U.S. Securities and

Exchange Commission

Washington, DC 20549

Notice of Exempt Solicitation

Submitted Pursuant

to Rule 14a-6(g)

1. Name of the Registrant: Magellan

Midstream Partners, L.P.

2. Name of person relying on exemption: Energy

Income Partners, LLC.

3. Address of person relying on exemption:

10 Wright Street, Westport, Connecticut 06880.

4. Written materials are submitted

pursuant to Rule 14a-6(g)(1):

WESTPORT, Conn., September 5, 2023, 2023 /PRNewswire/ -- Energy

Income Partners, LLC (EIP) the fourth largest and long-time shareholder in Magellan Midstream Partners, L.P. (“Magellan”)

believes that Magellan’s August 29, 2023 Presentation amounts to a series of scare tactics that present Magellan unitholders

with a false choice: merge with ONEOK or else. EIP’s decision to vote against the merger is based on the financials presented by

management that show definitively that Magellan is better off as a stand-alone company, and we urge our fellow unitholders to vote “no”.

EIP has released a new presentation on its website votemmp.com that

addresses Magellan’s August 29, 2023 presentation which further outlines the points below.

EIP calls out Magellan Board and Management for doubling down on Magellan’s

poor prospects as a standalone company formed as a partnership due to anticipated weakness in petroleum demand. Management’s assertion

that its poor prospects justify this merger belies their assertions in their own 10-K released February of 2023 and their Investor

Day presentation on April 2022. EIP observes that Magellan was making a public disclosure of its positive prospects AT THE SAME TIME

that it was negotiating a deal that it now says is intended to stave off these dangers.

EIP shows in its presentation that Magellan has tripled its earnings

over the last 15 years during which time refined petroleum demand has declined nearly 7%, disproving current management’s entire

thesis regarding the impact declining petroleum demand may have on per share earnings growth.

EIP calls out Magellan on warning unitholders that the price for units

and the multiples at which they trade could decline, while ignoring the tax savings that would result if the transaction were rejected.

EIP calls out Magellan for failing to conduct a fulsome sales process.

If this transaction is so important to avoid the secular risks that Magellan warns about, why did Magellan only speak to one counterparty

and why didn’t it conduct a broad process, and determine what other alternatives were available? A passive check following the announcement

of a transaction is hardly the way to maximize value if a sale is warranted. The current narrative that the ONEOK transaction is the solution

to the secular risks facing Magellan has all the appearance of an after-the-fact rationalization rather than a well-considered motivation.

EIP calls out Magellan’s Board for failing to engage with unitholders

including EIP to discuss alternatives including conversion to a C-Corporation or to provide analysis other than a naked conclusion that

such a transaction would be “complex” or “uneconomic.”

EIP calls out Magellan for mischaracterizing or misunderstanding EIP’s

tax analysis. Their Presentation contests the truism that investors benefit from the deferral of taxes because of the time value of money.

EIP has never disputed the existence of an existing tax liability only that its present value is far less than the $2.7 billion that would

be due upon completion of this merger.

EIP calls out Management for not disputing the poor growth prospects

for ONEOK evidenced by ONEOK’s own forecast in the S-4 of less than a 5% return on its growth capital over the next five years.

EIP has a greater belief in Magellan’s prospects than both Magellan’s

Board and Management. Based on financial analysis of the information provided by ONEOK and Magellan management, it is clear that staying

a stand-alone company with an appropriate analysis of alternatives such as a tax-efficient conversion to a C-Corp is better for unitholders

than the proposed merger. Magellan’s own 10-K, from February of 2023, highlighted its opportunity as a standalone company to

deploy capital to improve the value of its common units. Magellan is a top-tier company with excellent assets that generate stable fee-based

inflation hedged income that has consistently over time supported steady growing earnings.

About Energy Income Partners, LLC

Founded in 2003, Energy Income Partners (EIP), LLC is an asset manager

based in Westport, CT focusing on energy infrastructure. EIP's team has significant experience in the energy, pipeline and utility industries.

As of July 31, 2023 EIP has $5.2 billion in assets under management. www.eipinvestments.com

Disclosures:

This is not a solicitation of authority to vote your proxy. Please

DO NOT send us your proxy card. Energy Income Partners, LLC is not able to vote your proxies, nor does this communication contemplate

such an event. EIP urges shareholders to vote against the proposed merger or not vote which will have the same effect as voting no.

