LIONS GATE ENTERTAINMENT CORP /CN/ 00-0000000 0000929351 false 0000929351 2023-12-22 2023-12-22 0000929351 us-gaap:CommonClassAMember 2023-12-22 2023-12-22 0000929351 us-gaap:CommonClassBMember 2023-12-22 2023-12-22 0000929351 dei:OtherAddressMember 2023-12-22 2023-12-22

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 8-K

CURRENT REPORT

PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

Date of Report (Date of earliest event reported): December 22, 2023

Lions Gate Entertainment Corp.

(Exact name of registrant as specified in charter)

British Columbia, Canada

(State or Other Jurisdiction of Incorporation)

|

|

|

| 1-14880 |

|

N/A |

(Commission File Number) |

|

(IRS Employer

Identification No.) |

(Address of principal executive offices)

250 Howe Street 20th Floor

Vancouver, British Columbia V6C 3R8

and

2700 Colorado Avenue

Santa Monica, California 90404

Registrant’s telephone number, including area code: (877) 848-3866

No Change

(Former name or former address, if changed since last report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

| ☐ |

Written Communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| ☒ |

Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| ☐ |

Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| ☐ |

Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Securities registered pursuant to Section 12(b) of the Act:

|

|

|

|

|

Title of Each Class |

|

Trading

Symbol(s) |

|

Name of Each Exchange

on Which Registered |

| Class A Voting Common Shares, no par value per share |

|

LGF.A |

|

New York Stock Exchange |

| Class B Non-Voting Common Shares, no par value per share |

|

LGF.B |

|

New York Stock Exchange |

Indicate by check mark whether the registrant is an emerging growth company as defined in as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

| Item 7.01. |

Regulation FD. |

The information set forth in Item 8.01 is incorporated by reference herein.

On December 22, 2023, the Company and Screaming Eagle published an investor presentation in connection with the Business Combination, a copy of which is furnished with this Current Report on Form 8-K as Exhibit 99.2, and a document containing certain questions and answers regarding the Business Combination, which is furnished with this Current Report on Form 8-K as Exhibit 99.3, and each of which is incorporated by reference herein.

The information set forth in this Item 7.01 of this Current Report on Form 8-K is being furnished and shall not be deemed “filed” for purposes of Section 18 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), nor shall it be deemed incorporated by reference in any filing under the Securities Act of 1933, as amended, or the Exchange Act, except as shall be expressly set forth by specific reference in such a filing.

On December 22, 2023, Lions Gate Entertainment Corp. (the “Company”) issued a press release announcing its entry into a business combination agreement (the “Business Combination Agreement”), dated as of December 22, 2023, with Screaming Eagle Acquisition Corp., a Cayman Islands exempted company (“Screaming Eagle”), SEAC II Corp., a Cayman Islands exempted company and a wholly-owned subsidiary of Screaming Eagle (“New SEAC”), SEAC MergerCo, a Cayman Islands exempted company and a wholly-owned subsidiary of Screaming Eagle, 1455941 B.C. Unlimited Liability Company, a British Columbia unlimited liability company and a wholly-owned subsidiary of Screaming Eagle, LG Sirius Holdings ULC, a British Columbia unlimited liability company and wholly-owned subsidiary of the Company and LG Orion Holdings ULC, a British Columbia unlimited liability company and wholly-owned subsidiary of the Company (“StudioCo”). Pursuant to the terms and conditions of the Business Combination Agreement, the Company’s Studio Business (comprising its Motion Picture and Television Production segments) will be combined with Screaming Eagle through a series of transactions, including an amalgamation of StudioCo and New SEAC under a Canadian plan of arrangement (the “Business Combination”). A copy of the press release is being filed as Exhibit 99.1 to this Current Report on Form 8-K and is incorporated by reference herein.

| Item 9.01 |

Financial Statements and Exhibits. |

(d) Exhibits

Additional Information and Where to Find It

In connection with the transaction, New SEAC intends to file with the U.S. Securities and Exchange Commission (the “SEC”) a registration statement on Form S-4 (the “Registration Statement”), which will include a preliminary proxy statement of Screaming Eagle and a preliminary prospectus of New SEAC, and after the Registration Statement is declared effective, Screaming Eagle will mail the definitive proxy statement/prospectus relating to the transaction to its shareholders and public warrant holders as of the respective record date to be established for voting at the meeting of its shareholders (the “Screaming Eagle Shareholders Meeting”) and public warrant holders (“Screaming Eagle Public Warrant Holder Meeting”) to be held in connection with the transaction. The Registration Statement, including the proxy statement/prospectus contained therein, will contain important information about the transaction and the other matters to be voted upon at the Screaming Eagle Shareholders Meeting and Screaming Eagle Public Warrant Holder Meeting. This communication does not contain all the information that should be considered concerning the transaction and other matters and is not intended to provide the basis for any investment decision or any other decision in respect of such matters. Screaming Eagle, New SEAC and Lionsgate may also file other documents with the SEC regarding the transaction. Screaming Eagle’s shareholders, public warrant holders and other interested persons are advised to read, when available, the Registration Statement, including the preliminary proxy statement/prospectus contained therein, the amendments thereto and the definitive proxy statement/prospectus and other documents filed in connection with the transaction, as these materials will contain important information about Screaming Eagle, New SEAC, Lionsgate, Studio Business and the transaction.

Screaming Eagle’s shareholders, public warrant holders and other interested persons will be able to obtain copies of the Registration Statement, including the preliminary proxy statement/prospectus contained therein, the definitive proxy statement/prospectus and other documents filed or that will be filed with the SEC, free of charge, by Screaming Eagle, New SEAC and Lionsgate through the website maintained by the SEC at www.sec.gov.

Participants in the Solicitation

Screaming Eagle, New SEAC, Lionsgate and their respective directors and officers may be deemed participants in the solicitation of proxies of Screaming Eagle shareholders and public warrant holders in connection with the transaction. More detailed information regarding the directors and officers of Screaming Eagle, and a description of their interests in Screaming Eagle, is contained in Screaming Eagle’s filings with the SEC, including its Annual Report on Form 10-K for the fiscal year ended December 31, 2022, which was filed with the SEC on March 1, 2023, and is available free of charge at the SEC’s website at www.sec.gov. Information regarding the persons who may, under SEC rules, be deemed participants in the solicitation of proxies of Screaming Eagle’s shareholders and public warrant holders in connection with the transaction and other matters to be voted upon at the Screaming Eagle Shareholders Meeting and Screaming Eagle Public Warrant Holders Meeting will be set forth in the Registration Statement for the transaction when available.

