UNITED

STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

N-CSR

CERTIFIED

SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment

Company Act file number 811-22499

NXG

NextGen Infrastructure Income Fund

(Exact name of registrant as specified in charter)

600

N. Pearl Street, Suite 1205

Dallas,

TX 75201

(Address of principal executive offices) (Zip code)

John

Musgrave

600

N. Pearl Street, Suite 1205

Dallas,

TX 75201

(Name and address of agent for service)

214-692-6334

Registrant's

telephone number, including area code

Date

of fiscal year end: November 30

Date

of reporting period: November 30, 2023

Item

1. Reports to Stockholders.

Table of Contents

| |

|

Shareholder Letter |

1 |

Hypothetical Growth of a $10,000 Investment (Unaudited) |

5 |

Key Financial Data (Supplemental Unaudited Information) |

6 |

Allocation of Portfolio Assets (Unaudited) |

7 |

Schedule of Investments |

8 |

Statement of Assets & Liabilities |

11 |

Statement of Operations |

12 |

Statements of Changes in Net Assets |

13 |

Statement of Cash Flows |

14 |

Financial Highlights |

15 |

Notes to Financial Statements |

16 |

Report of Independent Registered Public Accounting Firm |

25 |

Trustees and Executive Officers (Unaudited) |

26 |

Certain Changes Occurring During the Prior Fiscal Year |

28 |

Additional Information (Unaudited) |

29 |

NXG NextGen Infrastructure Income Fund

Shareholder Letter |

Dear Fellow Shareholder,

NXG NextGen Infrastructure Income Fund (the “Fund”) generated a negative return for shareholders for the Fund’s twelve-month fiscal period, which ended November 30, 2023 (the “Period”). For the Period, the Fund delivered a net asset value total return (equal to the change in net asset value (NAV) per share plus reinvested cash distributions paid during the Period) of -19.04%, versus a total return of -0.76% for the S&P Global Infrastructure Index. See index descriptions at the end of this report. The Fund’s share price total return (equal to the change in market price per share plus reinvested cash distributions from underlying Fund investments paid during the Period) was -16.38% for the Period. The share price total return differs from the NAV total return due to fluctuations in the discount of share price to NAV. The Fund’s shares traded at a 19.8% discount to NAV as of the end of the Period, compared to a discount of 22.3% at the end of the Fund’s last fiscal year and a 23.3% discount on May 31, 2023.

Market and Themes Overview

The Fund invests along four main themes:

| |

●

|

Clean & Sustainable Infrastructure – Renewable energy, sustainable, and water

|

| |

●

|

Communication & Technology Infrastructure – Data storage and information highway

|

| |

●

|

Energy Infrastructure – Power generation and transmission and midstream energy

|

| |

●

|

Industrial Infrastructure – Freight transportation, ports and airports, and engineering

|

The Period began on a high note with strong performance through the month of January, continuing the recovery in global infrastructure stocks that followed a sharp decline in September and October of 2022. However, this progress was abruptly disrupted by a regional banking crisis involving the failure of several banks. The Federal Reserve found itself confronted with a challenging situation as it tackled two major issues concurrently: elevated inflation and the restoration of financial stability.

Throughout the Period, macroeconomic factors, including an apparent continuation of a soft Chinese economy, global recession fears, restrictive policy from central banks and subsequently elevated interest rates as compared to prior periods dominated concerns. These elevated interest rates, triggered by central banks worldwide in an effort to bring inflation to heel, introduced challenges to infrastructure equity returns. Challenges as sources of investment capital were diverted from commercial uses as investors found attractive yields in government treasury bonds. The level of interest rates consequently required to attract investors to commercial investment impacted the marginal cost of projects from cost of capital and equipment. The combined effect was a reduction in margins and activity that adversely impacted the current and potential returns for equity securities, particularly those with large capital requirements and margins that are more highly levered to the cost of capital. Within the Fund, the themes that were most impacted by this elevated rate regime were Clean & Sustainable Infrastructure and Industrial Infrastructure.

Opportunities for North American energy infrastructure continue even as the sector prioritizes maximizing shareholder returns. Given its robust fundamentals, appealing valuations, and defensive nature in an environment of high interest rates and inflation, combined with strong free cash flow (FCF) generation, we believe the midstream sector is well-positioned to potentially outperform on a relative basis. We also believe this recovery may have been influenced by the market’s realization of midstream energy companies’ financial strength. Remarkably, these companies generally do not require external capital due to their substantial FCF generation.

1

Furthermore, we expect the end of the central bank rate-hiking cycle and eventual move to moderation of policy rates to ease financial pressures on infrastructure operators more broadly, consequently improving returns to shareholders. Private consumers and government entities in the US and worldwide continue to drive demand for sustainable electrification, information connectivity, and streamlined supply chains, all of which will require investment in infrastructure assets. We believe this combination of factors sets a very favorable backdrop for equity investment in infrastructure companies.

Fund Performance

The Fund saw underperformance in high-yield oriented and longer-term growth-oriented stocks as interest rates rose over the Period. For some companies, execution delays in the Inflation Reduction Act (IRA) were an additional negative factor. Global hydrocarbon demand remained resilient while weakening somewhat near the end of the Period. Energy Infrastructure was the largest allocation in the Fund and along with Industrial Infrastructure were the themes with positive contributions to the Fund’s performance. Clean & Sustainable Infrastructure was the second largest allocation but was the largest performance detractor. The Fund had a small negative contribution from Communication & Technology Infrastructure.

The top contributors to performance were Equitrans Midstream Corporation, Targa Resources Corp., and Energy Transfer LP, all of which are Energy Infrastructure companies. All three companies were positively impacted by strong petroleum commodity prices and increased demand for domestic hydrocarbons.

Equitrans Midstream owns, develops and operates midstream assets in the Appalachian basin. Most notably and very publicly, it is working to complete the Mountain Valley Pipeline (MVP). Equitrans is strategically positioned to de-bottleneck the natural gas supply from the Appalachian basin with MVP and MVP Southgate projects. Previously and during the Period, MVP has been a high-profile, politically sensitive project. Within the passage of the May 2023 debt ceiling bill was a measure to complete the long-stalled pipeline. The pipeline is nearly complete, which should unlock the long sought after revenues for the company and provide access to much needed natural gas.

Targa Resources, which gathers, processes, fractionates, and exports natural gas and natural gas liquids (NGLs), took radical action with its dividend and capital spending in 2020 to repair its balance sheet and drive positive FCF. Throughout the period, Targa sustained its track record of industry-leading growth, surprising investors with substantial share buybacks and unveiling a new capital allocation plan aimed at returning more capital to investors. The company remained committed to executing various growth projects, including processing plants, fractionators, and additional export capacity, contributing to the global supply of dependable energy sources.

Energy Transfer, a Large Cap Diversified MLP company, maintained its successful track record of integrating acquisitions, facilitating steady business growth alongside four distribution increases and robust positive FCF. Throughout the year, the company announced several strategic acquisitions, expanding its asset footprint and operational capabilities. Additionally, improved operating fundamentals led to an increase in guidance, further bolstering the company’s performance.

The biggest detractors from performance were NextEra Energy Partners, LP, Atlantica Sustainable Infrastructure plc, and Plug Power Inc., all of which are Clean & Sustainable Infrastructure companies.

NextEra Energy Partners owns and operates a diversified portfolio of highly contracted renewable and conventional power generation projects. We believe the stock faced headwinds due to interest rate sensitivity and experienced a sell-off in line with the broader utility sector and clean energy-themed stocks. Additionally, the company was impacted by investors’ concerns over asset valuations and implications for the renewable YieldCo model in a higher interest rate environment.