The views expressed are those of Energy Income Partners, LLC as of

the date referenced and are subject to change at any time based on market or other conditions. These views are not intended to be a forecast

of future events or a guarantee of future results. These views may not be relied upon as investment advice. The information provided in

this material should not be considered a recommendation to buy or sell any of the securities mentioned. It should not be assumed that

investments in such securities have been or will be profitable. This piece is for informational purposes and should not be construed as

a research report.

Energy Income Partners, LLC conducted its own analysis based upon information

available to it at the time of the analysis which may change at any time without notice and does not make any warranty as to the accuracy

or completeness of any analysis, data point, assumption or opinion presented herein.

Distribution of this letter, regardless of the means or format of its

delivery, does not constitute the provision of tax advice by EIP, nor should any general analysis piece be relied upon for the formulation

of any targeted tax strategy. For more information regarding specific personal or corporate tax matters, including, but not limited to,

personal tax implications relating to specific portfolio transactions, please consult a qualified tax professional.

CONTACT: Jayme Martino, Investor Relations, 203-349-8232

©2023 ENERGY INCOME PARTNERS 1 U.S. Securities and Exchange Commission Washington, DC 20549 Notice of Exempt Solicitation Submitted Pursuant to Rule 14a - 6(g) 1. Name of the Registrant : Magellan Midstream Partners, L.P. 2. Name of person relying on exemption : Energy Income Partners, LLC. 3. Address of person relying on exemption : 10 Wright Street, Westport, Connecticut 06880. 4. Written materials are submitted pursuant to Rule 14a - 6(g)(1) :

EIP Overview of EIP’s Response to MMP August 29th Presentation September 5, 2023 ©2023 ENERGY INCOME PARTNERS

Overview of EIP’s Response to MMP August 29 th Presentation ©2023 ENERGY INCOME PARTNERS 3 • Magellan management seems to be doubling down on Magellan’s poor prospects as a stand - alone company formed as a partnership due to anticipated weakness in petroleum demand and higher tax liabilities for their limited partner unitholders yet offers no explanation of why this concern was not addressed by conducting a strategic sales process or pursuing its own tax - efficient C - Corp conversion. • Management’s dire predictions for the future of its business in the face of the energy transition directly contradict its own statements in last year’s MMP Investor Day presentation and its 2022 Annual Report on Form 10K. • EIP has a greater belief in Magellan’s prospects than both the Board and Management. Based on financial analysis of the information provided by management, EIP believes that staying a stand - alone company is better for unitholders than the proposed merger. • Magellan has high quality stable fee - based inflation hedged assets which has supported its long track record of superior growth in challenging business environments. Earnings per share have nearly tripled over the last 15 years, while U.S. petroleum demand declined ~7% and during which Magellan’s capital spending, as a percent of EBITDA, was the lowest of its peer group. Magellan unitholders should reject this proposed merger because the merger makes no strategic sense and provides a negative premium for unitholders.

Management Has No Confidence in the Future of the Company ©2023 ENERGY INCOME PARTNERS 4 Over the last year, Management has completely reversed its view of industry prospects and now agrees with bearish future petroleum demand forecasts by third parties, forecasts they had dismissed in the 2022 Annual Report (10K) and the 2022 Investor Day presentation. Management is committing a common error in equating per share earnings prospects with top line volumes. As shown in the below graph, petroleum demand in the US has declined about 7% since before the 2008 financial crisis, yet under prior management, Magellan earnings have nearly tripled. GFC = Global Financial Crisis LTM= Last twelve months BPD= Barrels per Day RTM= Rolling twelve months Source: Bloomberg, U.S. DOE EIA Weekly Petroleum Status Report, EIP

