UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

☒

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended March 31, 2023

☐

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from___________ to___________

Commission file number 000-27251

QDM International

Inc.

(Exact name of registrant as specified in its charter)

| Florida |

|

59-3564984 |

| (State or other jurisdiction of |

|

(I.R.S. Employer |

| incorporation or organization) |

|

Identification No.) |

| |

|

|

Room 1030B, 10/F, Ocean Centre, Harbour City,

5 Canton Road, Tsim Sha Tsui, Hong Kong |

|

- |

| (Address of principal executive offices) |

|

(Zip Code) |

| |

|

|

| + 852 34886893 |

| (Registrant’s telephone number, including area code) |

Securities registered pursuant to Section 12(b)

of the Act: None

Securities registered pursuant to Section 12(g)

of the Act: Common Stock, par value $0.0001

Indicate by check mark if the registrant is a

well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

No ☒

Indicate by check mark if the registrant is not

required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

No ☒

Indicate by check mark whether the registrant

(1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months

(or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements

for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant

has submitted electronically every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405

of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files)

Yes ☒ No ☐

Indicate by check mark whether the registrant

is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company.

See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,”

and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer |

☐ |

Accelerated filer |

☐ |

| Non-accelerated filer |

☒ |

Smaller reporting company |

☒ |

| |

|

Emerging growth company |

☐ |

If an emerging growth company, indicate by check

mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting

standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant

has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial

reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or

issued its audit report. ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant

included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether

any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the

registrant's executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant

is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐

No ☒

The aggregate market value of the voting and non-voting

common stock held by non-affiliates computed by reference to the price at which the common stock was last sold on the OTCQB Marketplace

operated by the OTC Markets as of September 30, 2022 ($0.81) was approximately $ 41,038.65.

As of June 29, 2023, 29,156,393 shares of common

stock, $0.0001 par value per share, of the registrant were issued and outstanding.

| Auditor Name: |

|

Auditor Location: |

|

Auditor Firm ID: |

| ZH CPA, LLC |

|

Denver, Colorado |

|

6413 |

TABLE OF CONTENTS

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K (the “Report”),

including, without limitation, statements under the heading “Management’s Discussion and Analysis of Financial Condition and

Results of Operations,” includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as

amended (the “Securities Act”) and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”).

These forward-looking statements can be identified by the use of forward-looking terminology, including the words “believes,”

“estimates,” “anticipates,” “expects,” “intends,” “plans,” “may,”

“will,” “potential,” “projects,” “predicts,” “continue,” or “should,”

or, in each case, their negative or other variations or comparable terminology. There can be no assurance that actual results will not

materially differ from expectations. These statements are based on management’s current expectations, but actual results may differ

materially due to various factors, including, but not limited to:

| ● | the impact of public health

epidemics, including the COVID-19 pandemic in Mainland China, Hong Kong and the rest of the world, on the market we operate in and our

business, results of operations and financial condition; |

| ● | the impact of political uncertainty

and social unrest in Hong Kong and laws, rules and regulations of the Chinese government aimed at addressing such unrest; |

| ● | the market for our services

in Hong Kong and Mainland China; |

| ● | our expansion and other plans

and opportunities; |

| ● | our future financial and operating

results, including revenues, income, expenditures, cash balances and other financial items; |

| ● | current and future economic

and political conditions in Hong Kong and Mainland China; |

| ● | the future growth of the Hong

Kong insurance industry as a whole and the professional insurance intermediary sector in particular; |

| ● | our ability to attract customers,

further enhance our brand recognition; |

| ● | our ability to hire and retain

qualified management personnel and key employees in order to enable them to develop our business; |

| ● | changes in applicable laws

or regulations in Hong Kong related to or that could impact our business; |

| ● | our management of business

through a U.S. publicly-traded and reporting company; and |

| ● | other assumptions regarding

or descriptions of potential future events or circumstances described in this Report underlying or relating to any forward-looking statements. |

The forward-looking statements contained in this

Report are based on our current expectations and beliefs concerning future developments and their potential effects on us. Future developments

affecting us may not be those that we have anticipated. These forward-looking statements involve a number of risks, uncertainties (some

of which are beyond our control) and other assumptions that may cause actual results or performance to be materially different from those

expressed or implied by these forward-looking statements. Should one or more of these risks or uncertainties materialize, or should any

of our assumptions prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements.

We undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or

otherwise, except as may be required under applicable securities laws.

By their nature, forward-looking statements involve

risks and uncertainties because they relate to events and depend on circumstances that may or may not occur in the future. We caution

you that forward-looking statements are not guarantees of future performance and that our actual results of operations, financial condition

and liquidity, and developments in the industry in which we operate may differ materially from those made in or suggested by the forward-looking

statements contained in this Report. In addition, even if our results of operations, financial condition and liquidity, and developments

in the industry in which we operate are consistent with the forward-looking statements contained in this Report, those results or developments

may not be indicative of results or developments in subsequent periods.

Unless otherwise indicated or the context otherwise

requires, references in this Report to:

| |

● |

“24/7 Kid” are to 24/7 Kid Doc, Inc., a Florida corporation and wholly-owned subsidiary of the Company; |

| |

● |

“BVI” are to the British Virgin Islands; |

| |

● |

“Common stock” are to the common stock of the Company, par value $0.0001 per share; |

| |

● |

“EUR,” “€” and “Euro” are to the legal currency of those member states of the European Union that have adopted the single currency; |

| |

● |

“HKD,” “HK$” and “Hong Kong dollars” are to the legal currency of Hong Kong; |

| |

● |

“QDM BVI” are to QDM Holdings Limited, a BVI company and a wholly-owned subsidiary of the Company; |

| |

● |

“QDM HK” are to QDM Group Limited, a Hong Kong corporation and a wholly-owned subsidiary of the QDM BVI; |

| |

● |

“QDM” and the “Company” refer to QDM International Inc., a Florida corporation; and |

| |

● |

“Series C Preferred Stock” are to the Series C Convertible Preferred Stock, par value $0.0001 per share, each convertible into eleven shares of common stock initially; |

| |

● |

the “Group” are to QDM BVI, QDM HK and YeeTah, collectively; |

| |

● |

“Technical representatives” are to licensed individuals who provide advice to an insurance policy holder or potential policy holder on insurance matters on behalf of an insurance agent or broker, or arrange contracts of insurance in or from Hong Kong on behalf of that insurance agent or broker; |

| |

● |

“US$,” “U.S. dollars,” “$,” and “USD” are to the legal currency of the United States; |

| |

● |

“We,” “us,” and “our” refer to QDM International Inc. and/or its consolidated subsidiaries, unless the context suggests otherwise; and |

| |

● |

“YeeTah” are to Hong Kong YeeTah Insurance Broker Limited,

formerly known as YeeTah Insurance Consultant Limited, a Hong Kong corporation and wholly-owned subsidiary of QDM HK. |

The Company, 24/7 Kid, and QDM BVI maintain their

books and records in U.S. dollars and in accordance with generally accepted accounting principles of the United States. QDM HK and YeeTah

maintain their books and records either in U.S. dollars or Hong Kong dollars. This Report also contains translations of Hong Kong dollars

into U.S. dollars for the convenience of the reader. The Hong Kong dollar is freely convertible into other currencies (including the U.S.

dollar). Since 1983, the Hong Kong dollar has effectively been officially linked to the U.S. dollar at the rate of approximately HK$7.80

= US$1.00. However, the market exchange rate of the Hong Kong dollar against the U.S. dollar continues to be influenced by the forces

of supply and demand in the foreign exchange market.