Forward-Looking Statements

This Current Report includes certain statements that may constitute “forward-looking statements” within the meaning of Section 27A of the Securities Act, and Section 21E of the Exchange Act. Forward-looking statements include, but are not limited to, statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions. The words “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intends,” “may,” “might,” “plan,” “possible,” “potential,” “predict,” “project,” “seek,” “should,” “target,” “would” and similar expressions may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking. Forward-looking statements may include, for example, statements about the Screaming Eagle or Lionsgate’s ability to effectuate the transaction discussed in this document; the benefits of the transaction; the future financial performance of Lionsgate Studios (which will be the go-forward public company following the completion of the transaction) following the transactions; changes in Lionsgate’s strategy, future operations, financial position, estimated revenues and losses, projected costs, prospects, plans and objectives of management. These forward-looking statements are based on information available as of the date of this document, and current expectations, forecasts and assumptions, and involve a number of judgments, risks and uncertainties. Accordingly, forward-looking statements should not be relied upon as representing Screaming Eagle, Lionsgate or New SEAC’s views as of any subsequent date, and none of Screaming Eagle, Lionsgate or New SEAC undertakes any obligation to update forward-looking statements to reflect events or circumstances after the date they were made, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws. Neither New SEAC nor Screaming Eagle gives any assurance that either New SEAC or Screaming Eagle will achieve its expectations. You should not place undue reliance on these forward-looking statements. As a result of a number of known and unknown risks and uncertainties, New SEAC’s actual results or performance may be materially different from those expressed or implied by these forward-looking statements. Some factors that could cause actual results to differ include: (i) the timing to complete the transaction by Screaming Eagle’s business combination deadline and the potential failure to obtain an extension of the business combination deadline if sought by Screaming Eagle; (ii) the occurrence of any event, change or other circumstances that could give rise to the termination of the definitive agreements relating to the transaction; (iii) the outcome of any legal, regulatory or governmental proceedings that may be instituted against New SEAC, Screaming Eagle, Lionsgate or any investigation or inquiry following announcement of the transaction, including in connection with the transaction; (iv) the inability to complete the transaction due to the failure to obtain approval of Screaming Eagle’s shareholders or Screaming Eagle’s public warrant holders; (v) Lionsgate’s and New SEAC’s success in retaining or recruiting, or changes required in, its officers, key employees or directors following the transaction; (vi) the ability of the parties to obtain the listing of Lionsgate Studios’ Common Shares on a national securities exchange upon the date of closing of the transaction; (vii) the risk that the transaction disrupts current plans and operations of Lionsgate; (viii) the ability to recognize the anticipated benefits of the transaction; (ix) unexpected costs related to the transaction; (x) the amount of redemptions by Screaming Eagle’s public shareholders being greater than expected; (xi) the management and board composition of Lionsgate Studios following completion of the transaction; (xii) limited liquidity and trading of Lionsgate Studios’ securities following completion of the transactions; (xiii) changes in domestic and foreign business, market, financial, political and legal conditions; (xiv) the possibility that Lionsgate or Screaming Eagle may be adversely affected by other economic, business, and/or competitive factors; (xv) operational risks; (xvi) litigation and regulatory enforcement risks, including the diversion of management time and attention and the additional costs and demands on Lionsgate’s resources; (xvii) the risk that the consummation of the transaction is substantially delayed or does not occur; and (xix) other risks and uncertainties indicated from time to time in the Registration Statement, including those under “Risk Factors” therein, and in the other filings of Screaming Eagle, New SEAC and Lionsgate with the SEC.

No Offer or Solicitation

This Current Report does not constitute (i) a solicitation of a proxy, consent or authorization with respect to any securities or in respect of the transaction or (ii) an offer to sell, a solicitation of an offer to buy, or a recommendation to purchase, any securities of Lionsgate, Screaming Eagle, the combined company or any of their respective affiliates. No offering of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the Securities Act of 1933, as amended, or an exemption therefrom, nor shall any sale of securities in any states or jurisdictions in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction be affected. No securities commission or securities regulatory authority in the United States or any other jurisdiction has in any way passed upon the merits of the transaction or the accuracy or adequacy of this communication.

Signature

Pursuant to the requirements of the Securities Exchange Act of 1934, as amended, the Registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

Date: December 22, 2023

|

|

|

| LIONS GATE ENTERTAINMENT CORP. |

| (Registrant) |

|

|

| By: |

|

/s/ James W. Barge |

| Name: |

|

James W. Barge |

| Title: |

|

Chief Financial Officer |

Exhibit 99.1

LIONSGATE STUDIOS TO LAUNCH AS A SEPARATELY TRADED PUBLIC COMPANY

Establishes One of the Largest Publicly Traded Pure Play Content Companies with an Enterprise Value of Approximately $4.6 Billion

Deal Expected to Raise Approximately $350 Million of Total Gross Proceeds

Upsized $175 Million in Committed PIPE (Private Investment in Public Equity) Financing Led by Top Mutual Fund Investors

Transaction Enabled by Business Combination with Screaming Eagle Acquisition Corp.

Common Shares of Lionsgate Studios Will Trade as a Single Class of Stock Separately from Lionsgate Class A and Class B Shares

(LGF.A, LGF.B)

SANTA MONICA, CA, and VANCOUVER, BC, December 22, 2023 – Lionsgate (NYSE: LGF.A, LGF.B)

today announced that its Studio Business, comprising its Television Studio and Motion Picture Group segments and one of the world’s most valuable film and television libraries, will be combined with Screaming Eagle

Acquisition Corp. (Nasdaq: SCRM) (“Screaming Eagle”) to launch Lionsgate Studios Corp. (“Lionsgate Studios”). Screaming Eagle is a publicly-traded company formed to merge with existing businesses.

The deal positions the standalone Lionsgate Studios as a platform-agnostic, pure play content company with a deep portfolio of franchise

properties including The Hunger Games, John Wick, The Twilight Saga and Ghosts, a robust film and television production and distribution business, a leading talent management and production company and a world-class film and

television library.

As a result of the transaction, 87.3% of the total shares of Lionsgate Studios are expected to continue to be held by

Lionsgate, while Screaming Eagle public shareholders and founders and common equity financing investors are expected to own an aggregate of approximately 12.7% of the combined company. The transaction values Lionsgate Studios at an enterprise

value of approximately $4.6 billion. Lionsgate Studios does not include the STARZ platform, which will continue to be wholly owned by Lionsgate.

In addition to establishing Lionsgate Studios as a standalone publicly-traded entity, the transaction is expected to deliver approximately

$350 million of gross proceeds to Lionsgate, including $175 million in PIPE financing already committed by leading mutual funds and other

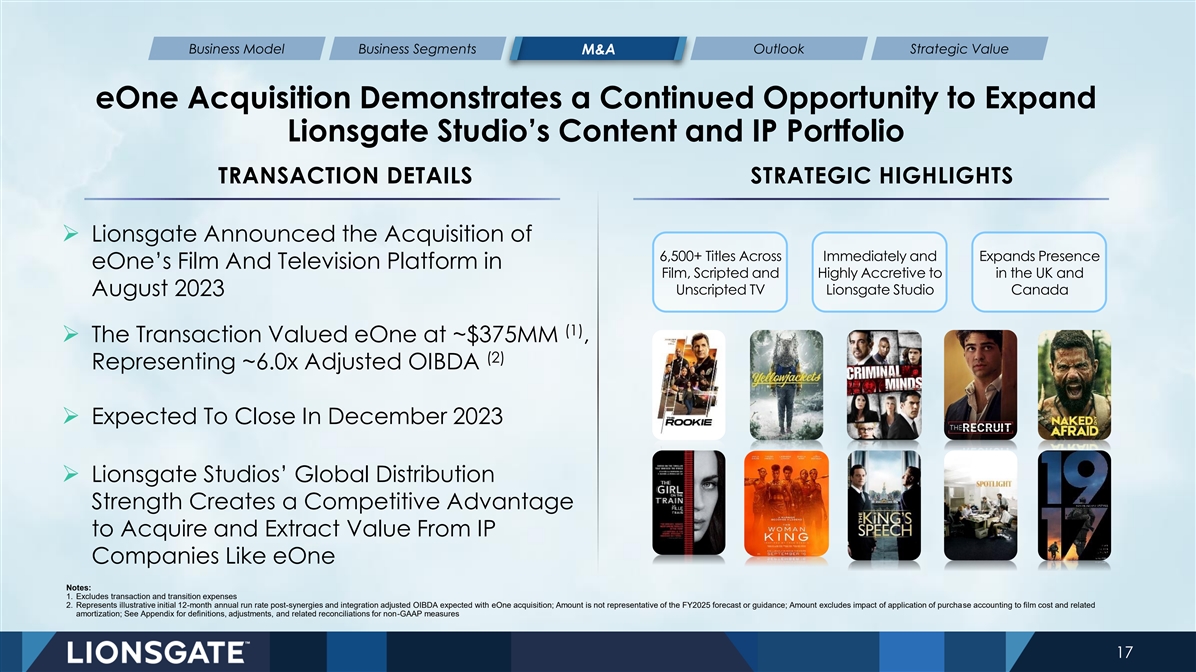

investors. Net proceeds from the transaction are expected to be used to enhance Lionsgate’s balance sheet and facilitate strategic initiatives, including those related to the eOne business,

which acquisition is scheduled to close by calendar year end.

