UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM

8-K

CURRENT

REPORT

Pursuant

to Section 13 or 15(d) of the

Securities

Exchange Act of 1934

Date

of Report (Date of earliest event reported): January 30, 2024

SOUTHERN

CALIFORNIA BANCORP

(Exact

name of registrant as specified in its charter)

| California |

|

001-41684 |

|

84-3288397 |

(State

or other jurisdiction

of

incorporation) |

|

(Commission

File

Number) |

|

(IRS

Employer

Identification

Number) |

| 12265

El Camino Real, Suite 210 |

|

|

| San

Diego, California |

|

92310 |

| (Address

of Principal Executive Offices) |

|

(Zip

Code) |

(844)

265-7622

(Registrant’s

Telephone Number, Including Area Code)

N/A

(Former

name or former address, if changed since last report.)

Check

the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under

any of the following provisions:

| ☒ |

Written

communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| |

|

| ☐ |

Soliciting

material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| |

|

| ☐ |

Pre-commencement

communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| |

|

| ☐ |

Pre-commencement

communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Securities

registered pursuant to Section 12(b) of the Act:

| Title

of each class |

|

Trading

Symbol(s) |

|

Name

of each exchange on which registered |

| Common

Stock |

|

BCAL |

|

The

Nasdaq Stock Market LLC |

Indicate

by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405

of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging

growth company ☒

If

an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☒

| Item 2.02 |

Results of Operations and Financial Condition |

On

January 30, 2024, Southern California Bancorp (the “Company”) issued an earnings release reporting its consolidated financial

results as of and for the fourth quarter and the full year of 2023. A copy of that earnings release is furnished as Exhibit 99.1 hereto.

| Item 7.01 | Regulation FD Disclosure |

A

copy of a slide presentation that the Company may use for upcoming meetings with investors and other interested parties is furnished

as Exhibit 99.2 hereto. Additionally, the Company has posted the slide presentation in the Investor Relations section of its website

at https://investor.banksocal.com. Information obtained or linked to the foregoing website shall not be deemed to be included in this

Current Report on Form 8-K.

In

accordance with General Instruction B.2 of Form 8-K, the information contained in this Current Report on Form 8-K, including Exhibit

99.1 and Exhibit 99.2, is being furnished and shall not be deemed “filed” for purposes of Section 18 of the Securities Exchange

Act of 1934, as amended (the “Exchange Act”), nor shall such information be deemed incorporated by reference into any filing

under the Securities Act of 1933, as amended, or the Exchange Act, except as shall be expressly set forth by specific reference in such

filing..

| Item 9.01 | Financial Statements and Exhibits. |

SIGNATURES

Pursuant

to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by

the undersigned hereunto duly authorized.

| |

SOUTHERN

CALIFORNIA BANCORP |

| |

|

| Date:

January 30, 2024 |

By: |

/s/

DAVID I. RAINER |

| |

|

David

I. Rainer |

| |

|

Chief

Executive Officer |

Exhibit

99.1

SOUTHERN

CALIFORNIA BANCORP REPORTS NET INCOME OF

$4.4 MILLION FOR THE FOURTH QUARTER AND $25.9 MILLION FOR THE FULL YEAR OF 2023

—

The Company Also Announced in a Separate Release that it has Entered into a Merger Agreement

with California BanCorp

San

Diego, Calif., January 30, 2024 – Southern California Bancorp (“us,” “we,” “our,” or the

“Company”) (NASDAQ: BCAL), the holding company for Bank of Southern California, N.A. (the “Bank”) announces its

consolidated financial results for the fourth quarter and full year of 2023.

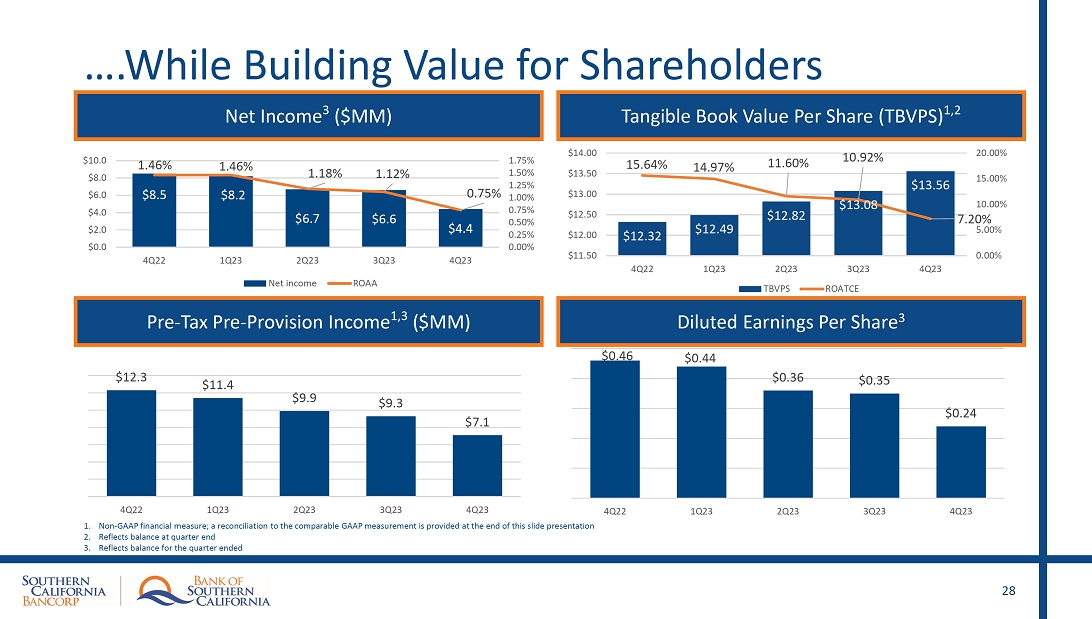

Southern

California Bancorp reported net income of $4.4 million for the fourth quarter of 2023, or $0.24 per diluted share, compared to net income

of $8.5 million, or $0.46 per diluted share in the fourth quarter of 2022, and net income of $6.6 million, or $0.35 per diluted share

in the third quarter of 2023. The Company reported net income of $25.9 million for the full year of 2023, or $1.39 per diluted share,

compared to net income of $16.1 million, or $0.88 per diluted share for the full year of 2022.

“I’m

pleased to report our 2023 full year results show strong growth over 2022, with 2023 net income of $25.9 million increasing $9.8 million

or 61% from the prior year, and earnings per share of $1.39 increasing 57% over the prior year,” said David Rainer, Chairman and

CEO of Southern California Bancorp and Bank of Southern California. “Our return on average assets of 1.12% grew significantly from

0.70% in the prior year and our net interest margin expanded to 4.33% from 4.06%, despite pressure from the industry-wide increase in

the cost of funds, the effects of which were somewhat offset by the Bank’s increased loan yield of 5.94% for 2023, up from 5.02%

for the prior year.

“The

highlights of our fourth quarter results include total loan growth of $29.4 million and an increase in tangible book value per share

(non-GAAP1) of $0.48 to $13.56, an increase of 3.7% from the prior quarter. Our fourth quarter results were impacted by a

$1 million pre-tax loss on the sale of securities yielding 2.4%, the proceeds of which were redeployed into securities yielding 4.7%,

which will add to future interest income and provide some protection if interest rates decrease. The fourth quarter was also impacted

by a $1.3 million charge-off for a nonaccrual loan we reported in the prior quarter, which was the result of a new appraisal of the collateral

backing the loan.

“We

are very excited about the merger with California BanCorp and California Bank of Commerce, which was jointly announced this morning.

We believe it will be beneficial for both companies’ shareholders, as well as our clients and employees, and I look forward to

working with California BanCorp Chief Executive Officer Steven Shelton and his team as we integrate our operations into one organization.”

Fourth

Quarter 2023 Highlights

| ● | Net

income of $4.4 million, compared with $6.6 million in the prior quarter |

| ● | Diluted

earnings per share of $0.24, compared with $0.35 in the prior quarter |

| ● | Net

interest margin of 4.05%, compared with 4.23% in the prior quarter; average loan yield

of 6.08% compared with 5.97% in the prior quarter |

| ● | Return

on average assets of 0.75%, compared with 1.12% in the prior quarter |

1

Reconciliations of the non–U.S. generally accepted accounting principles (“GAAP”) measures are set forth at the

end of this press release.

| ● | Return

on average common equity of 6.21%, compared with 9.38% in the prior quarter |

| ● | Efficiency

ratio (non-GAAP1) of 68.3%, compared with 61.4% in the prior quarter |

| ● | Tangible

book value per common share (“TBV”) (non-GAAP1) of $13.56 at December

31, 2023, up $0.48 from $13.08 at September 30, 2023 |

| ● | Total

assets of $2.36 billion at December 31, 2023, compared with $2.31 billion at September

30, 2023 |

| ● | Total

loans, including loans held for sale of $1.96 billion at December 31, 2023, compared

with $1.94 billion at September 30, 2023 |

| ● | Nonperforming

assets to total assets ratio of 0.55% at December 31, 2023, compared with 0.62% at September

30, 2023 |

| ● | Total

deposits of $1.94 billion at December 31, 2023, decreased $40.3 million or 2.0%, compared

with $1.98 billion at September 30, 2023 |

| ● | Noninterest-bearing

demand deposits were $675.1 million at December 31, 2023, representing 34.7% of total

deposits, compared with $736.0 million, or 37.1% of total deposits at September 30, 2023 |

| ● | Cost

of deposits was 1.81%, compared with 1.56% in the prior quarter |

| ● | Cost

of funds was 1.95%, compared with 1.62% in the prior quarter |

| ● | Bank’s

capital exceeds minimums to be “well-capitalized,” the highest regulatory

capital category |

Full

Year 2023 Highlights

| ● | Net

income increased to $25.9 million, up $9.8 million, or 60.8% from the prior year |

| ● | Diluted

earnings per share of $1.39, up $0.51, or 57.2% from the prior year |

| ● | Total

loan interest income increased to $114.0 million, up $27.6 million or 31.9% from the

prior year |

| ● | Net

interest margin of 4.33% for 2023, compared with 4.06% in the prior year; average loan

yield was 5.94%, up from 5.02% in the prior year |

| ● | Efficiency

ratio (non-GAAP1) of 61.3%, improved from 69.5% in the prior year |

| ● | Provision

for credit losses of $915 thousand under the Current Expected Credit Loss (“CECL”)

model, the provision was $6.0 million under the incurred loss model for the year ended December

31, 2022 |

| ● | Total

assets of $2.36 billion, up $76.3 million or 3.3% from December 31, 2022 |

| ● | Total

loans, including loans held for sale, increased to $1.96 billion, up $58.0 million from

December 31, 2022 |

| ● | Total

deposits of $1.94 billion, up $11.7 million from December 31, 2022 |

| ● | Noninterest

bearing demand deposits were $675.1 million, representing 34.7% of total deposits, compared

to $923.9 million, or 47.8% of total deposits at December 31, 2022 |

| ● | Cost

of deposits was 1.37%, up from 0.23% in the prior year |

| ● | Tangible

book value per common share (“TBV”) (non-GAAP1) of $13.56 at December

31, 2023, up $1.24 from December 31, 2022 |

Fourth

Quarter Operating Results

Net

Income

Net

income for the fourth quarter of 2023 was $4.4 million, or $0.24 per diluted share, compared with net income of $6.6 million, or $0.35

per diluted share in the third quarter of 2023. Pre-tax, pre-provision income (non-GAAP) for the fourth quarter was $7.1 million, a decrease

of $2.2 million or 23.4% from the prior quarter.

