0000827099false--12-31FY20220.0012000000001843704691743704690.0010.00112500001000270000027800518750230000051875023000001250730.130.1300120000600008270992022-01-012022-12-310000827099cpwr:SeriesDPreferredStockThreeMember2022-01-012022-12-310000827099cpwr:SeriesDPreferredStockFourMember2022-01-012022-12-310000827099cpwr:SeriesDPreferredStockFiveMember2022-01-012022-12-310000827099cpwr:CeoMemberus-gaap:SeriesDPreferredStockMember2022-01-012022-12-310000827099cpwr:CeoMemberus-gaap:SeriesDPreferredStockMember2022-12-310000827099cpwr:RelatedPartyNotePayable1Member2021-12-310000827099cpwr:RelatedPartyNotePayable1Member2022-12-310000827099cpwr:CompanyCEOMember2022-01-012022-12-310000827099cpwr:CompanyCEOMember2021-01-012021-12-310000827099cpwr:OneJanuaryTwentyElevenMembercpwr:EmploymentAgreementMembersrt:ChiefExecutiveOfficerMember2022-01-012022-12-310000827099cpwr:ConsultingAgreementMember2018-08-012018-08-140000827099cpwr:ConsultingAgreementMember2022-01-012022-12-310000827099cpwr:TradeBaseSalesIncMember2019-05-012019-05-280000827099cpwr:BrettMRegalMember2019-05-012019-05-2800008270992018-05-302018-07-1900008270992018-08-012018-08-0800008270992018-08-012018-08-2200008270992019-08-012019-08-1500008270992017-06-012017-06-260000827099cpwr:SeriesDPreferredStockTwoMember2021-12-310000827099cpwr:SeriesDPreferredStockOneMember2021-12-310000827099cpwr:SeriesDPreferredStockTwoMember2022-12-310000827099cpwr:SeriesDPreferredStockOneMember2022-12-3100008270992018-05-220000827099cpwr:SeriesDPreferredStockTwoMember2022-01-012022-12-310000827099cpwr:CommonStocksTwoMember2022-01-012022-12-310000827099cpwr:WarrantsMember2022-12-310000827099cpwr:WarrantsMember2020-12-310000827099cpwr:WarrantsMember2021-12-310000827099srt:MaximumMembercpwr:RemeasurementDateMember2021-01-012021-12-310000827099srt:MinimumMembercpwr:RemeasurementDateMember2021-01-012021-12-310000827099srt:MaximumMembercpwr:RemeasurementDateMember2022-01-012022-12-310000827099srt:MinimumMembercpwr:RemeasurementDateMember2022-01-012022-12-310000827099cpwr:RemeasurementDateMember2021-01-012021-12-310000827099cpwr:RemeasurementDateMember2022-01-012022-12-310000827099us-gaap:FairValueInputsLevel3Member2021-12-310000827099us-gaap:FairValueInputsLevel2Member2021-12-310000827099us-gaap:FairValueInputsLevel1Member2021-12-310000827099us-gaap:FairValueInputsLevel3Member2022-12-310000827099us-gaap:FairValueInputsLevel2Member2022-12-310000827099us-gaap:FairValueInputsLevel1Member2022-12-310000827099cpwr:CommonStocksOneMember2021-01-012021-12-310000827099cpwr:CommonStocksOneMember2022-01-012022-12-310000827099us-gaap:SeriesDPreferredStockMember2022-01-012022-12-310000827099cpwr:NotePayableTotalMember2021-12-310000827099cpwr:NotePayableTotalMember2022-12-310000827099cpwr:NotePayableThirtySevenMember2021-12-310000827099cpwr:NotePayableThirtySixMember2021-12-310000827099cpwr:NotePayableThirtyFiveMember2021-12-310000827099cpwr:NotePayableThirtyFourMember2021-12-310000827099cpwr:NotePayableThirtyThreeMember2021-12-310000827099cpwr:NotePayableThirtyTwoMember2021-12-310000827099cpwr:NotePayableThirtyOneMember2021-12-310000827099cpwr:NotePayableThirtyMember2021-12-310000827099cpwr:NotePayableTwentyNineMember2021-12-310000827099cpwr:NotePayableTwentyEightMember2021-12-310000827099cpwr:NotePayableTwentySevenMember2021-12-310000827099cpwr:NotePayableTwentySixMember2021-12-310000827099cpwr:NotePayableTwentyFiveMember2021-12-310000827099cpwr:NotePayableTwentyFourMember2021-12-310000827099cpwr:NotePayableTwentyThreeMember2021-12-310000827099cpwr:NotePayableTwentyTwoMember2021-12-310000827099cpwr:NotePayableTWentyOneMember2021-12-310000827099cpwr:NotePayableTwentyMember2021-12-310000827099cpwr:NotePayableNinteenMember2021-12-310000827099cpwr:NotePayableEighteenMember2021-12-310000827099cpwr:NotePayableSeventeenMember2021-12-310000827099cpwr:NotePayableSixteenMember2021-12-310000827099cpwr:NotePayableFifteenMember2021-12-310000827099cpwr:NotePayableFourteenMember2021-12-310000827099cpwr:NotePayableThirteenMember2021-12-310000827099cpwr:NotePayableTwelveMember2021-12-310000827099cpwr:NotePayableElevenMember2021-12-310000827099cpwr:NotePayableTenMember2021-12-310000827099cpwr:NotePayableNineMember2021-12-310000827099cpwr:NotePayableEightMember2021-12-310000827099cpwr:NotePayableSevenMember2021-12-310000827099cpwr:NotePayableSixMember2021-12-310000827099cpwr:NotePayableFiveMember2021-12-310000827099cpwr:NotePayableFourMember2021-12-310000827099cpwr:NotePayableThreeMember2021-12-310000827099cpwr:NotePayableTwoMember2021-12-310000827099cpwr:NotePayableOneMember2021-12-310000827099cpwr:NotePayableThirtySevenMember2022-12-310000827099cpwr:NotePayableThirtySixMember2022-12-310000827099cpwr:NotePayableThirtyFiveMember2022-12-310000827099cpwr:NotePayableThirtyFourMember2022-12-310000827099cpwr:NotePayableThirtyThreeMember2022-12-310000827099cpwr:NotePayableThirtyTwoMember2022-12-310000827099cpwr:NotePayableThirtyOneMember2022-12-310000827099cpwr:NotePayableThirtyMember2022-12-310000827099cpwr:NotePayableTwentyNineMember2022-12-310000827099cpwr:NotePayableTwentyEightMember2022-12-310000827099cpwr:NotePayableTwentySevenMember2022-12-310000827099cpwr:NotePayableTwentySixMember2022-12-310000827099cpwr:NotePayableTwentyFiveMember2022-12-310000827099cpwr:NotePayableTwentyFourMember2022-12-310000827099cpwr:NotePayableTwentyThreeMember2022-12-310000827099cpwr:NotePayableTwentyTwoMember2022-12-310000827099cpwr:NotePayableTWentyOneMember2022-12-310000827099cpwr:NotePayableTwentyMember2022-12-310000827099cpwr:NotePayableNinteenMember2022-12-310000827099cpwr:NotePayableEighteenMember2022-12-310000827099cpwr:NotePayableSeventeenMember2022-12-310000827099cpwr:NotePayableSixteenMember2022-12-310000827099cpwr:NotePayableFifteenMember2022-12-310000827099cpwr:NotePayableFourteenMember2022-12-310000827099cpwr:NotePayableThirteenMember2022-12-310000827099cpwr:NotePayableTwelveMember2022-12-310000827099cpwr:NotePayableElevenMember2022-12-310000827099cpwr:NotePayableTenMember2022-12-310000827099cpwr:NotePayableNineMember2022-12-310000827099cpwr:NotePayableEightMember2022-12-310000827099cpwr:NotePayableSevenMember2022-12-310000827099cpwr:NotePayableSixMember2022-12-310000827099cpwr:NotePayableFiveMember2022-12-310000827099cpwr:NotePayableFourMember2022-12-310000827099cpwr:NotePayableThreeMember2022-12-310000827099cpwr:NotePayableTwoMember2022-12-310000827099cpwr:NotePayableOneMember2022-12-310000827099cpwr:NotePayableThirtySevenMember2021-01-012021-12-310000827099cpwr:NotePayableThirtySixMember2021-01-012021-12