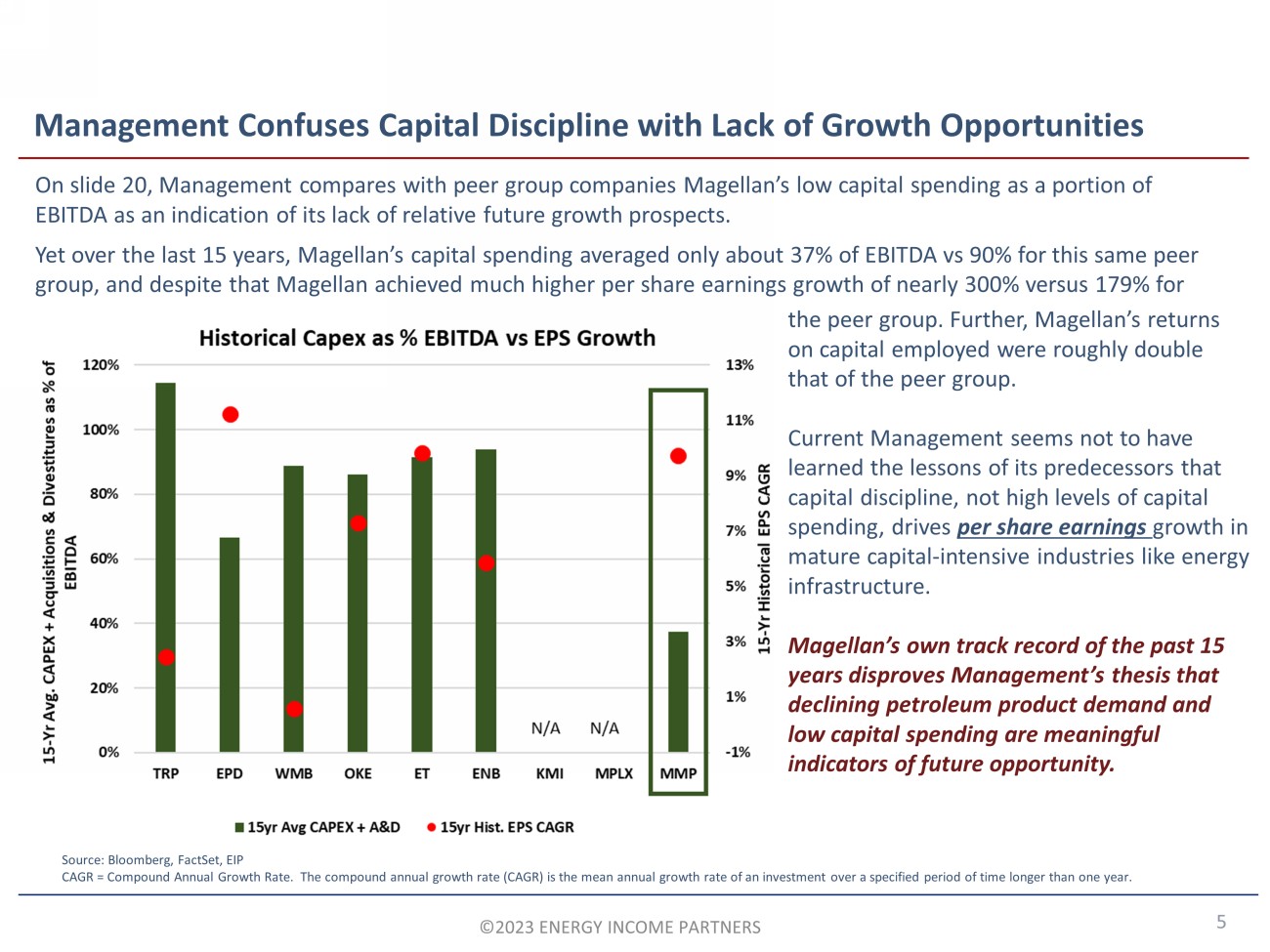

Management Confuses Capital Discipline with Lack of Growth Opportunities ©2023 ENERGY INCOME PARTNERS 5 On slide 20, Management compares with peer group companies Magellan’s low capital spending as a portion of EBITDA as an indication of its lack of relative future growth prospects. Yet o ver the last 15 years, Magellan’s capital spending averaged only about 37% of EBITDA vs 90% for this same peer group, and despite that Magellan achieved much higher per share earnings growth of nearly 300% versus 179% for Source: Bloomberg, FactSet, EIP CAGR = Compound Annual Growth Rate. The compound annual growth rate (CAGR) is the mean annual growth rate of an investment o ver a specified period of time longer than one year. the peer group. Further, Magellan’s returns on capital employed were roughly double that of the peer group. Current Management seems not to have learned the lessons of its predecessors that capital discipline, not high levels of capital spending, drives per share earnings growth in mature capital - intensive industries like energy infrastructure. Magellan’s own track record of the past 15 years disproves Management’s thesis that declining petroleum product demand and low capital spending are meaningful indicators of future opportunity.