Net

Interest Income and Net Interest Margin

Net

interest income for the fourth quarter of 2023 was $22.6 million, compared to $23.3 million in the prior quarter. The decrease in net

interest income was primarily due to a $1.8 million increase in total interest expense, partially offset by a $1.1 million increase in

total interest and dividend income in the fourth quarter of 2023 as compared to the prior quarter. During the fourth quarter of 2023,

loan interest income increased $1.0 million, total debt securities income increased $43 thousand, and interest and dividend income from

other financial institutions increased $51 thousand. The increase in interest income was due to a number of factors: a higher average

total loan balance from organic loan growth; a change in the interest-earning asset mix; and higher loan yields resulting from the benefit

of variable rate interest-earning loans repricing for the first time since the start of the rising interest rate environment. Additionally,

in the prior quarter we recorded a reversal of a non-accrual loan’s interest income of $264 thousand for which there was no significant

reversal of interest income in the current quarter. Average interest-earning assets increased $25.5 million, the result of a $30.0 million

increase in average total loans, a $5.9 million increase in average deposits in other financial institutions, a $1.1 million increase

in average total debt securities, and a $29 thousand increase in average restricted stock investments and other bank stock, partially

offset by a $11.6 million decrease in average Fed funds sold/resale agreements. The increase in interest expense for the fourth quarter

of 2023 was primarily due to a $639 thousand increase in interest expense on Federal Home Loan Bank (FHLB) borrowings, and a $1.1 million

increase in interest expense on interest-bearing deposits, the result of a $27.6 million increase in average interest-bearing deposits,

coupled with a 31 basis point increase in interest-bearing deposit costs.

Net

interest margin for the fourth quarter of 2023 was 4.05%, compared with 4.23% in the prior quarter. The decrease was primarily related

to a 33 basis point increase in the cost of funds, partially offset by a 13 basis point increase in the total interest-earning assets

yield, which was the result of higher market interest rates and a change in the Bank’s average interest-earning asset mix. The

yield on total average earning assets in the fourth quarter of 2023 was 5.85%, compared with 5.72% in the prior quarter. The yield on

average total loans in the fourth quarter of 2023 was 6.08%, an increase of 11 basis points from 5.97% in the prior quarter. The yield

on average total loans in the prior quarter included the impact of the reversal of a non-accrual loan’s interest, which decreased

the overall loan yield by 5 basis points. There was no significant reversal of interest income in the fourth quarter of 2023.

Cost

of funds for the fourth quarter of 2023 was 195 basis points, an increase of 33 basis points from 162 basis points in the prior quarter.

The increase was primarily driven by a 31 basis point increase in the cost of interest-bearing deposits, a 13 basis point increase in

the cost of FHLB borrowings, an increase in average interest-bearing deposits, and a decrease in average noninterest-bearing deposits.

Average noninterest-bearing demand deposits decreased $47.0 million to $721.2 million and represented 36.8% of total average deposits

for the fourth quarter of 2023, compared with $768.1 million and 38.8%, respectively, in the prior quarter; average interest-bearing

deposits increased $27.6 million to $1.24 billion during the fourth quarter of 2023. The total cost of deposits in the fourth quarter

of 2023 was 181 basis points, an increase of 25 basis points from 156 basis points in the prior quarter.

Average

total borrowings increased $44.7 million to $74.2 million for the fourth quarter of 2023, primarily due to an increase of $44.6 million

in average FHLB borrowings during the quarter. The average cost of total borrowings was 5.73% for the fourth quarter of 2023, down from

5.82% in the prior quarter.

Provision

for Credit Losses

The

Company recorded a provision for credit losses of $824 thousand in the fourth quarter of 2023, compared to a reversal of provision for

credit losses of $96 thousand in the prior quarter. The provision for credit losses in the fourth quarter of 2023 included a $307 thousand

negative provision for unfunded loan commitments primarily due to lower unfunded loan commitments. Total unfunded loan commitments decreased

$79.6 million to $410.8 million at December 31, 2023, from $490.4 million at September 30, 2023. The provision for credit losses for

the loan portfolio in the fourth quarter of 2023 was $1.1 million, an increase of $929 thousand from $202 thousand in the prior quarter.

The increase was driven primarily by an increase in net charge-offs, loan growth, an increase in substandard accruing loans and changes

in the portfolio mix, partially offset by an improvement in the reasonable and supportable forecast, primarily related to the economic

outlook from the Federal Reserve’s actions to control inflation, and a decrease in special mention loans. The Company’s management

continues to monitor macroeconomic variables related to increasing interest rates, inflation and the concerns of an economic downturn,

and believes it is appropriately provisioned for the current environment.

Noninterest

(Loss) Income

The

Company recorded a loss on noninterest income of $102 thousand in the fourth quarter of 2023, a decrease of $917 thousand compared to

total noninterest income of $815 thousand in the third quarter of 2023. In the fourth quarter of 2023, the Company recorded a loss on

sale of available-for-sale debt securities of $1.0 million in order to redeploy the proceeds into higher-yielding available-for-sale

debt securities, for which there was no comparable transaction in the third quarter of 2023. There was no gain on SBA 7A loan sales in

the fourth quarter and third quarter of 2023 primarily due to unattractive pricing in the secondary market.

Noninterest

Expense

Total

noninterest expense for the fourth quarter of 2023 was $15.3 million, an increase of $558 thousand from total noninterest expense of

$14.8 million in the prior quarter. In the fourth quarter of 2023, occupancy and equipment expenses increased by $99 thousand, legal,

audit and professional fees increased by $563 thousand, and other expenses increased by $125 thousand, partially offset by decreases

in salaries and employee benefits of $138 thousand.

The

$99 thousand increase in occupancy and equipment expenses was due primarily to an impairment charge related to the right-of-use asset

associated with a Company lease. The $563 thousand increase in legal, audit and professional fees was due primarily to an increase in

legal expenses and consulting expenses related to compliance projects and loan review projects. The $125 thousand increase in other expense

was due primarily to the increase in loan related expense. The $138 thousand decrease in salaries and benefits was due primarily to a

decrease in stock-based compensation expense resulting from the forfeitures for employee separation, partially offset by a decrease in

the deferred loan origination costs in the fourth quarter of 2023.

Efficiency

ratio (non-GAAP1) for the fourth quarter of 2023 was 68.3%, compared to 61.4% in the prior quarter.

Income

Tax

In

the fourth quarter of 2023, the Company’s income tax expense was $1.9 million, compared with $2.8 million in the third quarter

of 2023. The effective rate was 29.9% for the fourth quarter of 2023 and 30.2% for the third quarter of 2023. The effective rate was

29.7% for the year ended December 31, 2023. The decrease in the effective tax rate for the fourth quarter of 2023 was primarily attributable

to the impact of the vesting and exercise of equity awards combined with changes in the Company’s stock price over time, and other

deferred tax related adjustments.

Balance

Sheet

Assets

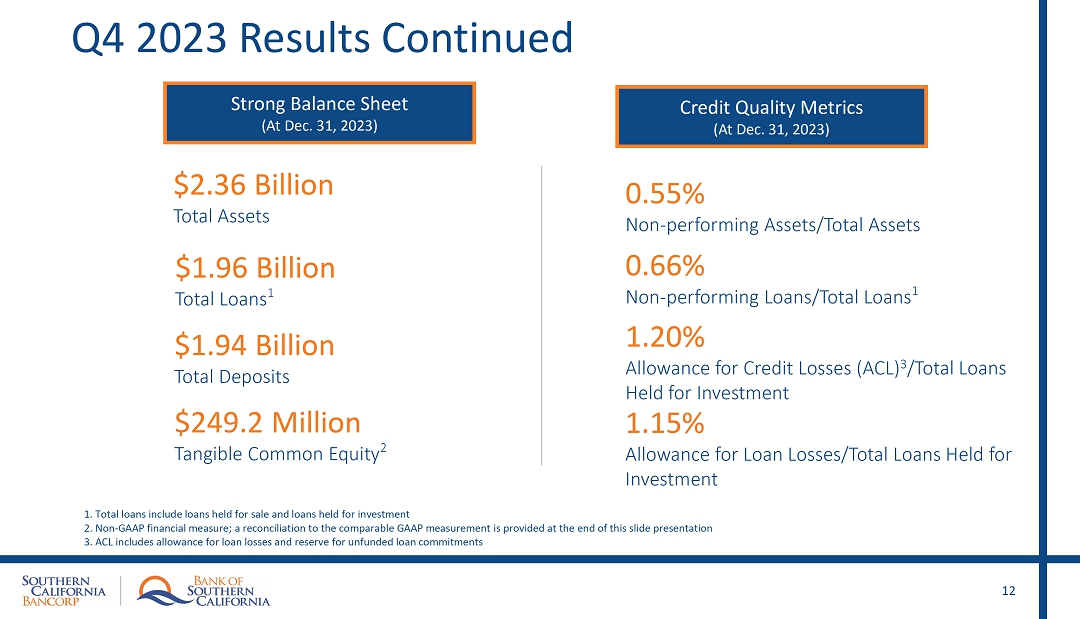

Total

assets at December 31, 2023 were $2.36 billion, an increase of $46.6 million or 2.0% from September 30, 2023. The increase in total assets

from the prior quarter was primarily related to a $29.4 million increase in total loans, including loans held for sale, a $18.2 million

increase in available-for-sale debt securities, and a $9.9 million increase in income tax receivable recorded in accrued interest and

other assets, partially offset by a $8.3 million decrease in cash and cash equivalents, and a $1.4 million decrease in deferred taxes,

net.