-310000827099cpwr:NotePayableThirtyFiveMember2021-01-012021-12-310000827099cpwr:NotePayableThirtyFourMember2021-01-012021-12-310000827099cpwr:NotePayableThirtyThreeMember2021-01-012021-12-310000827099cpwr:NotePayableThirtyTwoMember2021-01-012021-12-310000827099cpwr:NotePayableThirtyOneMember2021-01-012021-12-310000827099cpwr:NotePayableThirtyMember2021-01-012021-12-310000827099cpwr:NotePayableTwentyNineMember2021-01-012021-12-310000827099cpwr:NotePayableTwentyEightMember2021-01-012021-12-310000827099cpwr:NotePayableTwentySevenMember2021-01-012021-12-310000827099cpwr:NotePayableTwentySixMember2021-01-012021-12-310000827099cpwr:NotePayableTwentyFiveMember2021-01-012021-12-310000827099cpwr:NotePayableTwentyFourMember2021-01-012021-12-310000827099cpwr:NotePayableTwentyThreeMember2021-01-012021-12-310000827099cpwr:NotePayableTwentyTwoMember2021-01-012021-12-310000827099cpwr:NotePayableTWentyOneMember2021-01-012021-12-310000827099cpwr:NotePayableTwentyMember2021-01-012021-12-310000827099cpwr:NotePayableNinteenMember2021-01-012021-12-310000827099cpwr:NotePayableEighteenMember2021-01-012021-12-310000827099cpwr:NotePayableSeventeenMember2021-01-012021-12-310000827099cpwr:NotePayableSixteenMember2021-01-012021-12-310000827099cpwr:NotePayableFifteenMember2021-01-012021-12-310000827099cpwr:NotePayableFourteenMember2021-01-012021-12-310000827099cpwr:NotePayableThirteenMember2021-01-012021-12-310000827099cpwr:NotePayableTwelveMember2021-01-012021-12-310000827099cpwr:NotePayableElevenMember2021-01-012021-12-310000827099cpwr:NotePayableTenMember2021-01-012021-12-310000827099cpwr:NotePayableNineMember2021-01-012021-12-310000827099cpwr:NotePayableEightMember2021-01-012021-12-310000827099cpwr:NotePayableSevenMember2021-01-012021-12-310000827099cpwr:NotePayableSixMember2021-01-012021-12-310000827099cpwr:NotePayableFiveMember2021-01-012021-12-310000827099cpwr:NotePayableFourMember2021-01-012021-12-310000827099cpwr:NotePayableThreeMember2021-01-012021-12-310000827099cpwr:NotePayableTwoMember2021-01-012021-12-310000827099cpwr:NotePayableOneMember2021-01-012021-12-310000827099cpwr:NotePayableThirtySevenMember2022-01-012022-12-310000827099cpwr:NotePayableThirtySixMember2022-01-012022-12-310000827099cpwr:NotePayableThirtyFiveMember2022-01-012022-12-310000827099cpwr:NotePayableThirtyFourMember2022-01-012022-12-310000827099cpwr:NotePayableThirtyThreeMember2022-01-012022-12-310000827099cpwr:NotePayableThirtyTwoMember2022-01-012022-12-310000827099cpwr:NotePayableThirtyOneMember2022-01-012022-12-310000827099cpwr:NotePayableThirtyMember2022-01-012022-12-310000827099cpwr:NotePayableTwentyNineMember2022-01-012022-12-310000827099cpwr:NotePayableTwentyEightMember2022-01-012022-12-310000827099cpwr:NotePayableTwentySevenMember2022-01-012022-12-310000827099cpwr:NotePayableTwentySixMember2022-01-012022-12-310000827099cpwr:NotePayableTwentyFiveMember2022-01-012022-12-310000827099cpwr:NotePayableTwentyFourMember2022-01-012022-12-310000827099cpwr:NotePayableTwentyThreeMember2022-01-012022-12-310000827099cpwr:NotePayableTwentyTwoMember2022-01-012022-12-310000827099cpwr:NotePayableTWentyOneMember2022-01-012022-12-310000827099cpwr:NotePayableTwentyMember2022-01-012022-12-310000827099cpwr:NotePayableNinteenMember2022-01-012022-12-310000827099cpwr:NotePayableEighteenMember2022-01-012022-12-310000827099cpwr:NotePayableSeventeenMember2022-01-012022-12-310000827099cpwr:NotePayableSixteenMember2022-01-012022-12-310000827099cpwr:NotePayableFifteenMember2022-01-012022-12-310000827099cpwr:NotePayableFourteenMember2022-01-012022-12-310000827099cpwr:NotePayableThirteenMember2022-01-012022-12-310000827099cpwr:NotePayableTwelveMember2022-01-012022-12-310000827099cpwr:NotePayableElevenMember2022-01-012022-12-310000827099cpwr:NotePayableTenMember2022-01-012022-12-310000827099cpwr:NotePayableNineMember2022-01-012022-12-310000827099cpwr:NotePayableEightMember2022-01-012022-12-310000827099cpwr:NotePayableSevenMember2022-01-012022-12-310000827099cpwr:NotePayableSixMember2022-01-012022-12-310000827099cpwr:NotePayableFiveMember2022-01-012022-12-310000827099cpwr:NotePayableFourMember2022-01-012022-12-310000827099cpwr:NotePayableThreeMember2022-01-012022-12-310000827099cpwr:NotePayableTwoMember2022-01-012022-12-310000827099cpwr:NotePayableOneMember2022-01-012022-12-3100008270992022-03-110000827099cpwr:MRFeakinsMember2022-01-012022-12-310000827099cpwr:MRFeakinsMember2022-12-310000827099us-gaap:ConvertiblePreferredStockMember2022-01-012022-12-310000827099us-gaap:ConvertiblePreferredStockMember2021-01-012021-12-310000827099us-gaap:ConvertibleNotesPayableMember2022-01-012022-12-310000827099cpwr:WarrantsMember2022-01-012022-12-310000827099us-gaap:ConvertibleNotesPayableMember2021-01-012021-12-310000827099cpwr:WarrantsMember2021-01-012021-12-310000827099cpwr:OCEESInternationalMember2022-01-012022-12-310000827099cpwr:OceanThermalEnergyBahamasLtdMember2022-01-012022-12-310000827099cpwr:OTEBMMember2022-01-012022-12-310000827099us-gaap:RetainedEarningsMember2022-12-310000827099us-gaap:AdditionalPaidInCapitalMember2022-12-310000827099us-gaap:CommonStockMember2022-12-310000827099us-gaap:PreferredStockMember2022-12-310000827099us-gaap:RetainedEarningsMember2022-01-012022-12-310000827099us-gaap:AdditionalPaidInCapitalMember2022-01-012022-12-310000827099us-gaap:CommonStockMember2022-01-012022-12-310000827099us-gaap:PreferredStockMember2022-01-012022-12-310000827099us-gaap:RetainedEarningsMember2021-12-310000827099us-gaap:AdditionalPaidInCapitalMember2021-12-310000827099us-gaap:CommonStockMember2021-12-310000827099us-gaap:PreferredStockMember2021-12-310000827099us-gaap:RetainedEarningsMember2021-01-012021-12-310000827099us-gaap:AdditionalPaidInCapitalMember2021-01-012021-12-310000827099us-gaap:CommonStockMember2021-01-012021-12-310000827099us-gaap:PreferredStockMember2021-01-012021-12-3100008270992020-12-310000827099us-gaap:RetainedEarningsMember2020-12-310000827099us-gaap:AdditionalPaidInCapitalMember2020-12-310000827099us-gaap:CommonStockMember2020-12-310000827099us-gaap:PreferredStockMember2020-12-3100008270992021-01-012021-12-310000827099us-gaap:SeriesDPreferredStockMember2021-12-310000827099us-gaap:SeriesDPreferredStockMember2022-12-310000827099us-gaap:SeriesCPreferredStockMember2021-12-310000827099us-gaap:SeriesCPreferredStockMember2022-12-310000827099us-gaap:SeriesBPreferredStockMember2021-12-310000827099us-gaap:SeriesBPreferredStockMember2022-12-3100008270992021-12-3100008270992022-12-3100008270992023-08-18iso4217:USDxbrli:sharesiso4217:USDxbrli:sharesxbrli:pure

