0001690437

false

FY

true

Unlimited

Unlimited

0001690437

2022-07-01

2023-06-30

0001690437

2023-06-30

0001690437

2023-08-14

0001690437

2022-06-30

0001690437

2021-07-01

2022-06-30

0001690437

BAR:GoldBullionMember

2023-06-30

0001690437

BAR:GoldBullionMember

2022-06-30

0001690437

2020-07-01

2021-06-30

0001690437

2021-06-30

0001690437

2020-06-30

0001690437

us-gaap:GoldMember

us-gaap:FairValueInputsLevel1Member

2023-06-30

0001690437

us-gaap:GoldMember

us-gaap:FairValueInputsLevel2Member

2023-06-30

0001690437

us-gaap:GoldMember

us-gaap:FairValueInputsLevel3Member

2023-06-30

0001690437

us-gaap:FairValueInputsLevel1Member

2023-06-30

0001690437

us-gaap:FairValueInputsLevel2Member

2023-06-30

0001690437

us-gaap:FairValueInputsLevel3Member

2023-06-30

0001690437

us-gaap:GoldMember

us-gaap:FairValueInputsLevel1Member

2022-06-30

0001690437

us-gaap:GoldMember

us-gaap:FairValueInputsLevel2Member

2022-06-30

0001690437

us-gaap:GoldMember

us-gaap:FairValueInputsLevel3Member

2022-06-30

0001690437

us-gaap:FairValueInputsLevel1Member

2022-06-30

0001690437

us-gaap:FairValueInputsLevel2Member

2022-06-30

0001690437

us-gaap:FairValueInputsLevel3Member

2022-06-30

iso4217:USD

xbrli:shares

iso4217:USD

xbrli:shares

xbrli:pure

utr:oz

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

Form

10-K

(Mark

One)

☒

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

For

the fiscal year ended June 30, 2023

or

☐

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT

OF

1934

Commission

file number: 001-38195

GRANITESHARES

GOLD TRUST

(Exact

name of registrant as specified in its charter)

| New

York |

|

82-6393903 |

| (State

or other jurisdiction of |

|

(I.R.S.

Employer |

| incorporation

or organization) |

|

Identification

No.) |

| c/o

GRANITESHARES LLC |

|

|

222

Broadway – 21st floor

New

York, NY |

|

10038 |

| (Address

of principal executive offices) |

|

(Zip

Code) |

Registrant’s

telephone number, including area code:

(646)

876 5096

Securities

registered pursuant to Section 12(b) of the Act:

| Title

of each class |

|

Name

of each exchange on which registered |

| GraniteShares

Gold Shares |

|

|

Securities

registered pursuant to Section 12(g) of the Act: None

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate

by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐ No ☒

Indicate

by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2)

has been subject to such filing requirements for the past 90 days.

Yes

☒ No ☐

Indicate

by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data

File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months.

Yes

☒ No ☐

Indicate

by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained,

to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this

Form 10-K or any amendment to this Form 10-K. ☒

Indicate

by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting

company or emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller

reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large

accelerated filer |

☒ |

Accelerated

filer |

☐ |

| Non

accelerated filer |

☐ |

Smaller

reporting company |

☐ |

| |

|

Emerging

growth company |

☐ |

If

an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness

of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered

public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section

12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction

of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error

corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive

officers during the relevant recovery period pursuant to § 240.10D-1(b). ☐

Indicate

by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

Aggregate

market value of the registrant’s Shares outstanding based upon the closing price of a Share on June 30, 2023 as reported by the

NYSE Arca, Inc. on that date: $940,044,500.

As

of August 14, 2023, GraniteShares Gold Trust has 49,250,000 GraniteShares Gold Shares outstanding.

DOCUMENTS

INCORPORATED BY REFERENCE: None.

Statement

Regarding Forward-Looking Statements

This

Annual Report on Form 10-K includes statements which relate to future events or future performance. In some cases, you can identify such

forward-looking statements by terminology such as “may,” “will,” “should,” “expect,”

“plan,” “anticipate,” “believe,” “estimate,” “predict,” “potential”

or the negative of these terms or other comparable terminology. All statements (other than statements of historical fact) included in

this prospectus that address activities, events or developments that may occur in the future, including such matters as changes in commodity

prices and market conditions (for gold and the Shares), the Trust’s operations, the Sponsor’s plans and references to the

Trust’s future success and other similar matters are forward-looking statements. These statements are only predictions. Actual

events or results may differ materially. These statements are based upon certain assumptions and analyses made by the Sponsor on the

basis of its perception of historical trends, current conditions and expected future developments, as well as other factors it believes

are appropriate in the circumstances. Whether or not actual results and developments will conform to the Sponsor’s expectations

and predictions, however, is subject to a number of risks and uncertainties, including the special considerations discussed in this prospectus,

general economic, market and business conditions, changes in laws or regulations, including those concerning taxes, made by governmental

authorities or regulatory bodies, and other world economic and political developments. See “Risk Factors.” Consequently,

all the forward-looking statements made in this prospectus are qualified by these cautionary statements, and there can be no assurance

that the actual results or developments the Sponsor anticipates will be realized or, even if substantially realized, that they will result

in the expected consequences to, or have the expected effects on, the Trust’s operations or the value of the Shares. Moreover,

neither the Sponsor, nor any other person assumes responsibility for the accuracy or completeness of the forward-looking statements.

Neither the Trust nor the Sponsor undertakes an obligation to publicly update or conform to actual results any forward-looking statement,

whether as a result of new information, future developments or otherwise, except as required by law.

TABLE

OF CONTENTS

PART

I

Item

1. Business

The

purpose of the GraniteShares Gold Trust (the “Trust”) is to own gold transferred to the Trust in exchange for shares issued

by the Trust (“Shares”). Each Share represents a fractional undivided beneficial interest in and ownership of the Trust.

The assets of the Trust are anticipated to consist solely of gold bullion. The Trust was formed on August 24, 2017 when an initial deposit

of gold was made in exchange for the issuance of two Baskets (a “Basket” consists of 50,000 Shares).

The

sponsor of the Trust is GraniteShares LLC (the “Sponsor”). The trustee of the Trust is The Bank of New York Mellon (the “Trustee”)

and the custodian is ICBC Standard Bank (the “Custodian”).

The

Trust’s Shares at redeemable value decreased from US$ 996,127,089 on June 30, 2022 to US$ 935,811,456 on June 30, 2023, the Trust’s

fiscal year end. The Outstanding Shares in the Trust decreased from 55,300,000 Shares on June 30, 2022 to 49,450,000 Shares on June 30,

2023.

The

Trust is not managed like a corporation or an active investment vehicle. The Trust has no directors, officers or employees. It does not

engage in any activities designed to obtain a profit from or to improve the losses caused by changes in the price of gold. The gold held

by the Trust will only be delivered to pay the remuneration due to the Sponsor (the “Sponsor’s Fee”), distributed to

Authorized Participants (defined under Item 7) in connection with the redemption of Baskets or sold (1) on an as-needed basis to pay

Trust expenses not assumed by the Sponsor, (2) in the event the Trust terminates and liquidates its assets, or (3) as otherwise required

by law or regulation.

The

Trust is not registered as an investment company under the Investment Company Act of 1940 and is not required to register under such

act. The Trust does not and will not hold or trade in commodities futures contracts regulated by the Commodity Exchange Act (the “CEA”),

as administered by the Commodity Futures Trading Commission (the “CFTC”). The Trust is not a commodity pool for purposes

of the CEA and neither the Sponsor nor the Trustee is subject to regulation as a commodity pool operator or a commodity trading advisor

in connection with the Shares. The Trust has no fixed termination date.