Unless otherwise stated, all translations of Hong Kong dollars into

U.S. dollars were made at HK$7.80 = US$1.00, which is the prevailing exchange rate as of March 31, 2023. We make no representation

that the Hong Kong dollar or U.S. dollar amounts referred to in this Report could have been or could be converted into U.S. dollars or

Hong Kong dollars, as the case may be, at any particular rate or at all.

PART I

Item 1. Business.

Overview

QDM is a holding company incorporated in Florida

with no material operations, and we conduct our insurance brokerage business through our indirectly wholly-owned subsidiary, YeeTah, primarily

in Hong Kong.

YeeTah sells a wide range of insurance products

consisting of two major categories: (1) life and medical insurance, such as individual life insurance; and (2) general insurance, such

as automobile insurance, commercial property insurance, liability insurance and homeowner insurance. In addition, as a Mandatory Provident

Fund (“MPF”) intermediary, YeeTah also provides its customers with assistance on account opening and related services under

the MPF and the Occupational Retirement Schemes Ordinance schemes (“ORSO”) in Hong Kong, both of which are mandatory retirement

protection schemes set up for employees who are Hong Kong residents.

YeeTah sells insurance

products underwritten by insurance companies operating in Hong Kong to individual customers who are either Hong Kong residents or visitors

from Mainland China and are compensated for its services by commissions paid by insurance companies, typically based on a percentage of

the premium paid by the insured. Commissions generally depend on the type, term of insurance products and the particular insurance company

and they are usually paid by the insurance companies the next month after the cooling off period of the policies sold, which is generally

21 days after the earlier of the delivery of the policy or a cooling off notice to the policy holder.

As of the date of this

Report, YeeTah has been a party to agreements with 19 insurance companies in Hong Kong, and offers approximately 431 insurance products to

our customers. For the fiscal year ended March 31, 2023, an aggregate of 98.92% of YeeTah’s total commissions was attributable to

its top two insurance companies, each accounted for more than 10% of its total commissions. For the fiscal year ended March 31, 2022,

an aggregate of 81.45 % of YeeTah’s total commissions was attributable to its top two insurance companies, each accounted for

more than 10% of our total commissions.

As of March 31, 2023,

YeeTah had serviced an aggregate of 679 customers in connection with the purchase of an aggregate of 735 insurance products as well as

a total of 44 customers for MPF related services.

As an independent insurance

agency, YeeTah offers not only a broad range of insurance products underwritten by multiple insurance companies to address the needs of

increasingly sophisticated customers with diverse needs and preferences but also quality services covering the policy application, customer

information collection, analysis of policy selection, and after-sale services.

We focus on offering

long-term life insurance products including endowment life and annuity life insurance and distribute general insurance products including

automobile insurance, individual accident insurance, homeowner insurance, liability insurance and travel insurance. All of YeeTah’s

sales of life and medical insurance products and general insurance products are conducted through its licensed sales persons (known in

Hong Kong as technical representatives).

Hong Kong’s independent

insurance intermediary market is experiencing rapid growth due to increasing demands for insurance products by the Chinese population,

especially visitors from mainland China. We intend to grow our business by offering premium services and recruiting talent to join our

professional team and sales force, expanding our distribution network through building more connections with business partners in Hong

Kong and mainland China, such as wealth management companies, funds, trust companies, and overseas immigration agencies.

Public Offering

In March, 2023, the Company consummated a closing

of a public offering of its common stock, par value $0.0001 per share (the “2023 Offering”), in which the Company issued and

sold an aggregate of 28,910,400 shares of its common stock at a price of $0.081 per share to certain investors, generating gross proceeds

to the Company of $2,339,937. The material terms of the 2023 Offering are described in the prospectus, dated January 27, 2023, filed by

the Company with the SEC on February 01, 2023, pursuant to Rule 424(b) under the Securities Act. The Offering is registered pursuant to

the Company’s Registration Statement on Form S-1 (Registration No. 333-267263), originally filed with the SEC on September 2, 2022

(as amended, the “Registration Statement”), which was declared effective by the SEC on January 27, 2023.

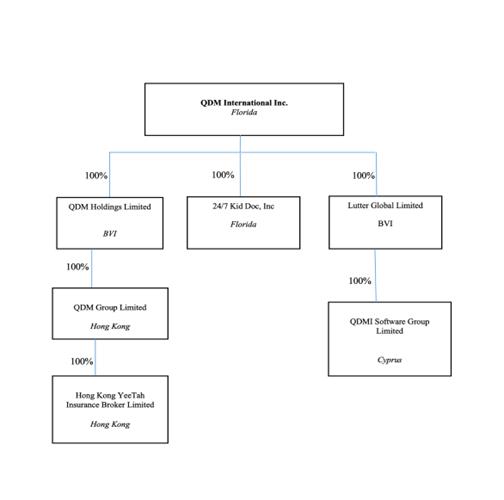

Holding Company Structure

QDM is not an operating company but a Florida

holding company with operations primarily conducted through its indirectly wholly-owned subsidiary based in Hong Kong. Our investors hold

shares of common stock in QDM, the Florida holding company.

We do not have or intend to set up any subsidiary

or enter into any contractual arrangements to establish a variable interest entity (“VIE”) structure with any entity in China.

24/7 Kid, Lutter Global Limited (“LGL”), and QDM Software Group Limited (“QDMS”) currently have no operations.

Our corporate organizational structure is as follows as of the date of this Report:

Our holding company structure presents unique

risks as our investors may never directly hold equity interests in our Hong Kong operating subsidiary and will be dependent upon dividends

and other distributions from our subsidiaries to finance our cash flow needs. Our ability to receive dividends and other contributions

from our subsidiaries are significantly affected by regulations promulgated by Hong Kong and PRC authorities. Any change in the interpretation

of existing rules and regulations or the promulgation of new rules and regulations may materially affect our operations and or the value

of our securities, including causing the value of our securities to significantly decline or become worthless. For a detailed description

of the risks facing the Company associated with our structure, please refer to “Item 1A. Risk Factors – Risks Related to

Doing Business in Hong Kong.”

Currently, PRC laws and regulations do not prohibit

direct foreign investment in our Hong Kong operating subsidiary. Nonetheless, in light of the recent statements and regulatory actions

by the PRC government, such as those related to Hong Kong’s national security, the promulgation of regulations prohibiting foreign

ownership of Chinese companies operating in certain industries, which are constantly evolving, and anti-monopoly concerns, we may be subject

to the risks of the uncertainty of any future actions of the PRC government in this regard, which would likely result in a material change

in our operations, including our ability to continue our existing holding company structure, carry on our current business, accept foreign

investments, and offer or continue to offer securities to our investors, and the resulting adverse change in value to our common stock.

We may also be subject to penalties and sanctions imposed by the PRC regulatory agencies, including the China Securities Regulatory Commission,

or CSRC, if we fail to comply with such rules and regulations, which would likely adversely affect the ability of the Company’s

securities to continue to trade on the OTCQB, which would likely cause the value of our securities to significantly decline or become

worthless.

The Holding Foreign Companies Accountable Act (the “HFCAA”)

As more stringent criteria applying to emerging market companies upon

assessing the qualification of their auditors have been imposed by the United States Securities and Exchange Commission (the “SEC”)

and the Public Company Accounting Oversight Board (the “PCAOB”) recently, and under the HFCAA, our securities may be prohibited

from being traded on the over-the-counter (the “OTC”) markets if our auditor is not inspected by the PCAOB for three consecutive

years, and this ultimately could result in trading in our securities being prohibited.