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2022

or

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _____________ to ___________________

Commission File No. 033-19411-C

OCEAN THERMAL ENERGY CORPORATION |

(Exact name of registrant as specified in its charter) |

Nevada | | 20-5081381 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

3675 Market Street, Suite 200, Philadelphia PA 19104

(Address of principal executive offices, including Zip Code)

717-299-1344

(Registrant’s telephone number, including area code)

Securities Registered pursuant to Section 12(b) of the Exchange Act:

Title of Class | | Trading Symbol | | Name of Each Exchange on Which Registered |

N/A | | N/A | | N/A |

Securities Registered pursuant to Section 12(g) of the Exchange Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☐ No ☒

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☐ No ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ☐ | Accelerated filer | ☐ |

Non-accelerated filer | ☒ | Smaller reporting company | ☒ |

Emerging growth company | ☐ | | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to § 240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter. The aggregate market value of the voting and nonvoting common equity held by nonaffiliates computed as of the price at which the common equity was last sold on the last business day of the registrant’s most recently completed second fiscal quarter was $1,692,066.

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date. As of August 18, 2023, there were 184,370,469 shares of the registrant’s common stock outstanding, par value $0.001.

DOCUMENTS INCORPORATED BY REFERENCE: None

TABLE OF CONTENTS

Throughout this report, unless otherwise designated, the terms “we,” “us,” “our,” and “our company” refer to Ocean Thermal Energy Corporation, a Nevada corporation, and our subsidiaries. All amounts in this report are in U.S. dollars, unless otherwise indicated.

CAUTIONARY STATEMENT ON FORWARD-LOOKING STATEMENTS

This report may contain certain “forward-looking” statements as such term is defined by the U.S. Securities and Exchange Commission (“SEC”) in its rules, regulations, and releases, which represent our expectations or beliefs, including statements concerning our operations, economic performance, financial condition, growth and acquisition strategies, investments, and future operational plans. For this purpose, any statements contained herein that are not statements of historical fact may be deemed to be forward-looking statements. Without limiting the generality of the foregoing, words such as “may,” “expect,” “believe,” “anticipate,” “intend,” “could,” “estimate,” “might,” “plan,” “propose,” “predict,” or “should,” or the negative or other variations thereof or comparable terminology, are intended to identify forward-looking statements. These statements by their nature involve substantial risks and uncertainties, certain of which are beyond our control, and actual results may differ materially depending on a variety of important factors, including uncertainty related to acquisitions, governmental regulation, management and maintenance of growth, the operations of the company and its subsidiaries, volatility of stock price, commercial viability of OTEC systems, and any other factors discussed in this and our other filings with the SEC.

These risks, uncertainties, and other factors include those set forth under “Risk Factors” of this report. Given these risks and uncertainties, readers are cautioned not to place undue reliance on our forward-looking statements. All subsequent written and oral forward-looking statements attributable to us or to persons acting on our behalf are expressly qualified in their entirety by these cautionary statements. Except as otherwise required by applicable law, we undertake no obligation to publicly update or revise any forward-looking statements or the risk factors described in this report or in the documents we incorporate by reference, whether as a result of new information, future events, changed circumstances, or any other reason after the date of this report.

This report contains forward-looking statements, including statements regarding, among other things:

| · | the significant international political and economic disruption caused by Russia’s military invasion of Ukraine; |

| | |

| · | our ability to continue as a going concern; |

| | |

| · | our anticipated needs for working capital; |

| | |

| · | our ability to secure financing; |

| | |

| · | the possibility that actual capital costs, operating costs, production, and economic returns may differ significantly from those that we have anticipated; |

| | |

| · | the financial model for our proposed projects has not been tested and may not be successful; |

| | |

| · | changing attitudes about environmental risks; |

| | |

| · | substantial regulation of our projects; |

| | |

| · | financial, technical, managerial, and sales risks that may make us unsuccessful; |

| | |

| · | our exposure to political and legal risks in developing or emerging markets where we propose to locate our plants; |

| | |

| · | technological advances that may render our technologies obsolete; and |

| | |

| · | operational problems, natural events or catastrophes, casualty loss, or other events that may impair the commercial operation of our projects. |

The forward-looking information is based on present circumstances and on our predictions respecting events that have not occurred, that may not occur, or that may occur with different consequences from those now assumed or anticipated. Actual events or results may differ materially from those discussed in forward-looking statements because of various factors, including the risks outlined under “Risk Factors,” and matters described in this report generally. The forward-looking statements included in this report are made only as of the date of this report.

PART I

ITEM 1. BUSINESS

Overview

We use our proprietary technology to develop designs for renewable energy systems, primarily for Ocean Thermal Energy Conversion (“OTEC”), Seawater Air Conditioning (“SWAC”), and Lake Source Cooling (“LSC”) systems. Our geographical markets are tropical and subtropical regions of the world for OTEC, SWAC, and LSC and worldwide markets for SWAC and LSC. We develop projects for renewable power generation, desalinated water production, and air conditioning using our proprietary technologies designed to extract energy from the temperature differences between warm surface water and cold deep water. In addition, our projects provide ancillary products such as potable/bottle water and high-profit aquaculture, mariculture, and agriculture opportunities.

Agreement to Sell Subsidiary

On August 25, 2022, we entered into a Stock Purchase Agreement to sell OCEES International, Inc., our wholly owned subsidiary (“OCEES”), to Epaphus Global Energy, LLC (“Epaphus”). Epaphus is controlled by Jeremy Feakins, our Chief Executive Officer and a director. The transaction was approved unanimously by our directors who do not have an interest in the transaction.

In exchange for the sale of OCEES, we will receive:

| · | $1,000,000 in the form of canceled amounts owed by us to certain individuals, including Mr. Feakins, who have assigned their right to receive those payments to Epaphus; |

| · | $75,000 in cash per month for 12 months following the date of the purchase agreement; and |

| · | 70% of the net profit of any currently contemplated project to build an ocean thermal energy conversion power plant entered into by OCEES. |

Under the terms of the purchase agreement, Epaphus has the unilateral right to return OCEES to us and receive a full refund of all portions of the purchase price paid as of the return of OCEES at any time for one year following the date of the purchase agreement.

The transaction had not closed as of December 31, 2022, nor through the date of filing of this report. The transaction has not been reflected in our financial statements at December 31, 2022.

Our Business

We develop projects for renewable power generation, desalinated water production, and air conditioning using proprietary intellectual property designed and developed by our own experienced oceanographers, engineers, and marine scientists. Plants using our technologies are designed to extract energy from the temperature difference between warm surface ocean water and cold deep seawater at a depth of approximately 3,000 feet. We believe these technologies provide practical solutions to the fundamental human needs for sustainable, affordable energy; desalinated water for domestic, agricultural, and aquaculture uses; and cooling, all without the use of fossil fuels.

| ● | Ocean Thermal Electrical Conversion, known in the industry as “OTEC,” power plants are designed to produce electricity. In addition, some of the seawater running through an OTEC plant can be desalinated efficiently, producing fresh water for agriculture and human consumption. |

| ● | Seawater Air Conditioning, known in its industry as SWAC, plants are designed to use cold water from ocean depths to provide air conditioning for large commercial buildings or other facilities. This same technology can also use deep cold water from lakes, known as Lake Source Cooling or LSC. |

Both OTEC and SWAC/LSC systems can be engineered to produce desalinated water for potable, agricultural, and fish farming/aquaculture uses.

Many applications of technologies based on ocean temperature differences between surface and deep seawater have been developed at the Natural Energy Laboratory of Hawaii Authority, or NELHA, test facility (http://nelha.hawaii.gov), including applications for desalinated seawater, fish-farming, and agriculture. Note: All URL addresses in this report are inactive textual references only. We believe our proprietary advances to existing technologies developed by others in the industry enhance their commercialization for the plants we propose to develop.