The

Sponsor of the registrant maintains an Internet website at www.graniteshares.com, through which the registrant’s annual reports

on Form 10-K, quarterly reports on Form 10-Q, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of

the Securities Exchange Act of 1934, as amended, or the Exchange Act, are made available free of charge as soon as reasonably practicable

after they have been filed or furnished to the Securities and Exchange Commission (the “SEC”). Additional information regarding

the Trust may also be found on the SEC’s EDGAR database at www.sec.gov.

Trust

Objective

The

objective of the Trust is for the value of the Shares to reflect, at any given time, the value of the assets owned by the Trust at that

time less the Trust’s accrued expenses and liabilities as of that time. The Shares are intended to constitute a simple and cost-effective

means of making an investment similar to an investment in gold. An investment in allocated physical gold bullion requires expensive and

sometimes complicated arrangements in connection with the assay, transportation and warehousing of the metal. Traditionally, such expense

and complications have resulted in investments in physical gold bullion being efficient only in amounts beyond the reach of many investors.

The Shares have been designed to remove the obstacles represented by the expense and complications involved in an investment in physical

gold bullion, while at the same time having an intrinsic value that reflects, at any given time, the price of the assets owned by the

Trust at such time less the Trust expenses and liabilities. Although the Shares are not the exact equivalent of an investment in gold,

they provide investors with an alternative that allows a level of participation in the gold market through the securities market.

Advantages

of investing in the Shares include:

Minimal

credit risk.

The

Shares are backed primarily by allocated physical gold bullion identified as the Trust’s property in the Custodian’s books.

The Trust arrangements contemplate that no Shares can be issued unless the corresponding amount of gold has been deposited into the Trust.

Once deposited into the Trust, gold is only removed from the Trust if (i) sold to pay Trust expenses (such as the Sponsor’s Fee

and any other expenses not assumed by the Sponsor) or liabilities to which the Trust may be subject, or (ii) transferred from the Trust’s

account to an Authorized Participant’s account in exchange for one or more Baskets of Shares surrendered for redemption.

Ease

and flexibility of investment.

Retail

investors may purchase and sell Shares through traditional brokerage accounts. Because the amount of gold corresponding to a Share is

significantly less than the minimum amounts of physical gold bullion that are commercially available for investment purposes, the cash

outlay necessary for an investment in Shares should be less than the amount required for currently existing means of investing in physical

gold bullion. Shares are eligible for margin accounts.

Relatively

cost efficient.

Although

the return, if any, of an investment in the Shares is subject to the additional expenses of the Trust, including the Sponsor’s

Fee, the Trustee’s Fee, the Custodian’s Fee, and to other costs and expenses not assumed by the Sponsor which would not be

incurred in the case of a direct investment in gold, the Shares may represent a cost-efficient alternative for investors not otherwise

in a position to participate directly in the market for allocated physical gold bullion, because the expenses involved in an investment

in allocated physical gold bullion through the Shares are dispersed among all holders of Shares.

Description

of the Gold Industry

Introduction

This

section provides a brief introduction to the gold industry by looking at some of the key participants, detailing the primary sources

of demand and supply and outlining the role of the “official” sector (i.e., central banks) in the market.

Market

Participants

The

participants in the world gold industry may be classified in the following sectors: the mining and producer sector, the banking sector,

the official sector, the investment sector, and the manufacturing sector. A brief description of each follows.

The

Mining and Producer Sector

This

group includes mining companies that specialize in gold and silver production; mining companies that produce gold as a by-product of

other production (such as a copper or silver producer); scrap merchants and recyclers.

The

Banking Sector

Bullion

banks provide a variety of services to the gold market and its participants, thereby facilitating interactions between other parties.

Services provided by the bullion banking community include traditional banking products as well as mine financing, physical gold purchases

and sales, hedging and risk management, inventory management for industrial users and consumers, and gold deposit and loan instruments.

The

Official Sector

The

official sector encompasses the activities of the various central banking operations of gold-holding countries. Having been a source

of gold supply for many years, the official sector became a source of net demand in 2010. The prominence given by market commentators

to this activity coupled with the total amount of gold held by the official sector has resulted in this area being a significant shift

in the gold market.

The

Investment Sector

This

sector includes the investment and trading activities of both professional and private investors and speculators. These participants

range from large hedge and mutual funds to day-traders on futures exchanges and retail-level coin collectors.

The

Manufacturing Sector

The

fabrication and manufacturing sector represents all the commercial and industrial users of gold for whom gold is a daily part of their

business. The jewelry industry is a large user of gold. Other industrial users of gold include the electronics and dental industries.

World

Gold Supply and Demand (2012-2022)

The

following table sets forth a summary of the world gold supply and demand from 2012 to 2022:

| In tonnes(1) | |

2012 | | |

2013 | | |

2014 | | |

2015 | | |

2016 | | |

2017 | | |

2018 | | |

2019 | | |

2020 | | |

2021 | | |

2022 | |

| Supply | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Mine production | |

| 2,957.2 | | |

| 3,166.8 | | |

| 3,270.5 | | |

| 3,361.3 | | |

| 3,509.6 | | |

| 3,573.1 | | |

| 3,665.6 | | |

| 3,594.5 | | |

| 3,472.4 | | |

| 3,568.9 | | |

| 3,611.9 | |

| Net producer hedging | |

| -45.3 | | |

| -27.9 | | |

| 104.9 | | |

| 12.9 | | |

| 37.6 | | |

| -25.5 | | |

| -11.6 | | |

| 6.2 | | |

| -39.1 | | |

| -22.7 | | |

| -1.5 | |

| Recycled gold | |

| 1,636.8 | | |

| 1,195.3 | | |

| 1,129.6 | | |

| 1,067.1 | | |

| 1,232.1 | | |

| 1,112.4 | | |

| 1,131.7 | | |

| 1,275.7 | | |

| 1,293.1 | | |

| 1,136.2 | | |

| 1,144.1 | |

| Total supply | |

| 4,548.6 | | |

| 4,334.1 | | |

| 4,505.0 | | |

| 4,441.3 | | |

| 4,779.3 | | |

| 4,666.0 | | |

| 4,775.3 | | |

| 4,876.3 | | |

| 4,726.2 | | |

| 4,682.4 | | |

| 4,754.5 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Demand | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Fabrication | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Jewellery1 | |