The Holding Foreign Companies Accountable Act,

or the HFCAA, was enacted on December 18, 2020. The HFCAA states if the SEC determines that we have filed audit reports issued by

a registered public accounting firm that has not been subject to inspection by the PCAOB for three consecutive years beginning in

2021, the SEC shall prohibit our shares from being traded on a national securities exchange or in the over-the-counter trading market

in the United States.

On March 24, 2021, the SEC adopted interim

final rules relating to the implementation of certain disclosure and documentation requirements of the HFCAA. A company will be required

to comply with these rules if the SEC identifies it as having a “non-inspection” year under a process to be subsequently established

by the SEC. The SEC is assessing how to implement other requirements of the HFCAA, including the listing and trading prohibition

requirements described above. Furthermore, on June 22, 2021, the U.S. Senate passed the Accelerating Holding Foreign Companies

Accountable Act (the “AHFCAA”), which was signed into law on December 29, 2022, amending the HFCAA and requiring the

SEC to prohibit an issuer’s securities from trading on any U.S. stock exchange if its auditor is not subject to PCAOB inspections

for two consecutive years instead of three consecutive years. On September 22, 2021, the PCAOB adopted a final rule implementing

the HFCAA, which provides a framework for the PCAOB to use when determining, as contemplated under the HFCAA, whether the PCAOB is unable

to inspect or investigate completely registered public accounting firms located in a foreign jurisdiction because of a position taken

by one or more authorities in that jurisdiction. On December 2, 2021, the SEC issued amendments to finalize rules implementing the

submission and disclosure requirements in the HFCAA. The rules apply to registrants that the SEC identifies as having filed an annual

report with an audit report issued by a registered public accounting firm that is located in a foreign jurisdiction and that PCAOB is

unable to inspect or investigate completely because of a position taken by an authority in foreign jurisdictions. On December 16,

2021, the PCAOB issued a Determination Report which found that the PCAOB is unable to inspect or investigate completely registered public

accounting firms headquartered in: (i) China, and (ii) Hong Kong.

On August 26, 2022, the PCAOB announced and

signed a Statement of Protocol (the “Protocol”) with the China Securities Regulatory Commission and the Ministry of Finance

of the People’s Republic of China. The Protocol provides the PCAOB with: (1) sole discretion to select the firms, audit engagements

and potential violations it inspects and investigates, without any involvement of Chinese authorities; (2) procedures for PCAOB inspectors

and investigators to view complete audit work papers with all information included and for the PCAOB to retain information as needed;

(3) direct access to interview and take testimony from all personnel associated with the audits the PCAOB inspects or investigates.

On December 15, 2022, the PCAOB issued a

new Determination Report which: (1) vacated the December 16, 2021 Determination Report; and (2) concluded that the PCAOB

has been able to conduct inspections and investigations completely in the PRC in 2022. The December 15, 2022 Determination Report

cautions, however, that authorities in the PRC might take positions at any time that would prevent the PCAOB from continuing to inspect

or investigate completely. As required by the HFCAA, if in the future the PCAOB determines it no longer can inspect or investigate completely

because of a position taken by an authority in the PRC, the PCAOB will act expeditiously to consider whether it should issue a new determination.

As of the date of this Report,

our auditor, ZH CPA, LLC is not subject to the determinations as to inability to inspect or investigate completely as announced by the

PCAOB on December 16, 2021 as they are not on the list published by the PCAOB. As a firm registered with the PCAOB, ZH CPA, LLC is headquartered

in Denver, Colorado, and is subject to laws in the United States which provide that the PCAOB shall conduct regular inspections to assess

the auditor’s compliance with the applicable professional standards. We have no intention of dismissing ZH CPA, LLC in the future

or engaging any auditor not based in the U.S. and not subject to regular inspection by the PCAOB. There is no guarantee, however, that

any future auditor engaged by the Company would remain subject to full PCAOB inspection during the entire term of our engagement. If it

is later determined that the PCAOB is unable to inspect or investigate our auditor completely, investor may be deprived of the benefits

of such inspection. Any audit reports not issued by auditors that are completely inspected by the PCAOB, or a lack of PCAOB inspections

of audit work undertaken in China or Hong Kong that prevents the PCAOB from regularly evaluating our auditors’ audits and their

quality control procedures, could result in a lack of assurance that our financial statements and disclosures are adequate and accurate.

See “Item 1A. Risk Factors – Risks Related to Doing Business in Hong Kong — Under the HFCAA, our securities

may be prohibited from being traded on any U.S. securities exchange, including the New York Stock Exchange and Nasdaq, or through any

other trading method within the SEC’s regulatory jurisdiction, including the OTC markets if our auditor is not inspected by the

PCAOB for three consecutive years, and this ultimately could result in trading in our securities being prohibited. Furthermore, on June

22, 2021, the U.S. Senate passed the Accelerating Holding Foreign Companies Accountable Act, which, if enacted, would amend the HFCAA

and require the SEC to prohibit an issuer’s securities from trading on any U.S. stock exchanges or the OTC markets if its auditor

is not subject to PCAOB inspections for two consecutive years instead of three” on page 34.

Transfers of Cash to and from Our Subsidiaries

QDM is a holding company incorporated in Florida

with no material operations of its own, and we conduct our insurance brokerage business through our indirectly wholly-owned subsidiary,

YeeTah, primarily in Hong Kong. We may rely on dividends and other distributions on equity to be paid by our Hong Kong subsidiary to fund

our cash and financing requirements, including the funds necessary to pay dividends and other cash distributions to our stockholders,

to service any debt we may incur and to pay our operating expenses. Currently, substantially all of our operations are in Hong Kong. We

do not have or intend to set up any subsidiary or enter into any contractual arrangements to establish a VIE structure with any entity

in China. Hong Kong is a special administrative region of the PRC and the basic policies of the PRC regarding Hong Kong are reflected

in the Basic Law of the Hong Kong Special Administrative Region of the People’s Republic of China (the “Basic Law”),

providing Hong Kong with a high degree of autonomy and executive, legislative and independent judicial powers, including that of final

adjudication under the principle of “one country, two systems.” The laws and regulations of the PRC do not currently have

any material impact on transfer of cash from us to YeeTah or from YeeTah to us and the investors in the U.S. In addition, there are no

restrictions or limitations under the laws of Hong Kong imposed on the conversion of Hong Kong dollar into foreign currencies and the

remittance of currencies out of Hong Kong or across borders and to U.S investors.

We are permitted under the Florida law to provide

funding to our subsidiaries, including YeeTah, through loans or capital contributions without restrictions on the amount of the funds.

There are no restrictions or limitations on our ability to distribute earnings from our businesses, including our subsidiaries, to the

U.S. investors. YeeTah is permitted under the laws of Hong Kong to provide funding to QDM HK and QDM BVI, the holding company incorporated

in Hong Kong and the British Virgin Islands, respectively, through dividend or other distribution without restrictions on the amount of

the funds. As of the date of this Report, there has been no dividends or distributions between our holding company and our subsidiaries

nor do we expect such dividends or distributions to occur in the foreseeable future among our holding company and its subsidiaries.