We have recruited a scientific and engineering team that includes oceanographers, engineers, and marine scientists who have worked for a variety of organizations since the 1970s on several systems based on extracting the energy from the temperature differences between surface and deep seawater, including projects by NELHA, the Argonne National Laboratory (http://www.anl.gov), and others. Our executive team members have complementary experience in leading engineering and technical companies and projects from start-up to commercialization.

We expect to use our technology to develop an OTEC EcoVillage, which should add significant value to our business. We plan to facilitate the development of sustainable living communities by creating an ecologically sustainable “OTEC EcoVillage” powered by 100% fossil-fuel free electricity. In the development, buildings will be cooled by energy-efficient and chemical-free systems, and water for drinking, aquaculture, and agriculture will be produced onsite. The OTEC EcoVillage project consists, in part, of an OTEC plant that will provide all power and water to about 400 residences, a hotel, and a shopping center, as well as models of sustainable agriculture, food production, and other economic developments. Each sale of luxury EcoVillage residences will support the development of environmentally responsible affordable communities currently in development in tropical and subtropical regions of the world. We believe our OTEC EcoVillage will be the first development in the world offering a net-zero carbon footprint. This will be our pilot project, launched to prove the viability of OTEC technology to provide affordable renewable energy for entire communities. We believe this project could be highly profitable and generate significant value for our shareholders.

Through our Small Business Innovation Research credentials, we continue to discuss opportunities to design, build, own, and operate an OTEC system producing base-load sustainable electricity and desalinated water without using fossil fuels to do so. Our discussions have included OTEC designs for a Naval Support Facility in the Indian Ocean and military bases in tropical regions.

Our Vision

Our vision is to bring our technologies to tropical and subtropical regions of the world where about three billion people live. Our market includes 68 countries and 29 territories with suitable sea depth, shore configuration, and market need; we plan to be the first company in the world to design and build a commercial-scale OTEC plant and, to that end, have several projects in the planning stages. Our initial markets and potential projects include several U.S. Department of Defense bases situated in the Asia Pacific and other regions where energy independence is crucial. Currently, we have projects in the planning and development stages in Puerto Rico and the U.S. Virgin Islands.

Our Technology

OTEC is a self-sustaining energy source, with no supplemental power required to generate continuous (24/7) electricity. It works by converting heat from the sun, which has warmed ocean surface water, into electric power, and then completing the process by cooling the plant with cold water from deep in the ocean. The cold water can also be used for very efficient air conditioning and desalinated to produce fresh water. OTEC has worked in test settings where there exists a natural temperature gradient of 20 degrees Celsius or greater in the ocean. We believe OTEC can deliver sustainable electricity in tropical and subtropical regions of the world at rates approximately 20-40% lower than typical costs for electricity produced by fossil fuels in those markets.

Further, we believe that a small, commercial OTEC plant could offer competitive returns even in a market where the cost of electricity is as low as $0.30 per kilowatt-hour, or kWh. The Caribbean depends on imported oil for approximately 90% of its energy needs. The electricity prices in the Caribbean are extremely high, with an average of $0.34 per kWh and as high as $0.50 per kWh, which is nearly four times the price paid in the United States, according to a 2017 renewable energy report, when oil prices were lower. For the U.S. Virgin Islands, the Water and Power Authority of the Virgin Islands reported that as of February 1, 2020, the average price for electricity for commercial customers was nearly $0.47 per kWh. We believe that we have an opportunity to offer base-load energy (the amount of energy required to meet minimum requirements) pricing that is better than our customer’s next best alternative in the markets where electricity costs are $0.30 or more per kWh.

Technology advancements have significantly reduced the capital costs of OTEC to make it competitive compared to traditional energy sources. Technology improvements include larger diameter seawater pipes manufactured with improved materials, increased pumping capabilities from OTEC depths, better understanding of material requirements in the deep ocean environment, more experience in deep water pipeline and cable installation techniques, and more accurate sea bottom mapping technology, which is required for platform positioning and pipe installation. The cold-water pipes at a demonstration site in Hawaii have been in continuous operation for more than 20 years, and the technology has improved significantly since the Hawaiian installation.

We estimate that a small OTEC plant that delivers 13 megawatts (MWs) per hour would currently cost approximately $250 million. This is the plant size that we typically propose for our initial target markets to meet 20% or more of their current demand for electricity and a large portion of their need for fresh drinking water and agricultural water. OTEC has been proven in test settings at NELHA, where a Department of Energy-sponsored OTEC plant operated successfully throughout the 1990s to produce continuous, affordable electricity from the sea without the use of fossil fuels. Spin-off technologies of desalination and seawater cooling, developed from the OTEC plant at NELHA, have also become economically and technically feasible.

Finally, we believe the decreasing supply and increasing cost of fossil-fuel-based energy has intensified the search for renewable alternatives. We further believe that renewable energy sources, although traditionally more expensive than comparable fossil-fuel plants, have many advantages, including increased national energy security, decreased carbon emissions, and compliance with renewable energy mandates and air quality regulations. We believe these market forces will continue and potentially increase. In remote islands where shipping costs and limited economies of scale substantially increase fossil-fuel-based energy, renewable energy sources may be attractive. Many islands contain strategic military bases with high-energy demands that we believe would greatly benefit from a less expensive, reliable source of energy that is produced locally, such as OTEC.

SWAC//LSC is a process that uses cold water from locations such as the ocean or deep lakes to provide the cooling capacity to replace traditional electrical chillers in an air conditioning system. SWAC/LSC applications can reduce the energy consumption of a traditional air-conditioning system by as much as 90%. Even when the capital cost amortization of building a typically sized SWAC/LSC system providing 9,800 tons of cooling ($140-$150 million) are taken into account, SWAC/LSC can save the customer approximately 25-40% when compared to conventional systems—we estimate savings can be as high as 50% in locations where air temperatures and electricity costs are high. Cooling systems using seawater or groundwater for large commercial structures are in use at numerous locations developed and operated by others worldwide, including Heathrow Airport, UK; Finland (Google Data Center); Cornell University, NY; Stockholm, Sweden; and the City of Toronto, Canada.

How Our Technology Works

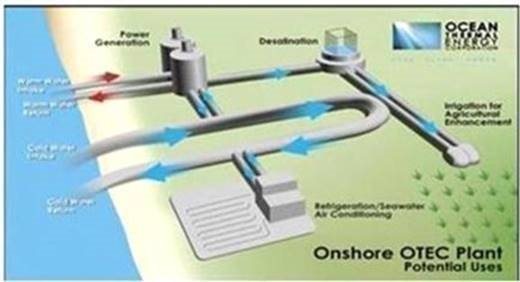

OTEC uses the natural temperature difference between cooler deep ocean water at a depth of approximately 3,000 feet and warmer shallow or surface water to create energy. An OTEC plant project involves installing about 6.0 feet diameter, deep-ocean intake pipes (which can readily be purchased), together with surface water pipes, to bring seawater onshore. OTEC uses a heat pump cycle to generate power. In this application, an array of heat exchangers transfers the warm ocean surface water as an energy source to vaporize a liquid in a closed loop, driving a turbine, which in turn drives a generator to produce electricity. The cold deep ocean water provides the required temperature to condense vapor back into a liquid, thus completing the thermodynamic cycle, which is constantly and continuously repeated. The working fluid is typically ammonia, as it has a low boiling point. Its high hydrogen density makes ammonia a very promising green energy storage and distribution media. Among practical fuels, ammonia has the highest hydrogen density, including hydrogen itself, in either its low temperature, or cryogenic, and compressed forms. Moreover, since the ammonia molecule is free of carbon atoms (unlike many other practical fuels), combustion of ammonia does not result in any carbon dioxide emissions. The fact that ammonia is already a widely produced and used commodity with well-established distribution and handling procedures allows for its use as an alternative fuel. This same general principle is used in steam turbines, internal combustion engines, and, in reverse, refrigerators. Rather than using heat energy from the burning of fossil fuels, OTEC power draws on temperature differences of the ocean caused by the sun’s warming of the ocean’s surface, providing an unlimited and free source of energy.