| 2,140.9 | | |

| 2,735.3 | | |

| 2,544.4 | | |

| 2,479.2 | | |

| 2,018.8 | | |

| 2,257.5 | | |

| 2,290.0 | | |

| 2,152.1 | | |

| 1,324.0 | | |

| 2,230.6 | | |

| 2,189.8 | |

| Technology | |

| 382.3 | | |

| 355.8 | | |

| 348.4 | | |

| 331.7 | | |

| 323.0 | | |

| 332.6 | | |

| 334.8 | | |

| 326.0 | | |

| 302.8 | | |

| 330.2 | | |

| 308.5 | |

| Investment | |

| 1,621.0 | | |

| 797.7 | | |

| 900.7 | | |

| 967.0 | | |

| 1,614.2 | | |

| 1,315.0 | | |

| 1,164.0 | | |

| 1,271.1 | | |

| 1,796.3 | | |

| 1,001.9 | | |

| 1,106.8 | |

| Central bank & other inst. | |

| 569.2 | | |

| 629.5 | | |

| 601.1 | | |

| 579.6 | | |

| 394.9 | | |

| 378.6 | | |

| 656.2 | | |

| 605.4 | | |

| 254.9 | | |

| 450.1 | | |

| 1,135.7 | |

| Gold demand | |

| 4,713.3 | | |

| 4,518.2 | | |

| 4,394.6 | | |

| 4,357.4 | | |

| 4,350.8 | | |

| 4,283.6 | | |

| 4,445.0 | | |

| 4,359.3 | | |

| 3,677.9 | | |

| 4,012.8 | | |

| 4,740.7 | |

| OTC and other | |

| -164.7 | | |

| -184.1 | | |

| 110.4 | | |

| 83.8 | | |

| 428.5 | | |

| 376.4 | | |

| 330.3 | | |

| 521.8 | | |

| 1,048.5 | | |

| 669.6 | | |

| 13.8 | |

| Total demand | |

| 4,548.6 | | |

| 4,334.1 | | |

| 4,505.0 | | |

| 4,441.3 | | |

| 4,779.3 | | |

| 4,666.0 | | |

| 4,775.3 | | |

| 4,876.3 | | |

| 4,726.4 | | |

| 4,682.4 | | |

| 4,754.5 | |

| LBMA Gold Price (US$/oz) | |

| 1,668.98 | | |

| 1,411.23 | | |

| 1,266.40 | | |

| 1,160.06 | | |

| 1,250.80 | | |

| 1,257.15 | | |

| 1,268.49 | | |

| 1,392.60 | | |

| 1769.59 | | |

| 1,798.61 | | |

| 1,800.09 | |

| Note:

|

Totals

may not add due to independent rounding. Net producer hedging is the change in the physical market impact of mining companies’

gold loans, forwards and options positions. |

| |

|

| (1)

|

“Tonne”

refers to one metric ton. This is equivalent to 1,000 kilograms or 32,150.7465 troy ounces. |

Source:

Gold Demand Trends 2023 Statistics, World Gold Council

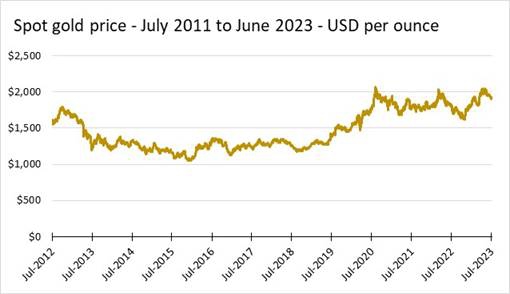

Historical

Chart of the Price of Gold

The

price of gold is volatile, and its fluctuations are expected to have a direct impact on the value of the Shares. However, movements in

the price of gold in the past, and any past or present trends, are not a reliable indicator of future movements. Movements may be influenced

by various factors, including announcements from central banks regarding a country’s reserve gold holdings, agreements among central

banks, fluctuations in the value of the U.S. dollar, political uncertainties around the world, and economic concerns.

The

following chart illustrates the changes in the gold spot prices from July 2012 through June 2023:

Source:

Bloomberg and GraniteShares

Operation

of the Gold Market

The

global trade in gold consists of Over-the-Counter (“OTC”) transactions in spot, forwards, and options and other derivatives,

together with exchange-traded futures and options.

Over-the-Counter

Market

The

OTC gold market includes spot, forward, and option and other derivative transactions conducted on a principal-to-principal basis. While

this is a global, nearly 24-hour per day market, its main centers are London, New York and Zurich.

Most

OTC market trades are cleared through London. The LBMA plays an important role in setting OTC gold trading industry standards. A London

Good Delivery Bar (as described below), which is acceptable for settlement of any OTC transaction, will be acceptable for delivery to

the Trust in connection with the issuance of Baskets.

Futures

Exchanges

Futures

exchanges seek to provide a neutral, regulated marketplace for the trading of derivatives contracts for commodities, such as futures,

options and certain swaps. The terms of these contracts are defined by an exchange for each commodity. For each commodity traded, the

contract specifies the precise commodity quality and quantity standards, as well as the location and timing of physical delivery for

the reference physical commodity, although only a very small number of these contracts result in the actual commodity delivery.

An

exchange does not buy or sell those contracts, but seeks to offer a transparent forum where members, on their own behalf or on the behalf

of customers, can trade the contracts in a safe, efficient and orderly manner. The futures and options contracts, as well as some swaps,

are cleared through a derivatives clearing organization which ensures more accurate valuation of positions in these contracts as well

as settlement of trades in these contracts.

The

most significant gold futures exchange in the U.S. is COMEX, operated by Commodities Exchange, Inc., a subsidiary of New York Mercantile

Exchange, Inc., and a subsidiary of the Chicago Mercantile Exchange Group (the “CME Group”). Other commodity exchanges include

the Tokyo Commodity Exchange (“TOCOM”), the Multi Commodity Exchange Of India (“MCX”), the Shanghai Futures Exchange,

ICE Futures US (the “ICE”), and the Dubai Gold & Commodities Exchange.

Exchange

Regulation

In

addition to the public nature of the pricing, futures exchanges in the United States are regulated at two levels, internal and external

governmental supervision. The internal is performed through self-regulation as self-regulatory organizations and consists of regular

monitoring of the trading process to ensure that it is conducted in conformance with all exchange rules; the financial condition of all

exchange member firms to ensure that they continuously meet financial commitments; and the positions of commercial and non-commercial

customers to ensure that physical delivery and other commercial commitments can be met, and that pricing is not being improperly affected

by the size of any particular customer positions. External governmental oversight is performed by the CFTC, which reviews all the rules

and regulations of United States futures exchanges and monitors their enforcement. The CFTC oversees the operation of the U.S. commodity

futures markets, including COMEX and ICE Futures US. One of the principal public policy objectives of the Commodity Exchange Act is to

ensure the integrity of the markets it oversees and the reliability of the prices of trades on those markets. The Commodity Exchange

Act and CFTC require futures exchanges to ensure compliance with core principles applicable to designated contract markets to have rules

and procedures to prevent market manipulation, abusive trade practice and fraud, and the CFTC conducts regular review of the markets’

rule enforcement programs. Other local regulators enforce their own regulations governing trading platforms and futures exchanges located

in their jurisdictions.

The

London Bullion Market

Most

trading in physical gold is conducted on the OTC market, predominantly in London. The LBMA coordinates various OTC-market activities,

including clearing and vaulting, acts as the principal intermediary between physical gold market participants and the relevant regulators,

promotes good trading practices and develops standard market documentation. In addition, the LBMA promotes refining standards for the

gold market by maintaining the “London Good Delivery List,” which identifies refiners of gold that have been approved by

the LBMA.

In

the OTC market, gold bars that meet the specifications for weight, dimensions, fineness (or purity), identifying marks (including the

assay stamp of an LBMA-acceptable refiner) and appearance described in “The Good Delivery Rules for Gold and Silver Bars”

published by the LBMA are referred to as “London Good Delivery Bars.” A London Good Delivery Bar (typically called a “400

ounce bar”) must contain between 350 and 430 fine troy ounces of gold (1 troy ounce = 31.1034768 grams), with a minimum fineness

(or purity) of 995 parts per 1000 (99.5%), be of good appearance and be easy to handle and stack. The fine gold content of a gold bar

is calculated by multiplying the gross weight of the bar (expressed in units of 0.025 troy ounces) by the fineness of the bar. A London

Good Delivery Bar must also bear the stamp of one of the refiners identified on the London Good Delivery List.

London

Market Regulation

Following

the enactment of the Financial Markets Act 2012, the Prudential Regulation Authority of the Bank of England is responsible for regulating

most of the financial firms that are active in the bullion market, and the Financial Conduct Authority is responsible for consumer and

competition issues. Trading in spot, forwards and wholesale deposits in the bullion market is subject to the Non-Investment Products

Code adopted by market participants.

Not

a Regulated Commodity Pool

The

Trust does not trade in gold futures, options or swap contracts on any futures exchange or over the counter. The Trust takes delivery

of gold that complies with the LBMA gold delivery rules. Because the Trust does not trade in gold futures, options or swap contracts

on any futures exchange or OTC, the Trust is not regulated by the CFTC or the NFA under the Commodity Exchange Act as a “commodity

pool,” and is not required to be operated by a CFTC-regulated commodity pool operator or advised by a commodity trading advisor.