Loans

Total

loans held for investment were $1.96 billion at December 31, 2023, compared to $1.93 billion at September 30, 2023, with fourth quarter

of 2023 new originations of $34.0 million and net advances of $40.1 million, partially offset by payoffs of $45.9 million, and a charge-off

of $1.3 million. Total loans secured by real estate increased by $16.1 million, with construction and land development loans increasing

by $6.2 million, commercial real estate and other loans increasing by $4.6 million, and multifamily loans increasing by $3.1 million,

1-4 family residential loans increasing by $2.2 million, and consumer loans increasing by $1.6 million. The Company had $7.3 million

in SBA 7A loans held for sale at December 31, 2023, compared to $4.8 million at September 30, 2023.

Deposits

Total

deposits at December 31, 2023 were $1.94 billion, a decrease of $40.3 million from September 30, 2023. Noninterest-bearing demand deposits

at December 31, 2023, were $675.1 million, or 34.7% of total deposits, compared with $736.0 million, or 37.1% of total deposits at September

30, 2023. At December 31, 2023, total interest-bearing deposits were $1.27 billion, compared to $1.25 billion at September 30, 2023.

At December 31, 2023, total brokered time deposits were $107.8 million, compared to $84.5 million at September 30, 2023. Given the nature

of the Company’s commercial banking model, at December 31, 2023, approximately 42% of total deposits exceeded the FDIC insurance

limits. The Company offers the Insured Cash Sweep (ICS) product, providing customers with FDIC insurance coverage at ICS network institutions.

At December 31, 2023, ICS deposits were $274.1 million, or 14.1% of total deposits, compared to $252.7 million, or 12.7% of total deposits

at September 30, 2023.

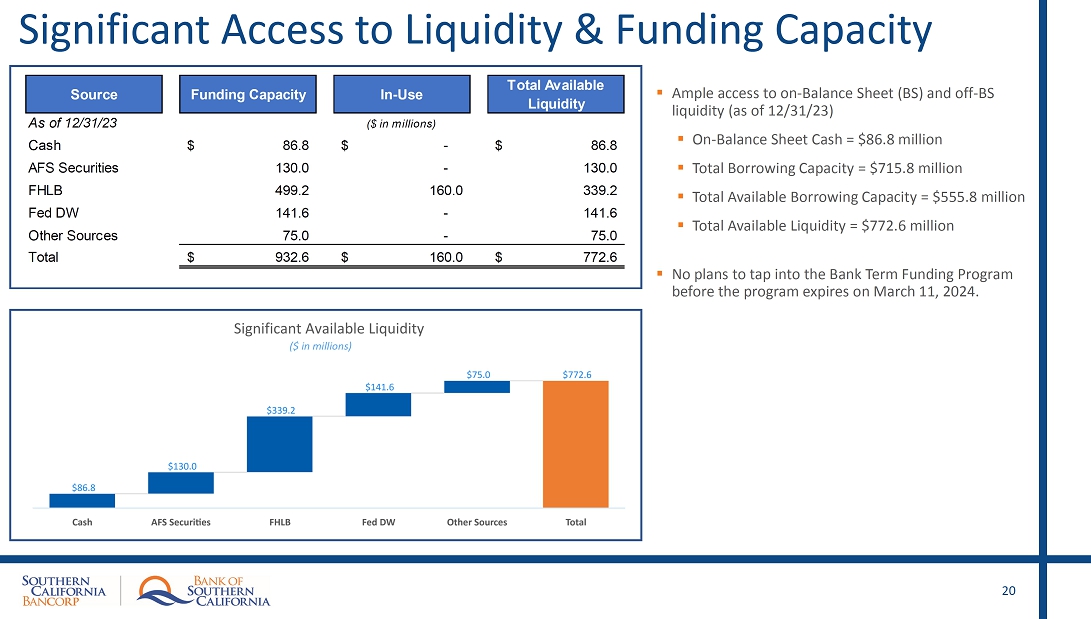

Federal

Home Loan Bank (“FHLB”) and Liquidity

At

December 31, 2023, the Company had overnight FHLB borrowings of $85.0 million, a $77.0 million increase from September 30, 2023. There

were no outstanding Federal Reserve Discount Window borrowings at December 31, 2023 or September 30, 2023, and the Company has not participated

in the Federal Reserve Bank Term Funding Program.

At

December 31, 2023, the Company had available borrowing capacity from the FHLB secured line of credit of approximately $339.2 million

and available borrowing capacity from the Federal Reserve Discount Window of approximately $141.6 million. The Company also had available

borrowing capacity from three unsecured credit lines from correspondent banks of approximately $75.0 million at December 31, 2023, with

no outstanding borrowings. Total available borrowing capacity was $555.8 million at December 31, 2023. Additionally, the Company had

unpledged liquid securities at fair value of approximately $130.0 million and cash and cash equivalents of $86.8 million at December

31, 2023.

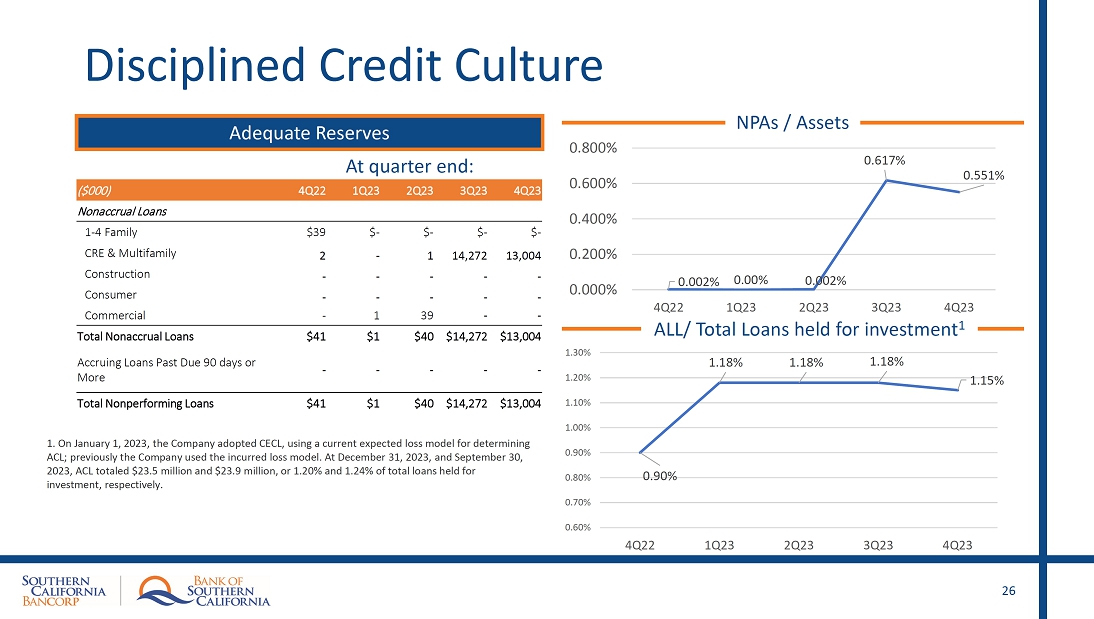

Asset

Quality

Total

non-performing assets decreased to $13.0 million, or 0.55% of total assets at December 31, 2023, compared with $14.3 million, or 0.62%

of total assets at September 30, 2023. The decrease from September 30, 2023, was primarily due to a $1.3 million charge-off for a non-accrual

multifamily loan with a net carrying value before charge-off of $14.3 million during the fourth quarter of 2023. The non-accrual multifamily

loan added to non-accrual loans during the third quarter of 2023 is collateralized by three investment multifamily properties located

in the city of Santa Monica, California. A court appointed receiver is in place and the Company is aggressively pursuing the resolution

of this matter. During the fourth quarter of 2023, the Company received the updated appraisals for the three multifamily properties;

the combined “As-Is” collateral value, after accounting for estimated selling costs, the estimated net collateral value was

$1.3 million lower than the subject loan’s net carrying value resulting in a partial charge-off in the fourth quarter of 2023.

Special mention loans decreased by $289 thousand during the fourth quarter of 2023 to $3.0 million at December 31, 2023, due mostly to

two commercial and industrial loans from one relationship with a net carrying value of $425 thousand that were upgraded from special

mention loans to pass loans. Substandard accruing loans increased by $3.0 million during the fourth quarter of 2023 to $6.5 million at

December 31, 2023 due mostly to a commercial and industrial loan from one relationship with a net carrying value of $3.1 million that

was downgraded from a pass loan, partially offset by payoffs and net paydowns.

The

Company had no loans over 90 days past due that were accruing interest at December 31, 2023, and September 30, 2023.

There

were $19 thousand of loan delinquencies (30-89 days past due) related to a Paycheck Protection Program loan at December 31, 2023, compared

to $96 thousand loan delinquencies (30-89 days past due) at September 30, 2023.

The

allowance for credit losses, which is comprised of allowance for loan losses (ALL) and reserve for unfunded loan commitments, totaled

$23.5 million, or 1.20% of total loans held for investment at December 31, 2023, compared to $23.9 million, or 1.24% at September 30,

2023. The $443 thousand decrease in the allowance included a $1.1 million provision for credit losses for the loan portfolio, partially

offset by a net charge-off of $1.3 million, and a $307 thousand negative credit provision for unfunded loan commitments for the quarter

ended December 31, 2023.

The

allowance for loan losses was $22.6 million, or 1.15% of total loans held for investment at December 31, 2023, compared to $22.7 million,

or 1.18% at September 30, 2023.