Atlantica Sustainable Infrastructure provides traditional and renewable energy solutions primarily in Europe and the Americas. Similarly to NextEra, we believe the stock faced valuation headwinds due to interest rate sensitivity and experienced a sell-off in line with the broader utility sector as well as the sustainability of the YieldCo model.

2

Plug Power operates a “green” hydrogen company and focuses on building an end-to-end hydrogen ecosystem of production, storage, and delivery to energy generation. There are several potential positive catalysts in Plug’s future, not the least of which was the Section 45V production tax credit in the IRA clarification; however, the lack of clarification and overall subpar execution resulted in liquidity concerns for the company and subsequently weighed significantly on the stock price. These liquidity concerns compelled the company to issue a “going concern” warning with its third quarter 2023 results.

Leverage

The Fund employs leverage for additional income and total return potential. We seek to maintain a leverage ratio between 20% and 35% of managed assets during normal market conditions. Average leverage for the period was 29% of managed assets, which compares to an average leverage ratio of 31% in the prior fiscal year. As the prices of the Fund’s investments increase or decline, there is a risk that the impact of the Fund’s NAV and total return will be negatively impacted by leverage.

Closing

The period proved to be challenging in terms of performance and the factors impacting the multi-faceted drivers of Fund’s investment themes. For this reason, the Fund’s exposure was pivoted to investments with longer lived assets and more stable and identifiable cash flow generation. Challenging times often beget return potential and we believe that the near term future presents such an opportunity. Many company strategies and business plans were sorely tested and those that persevered are generally stronger for it, creating a potentially better company execution base and positive operating leverage over the next 12 to 24 months. There are and will continue to be macro headwinds and tailwinds in addition to specific company execution and opportunity sets and we aim to guide the Fund through them profitably.

We truly appreciate your support and look forward to continuing to help you achieve your investment goals.

Sincerely,

John Musgrave

Chief Executive Officer, President, Chief Investment Officer and Portfolio Manager

The information provided herein represents the opinion of the Fund’s portfolio managers and is not intended to be a forecast of future events, a guarantee of future results, nor investment advice. The opinions expressed are as of the date of this report and are subject to change.

The information in this report is not a complete analysis of every aspect of any market, sector, industry, security or the Fund itself. Statements of fact are from sources considered reliable, but the Fund makes no representation or warranty as to their completeness or accuracy. Discussions of specific investments are for illustration only and are not intended as recommendations of individual investments. Please refer to the Schedule of Investments for a complete list of Fund holdings.

Past performance does not guarantee future results. Investment return, net asset value and common share market price will fluctuate so that you may have a gain or loss when you sell shares. Since the Fund is a closed-end management investment company, shares of the Fund may trade at a discount or premium from net asset value. This characteristic is separate and distinct from the risk that net asset value could decrease as a result of investment activities and may be a greater risk to investors expecting to sell their shares after a short time. The Fund cannot predict whether shares will trade at, above or below net asset value. The Fund should not be viewed as a vehicle for trading purposes. It is designed primarily for risk-tolerant long-term investors.

An investment in the Fund involves risks. Leverage creates risks which may adversely affect returns, including the likelihood of greater volatility of net asset value and market price of the Fund’s common shares. The Fund is non-diversified, meaning it may concentrate its assets in fewer individual holdings than a diversified fund. Therefore, the Fund is more exposed to individual stock volatility than a diversified fund.

The Fund invests in infrastructure companies, which may be subject to a variety of factors that may adversely affect their business or operations, including high interest costs in connection with capital construction and improvement programs, high leverage, costs associated with environmental and other regulations, the effects of economic slowdown, surplus capacity, increased competition from other providers

3

of services, uncertainties concerning the availability of fuel at reasonable prices, the effects of energy conservation policies and other factors. Sustainable infrastructure investments are subject to certain additional risks including high dependency upon on government policies that support renewable power generation and enhance the economic viability of owning renewable electric generation assets; adverse impacts from the reduction or discontinuation of tax benefits and other similar subsidies that benefit sustainable infrastructure companies; dependency on suitable weather condition and risk of damage to components used in the generation of renewable energy by severe weather; adverse changes and volatility in the wholesale market price for electricity in the markets served; the use of newly developed, less proven, technologies and the risk of failure of new technology to perform as anticipated; and dependence on a limited number of suppliers of system components and the occurrence of shortages, delays or component price changes. There is a risk that regulations that provide incentives for renewable energy could change or expire in a manner that adversely impacts the market for sustainable infrastructure companies generally. Technology and communications infrastructure investments are subject to certain additional risks including rapidly changing technologies and existing product obsolescence; short product life cycles; fierce competition; high research and development costs; aggressive pricing and reduced profit margins; the loss of patent, copyright and trademark protections; cyclical market patterns; evolving industry standards; frequent new product introductions and new market entrants; cyber security risks that include, among other things, theft, unauthorized monitoring, release, misuse, loss, destruction or corruption of confidential and highly restricted data, denial of service attacks, unauthorized access to relevant systems, compromises to networks or devices that the information infrastructure companies use, or operational disruption or failures in the physical infrastructure or operating systems, potentially resulting in, among other things, financial losses, violations of applicable privacy and other laws, regulatory fines, penalties, reputational damage, reimbursement or other compensation costs and/or additional compliance costs.

The Fund incurs operating expenses, including advisory fees, as well as leverage costs. Investment returns for the Fund are shown net of fees and expenses.

Fund holdings and sector allocations are subject to change at any time and are not recommendations to buy or sell any security. Please refer to the Schedule of Investments for a complete list of Fund holdings.

The S&P 500 Index is an unmanaged index of common stocks that is frequently used as a general measure of stock market performance. The S&P Global Infrastructure index is an unmanaged index of 75 companies around the world chosen to represent the infrastructure industry in three distinct infrastructure clusters: energy, transportation and utilities. The indices include reinvested dividends by do not include fees or expenses. It is not possible to invest directly in an index.

4

NXG NextGen Infrastructure Income Fund

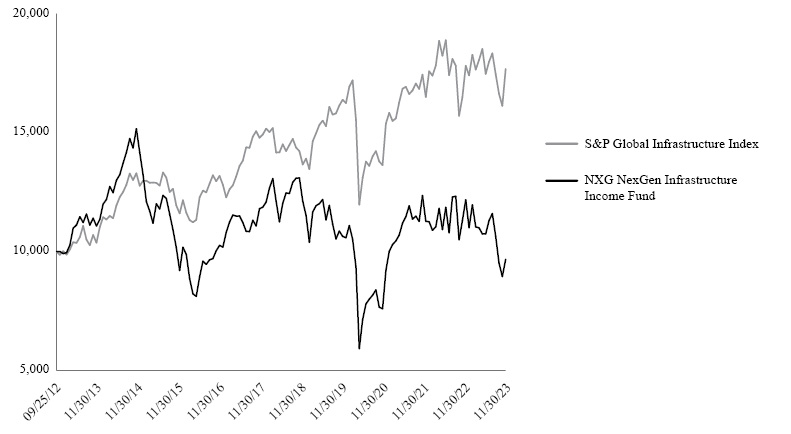

Hypothetical Growth of a $10,000 Investment (Unaudited) |

AVERAGE ANNUAL RETURNS

November 30, 2023 |

| |

1 Year |

5 Year |

10 Year |

Cushing NextGen Infrastructure Income Fund |

-19.04% |

-1.89% |

-1.08% |

| |

|

|

|

S&P Global Infrastructure Index |

-0.76% |

4.91% |

4.53% |

Data for NXG NextGen Infrastructure Income Fund (the “Fund”) represents returns based on the change in the Fund’s net asset value assuming the reinvestment of all dividends and distributions. These returns differ from the total investment return based on market value of the Fund’s shares due to the difference between the Fund’s net asset value of its shares outstanding (See page 16 for total investment return based on market value). Past performance is no guarantee of future results.