Common shares of Lionsgate Studios will trade separately from

Lionsgate’s Class A (LGF.A) and Class B (LGF.B) common shares as a single class of stock. The transaction is subject to certain closing conditions, including regulatory approvals and approval from the shareholders and public

warrant holders of Screaming Eagle, and is expected to close in the spring of 2024.

“This transaction creates one of the world’s

largest publicly-traded pure play content platforms with the ability to deliver significant incremental value to all of our stakeholders,” said Lionsgate CEO Jon Feltheimer and Vice Chair Michael Burns. “Coupled with the

acquisition of the eOne platform scheduled to close next week, the expansion of our partnership with 3 Arts and the strong performance of our content slates, we’ve put together all of the pieces for a thriving standalone content company with a

strong financial growth trajectory.”

“We are thrilled to be part of establishing Lionsgate Studios as one of the only pure play

content companies in the public markets, which is well positioned to unlock value for both existing and new shareholders,” said Screaming Eagle CEO Eli Baker. “We believe this will be seen as one of the most innovative and value

creating transactions the market has seen in some time.”

Transaction Details

The transaction is expected to deliver approximately $350 million of gross proceeds to Lionsgate, consisting of $175 million in

gross proceeds from a committed PIPE and $175 million in proceeds from the Screaming Eagle trust. Net proceeds from the transaction will be used to enhance Lionsgate’s balance sheet and facilitate strategic initiatives including the

eOne acquisition which is scheduled to close by calendar year end.

Due to tax and other considerations, Lionsgate Studios has made it a

condition of the transaction to receive not more than $175 million of gross trust proceeds. In the event that unredeemed amounts exceed $175 million, such non-redeeming shareholders will receive a

mix of consideration in the form of shares in Lionsgate Studios and cash (from Screaming Eagle) (as cash value in trust), pro-rata with all other non-redeeming

shareholders (excluding PIPE investors and those investors committing to non-redemption arrangements).

It is also a condition of closing that all of Screaming Eagle’s public and private placement warrants be eliminated. Screaming Eagle

private placement warrants will be eliminated for no consideration. Screaming Eagle’s public warrants will be repurchased for $0.50 per warrant from warrant holders pursuant to one of the voting proposals associated with the business

combination. Screaming Eagle has obtained the written consent from warrant holders owning approximately 44.19% of all public warrants outstanding to vote in favor of the public warrant repurchase. For all public warrants to be compulsorily acquired

for $0.50 per warrant, an additional 5.81% is required to be obtained prior to the voting date for the business combination.

Upon closing of the transaction, it is expected that Lionsgate shareholders will indirectly

own an approximately 87.3% stake in Lionsgate Studios, while Screaming Eagle public shareholders, founders and PIPE investors will own approximately 5.7%, 0.7% and 6.3% of Lionsgate Studios, respectively. Screaming Eagle founders and

independent directors will collectively forfeit approximately 14.5 million of their founder shares and will retain approximately 2.0 million common shares upfront and Screaming Eagle founders will be entitled to receive an additional

2.2 million common shares if the trading price of Lionsgate Studios common shares increases 50% from $10.70. In connection with the transaction, the Screaming Eagle founders will forfeit all of their Screaming Eagle private placement

warrants.

Lionsgate is expected to maintain its current corporate debt structure in this transaction.

Morgan Stanley & Co. LLC (“Morgan Stanley”) is acting as financial advisor to Lionsgate. Citigroup Global Markets Inc.

(“Citigroup”) is acting as financial advisor to Screaming Eagle. Citigroup and Morgan Stanley are acting as co-placement agents for Screaming Eagle with respect to the common equity financing.

Wachtell, Lipton, Rosen & Katz is acting as legal advisor to Lionsgate and Denton’s Canada LLP is acting as legal advisor to Lionsgate in Canada. White & Case LLP is acting as legal advisor to Screaming Eagle and Goodmans

LLP is acting as legal advisor to Screaming Eagle in Canada. Davis Polk & Wardwell LLP is acting as legal advisor to Citigroup and Morgan Stanley in connection with their roles as co-placement

agents.

Lionsgate senior management will hold a call to discuss the transaction on Thursday, January 4, at 5:00 PM ET/2:00

PM PT. Interested parties may listen to the live webcast by visiting the events page on the Lionsgate Investor Relations website or via the following link. A full replay will become available the evening of

January 4 by clicking the same link. Answers to Frequently Asked Questions can be found as Exhibit 99.3 to our Current Report on Form 8-K filed with the Securities and Exchange Commission on

December 22, 2023.

About Lionsgate

Lionsgate (NYSE: LGF.A, LGF.B) encompasses world-class motion picture and television studio operations aligned with the STARZ premium

subscription platform to bring a unique and varied portfolio of entertainment to consumers around the world. Lionsgate’s film, television, subscription and location-based entertainment businesses are backed by a 18,000-title library and a valuable collection of iconic film and television franchises. A digital age company driven by its entrepreneurial culture and commitment to innovation, the Lionsgate brand is synonymous

with bold, original, relatable entertainment for audiences worldwide.

###

For further information, investors should contact:

Nilay Shah

310-255-3651

nshah@lionsgate.com

For media inquiries, please contact:

Peter D. Wilkes

310-255-3726

pwilkes@lionsgate.com

Additional Information About the Transaction and Where to Find It

In connection with the transaction, a subsidiary of Screaming Eagle (“New Screaming Eagle”) intends to file with the U.S. Securities and Exchange

Commission (the “SEC”) a registration statement on Form S-4 (the “Registration Statement”), which will include a preliminary proxy statement of Screaming Eagle and a preliminary prospectus

of New Screaming Eagle, and after the Registration Statement is declared effective, Screaming Eagle will mail the definitive proxy statement/prospectus relating to the transaction to its shareholders and public warrant holders as of the respective

record date to be established for voting at the meeting of its shareholders (the “Screaming Eagle Shareholders Meeting”) and public warrant holders (“Screaming Eagle Public Warrant Holder Meeting”) to be held in connection with

the transaction. The Registration Statement, including the proxy statement/prospectus contained therein, will contain important information about the transaction and the other matters to be voted upon at the Screaming Eagle Shareholders Meeting and

Screaming Eagle Public Warrant Holder Meeting. This communication does not contain all the information that should be considered concerning the transaction and other matters and is not intended to provide the basis for any investment decision or any

other decision in respect of such matters. Screaming Eagle, New Screaming Eagle and Lionsgate may also file other documents with the SEC regarding the transaction. Screaming Eagle’s shareholders, public warrant holders and other interested

persons are advised to read, when available, the Registration Statement, including the preliminary proxy statement/prospectus contained therein, the amendments thereto and the definitive proxy statement/prospectus and other documents filed in

connection with the transaction, as these materials will contain important information about Screaming Eagle, New Screaming Eagle, Lionsgate, Studio Business and the transaction.

Screaming Eagle’s shareholders, public warrant holders and other interested persons will be able to obtain copies of the Registration Statement,

including the preliminary proxy statement/prospectus contained therein, the definitive proxy statement/prospectus and other documents filed or that will be filed with the SEC, free of charge, by Screaming Eagle, New Screaming Eagle and Lionsgate

through the website maintained by the SEC at www.sec.gov.