Investors in the Trust do not receive the regulatory protections afforded to investors in commodity pools operated by registered commodity

pool operators, nor may any futures exchange or the NFA enforce its rules with respect to the Trust’s activities. In addition,

investors in the Trust do not benefit from the protections afforded to investors in gold futures, options or swaps contracts on regulated

futures exchanges or OTC.

Other

Methods of Investing in Gold

The

Trust competes with other financial vehicles, including traditional debt and equity securities issued by companies in the gold industry

and other securities backed by or linked to gold, direct investments in gold and investment vehicles similar to the Trust.

Secondary

Market Trading

While

the Trust seeks to reflect generally the performance of the price of gold less the Trust’s expenses and liabilities, Shares may

trade at, above or below their NAV. The NAV of Shares will fluctuate with changes in the market value of the Trust’s assets. The

trading prices of Shares will fluctuate in accordance with changes in their NAV as well as market supply and demand. The amount of the

discount or premium in the trading price relative to the NAV may be influenced by non-concurrent trading hours between the major gold

markets and the Exchange. While the Shares trade on the Exchange until 4:00 p.m. (New York time), liquidity in the market for gold may

be reduced after the close of the major world gold markets, including London, Zurich and COMEX. As a result, during this time, trading

spreads, and the resulting premium or discount, on Shares may widen. However, given that Baskets of Shares can be created and redeemed

in exchange for the underlying amount of gold, the Sponsor believes that the arbitrage opportunities may provide a mechanism to mitigate

the effect of such premium or discount.

Valuation

of Gold; Computation of Net Asset Value

On

each business day, as soon as practicable after 4:00 p.m. (New York time), the Trustee evaluates the gold held by the Trust and determines

the net asset value of the Trust and the NAV. For purposes of making these calculations, a business day means any day other than a day

when the Exchange is closed for regular trading.

The

Trustee values the gold held by the Trust using that day’s LBMA Gold Price PM. LBMA Gold Price PM is the price per fine troy ounce

of gold, stated in U.S. dollars, determined by IBA following one or more 30-second electronic auctions conducted starting at 3:00 p.m.

(London time), on each day that the London gold market is open for business, and announced by the LBMA shortly thereafter. If there is

no LBMA Gold Price PM on any day, the Trustee is authorized to use the LBMA Gold Price AM announced on that day. If neither price is

available for that day, the Trustee will value the Trust’s gold based on the most recently announced LBMA Gold Price PM or LBMA

Gold Price AM. If the Sponsor determines that such price is inappropriate to use, the Sponsor will identify an alternate basis for evaluation

to be employed by the Trustee. Further, the Sponsor may instruct the Trustee to use on an on-going basis a different publicly available

price which the Sponsor determines to fairly represent the commercial value of the Trust’s gold. Neither the Trustee nor the Sponsor

are liable to any person for the determination that the most recently announced LBMA Gold Price PM (or other benchmark price) is not

appropriate as a basis for evaluation of the gold held or receivable by the Trust or for any determination as to the alternative basis

for evaluation, provided that such determination is made in good faith.

On

each day that the LBMA Gold Price PM is to be determined, a price for the first round of auction (and any round thereafter) is set by

a chairperson appointed by IBA, based on a set of rules and taking into account relevant pricing information available at the time, and

made publicly available in advance of the auction. Beginning at 3:00 p.m. (London time), the direct participants pre-qualified by IBA

and their sponsored clients are allowed, but not required, to electronically submit during a 30-second period buy and/or sell orders

for spot transactions in gold at the pre-determined price. If at the conclusion of the 30-second round the market is determined by IBA

to be balanced, the price determined by a chairperson for that round is the LBMA Gold Price PM for that day and announced as such by

the LBMA. If the market is not balanced at the end of the first auction, a chairperson will revise the starting price, and an additional

30-second auction is held at the new price. If necessary, the process is repeated until the market is determined to be balanced and the

price at which that determination occurs is the LBMA Gold Price PM for that date. For these purposes, the market is considered to be

balanced when, at the end of an auction, the total number of ounces of gold for which buy orders were submitted in that auction falls

within a certain pre-determined margin of tolerance from the total number of ounces of gold for which sell orders were submitted in the

auction. Once the LBMA Gold Price PM has been determined for a given day, the buy and sell orders entered by the auction participants

during the last auction will be executed at that day’s LBMA Gold Price PM. Any market imbalance remaining after the last auction

(which must be within the margin of tolerance) is allocated equally among all participants (and not only those participating in any auction

held on that date). IBA reserves a right to limit the allocation of any market imbalance on any date only among participants that have

entered an order during an auction on that date.

Once

the value of the Trust’s gold has been determined, the Trustee subtracts all accrued fees, expenses and other liabilities of the

Trust from the total value of the gold and all other assets of the Trust. The resulting figure is the net asset value of the Trust. The

Trustee determines the NAV per Share by dividing the net asset value of the Trust by the number of Shares outstanding at the time the

computation is made. Any estimate of the accrued but unpaid fees, expenses and liabilities of the Trust for purposes of computing the

net asset value of the Trust and NAV per Share of the Trust made by the Trustee in good faith shall be conclusive upon all persons interested

in the Trust.

Trust

Expenses

The

Trust’s only ordinary recurring expense is expected to be the Sponsor’s Fee. In exchange for the Sponsor’s Fee, the

Sponsor has agreed to assume the following expenses incurred by the Trust: The Trustee’s Fee and its ordinary out-of-pocket expenses,

the Custodian’s Fee and its reimbursable expenses, the Exchange listing fees, SEC registration fees, marketing expenses, printing

and mailing costs, audit fees and expenses and up to $100,000 per annum in legal fees and expenses.

The

Sponsor’s Fee is accrued daily at an annualized rate equal to 0.1749% of the net asset value of the Trust and is payable monthly

in arrears. The Sponsor may, at its discretion and from time to time, waive all or a portion of the Sponsor’s Fee for stated periods

of time. The Sponsor is under no obligation to waive any portion of its fees and any such waiver shall create no obligation to waive

any such fees during any period not covered by the waiver. Presently, the Sponsor does not intend to waive any part of its fee. Furthermore,

the Sponsor may, in its sole discretion, agree to rebate all or a portion of the Sponsor’s Fee attributable to Shares held by certain

institutional investors subject to minimum Share holding and lock up requirements as determined by the Sponsor to foster stability in

the Trust’s asset levels. Any such rebate will be subject to negotiation and written agreement between the Sponsor and the investor

on a case by case basis. The Sponsor is under no obligation to provide any rebates of the Sponsor’s Fee. Neither the Trust nor

the Trustee will be a party to any Sponsor’s Fee rebate arrangements negotiated by the Sponsor. Any Sponsor’s Fee rebate

shall be paid from the funds of the Sponsor and not from the assets of the Trust.

The

Sponsor’s Fee will be paid through delivery of gold from the Trust Unallocated Account that has been de-allocated from the Trust

Allocated Account for this purpose. The Trustee will, when directed by the Sponsor, and, in the absence of such direction, may, in its

discretion, sell gold in such quantity and at such times, as may be necessary to permit payment of the Trust expenses or liabilities

not assumed by the Sponsor. The Trustee will endeavor to sell gold at such times and in the smallest amounts required to permit such

payments as they become due, it being the intention to avoid or minimize the Trust’s holdings of assets other than gold. Accordingly,

the amount of gold to be sold will vary from time to time depending on the level of the Trust’s expenses and the market price of

gold. The Custodian may, but is not required to purchase gold needed to cover Trust expenses provided that if the Trustee’s instruction

to sell gold is received by the Custodian by 2:00 p.m. (London time), the purchase price for the gold will be that day’s LBMA Gold

Price PM (or other applicable benchmark price), and if the Trustee’s instruction to sell gold is received by the Custodian after

2:00 p.m. (London time), the purchase price will be the next LBMA Gold Price PM (or other applicable benchmark price) available after

that day.