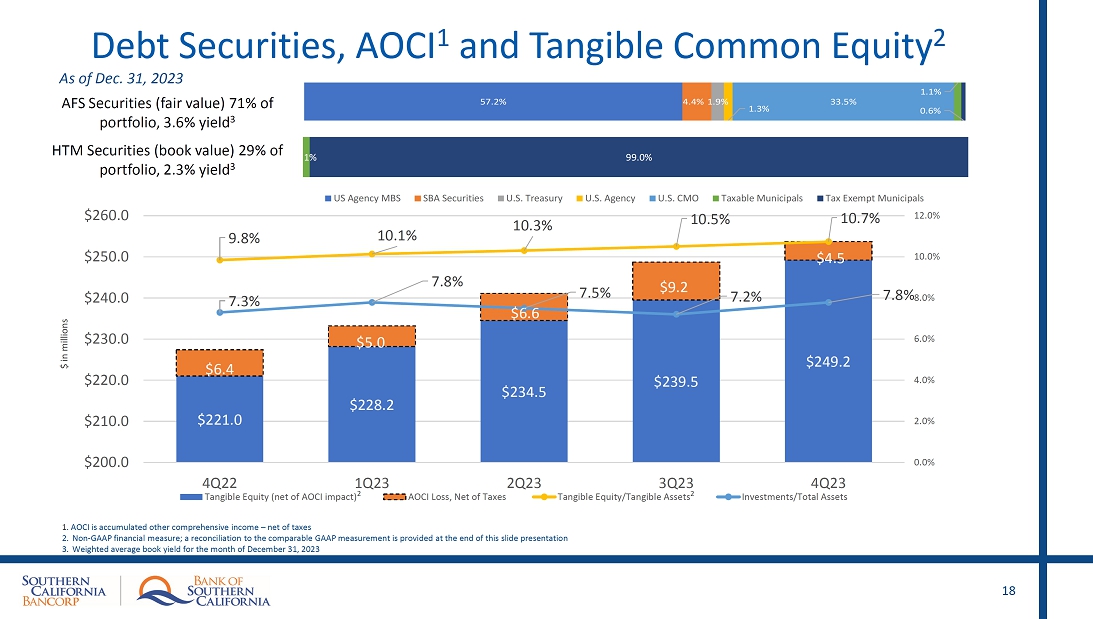

Capital

Tangible

book value (non-GAAP) per common share at December 31, 2023, was $13.56, compared with $13.08 at September 30, 2023. In the fourth quarter

of 2023, tangible book value was primarily impacted by net income, stock-based compensation expense, and a decrease in net of tax unrealized

losses on available-for-sale debt securities. Other comprehensive losses related to unrealized losses, net of taxes, on available-for-sale

debt securities decreased by $4.7 million to $4.5 million at December 31, 2023 from $9.2 million at September 30, 2023. The decrease

in the unrealized losses, net of taxes, on available-for-sale debt securities was primarily attributable to factors other than credit

related, including changes in interest rates driven by the Federal Reserve’s policy to fight inflation, and general volatility

in credit market conditions. Tangible common equity (non-GAAP) as a percent of total tangible assets (non-GAAP) at December 31, 2023

increased to 10.73% from 10.53% in the prior quarter, and unrealized losses as a percent of tangible common equity (non-GAAP) at December

31, 2023 decreased to 1.8% from 3.9% in the prior quarter.

The

Bank’s leverage capital ratio and total risk-based capital ratio were 11.65% and 13.51%, respectively, at December 31, 2023. The

Bank elected the three-year phase-in period under the regulatory capital rules, which allow a phase-in of the Day 1 CECL transition adjustment

to the regulatory capital at 25% per year over a three-year transition period.

ABOUT

SOUTHERN CALIFORNIA BANCORP AND BANK OF SOUTHERN CALIFORNIA, N.A.

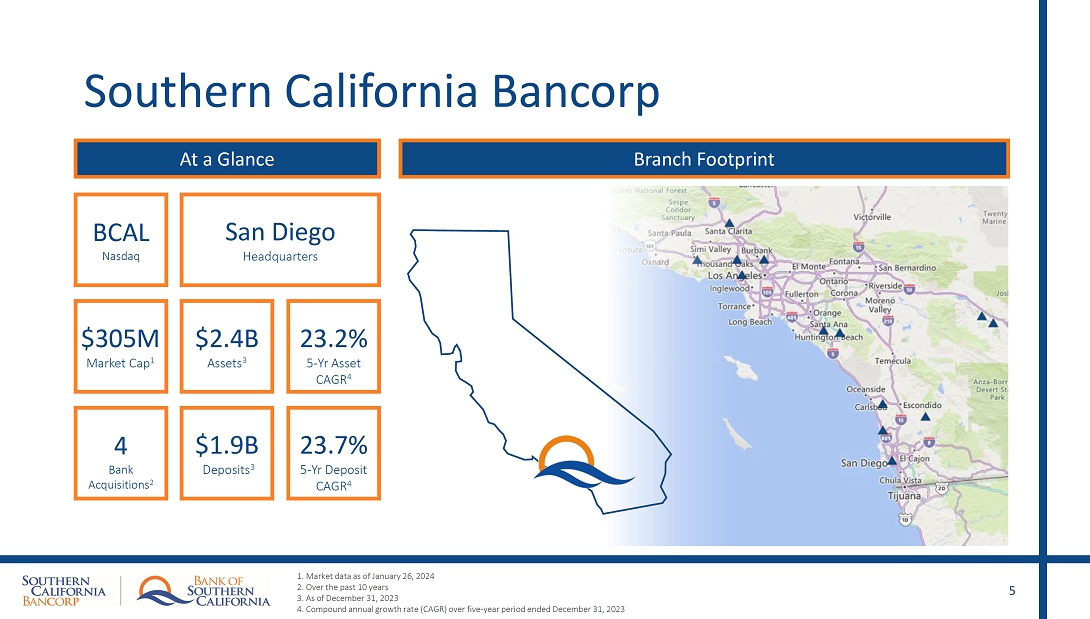

Southern

California Bancorp (NASDAQ: BCAL) is a registered bank holding company headquartered in San Diego, California. Bank of Southern California,

N.A., a national banking association chartered under the laws of the United States (the “Bank”) and regulated by the Office

of Comptroller of the Currency, is a wholly owned subsidiary of Southern California Bancorp. Established in 2001 and headquartered in

San Diego, California, the Bank offers a range of financial products and services to individuals, professionals, and small- to medium-sized

businesses through its 13 branch offices serving Orange, Los Angeles, Riverside, San Diego, and Ventura counties, as well as the Inland

Empire. The Bank’s solutions-driven, relationship-based approach to banking provides accessibility to decision makers and enhances

value through strong partnerships with its clients. Additional information is available at www.banksocal.com.

CAUTIONARY

NOTE REGARDING FORWARD-LOOKING STATEMENTS

In

addition to historical information, this release includes forward-looking statements within the meaning of the Private Securities Litigation

Reform Act of 1995. Forward-looking statements relate to expectations, beliefs, projections, future plans and strategies, anticipated

events or trends and other matters that are not historical facts. Examples of forward-looking statements include, among others, statements

regarding expectations, plans or objectives for future operations, products or services, loan recoveries and the proposed merger (the

“Merger”) of the Company and California

BanCorp

(“CBC”), as well as forecasts relating to financial and operating results or other measures of economic performance. Forward-looking

statements reflect management’s current view about future events and involve risks and uncertainties that may cause actual results

to differ from those expressed in the forward-looking statement or historical results. Forward-looking statements can be identified by

the fact that they do not relate strictly to historical or current facts and often include the words or phrases such as “aim,”

“can,” “may,” “could,” “predict,” “should,” “will,” “would,”

“believe,” “anticipate,” “estimate,” “expect,” “hope,” “intend,”

“plan,” “potential,” “project,” “will likely result,” “continue,” “seek,”

“shall,” “possible,” “projection,” “optimistic,” and “outlook,” and variations

of these words and similar expressions.

Some

factors that could cause actual results to differ materially from historical or expected results include, among others: the risk

factors discussed in the Company’s Registration Statement on Form 10, as amended, filed with the Securities and Exchange

Commission (“SEC”); changes in real estate markets and general economic conditions, either nationally or locally in the

areas in which the Company conducts business; the impact on financial markets from geopolitical conflicts; inflation, interest rate,

market and monetary fluctuations; increases in competitive pressures among financial institutions and businesses offering similar

products and services; higher than anticipated defaults in the Company’s loan portfolio; changes in management’s

estimate of the adequacy of the allowance for credit losses; legislative or regulatory changes or changes in accounting principles,

policies or guidelines; the impacts of recent bank failures; the occurrence of any event, change or other circumstances that could

give rise to the right of the Company or CBC to terminate their agreement with respect to the Merger; the outcome of any legal

proceedings that may be instituted against the Company or CBC; delays in completing the Merger; the failure to obtain necessary

regulatory approvals (and the risk that such approvals impose conditions that could adversely affect the combined company or the

expected benefits of the Merger); the failure to obtain shareholder approvals or to satisfy any of the other conditions to the

Merger on a timely basis or at all; the ability to complete the Merger and integration of the Company and CBC successfully; costs

being greater than anticipated; cost savings being less than anticipated; the risk that the Merger disrupts the business of the

Company, CBC or both; difficulties in retaining senior management, employees or customers; and other factors that may affect the

future results of the Company and CBC.

Additional

information regarding these and other risks and uncertainties to which our business and future financial performance are subject is contained

in the Company’s Registration Statement on Form 10, as amended and other documents the Company files with the SEC from time to

time.

Any

forward-looking statement made in this release is based only on information currently available to management and speaks only as of the

date on which it is made. The Company does not undertake, and specifically disclaims any obligation, to update any forward-looking statements

to reflect occurrences or unanticipated events or circumstances after the date of such statements or to conform such forward-looking

statements to actual results or to changes in its opinions or expectations, except as required by law.

ADDITIONAL

INFORMATION AND WHERE TO FIND IT

In

connection with the Merger, the Company will file with the SEC a Registration Statement on Form S-4 that will include a joint proxy statement

of the Company and CBC and a prospectus of the Company, as well as other relevant documents concerning the proposed transaction. Certain

matters in respect of the Merger will be submitted to the Company’s and CBC’s shareholders for their consideration. This

communication does not constitute an offer to sell or the solicitation of an offer to buy any securities or a solicitation of any vote

or approval, nor shall there be any sale of securities, in any jurisdiction in which such offer, solicitation or sale would be unlawful

prior to registration or qualification under the securities laws of any such jurisdiction.