Participants in the Solicitation

Screaming Eagle, New Screaming Eagle, Lionsgate and their respective directors and officers may be deemed participants in the solicitation of proxies of

Screaming Eagle shareholders and public warrant holders in connection with the transaction. More detailed information regarding the directors and officers of Screaming Eagle, and a description of their interests in Screaming Eagle, is contained in

Screaming Eagle’s filings with the SEC, including its Annual Report on Form 10-K

for the fiscal year ended December 31, 2022, which was filed with the SEC on March 1, 2023, and is available free of charge at the SEC’s website at www.sec.gov. Information

regarding the persons who may, under SEC rules, be deemed participants in the solicitation of proxies of Screaming Eagle’s shareholders and public warrant holders in connection with the transaction and other matters to be voted upon at the

Screaming Eagle Shareholders Meeting and SEAC Public Warrant Holders Meeting will be set forth in the Registration Statement for the transaction when available.

Forward-Looking Statements

This

communication includes certain statements that may constitute “forward-looking statements” within the meaning of Section 27A of the Securities Act, and Section 21E of the Exchange Act. Forward-looking statements include, but are

not limited to, statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions. The words “anticipate,” “believe,” “continue,”

“could,” “estimate,” “expect,” “intends,” “may,” “might,” “plan,” “possible,” “potential,” “predict,” “project,” “seek,”

“should,” “target,” “would” and similar expressions may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking. Forward-looking statements may include,

for example, statements about the Screaming Eagle or Lionsgate’s ability to effectuate the transaction discussed in this document; the benefits of the transaction; the future financial performance of Lionsgate Studios (which will be the go-forward public company following the completion of the transaction) following the transactions; changes in Lionsgate’s strategy, future operations, financial position, estimated revenues and losses,

projected costs, prospects, plans and objectives of management. These forward-looking statements are based on information available as of the date of this document, and current expectations, forecasts and assumptions, and involve a number of

judgments, risks and uncertainties. Accordingly, forward-looking statements should not be relied upon as representing Screaming Eagle, Lionsgate or New Screaming Eagle’s views as of any subsequent date, and none of Screaming Eagle, Lionsgate or

New Screaming Eagle undertakes any obligation to update forward-looking statements to reflect events or circumstances after the date they were made, whether as a result of new information, future events or otherwise, except as may be required under

applicable securities laws. Neither New Screaming Eagle nor Screaming Eagle gives any assurance that either New Screaming Eagle or Screaming Eagle will achieve its expectations. You should not place undue reliance on these forward-looking

statements. As a result of a number of known and unknown risks and uncertainties, New Screaming Eagle’s actual results or performance may be materially different from those expressed or implied by these forward-looking statements. Some factors

that could cause actual results to differ include: (i) the timing to complete the transaction by Screaming Eagle’s business combination deadline and the potential failure to obtain an extension of the business combination deadline if

sought by Screaming Eagle; (ii) the occurrence of any event, change or other circumstances that could give rise to the termination of the definitive agreements relating to the transaction; (iii) the outcome of any legal, regulatory or

governmental proceedings that may be instituted against New Screaming Eagle, Screaming Eagle, Lionsgate or any investigation or inquiry following announcement of the transaction, including in connection with the transaction; (iv) the inability

to complete the transaction due to the failure to obtain approval of Screaming Eagle’s shareholders or Screaming Eagle’s public warrant holders; (v) Lionsgate’s and New Screaming Eagle’s success in retaining or recruiting,

or changes required in, its officers,

key employees or directors following the transaction; (vi) the ability of the parties to obtain the listing of Lionsgate Studios’ Common Shares on a national securities exchange upon

the date of closing of the transaction; (vii) the risk that the transaction disrupts current plans and operations of Lionsgate; (viii) the ability to recognize the anticipated benefits of the transaction; (ix) unexpected costs related

to the transaction; (x) the amount of redemptions by Screaming Eagle’s public shareholders being greater than expected; (xi) the management and board composition of Lionsgate Studios following completion of the transaction;

(xii) limited liquidity and trading of Lionsgate Studios’ securities following completion of the transactions; (xiii) changes in domestic and foreign business, market, financial, political and legal conditions, (xiv) the

possibility that Lionsgate or Screaming Eagle may be adversely affected by other economic, business, and/or competitive factors; (xv) operational risks; (xvi) litigation and regulatory enforcement risks, including the diversion of

management time and attention and the additional costs and demands on Lionsgate’s resources; (xvii) the risk that the consummation of the transaction is substantially delayed or does not occur; and (xix) other risks and uncertainties

indicated from time to time in the Registration Statement, including those under “Risk Factors” therein, and in the other filings of Screaming Eagle, New Screaming Eagle and Lionsgate with the SEC.

No Offer or Solicitation

This

communication does not constitute (i) a solicitation of a proxy, consent or authorization with respect to any securities or in respect of the transaction or (ii) an offer to sell, a solicitation of an offer to buy, or a recommendation to

purchase, any securities of Lionsgate, Screaming Eagle, the combined company or any of their respective affiliates. No offering of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the Securities

Act of 1933, as amended, or an exemption therefrom, nor shall any sale of securities in any states or jurisdictions in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any

such jurisdiction be affected. No securities commission or securities regulatory authority in the United States or any other jurisdiction has in any way passed upon the merits of the transaction or the accuracy or adequacy of this communication.

Additional Information Available on Lionsgate’s Website

The information in this press release should be read in conjunction with the financial statements and footnotes contained in the Lionsgate Quarterly

Report on Form 10-Q for the quarter ended September 30, 2023, which has been posted on Lionsgate’s website

at http://investors.lionsgate.com/financial-reports/sec-filings.

Reconciliation of non-GAAP forward-looking

measures

for the fiscal years ending March 31, 2024 and March 31, 2025

Adjusted OIBDA: Adjusted OIBDA is defined as operating income (loss) before adjusted depreciation and amortization (“OIBDA”), adjusted

for adjusted share-based compensation (“adjusted SBC”), purchase accounting and related adjustments, restructuring and other costs, certain charges (benefits) related to the COVID-19 global pandemic,

certain programming and content charges as a result of management changes and/or changes in strategy, and unusual gains or losses (such as goodwill and intangible asset impairment and charges related to Russia’s invasion of Ukraine), when

applicable.

| |

• |

|

Adjusted depreciation and amortization represents depreciation and amortization as presented on our consolidated

statement of operations, less the depreciation and amortization related to the amortization of purchase accounting and related adjustments associated with recent acquisitions. Accordingly, the full impact of the purchase accounting is included in

the adjustment for “purchase accounting and related adjustments”, described below. |

| |

• |

|

Adjusted share-based compensation represents share-based compensation excluding the impact of the acceleration of

certain vesting schedules for equity awards pursuant to certain severance arrangements, which are included in restructuring and other expenses, when applicable. |

| |

• |

|

Restructuring and other includes restructuring and severance costs, certain transaction and other costs, and

certain unusual items, when applicable. |

| |

• |

|

COVID-19 related charges or benefits include incremental costs associated

with the pausing and restarting of productions including paying/hiring certain cast and crew, maintaining idle facilities and equipment costs, and when applicable, certain motion picture and television impairments and development charges associated

with changes in performance expectations or the feasibility of completing the project resulting from circumstances associated with the COVID-19 global pandemic, net of insurance recoveries, which are included

in direct operating expense, when applicable. In addition, the costs include early or contractual marketing spends for film releases and events that have been canceled or delayed and will provide no economic benefit, which are included in

distribution and marketing expense, when applicable. |

| |

• |

|

Programming and content charges include certain charges as a result of changes in management and/or changes in

programming and content strategy, which are included in direct operating expenses, when applicable. |

| |

• |

|

Purchase accounting and related adjustments primarily represent the amortization of non-cash fair value adjustments to certain assets acquired in recent acquisitions. These adjustments include the accretion of the noncontrolling interest discount related to Pilgrim Media Group and 3 Arts

Entertainment, the non-cash charge for the amortization of the recoupable portion of the purchase price and the expense associated with the noncontrolling equity interests in the distributable earnings related

to 3 Arts Entertainment, all of which are accounted for as compensation and are included in general and administrative expense. |

Adjusted OIBDA is calculated similar to how Lionsgate defines segment profit and manages and evaluates its

segment operations. Segment profit also excludes corporate general and administrative expense.