The S&P Global Infrastructure Index is an unmanaged index of 75 complanies around the world chosen to represent the infrastructure industry in three distinct clusters: energy, transportation and utiliities. You cannot invest directly in an index.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of the Fund shares.

5

NXG NextGen Infrastructure Income Fund

Key Financial Data (Supplemental Unaudited Information) |

The Information presented below regarding Distributable Cash Flow is supplemental non-GAAP financial information, which we believe is meaningful to understanding our operating performance. Supplemental non-GAAP measures should be read in conjunction with our full financial statements.

| |

|

Fiscal Year

Ended

11/30/23 |

|

|

Fiscal Year

Ended

11/30/22 |

|

|

Fiscal Year

Ended

11/30/21 |

|

|

Fiscal Year

Ended

11/30/20 |

|

|

Fiscal Year

Ended

11/30/19 (a) |

|

FINANCIAL DATA |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total income from investments |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Distributions and dividends received, net of foreign taxes withheld |

|

$ |

9,878,217 |

|

|

$ |

8,667,303 |

|

|

$ |

9,924,383 |

|

|

$ |

7,035,276 |

|

|

$ |

8,582,200 |

|

Interest income & other |

|

$ |

878,205 |

|

|

$ |

1,047,575 |

|

|

$ |

1,061,057 |

|

|

$ |

1,883,405 |

|

|

$ |

3,366,509 |

|

Total income from investments |

|

$ |

10,756,422 |

|

|

$ |

9,714,878 |

|

|

$ |

10,985,440 |

|

|

$ |

8,918,681 |

|

|

$ |

11,948,709 |

|

Advisery fee and operating expenses |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Advisery fees, less expenses waived by Adviser |

|

$ |

1,645,272 |

|

|

$ |

1,864,503 |

|

|

$ |

1,894,568 |

|

|

$ |

1,397,229 |

|

|

$ |

2,044,632 |

|

Operating expenses (b) |

|

|

792,592 |

|

|

|

778,446 |

|

|

|

735,891 |

|

|

|

720,285 |

|

|

|

628,582 |

|

Leverage costs |

|

|

2,594,415 |

|

|

|

1,285,151 |

|

|

|

538,072 |

|

|

|

169,833 |

|

|

|

723,266 |

|

Total advisory fees and operating expenses |

|

$ |

5,032,279 |

|

|

$ |

3,928,100 |

|

|

$ |

3,168,531 |

|

|

$ |

2,287,347 |

|

|

$ |

3,396,480 |

|

Distributable Cash Flow (DCF) (c) |

|

$ |

5,724,143 |

|

|

$ |

5,786,778 |

|

|

$ |

7,816,909 |

|

|

$ |

6,631,334 |

|

|

$ |

8,552,229 |

|

Distributions paid on common stock |

|

$ |

10,241,388 |

|

|

$ |

6,656,226 |

|

|

$ |

6,656,226 |

|

|

$ |

11,863,818 |

|

|

$ |

14,226,174 |

|

Distributions paid on common stock per share |

|

$ |

3.94 |

|

|

$ |

2.56 |

|

|

$ |

2.56 |

|

|

$ |

4.56 |

|

|

$ |

6.56 |

|

Distribution Coverage Ratio |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Before advisory fee and operating expenses |

|

|

1.1x |

|

|

|

1.5x |

|

|

|

1.7x |

|

|

|

0.8x |

|

|

|

0.8x |

|

After advisory fee and operating expenses |

|

|

0.6x |

|

|

|

0.9x |

|

|

|

1.2x |

|

|

|

0.6x |

|

|

|

0.6x |

|

OTHER FUND DATA (end of period) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Assets, end of fiscal year |

|

|

146,276,580 |

|

|

|

194,194,289 |

|

|

|

202,602,696 |

|

|

|

137,938,612 |

|

|

|

151,957,589 |

|

Unrealized appreciation (depreciation) |

|

|

10,735,135 |

|

|

|

5,288,776 |

|

|

|

6,456,872 |

|

|

|

16,360,633 |

|

|

|

(14,379,305 |

) |

Short-term borrowings |

|

|

36,810,000 |

|

|

|

41,410,000 |

|

|

|

56,410,000 |

|

|

|

18,310,000 |

|

|

|

0 |

|

Short-term borrowings as a percent of total assets |

|

|

25 |

% |

|

|

21 |

% |

|

|

28 |

% |

|

|

13 |

% |

|

|

0 |

% |

Net Assets, end of fiscal year |

|

|

103,681,589 |

|

|

|

142,434,269 |

|

|

|

138,537,314 |

|

|

|

119,348,473 |

|

|

|

151,638,988 |

|

Net Asset Value per common share |

|

$ |

39.85 |

|

|

$ |

54.75 |

|

|

$ |

53.25 |

|

|

$ |

45.87 |

|

|

$ |

58.28 |

|

Market Value per share |

|

$ |

31.97 |

|

|

$ |

42.53 |

|

|

$ |

45.02 |

|

|

$ |

35.74 |

|

|

$ |

50.72 |

|

Market Capitalization |

|

$ |

83,176,797 |

|

|

$ |

110,650,896 |

|

|

$ |

117,129,164 |

|

|

$ |

92,985,258 |

|

|

$ |

527,835,787 |

|

Shares Outstanding |

|

|

2,601,714 |

|

|

|

2,601,714 |

|

|

|

2,601,714 |

|

|

|

2,601,714 |

|

|

|

10,406,857 |

|

|

(a)

|

Per share data adjusted for 1:4 reverse stock split completed as of June 12, 2020.

|

|

(b)

|

Excludes expenses related to capital raising.

|

|

(c)

|

“Net Investment Income” on the Statement of Operations is adjusted as follows to reconcile to Distributable Cash Flow: increased by the return of capital on MLP distributions.

|

6

NXG NextGen Infrastructure Income Fund

Allocation of Portfolio Assets(1) (Unaudited)

November 30, 2023

(Expressed as a Percentage of Total Investments) |

Large Cap Diversified C Corps (2)(3) |

|

|

26.6 |

% |

Natural Gas Transportation & Storage (2) |

|

|

15.3 |

% |

Large Cap MLP (3) |

|

|

11.0 |

% |

Natural Gas Gatherers & Processors (2) |

|

|

7.0 |

% |

Utilities (2) |

|

|

6.8 |

% |

Short-Term Investments |

|

|

6.7 |

% |

NG Gatherers & Processors (2) |

|

|

4.1 |

% |

Engineering & Construction (2) |

|

|

3.9 |

% |

Refiners (2) |

|

|

3.7 |

% |

Cruide Oil & Refined Products (2) |

|

|

3.0 |

% |

Solar (2) |

|

|

2.0 |

% |

Upstream MLP (3) |

|

|

1.9 |

% |

LNG Midstream (2) |

|

|

1.8 |

% |

Mineral Royalties (2) |

|

|

1.5 |

% |

Renewable Generation(2) |

|

|

1.3 |

% |

Yield Co (3) |

|

|

1.1 |

% |

Towers (4) |

|

|

0.8 |

% |

Cloud Services (2) |

|

|

0.8 |

% |

Industrials (2) |

|

|

0.4 |

% |

Diversified Renewable Generation (2) |

|

|

0.3 |

% |

| |

|

|

100.0 |

% |

|

(1)

|

Fund holdings and sector allocations are subject to change and there is no assurance that the Fund will continue to hold any particular security.