INVESTORS

AND SHAREHOLDERS ARE URGED TO READ THE REGISTRATION STATEMENT AND THE JOINT PROXY STATEMENT/PROSPECTUS REGARDING THE MERGER WHEN THEY

BECOME AVAILABLE AND ANY OTHER RELEVANT DOCUMENTS FILED WITH THE SEC IN CONNECTION WITH THE MERGER BECAUSE THEY WILL CONTAIN IMPORTANT

INFORMATION.

Investors

will be able to obtain a free copy of the definitive joint proxy statement/prospectus, as well as other filings containing information

about the Company and CBC, without charge, at the SEC’s website, www.sec.gov. Copies of the joint proxy statement/prospectus and

the filings with the SEC that will be incorporated by reference in the joint proxy statement/prospectus can also be obtained, without

charge, in the “Investor Relations” section of the Company’s website at www.banksocal.com (for the Company’s

filings) and in the “Investor Relations” section of CBC’s website, www.californiabankofcommerce.com (for CBC’s

filings).

PARTICIPANTS

IN THE SOLICITATION

The

Company, CBC and certain of their respective directors and executive officers may be deemed to be participants in the solicitation of

proxies from the shareholders of the Company and CBC in connection with the Merger. Information regarding the Company’s directors

and executive officers and their ownership of Company common stock is available in the Company’s definitive proxy statement for

its 2023 annual meeting of shareholders filed with the SEC on June 13, 2023 and other documents filed by the Company with the SEC. Information

regarding CBC’s directors and executive officers and their ownership of CBC common stock is available in CBC’s definitive

proxy statement for its 2023 annual meeting of shareholders filed with the SEC on April 20, 2023 and other documents filed by CBC with

the SEC. Other information regarding the participants in the proxy solicitation and their ownership of common stock will be contained

in the joint proxy statement/prospectus relating to the Merger. Free copies of these documents may be obtained as described in the preceding

paragraph.

Southern

California Bancorp and Subsidiary

Financial

Highlights (Unaudited)

| | |

At

or for the Three

Months Ended | | |

At

or for the Year

Ended | |

| | |

December

31,

2023 | | |

September

30,

2023 | | |

December

31,

2022 | | |

December

31,

2023 | | |

December

31,

2022 | |

| |

($

in thousands except share and per share data) | |

| EARNINGS | |

| |

| Net

interest income | |

$ | 22,559 | | |

$ | 23,261 | | |

$ | 25,269 | | |

$ | 94,138 | | |

$ | 87,786 | |

| Provision

for (reversal of) credit losses | |

$ | 824 | | |

$ | (96 | ) | |

$ | 750 | | |

$ | 915 | | |

$ | 5,956 | |

| Noninterest

(loss) income | |

$ | (102 | ) | |

$ | 815 | | |

$ | 188 | | |

$ | 3,379 | | |

$ | 3,675 | |

| Noninterest

expense | |

$ | 15,339 | | |

$ | 14,781 | | |

$ | 13,112 | | |

$ | 59,746 | | |

$ | 63,522 | |

| Income

tax expense | |

$ | 1,882 | | |

$ | 2,835 | | |

$ | 3,121 | | |

$ | 10,946 | | |

$ | 5,870 | |

| Net

income | |

$ | 4,412 | | |

$ | 6,556 | | |

$ | 8,474 | | |

$ | 25,910 | | |

$ | 16,113 | |

| Pre-tax

pre-provision income (1) | |

$ | 7,118 | | |

$ | 9,295 | | |

$ | 12,345 | | |

$ | 37,771 | | |

$ | 27,939 | |

| Adjusted

pre-tax pre-provision income (1) | |

$ | 7,118 | | |

$ | 9,295 | | |

$ | 12,337 | | |

$ | 37,771 | | |

$ | 34,416 | |

| Diluted

earnings per share | |

$ | 0.24 | | |

$ | 0.35 | | |

$ | 0.46 | | |

$ | 1.39 | | |

$ | 0.88 | |

| Shares

outstanding at period end | |

| 18,369,115 | | |

| 18,309,282 | | |

| 17,940,283 | | |

| 18,369,115 | | |

| 17,940,283 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| PERFORMANCE

RATIOS | |

| | | |

| | | |

| | | |

| | | |

| | |

| Return

on average assets | |

| 0.75 | % | |

| 1.12 | % | |

| 1.46 | % | |

| 1.12 | % | |

| 0.70 | % |

| Adjusted

return on average assets (1) | |

| 0.75 | % | |

| 1.12 | % | |

| 1.45 | % | |

| 1.12 | % | |

| 0.90 | % |

| Return

on average common equity | |

| 6.21 | % | |

| 9.38 | % | |

| 13.21 | % | |

| 9.48 | % | |

| 6.44 | % |

| Adjusted

return on average common equity (1) | |

| 6.21 | % | |

| 9.38 | % | |

| 13.20 | % | |

| 9.48 | % | |

| 8.28 | % |

| Yield

on total loans | |

| 6.08 | % | |

| 5.97 | % | |

| 5.47 | % | |

| 5.94 | % | |

| 5.02 | % |

| Yield

on interest earning assets | |

| 5.85 | % | |

| 5.72 | % | |

| 5.14 | % | |

| 5.69 | % | |

| 4.33 | % |

| Cost

of deposits | |

| 1.81 | % | |

| 1.56 | % | |

| 0.51 | % | |

| 1.37 | % | |

| 0.23 | % |

| Cost

of funds | |

| 1.95 | % | |

| 1.62 | % | |

| 0.56 | % | |

| 1.46 | % | |

| 0.29 | % |

| Net

interest margin | |

| 4.05 | % | |

| 4.23 | % | |

| 4.62 | % | |

| 4.33 | % | |

| 4.06 | % |

| Efficiency

ratio (1) | |

| 68.30 | % | |

| 61.39 | % | |

| 51.51 | % | |

| 61.27 | % | |

| 69.45 | % |

| Adjusted

efficiency ratio (1) | |

| 68.30 | % | |

| 61.39 | % | |

| 51.54 | % | |

| 61.27 | % | |

| 62.37 | % |

| | |

As

of | |

| | |

December

31,

2023 | | |

September

30,

2023 | | |

December

31,

2022 | |

| |

| ($

in thousands except share and per share data) | |

| CAPITAL | |

| | |

| Tangible

equity to tangible assets (1) | |

| 10.73 | % | |

| 10.53 | % | |

| 9.84 | % |

| Book

value (BV) per common share | |

$ | 15.69 | | |

$ | 15.21 | | |

$ | 14.51 | |

| Tangible

BV per common share (1) | |

$ | 13.56 | | |

$ | 13.08 | | |

$ | 12.32 | |

| | |

| | | |

| | | |

| | |

| ASSET

QUALITY | |

| | | |

| | | |

| | |

| Allowance

for loan losses (ALL) | |

$ | 22,569 | | |

$ | 22,705 | | |

$ | 17,099 | |

| Reserve

for unfunded loan commitments | |

$ | 933 | | |

$ | 1,240 | | |

$ | 1,310 | |

| Allowance

for credit losses (ACL) | |

$ | 23,502 | | |

$ | 23,945 | | |

$ | 18,409 | |

| ALL

to total loans held for investment | |

| 1.15 | % | |

| 1.18 | % | |

| 0.90 | % |

| ACL

to total loans held for investment | |

| 1.20 | % | |

| 1.24 | % | |

| 0.97 | % |

| Nonperforming

loans | |

$ | 13,004 | | |

$ | 14,272 | | |

$ | 41 | |

| Other

real estate owned | |

$ | — | | |

$ | — | | |

$ | — | |

| Nonperforming

assets to total assets | |

| 0.55 | % | |

| 0.62 | % | |

| — | % |

| | |

| | | |

| | | |

| | |

| END

OF PERIOD BALANCES | |

| | | |

| | | |

| | |

| Total

loans, including loans held for sale | |

$ | 1,964,791 | | |

$ | 1,935,364 | | |

$ | 1,906,800 | |

| Total

assets | |

$ | 2,360,252 | | |

$ | 2,313,649 | | |

$ | 2,283,927 | |

| Deposits | |

$ | 1,943,556 | | |

$ | 1,983,857 | | |

$ | 1,931,905 | |

| Loans

to deposits | |

| 101.1 | % | |

| 97.6 | % | |

| 98.7 | % |

| Shareholders’

equity | |

$ | 288,152 | | |

$ | 278,550 | | |

$ | 260,355 | |

| (1) |

Non-GAAP measure. See – GAAP to Non-GAAP reconciliation |

| | |

At

or for the Three

Months Ended | | |

At

or for the Year

Ended | |

| ALLOWANCE

for CREDIT LOSSES | |

December

31,

2023 | | |

September

30,

2023 | | |

December

31,

2022 | | |

December

31,

2023 | | |

December

31,

2022 | |

| | |

($

in thousands) | |

| Allowance

for loan losses | |

| | | |

| | | |

| | | |

| | | |

| | |

| Balance

at beginning of period | |

$ | 22,705 | | |

$ | 22,502 | | |

$ | 16,436 | | |

$ | 17,099 | | |

$ | 11,657 | |

| Adoption

of ASU 2016-13 (1) | |

| — | | |

| — | | |

| — | | |

| 5,027 | | |

| — | |

| Provision

for credit losses | |

| 1,131 | | |

| 202 | | |

| 650 | | |

| 1,731 | | |

| 5,450 | |

| Charge-offs | |

| (1,267 | ) | |

| — | | |

| — | | |

| (1,303 | ) | |

| (21 | ) |

| Recoveries | |

| — | | |

| 1 | | |

| 13 | | |

| 15 | | |

| 13 | |

| Net

(charge-offs) recoveries | |

| (1,267 | ) | |

| 1 | | |

| 13 | | |

| (1,288 | ) | |

| (8 | ) |

| Balance,

end of period | |

$ | 22,569 | | |

$ | 22,705 | | |

$ | 17,099 | | |

$ | 22,569 | | |

$ | 17,099 | |

| Reserve

for unfunded loan commitments | |

| | | |

| | | |

| | | |

| | | |

| | |

| Balance,

beginning of period | |

$ | 1,240 | | |

$ | 1,538 | | |

$ | 1,210 | | |

$ | 1,310 | | |

$ | 804 | |

| Adoption

of ASU 2016-13 (1) | |

| — | | |

| — | | |

| — | | |

| 439 | | |

| — | |

| (Reversal

of) provision for credit losses | |

| (307 | ) | |

| (298 | ) | |

| 100 | | |

| (816 | ) | |

| 506 | |

| Balance,

end of period | |

| 933 | | |

| 1,240 | | |

| 1,310 | | |

| 933 | | |

| 1,310 | |

| Allowance

for credit losses | |

$ | 23,502 | | |

$ | 23,945 | | |

$ | 18,409 | | |

$ | 23,502 | | |

$ | 18,409 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| ALL

to total loans held for investment | |

| 1.15 | % | |

| 1.18 | % | |

| 0.90 | % | |

| 1.15 | % | |

| 0.90 | % |

| ACL

to total loans held for investment | |

| 1.20 | % | |

| 1.24 | % | |

| 0.97 | % | |

| 1.20 | % | |

| 0.97 | % |

| (1) |

Represents

the impact of adopting ASU 2016-13, Financial Instruments - Credit Losses on January 1, 2023. As a result of adopting ASU 2016-13,