Cash

held by the Trustee pending payment of the Trust’s expenses will not bear any interest. Each sale of gold by the Trust will be

a taxable event to Shareholders for federal income tax purposes. See “United States Federal Income Tax Consequences—Taxation

of U.S. Shareholders.”

The

Sponsor’s Fee for the fiscal year ended June 30, 2023 was $1,602,240.

Deposit

of Gold; Issuance of Baskets

The

Trust creates and redeems Shares on a continuous basis but only in Baskets of 50,000 Shares. Upon the deposit of the corresponding amount

of gold with the Custodian, and the payment of the Trustee’s applicable fee and of any expenses, taxes or charges (such as stamp

taxes or stock transfer taxes or fees), the Trustee will deliver the appropriate number of Baskets to the DTC account of the depositing

Authorized Participant. Only Authorized Participants can deposit gold and receive Baskets of Shares in exchange. As of the date of this

prospectus, J.P. Morgan Securities LLC, Merrill Lynch Professional Clearing Corp., Morgan Stanley & Co. LLC, and Virtu Americas LLC

are the Authorized Participants. The Sponsor and the Trustee maintain a current list of Authorized Participants. Gold allocated by the

Custodian to the Trust Allocated Account must meet the London Good Delivery Standards.

Before

making a deposit, the Authorized Participant must deliver to the Trustee a written purchase order indicating the number of Baskets it

intends to acquire. The Trustee will acknowledge the purchase order unless it or the Sponsor decides to refuse the purchase order as

permitted by the Trust Agreement. The date the Trustee receives that order determines the Basket Amount the Authorized Participant needs

to deposit. However, orders received by the Trustee after 3:59 p.m. (New York time) on a business day or on a business day when the LBMA

Gold Price PM or other applicable benchmark price is not announced, will not be accepted.

If

the Trustee accepts the purchase order, it transmits to the Authorized Participant, via facsimile or electronic mail message, no later

than 5:30 p.m. (New York time) on the date such purchase order is received, or deemed received, a copy of the purchase order endorsed

“Accepted” by the Trustee and indicating the Basket Amount that the Authorized Participant must deliver to the Custodian

at the Trust Unallocated Account loco London in exchange for each Basket. Prior to the Trustee’s acceptance as specified above,

a purchase order only represents the Authorized Participant’s unilateral offer to deposit gold in exchange for Baskets of Shares

and has no binding effect upon the Trust, the Trustee, the Custodian or any other party.

The

Basket Amount necessary for the creation of a Basket changes from day to day. On each day that the Exchange is open for regular trading,

the Trustee adjusts the quantity of gold constituting the Basket Amount as appropriate to reflect sales of gold, any loss of gold that

may occur, and accrued expenses. The computation is made by the Trustee as promptly as practicable after 4:00 p.m. (New York time). See

“The Trust—Valuation of Gold; Computation of Net Asset Value” for a description of how the LBMA Gold Price PM is determined,

and description of how the Trustee determines the NAV. The Trustee determines the Basket Amount for a given day by dividing the number

of Fine Ounces of gold held by the Trust as of the opening of business on that business day, adjusted for the amount of gold constituting

estimated accrued but unpaid fees and expenses of the Trust as of the opening of business on that business day, by the quotient of the

number of Shares outstanding at the opening of business divided by 50,000. Fractions of a Fine Ounce of gold smaller than 0.001 Fine

Ounce are disregarded for purposes of the computation of the Basket Amount. The Basket Amount so determined is communicated via electronic

mail message to all Authorized Participants, and made available on the Sponsor’s website for the Shares. The Exchange also publishes

the Basket Amount determined by the Trustee as indicated above.

Because

the Sponsor has assumed what are expected to be most of the Trust’s expenses, and the Sponsor’s Fee accrues daily at the

same rate (i.e., 1/365th for a non-leap year or 1/366th for a leap year of the daily net asset value of the Trust multiplied

by 0.1749%), in the absence of any extraordinary expenses or liabilities, the amount of gold by which the Basket Amount decreases each

day is predictable. Authorized Participants may use that indicative Basket Amount as guidance regarding the amount of gold that they

may expect to have to deposit with the Custodian in respect of purchase orders placed by them on such next business day and accepted

by the Trustee. The Authorized Participant Agreement provides, however, that once a purchase order has been accepted by the Trustee,

the Authorized Participant will be required to deposit with the Custodian the Basket Amount determined by the Trustee on the effective

date of the purchase order.

No

Shares are issued unless and until the Custodian has informed the Trustee that it has allocated to the Trust Allocated Account (other

than up to 430 Fine Ounces, which may be held in the Trust Unallocated Account) the corresponding amount of gold.

Redemption

of Baskets

Authorized

Participants, acting on authority of the registered holder of Shares or on their own account, may surrender Baskets of Shares in exchange

for the corresponding Basket Amount announced by the Trustee. Upon the surrender of such Shares and the payment of the Trustee’s

applicable fee and of any expenses, taxes or charges (such as stamp taxes or stock transfer taxes or fees), the Trustee will deliver

to the order of the redeeming Authorized Participant the amount of gold corresponding to the redeemed Baskets. Shares can only be surrendered

for redemption in Baskets of 50,000 Shares each.

Before

surrendering Baskets of Shares for redemption, an Authorized Participant must deliver to the Trustee a written request indicating the

number of Baskets it intends to redeem or on a business day when the LBMA Gold Price PM or other applicable benchmark price is not announced.

The date the Trustee receives that order determines the Basket Amount to be received in exchange. However, orders received by the Trustee

after 3:59 p.m. (New York time) on a business day or on a business day when the LBMA Gold Price PM or other applicable benchmark price

is not announced, will not be accepted.

The

redemption distribution from the Trust will consist of a credit to the redeeming Authorized Participant’s unallocated account representing

the amount of the gold held by the Trust evidenced by the Shares being redeemed as of the date of the redemption order. Fractions of

a Fine Ounce included in the redemption distribution smaller than 0.001 of a Fine Ounce are disregarded. The redemption distribution

will not be delivered unless and until all of the Shares to be redeemed have been received by the Trustee.

In

connection with any issuance or redemption of Shares, the Authorized Participant shall be responsible for paying or reimbursing to the

Custodian and the Trustee the amount of any applicable tax, fees or other governmental charge that may be due in connection with the

transfer of gold and the issuance and delivery of Shares, and any expense associated with the delivery of gold other than by credit to

an Authorized Participant’s unallocated account with the Custodian.

Redemptions

may be suspended, or the date for delivery of gold may be postponed, only (i) during any period in which regular trading on the Exchange

is suspended or restricted or the Exchange is closed (other than scheduled holiday or weekend closings), or (ii) during an emergency

as a result of which delivery, disposal or evaluation of gold is not reasonably practicable. Neither the Trustee nor the Sponsor will

be liable to any person by reason of any such suspension or postponement.

Fees

and Expenses of the Trustee

Each

deposit of gold for the creation of Baskets of Shares and each surrender of Baskets of Shares for the purpose of withdrawing Trust property

(including if the Trust Agreement terminates) must be accompanied by a payment to the Trustee of a fee of $500 (or such other fee as

the Trustee, with the prior written consent of the Sponsor, may from time to time announce).