Total Segment Profit and Studio Business Segment

Profit and Studio Business Adjusted OIBDA: We present the sum of our Motion Picture and Television Production segment profit as our “Studio Business” segment profit, and we define our Studio Business Adjusted OIBDA as Studio

Business segment profit less corporate general and administrative expenses. Total segment profit and Studio Business segment profit and Studio Business Adjusted OIBDA, when presented outside of the segment information and reconciliations included in

our consolidated financial statements, is considered a non-GAAP financial measure, and should be considered in addition to, not as a substitute for, or superior to, measures of financial performance prepared

in accordance with United States GAAP. We use this non-GAAP measure, among other measures, to evaluate the aggregate operating performance of our business.

Lionsgate believes the presentation of total segment profit and Studio Business segment profit is relevant and useful for investors because it allows

investors to view total segment performance in a manner similar to the primary method used by Lionsgate’s management and enables them to understand the fundamental performance of Lionsgate’s businesses before

non-operating items. Total segment profit and Studio Business segment profit is considered an important measure of Lionsgate’s performance because it reflects the aggregate profit contribution from

Lionsgate’s segments, both in total and for the Studio Business and represents a measure, consistent with our segment profit, that eliminates amounts that, in management’s opinion, do not necessarily reflect the fundamental performance of

Lionsgate’s businesses, are infrequent in occurrence, and in some cases are non-cash expenses. Not all companies calculate segment profit or total segment profit in the same manner, and segment profit and

total segment profit as defined by Lionsgate may not be comparable to similarly titled measures presented by other companies due to differences in the methods of calculation and excluded items.

Overall: These measures are non-GAAP financial measures as defined in Regulation G promulgated by

the SEC and are in addition to, not a substitute for, or superior to, measures of financial performance prepared in accordance with United States GAAP.

We use these non-GAAP measures, among other measures, to evaluate the operating performance of our business. We

believe these measures provide useful information to investors regarding our results of operations and cash flows before non-operating items. Adjusted OIBDA is considered an important measure of

Lionsgate’s performance because this measure eliminates amounts that, in management’s opinion, do not necessarily reflect the fundamental performance of Lionsgate’s businesses, are infrequent in occurrence, and in some cases are non-cash expenses.

These non-GAAP measures are commonly used in the

entertainment industry and by financial analysts and others who follow the industry to measure operating performance. However, not all companies calculate these measures in the same manner and the measures as presented may not be comparable to

similarly titled measures presented by other companies due to differences in the methods of calculation and excluded items.

A general limitation of these non-GAAP financial measures is that

they are not prepared in accordance with U.S. generally accepted accounting principles. These measures should be reviewed in conjunction with the relevant GAAP financial measures and are not presented as alternative measures of operating income as

determined in accordance with GAAP.

The following table sets forth Total Studio Business segment profit, Studio Business Adjusted OIBDA and Adjusted

OIBDA on an actual basis for the fiscal years ended March 31, 2022 and 2023 and forecasted for the fiscal years ended March 31, 2024 and 2025:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Fiscal Year

Ended

March 31,

2022 |

|

|

Fiscal Year

Ended

March 31,

2023 |

|

|

Fiscal Year

Ended

March 31,

2024 |

|

|

Fiscal Year

Ended

March 31,

2025 |

|

| |

|

Actual |

|

|

Actual |

|

|

Estimated |

|

|

Estimated |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

(Unaudited, amounts in millions) |

|

| Total Studio Business Segment

Profit(1) |

|

$ |

346.8 |

|

|

$ |

409.9 |

|

|

$ |

445.0 |

|

|

$ |

500.0 |

|

| Corporate general and administrative expenses |

|

|

(97.1 |

) |

|

|

(122.9 |

) |

|

|

(125.0 |

) |

|

|

(130.0 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Studio Business Adjusted

OIBDA(1) |

|

$ |

249.7 |

|

|

$ |

287.0 |

|

|

$ |

320.0 |

(2) |

|

$ |

370.0 |

|

| Media Networks segment profit |

|

|

155.2 |

|

|

|

106.8 |

|

|

|

200.0 |

(3) |

|

|

Not Provided |

|

| Intersegment eliminations |

|

|

(2.7 |

) |

|

|

(35.7 |

) |

|

|

(100.0 |

) |

|

|

Not Provided |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Adjusted OIBDA(1) |

|

$ |

402.2 |

|

|

$ |

358.1 |

|

|

$ |

420.0 |

|

|

|

Not Provided |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| (1) |

See above for the definition of Studio Business Segment Profit, Studio Business Adjusted OIBDA and Adjusted

OIBDA and see below for the reconciliation to the most directly comparable GAAP financial measure. |

| (2) |

Represents consensus as of November 9, 2023 and is within the Studio Business guidance range of

$300 million to $350 million. |

| (3) |

Represents consensus as of November 9, 2023 and is within the Media Networks segment guidance range of

$175 million to $200 million. |

The following table reconciles the GAAP measure, operating income (loss) to the non-GAAP, forward looking projected measure, Adjusted OIBDA and Total Segment Profit on an actual basis for the fiscal year ended March 31, 2022 and 2023 and forecasted for the fiscal year ending March 31,

2024 and March 31, 2025:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Fiscal Year

Ended

March 31,

2022 |

|

|

Fiscal Year

Ended

March 31,

2023 |

|

|

Fiscal Year

Ended

March 31,

2024 |

|

|

Fiscal Year

Ended

March 31,

2025 |

|

| |

|

Actual |

|

|

Actual |

|

|

Estimated |

|

|

Estimated |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

(Unaudited, amounts in millions) |

|

| Operating income (loss) |

|

$ |

9.0 |

|

|

$ |

(1,857.7 |

) |

|

|

NRE |

|

|

|

NRE |

|

| Goodwill and intangible asset impairment |

|

|

— |

|

|

|

1,475.0 |

|

|

|

663.9 |

|

|

|

NRE |

|

| Adjusted depreciation and amortization |

|

|

43.0 |

|

|

|

40.2 |

|

|

|

41.0 |

|

|

|

NRE |

|

| Restructuring and other(1) |

|

|

16.8 |

|

|

|

411.9 |

|

|

|

NRE |

|

|

|

NRE |

|

| COVID-19 related charges (benefit)(2) |

|

|

(3.4 |

) |

|

|

(11.6 |

) |

|

|

NRE |

|

|

|

NRE |

|

| Programming and content charges(3) |

|

|

36.9 |

|

|

|

7.0 |

|

|

|

NRE |

|

|

|

NRE |

|

| Charges related to Russia’s invasion of Ukraine |

|

|

5.9 |

|

|

|

— |

|

|

|

NRE |

|

|

|

NRE |

|

| Adjusted share-based compensation

expense(4) |

|

|

100.0 |

|

|

|

97.8 |

|

|

|

NRE |

|

|

|

NRE |

|

| Purchase accounting and related

adjustments(5) |

|

|

194.0 |

|

|

|

195.5 |

|

|

|

NRE |

|

|

|

NRE |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Adjusted OIBDA |

|

$ |

402.2 |

|

|

$ |

358.1 |

|

|

$ |

420.0 |

|

|

|

Not Provided |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

NRE:

Individual items are not reasonably estimated due to the nature of the items.

| |

(1) |

Restructuring and other is intended by its very nature for unusual items and thus not reasonably estimable.