|

|

(2)

|

Common Stock

|

|

(3)

|

Master Limited Partnerships and Related Companies

|

|

(4)

|

Real Estate Investment Trusts

|

|

(5)

|

Senior Notes

|

7

NXG NextGen Infrastructure Income Fund |

Schedule of Investments |

November 30, 2023 |

Common Stock — 104.0% |

|

Shares |

|

|

Fair Value |

|

Cloud Services — 1.1% |

|

|

|

|

|

|

|

|

Akamai Technologies, Inc.(3) |

|

|

10,000 |

|

|

$ |

1,155,300 |

|

| |

|

|

|

|

|

|

|

|

Crude Oil & Refined Products — 4.2% |

|

|

|

|

|

|

|

|

Genesis Energy, L.P. |

|

|

345,000 |

|

|

|

4,333,200 |

|

| |

|

|

|

|

|

|

|

|

Diversified Renewable Generation — 0.5% |

|

|

|

|

|

|

|

|

Renew Energy Global plc(2)(3) |

|

|

75,000 |

|

|

|

483,000 |

|

| |

|

|

|

|

|

|

|

|

Engineering & Construction — 5.4% |

|

|

|

|

|

|

|

|

Ameresco, Inc.(3) |

|

|

18,000 |

|

|

|

539,280 |

|

Jacobs Solutions, Inc. |

|

|

40,000 |

|

|

|

5,087,200 |

|

| |

|

|

|

|

|

|

5,626,480 |

|

Industrials- 0.6% |

|

|

|

|

|

|

|

|

Plug Power, Inc.(3) |

|

|

150,000 |

|

|

|

606,000 |

|

| |

|

|

|

|

|

|

|

|

Large Cap Diversified C Corps. - 31.0% |

|

|

|

|

|

|

|

|

Cheniere Energy, Inc. |

|

|

31,000 |

|

|

|

5,646,650 |

|

Kinder Morgan, Inc. |

|

|

472,000 |

|

|

|

8,293,040 |

|

Oneok, Inc. |

|

|

79,000 |

|

|

|

5,439,150 |

|

Pembina Pipeline Corporation(1)(2) |

|

|

131,000 |

|

|

|

4,379,330 |

|

TC Energy Corporation(2) |

|

|

80,000 |

|

|

|

3,001,600 |

|

Williams Companies, Inc. |

|

|

147,000 |

|

|

|

5,408,130 |

|

| |

|

|

|

|

|

|

32,167,900 |

|

LNG Midstream — 2.6% |

|

|

|

|

|

|

|

|

New Fortress Energy, Inc. |

|

|

70,000 |

|

|

|

2,693,600 |

|

| |

|

|

|

|

|

|

|

|

Mineral Royalties — 2.1% |

|

|

|

|

|

|

|

|

Sitio Royalties Corporation |

|

|

100,000 |

|

|

|

2,203,000 |

|

| |

|

|

|

|

|

|

|

|

Natural Gas Gatherers & Processors — 9.9% |

|

|

|

|

|

|

|

|

DT Midstream, Inc. |

|

|

78,000 |

|

|

|

4,468,620 |

|

Western Midstream Partners, L.P. |

|

|

194,000 |

|

|

|

5,785,080 |

|

| |

|

|

|

|

|

|

10,253,700 |

|

NG Gatherers & Processors — 5.7% |

|

|

|

|

|

|

|

|

Equitrans Midstream Corporation(1) |

|

|

633,000 |

|

|

|

5,937,540 |

|

| |

|

|

|

|

|

|

|

|

Natural Gas Transportation & Storage — 21.6% |

|

|

|

|

|

|

|

|

Antero Midstream Corporation |

|

|

256,000 |

|

|

|

3,409,920 |

|

Enlink Midstream LLC |

|

|

308,000 |

|

|

|

4,210,360 |

|

Hess Midstream, L.P. |

|

|

150,000 |

|

|

|

4,881,000 |

|

Targa Res Corporation |

|

|

109,000 |

|

|

|

9,859,050 |

|

| |

|

|

|

|

|

|

22,360,330 |

|

Refiners — 5.1% |

|

|

|

|

|

|

|

|

Marathon Pete Corporation |

|

|

21,000 |

|

|

|

3,132,990 |

|

Phillips 66 |

|

|

17,000 |

|

|

|

2,191,130 |

|

| |

|

|

|

|

|

|

5,324,120 |

|

See Accompanying Notes to the Financial Statements.

8

NXG NextGen Infrastructure Income Fund |

Schedule of Investments |

November 30, 2023 — (Continued) |

Common Stock — (Continued) |

|

Shares |

|

|

Fair Value |

|

Renewable Generation — 1.9% |

|

|

|

|

|

|

|

|

Ormat Technologies, Inc. |

|

|

20,000 |

|

|

$ |

1,346,400 |

|

Sunnova Energy International, Inc.(3) |

|

|

50,000 |

|

|

|

580,000 |

|

| |

|

|

|

|

|

|

1,926,400 |

|

Solar — 2.7% |

|

|

|

|

|

|

|

|

Atlantica Sustainable Infrastructure plc(1)(2) |

|

|

150,000 |

|

|

|

2,853,000 |

|

| |

|

|

|

|

|

|

|

|

Utilities — 9.6% |

|

|

|

|

|

|

|

|

Clearway Energy, Inc.(1) |

|

|

229,000 |

|

|

|

5,718,130 |

|

Consolidated Edison, Inc. |

|

|

34,000 |

|

|

|

3,063,740 |

|

Vistra Corporation |

|

|

33,000 |

|

|

|

1,168,530 |

|

| |

|

|

|

|

|

|

9,950,400 |

|

Total Common Stocks (Cost $98,857,915) |

|

|

|

|

|

$ |

107,873,970 |

|

| |

|

|

|

|

|

|

|

|

Master Limited Partnerships and

Related Companies — 26.1% |

|

Units |

|

|

|

|

Large Cap Diversified C Corps — 6.5% |

|

|

|

|

|

|

|

|

Plains GP Holdings, L.P.(1) |

|

|

414,000 |

|

|

$ |

6,690,240 |

|

| |

|

|

|

|

|

|

|

|

Large Cap MLP — 15.4% |

|

|

|

|

|

|

|

|

Energy Transfer, L.P.(1) |

|

|

578,999 |

|

|

|

8,042,302 |

|

Enterprise Prods Partners, L.P. |

|

|

145,000 |

|

|

|

3,883,100 |

|

MPLX, L.P.(1) |

|

|

111,000 |

|

|

|

4,047,060 |

|

| |

|

|

|

|

|

|

15,972,462 |

|

Upstream MLP — 2.7% |

|

|

|

|

|

|

|

|

TXO Energy Partners, L.P. |

|

|

154,000 |

|

|

|

2,812,040 |

|

| |

|

|

|

|

|

|

|

|

YieldCo — 1.5% |

|

|

|

|

|

|

|

|

NextEra Energy Partners, L.P. |

|

|

65,000 |

|

|

|

1,530,100 |

|

| |

|

|

|

|

|

|

|

|

Total Master Limited Partnerships and Related Companies (Cost $20,364,974) |

|

|

|

|

|

$ |

27,004,842 |

|

| |

|

|

|

|

|

|

|

|

Real Estate Investment Trusts — 1.1% |

|

Shares |

|

|

|

|

Towers — 1.1% |

|

|

|

|

|

|

|

|

Crown Castle, Inc. |

|

|

10,000 |

|

|

$ |

1,172,800 |

|

| |

|

|

|

|

|

|

|

|

Total Real Estate Investment Trusts (Cost $1,160,905) |

|

|

|

|

|

$ |

1,172,800 |

|

| |

|

|

|

|

|

|

|

|

Fixed Income — 0.0% |

|

Principal

Amount |

|

|

|

|

Exploration & Production — 0.0% |

|

|

|

|

|

|

|

|

Sanchez Energy Corporation, 6.125%, due 01/15/2023(1) |

|

|

5,000,000 |

|

|

$ |

— |

|

| |

|

|

|

|

|

|

|

|

Total Fixed Income (Cost $4,932,683) |

|

|

|

|

|

$ |

— |

|

See Accompanying Notes to the Financial Statements.