YeeTah currently intends to retain all available

funds and future earnings, if any, for the operation and expansion of its business and does not anticipate declaring or paying any dividends

in the foreseeable future. There are no significant restrictions and limitations on our ability

to distribute earnings from our businesses, including our subsidiaries, to the parent company and U.S. investors or our ability to settle

amounts owed. There are no significant restrictions on foreign exchange or our ability to transfer cash between entities within our group,

across borders, or to U.S. investors. However, the PRC government has significant authority to intervene or influence the China operations

of an offshore holding company at any time, and such oversight may also extend to our Hong Kong operating company. We cannot assure you

that the PRC government will not prevent us from transferring the cash we maintain in Hong Kong outside of Hong Kong, or restrict our

ability to deploy our cash into business or to pay dividends. We could also be subject to limitations on the transfer or the use of our

cash if we expand our business operations into China or conduct our operations in some other ways such that we become subject to PRC laws

that regulate these activities. In addition, if YeeTah incurs debt on its own behalf in the future, the instruments governing the

debt may restrict its ability to pay dividends or make other distributions to us. Any limitation

on our ability to transfer or use our cash could materially and adversely limit our ability to grow, make investments or acquisitions

that could be beneficial to our business, pay dividends, or otherwise fund and conduct our business.

We have never paid or declared any cash dividends

on our common stock and do not anticipate paying cash dividends in the foreseeable future. The declaration of dividends on any class of

shares is within the discretion of our board of directors, subject to the Florida law, out of legally available funds, and will depend

on the assessment of, among other factors, earnings, capital requirements and our operating and financial condition. If we determine to

pay dividends on any of our capital stock in the future, we will be dependent on receipt of funds from our Hong Kong subsidiary, YeeTah.

None of our subsidiaries has made any dividends or distributions to us. Under the current practice of the Inland Revenue Department of

Hong Kong, no tax is payable in Hong Kong in respect of dividends paid by us. See “Item 1A. Risk Factors – Risks Related

to Our Business and Industry – We rely on dividends and other distributions on equity paid by our subsidiaries to fund any cash

and financing requirements we may have, and any limitation on the ability of our subsidiaries to make payments to us could have a material

adverse effect on our ability to conduct our business” on page 30 and “Item 1A. Risk Factors – Risks Related

to Doing Business in Hong Kong - Our Hong Kong subsidiary may be subject to restrictions on paying dividends or making other payments

to us, which may restrict its ability to satisfy liquidity requirements, conduct business and pay dividends to holders of our common stock.

Dividends payable to our foreign investors and gains on the sale of our shares of common stock by our foreign investors may become subject

to tax by the PRC” on page 32.

Regulatory Permissions and Developments

Our counsel as to PRC law has advised us that

the laws and regulations of the PRC do not currently have any material impact on our business, financial condition or results of operations.

However, there is no assurance that there will not be any changes in the economic, political and legal environment in Hong Kong in the

future. If there is a significant change to current political arrangements between mainland China and Hong Kong, companies operating in

Hong Kong such as us may face similar regulatory risks as those operated in PRC, including their ability to offer securities to investors,

list their securities on a U.S. or other foreign exchange, conduct their business or accept foreign investment. In light of China’s

recent expansion of authority in Hong Kong, there are risks and uncertainties which we cannot foresee for the time being, and rules and

regulations in China can change quickly with little or no advance notice. The Chinese government may intervene or influence our current

and future operations in Hong Kong at any time, or may exert more control over offerings conducted overseas and/or foreign investment

in issuers likes ourselves. See “Item 1A. Risk Factors – Risks Related to Doing Business in Hong Kong.”

We are aware that the PRC government initiated

a series of regulatory actions and statements to regulate business operations in certain areas in China with little advance notice, including

cracking down on illegal activities in the securities market, enhancing supervision over China-based companies listed overseas using variable

interest entity structure, adopting new measures to extend the scope of cybersecurity reviews, and expanding the efforts in anti-monopoly

enforcement.

For example, on June 10, 2021, the Standing Committee

of the National People’s Congress enacted the PRC Data Security Law, which took effect on September 1, 2021. The law requires data

collection to be conducted in a legitimate and proper manner, and stipulates that, for the purpose of data protection, data processing

activities must be conducted based on data classification and hierarchical protection system for data security.

On July 6, 2021, the General Office of the Communist

Party of China Central Committee and the General Office of the State Council jointly issued a document to crack down on certain activities

in the securities markets and promote the high-quality development of the capital markets, which, among other things, requires the relevant

governmental authorities to strengthen cross-border oversight of law-enforcement and judicial cooperation, to enhance supervision over

Chinese-based companies listed overseas, and to establish and improve the system of extraterritorial application of the PRC securities

laws.

On August 20, 2021, the 30th meeting of the Standing

Committee of the 13th National People’s Congress voted and passed the “Personal Information Protection Law of the People’s

Republic of China,” or “PRC Personal Information Protection Law,” which became effective on November 1, 2021. The PRC

Personal Information Protection Law applies to the processing of personal information of natural persons within the territory of China

that is carried out outside of China where (i) such processing is for the purpose of providing products or services for natural persons

within China, (ii) such processing is to analyze or evaluate the behavior of natural persons within China, or (iii) there are any other

circumstances stipulated by related laws and administrative regulations.

On December 24, 2021, the CSRC, together with

other relevant government authorities in China issued the Provisions of the State Council on the Administration of Overseas Securities

Offering and Listing by Domestic Companies (Draft for Comments), and the Measures for the Filing of Overseas Securities Offering and Listing

by Domestic Companies (Draft for Comments) (“Draft Overseas Listing Regulations”). The Draft Overseas Listing Regulations

require that a PRC domestic enterprise seeking to issue and list its shares overseas (“Overseas Issuance and Listing”) shall

complete the filing procedures of and submit the relevant information to CSRC. The Overseas Issuance and Listing includes direct and indirect

issuance and listing. Where an enterprise whose principal business activities are conducted in PRC seeks to issue and list its shares

in the name of an overseas enterprise (“Overseas Issuer”) on the basis of the equity, assets, income or other similar rights

and interests of the relevant PRC domestic enterprise, such activities shall be deemed an indirect overseas issuance and listing (“Indirect

Overseas Issuance and Listing”) under the Draft Overseas Listing Regulations.

On December 28, 2021, the Cyberspace Administration

of China (the “CAC”) jointly with the relevant authorities formally published Measures for Cybersecurity Review (2021) which

took effect on February 15, 2022, replacing the former Measures for Cybersecurity Review (2020) issued on July 10, 2021. Measures for

Cybersecurity Review (2021) stipulates that operators of critical information infrastructure purchasing network products and services,

and online platform operators (together with the operators of critical information infrastructure, the “Operators”) carrying

out data processing activities that affect or may affect national security, shall conduct a cybersecurity review, and any online platform

operator who controls more than one million users’ personal information must undergo a cybersecurity.

On February 17, 2023, with the approval of the

State Council, the CSRC promulgated the Trial Administrative Measures of Overseas Securities Offering and Listing by Domestic Companies,

or the Trial Measures, and five supporting guidelines, which came into effect on March 31, 2023. Pursuant to the Trial Measures, (i) domestic

companies that seek to offer or list securities overseas, both directly and indirectly, shall complete filing procedures with the CSRC

pursuant to the requirements of the Trial Measures within three working days following their submission of initial public offerings or

listing applications. If a domestic company fails to complete the required filing procedures or conceals any material fact or falsifies

any major content in its filing documents, such domestic company may be subject to administrative penalties, such as an order to rectify,

warnings and fines, and its controlling shareholders, actual controllers, the person directly in charge and other directly liable persons

may also be subject to administrative penalties, such as warnings and fines; (ii) if the issuer meets both of the following criteria,

the overseas offering and listing conducted by such issuer shall be deemed an indirect overseas offering and listing by a PRC domestic

company: (A) 50% or more of any of the issuer’s operating revenue, total profit, total assets or net assets as documented in its

audited consolidated financial statements for the most recent fiscal year were derived from PRC domestic companies; and (B) the majority

of the issuer’s business activities are carried out in mainland China, or its main place(s) of business are located in mainland

China, or the majority of its senior management team in charge of its business operations and management are PRC citizens or have their

usual place(s) of residence located in mainland China. In such circumstances, where a PRC domestic company is seeking an indirect overseas

offering and listing in an overseas market, the issuer shall designate a major domestic operating entity responsible for all filing procedures

with the CSRC, and where an issuer makes an application for an initial public offering or listing in an overseas market, the issuer shall

submit filings with the CSRC within three business days after such application is submitted.