We’ve had restructuring and other charges in the past, which have included severance charges, and transaction, integration costs and legal costs associated with certain strategic transactions, restructuring activities and legal matters.

|

| |

(2) |

COVID-19 related charges (benefit) are not predictable due to the

nature of the COVID-19 pandemic. However, the charges we are incurring have been diminishing, and insurance recovery exceeded the charges in fiscal 2023. Given the unpredictability of these charges and the

insurance recovery, we are unable to provide a reliable estimate. |

| |

(3) |

Programming and content charges include certain charges as a result of changes in management and/or changes in

programming and content strategy, which are included in direct operating expenses, when applicable. Due to these costs being associated with unusual events, we are unable to provide a reliable estimate of these costs, if any, to be incurred in the

future. |

| |

(4) |

Forecasting the future market price of Lionsgate’s common shares is inherently difficult, which impacts

share-based compensation and accordingly, we are unable to reliably estimate these amounts. |

| |

(5) |

Purchase accounting and related adjustments primarily represent the amortization of non-cash fair value adjustments to certain assets acquired in recent acquisitions. These amounts may vary significantly depending on the level of future acquisitions, and thus we are unable to provide a reliable

estimate. |

The following table reconciles the GAAP measure, operating income (loss) to the non-GAAP, forward looking projected measure, Adjusted OIBDA forecasted for the estimated initial 12 month run-rate of eOne post the completion of the eOne integration into

Lionsgate and realization of transaction synergies:

|

|

|

|

|

| |

|

Estimated

Initial 12 Month

Run-Rate of eOne

Adjusted OIBDA |

|

| |

|

(Unaudited amounts

in millions) |

|

| Operating income (loss) |

|

|

NRE |

|

| Adjusted depreciation and amortization |

|

|

NRE |

|

| Restructuring and other(1) |

|

|

NRE |

|

| Adjusted share-based compensation

expense(2) |

|

|

NRE |

|

| Purchase accounting and related

adjustments(3) |

|

|

NRE |

|

|

|

|

|

|

| Adjusted OIBDA |

|

$ |

60.0 |

(4) |

|

|

|

|

|

NRE:

Individual items are not reasonably estimated due to the nature of the items.

Note: Certain reconciling items included in the Lionsgate reconciliation

table are excluded from the eOne reconciliation table as they are not currently expected to occur.

| |

(1) |

Restructuring and other is intended by its very nature for unusual items and thus not reasonably estimable.

We’ve had restructuring and other charges in the past, which have included severance charges, and transaction, integration costs and legal costs associated with certain strategic transactions, restructuring activities and legal matters.

|

| |

(2) |

Forecasting the future market price of Lionsgate’s common shares is inherently difficult, which impacts

share-based compensation and accordingly, we are unable to reliably estimate these amounts. |

| |

(3) |

Purchase accounting and related adjustments primarily represent the amortization of non-cash fair value adjustments to certain assets acquired in recent acquisitions. These amounts may vary significantly depending on the level of future acquisitions, and thus we are unable to provide a reliable

estimate. These amounts exclude any adjustment to fair value for the allocation of the purchase price of eOne to the film and television program assets acquired, and related amortization expense. |

| |

(4) |

Illustrative initial 12 month run-rate post-synergies and integration

adjusted OIBDA expected with the eOne acquisition. Represents the mid-point of the $50 million to $75 million estimate. For clarity, this amount is not meant to be the fiscal 2025 forecast or

guidance, and this amount excludes the impact of the application of purchase accounting to the film cost and related amortization, as described in footnote (3) above. |

Safe Harbor Statement

The preceding forward-looking

projection of Adjusted OIBDA over the fiscal year ending 2024 represents a forward-looking statement and projection based on expectations, assumptions and estimates that Lionsgate believes are reasonable given its assessment of historical trends and

other information reasonably available as of November 9, 2023. Forward-looking statements can often be identified by words such as “expect” and “anticipate”. The amounts consist of projections only, and are subject to a wide

range of known and unknown business risks and uncertainties, including

those, described in Lionsgate’s Securities and Exchange and Commission (“SEC”) filings referred to below, many of which are beyond Lionsgate’s control. Forward-looking

statements such as those contained above should not be regarded as representations by Lionsgate that the projected results will be achieved. Projections and estimates are necessarily speculative in nature and actual results may vary materially from

the outlook Lionsgate provides today. Lionsgate undertakes no obligation to publicly update or revise any forward-looking statements, including the forecasts set forth herein, except as required by law.

The forecast set forth above should be read together with Lionsgate’s Annual Report on Form 10-K for the year

ended March 31, 2023 including the risks identified under “Item 1A. Risk Factors” and Lionsgate’s other SEC filings.

Exhibit 99.2 Lionsgate Studios Investor Presentation December

2023

Disclaimer This presentation (together with oral statements made in

connection herewith, this “Presentation”) is provided for informational purposes only and has been prepared to assist interested parties in making their own evaluation with respect to a potential business combination involving LG Orion

Holdings Inc. (“LG Studio” or the “Company”), a wholly owned subsidiary of Lions Gate Entertainment Corp. (“Lionsgate”) created to hold the Studio Business of Lionsgate and Screaming Eagle Acquisition Corp.

(“SEAC”) and related transactions (the “Proposed Business Combination”) and for no other purpose. By accepting this Presentation, you acknowledge and agree that all of the information contained herein or disclosed orally

during this Presentation is confidential, that you will not copy, reproduce, distribute, disclose or use such information for any purpose without the prior written consent of Lionsgate other than for the purpose of your firm’s participation in

the potential financing, and that you will return to LG Studio, Lionsgate and SEAC or delete or destroy this Presentation (with confirmation thereof) upon request. No representations or warranties, express or implied are given in, or in respect of,

the accuracy or completeness of this Presentation or any other information (whether written or oral) that has been or will be provided to you. You also acknowledge that (i) the United States securities laws restrict persons with material non-public

information about a company from purchasing or selling securities of such company or certain other companies, or from communicating such information to any other person under circumstances in which it is reasonably foreseeable that such person is

likely to purchase or sell such securities on the basis of such information, (ii) you are familiar with the Securities Exchange Act of 1934, as amended (the Exchange Act ), and the legal and regulatory sanctions attached to the misuse, disclosure or

improper circulation of this Presentation, and (iii) you will neither use, nor cause any third party to use, this Presentation or any information contained herein in contravention of the Exchange Act, including, without limitation, Rule 10b-5

thereunder. You also acknowledge that Canadian securities laws restrict those persons who are in a “special relationship” (as defined under Canadian securities laws) with an issuer and who know of a material fact or material change with

respect to the issuer, which material fact or material change has not been generally disclosed, from (i) entering into a transaction involving a security of an issuer, or a related financial instrument of a security of an issuer, (ii) informing

another person of a material fact or material change with respect to the issuer, or (iii) recommending or encouraging another person to enter into a transaction involving a security of the issuer or a related financial instrument of a security of

the issuer, subject to certain exceptions. To the fullest extent permitted by law, in no circumstances will SEAC, LG Studio, Lionsgate, or any of their respective subsidiaries, stockholders, affiliates, representatives, partners, directors,

officers, employees, advisers or agents be responsible or liable for any direct, indirect or consequential loss or loss of profit arising from the use of this Presentation, its contents, its omissions, reliance on the information contained within

it, or on opinions communicated in relation thereto or otherwise arising in connection therewith. In addition, this Presentation does not purport to be all-inclusive or to contain all of the information that may be required to make a full analysis

of LG Studio or the Proposed Business Combination. You also acknowledge and agree that the information contained in this Presentation is preliminary in nature and is subject to change, and any such changes may be material. Any information, data or

statistics on past performance or modeling contained herein is not an indication as to future performance. SEAC, Lionsgate and LG Studio assume no obligation to update the information in this Presentation. Viewers of this Presentation should each

make their own evaluation of LG Studio and of the relevance and adequacy of the information contained herein or disclosed orally and should make such other investigations as they deem necessary. Nothing herein should be construed as legal,

financial, tax or other advice. You should consult your own advisers concerning any legal, financial, tax or other considerations concerning the opportunity described herein. The information included in this Presentation cannot address, and are not

intended to address, your specific investment objectives, financial situations or financial needs. SEAC, Lionsgate and LG Studio are engaged in ongoing negotiations of a potential business combination agreement (“BCA”) with respect to

the Proposed Business Combination. The Proposed Business Combination is subject to, among other things, the approval by SEAC’s stockholders, entry into definitive documentation (including a BCA), satisfaction of the conditions stated in any

BCA and other closing conditions. Accordingly, there can be no assurance that the Proposed Business Combination will be consummated. Investing in the securities to be issued in connection with the potential financing involves a high degree of risk.