9

NXG NextGen Infrastructure Income Fund |

Schedule of Investments |

November 30, 2023 — (Continued) |

Short-Term Investments -

Investment Companies — 9.5% |

|

Shares |

|

|

Fair Value |

|

First American Government Obligations Fund - Class X, 5.29%(1)(4) |

|

|

4,912,496 |

|

|

$ |

4,912,495 |

|

First American Treasury Obligations Fund - Class X, 5.28%(1)(4) |

|

|

4,912,495 |

|

|

|

4,912,495 |

|

Total Short-Term Investments - Investment Companies (Cost $9,824,990) |

|

|

|

|

|

$ |

9,824,990 |

|

Total Investments — 140.7% (Cost $135,141,467) |

|

|

|

|

|

$ |

145,876,602 |

|

Liabilities in Excess of Other Assets — (40.7)% |

|

|

|

|

|

|

(42,195,013 |

) |

Net Assets Applicable to Common Stockholders — 100.0% |

|

|

|

|

|

$ |

103,681,589 |

|

|

(1)

|

All or a portion of these securities are held as collateral pursuant to the loan agreements.

|

|

(2)

|

Foreign issued security. Foreign concentration is as follows: Canada 7.12% and United Kingdom 3.22%.

|

|

(3)

|

No distribution or dividend was made during the fiscal year ended November 30, 2023. As such, it is classified as a non-income producing security as of November 30, 2023.

|

|

(4)

|

Rate reported is the current yield as of November 30, 2023.

|

See Accompanying Notes to the Financial Statements.

10

NXG NextGen Infrastructure Income Fund

Statement of Assets & Liabilities

November 30, 2023 |

Assets |

|

|

|

|

Investments, at fair value (cost $135,141,467) |

|

$ |

145,876,602 |

|

Distributions and dividends receivable |

|

|

317,017 |

|

Prepaid expenses and other receivables |

|

|

82,961 |

|

Total assets |

|

|

146,276,580 |

|

Liabilities |

|

|

|

|

Short-term borrowings |

|

|

36,810,000 |

|

Distributions and dividends payable |

|

|

18,925 |

|

Payable for investments purchased |

|

|

5,571,068 |

|

Accrued interest expense |

|

|

2,383 |

|

Accrued expenses and other liabilities |

|

|

192,615 |

|

Total liabilities |

|

|

42,594,991 |

|

Net assets applicable to common stockholders |

|

$ |

103,681,589 |

|

Components of Net Assets |

|

|

|

|

Capital stock, $0.001 par value; 2,601,714 shares issued and outstanding (unlimited shares authorized) |

|

$ |

2,602 |

|

Additional paid-in capital |

|

|

144,404,276 |

|

Accumulated net losses |

|

|

(40,725,289 |

) |

Net assets applicable to common stockholders |

|

$ |

103,681,589 |

|

Net asset value per common share outstanding (net assets applicable to common shares divided by common shares outstanding) |

|

$ |

39.85 |

|

See Accompanying Notes to the Financial Statements.

11

NXG NextGen Infrastructure Income Fund

Statement of Operations

Fiscal Year Ended November 30, 2023 |

Investment Income |

|

|

|

|

Distributions and dividends received, net of foreign taxes withheld of $175,582 |

|

$ |

9,878,217 |

|

Less: return of capital on distributions |

|

|

(5,190,778 |

) |

Distribution and dividend income |

|

|

4,687,439 |

|

Interest income |

|

|

878,177 |

|

Other income |

|

|

28 |

|

Total Investment Income |

|

|

5,565,644 |

|

Expenses |

|

|

|

|

Adviser fees |

|

|

2,054,840 |

|

Professional fees |

|

|

262,123 |

|

Trustees’ fees |

|

|

222,866 |

|

Administrator fees |

|

|

137,296 |

|

Insurance expense |

|

|

52,052 |

|

Reports to stockholders |

|

|

40,240 |

|

Registration fees |

|

|

31,564 |

|

Custodian fees and expenses |

|

|

23,649 |

|

Transfer agent fees |

|

|

19,046 |

|

Fund accounting fees |

|

|

3,756 |

|

Total Expenses before Interest Expense |

|

|

2,847,432 |

|

Interest expense |

|

|

2,594,415 |

|

Total Expenses |

|

|

5,441,847 |

|

Less: expense waived by Adviser |

|

|

(409,568 |

) |

Net Expenses |

|

|

5,032,279 |

|

Net Investment Income |

|

|

533,365 |

|

Realized and Unrealized Gain (Loss) on Investments |

|

|

|

|

Net realized loss on investments |

|

|

(35,266,157 |

) |

Net realized gain on options |

|

|

737,749 |

|

Net realized loss on investments and options |

|

|

(34,528,408 |

) |

Net change in unrealized appreciation of investments |

|

|

5,483,751 |

|

Net Realized and Unrealized Loss on Investments |

|

|

(29,044,657 |

) |

Net Decrease in Net Assets Applicable to Common Stockholders Resulting from Operations |

|

$ |

(28,511,292 |

) |

See Accompanying Notes to the Financial Statements.

12

NXG NextGen Infrastructure Income Fund

Statements of Changes in Net Assets |

| |

|

Fiscal Year

Ended

November 30,

2023 |

|

|

Fiscal Year

Ended

November 30,

2022 |

|

Operations |

|

|

|

|

|

|

|

|

Net investment income income (loss) |

|

$ |

533,365 |

|

|

$ |

(160,138 |

) |

Net realized gain (loss) on investments and options |

|

|

(34,528,408 |

) |

|

|

11,907,876 |

|

Net change in unrealized appreciation/depreciation of investments and foreign currency |

|

|

5,483,751 |

|

|

|

(1,194,557 |

) |

Net increase (decrease) in net assets applicable to common stockholders resulting from operations |

|

|

(28,511,292 |

) |

|

|

10,553,181 |

|

Distributions and Dividends to Common Stockholders |

|

|

|

|

|

|

|

|

Distributable earnings |

|

|

(5,658,992 |

) |

|

|

— |

|

Return of capital |

|

|

(4,582,396 |

) |

|

|

(6,656,226 |

) |

Total distributions and dividends to common stockholders |

|

|

(10,241,388 |

) |

|

|

(6,656,226 |

) |

Total increase (decrease) in net assets applicable to common stockholders |

|

|

(38,752,680 |

) |

|

|

3,896,955 |

|

Net Assets |

|

|

|

|

|

|

|

|

Beginning of fiscal year |

|

|

142,434,269 |

|

|

|

138,537,314 |

|

End of fiscal year |

|

$ |

103,681,589 |

|

|

$ |

142,434,269 |

|

See Accompanying Notes to the Financial Statements.