OTEC and SWAC/LSC infrastructure offers a modular design that facilitates adding components to satisfy customer requirements and access to a sufficient supply of cold water. These components include reverse-osmosis desalination plants to produce drinkable water, bottling plants to commercialize the drinkable water, and off-take solutions for aquaculture uses (such as fish farms), which benefit from the enhanced nutrient content of deep ocean water. A further advantage of a modular design is that, depending on the patterns of electricity demand and output of the OTEC plant, a desalination plant can be run using the excess electricity capacity.

Currently, OTEC requires a minimum temperature difference of approximately 20 degrees Celsius to operate, with each degree greater than this increasing output by approximately 10-15%. OTEC has potential applications in tropical and subtropical zones and is particularly well suited for tropical islands and coastal areas with proximate access to both cold deep water and warm surface water. These communities are typically subject to high and fluctuating energy costs ranging from $0.28-$0.75 per kWh, as they rely on importing fossil fuels for power generation. Data from the National Renewable Energy Laboratory of the U.S. Department of Energy website indicated that at least 68 countries and 29 territories around the globe appear to meet these criteria.

The world’s largest OTEC power plant to date is operational at the NELHA facility in Hawaii and has been connected to the electrical grid. It provides base-load electricity produced by OTEC to residential homes. Around the world, a couple of other successful developmental and experimental plants have been built, and the U.S. National Oceanic and Atmospheric Administration, or NOAA, has stated that: “The qualitative analysis of the technical readiness of OTEC by experts at this workshop suggest that a <10 MWe floating, closed-cycle OTEC facility is technically feasible using current design, manufacturing, deployment techniques and materials” (https://coast.noaa.gov/data/czm/media/otec_nov09_tech.pdf). We believe that we have sufficient skill and knowledge to now commercialize 5-MW to 30-MW land-based OTEC plants, using off-the-shelf components, including the cold-water piping.

SWAC/LSC is a significantly more cost-effective and environmentally friendly way to implement air-conditioning using cold water sourced from lakes or, analogous with OTEC, deep ocean water, rather than from an electric chiller. Comparing Federal Energy Management Program engineering efficiency requirements of approximately 0.94 kilowatts of electricity per ton of cooling capacity with our own engineering estimates of 0.09 kilowatts of electricity per ton of cooling capacity, as calculated by DCO Energy, our engineering, procurement, and construction partner, we estimate that SWAC/LSC systems can reduce electricity consumption by up to 80-90% over conventional systems. Therefore, we believe energy reductions may make SWAC/LSC systems well-suited for large structures, such as office complexes, medical centers, resorts, data centers, airports, and shopping malls. We believe that other SWAC/LSC plants we may develop will likely achieve similar efficiencies. There are examples of proven successful SWAC/LSC systems in use, including a large 79,000-ton system used to cool buildings in the downtown area of the City of Toronto, Canada; a SWAC system in Google’s data center in Finland that uses waters from the Baltic Sea to keep servers cool; and a system with more than 18,000 tons of cooling in operation at Cornell University, Ithaca, New York. On January 10, 2018, William S. (Lanny) Joyce joined our board of advisors. Mr. Joyce was the Director of Utilities and Energy Management in the Energy and Sustainability Department at Cornell University, Ithaca, New York. Mr. Joyce initiated and was project manager for innovative and award-winning Cornell University LSC project completed in 2000 that provides all the chilled water production on the central campus utilizing a renewable resource and 86% less energy.

OTEC Versus Other Energy Sources

The construction costs of power plants using any technology are much higher in remote locations, such as tropical islands, than on the mainland of the United States, principally due to the need to transport materials, components, and other construction supplies and labor not available locally. There are also considerations that make those other technologies less attractive in those areas. We believe the consistency of OTEC during its life provides clear advantages over other power-generation technology in the tropical and subtropical markets, because its base-load power (available at all times and not subject to fluctuations throughout the day) is an important asset to the small transmission grid, which is typical in these regions.

Combined-cycle natural gas plants typically need to be capable of generating several hundred MWs to attain the lower-cost, per-kilowatt installed values that make the plant economically feasible. Tropical locations do not have large enough grids and market demand to make that plant size reasonable. Further, tropical locations frequently do not have domestic fuel supplies, requiring fuel to be imported. In order to import natural gas, it must be liquefied for shipment and then vaporized at the location. There are initial cost and public safety concerns with such facilities. In addition, gas-fired plants emit undesirable nitrogen oxide, carbon dioxide, and volatile organic compounds.

Solar applications continue to increase as the cost and effectiveness of photovoltaic panels improve. However, we estimate that the cost to install solar panels in tropical regions remains high. Beyond the issues with shipping and labor costs that all construction must overcome, the design and building code requirements are tougher in storm-prone areas, which are subject to potential wind damage from hurricanes, earthquakes, and typhoons, than are typically encountered in mainland nontropical installations. Support structures must be more substantial in order to hold the solar panels in place in case of hurricane-force winds. Solar power, like wind power, places substantial stress on an electrical grid. Since the input of both of these sources is subject to weather conditions, they cannot be considered reliable suppliers of power, and back-up capacity is necessary. Further, instantaneous changes in output due to sporadic cloud cover create transient power flow to the grid and difficulties in maintaining proper voltages and stability. OTEC is a stabilizing source to the grid, providing constant and predictable power, and has no emissions. The ability of OTEC to provide constant, continuous power is a large benefit as compared to any of the other renewable options available.

Our estimated price for OTEC-generated power of approximately $0.30 per kWh under current economic conditions, which can be as low as $0.18 net per kWh with maximum efficiency and revenue from water production, is also constant both throughout the year and over a plant’s life. OTEC’s power price, determined almost entirely by the amortization of its initial cost, is a protection against inflation and rising interest rates, which greatly affect coal and oil. Customers in our target markets currently pay from $0.35 to as high as $0.60 per kWh for power from coal and oil-fueled power plants. However, imported fuels are subject to price volatility, which has a direct impact on the cost of electricity and adds operating risk during the life of a plant. The fuel handling to allow for the shipping, storage, and local transport is expensive, a potential source of damaging fuel spills and a basis for environmental concerns. Fossil-fuel plants create pollution, emit carbon dioxide, and are visually unappealing, which is of particular concern in tropical areas renowned for their clear, pristine air and beauty. We project OTEC can save these markets up to 40%, compared to their current electrical costs, and when revenues from fresh drinking water, aquaculture, and agriculture production are considered, the justification is even more compelling.

Overview of the Market and the Feasibility of OTEC in Current Market Conditions

We believe that OTEC is now an economically, technologically, and environmentally competitive power source, especially for developing or emerging countries in certain tropical and subtropical regions contiguous to oceans. Our natural target markets are communities in countries around the Caribbean, Asia, and the Pacific. These locations are typically characterized by limited infrastructure, high-energy costs, mostly imported or expensively generated electricity, and frequently with significant fresh water and food shortages. These are serious limitations on economic development, which we believe our OTEC technology can address.

Data presented to the Sustainable Use of Oceans in the Context of the Green Economy and the Eradication of Poverty workshop in Monaco in 2011 by Whitney Blanchard of the Office of Ocean and Coastal Resource Management, National Oceanic and Atmospheric Administration, show that at least 98 nations and territories using an estimated five terawatts of potential OTEC net power are candidates for OTEC-power systems. Blanchard specifically notes that Hawaii, Guam, Florida, Puerto Rico, and the U.S. Virgin Islands are suitable for OTEC.

Over the past 15 years, there have been substantial changes in many areas that have now made the commercialization of OTEC a reality, influenced by the increasing price of oil, which until 2006/2007 had been relatively inexpensive.

Recent oil prices have been volatile, owing in part to political instability in Eastern Europe and elsewhere. Crude oil prices increased in 2021 as increasing COVID-19 vaccination rates, loosening pandemic-related restrictions, and recovering economies resulted in global petroleum demand rising faster than petroleum supply. The spot price of Brent crude oil, a global benchmark, started the 2021 year at $50 per barrel and increased to a high of $86 per barrel in late October before declining in the final weeks of the year. As a result of the conflict in Eastern Europe, oil prices were up 30% in February 2022, with oil prices hitting a high of about $130 per barrel before settling in the $100 range in mid-March 2022. As of July 2023, oil is quoted at more than $80.00 per barrel.