On February 24, 2023, the CSRC, together with

the MOF, National Administration of State Secrets Protection and National Archives Administration of China, revised the Provisions issued

by the CSRC and National Administration of State Secrets Protection and National Archives Administration of China in 2009. The revised

Provisions were issued under the title the “Provisions on Strengthening Confidentiality and Archives Administration of Overseas

Securities Offering and Listing by Domestic Companies,” and became effective on March 31, 2023 together with the Trial Measures.

One of the major revisions to the revised Provisions is expanding their application to cover indirect overseas offering and listing, as

is consistent with the Trial Measures. The revised Provisions require that, among other things, (a) a domestic company that plans to,

either directly or indirectly through its overseas listed entity, publicly disclose or provide to relevant individuals or entities, including

securities companies, securities service providers, and overseas regulators, any documents and materials that contain state secrets or

working secrets of government agencies, shall first obtain approval from competent authorities according to law, and file with the secrecy

administrative department at the same level; and (b) a domestic company that plans to, either directly or indirectly through its overseas

listed entity, publicly disclose or provide to relevant individuals and entities, including securities companies, securities service providers,

and overseas regulators, any other documents and materials that, if leaked, will be detrimental to national security or public interest,

shall strictly fulfill relevant procedures stipulated by applicable national regulations. As of the date of this Report, the revised Provisions

have come into effect. Any failure or perceived failure by our Company or our subsidiaries to comply with the above confidentiality and

archives administration requirements under the revised Provisions and other PRC laws and regulations may result in the relevant entities

being held legally liable by competent authorities, and referred to the judicial organ to be investigated for criminal liability if suspected

of committing a crime.

Except for the Basic Law, national laws of the

PRC do not apply in Hong Kong unless they are listed in Annex III of the Basic Law and applied locally by promulgation or local legislation.

National laws that may be listed in Annex III are currently limited under the Basic Law to those which fall within the scope of defense

and foreign affairs as well as other matters outside the limits of the autonomy of Hong Kong. National laws and regulations relating to

data protection, cybersecurity and anti-monopoly have not been listed in Annex III and do not apply directly to Hong Kong and, as such,

we are advised by our counsel as to PRC law that that the CAC and CSRC do not currently have jurisdiction over companies operating in

Hong Kong.

Our counsel as to PRC law has advised us that

that we are not currently required to obtain any permission or approval from the CSRC, the CAC or any other regulatory authority in the

PRC for our operations, the trading of our securities on the OTCQB and the offering of our securities to foreign investors. The

business of our subsidiary is not subject to cybersecurity review with the CAC, given that PRC laws on data protection and cybersecurity

do not currently apply to Hong Kong. To the extent that if we become subject to such PRC laws in the future, we do not believe we are

required to conduct a cybersecurity review because (i) we do not possess a large amount of personal information in our business operations;

and (ii) data processed in our business does not have a bearing on national security and thus may not be classified as core or important

data by the authorities. In addition, we are not subject to merger control review by China’s anti-monopoly enforcement agency as

such PRC enforcement agency does not currently have jurisdiction over our Hong Kong operating subsidiary. However, our operations could

be adversely affected, directly or indirectly, by existing or future laws and regulations relating to our business or industry, if we

inadvertently conclude that such approvals are not required when they are, or applicable laws, regulations, or interpretations change

and we are required to obtain approval in the future. We may be subject to penalties and sanctions imposed by the PRC regulatory agencies,

including the CSRC, if we fail to comply with such rules and regulations, which could adversely affect the ability of the Company’s

securities to continue to trade on the OTCQB, which may cause the value of our securities to significantly decline or become worthless.

In addition, in light of the recent statements

and regulatory actions by the PRC government, such as those related to Hong Kong’s national security, the promulgation of regulations

prohibiting foreign ownership of Chinese companies operating in certain industries, which are constantly evolving, and anti-monopoly concerns,

we may be subject to the risks of uncertainty of any future actions of the PRC government in this regard including the risk that the PRC

government could disallow our holding company structure, which may result in a material change in our operations, including our ability

to continue our existing holding company structure, carry on our current business, accept foreign investments, and offer or continue to

offer securities to our investors. These adverse actions could cause the value of our securities to significantly decline or become worthless.

There may be prominent risks associated with our

operations being in Hong Kong. For example, as a U.S.-listed public company operating primarily in Hong Kong, we may face heightened scrutiny,

criticism and negative publicity, which could result in a material change in our operations and the value of our common stock. Additionally,

we are subject to certain legal and operational risks associated with our business operations in Hong Kong, which is subject to political

and economic influence from China. PRC laws and regulations governing our current business operations are sometimes vague and uncertain,

and we may face the risk that changes in the policies of the PRC government could have a significant impact upon the business we may be

able to conduct in Hong Kong and the profitability of such business. Therefore, these risks associated with being based in or having the

majority of our operations in Hong Kong could likely cause the value of our securities to significantly decline or be worthless. Furthermore,

these risks would likely result in a material change in our business operations or a complete hinderance of our ability to offer or continue

to offer our securities to investors. Furthermore, changes in Chinese internal regulatory mandates, such as the Regulations on Mergers

and Acquisitions of Domestic Enterprises by Foreign Investors (the “M&A Rules”), the Anti-Monopoly Law, the Cybersecurity

Law and the Data Security Law, may target the Company’s corporate structure and impact our ability to conduct business in Hong Kong, accept

foreign investments, or list on an U.S. or other foreign exchange.

The U.S. government,

including the SEC, has recently made statements and taken certain actions that may lead to significant changes to U.S. and international

relations, and will impact companies with connections to the United States or China (including Hong Kong). The SEC has issued statements

primarily focused on companies with significant China-based operations. For example, on July 30, 2021, Gary Gensler, Chairman of the SEC,

issued a Statement on Investor Protection Related to Recent Developments in China, pursuant to which Chairman Gensler stated that he has

asked the SEC staff to engage in targeted additional reviews of filings for companies with significant China-based operations.

For a detailed description of the risks facing

the Company and the risks associated with having our operations in Hong Kong, please refer to “Item 1A. Risk Factors –

Risks Related to Doing Business in Hong Kong.”

Corporate History

QDM was incorporated in Florida in March 2020

as the successor to 24/7 Kid, which was incorporated in Florida in November 1998. 24/7 Kid was a telemedicine company that provided Connect-a-Doc

telemedicine kits to schools and its services aimed at providing an alternative to schools that desire to provide a higher level of healthcare

to their students but are unable to keep a full-time school nurse available.