13

NXG NextGen Infrastructure Income Fund

Statement of Cash Flows

Fiscal Year Ended November 30, 2023 |

OPERATING ACTIVITIES |

|

|

|

|

Net Decrease in Net Assets Applicable to Common Stockholders |

|

|

|

|

Resulting from Operations |

|

$ |

(28,511,292 |

) |

Adjustments to reconcile net decrease in the net assets applicable to common stockholders resulting from operations to net cash provided by operating activities |

|

|

|

|

Net change in unrealized appreciation/depreciation of investments and foreign currency |

|

|

(5,483,751 |

) |

Purchases of investments |

|

|

(398,736,812 |

) |

Proceeds from sales of investments and other transactions |

|

|

407,072,327 |

|

Proceeds from option transactions, net |

|

|

3,784,702 |

|

Return of capital on distributions and dividends |

|

|

5,190,778 |

|

Net realized loss on sales of investments and options |

|

|

34,528,408 |

|

Net sales of short-term investments |

|

|

720,325 |

|

Net accretion/amortization of senior notes’ premiums/discounts |

|

|

52,483 |

|

Changes in operating assets and liabilities |

|

|

|

|

Distributions and dividends receivable |

|

|

68,046 |

|

Prepaid expenses and other receivables |

|

|

318,062 |

|

Payable to Adviser, net of waiver |

|

|

(154,882 |

) |

Payable for investments purchased |

|

|

5,571,068 |

|

Due to custodian |

|

|

(10,000,000 |

) |

Accrued interest expense |

|

|

(7,124 |

) |

Accrued expenses and other liabilities |

|

|

11,635 |

|

Net cash provided by operating activities |

|

|

14,423,973 |

|

FINANCING ACTIVITIES |

|

|

|

|

Proceeds from borrowing facility |

|

|

71,600,000 |

|

Repayment of borrowing facility |

|

|

(76,200,000 |

) |

Distributions and dividends paid to common stockholders |

|

|

(10,227,112 |

) |

Net cash used in financing activities |

|

|

(14,827,112 |

) |

CHANGE IN CASH AND CASH EQUIVALENTS |

|

|

(403,139 |

) |

CASH AND CASH EQUIVALENTS: |

|

|

|

|

Beginning of fiscal year |

|

|

403,139 |

|

End of fiscal year |

|

$ |

— |

|

SUPPLEMENTAL DISCLOSURE OF CASH FLOW AND NON-CASH INFORMATION |

|

|

|

|

Interest Paid |

|

$ |

2,601,539 |

|

See Accompanying Notes to the Financial Statements.

14

NXG NextGen Infrastructure Income Fund

Financial Highlights |

| |

|

Fiscal Year

Ended

November 30,

2023 |

|

|

Fiscal Year

Ended

November 30,

2022 |

|

|

Fiscal Year

Ended

November 30,

2021 |

|

|

Fiscal Year

Ended

November 30,

2020 |

|

|

Fiscal Year

Ended

November 30,

2019(1) |

|

Per Common Share Data (2) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net Asset Value, beginning of fiscal year |

|

$ |

54.75 |

|

|

$ |

53.25 |

|

|

$ |

45.87 |

|

|

$ |

58.28 |

|

|

$ |

70.12 |

|

Income from Investment Operations: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net investment income (loss) |

|

|

0.21 |

|

|

|

(0.06 |

) |

|

|

0.70 |

|

|

|

(0.11 |

) |

|

|

0.24 |

|

Net realized and unrealized gain (loss) on investments |

|

|

(11.17 |

) |

|

|

4.12 |

|

|

|

9.24 |

|

|

|

(7.74 |

) |

|

|

(1.80 |

) |

Total increase (decrease) from investment operations |

|

|

(10.96 |

) |

|

|

4.06 |

|

|

|

9.94 |

|

|

|

(7.85 |

) |

|

|

(1.56 |

) |

Less Distributions to Common Stockholders: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net investment income |

|

|

(2.18 |

) |

|

|

— |

|

|

|

— |

|

|

|

(0.59 |

) |

|

|

(1.28 |

) |

Net realized gain |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(2.68 |

) |

Return of capital |

|

|

(1.76 |

) |

|

|

(2.56 |

) |

|

|

(2.56 |

) |

|

|

(3.97 |

) |

|

|

(2.60 |

) |

Total distributions to common stockholders |

|

|

(3.94 |

) |

|

|

(2.56 |

) |

|

|

(2.56 |

) |

|

|

(4.56 |

) |

|

|

(6.56 |

) |

Capital Share Transactions: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Premiums less underwriting discounts and offering costs on issuance of common shares |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(3.72 |

)(4) |

Net Asset Value, end of fiscal year |

|

$ |

39.85 |

|

|

$ |

54.75 |

|

|

$ |

53.25 |

|

|

$ |

45.87 |

|

|

$ |

58.28 |

|

Per common share fair value, end of fiscal year |

|

$ |

31.97 |

|

|

$ |

42.53 |

|

|

$ |

45.02 |

|

|

$ |

35.74 |

|

|

$ |

50.72 |

|

Total Investment Return Based on Fair Value (5) |

|

|

(16.38 |

)% |

|

|

0.34 |

% |

|

|

33.40 |

% |

|

|

(19.52 |

)% |

|

|

(12.23 |

)% |

Supplemental Data and Ratios |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net assets applicable to common stockholders, end of fiscal year (000’s) |

|

$ |

103,682 |

|

|

$ |

142,434 |

|

|

$ |

138,537 |

|

|

$ |

119,348 |

|

|

$ |

151,639 |

|

Ratio of expenses to average net assets after waiver (6) |

|

|

4.15 |

% |

|

|

2.88 |

% |

|

|

2.25 |

% |

|

|

1.99 |

% |

|

|

2.39 |

% |

Ratio of net investment income (loss) to average net assets before waiver |

|

|

0.10 |

% |

|

|

(0.46 |

)% |

|

|

0.95 |

% |

|

|

0.92 |

% |

|

|

2.26 |

% |

Ratio of net investment income (loss) to average net assets after waiver |

|

|

0.44 |

% |

|

|

(0.12 |

)% |

|

|

1.29 |

% |

|

|

1.10 |

% |

|

|

2.26 |

% |

Portfolio turnover rate |

|

|

251.22 |

% |

|

|

124.56 |

% |

|

|

125.80 |

% |

|

|

71.35 |

% |

|

|

59.32 |

% |

Total borrowings outstanding (in thousands) |

|

$ |

36,810 |

|

|

$ |

41,410 |

|

|

$ |

56,410 |

|

|

$ |

18,310 |

|

|

$ |

— |

|

Asset coverage, per $1,000 of indebtedness (7) |

|

$ |

3,817 |

|

|

$ |

4,440 |

|

|

$ |

3,456 |

|

|

$ |

7,518 |

|

|

$ |

— |

|

|

(1)

|

Per share data adjusted for 1:4 reverse stock split completed as of June 12, 2020.

|

|

(2)

|

Information presented relates to a share of common stock outstanding for the entire period.

|

|

(3)

|

Represents the share impact related to a rights offering, which was completed on March 22, 2018.

|

|

(4)

|

Represents the share impact related to a rights offering, which was completed on July 18, 2019.

|

|

(5)

|

The calculation assumes reinvestment of dividends at actual prices pursuant to the Fund’s dividend reinvestment plan. Total investment return does not reflect brokerage commissions.

|

|

(6)

|

The ratio of expenses to average net assets before waiver was 4.49%, 3.22%, 2.59%, 2.16%, and 2.39% for the fiscal years ended November 30, 2023, 2022, 2021, 2020, and 2019, respectively.

|

|

(7)

|

Calculated by subtracting the Fund’s total liabilities (not including borrowings) from the Fund’s total assets and dividing by the total borrowings.

|

See Accompanying Notes to the Financial Statements.