Facts like these have resulted in increased attention and interest in OTEC in the commercial sector and among candidates. With OTEC power, customers can decouple the price of electricity from the price of oil.

The International Energy Agency’s World Energy Outlook expects liquid natural gas export capacity to grow rapidly in the short term, with major new sources of supply coming mostly from Australia and the United States.

Liquid natural gas prices have collapsed, in part because demand is turning out to be weaker than some previously anticipated. Additionally, many rules and regulations are in effect to mitigate the environmental issues associated with liquid natural gas extraction, transportation, and storage, adding significant costs.

According to the U.S. Environmental Protection Agency, in the United States, nearly 29% of 2017 greenhouse gas emissions was generated primarily from burning fossil fuel for our cars, trucks, ships, trains, and planes. Over 90% of the fuel used for transportation is petroleum-based, which includes gasoline and diesel. The electric power sector accounted for 28% of total greenhouse gas emissions in 2017.

According to the U.S. Environmental Protection Agency: “Global carbon emissions from fossil fuels have significantly increased since 1900. Since 1970, CO2 emissions have increased by about 90%, with emissions from fossil fuel combustion and industrial processes contributing about 78% of the total greenhouse gas emissions increase from 1970 to 2011. Agriculture, deforestation, and other land-use changes have been the second-largest contributors.”

Greenhouse gas emissions from electricity have increased between 1990 and 2007 as electricity demand grew and fossil fuels remained the dominant source for generations. Fossil-fuel-fired power plants are a significant source of domestic carbon dioxide emissions, the primary cause of global warming. To generate electricity, fossil-fuel-fired power plants use natural gas, petroleum, coal, or any form of solid, liquid, or gaseous fuel derived from such materials. Along with the increasing use of renewable energy, the greenhouse emissions from power generation have decreased since 2007, approaching the 1990 levels.

The U.S. Energy Information Administration (“EIA”) states that renewable energy plays an important role in reducing greenhouse gas emissions. Energy consumption of biofuels, geothermal energy, solar energy, and wind energy in the United States has increased. Total U.S. renewable energy production and consumption reached record highs in 2020. In 2020, renewable energy provided about 11.59 quadrillion British thermal units (Btu)—1 quadrillion is the number 1 followed by 15 zeros—equal to 12% of total U.S. energy consumption. The electric power sector accounted for about 60% of total U.S. renewable energy consumption in 2020 and about 20% of total U.S. electricity generation was from renewable energy sources.

According to the EIA, renewable energy can play an important role in U.S. energy security and in reducing greenhouse gas emissions. Using renewable energy can help to reduce energy imports and reduce fossil fuel use, which is the largest source of U.S. carbon dioxide emissions. In the Annual Energy Outlook 2021 reference case, EIA projects that U.S. renewable energy consumption will continue to increase through 2050. The reference case generally assumes that current laws and regulations that affect the energy sector, including laws that have end dates, remain unchanged throughout the projection period.

Interest in renewable energy from the U.S. military, especially the U.S. Army, has increased as articulated by Secretary of the Army Christine E. Wormuth in the 2022 United States Army Climate Strategy:

As the Army optimizes the use of fuel, water, electricity, and other resources, we increase our resilience while saving taxpayer dollars and reducing our impact on the planet. The Army will mitigate and adapt to climate change, and in doing so gain a strategic advantage, especially as we continue to outpace our near-peer competitors.

The President’s purpose in Executive Order 14008 clearly stated the need to combat climate change:

It is the policy of my Administration to lead the Nation’s effort to combat the climate crisis by example—specifically, by aligning the management of Federal procurement and real property, public lands and waters, and financial programs to support robust climate action. By providing an immediate, clear, and stable source of product demand, increased transparency and data, and robust standards for the market, my Administration will help to catalyze private sector investment into, and accelerate the advancement of America’s industrial capacity to supply, domestic clean energy, buildings, vehicles, and other necessary products and materials.

People in many countries today, including the United States, are concerned with environmental issues caused by fossil-fuel-generated power. Gallup surveys find public acceptance of climate change is rising. Close to two-thirds of U.S. adults are concerned about global warming, with 43% worrying about it “a great deal” and 22% “a fair amount.” Gallup surveys also find 43% of Americans believe that global warming will pose a serious threat to themselves or their way of life in their lifetime, underscoring that roughly four in 10 harbor strong concern. The latest results, from a March 1-15, 2021, Gallup poll, predate the hottest summer on record in the lower 48 states.

The international concern about the harmful effects of climate change led to the negotiation of the Paris Agreement in December 2015 as the culmination of the 2015 United Nations Climate Change Conference. The agreement provides for members to reduce their carbon output as soon as possible and to do their best to keep global warming to no more than two degrees Celsius, or 3.6 degrees Fahrenheit. In order to achieve the desired results, there would have to be a worldwide reduction in emissions from fossil fuels and a shift to renewable resources.

Global acceptance of human influence on climate change may also contribute to a shift in the demand for OTEC. As evidenced by the Paris Agreement reached in December 2015 to combat climate change, 195 nations expressly recognized that conventional fossil-fuel powered energy technologies affect global climate change and the need to embrace a sustainable future in energy and water. Low-lying coastal countries (sometimes referred to as small island developing states) that tend to share similar sustainable development challenges, including small but growing populations, limited resources, remoteness, susceptibility to natural disasters, vulnerability to external shocks, excessive dependence on international trade, and fragile environments, have embraced this recognition and are keenly aware that they are on the frontline of early impact of sea level rise and are aggressively trying to embrace sustainable-energy alternatives. This is a major driving force for OTEC in primary early markets.

In February 2021, the United States officially rejoined the Paris Climate Accord, standing with the world to help fight the ‘existential crisis’ of global warming. Even during the years the United States had withdrawn from the Paris Climate Accord, a coalition of 14 U.S. states, including California and New York, said they were on track to meet the U.S. target of a 26-28% reduction in greenhouse gas emissions by 2025, compared to 2005 level.

The United Kingdom hosted the 26th UN Climate Change Conference of the Parties (COP26) in Glasgow on 31 October – 13 November 2021. The COP26 summit brought parties together to accelerate action towards the goals of the Paris Agreement and the UN Framework Convention on Climate Change.

We believe the ongoing concerns about environmental issues and the price instability of fossil-fuel prices are motivation for increased commercial interest in OTEC, renewed activity in the commercial sector, and increased interest among communities and agencies that recognize the potential benefits of this technology, including the U.S. Department of Defense and U.S. Department of the Interior territories.

Several large companies have used their OTEC technology experience to introduce OTEC systems worldwide, supporting the argument that the technology is now at the point where it can be introduced at a commercial level:

| ● | Since early 2014, we have been working with several industrialized and developing countries, including U.S. Virgin Islands, The Bahamas, Cayman Islands, and others, and investigating suitable OTEC sites, infrastructural solutions, and funding opportunities. |

| ● | Two nongovernmental organizations promoting OTEC have been created: OTEC Foundation (based in The Netherlands) and OTEC Africa (based in Sweden). |

| ● | New technological advances for larger and more robust deep seawater pipes and more efficient and cost-effective heat exchangers, pumps, and other components have, in our opinion, further improved the economics for OTEC. |

| ● | Many countries, including a large number of Caribbean nations, now have renewable energy standards and are looking at ways to reduce their carbon footprints, decouple the price of electricity from the volatile price of oil, and increase energy security. Along with these countries, we are aware that Hawaii, U.S. territories, and the U.S. Department of Defense are looking at OTEC as a possible source of renewable energy and water for drinking, fish farming, and agriculture. |

| ● | The NELHA demonstration OTEC plant in Hawaii can produce 100 kilowatts of sustainable, continuous electricity annually and had powered a neighborhood of 120 homes. |

Recent international political instability, especially in Eastern Europe, proved that fossil-fuel-producing regions and oil price volatility have exposed the criticality of energy security and independence for all countries. The need to have a tighter control of domestic energy requirements is a matter of increasing international concern. Continued reliance on other countries (particularly those in oil-producing regions) is no longer a favorable option. We believe these considerations will continue to drive renewable research and commercialization efforts that promote technologies with global potential to replace fossil-fuel-based energy systems and benefit from base-load capabilities like OTEC.