The

Trustee is entitled to reimburse itself from the assets of the Trust for all expenses and disbursements incurred by it for extraordinary

services it may provide to the Trust or in connection with any discretionary action the Trustee may take to protect the Trust or the

interests of the holders.

The

Sponsor

The

Sponsor is a Delaware limited liability company and was formed on January 6, 2017. The Sponsor’s office is located at 222 Broadway,

New York, New York 10038. Under the Delaware Limited Liability Company Act and the governing documents of the Sponsor, the sole member

of the Sponsor, GraniteShares, Inc., is not responsible for the debts, obligations and liabilities of the Sponsor solely by reason of

being the sole member of the Sponsor.

The

Sponsor’s Role

The

Sponsor arranged for the creation of the Trust and is responsible for the ongoing registration of the Shares for their public offering

in the United States and the listing of the Shares on the Exchange. The Sponsor has agreed to assume the organizational expenses of the

Trust and the following expenses incurred by the Trust: The Trustee’s monthly fee and its ordinary out-of-pocket expenses, the

Custodian’s Fee and its reimbursable expenses, Exchange listing fees, SEC registration fees, marketing expenses, printing and mailing

costs, audit fees and expenses and up to $100,000 per annum in legal fees and expenses.

The

Sponsor will not exercise day-to-day oversight over the Trustee or the Custodian. The Sponsor may remove the Trustee and appoint a successor

Trustee (i) if the Trustee ceases to meet certain objective requirements (including the requirement that it has capital, surplus and

undivided profits of at least $150 million), (ii) if, having received written notice of a material breach of its obligations under the

Trust Agreement, the Trustee has not cured the breach within 30 days, or (iii) if the Trustee refuses to consent to the implementation

of an amendment to the Trust’s initial Internal Control Over Financial Reporting. The Sponsor also has the right to replace the

Trustee during the 90 days following any merger, consolidation or conversion in which the Trustee is not the surviving entity or, in

its discretion, on the fifth anniversary of the creation of the Trust or on any subsequent third anniversary thereafter. The Sponsor

also has the right to direct the Trustee to appoint any new or additional Custodian that the Sponsor selects.

The

Sponsor has developed a marketing plan for the Trust, prepares marketing materials regarding the Shares, including the content of the

Trust’s website, and executes the marketing plan for the Trust on an ongoing basis.

The

Trustee

The

Bank of New York Mellon, a banking corporation organized under the laws of the State of New York with trust powers, serves as the Trustee.

The Bank of New York Mellon has a trust office at 2 Hanson Place, 9th Floor, Brooklyn, New York 11217. The Bank of New York Mellon is

subject to supervision by the New York State Department of Financial Services and the Board of Governors of the Federal Reserve System.

A copy of the Trust Agreement is available for inspection at The Bank of New York Mellon’s trust office identified above. The Bank

of New York Mellon had at least $150 million in capital and retained earnings as of June 30, 2023.

The

Trustee’s Role

The

Trustee is responsible for the day-to-day administration of the Trust. This includes (i) processing orders for the creation and redemption

of Baskets; (ii) coordinating with the Custodian the receipt and delivery of gold transferred to, or by, the Trust in connection with

each issuance and redemption of Baskets; (iii) calculating the net asset value of the Trust on each business day; and (iv) selling the

Trust’s gold as needed to cover the Trust’s expenses. The Trustee intends to regularly communicate with the Sponsor to monitor

the overall performance of the Trust. The Trustee does not monitor the performance of the Custodian other than to review the reports

provided by the Custodian pursuant to the Custody Agreements. The Trustee, along with the Sponsor, will liaise with the Trust’s

legal, accounting and other professional service providers as needed. The Trustee will assist and support the Sponsor with the preparation

of the financial statements of the Trust and with all periodic reports required to be filed with the SEC on behalf of the Trust.

The

Custodian

ICBC

Standard Bank Plc, a public limited company incorporated under the laws of England and Wales, serves as the Custodian of the Trust’s

gold.

The

Custodian’s Role

The

Custodian is responsible for holding the Trust’s allocated gold as well as receiving and converting allocated and unallocated gold

on behalf of the Trust. Unless otherwise agreed between the Trustee (as instructed by the Sponsor) and the Custodian, physical gold must

be held by the Custodian at its London vault premises. At the end of each business day, the Custodian will hold no more than 430 Fine

Ounces of unallocated gold for the Trust, which corresponds to the maximum Fine Ounce weight of a London Good Delivery Bar. The Custodian

converts the Trust’s gold between allocated and unallocated gold when: (1) Authorized Participants engage in creation and redemption

transactions with the Trust; or (2) gold is sold to pay Trust expenses. The Custodian will facilitate the transfer of gold in and out

of the Trust through the unallocated gold accounts it may maintain for each Authorized Participant or unallocated gold accounts that

may be maintained for an Authorized Participant by another LBMA-approved gold-clearing bank, and through the unallocated gold account

it will maintain for the Trust. The Custodian is responsible for allocating specific bars of gold to the Trust Allocated Account.

The

Custodian will provide the Trustee with regular reports detailing the gold transfers in and out of the Trust Unallocated Account with

the Custodian and identifying the gold bars held in the Trust Allocated Account.

The

Custodian’s fees and expenses are to be paid by the Sponsor. The Custodian and its affiliates may from time to time act as Authorized

Participants or purchase or sell gold or shares for their own account, as an agent for their customers and for accounts over which they

exercise investment discretion. The Trustee, on behalf of the Trust, has entered into the Custody Agreements with the Custodian, under

which the Custodian maintains the Trust Unallocated Account and the Trust Allocated Account.

Pursuant

to the Trust Agreement, if, upon the resignation of the Custodian, there would be no custodian acting pursuant to the Custody Agreements,

the Trustee shall, promptly after receiving notice of such resignation, appoint a substitute custodian or custodians selected by the

Sponsor pursuant to custody agreement(s) approved by the Sponsor (provided, however, that the rights and duties of the Trustee under

the Trust Agreement and the custody agreement(s) shall not be materially altered without its consent). When directed by the Sponsor,

and to the extent permitted by, and in the manner provided by, the Custody Agreements, the Trustee shall remove the Custodian and appoint

a substitute or appoint an additional custodian or custodians selected by the Sponsor. Each such substitute or additional custodian shall,

forthwith upon its appointment, enter into a Custody Agreement in form and substance approved by the Sponsor. After the entry into the

Custody Agreements, the Trustee shall not enter into or amend any Custody Agreement with a custodian without the written approval of

the Sponsor (which approval shall not be unreasonably withheld or delayed). When instructed by the Sponsor, the Trustee shall demand

that a custodian of the Trust deliver such of the Trust’s gold held by it as is requested of it to any other custodian or such

substitute or additional custodian or custodians directed by the Sponsor. In connection with such transfer of physical gold, the Trustee

will, at the direction of the Sponsor, cause the physical gold to be weighed or assayed. The Trustee shall have no liability for any

transfer of physical gold or weighing or assaying of delivered physical gold as directed by the Sponsor, and in the absence of such direction

shall have no obligation to effect such a delivery or to cause the delivered physical gold to be weighed, assayed or otherwise validated.

Under

the Trust Agreement, the Sponsor is responsible for appointing accountants, auditors or other inspectors to audit or examine the accounts

and operations of the Custodian and any successor custodian or additional custodian at such times as directed by the Sponsor as permitted

by the Custody Agreements. See “Inspection of Gold” for a summary of the provisions of the Custody Agreements permitting

the Sponsor and the Trustee and their identified representatives, independent public accountants and physical gold auditors to access

the premises of the Custodian and to examine the physical gold and records maintained by the Custodian pursuant to the Custody Agreements.

The Trustee has no obligation to monitor the activities of the Custodian other than to receive and review such reports of the gold held

for the Trust by such Custodian and of transactions in gold held for the account of the Trust made by such Custodian pursuant to the

Custody Agreements.