15

NXG NextGen Infrastructure Income Fund

Notes to Financial Statements

November 30, 2023 |

1. Organization

NXG NextGen Infrastructure Income Fund (formerly, The Cushing® NextGen Infrastructure Income Fund) (the “Fund”) was formed as a Delaware statutory trust on November 16, 2010, and is registered as a diversified, closed-end management investment company under the Investment Company Act of 1940, as amended (the “1940 Act”). The Fund is managed by Cushing® Asset Management, LP, d/b/a NXG Investment Management (the “Adviser”). The Fund’s investment objective is to seek a high total return with an emphasis on current income. The Fund commenced operations on September 25, 2012. The Fund’s common shares are listed on the New York Stock Exchange under the symbol “NXG.”

2. Significant Accounting Policies

A. Use of Estimates

The following is a summary of significant accounting policies, consistently followed by the Fund in preparation of the financial statements. The Fund is considered an investment company and accordingly, follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board Accounting Standard Codification Topic 946, Financial Services - Investment Companies, which is part of U.S. Generally Accepted Accounting Principles (“U.S. GAAP”).

The preparation of financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amount of assets and liabilities, recognition of distribution income and disclosure of contingent assets and liabilities at the date of the financial statements. Actual results could differ from those estimates.

The Board of Trustees has designated the Adviser as the “valuation designee” for the Fund pursuant to Rule 2a-5 under the 1940 Act. The valuation designee is responsible for making fair value determinations pursuant to valuation policies and procedures adopted by the Adviser and the Fund (the “Valuation Policy”). A committee of voting members comprised of senior personnel of the Adviser considers various pricing issues and establishes fair valuations of portfolio securities and other instruments held by the Fund in accordance with the Valuation Policy (the “Valuation Committee”). The Adviser as valuation designee is subject to monitoring and oversight by the Board of Trustees. As a general principle, the fair value of a portfolio instrument is the amount that an owner might reasonably expect to receive upon the instrument’s current sale. A range of factors and analysis may be considered when determining fair value, including relevant market data, interest rates, credit considerations and/or issuer specific news. The Valuation Committee may consult with and receive input from third parties and will utilize a variety of market data including yields or prices of investments of comparable quality, type of issue, coupon, maturity, rating, indications of value from security dealers, evaluations of anticipated cash flows or collateral, spread over U.S. Treasury obligations, and other information and analysis. In addition, the Valuation Committee may consider valuations provided by valuation firms retained to assist in the valuation of certain of the Fund’s investments. Fair valuation involves subjective judgments. While the Fund’s use of fair valuation is intended to result in calculation of net asset value that fairly reflects values of the Fund’s portfolio securities as of the time of pricing, the Fund cannot guarantee that any fair valuation will, in fact, approximate the amount the Fund would actually realize upon the sale of the securities in question. It is possible that the fair value determined for a portfolio instrument may be materially different from the value that could be realized upon the sale of that instrument.

16

B. Investment Valuation

The valuation designee uses the following valuation methods to determine fair value as either fair value for investments for which market quotations are available, or if not available, the fair value, as determined in good faith pursuant to the Valuation Policy. The valuation of the portfolio securities of the Fund currently includes the following processes:

| |

(i)

|

The market value of each security listed or traded on any recognized securities exchange or automated quotation system will be the last reported sale price at the relevant valuation date on the composite tape or on the principal exchange on which such security is traded except those listed on the NASDAQ Global Market®, NASDAQ Global Select Market® and the NASDAQ Capital Market® exchanges (collectively, “NASDAQ”). Securities traded on NASDAQ will be valued at the NASDAQ Official Closing Price (“NOCP”). If no sale is reported on that date, the security will be valued at the last reported bid price. If the Valuation Committee (the “Committee”) determines that price is not representative of the actual market price, the Committee may determine the fair value of the security.

|

| |

(ii)

|

Securities not traded on a U.S. exchange or NASDAQ and foreign securities that are traded on foreign exchanges whose operations are similar to the U.S. over-the-counter market will be valued at prices supplied by a pricing service. If the Committee determines that price is not representative of the actual market price, the Committee may determine the fair value of the security.

|

| |

(iii)

|

Debt securities will be valued based on evaluated mean prices by an outside pricing service that employs a pricing model that takes into account bids, yield spreads, and/or other market data and specific security characteristics (e.g., credit quality, maturity and coupon rate). If a price cannot be obtained from pricing services, quotes from market makers or brokers may be used. When possible, more than one market maker or broker should be utilized and the mean of bid and ask prices should be used.

|

| |

(iv)

|

Private Placements in Public Entities (“PIPES”) will be valued using the price of the publicly traded common stock as a baseline, deducting the discount realized on the original purchase and amortizing the difference over the restricted period.

|

| |

(v)

|

Listed options on debt or equity securities are valued at the last sale price or, if there are no trades for the day, the mean of the closing bid price and ask price. Unlisted options on debt or equity securities are valued based upon their composite bid prices if held long, or their composite ask prices if held short. Futures are valued at the settlement price. Premiums for the sale of options written by an investment company registered under the 1940 Act (a “Registered Fund”) Fund will be included in the assets of such Registered Fund, and the market value of such options will be included as a liability.

|

| |

(vi)

|

For valuation purposes, quotations of foreign portfolio securities, other assets and liabilities and forward contracts stated in foreign currency are as of the close of regular trading on the Exchange each day the Exchange is open for trading (or earlier as may be specified by the Registered Fund) and translated into U.S. dollar equivalents at the current prevailing market rates as quoted by a pricing service.

|

| |

(vii)

|

Foreign securities are valued using “fair value factors”. Fair value factors consider daily trade activity and price changes for depositary receipts, exchange-traded funds, index futures, foreign currency exchange activity, or other relevant market data.

|

| |

(viii)

|

Over-the-counter options on foreign securities and currencies are fair valued by obtaining the “last available bid” from a single dealer that is either the writer or purchaser of the option.

|

| |

(ix)

|

Swaps will be valued using market-based prices provided by pricing services or broker-dealer bid counterparty quotations.

|

17

| |

(x)

|

Whenever trading in a listed security held in a portfolio is temporarily suspended, halted or delisted from an exchange, the security may be priced using the last closing price for a period of up to 5 business days. The Committee will continue to monitor the security during this period and, if there is a belief that the last closing price does not reflect the fair value of such security, then the value of such security will be determined by the Committee based on factors the Committee deems relevant. Whenever any such valuation determination is made, the Committee will monitor the market and other sources of information available to it in order to ascertain whether any change in circumstance would suggest a change in the value so determined.

|

The Fund may engage in short sale transactions. For financial statement purposes, an amount equal to the settlement amount, if any, is included in the Statement of Assets and Liabilities as a liability. The amount of the liability is subsequently marked-to-market to reflect the fair value of the short positions. Subsequent fluctuations in market prices of securities sold short may require purchasing the securities at prices which may differ from the fair value reflected on the Statement of Assets and Liabilities. When the Fund sells a security short, it must borrow the security sold short and deliver it to the broker-dealer through which it made the short sale. A gain, limited to the price at which the Fund sold the security short, or a loss, unlimited in size, will be recognized under the termination of a short sale. The Fund is also subject to the risk that it may be unable to reacquire a security to terminate a short position except at a price substantially more than the last quoted price. The Fund is liable for any distributions and dividends (collectively referred to as “Distributions”) paid on securities sold short and such amounts, if any, would be reflected as Distribution expense in the Statement of Operations. The Fund’s obligation to replace the borrowed security will be secured by collateral deposited with the broker-dealer. The Fund also will be required to segregate similar collateral to the extent, if any, necessary so that the value of both collateral amounts in the aggregate is at all times equal to at least 100% of the current fair value of the securities sold short.