Our current management team has led the development of the business since 2010 and has advanced the technology and understanding of OTEC, SWAC/LSC to worldwide markets. We believe these efforts have helped us establish an eager marketplace for our technology and an understanding as to the importance of designing, building, and operating a commercial-grade OTEC system. Our efforts in the U.S. Virgin Islands included an extensive feasibility study explaining how OTEC could operate successfully in the territory. The Public Services Commission of the U.S. Virgin Islands has approved our application to be a “qualified facility” and build a 15MW OTEC plant on the island of St. Croix. In addition to the OTEC plant, we have presented testimony to the territory showing how OTEC could provide potable water to the U.S. Virgin Islands.

We are discussing both OTEC and SWAC/LSC projects with various federal government departments. Currently, several projects are in the planning and discussion phase:

| ● | We have provided a detailed study and designs for OTEC and/or SWAC/LSC for an Eco Village powered by an OTEC plant for the U.S. Virgin Islands. |

| ● | We have made application for several grants through the U.S. Department of Energy to support the commercialization of OTEC technology together with the production of "green hydrogen.” |

| ● | We continue to respond to inquiries for OTEC/SWAC/LSC from potential customers around the world. |

| ● | We continue to utilize our Small Business Innovation Research credentials in discussions with the U.S. government, including for remote military bases in tropical regions. |

In light of the foregoing, we believe that it is now appropriate to seek additional funding to further progress and build our engineering and technical teams, develop our intellectual property, file patents for several OTEC technical systems, and advance our current opportunities to support our growth strategy.

Our Competition

We compete in the development, construction, and operation of OTEC and SWAC/LSC plants with other operators that develop similar facilities powered by other energy sources, primarily oil, natural gas, nuclear energy, and solar power. These traditional energy sources have well-established infrastructures for production, delivery, and supply, with well-known commercial terms. In developing our OTEC and SWAC/LSC plants, we will need to satisfy our customers that these technologies are sound and economical, which may be a challenge until and unless we have an established successful operating history. The energy industry is dominated by an array of companies of all sizes that have proven technologies and well-established fuel sources from a number of suppliers.

We expect that we will encounter increasing competition for OTEC and SWAC/LSC plants. Other firms with greater financial and technical resources are focusing on commercialization of these technologies. Our competitors may benefit from collaborative relationships with countries, including a large number of Caribbean nations, that now have renewable-energy standards and are looking at ways to reduce their carbon footprints, decouple the price of electricity from the volatile price of oil, and increase energy security. Other competitors may have advantageous relationships with authorities such as Hawaii, U.S. territories, and the U.S. Department of Defense, which are looking at OTEC as a possible source of renewable energy and water for drinking, fish farming, and agriculture.

We cannot assure that we will be able to compete effectively as the industry grows and becomes more established and as OTEC and SWAC/LSC plants become more accepted as viable and economic energy solutions.

We believe competition in this industry is and will be based on technical soundness and viability, the economics of plant outputs as compared to other energy sources, developmental reputation and expertise, financial capability, and ability to develop relationships with potential customers. All these factors are outside our control.

Our Operational Strategy and Economic Models

We have developed economic models of costs and potential revenue structures that we will seek to implement as we develop OTEC and SWAC/LSC projects.

OTEC Projects

The estimated construction costs for a 20-MW plant are approximately $445 million with hard costs of approximately $301 million for the power system and platform construction and piping, which make up 68% of the total. The remaining 32% consists of other construction costs and the deployment of the cold water pipe and soft costs of approximately $144 million for design, permits and licensing, environmental impact assessment, bathymetry, contractor fees, and insurance.

Once operational, the capacity factor, which is the projected percent of time that a power system will be fully operational, considering maintenance, inspections, and estimated unforeseen events, is expected to be 95% annually. This factor is used in our financial calculations, which means the plant will not be generating revenue for 5% of the year. Most fossil-fuel plants have capacity factors around 90%, as a result of the major maintenance for high-temperature boilers, fossil-fuel feed in systems, safety inspections, cleaning, etc. The normal maintenance cycle for the pumps, turbine, and generators used in the OTEC plant is typically every five years. This includes the cleaning of the heat exchangers and installation of new seals.

We anticipate that project returns will be comprised of two components: First, as the project developer, we will seek a lump-sum payment as a development fee at the time of closing the project financing for each project. These payments will be allocated toward reimbursement of development costs and perhaps a financial return at the early stage of each project. The development fee will vary, but initially we will seek a fee of approximately 3% of the project cost, payable upon closing the project financing. Second, we will retain a percentage of equity in the project, with a goal to retain a minimum of 51% of the equity in any OTEC project in order to participate in operating revenues.

We will seek revenue from OTEC plants from contract pricing charged on an energy-only price per kWh or on the basis of a generating capacity payment priced per kilowatt per month and an energy usage price per kWh. In many of the countries of the world where we intend to build OTEC and SWAC/LSC plants, potable water is in short supply. In some locations, water is considered the more important commodity. Depending on the part of the world in which the plant is built, in addition to revenue from power generation, supplying water for drinking, fish farming, and agriculture would significantly increase plant revenue.

We cannot assure that we can maintain the revenue points noted above, that any fees received will offset development costs incurred to date, or that any operating plant will generate revenue.

SWAC/LSC Projects

The estimated construction costs for a SWAC/LSC plant are approximately $150 million with hard costs of approximately $91 million for piping and installation, which make up 60% of the total. The remaining 40% consists of the pump house, central utility plant (CUP), mechanical and engineering equipment, design, and other contingency costs and soft costs of approximately $59 million for the CUP license, permits, environmental impact assessment, bathymetry, and insurance.

Under our economic model, we will seek revenue at two stages of the project. First, as the project developer, we will seek a lump-sum payment of a development fee equal to approximately 3% of the project cost at the time of closing the project financing for each project. These payments would provide us with income at the early stage of each project. If we are able to negotiate a development fee, we estimate that it will vary, but typically will be in the $2,500,000-$3,500,000 range. The second component of project returns is based upon the percentage of equity we will retain in the project.

SWAC/LSC contract revenue will be based typically on three charges:

| ● | Fixed Price–this is based upon the capital costs of the project paid over the term of the debt and with the intention of covering the costs of debt. |

| ● | Operation and Maintenance–this payment covers the cost of the labor and fixed overhead needed to run the SWAC/LSC system, as well as any traditional chiller plant operating to fulfill back-up or peak-load requirements. |

| ● | Chilled Water Payment–this is a variable charge based on the actual chilled water use and chilled water generated both by the SWAC/LSC and conventional system at the agreed upon conversion factors of kilowatt/ton and current electricity costs in U.S. dollars per kWh. |

We plan to structure project financing with the goal of retaining 100% of the equity in any SWAC/LSC project. We cannot assure that we will recover project development costs or realize a financial return over the life of the project.

Our Project Timeline

We have not designed, constructed, and placed into operation any OTEC or SWAC/LSC plants. However, based on our planning process and early development experience to date, we estimate that it will take approximately two years or more, depending on local conditions, including regulatory and permitting requirements, to take a project from a preliminary memorandum of understanding with a potential power or other product purchaser to completion and commencement of operation.

Our Strategic Relationships

We have a strategic relationship with DCO Energy, LLC, Mays Landing, New Jersey, an American energy development company specializing in the development, engineering, construction, start-up, commissioning, operation, maintenance and management, as well as ownership, of central energy centers, renewable energy projects, and combined heat, chilling, and power-production facilities. DCO Energy was formed in 2000 and has independently developed and/or operated energy producing facilities of approximately 275 MW of electric, 400 MMBtu/hr of heat recovery, 1,500 MMBtu/hr of boiler capacity, and 130,000 tons of chilled water capacity, totaling over $1 billion of assets. DCO Energy provides financing, engineering and design, construction management, start-up and commissioning resources, and long-term operating and maintenance services for its own projects as well as third-party clients.

Our Construction and Components

Once we have designed the system, we will review the design with our engineering, procurement, and construction partner to maximize the chances that the project can be delivered according to plan and on budget. We expect our construction contracts to be at a fixed price and to include penalties if the construction timetable is missed. We may, but are not obligated to, engage DCO Energy to construct our plants or serve as our owners’ engineer.