Investors should carefully consider the risks and uncertainties inherent in an investment in the securities before subscribing for the securities. The Summary Risk Factors contained herein are not the only ones the parties face. Additional risks

that the parties currently do not know about or that they currently believe to be immaterial may also impair their business, financial condition or results of operations. You should perform your own due diligence prior to making an investment in

SEAC and/or LG Studio. This Presentation does not constitute, and under no circumstances is it to be construed as, an offer, advertisement or invitation for the sale or purchase of the securities, assets or business described herein or a commitment

to LG Studio, Lionsgate or SEAC with respect to any of the foregoing, and this Presentation shall not form the basis of any contract. LG Studio, Lionsgate and SEAC expressly reserve the right, at any time and in any respect, to amend or terminate

this process, to terminate discussion with any or all potential investors, to accept or reject any proposals and to negotiate with, or cease negotiations with, any party regarding a transaction involving LG Studio and SEAC. This Presentation shall

not constitute a “solicitation” as defined in Section 14 of the Exchange Act. This Presentation does not constitute an offer, or a solicitation of an offer, to buy or sell any securities, investment or any other specific product, or a

solicitation of any vote or approval, nor shall there be any sale of securities, investment or other specific product in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the

securities laws of any such jurisdiction. Any offering of securities (the “Securities”) as contemplated in connection with this presentation will not be registered under the Securities Act of 1933, as amended (the “Securities

Act”), and will be offered as a private placement to a limited number of institutional “accredited investors” as defined in Rule 501(a)(1), (2), (3) or (7) under the Securities Act and “Institutional Accounts” as

defined in FINRA Rule 4512(c). Accordingly, the Securities must continue to be held unless a subsequent disposition is registered or exempt from the registration requirements of the Securities Act. SEAC, Lionsgate and LG Studio reserve the right to

amend or terminate discussions with any or all potential investors, to accept or reject any proposals and to negotiate with, or cease negotiations with, any party regarding any transaction involving SEAC, Lionsgate and LG Studio for any reason.

There shall not be any offer or sale of any securities in any jurisdiction where, or to any person to whom, such offer or sale may be unlawful under the laws of such jurisdiction. Investors should consult with their counsel as to the applicable

requirements for a purchaser to avail itself of any exemption under the Securities Act. The transfer of the Securities may also be subject to conditions set forth in an agreement under which they are to be issued. Investors should be aware that they

may be required to bear the financial risk of their investment for an indefinite period of time. None of Lionsgate, LG Studio or SEAC is making an offer of any Securities in any state or other jurisdiction where the offer is not permitted. Neither

the U.S. Securities and exchange commission (“SEC”) nor any state or provincial securities commission or securities regulatory authority has approved or disapproved of the securities or determined if this presentation is truthful or

complete. If the Proposed Business Combination is pursued, SEAC, LG Studio or one of their respective affiliates will be required to file a registration statement on Form S-4 (or other applicable SEC form) relating to the Proposed Business

Combination, SEAC will be required to file a proxy statement, and the parties will be required to file other relevant documents with the SEC. You are urged to read the proxy statement/prospectus and any other relevant documents filed with the SEC

when they become available because, among other things, they will contain updates to the financial, industry and other information herein as well as important information about SEAC, LG Studio and the Proposed Business Combination. When available,

the proxy statement/prospectus and other relevant materials for the Proposed Business Combination will be mailed to stockholders of SEAC as of a record date to be established for voting on the proposed Business Combination. Stockholders will also be

able to obtain copies of the preliminary proxy statement/prospectus and other documents filed with the SEC, without charge, once available, at the SEC’s website at www.sec.gov. Forward-looking statements and risk factors All statements other

than statements of historical facts contained in this Presentation are forward-looking statements. Forward-looking statements may generally be identified by the use of words such as “believe,” “may,” “will,”

“estimate,” “continue,” “anticipate,” “intend,” “expect,” “should,” “would,” “plan,” “project,” “forecast,”

“predict,” “potential,” “seem,” “seek,” “future,” “outlook,” “target” or other similar expressions that predict or indicate future events or trends or that are not

statements of historical matters. These forward-looking statements include, but are not limited to, statements regarding estimates and forecasts of financial and performance metrics and projections of market opportunity and market share. These

statements are based on management’s current estimations and analysis, are subject to various assumptions that the parties believe are reasonable at this time, whether or not identified in this Presentation, reflect the current expectations

Lionsgate’s management as of the date of this Presentation and are not predictions of actual performance. 2

Disclaimer Forward-looking statements and risk factors (cont’d)

These forward-looking statements are provided for illustrative purposes only and are not intended to serve as and must not be relied on by any investor as, a guarantee, an assurance, a prediction or a definitive statement of fact or probability.

Actual events and circumstances are difficult or impossible to predict and may differ from assumptions and such differences may be material. Many actual events and circumstances are beyond the control of LG Studio, Lionsgate and SEAC. These

forward-looking statements are subject to a number of risks and uncertainties, including changes in domestic and foreign business, market, financial, political and legal conditions; the inability of the parties to successfully or timely consummate

the Proposed Business Combination, including the risk that any required regulatory approvals are not obtained, are delayed or are subject to unanticipated conditions that could adversely affect the combined company or the expected benefits of the

Proposed Business Combination or that the approval of the stockholders of SEAC is not obtained; failure to realize the anticipated benefits of the Proposed Business Combination; risks relating to the uncertainty of the projected financial

information with respect to Lionsgate’s Studio business; the effects of competition on Lionsgate’s Studio business; the amount of redemption requests made by SEAC’s public stockholders; the ability of SEAC or the combined company

to issue equity or equity- linked securities in connection with the Proposed Business Combination or in the future; the risk of litigation and/or regulatory actions related to the Proposed Business Combination; diversion of management time from

ongoing business operations due to the Proposed Business Combination; the risk that the Proposed Business Combination could have an adverse effect on the ability of Lionsgate’s Studio business to retain customers and retain and hire key

personnel and maintain relationships with customers, suppliers, employees, stockholders and other business relationships; and those factors discussed under the heading “Risk Factors” in SEAC’s Annual Report on Form 10-K filed with

the SEC on March 1, 2023, SEAC’s Quarterly Report on Form 10-Q filed with the SEC on September 9, 2023, Lionsgate’s Annual Report on Form 10-K filed with the SEC on May 25, 2023, Lionsgate’s Quarterly Report on Form 10-Q filed with

the SEC on November 9, 2023, Lionsgate’s Proxy Statement Pursuant to Section 14(a) of the Securities Exchange Act of 1934 filed with the SEC on October 13, 2023, LG Studio’s registration statement on Form 10 filed with the SEC on July

12, 2023 and other periodic public filings of SEAC, LG Studio or Lionsgate filed, or to be filed, with the SEC, any provincial securities commissions or securities regulatory authorities in Canada, or on the SEDAR+ website at www.sedarplus.ca, as

applicable . You should also carefully consider the risks and uncertainties described in the “Risk Factors” section of the proxy statement/prospectus on Form S-4 (or other applicable SEC form) relating to the Proposed Business