C. Security Transactions, Investment Income and Expenses

Security transactions are accounted for on the date the securities are purchased or sold (trade date). Realized gains and losses are reported on a high cost basis. Interest income is recognized on an accrual basis, including amortization of premiums and accretion of discounts. Distributions are recorded on the ex- dividend date. Distributions received from the Fund’s investments in master limited partnerships (“MLPs”) and real estate investment trusts (“REITs”) generally are comprised of ordinary income, capital gains and return of capital. The Fund records investment income on the ex-date of the distributions. For financial statement purposes, the Fund uses return of capital and income estimates to allocate the distribution income received. Such estimates are based on historical information available from each MLP and REIT and other industry sources. These estimates may subsequently be revised based on information received from the MLPs and REITs after their tax reporting periods are concluded, as the actual character of these distributions is not known until after the fiscal year end of the Fund.

The Fund estimates the allocation of investment income and return of capital for the distributions received from its portfolio investments within the Statement of Operations. For the fiscal year ended November 30, 2023, the Fund has estimated approximately 53% of the distributions from its portfolio investments to be return of capital.

Expenses are recorded on an accrual basis.

D. Distributions to Shareholders

The Fund’s distributions may include a return of capital to shareholders to the extent that distributions are in excess of the Fund’s net investment income and net capital gains, determined in accordance with U.S. federal income tax regulations. Distributions that are treated for U.S. federal income tax purposes as a return of capital will reduce each shareholder’s basis in his or her shares and, to the extent the return of capital exceeds such basis, will be treated as a gain to the shareholder from a sale of shares. Returns of shareholder capital may have the effect of reducing the Fund’s assets and increasing the Fund’s expense ratio.

18

For the fiscal year ended November 30, 2022, the Fund’s distributions were expected to be 100%, or $6,656,226, return of capital. For the fiscal year ended November 30, 2023, the Fund’s distributions were expected to be 55%, or $5,658,992, ordinary income, and 45%, or $4,582,396, return of capital. The final character of distributions paid for the fiscal year ended November 30, 2023 will be determined in early 2024.

E. Federal Income Taxation

The Fund intends to qualify each year for special tax treatment afforded to a regulated investment company (“RIC”) under Subchapter M of the Internal Revenue Code of 1986, as amended (“IRC”). In order to qualify as a RIC, the Fund must, among other things, satisfy income, asset diversification and distribution requirements. As long as it so qualifies, the Fund will not be subject to U.S. federal income tax to the extent that it distributes annually its investment company taxable income (which includes ordinary income and the excess of net short- term capital gain over net long-term capital loss) and its “net capital gain” (i.e., the excess of net long-term capital gain over net short-term capital loss). The Fund intends to distribute at least annually substantially all of such income and gain. If the Fund retains any investment company taxable income or net capital gain, it will be subject to U.S. federal income tax on the retained amount at regular corporate tax rates. In addition, if the Fund fails to qualify as a RIC for any taxable year, it will be subject to U.S. federal income tax on all of its income and gains at regular corporate tax rates.

The Fund recognizes in the financial statements the impact of a tax position, if that position is more-likely- than-not to be sustained on examination by the taxing authorities, based on the technical merits of the position. Tax benefits resulting from such a position are measured as the amount that has a greater than fifty percent likelihood on a cumulative basis to be sustained on examination.

F. Cash and Cash Equivalents

The Fund considers all highly liquid investments purchased with initial maturity equal to or less than three months to be cash equivalents.

G. Cash Flow Information

The Fund makes distributions from investments, which include the amount received as cash distributions from MLPs, common stock dividends and interest payments. These activities are reported in the Statement of Changes in Net Assets, and additional information on cash receipts and payments is presented in the Statement of Cash Flows.

H. Indemnification

Under the Fund’s organizational documents, its officers and trustees are indemnified against certain liabilities arising out of the performance of their duties to the Fund. In addition, in the normal course of business, the Fund may enter into contracts that provide general indemnification to other parties. The Fund’s maximum exposure under such indemnification arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet occurred and may not occur. However, the Fund has not had prior claims or losses pursuant to these contracts and expects the risk of loss to be remote.

I. Derivative Financial Instruments

The Fund provides disclosure regarding derivatives and hedging activity to allow investors to understand how and why the Fund uses derivatives, how derivatives are accounted for, and how derivative instruments affect the Fund’s results of operations and financial position.

The Fund occasionally purchases and sells (“writes”) put and call equity options as a source of potential protection against a broad market decline. A purchaser of a put option has the right, but not the obligation, to sell the underlying instrument at an agreed upon price (“strike price”) to the option seller. A purchaser of a call option has the right, but not the obligation, to purchase the underlying instrument at the strike price from the option seller. Options are settled for cash.

19

Purchased Options — Premiums paid by the Fund for purchased options are included in the Statement of Assets and Liabilities as an investment. The option is adjusted daily to reflect the fair value of the option and any change in fair value is recorded as unrealized appreciation or depreciation of investments. If the option is allowed to expire, the Fund will lose the entire premium paid and record a realized loss for the premium amount. Premiums paid for purchased options which are exercised or closed are added to the amounts paid or offset against the proceeds on the underlying investment transaction to determine the realized gain/loss or cost basis of the security.

Written Options — Premiums received by the Fund for written options are included in the Statement of Assets and Liabilities. The amount of the liability is adjusted daily to reflect the fair value of the written option and any change in fair value is recorded as unrealized appreciation or depreciation of investments. Premiums received from written options that expire are treated as realized gains. The Fund records a realized gain or loss on written options based on whether the cost of the closing transaction exceeds the premium received. If a call option is exercised by the option buyer, the premium received by the Fund is added to the proceeds from the sale of the underlying security to the option buyer and compared to the cost of the closing transaction to determine whether there has been a realized gain or loss. If a put option is exercised by an option buyer, the premium received by the option seller reduces the cost basis of the purchased security.

Written uncovered call options subject the Fund to unlimited risk of loss. Written covered call options limit the upside potential of a security above the strike price. Put options written subject the Fund to risk of loss if the value of the security declines below the exercise price minus the put premium.

The Fund is not subject to credit risk on written options as the counterparty has already performed its obligation by paying the premium at the inception of the contract.

The Fund has adopted the disclosure provisions of Financial Accounting Standards Board (“FASB”) Accounting Standard Codification 815, Derivatives and Hedging (“ASC 815”). ASC 815 requires enhanced disclosures about the Fund’s use of and accounting for derivative instruments and the effect of derivative instruments on the Fund’s results of operations and financial position. Tabular disclosure regarding derivative fair value and gain/ loss by contract type (e.g., interest rate contracts, foreign exchange contracts, credit contracts, etc.) is required and derivatives accounted for as hedging instruments under ASC 815 must be disclosed separately from those that do not qualify for hedge accounting. Even though the Fund may use derivatives in an attempt to achieve an economic hedge, the Fund’s derivatives are not accounted for as hedging instruments under ASC 815 because investment companies account for their derivatives at fair value and record any changes in fair value in current period earnings.

There were no transactions in purchased options during the fiscal year ended November 30, 2023.

The average monthly fair value of written options during the fiscal year ended November 30, 2023 was $27,021.

The effect of derivative instruments on the Statement of Operations for the fiscal year ended November 30, 2023:

Liability Derivatives |

Risk Exposure Category |

|

Statement of Asset and Liabilities Location |