our methodology to compute our allowance for credit losses is based on a current expected credit loss methodology, rather than the

previously applied incurred loss methodology. |

Southern

California Bancorp and Subsidiary

Balance

Sheets (Unaudited)

| | |

December

31,

2023 | | |

September

30,

2023 | | |

December

31,

2022 | |

| |

| ($

in thousands) | | |

| ASSETS | |

| | | |

| Cash

and due from banks | |

$ | 33,008 | | |

$ | 33,517 | | |

$ | 60,295 | |

| Federal

funds sold & interest-bearing balances | |

| 53,785 | | |

| 61,604 | | |

| 26,465 | |

| Total

cash and cash equivalents | |

| 86,793 | | |

| 95,121 | | |

| 86,760 | |

| | |

| | | |

| | | |

| | |

| Securities

available-for-sale, at fair value | |

| 130,035 | | |

| 111,840 | | |

| 112,580 | |

| Securities

held-to-maturity, at cost (fair value of $50,432 at December 31, 2023; $45,224 at September 30, 2023; and $47,906 at December 31,

2022) | |

| 53,616 | | |

| 53,699 | | |

| 53,946 | |

| Loans

held for sale | |

| 7,349 | | |

| 4,813 | | |

| 9,027 | |

| Loans

held for investment: | |

| | | |

| | | |

| | |

| Construction

& land development | |

| 243,521 | | |

| 237,320 | | |

| 239,067 | |

| 1-4

family residential | |

| 143,903 | | |

| 141,668 | | |

| 144,322 | |

| Multifamily | |

| 221,247 | | |

| 218,170 | | |

| 218,606 | |

| Other

commercial real estate | |

| 1,024,243 | | |

| 1,019,647 | | |

| 958,676 | |

| Commercial

& industrial | |

| 320,142 | | |

| 310,990 | | |

| 331,644 | |

| Other

consumer | |

| 4,386 | | |

| 2,756 | | |

| 5,458 | |

| Total

loans held for investment | |

| 1,957,442 | | |

| 1,930,551 | | |

| 1,897,773 | |

| Allowance

for credit losses - loans | |

| (22,569 | ) | |

| (22,705 | ) | |

| (17,099 | ) |

| Total

loans held for investment, net | |

| 1,934,873 | | |

| 1,907,846 | | |

| 1,880,674 | |

| | |

| | | |

| | | |

| | |

| Restricted

stock at cost | |

| 16,055 | | |

| 16,027 | | |

| 14,543 | |

| Premises

and equipment | |

| 13,270 | | |

| 13,565 | | |

| 14,334 | |

| Right

of use asset | |

| 9,291 | | |

| 10,007 | | |

| 8,607 | |

| Goodwill | |

| 37,803 | | |

| 37,803 | | |

| 37,803 | |

| Core

deposit intangible | |

| 1,195 | | |

| 1,275 | | |

| 1,584 | |

| Bank

owned life insurance | |

| 38,918 | | |

| 38,665 | | |

| 37,972 | |

| Deferred

taxes, net | |

| 11,137 | | |

| 12,542 | | |

| 10,699 | |

| Accrued

interest and other assets | |

| 19,917 | | |

| 10,446 | | |

| 15,398 | |

| Total

assets | |

$ | 2,360,252 | | |

$ | 2,313,649 | | |

$ | 2,283,927 | |

| | |

| | | |

| | | |

| | |

| LIABILITIES

AND SHAREHOLDERS’ EQUITY | |

| | | |

| | | |

| | |

| Deposits: | |

| | | |

| | | |

| | |

| Noninterest-bearing

demand | |

$ | 675,098 | | |

$ | 735,979 | | |

$ | 923,899 | |

| Interest-bearing

NOW accounts | |

| 381,943 | | |

| 354,489 | | |

| 209,625 | |

| Money

market and savings accounts | |

| 636,685 | | |

| 699,942 | | |

| 668,602 | |

| Time

deposits | |

| 249,830 | | |

| 193,447 | | |

| 129,779 | |

| Total

deposits | |

| 1,943,556 | | |

| 1,983,857 | | |

| 1,931,905 | |

| | |

| | | |

| | | |

| | |

| Borrowings | |

| 102,865 | | |

| 25,842 | | |

| 67,770 | |

| Operating

lease liability | |

| 12,117 | | |

| 12,657 | | |

| 11,055 | |

| Accrued

interest and other liabilities | |

| 13,562 | | |

| 12,743 | | |

| 12,842 | |

| Total

liabilities | |

| 2,072,100 | | |

| 2,035,099 | | |

| 2,023,572 | |

| | |

| | | |

| | | |

| | |

| Shareholders’

Equity: | |

| | | |

| | | |

| | |

| Common

stock - 50,000,000 shares authorized, no par value; issued and outstanding 18,369,115 at December 31, 2023; 18,309,282 at September

30, 2023 and 17,940,283 at December 31, 2022) | |

| 222,036 | | |

| 221,632 | | |

| 218,280 | |

| Retained

earnings | |

| 70,575 | | |

| 66,163 | | |

| 48,516 | |

| Accumulated

other comprehensive loss - net of taxes | |

| (4,459 | ) | |

| (9,245 | ) | |

| (6,441 | ) |

| Total

shareholders’ equity | |

| 288,152 | | |

| 278,550 | | |

| 260,355 | |

| Total

liabilities and shareholders’ equity | |

$ | 2,360,252 | | |

$ | 2,313,649 | | |

$ | 2,283,927 | |

Southern

California Bancorp and Subsidiary

Income

Statements - Quarterly and Year-to-Date (Unaudited)

| | |

Three

Months Ended | | |

Year

Ended | |

| | |

December

31,

2023 | | |

September

30,

2023 | | |

December

31,

2022 | | |

December

31,

2023 | | |

December

31,

2022 | |

| | |

($

in thousands except share and per share data) | |

| INTEREST

AND DIVIDEND INCOME | |

| | | |

| | | |

| | | |

| | | |

| | |

| Interest

and fees on loans | |

$ | 29,968 | | |

$ | 28,977 | | |

$ | 25,781 | | |

$ | 113,951 | | |

$ | 86,366 | |

| Interest

on debt securities | |

| 991 | | |

| 942 | | |

| 647 | | |

| 3,497 | | |

| 2,013 | |

| Interest

on tax-exempted debt securities | |

| 353 | | |

| 359 | | |

| 488 | | |

| 1,655 | | |

| 1,372 | |

| Interest

and dividends from other institutions | |

| 1,257 | | |

| 1,206 | | |

| 1,227 | | |

| 4,419 | | |

| 3,824 | |

| Total

interest and dividend income | |

| 32,569 | | |

| 31,484 | | |

| 28,143 | | |

| 123,522 | | |

| 93,575 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| INTEREST

EXPENSE | |

| | | |

| | | |

| | | |

| | | |

| | |

| Interest

on NOW, savings, and money market accounts | |

| 6,606 | | |

| 5,922 | | |

| 2,096 | | |

| 20,161 | | |

| 3,793 | |

| Interest

on time deposits | |

| 2,331 | | |

| 1,867 | | |

| 463 | | |

| 6,704 | | |

| 797 | |

| Interest

on borrowings | |

| 1,073 | | |

| 434 | | |

| 315 | | |

| 2,519 | | |

| 1,199 | |

| Total

interest expense | |

| 10,010 | | |

| 8,223 | | |

| 2,874 | | |

| 29,384 | | |

| 5,789 | |

| Net

interest income | |

| 22,559 | | |

| 23,261 | | |

| 25,269 | | |

| 94,138 | | |

| 87,786 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Provision

for (reversal of) credit losses (1) | |

| 824 | | |

| (96 | ) | |

| 750 | | |

| 915 | | |

| 5,956 | |

| Net

interest income after provision for credit losses | |

| 21,735 | | |

| 23,357 | | |

| 24,519 | | |

| 93,223 | | |

| 81,830 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| NONINTEREST

(LOSS) INCOME | |

| | | |

| | | |

| | | |

| | | |

| | |

| Service

charges and fees on deposit accounts | |

| 507 | | |

| 470 | | |

| 456 | | |

| 1,946 | | |

| 1,796 | |

| (Loss)