Inspection

of Gold

Under

the Custody Agreements, the Custodian will allow the Sponsor and the Trustee and their identified representatives, independent public

accountants and physical gold auditors (currently Bureau Veritas), access to its premises upon reasonable notice during normal business

hours, to examine the physical gold and such records as they may reasonably require to perform their respective duties with regard to

investors in Shares. The Trustee agrees that any such access shall be subject to execution of a confidentiality agreement and agreement

to the Custodian’s security procedures, and any such audit shall be at the Trust’s expense.

Description

of the Shares

General

The

Trustee is authorized under the Trust Agreement to create and issue an unlimited number of Shares. The Trustee creates Shares only in

Baskets (a Basket equals a block of 50,000 Shares) and only upon the order of an Authorized Participant. The Shares represent units of

fractional undivided beneficial interest in and ownership of the Trust and have no par value. Any creation and issuance of Shares above

the amount registered on the Trust’s then-current and effective registration statement with the SEC will require the registration

of such additional Shares.

Description

of Limited Rights

The

Shares do not represent a traditional investment and Shareholders should not view them as similar to “shares” of a corporation

operating a business enterprise with management and a board of directors. Shareholders do not have the statutory rights normally associated

with the ownership of shares of a corporation, including, for example, the right to bring “oppression” or “derivative”

actions. All Shares are of the same class with equal rights and privileges. Each Share is transferable, is fully paid and non-assessable

and entitles the holder to vote on the limited matters upon which Shareholders may vote under the Trust Agreement. The Shares do not

entitle their holders to any conversion or pre-emptive rights, or, except as provided below, any redemption rights or rights to distributions.

Distributions

If

the Trust is terminated and liquidated, the Trustee will distribute to the Shareholders any amounts remaining after the satisfaction

of all outstanding liabilities of the Trust and the establishment of such reserves for applicable taxes, other governmental charges and

contingent or future liabilities as the Trustee shall determine. Shareholders of record on the record date fixed by the Trustee for a

distribution will be entitled to receive their pro rata portion of any distribution.

Voting

and Approvals

Under

the Trust Agreement, Shareholders have no voting rights, except in limited circumstances. The Trustee may terminate the Trust upon the

agreement of Shareholders owning at least 75% of the outstanding Shares. In addition, certain amendments to the Trust Agreement require

advance notice to the Shareholders before the effectiveness of such amendments, but no Shareholder vote or approval is required for any

amendment to the Trust Agreement.

Redemption

of the Shares

The

Shares may only be redeemed by or through an Authorized Participant and only in Baskets.

Book-Entry

Form

Individual

certificates will not be issued for the Shares. Instead, one or more global certificates is deposited by the Trustee with DTC and registered

in the name of Cede & Co., as nominee for DTC. The global certificates evidence all of the Shares outstanding at any time. Under

the Trust Agreement, Shareholders are limited to (1) participants in DTC such as banks, brokers, dealers and trust companies (DTC Participants),

(2) those who maintain, either directly or indirectly, a custodial relationship with a DTC Participant (Indirect Participants), and (3)

those banks, brokers, dealers, trust companies and others who hold interests in the Shares through DTC Participants or Indirect Participants.

The Shares are only transferable through the book-entry system of DTC. Shareholders who are not DTC Participants may transfer their Shares

through DTC by instructing the DTC Participant holding their Shares (or by instructing the Indirect Participant or other entity through

which their Shares are held) to transfer the Shares. Transfers will be made in accordance with standard securities industry practice.

Custody

of the Trust’s Gold

The

Custodian, as instructed by the Trustee on behalf of the Trust, is authorized to accept, on behalf of the Trust, deposits of gold in

unallocated form. Acting on standing instructions specified in the Custody Agreements, the Custodian allocates gold deposited in unallocated

form with the Trust by selecting bars of physical gold for deposit to the Trust Allocated Account. All physical gold allocated to the

Trust must conform to the rules, regulations, practices and customs of the LPPM (including without limitation the good delivery rules

of the LPPM).

Gold

held for the Trust Allocated Account by the Custodian is held at the Custodian’s London vault. Gold temporarily held by the Custodian’s

currently selected sub-custodians and by sub-custodians of sub-custodians may be held in vaults located in England or in other locations.

When physical gold is held for the Trust Allocated Account by a sub-custodian, the Custodian will use, or where applicable require any

sub-custodian to use, commercially reasonable efforts to promptly transport such physical gold held on behalf of the Trust to the Custodian’s

London vault premises at the Custodian’s own cost and risk.

The

Custodian’s vault is managed by The Brink’s Company. The Custodian segregates by identification in its books and records

the Trust’s gold in the Trust Allocated Account from any other gold which it owns or holds for others and requires the sub-custodians

it selects to so segregate the Trust’s gold held by them. This requirement reflects the current custody practice in the London

bullion market and, under the Trust Allocated Account Agreement, the Custodian is deemed to have communicated such requirement by virtue

of its participation in the London bullion market. The Custodian’s books and records are expected, as a matter of current London

bullion market custody practice, to identify every bar of gold held in the Trust Allocated Account in its own vault by refiner, assay,

serial number and weight. Sub-custodians selected by the Custodian are also expected, as a matter of current industry practice, to identify

in their books and records each bar of gold held for the Custodian by serial number and such sub-custodians may use other identifying

information.

The

Sponsor has contracted with a specialist bullion assaying firm to provide biannual inspections of the gold bars held on behalf of the

Trust and the Custodian’s records concerning the Trust Allocated Account and the Trust Unallocated Account as they may be reasonably

required to perform their respective duties to Shareholders. One audit will be conducted at the end of the fiscal year (June 30) and

the other at random, with the consent of the Custodian, on a date selected by the assaying firm.

United

States Federal Income Tax Consequences

The

following discussion of the material United States federal income tax consequences that generally will apply to the purchase, ownership

and disposition of Shares by a U.S. Shareholder (as defined below), and certain United States federal income consequences that may apply

to an investment in Shares by a Non-U.S. Shareholder (as defined below), represents, insofar as it describes conclusions as to United

States federal income tax law and subject to the limitations and qualifications described therein, the opinion of Thompson Hine LLP,

special United States federal income tax counsel to the Sponsor. The discussion below is based on the Internal Revenue Code of 1986,

as amended (the “Code”), Treasury Regulations promulgated thereunder and judicial and administrative interpretations of the

Code, all as in effect on the date of this prospectus and all of which are subject to change either prospectively or retroactively. The

tax treatment of Shareholders may vary depending upon their own particular circumstances. Certain Shareholders (including but not limited

to banks, financial institutions, insurance companies, tax-exempt organizations, broker-dealers, traders, Shareholders that are partnerships

for United States federal income tax purposes, persons holding Shares as a position in a “hedging,” “straddle,”

“conversion,” or “constructive sale” transaction for United States federal income tax purposes, persons whose

“functional currency” is not the U.S. dollar, persons with “applicable financial statements” within the meaning

of Section 451(b) of the Code, or other investors with special circumstances) may be subject to special rules not discussed below. In

addition, the following discussion applies only to investors who will hold Shares as “capital assets” within the meaning

of Section 1221 of the Code. Moreover, the discussion below does not address the effect of any state, local or foreign tax law on an

owner of Shares. Purchasers of Shares are urged to consult their own tax advisers with respect to all federal, state, local and foreign

tax law considerations potentially applicable to their investment in Shares.