Combination, which is expected to be filed with the SEC, and other documents filed from time to time with the SEC. These filings identify and address other important risks and uncertainties that could cause actual events and results to diverge

materially from those contained in the forward-looking statements in this presentation. If any of these risks materialize or SEAC’s, Lionsgate’s or LG Studio’s assumptions prove incorrect, actual results could differ materially

from the results implied by these forward-looking statements. There may be additional risks that neither SEAC, Lionsgate nor LG Studio presently know or that SEAC, Lionsgate and LG Studio currently believe are immaterial that could also cause actual

results to differ from those contained in the forward-looking statements. In addition, forward-looking statements reflect Lionsgate’s expectations, plans or forecasts of future events and views as of the date of this Presentation. SEAC,

Lionsgate and LG Studio anticipate that subsequent events and developments will cause their assessments to change. It is not possible to predict all risks, nor assess the impact of all factors on LG Studio’s business or the extent to which any

factor, or combination of factors, may cause LG Studio’s actual results, performance or financial condition to be materially different from the expectations of future results, performance or financial condition. In addition, the analyses of

Lionsgate, LG Studio and SEAC contained herein are not, and do not purport to be, appraisals or the securities, assets or business of LG Studio, SEAC or any other entity. While SEAC, Lionsgate and LG Studio may elect to update these forward-looking

statements at some point in the future, SEAC, Lionsgate and LG Studio specifically disclaim any obligation to do so. These forward-looking statements should not be relied upon as representing SEAC’s, Lionsgate’s and LG Studio’s

assessments as of any date subsequent to the date of this Presentation. Accordingly, undue reliance should not be placed upon the forward-looking statements. Use of projections The projections, estimates and targets in this Presentation are

forward-looking statements that are based on assumptions that are inherently subject to significant uncertainties and contingences, many of which are beyond Lionsgate’s, LG Studio’s and SEAC’s control. Lionsgate’s and

SEAC’s independent auditors did not audit, review, compile or perform any procedures with respect to such projections, estimates, or targets for the purpose of their inclusion in this Presentation, and accordingly, such auditors neither

expressed an opinion nor provided any other form of assurance with respect thereto for the purpose of this Presentation. While all protections, estimates, and targets are necessarily speculative, LG Studio and Lionsgate believe that the preparation

of prospective financial information involves increasingly higher levels of uncertainty the further out the projection, estimate, or target extends from the date of preparation. The assumptions and estimates underlying projected, expected, or

targeted results are inherently uncertain and are subject to a wide variety of risks and uncertainties, including but not limited to those mentioned in the immediately preceding paragraph, that could cause actual results to differ materially from

those contained in such projections, estimates, and targets. The inclusion of projections, estimates, and targets in this Presentation should not be regarded as an indication that Lionsgate, LG Studio, SEAC, or their respective representatives

considered or consider such financial projections, estimates, and targets to be a reliable prediction of future events. See “Forward-looking Statements” above. To the extent any forward-looking information in this presentation

constitutes “future-oriented financial information” or “financial outlooks” within the meaning of applicable Canadian securities laws, such information is being provided to demonstrate the potential benefits of the Proposed

Business Combination, and the reader is cautioned that this information may not be appropriate for any other purpose and the reader should not place undue reliance on such future-oriented financial information and financial outlooks. Future-oriented

financial information and financial outlooks, as with forward-looking information generally, are, without limitation, based on the assumptions and subject to the risks set out herein. The results of operations and estimated and forecasted revenue of

Lionsgate, LG Studio and/or SEAC may differ materially from management’s current expectations. Such information is presented for illustrative purposes only and may not be an indication of the actual future results of operations or earnings of

Lionsgate, LG Studio and/or SEAC. Industry and market data In this Presentation, Lionsgate and LG Studio may rely on and refer to certain information and statistics obtained from third-party sources which they believe to be reliable. Lionsgate and

LG Studio have not independently verified the accuracy or completeness of any such third-party information. No representation is made as to the reasonableness of the assumptions made within or the accuracy or completeness of any such third-party

information, and you are cautioned not to place undue weight on such information. Participants in the solicitation SEAC and its directors and executive officers may be deemed participants in the solicitation of proxies from SEAC’s stockholders

with respect to the Proposed Business Combination. A list of the names of those directors and executive officers and a description of their interests in SEAC is contained in SEAC’s final prospectus related to its initial public offering dated

January 7, 2022, which was filed with the SEC and is available free of charge at the SEC’s web site at www.sec.gov, or by directing a request to: roconnor@eaglesinvest.com. Additional information regarding the interests of such participants

will be contained in the proxy statement/prospectus for the proposed Business Combination when available. Lionsgate and LG Studio and their respective directors and executive officers may also be deemed to be participants in the solicitation of

proxies from the stockholders of SEAC in connection with the proposed Business Combination. A list of the names of such directors and executive officers and information regarding their interests in the proposed Business Combination will be included

in the proxy statement/prospectus for the proposed Business Combination when available. Investment in any securities described herein has not been approved or disapproved by the Securities and Exchange Commission or any state or provincial

securities commission or securities regulatory authority nor has any authority passed upon or endorsed the merits of the offering or the accuracy or adequacy of the information contained herein any representation to the contrary is a criminal

offense. LG Studio, Lionsgate and SEAC reserve the right to negotiate with one or more parties and to enter into a definitive agreement relating to the transaction at any time and without prior notice to the recipient or any other person or entity.

LG Studio, Lionsgate and SEAC also reserve the right, at any time and without prior notice and without assigning any reason therefor, (i) to terminate the further participation by the recipient or any other person or entity in the consideration of,

and proposed process relating to, the transaction, (ii) to modify any of the rules or procedures relating to such consideration and proposed process and (iii) to terminate entirely such consideration and proposed process. No representation or

warranty (whether express or implied) has been made by LG Studio, Lionsgate, SEAC or any of their respective directors, officers, employees, affiliates, agents, advisors or representatives with respect to the proposed process or the manner in which

the proposed process is conducted, and the recipient disclaims any such representation or warranty. The recipient acknowledges that LG Studio, Lionsgate, SEAC and their respective directors, officers, employees, affiliates, agents, advisors or

representatives are under no obligation to accept any offer or proposal by any person or entity regarding the transaction. None of LG Studio, Lionsgate, SEAC or any of their respective directors, officers, employees, affiliates, agents, advisors or

representatives has any legal, fiduciary or other duty to any recipient with respect to the manner in which the proposed process is conducted. 3

Lionsgate Studios and Screaming Eagle Presenters JON MICHAEL BURNS JIMMY

FELTHEIMER BARGE Vice Chairman, Lionsgate Chief Executive Officer, Chief Financial Officer, Lionsgate Lionsgate HARRY ELI SLOAN BAKER Chairman, Chief Executive Officer, Screaming Eagle Screaming Eagle 4

A Standalone Lionsgate Studios Unlocks Value as a Pure-Play Content

Company Platform-Agnostic, Pure-Play Content Studio Benefits from a $2.9Bn 1 Changing Industry Ecosystem FY24E Revenue Double Digit Lower Risk Film and TV Model Generates Strong, Steady FY24E to FY25E 2 AOIBDA Growth AOIBDA Growth +12.5% Deep

Portfolio of Franchise Film and TV Intellectual Property 3 Reported Library and Enduring Library Rights (1) Revenue CAGR Focused M&A Strategy to Enhance the Library and Core 14 4 Acquisitions Business Segments (2) Since 2000 10.7x 28.8x 5 Unique

and Valuable Strategic Asset Investor Median Historical (3) (4) Entry Multiple Takeout Comps Enables Direct Investment in a Standalone Studio and its World-Class IP with a Single Share Class Notes: 1. FY2019A-FY2023A CAGR; Reported Library Revenue