In our systems, the two most important components are heat exchangers and deep-water intake pipes. Although there are multiple providers of each of these components, the supply of the best components comes from just a few companies globally. We expect to source our deep-water intake pipes from Pipelife of Norway, the only company we know of that makes pipes of sufficient quality, strength, and diameter (2.5 meters) to support our planned OTEC plants. However, we expect that we could work around a lack of supply from Pipelife by using multiple smaller pipes that are widely available on the market, although this would increase our construction costs.

We will also need the highest quality, large heat exchangers for our systems; heat exchangers represent a large percentage of the projected costs of our OTEC and SWAC/LSC systems and account for a significant portion of the complexity inherent in commercial OTEC and SWAC/LSC designs.

Other major components, such as ammonia turbines, generators, and pumps, are manufactured by several multinational companies, including General Electric and Siemens.

Our Operations

For OTEC electricity-generating facilities, we intend to enter into 20- to 30-year power purchase agreements, or PPAs, pursuant to which the project would supply fixed-price, baseload electricity to satisfy the minimum demand of the purchaser’s customers. This PPA structure allows customers to plan and budget their energy costs over the life of the contract. For our SWAC/LSC systems, we intend to enter into 20- to 30-year energy service agreements, or ESAs, to supply minimum quantities of chilled water for use in a customer’s air conditioning system.

We anticipate that operations of OTEC and SWAC/LSC plants will be subcontracted to third parties that will take responsibility for ensuring the efficient operation of the plants. These arrangements may reduce our exposure to operational risk, although they may also reduce our financial return if actual operating costs are less than the subcontract payments. We cannot assure that any OTEC and SWAC/LSC plants will permit the PPAs and ESAs to yield minimum target internal rates of return. Our first projects are likely to have lower returns than subsequent projects. Variances in internal rates of return may occur due to a range of factors, including availability and structure of project financing and localized issues such as taxes, some of which may be outside of our control.

We expect our OTEC contract pricing will be charged either on an energy-only price per kWh or on the basis of a capacity payment priced per kilowatt per month and an energy usage price per kWh. We cannot assure that this pricing will enable us to recoup our funding and project costs and allow us to earn a profit.

Marketing Strategies

Our marketing and sales efforts are managed and directed by our chairman and chief executive officer, Jeremy P. Feakins, who has 40 years’ experience of senior-level sales in both commercial and governmental markets. Our marketing campaign has focused on explaining to potential customers the economic, environmental, and other benefits of OTEC and SWAC/LSC through personal contacts, industry interactions, our website, and social media channels.

Our target markets are comprised of large institutional customers that typically include governments, utilities, large resorts, hospitals, educational institutions, and municipalities. We market to them directly through personal meetings and contact by our chief executive officer and other key members of our team. We also make extensive use of centers of influence either to heighten awareness of our products in the minds of key customers’ decision-makers or to secure face-to-face meetings and preliminary agreements between our customers and our chief executive officer.

Sales cycles in our business are extremely long and complex and often involve multiple meetings with governmental, regulatory, electric utility, and corporate entities. Therefore, we cannot predict when or if any of the projects we currently have under development will progress to a signed contract or operational phase and generate revenue. We do not expect sales to be seasonal or cyclical.

Material Regulation

Our business and products are subject to material regulation. However, because we contemplate offering our products and services in different countries, the specific nature of the regulatory requirements will be wholly dependent on the nation where the project will be located and the national, state, and local regulations that apply at that location. In all cases, we expect the level of regulation will be material and will require significant permitting and ongoing compliance during the life of the project.

The most significant regulations will likely be environmental and will include mitigating possible adverse effects during both the construction and operational phases of the project. However, we believe that the limited plant site disturbance of both SWAC/LSC and OTEC projects, together with the significantly lower emissions that result from these projects as compared to fossil-fuel electrical generation, will make compliance with all such regulation manageable in the normal course.

The second most significant regulations will likely involve coordination with existing infrastructure. We believe compliance with this type of regulation is a routine civil engineering coordination process that exists for all new buildings and infrastructure projects of all types. Again, we believe that the design of both SWAC/LSC and OTEC projects can readily be modified to avoid interference with existing infrastructure in most cases.

Facilities

Our principal executive offices are located at. 3675 Market Street, Suite 200, Philadelphia PA 19104. We maintain a small office in Lancaster, PA. Our telephone number at that address is (717) 299-1344.

Intellectual Property

We use, or intend to employ in the performance of our material contracts, intellectual property rights in relation to the design and development of OTEC plants. Our intellectual property rights can be categorized broadly as proprietary know-how, technical databases, and trade secrets comprising concept designs, plant design, and economic models. Additionally, we have applied to register the trademark TOO DEEP® at the U.S. Patent and Trademark Office for the provision of desalinated deep ocean water for consumption. The U.S. Patent and Trademark Office has approved an extension of our Notice of Allowance until 2022.

We may apply for patents for components of our intellectual property for OTEC and SWAC/LSC systems, including novel or new methodologies for cold-water piping, heat exchanges, and computer-aided design programs. We cannot assure that any patents we seek will be granted.

Our intellectual property has been developed by our employees and is protected under employee agreements confirming that the rights in the inventions and developments made by the employees are our property. Confidential information is protected by nondisclosure agreements we entered into with prospective partners or other third parties with which we do business.

We have not received any notification from third parties that our processes or designs infringe any third-party rights, and we are not aware of any valid and enforceable third-party intellectual property rights that infringe our intellectual property rights. Currently, there is no patent for any company for OTEC technology.

Employees

We currently have two employees, consisting of one officer and one finance/accounting. There are no collective-bargaining agreements with our employees, and we have not experienced work interruptions or strikes.

ITEM 1A. RISK FACTORS

Investing in our common stock involves a high degree of risk. Investors should carefully consider the risks described below, as well as the other information in this report, including our financial statements and the related notes and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” before deciding whether to invest in our common stock. The occurrence of any of the events or developments described below could harm our business, financial condition, operating results, and growth prospects. In such an event, the market price of our common stock could decline, and investors may lose all or part of their investment. Additional risks and uncertainties not presently known to us or that we currently deem immaterial also may impair our business operations.

Risks Related to Our Financial Condition

Russia’s military intervention in Ukraine and the international community’s response have created substantial political and economic disruption, uncertainty, and risk.

Russia’s military intervention in Ukraine in late February 2022, Ukraine’s widespread resistance, and the NATO-led and United States coordinated economic, financial, communications, and other sanctions imposed by other countries have created significant political and economic world uncertainty. There is significant risk of expanded military confrontation between Russia and other countries, possibly including the United States. Current and likely additional international sanctions against Russia may contribute to higher costs, particularly for petroleum-based products. These and related actions, responses, and consequences that cannot now be predicted or controlled may contribute to worldwide economic reversals. In these circumstances, our efforts to commercialize our technology may be delayed or otherwise negatively impacted.

The auditors’ report for the years ended December 31, 2022 and 2021, contains an explanatory paragraph about our ability to continue as a going concern.

The report of our auditors on our consolidated financial statements for the years ended December 31, 2022 and 2021, as well as for prior years, contains an explanatory paragraph raising substantial doubt about our ability to continue as a going concern. We had a net loss of $6,912,102 and $2,670,637, respectively; used cash in operations of $327,213 and $542,630, respectively; had a working capital deficiency of $36,199,026 and $29,801,131, respectively; and had an accumulated deficit of $96,496,618 and $89,584,516, respectively, at December 31, 2022 and 2021. These factors raise substantial doubt about our ability to continue as a going concern. Our ability to continue as a going concern beyond December 31, 2022, is dependent on our ability to raise additional capital through the sale of debt or equity securities or stockholder loans and to implement our business plan during the next 12 months. The financial statements do not include any adjustments that might be necessary if we are unable to continue as a going concern. Management believes that actions presently being taken to obtain additional funding through implementing our strategic plans, broadly based marketing strategy, and sales incentives to expand operations will provide the opportunity for us to continue as a going concern.

We have no current project that will generate revenues in the near future.