gain on sale of loans | |

| — | | |

| (54 | ) | |

| 293 | | |

| 831 | | |

| 1,349 | |

| Bank

owned life insurance income | |

| 253 | | |

| 238 | | |

| 221 | | |

| 946 | | |

| 1,490 | |

| Servicing

and related income on loans | |

| 17 | | |

| 61 | | |

| 53 | | |

| 240 | | |

| 192 | |

| Loss

on sale of debt securities | |

| (1,008 | ) | |

| — | | |

| (994 | ) | |

| (974 | ) | |

| (994 | ) |

| Loss

on sale of building and related fixed assets | |

| — | | |

| — | | |

| — | | |

| — | | |

| (768 | ) |

| Other

charges and fees | |

| 129 | | |

| 100 | | |

| 159 | | |

| 390 | | |

| 610 | |

| Total

noninterest (loss) income | |

| (102 | ) | |

| 815 | | |

| 188 | | |

| 3,379 | | |

| 3,675 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| NONINTEREST

EXPENSE | |

| | | |

| | | |

| | | |

| | | |

| | |

| Salaries

and employee benefits | |

| 9,598 | | |

| 9,736 | | |

| 8,634 | | |

| 39,249 | | |

| 37,069 | |

| Occupancy

and equipment expenses | |

| 1,678 | | |

| 1,579 | | |

| 1,458 | | |

| 6,231 | | |

| 6,210 | |

| Data

processing | |

| 1,158 | | |

| 1,144 | | |

| 1,089 | | |

| 4,534 | | |

| 4,609 | |

| Legal,

audit and professional | |

| 1,161 | | |

| 598 | | |

| 487 | | |

| 3,211 | | |

| 2,597 | |

| Regulatory

assessments | |

| 320 | | |

| 369 | | |

| 345 | | |

| 1,508 | | |

| 1,550 | |

| Director

and shareholder expenses | |

| 207 | | |

| 215 | | |

| 219 | | |

| 849 | | |

| 946 | |

| Merger

and related (income) expenses | |

| — | | |

| — | | |

| (8 | ) | |

| — | | |

| 1,177 | |

| Core

deposit intangible amortization | |

| 80 | | |

| 128 | | |

| 140 | | |

| 389 | | |

| 438 | |

| Litigation

settlements, net | |

| — | | |

| — | | |

| — | | |

| — | | |

| 5,525 | |

| Other

expense | |

| 1,137 | | |

| 1,012 | | |

| 748 | | |

| 3,775 | | |

| 3,401 | |

| Total

noninterest expense | |

| 15,339 | | |

| 14,781 | | |

| 13,112 | | |

| 59,746 | | |

| 63,522 | |

| Income

before income taxes | |

| 6,294 | | |

| 9,391 | | |

| 11,595 | | |

| 36,856 | | |

| 21,983 | |

| Income

tax expense | |

| 1,882 | | |

| 2,835 | | |

| 3,121 | | |

| 10,946 | | |

| 5,870 | |

| Net

income | |

$ | 4,412 | | |

$ | 6,556 | | |

$ | 8,474 | | |

$ | 25,910 | | |

$ | 16,113 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Net

income per share - basic | |

$ | 0.24 | | |

$ | 0.36 | | |

$ | 0.47 | | |

$ | 1.42 | | |

$ | 0.90 | |

| Net

income per share - diluted | |

$ | 0.24 | | |

$ | 0.35 | | |

$ | 0.46 | | |

$ | 1.39 | | |

$ | 0.88 | |

| Weighted

average common share-diluted | |

| 18,727,519 | | |

| 18,672,132 | | |

| 18,359,781 | | |

| 18,656,742 | | |

| 18,228,287 | |

| Pre-tax,

pre-provision income (2) | |

$ | 7,118 | | |

$ | 9,295 | | |

$ | 12,345 | | |

$ | 37,771 | | |

$ | 27,939 | |

| (1) |

Included (reversal of) provision for unfunded commitments

of $(307) thousand, $(298) thousand and $100 thousand for the three months ended December 31, 2023, September 30, 2023 and December 31,

2022, respectively; and $(816) thousand and $506 thousand for the year ended December 31, 2023 and December 31, 2022, respectively. |

| (2) |

Non-GAAP measure. See – GAAP to Non-GAAP reconciliation. |

Southern

California Bancorp and Subsidiary

Average

Balance Sheets and Yield Analysis

(Unaudited)

| | |

Three

Months Ended | |

| | |

December

31, 2023 | | |

September

30, 2023 | | |

December

31, 2022 | |

| | |

Average

Balance | | |

Income/ Expense | | |

Yield/ Cost | | |

Average

Balance | | |

Income/ Expense | | |

Yield/ Cost | | |

Average

Balance | | |

Income/ Expense | | |

Yield/ Cost | |

| |

($

in thousands) | |

| Assets | |

| |

| Interest-earning

assets: | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Total

loans | |

$ | 1,954,396 | | |

$ | 29,968 | | |

| 6.08 | % | |

$ | 1,924,384 | | |

$ | 28,977 | | |

| 5.97 | % | |

$ | 1,870,705 | | |

$ | 25,781 | | |

| 5.47 | % |

| Taxable

debt securities | |

| 113,375 | | |

| 991 | | |

| 3.47 | % | |

| 111,254 | | |

| 942 | | |

| 3.36 | % | |

| 102,205 | | |

| 647 | | |

| 2.51 | % |

| Tax-exempt

debt securities (1) | |

| 58,644 | | |

| 353 | | |

| 3.02 | % | |

| 59,630 | | |

| 359 | | |

| 3.02 | % | |

| 73,166 | | |

| 488 | | |

| 3.35 | % |

| Deposits

in other financial institutions | |

| 56,313 | | |

| 759 | | |

| 5.35 | % | |

| 50,367 | | |

| 681 | | |

| 5.36 | % | |

| 40,781 | | |

| 347 | | |

| 3.38 | % |

| Fed

funds sold/resale agreements | |

| 9,008 | | |

| 125 | | |

| 5.51 | % | |

| 20,653 | | |

| 283 | | |

| 5.44 | % | |

| 68,437 | | |

| 636 | | |

| 3.69 | % |

| Restricted

stock investments and other bank stock | |

| 16,394 | | |

| 373 | | |

| 9.03 | % | |

| 16,365 | | |

| 242 | | |

| 5.87 | % | |

| 14,883 | | |

| 244 | | |

| 6.50 | % |

| Total

interest-earning assets | |

| 2,208,130 | | |

| 32,569 | | |

| 5.85 | % | |

| 2,182,653 | | |

| 31,484 | | |

| 5.72 | % | |

| 2,170,177 | | |

| 28,143 | | |

| 5.14 | % |

| Total

noninterest-earning assets | |

| 137,193 | | |

| | | |

| | | |

| 131,288 | | |

| | | |

| | | |

| 139,205 | | |

| | | |

| | |

| Total

assets | |

$ | 2,345,323 | | |

| | | |

| | | |

$ | 2,313,941 | | |

| | | |

| | | |

$ | 2,309,382 | | |

| | | |

| | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Liabilities

and Shareholders’ Equity | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Interest-bearing

liabilities: | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Interest-bearing

NOW accounts | |

$ | 362,579 | | |

$ | 1,860 | | |

| 2.04 | % | |

$ | 353,714 | | |

$ | 1,706 | | |

| 1.91 | % | |

$ | 215,272 | | |

$ | 121 | | |

| 0.22 | % |

| Money

market and savings accounts | |

| 669,391 | | |

| 4,746 | | |

| 2.81 | % | |

| 675,609 | | |

| 4,216 | | |

| 2.48 | % | |

| 700,544 | | |

| 1,975 | | |

| 1.12 | % |

| Time

deposits | |

| 208,700 | | |

| 2,331 | | |

| 4.43 | % | |

| 183,745 | | |

| 1,867 | | |

| 4.03 | % | |

| 123,524 | | |

| 463 | | |

| 1.49 | % |

| Total

interest-bearing deposits | |

| 1,240,670 | | |

| 8,937 | | |

| 2.86 | % | |

| 1,213,068 | | |

| 7,789 | | |

| 2.55 | % | |

| 1,039,340 | | |

| 2,559 | | |

| 0.98 | % |

| Borrowings: | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| FHLB

advances | |

| 56,380 | | |

| 802 | | |

| 5.64 | % | |

| 11,731 | | |

| 163 | | |

| 5.51 | % | |

| 3,696 | | |

| 44 | | |

| 4.72 | % |

| Subordinated

debt | |

| 17,854 | | |

| 271 | | |

| 6.02 | % | |

| 17,830 | | |

| 271 | | |

| 6.03 | % | |

| 17,759 | | |

| 271 | | |

| 6.05 | % |

| Total

borrowings | |

| 74,234 | | |

| 1,073 | | |

| 5.73 | % | |

| 29,561 | | |

| 434 | | |

| 5.82 | % | |

| 21,455 | | |

| 315 | | |

| 5.82 | % |

| Total

interest-bearing liabilities | |

| 1,314,904 | | |

| 10,010 | | |

| 3.02 | % | |

| 1,242,629 | | |

| 8,223 | | |

| 2.63 | % | |

| 1,060,795 | | |

| 2,874 | | |

| 1.07 | % |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Noninterest-bearing

liabilities: | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Noninterest-bearing

deposits (2) | |

| 721,169 | | |

| | | |

| | | |

| 768,148 | | |

| | | |

| | | |

| 970,908 | | |

| | | |

| | |

| Other

liabilities | |

| 27,178 | | |

| | | |

| | | |

| 25,722 | | |

| | | |

| | | |

| 23,199 | | |

| | | |

| | |

| Shareholders’

equity | |

| 282,072 | | |

| | | |

| | | |

| 277,442 | | |

| | | |

| | | |

| 254,480 | | |

| | | |

| | |

| Total

Liabilities and Shareholders’ Equity | |

$ | 2,345,323 | | |

| | | |

| | | |

$ | 2,313,941 | | |

| | | |

| | | |

$ | 2,309,382 | | |

| | | |

| | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Net

interest spread | |

| | | |

| | | |

| 2.83 | % | |

| | | |

| | | |

| 3.09 | % | |

| | | |

| | | |

| 4.07 | % |

| Net

interest income and margin | |

| | | |

$ | 22,559 | | |

| 4.05 | % | |

| | | |

$ | 23,261 | | |

| 4.23 | % | |

| | | |

$ | 25,269 | | |

| 4.62 | % |

| Cost

of deposits | |

| | | |

| | | |

| 1.81 | % | |

| | | |

| | | |

| 1.56 | % | |

| | | |

| | | |

| 0.51 | % |

| Cost

of funds | |

| | | |

| | | |

| 1.95 | % | |

| | | |

| | | |

| 1.62 | % | |

| | | |

| | | |

| 0.56 | % |

| (1) |

Tax-exempt debt securities yields are presented on a tax

equivalent basis using a 21% tax rate. |

| (2) |

Average noninterest-bearing deposits represent 36.76%, 38.77%

and 48.30% of average total deposits for the three months ended December 31, 2023, September 30, 2023 and December 31, 2022, respectively. |