On March 3, 2020, a stock purchase agreement (the “Purchase

Agreement”) was entered into by and between Huihe Zheng, our Chief Executive Officer and Chairman and Tim Shannon, our then controlling

stockholder as well as Chief Executive Officer, Chief Financial Officer, President and director. Pursuant to the Purchase Agreement,

Mr. Shannon sold to Mr. Zheng (i) 710,000 shares of common stock of 24/7 Kid, representing 42.6% of the total issued and outstanding

shares of common stock of 24/7 Kid as of March 9, 2020 and (ii) 13,500 shares of Series B Preferred Stock, each entitling the holder

to 100 votes on all corporate matters submitted for stockholder approval, in consideration of $500,000 in cash from Mr. Zheng’s

personal funds. The shares of common stock and Series B Preferred Stock acquired by Mr. Zheng, in the aggregate, represented 68.3% of

the outstanding voting securities of 24/7 Kid as of March 9, 2020, and the acquisition of such shares resulted in a change in control

of 24/7 Kid.

On March 11, 2020, we were incorporated in Florida

as a wholly owned subsidiary of 24/7 Kid and QDM Merger Sub, Inc. (“Merger Sub”) was incorporated in Florida as our wholly

owned subsidiary, for the purposes of effectuating a name change by implementing a reorganization of the corporate structure of 24/7 Kid

through a merger (the “Merger”). On March 13, 2020, an Agreement and Plan of Merger (the “Merger Agreement”) was

entered into by and among 24/7 Kid, the Company, and the Merger Sub. On April 8, 2020, the Articles of Merger were filed with the State

of Florida to effect the Merger as stipulated by the Merger Agreement.

Pursuant to the Merger Agreement, Merger Sub merged

with and into 24/7 Kid, with 24/7 Kid being the surviving entity. As a result, the separate corporate existence of Merger Sub ceased and

24/7 Kid became a direct, wholly-owned subsidiary of the Company. Pursuant to the Merger Agreement and as a result of the Merger, all

issued and outstanding shares of common stock and Series B Preferred Stock of 24/7 Kid were converted into shares of the Company’s

common stock and Series B Preferred Stock, respectively, on a one-for-one basis, with the Company securities having the same designations,

rights, powers and preferences and the qualifications, limitations and restrictions as the corresponding share of the securities of 24/7

Kid being converted. As a result, upon consummation of the Merger, all of the stockholders of 24/7 Kid immediately prior to the Merger

became stockholders of the Company and all the directors and officers of 24/7 Kid became the directors and officers of the Company. Upon

consummation of the Merger, we became the successor issuer to 24/7 Kid pursuant to 12g-3(a) and as a result shares of our common stock

were deemed to be registered under Section 12(g) of the Exchange Act.

On October 21, 2020, we entered into a share exchange

agreement (the “Share Exchange Agreement”) with QDM BVI, and Huihe Zheng, the sole shareholder of QDM BVI (the “QDM

BVI Shareholder”), who is also our principal stockholder and serves as our Chairman and Chief Executive Officer, to acquire all

the issued and outstanding capital stock of QDM BVI in exchange for the issuance to the QDM BVI Shareholder 900,000 shares of a newly

designated Series C Preferred Stock, with each share of Series C Preferred Stock initially being convertible into 11 shares of our common

stock, subject to certain adjustments and limitations (the transaction, the “Share Exchange”). The Share Exchange closed on

October 21, 2020. As a result of the consummation of the Share Exchange, we acquired QDM BVI, QDM HK and YeeTah, which is an insurance

brokerage company primarily engaged in the sales and distribution of insurance products in Hong Kong. Since the consummation of the Share

Exchange, we have assumed the business operations of the Group as our own.

As described above, on October 21, 2020, we acquired

all the issued and outstanding capital stock of QDM BVI pursuant to the Share Exchange Agreement and QDM BVI became our wholly owned subsidiary.

The acquisition was accounted for as a recapitalization effected by a share exchange, wherein QDM BVI is considered the acquirer for accounting

and financial reporting purposes. The assets and liabilities of QDM BVI have been brought forward at their book value and no goodwill

has been recognized.

Consequently, the assets and liabilities and the

historical operations that will be reflected in the financial statements prior to the Share Exchange will be those of the Group and will

be recorded at the historical cost basis of the Group, and the consolidated financial statements after completion of the Share Exchange

will include the assets and liabilities of the Group, historical operations of the Group, and operations of the Company and its subsidiaries

from the closing date of the Share Exchange.

As a result of the acquisition of all the issued

and outstanding capital stock of QDM BVI, we assumed the business operations of the Group as our own.

On November 3, 2021, we acquired 100% of the issued

and outstanding shares of QDMS, a company incorporated on February 6, 2020 in Cyprus. We acquired QDMS through an intermediary holding

company, LGL , which was incorporated on July 29, 2021 in the BVI. Before the acquisition, Huihe Zheng was the sole shareholder of QDMS.

As part of the acquisition, Mr. Zheng sold all the shares of QDMS to LGL for a consideration of EUR5,000 in November 2021 and at the same

time the sole shareholder of LGL, Mengting Xu, transferred all her shares in LGL to us for a consideration of USD$1.00. As a result, we

acquired a 100% ownership of LGL, which, in turn, owns 100% of QDMS. Although QDMS has no operation as of the date of this Report, QDMS

plans to engage in the research and development of CRM SaaS, with a business model derived from “customer-centered” CRM concept

to improve enterprise-customers relationship. We plan to market QDMS’ SaaS services to our network of banks, securities companies,

insurance companies and other financial services providers in Hong Kong and China.

Our

current principal offices are located at Room 1030B, 10/F, Ocean Centre, Harbour City,5 Canton Road, Tsim Sha Tsui, Kowloon, Hong Kong.

Our phone number is +852 34886893

QDM is organized under the laws of the State of

Florida as a holding company that conducts its business through a number of subsidiaries organized under the laws of foreign jurisdictions

such as Hong Kong and the BVI. This may have an adverse impact on the ability of U.S. investors to enforce a judgment obtained in U.S.

Courts against these entities, or to effect service of process on the officers and directors managing the foreign subsidiaries.

Competitive Advantages

We believe that the following competitive strengths

contribute to our growth and differentiate us from our competitors:

| |

● |

Premium Customer Service Experience. We believe providing superior customer service to our existing and potential customers is the most important aspect of our business in terms of brand building and product differentiation. We have designed our services to provide personalized customer service throughout the whole insurance purchase process, including in-depth customer needs analysis, product and plan customization, product evaluation and selection, and claim settlement related assistance. |

| |

● |

Concentrated Insurance Product Offerings. Hong

Kong’s independent insurance intermediary companies generally focus on both life insurance and property insurance, but our

strategy has been to focus on life insurance because of generally higher commissions. As of March 31, 2023, YeeTah had distributed

an aggregate of 735 life and medical insurance policies from 19 insurance companies in Hong Kong. We believe our ability to

offer concentrated products and services makes us an attractive distributor for our insurance company partners, and enables us to

provide quality service to our customers. |

| |

● |

Good Relationships with Insurance Companies. We maintain good relationships with the leading insurance companies in Hong Kong, including but not limited to, Prudential and AIA International Limited which have very stringent requirements on selection of brokers. YeeTah has been working with them for a few years and is able to pass their annual evaluations and receive favorable commission rates. |

| |

● |

Experienced Management Team in the Insurance Industry. YeeTah’s responsible officer has more than ten years of experience serving as a senior executive in the insurance industry and is familiar with the insurance intermediary industry and the regulatory environment in Hong Kong. In addition, YeeTah’s administrative manager has more than 20 years of experience in the insurance industry and ten years of management experience. |

| |

● |

Strong Commitment to Rigorous Training and Development. Given the rapid development of new insurance products and the heavy reliance on face-to-face sales efforts in Hong Kong’s insurance industry, we believe that YeeTah’s strong in-house training program, which covers both product knowledge and sales skills, gives it a competitive edge over the other professional insurance intermediaries and helps YeeTah retain its sales force and improve our sales. The training also emphasizes inculcating in YeeTah’s technical representatives our corporate culture of customer service and commitment to high ethical standards. |

