities deposited in the TOB Issuer, the inability of the TOB Issuer to obtain liquidity support for the TOB Floaters, a substantial decline in the market value of the Underlying Securities deposited

in the TOB Issuer, or the inability of the sponsor to remarket any TOB Floaters tendered to it by holders

of the TOB Floaters. In such an event, the TOB Floaters would be redeemed by the TOB Issuer at par (plus accrued interest) out of the proceeds from a sale of the Underlying Securities deposited in the TOB Issuer. If this happens, the Fund would be

entitled to the assets of the TOB Issuer, if any, that remain after the TOB Floaters have been redeemed at

par (plus accrued interest). If there are insufficient proceeds from the sale of these Underlying Securities to redeem all of the TOB Floaters at par (plus accrued interest), the liquidity provider or holders of the TOB Floaters would bear the losses on

those securities and there would be no recourse to the Fund’s assets (unless the Fund held a recourse

TOB Residual).

To the extent that the remarketing agent and/or the liquidity provider is a banking entity, the TOB may face heightened liquidity risks due to restrictions applicable to banking entities under the

Volcker Rule. The Volcker Rule generally prohibits banking entities from engaging in proprietary trading or

from acquiring or retaining an ownership interest in, or sponsoring, a hedge fund or private equity fund (a “Covered Fund”). TOB Issuers are often structured as a Covered Fund, and therefore, a banking entity that is a remarketing agent would

not be able to repurchase tendered TOB Floaters for its own account upon a failed remarketing. In the event

of a failed remarketing, a banking entity serving as liquidity provider may loan the necessary funds to the TOB Issuer to

Notes to

Financial Statements (continued)

purchase the tendered TOB Floaters. The TOB Issuer, not the Fund

Sponsor or the Fund, would be the borrower and the loan from the liquidity provider will be secured by the

purchased TOB Floaters now held by the TOB Issuer. However, the Fund Sponsor and the Fund would bear the

risk of loss with respect to any liquidity shortfall to the extent it entered into a reimbursement agreement with the liquidity provider. If a TOB Issuer in which the Fund invests experiences adverse events in connection with a failed remarketing of TOB Floaters

or a liquidity shortfall, the Fund would experience a loss.

For financial reporting purposes, Underlying Securities that are deposited into a TOB Issuer are treated as investments

of the Fund, and are presented in the Fund’s Portfolio of Investments. Outstanding TOB Floaters