Southern

California Bancorp and Subsidiary

Average

Balance Sheets and Yield Analysis

(Unaudited)

| | |

Year

Ended | |

| | |

December

31, 2023 | | |

December

31, 2022 | |

| | |

Average

Balance | | |

Income/ Expense | | |

Yield/ Cost | | |

Average

Balance | | |

Income/ Expense | | |

Yield/ Cost | |

| |

($

in thousands) | |

| Assets | |

| |

| Interest-earning

assets: | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Total

loans | |

$ | 1,918,443 | | |

$ | 113,951 | | |

| 5.94 | % | |

$ | 1,720,560 | | |

$ | 86,366 | | |

| 5.02 | % |

| Taxable

debt securities | |

| 107,021 | | |

| 3,497 | | |

| 3.27 | % | |

| 96,357 | | |

| 2,013 | | |

| 2.09 | % |

| Tax-exempt

debt securities (1) | |

| 65,674 | | |

| 1,655 | | |

| 3.19 | % | |

| 54,744 | | |

| 1,372 | | |

| 3.17 | % |

| Deposits

in other financial institutions | |

| 46,826 | | |

| 2,434 | | |

| 5.20 | % | |

| 210,467 | | |

| 1,508 | | |

| 0.72 | % |

| Fed

funds sold/resale agreements | |

| 18,114 | | |

| 923 | | |

| 5.10 | % | |

| 65,172 | | |

| 1,388 | | |

| 2.13 | % |

| Restricted

stock investments and other bank stock | |

| 15,930 | | |

| 1,062 | | |

| 6.67 | % | |

| 14,668 | | |

| 928 | | |

| 6.33 | % |

| Total

interest-earning assets | |

| 2,172,008 | | |

| 123,522 | | |

| 5.69 | % | |

| 2,161,968 | | |

| 93,575 | | |

| 4.33 | % |

| Total

noninterest-earning assets | |

| 134,225 | | |

| | | |

| | | |

| 139,450 | | |

| | | |

| | |

| Total

assets | |

$ | 2,306,233 | | |

| | | |

| | | |

$ | 2,301,418 | | |

| | | |

| | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Liabilities

and Shareholders’ Equity | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Interest-bearing

liabilities: | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Interest-bearing

NOW accounts | |

$ | 308,537 | | |

$ | 5,161 | | |

| 1.67 | % | |

$ | 211,075 | | |

$ | 312 | | |

| 0.15 | % |

| Money

market and savings accounts | |

| 673,176 | | |

| 15,000 | | |

| 2.23 | % | |

| 690,830 | | |

| 3,481 | | |

| 0.50 | % |

| Time

deposits | |

| 180,219 | | |

| 6,704 | | |

| 3.72 | % | |

| 100,746 | | |

| 797 | | |

| 0.79 | % |

| Total

interest-bearing deposits | |

| 1,161,932 | | |

| 26,865 | | |

| 2.31 | % | |

| 1,002,651 | | |

| 4,590 | | |

| 0.46 | % |

| Borrowings: | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| FHLB

advances | |

| 26,390 | | |

| 1,434 | | |

| 5.43 | % | |

| 932 | | |

| 43 | | |

| 4.61 | % |

| Subordinated

debt | |

| 17,818 | | |

| 1,085 | | |

| 6.09 | % | |

| 17,723 | | |

| 1,086 | | |

| 6.13 | % |

| TruPS | |

| — | | |

| — | | |

| — | % | |

| 1,239 | | |

| 70 | | |

| 5.65 | % |

| Total

borrowings | |

| 44,208 | | |

| 2,519 | | |

| 5.70 | % | |

| 19,894 | | |

| 1,199 | | |

| 6.03 | % |

| Total

interest-bearing liabilities | |

| 1,206,140 | | |

| 29,384 | | |

| 2.44 | % | |

| 1,022,545 | | |

| 5,789 | | |

| 0.57 | % |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Noninterest-bearing

liabilities: | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Noninterest-bearing

deposits (2) | |

| 801,882 | | |

| | | |

| | | |

| 1,006,795 | | |

| | | |

| | |

| Other

liabilities | |

| 24,865 | | |

| | | |

| | | |

| 22,024 | | |

| | | |

| | |

| Shareholders’

equity | |

| 273,346 | | |

| | | |

| | | |

| 250,054 | | |

| | | |

| | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Total

Liabilities and Shareholders’ Equity | |

$ | 2,306,233 | | |

| | | |

| | | |

$ | 2,301,418 | | |

| | | |

| | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Net

interest spread | |

| | | |

| | | |

| 3.25 | % | |

| | | |

| | | |

| 3.76 | % |

| Net

interest income and margin | |

| | | |

$ | 94,138 | | |

| 4.33 | % | |

| | | |

$ | 87,786 | | |

| 4.06 | % |

| Cost

of deposits | |

| | | |

| | | |

| 1.37 | % | |

| | | |

| | | |

| 0.23 | % |

| Cost

of funds | |

| | | |

| | | |

| 1.46 | % | |

| | | |

| | | |

| 0.29 | % |

| (1) |

Tax-exempt

debt securities yields are presented on a tax equivalent basis using a 21% tax rate. |

| (2) |

Average

noninterest-bearing deposits represent 40.83%, and 50.10% of average total deposits for the year ended December 31, 2023 and December

31, 2022, respectively. |

Southern

California Bancorp and Subsidiary

GAAP

to Non-GAAP Reconciliation

(Unaudited)

The

following tables present a reconciliation of non-GAAP financial measures to GAAP measures for: (1) adjusted net income, (2) efficiency

ratio, (3) adjusted efficiency ratio, (4) pre-tax pre-provision income, (5) adjusted pre-tax pre-provision income, (6) average tangible

common equity, (7) adjusted return on average assets, (8) adjusted return on average equity, (9) return on average tangible common equity,

(10) adjusted return on average tangible common equity, (11) tangible common equity, (12) tangible assets, (13) tangible common equity

to tangible asset ratio, and (14) tangible book value per share. We believe the presentation of certain non-GAAP financial measures provides

useful information to assess our consolidated financial condition and consolidated results of operations and to assist investors in evaluating

our financial results relative to our peers. These non-GAAP financial measures complement our GAAP reporting and are presented below

to provide investors and others with information that we use to manage the business each period. Because not all companies use identical

calculations, the presentation of these non-GAAP financial measures may not be comparable to other similarly titled measures used by

other companies. These non-GAAP measures should be taken together with the corresponding GAAP measures and should not be considered a

substitute of the GAAP measures.

| | |

Three

Months Ended | | |

Year

Ended | |

| | |

December

31,

2023 | | |

September

30,

2023 | | |

December

31,

2022 | | |

December

31,

2023 | | |

December

31,

2022 | |

| | |

($

in thousands) | |

| Adjusted

net income | |

| | | |

| | | |

| | | |

| | | |

| | |

| Net

income | |

$ | 4,412 | | |

$ | 6,556 | | |

$ | 8,474 | | |

$ | 25,910 | | |

$ | 16,113 | |

| (Deduct)

add: After-tax merger and related (income) expenses (1) | |

| — | | |

| — | | |

| (6 | ) | |

| — | | |

| 846 | |

| Add:

After-tax litigation settlements, net (1) | |

| — | | |

| — | | |

| — | | |

| — | | |

| 3,734 | |

| Adjusted

net income (non-GAAP) | |

$ | 4,412 | | |

$ | 6,556 | | |

$ | 8,468 | | |

$ | 25,910 | | |

$ | 20,693 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Efficiency

Ratio | |

| | | |

| | | |

| | | |

| | | |

| | |

| Noninterest

expense | |

$ | 15,339 | | |

$ | 14,781 | | |

$ | 13,112 | | |

$ | 59,746 | | |

$ | 63,522 | |

| (Add)

deduct: Merger and related (income) expenses | |

| — | | |

| — | | |

| (8 | ) | |

| — | | |

| 1,177 | |

| Deduct:

Litigation settlements, net | |

| — | | |

| — | | |

| — | | |

| — | | |

| 5,300 | |

| Adjusted

noninterest expense | |

| 15,339 | | |

| 14,781 | | |

| 13,120 | | |

| 59,746 | | |

| 57,045 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Net

interest income | |

| 22,559 | | |

| 23,261 | | |

| 25,269 | | |

| 94,138 | | |

| 87,786 | |

| Noninterest

(loss) income | |

| (102 | ) | |

| 815 | | |

| 188 | | |

| 3,379 | | |

| 3,675 | |

| Total

net interest income and noninterest (loss) income | |

$ | 22,457 | | |

$ | 24,076 | | |

$ | 25,457 | | |

$ | 97,517 | | |

$ | 91,461 | |

| Efficiency

ratio (non-GAAP) | |

| 68.3 | % | |

| 61.4 | % | |

| 51.5 | % | |

| 61.3 | % | |

| 69.5 | % |

| Adjusted

efficiency ratio (non-GAAP) | |

| 68.3 | % | |

| 61.4 | % | |

| 51.5 | % | |

| 61.3 | % | |

| 62.4 | % |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Pre-tax

pre-provision income | |

| | | |

| | | |

| | | |

| | | |

| | |

| Net

interest income | |

$ | 22,559 | | |

$ | 23,261 | | |

$ | 25,269 | | |

$ | 94,138 | | |

$ | 87,786 | |

| Noninterest

(loss) income | |

| (102 | ) | |

| 815 | | |

| 188 | | |

| 3,379 | | |

| 3,675 | |

| Total

net interest income and noninterest (loss) income | |

| 22,457 | | |

| 24,076 | | |

| 25,457 | | |

| 97,517 | | |

| 91,461 | |

| Less:

Noninterest expense | |

| 15,339 | | |

| 14,781 | | |

| 13,112 | | |

| 59,746 | | |

| 63,522 | |

| Pre-tax

pre-provision income (non-GAAP) | |

| 7,118 | | |

| 9,295 | | |

| 12,345 | | |

| 37,771 | | |

| 27,939 | |

| (Deduct)

add: Merger and related (income) expenses | |

| — | | |

| — | | |

| (8 | ) | |

| — | | |

| 1,177 | |

| Add:

Litigation settlements, net | |

| — | | |

| — | | |

| — | | |

| — | | |

| 5,300 | |

| Adjusted

pre-tax pre-provision income (non-GAAP) | |