Growth Strategy

Our goal is to further expand our distribution

network. To achieve this goal, we intend to capitalize on the growth potential of mainland China and Hong Kong’s insurance industry

and the insurance intermediary sector, leverage our competitive strengths and pursue the following strategy:

| |

● |

Pursue Acquisitions of Other Insurance Intermediaries. We intend to acquire suitable insurance intermediaries in mainland China in order to achieve the objective of growth and provide an area of expansion that will add to insurance product/service lines in a market that is currently not served by us. |

| |

● |

Further Participation in the Growing Life-Insurance Sector in Hong Kong. Life insurance products that require periodic premium payments have the potential to generate sustained revenue over an extended period of time. In order to take advantage of the significant growth potential of Hong Kong’s life issuance market and generate recurring income, we intend to continue to devote significant resources to growing this business line. We intend to actively recruit sales and marketing professionals to help increase sales of life insurance products in Hong Kong. We also intend to improve the productivity of individual technical representatives through rigorous training. In addition, we plan on leveraging our existing customer base to cross-sell life insurance products to our non-life insurance customers. |

| |

● |

Further Expand Our Distribution Network Through Building Relationships with Strategic Partners. The insurance intermediary sector in Hong Kong is highly competitive. We plan to grow our distribution network by building relationships with partners in mainland China that have the potential of generating large premium in sales such as financial institutes, real estate companies and other public entities and with wealth management companies, high net-worth clients and strategic partners in the Hong Kong market through recruiting and hiring more sales professionals to cover strategic partners. We believe that expanding our distribution network will help us generate more business and grow our sales. |

| |

● |

Continue to Strengthen Our Relationships with Leading Insurance Companies. We currently establish and maintain most of our business relationships with insurance companies in Hong Kong. As we plan to expand our distribution network through partners in China in an effort to increase our sales volumes in the future, we hope to obtain favorable commission rates and exclusive rights to distribute high-margin products or collaborate with our insurance company partners to custom-develop products to suit the needs of our prospective customers. |

Recent Developments

Impact of COVID-19

In 2019, an outbreak of a novel strain of the

coronavirus, COVID-19, was identified in China and has subsequently been recognized as a pandemic by the World Health Organization. The

COVID-19 pandemic has severely restricted the level of economic activity around the world. In response to this pandemic, the governments

of many countries, states, cities and other geographic regions, including Hong Kong, have taken preventative or protective actions, such

as imposing restrictions on travel and business operations and advising or requiring individuals to limit or forego their time outside

of their homes.

Due to the COVID-19 pandemic, insurance brokers

in Hong Kong have been greatly affected by the implementation of travel restrictions and social distancing measures. These restrictions

and measures have resulted in a significant decrease in new business for insurance brokers, such as YeeTah, that rely on in-person consultations

and storefronts for customer acquisition.

Customers from mainland China contributed to a

large part of YeeTah’s commissions. Regulations require their physical presence in Hong Kong to complete the policy contract. However,

due to the political turmoil and travel restrictions related to the COVID-19 epidemic, mainland Chinese customers dropped sharply. As

a result, YeeTah’s revenue from commissions on new business decreased significantly during the pandemic. YeeTah’s commissions

from renewal premiums were materially affected since the mainland Chinese customers were late in making the renewal payments due to inability

to visit Hong Kong to make the payments. Most of YeeTah’s mainland customers do not have Hong Kong bank account and used to pay

their premiums through credit card or in cash in person.

In early 2023, Hong Kong has fully reopened its

borders with mainland China. With the lifting of travel restriction, customers from mainland China can travel to Hong Kong again to meet

with insurance brokers. As a result, the Company’s revenue has significantly increased for the years ended March 31, 2023 compared

to fiscal 2022. Refer to “Results of Operations” below for details.

In May 2023, the World Health Organization declared

an end to the Covid-19 emergency.

Public Offering

In March, 2023, the Company consummated a closing

of a public offering of its common stock, par value $0.0001 per share (the “2023 Offering”), in which the Company issued and

sold an aggregate of 28,910,400 shares of its common stock at a price of $0.081 per share to certain investors, generating gross proceeds

to the Company of $2,339,937. The material terms of the 2023 Offering are described in the prospectus, dated January 27, 2023, filed by

the Company with the SEC on February 01, 2023, pursuant to Rule 424(b) under the Securities Act. The Offering is registered pursuant to

the Company’s Registration Statement on Form S-1 (Registration No. 333-267263), originally filed with the SEC on September 2, 2022

(as amended, the “Registration Statement”), which was declared effective by the SEC on January 27, 2023.

Change of Principal Office

Our principal executive office changed from Room

715, 7F, The Place Tower C, No. 150 Zunyi Road, Changning District, Shanghai, China to our current principal office, which are located

at Room 1030B, 10/F, Ocean Centre, Harbour City,5 Canton Road, Tsim Sha Tsui, Kowloon, Hong Kong. Our current phone number is + 85234886893.

The Hong Kong Insurance Market

Hong Kong has one of the most developed insurance

markets in Asia, with the per capita insurance premium standing at high levels and has attracted many of the world’s top insurance

companies. According to the Statistical Highlights issued by Research Office of the Legislative Council Secretariat on May 10, 2019, the

Hong Kong insurance industry has shown a considerable growth in recent years. In 2018, the total gross premiums of the industry were about

HK$531.7 billion (approximately $68.17 billion), representing an increase of 78% over 2013, primarily as a result of an increase of 86%

in long term business (e.g., life and annuity), which we believe might be indicative of the increasing demand for long term insurance

products due to aging population.

As of March 31, 2023,

there were 164 authorized insurers in Hong Kong, of which 89 were pure general insurers, 53 were pure long term insurers, 19 were composite

insurers and 3 were special purpose insurers; furthermore, there were 1,733 licensed insurance agencies, 79,323 licensed individual insurance

agents and 24,060 licensed technical representatives (agent). In addition, there were 817 licensed insurance broker companies and

10,624 licensed technical representatives (broker) on the same date. In 2021, the total gross premiums of the Hong Kong insurance industry

increased by 0.06% to $581.7 billion.

Market Potential and Recent Trends

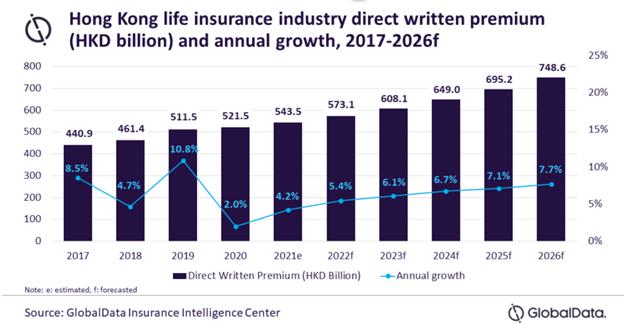

Life insurance industry in Hong Kong is forecasted

by Global data to reach US $96.5 billion in 2026. Hong Kong life insurance industry is projected to grow at a compound annual growth rate

(CAGR) of 6.6% from HKD543.5b billion (approximately US$70.0 billion) in 2021 to HKD748.6 billion (approximately $US 96.5 billion) in

2026, in terms of direct written premiums (“DWP”), according to GlobalData.