For

purposes of this discussion, a “U.S. Shareholder” is a Shareholder that is:

| |

- |

an

individual who is treated as a citizen or resident of the United States for United States federal income tax purposes; |

| |

|

|

| |

- |

a

corporation (or entity treated as a corporation for United States federal income tax purposes) created or organized in or under the

laws of the United States, any state thereof or the District of Columbia; |

| |

|

|

| |

- |

an

estate, the income of which is includible in gross income for United States federal income tax purposes regardless of its source;

or |

| |

|

|

| |

- |

a

trust, if a court within the United States is able to exercise primary supervision over the administration of the trust and one or

more United States persons have the authority to control all substantial decisions of the trust, or a trust that has made a valid

election under applicable Treasury Regulations to be treated as a domestic trust. |

A

Shareholder that is not a U.S. Shareholder as defined above is considered a “Non-U.S. Shareholder” for purposes of this discussion.

If a partnership or other entity or arrangement treated as a partnership for U.S. federal income tax purposes holds Shares, the tax treatment

of a partner generally depends upon the status of the partner and the activities of the partnership. If you are a partner of a partnership

holding Shares, the discussion below may not be applicable and we urge you to consult your own tax adviser for the U.S. federal tax implications

of the purchase, ownership and disposition of such Shares.

Taxation

of the Trust

The

Sponsor and the Trustee will treat the Trust as a “grantor trust” for United States federal income tax purposes. In the opinion

of Thompson Hine LLP, special United States federal income tax counsel to the Sponsor, the Trust will be classified as a “grantor

trust” for United States federal income tax purposes. As a result, the Trust itself will not be subject to United States federal

income tax. Instead, the Trust’s income and expenses will “flow through” to the Shareholders, and the Trustee will

report the Trust’s income, gains, losses and deductions to the Internal Revenue Service (the “IRS”) on that basis.

The opinion of Thompson Hine LLP represents only its best legal judgment and is not binding on the IRS or any court. Accordingly, there

can be no assurance that the IRS will agree with the conclusions of counsel’s opinion and it is possible that the IRS or another

tax authority could assert a position contrary to one or all of those conclusions and that a court could sustain that contrary position.

Neither the Sponsor nor the Trustee will request a ruling from the IRS with respect to the classification of the Trust for United States

federal income tax purposes. If the IRS were to assert successfully that the Trust is not classified as a “grantor trust,”

the Trust would likely be classified as a partnership for United States federal income tax purposes, which may affect the timing and

other tax consequences to the Shareholders.

The

following discussion assumes that the Trust will be classified as a “grantor trust” for United States federal income tax

purposes.

Taxation

of U.S. Shareholders

Shareholders

will be treated, for United States federal income tax purposes, as if they directly owned a pro rata share of the underlying assets held

in the Trust. Shareholders also will be treated as if they directly received their respective pro rata shares of the Trust’s income,

if any, and as if they directly incurred their respective pro rata shares of the Trust’s expenses. In the case of a Shareholder

that purchases Shares for cash, its initial tax basis in its pro rata share of the assets held in the Trust at the time it acquires its

Shares will be equal to its cost of acquiring the Shares. In the case of a Shareholder that acquires its Shares as part of a creation

of a Basket, the delivery of gold to the Trust in exchange for the underlying gold represented by the Shares will not be a taxable event

to the Shareholder, and the Shareholder’s tax basis and holding period for the Shareholder’s pro rata share of the gold held

in the Trust will be the same as its tax basis and holding period for the gold delivered in exchange therefor. For purposes of this discussion,

and unless stated otherwise, it is assumed that all of a Shareholder’s Shares are acquired on the same date and at the same price

per Share. Shareholders that hold multiple lots of Shares, or that are contemplating acquiring multiple lots of Shares, should consult

their own tax advisers as to the determination of the tax basis and holding period for the underlying gold related to such Shares.

When

the Trust sells gold, for example to pay expenses, a Shareholder will recognize gain or loss in an amount equal to the difference between

(a) the Shareholder’s pro rata share of the amount realized by the Trust upon the sale and (b) the Shareholder’s tax basis

for its pro rata share of the gold that was sold. A Shareholder’s tax basis for its share of any gold sold by the Trust generally

will be determined by multiplying the Shareholder’s total basis for its share of all of the gold held in the Trust immediately

prior to the sale, by a fraction the numerator of which is the amount of gold sold, and the denominator of which is the total amount

of the gold held in the Trust immediately prior to the sale. After any such sale, a Shareholder’s tax basis for its pro rata share

of the gold remaining in the Trust will be equal to its tax basis for its share of the total amount of the gold held in the Trust immediately

prior to the sale, less the portion of such basis allocable to its share of the gold that was sold.

Upon

a Shareholder’s sale of some or all of its Shares, the Shareholder will be treated as having sold the portion or all, respectively,

of its pro rata share of the gold held in the Trust at the time of the sale that is attributable to the Shares sold. Accordingly, the

Shareholder generally will recognize gain or loss on the sale in an amount equal to the difference between (a) the amount realized pursuant

to the sale of the Shares, and (b) the Shareholder’s tax basis for the portion of its pro rata share of the gold held in the Trust

at the time of sale that is attributable to the Shares sold, as determined in the manner described in the preceding paragraph.

A

redemption of some or all of a Shareholder’s Shares in exchange for the underlying gold represented by the Shares redeemed generally

will not be a taxable event to the Shareholder. The Shareholder’s tax basis for the gold received in the redemption generally will

be the same as the Shareholder’s tax basis for the portion of its pro rata share of the gold held in the Trust immediately prior

to the redemption that is attributable to the Shares redeemed. The Shareholder’s holding period with respect to the gold received

should include the period during which the Shareholder held the Shares redeemed. A subsequent sale of the gold received by the Shareholder

will be a taxable event, unless a nonrecognition provision of the Code applies to such sale.

After

any sale or redemption of less than all of a Shareholder’s Shares, the Shareholder’s tax basis for its pro rata share of

the gold held in the Trust immediately after such sale or redemption generally will be equal to its tax basis for its share of the total

amount of the gold held in the Trust immediately prior to the sale or redemption, less the portion of such basis which is taken into

account in determining the amount of gain or loss recognized by the Shareholder upon such sale or, in the case of a redemption, that

is treated as the basis of the gold received by the Shareholder in the redemption.

Maximum

28% Long-Term Capital Gains Tax Rate for U.S. Shareholders Who Are Individuals

Under

current law, gains recognized by individuals from the sale of “collectibles,” including gold, held for more than one year

are taxed at a maximum rate of 28%, rather than the current maximum 20% rate applicable to most other long-term capital gains. For these

purposes, gain recognized by an individual upon the sale of an interest in a trust that holds collectibles is treated as gain recognized

on the sale of collectibles, to the extent that the gain is attributable to unrealized appreciation in value of the collectibles held

by the Trust. Therefore, any gain recognized by an individual U.S. Shareholder attributable to a sale of Shares held for more than one

year, or attributable to the Trust’s sale of any gold which the Shareholder is treated (through its ownership of Shares) as having

held for more than one year, generally will be taxed at a maximum federal income tax rate of 28%. The federal income tax rates for capital

gains recognized upon the sale of assets held by an individual U.S. Shareholder for one year or less are generally the same as those

at which ordinary income is taxed. A U.S. corporation’s capital gain is generally taxed at the same federal income tax rates applicable

to the corporation’s ordinary income.

3.8%

Tax on Net Investment Income

Certain

U.S. Shareholders who are individuals are required to pay a 3.8% tax on the lesser of the excess of their modified adjusted gross income

over a threshold amount ($250,000 for married persons filing jointly and $200,000 for single taxpayers) or their “net investment

income,” which generally includes capital gains from the disposition of property. This tax is in addition to any capital gains

taxes due on such investment income. A similar tax applies to estates and trusts. U.S. Shareholders should consult their own tax advisers

regarding the effect, if any, this law may have on their investment in the Shares.