Whole life insurance was the largest segment

with a DWP share of 64.8% in 2020. It declined by 1.1% in 2020 due to the COVID-19 pandemic-led travel restrictions. Prior to the pandemic,

a large proportion of whole life insurance premiums were attributed to Chinese visitors, who purchased their policies from Hong Kong due

to favorable terms and greater flexibility offered to them as compared to policies sold in China. Endowment insurance was the second-largest

line with a 13.4% share in 2020. It grew by 17.5% in 2020, driven by strong demand for high return insurance policies. The introduction

of investment-linked insurance with high mortality coverage is expected to support the demand for endowment products. Endowment insurance

is expected to grow at a CAGR of 9.9% during 2021-2026.

General annuity, which is the third-largest line with a DWP share of

9.3%, was declined by 16.2% in 2020. It is expected to grow at a CAGR of 6.3% during 2021-2026, driven by the demographic factors such

as higher life expectancy. In addition, the introduction of tax benefits on Qualified Deferred Annuity Policies in September 2021 will

further support the demand for annuity products. Term life, pension, and other life insurance lines accounted for the remaining 12.5%

share. Hong Kong’s life insurance market is expected to be the third-highest in the Asia-Pacific region, after India and China,

with a projected CAGR of 6.6% during 2021 to 2026. Gradual resumption in economic activities and increase in the sale of life insurance

policies to mainland Chinese visitors are expected to support the growth of Hong Kong life insurance market over the next five years.

Products and Services

We market and sell two broad categories of insurance

products: (1) life and medical insurance products, and (2) general insurance products. As of the date of this Report, insurance products

we sell are underwritten by 19 insurance companies in Hong Kong. In addition, as an MPF Intermediary, we also assist our customers with

their investment through the MPF and the ORSO schemes in Hong Kong. Such services primarily include collection and provision of information

on investment products and exclude investment advisory services.

Life and Medical Insurance Products

Our life and medical

insurance products collectively accounted for approximately 99.49% and 92.7% of our net revenues for the fiscal years ended March 31,

2023 and 2022, respectively. For life and medical insurance products purchased by our customers, we generally receive commissions in the

range of 2.72% to 168% of the first year premiums and in the range of 0% to 49.5% of renewal premiums.

The sale of life and medical insurance products

is, and we currently expect it to continue to be, the major source of our revenue in the next several years. We began offering life insurance

products in 2015 with a focus on individual life products with periodic payment schedules. The major life and medical insurance products

we sell can be broadly classified into the categories set forth below. Due to constant product innovation by insurance companies, some

of the insurance products we sell combine features of one or more of the categories listed below:

| |

● |

Individual Health Insurance. The individual health insurance products we sell primarily consist of critical illness insurance products, which provide guaranteed benefits when the insured is diagnosed with specified serious illnesses, and medical insurance products, which provide conditional reimbursement for medical expenses during the coverage period. In return, the insured makes periodic payment of premiums over a pre-determined period. |

| |

● |

Individual Annuity. The individual annuity products we sell generally provide annual benefit payments after the insured attains a certain age, or for a fixed time period, and provide a lump sum payment at the end of the coverage period. In addition, the beneficiary designated in the annuity contract will receive guaranteed benefits upon the death of the insured during the coverage period. In return, the purchaser of the annuity products makes periodic payments of premiums during a pre-determined accumulation period. |

| |

● |

Individual Endowment Life Insurance. The individual endowment products we sell generally provide insurance coverage for the insured for a specified time period and maturity benefits if the insured reaches a specified age. The individual endowment products we sell also provide to a beneficiary designated by the insured guaranteed benefits upon the death of the insured within the coverage period. In return, the insured makes periodic payment of premiums over a pre-determined period. |

We believe due to mainland

China and Hong Kong’s rapidly aging population, high national savings rate, sustained economic development, rising household income,

strong support from government policies and regulations, and enhanced risk protection awareness, Hong Kong’s life and medical insurance

sector will experience faster growth than the other insurance sectors, and currently we plan to allocate greater resources to develop

our life and medical insurance business.

General Insurance Products

Our general insurance

products, also known as property and casualty insurance products, accounted for approximately 0.51% and 7.3% of our net revenues for

the fiscal years ended March 31, 2023 and 2022, respectively. For general insurance products purchased by our customers, we generally

receive commissions from the insurance companies in the range of 5.0% - 55.0% of the premiums. The major general insurance products we

offer or facilitate to individual customers can be further classified into the following categories:

| |

● |

Individual Accident Insurance. The individual accident insurance products we sell generally provide a guaranteed benefit during the coverage period in the event of death or disability of the insured as a result of an accident, or a reimbursement of medical expenses to the insured in connection with an accident. These products typically require only a single premium payment for each coverage period. Because most of the individual accident insurance products we sell are underwritten by general insurance companies, we classify individual accident insurance products as general insurance products. |

| |

● |

Travel Insurance. The travel insurance products we sell are short-term insurance providing guaranteed benefit in the event of death or disability and covering travel-related emergencies and losses, either within one’s own country, or internationally. These products typically require only a single premium payment for each coverage period. |

| |

● |

Homeowner Insurance. The homeowner insurance products we sell primarily cover damages to the insured house, along with furniture and household electrical appliance in the house caused by a number of incidents such as fire, flood and explosion. |

| |

● |

Auto Insurance. We facilitate both standard auto insurance policies and supplemental policies, which we refer to as riders. The standard auto insurance policies we facilitate generally have a term of one year and cover damages caused to the insured vehicle by collision and other traffic accidents, falling or flying objects, fire, explosion and natural disasters. We also facilitate standard third-party liability insurance policies, which cover bodily injury and property damage caused by an accident involving an insured vehicle to a person not in the insured vehicle. The riders we facilitate cover additional losses, such as liability to passengers, losses arising from vehicle theft and robbery, broken glass and vehicle body scratches. |

MPF and ORSO Services

The MPF is a compulsory saving scheme (pension fund) for the retirement

of residents in Hong Kong. Most employees and their employers are required to contribute monthly to the MPF schemes provided by approved

private organizations based on the salary and period of employment of the employee. ORSO schemes are retirement schemes set up voluntarily

by employers to provide retirement benefits for their employees. MPF is the mainstream retire plan in Hong Kong. We introduce customers

to the service providers of the MPF and ORSO schemes approved by MPF as trustees to administer the MPF and ORSO schemes. As of March 31,

2023, there were a total 12 approved trustees in Hong Kong, of which, four have signed agreements with us in connection with its provision

of MPF and ORSO related services. We assist employees who are Hong Kong residents to open personal accounts with a new approved trustee

and employers in Hong Kong to set up corporate accounts. We receive service fees in the range of 1.0% - 5.0% of the total investment transferred

by an employee/employer to the new trustee and are paid by the trustee once the transaction is completed. We assisted an aggregate of

44 customers with account opening and transfer of funds through the MPF scheme since inception.

Distribution Network and Marketing

We rely on our technical representatives to market

and sell insurance products in Hong Kong. As of March 31, 2023, we had six technical representatives in Hong Kong. YeeTah was a party

to an agreement with YeeTah Financial Group Co., Ltd. (“YeeTah Financial”), a company controlled by its former officer and

director, which referred customers, most of whom were mainland visitors, to YeeTah for the purchase of insurance products in Hong Kong

in exchange for certain fees paid by YeeTah out of its commissions earned through the insurance policies purchased by the referred customers.

Customers

From March 2017 to March 31, 2023, the total number

of our individual customers grew from 329 to 679. By providing premium customer services to our customers, we also strive to build