©2023 ENERGY INCOME PARTNERS 6 Quotes from MMP 2022 Analyst Day “If you look at the next 10 years, there's very much a consensus that refined products demand, gasoline demand is going to be stable, and it may even increase a little bit, but it's going to be stable for the next 10 years.” “I think it's pretty clear that whatever is going to happen is likely to happen over a very long period of time, and in our opinion, at a much slower pace even than the most pessimistic curves that we've already shown you.” “We don't think we have to be exactly right nor do we have to have all of the answers to know that we're going to have a pretty bright future and have an opportunity to create a lot of value” “the really almost irreplaceable nature of many of our assets on top of that, and it's a very powerful economic proposition that we have. We think that's underappreciated. We've got 35 years.” “Whatever happens with EVs, whatever the adoption curve is, it will be slower in our market area. We may not be right about the United States, it will be slower in our market area because of demographics and those demographics are not changing very fast.” Re: third party modeling & forecasts: • “There's a lot of curves with sort of downward sloping. Hopefully, they read the transcript to go with it, right?” • “just pick the pessimistic case and we still have a very optimistic story when you look at the actual economics of what we think we're going to be able to do” • “When we do our own modeling, we consider others. And we put it all together, we think we're going to have a really healthy business for a very long time.” Quotes from MMP 2023 Presentation “Refined products and crude oil sectors face energy transition and re - contracting risks. ” “Standalone MMP faces long - term secular risks.” “Growth through re - investment of excess cash flow is challenged. Fewer opportunities in mature refined products sector and over - built crude oil pipeline infrastructure.” “Standalone company exposes unitholders to adverse secular risks and a diminishing solution set.” “Core refined products business is mature with reduced future growth opportunities” “Leading industry sources (e.g., Wood Mackenzie, S&P) expect U.S. gasoline demand will decline by >55% from 2022 - 2050” VS What is Motivating Management’s Change in Outlook?

©2023 ENERGY INCOME PARTNERS 7 Quotes from MMP 2022 Annual Report on SEC From 10K “We will remain an important part of a successful energy transition. The services we provide are vital to ensuring our communities and economies function while the U.S. and the world pursue a transition from fossil fuels. Supported by industry and government forecasts, we believe demand for the fuels we deliver will remain steady for the foreseeable future and essential for many decades and likely beyond.” “World events over the past year have reinforced the criticality of the energy industry to our country and the world. We are well positioned to responsibly provide the essential fuels such as gasoline, diesel fuel and jet fuel that our communities and economy rely on daily.” “Dynamic energy markets provide both challenges and opportunities. We own the longest refined pipeline in the country and can access nearly 50% of the nation’s refining capacity. During 2022 we shipped record refined products volumes as customers took advantage of our network’s extensive connectivity to overcome various supply disruptions in the markets we serve.” What is Motivating Management’s Change in Outlook?

©2023 ENERGY INCOME PARTNERS 8 Quotes from MMP 2022 Annual Report on SEC From 10K “We continue to pursue investment opportunities that meet our disciplined financial requirements. For example, we have completed a number of small bolt - on projects over the past year, including recent pipeline expansions to New Mexico and Colorado. Additionally, during 2022, we launched an expansion of our refined products pipeline to El Paso, Texas, which will connect more supply to growing markets in Texas, Arizona and Mexico and is supported by commitments from high - quality counterparties.” “While we expect to continue finding opportunities to invest in new projects, attractive opportunities have been more limited over the last few years. This more limited capital investment environment, along with the fact that we believe the value of our equity has not reflected the economic potential of our company, has allowed us to invest in ourselves by repurchasing equity.” “Through our equity repurchase program, we have reduced the number of our outstanding units by 11% over the last three years, providing meaningful growth in earnings and distributable cash flow on a per unit basis.” What is Motivating Management’s Change in Outlook?

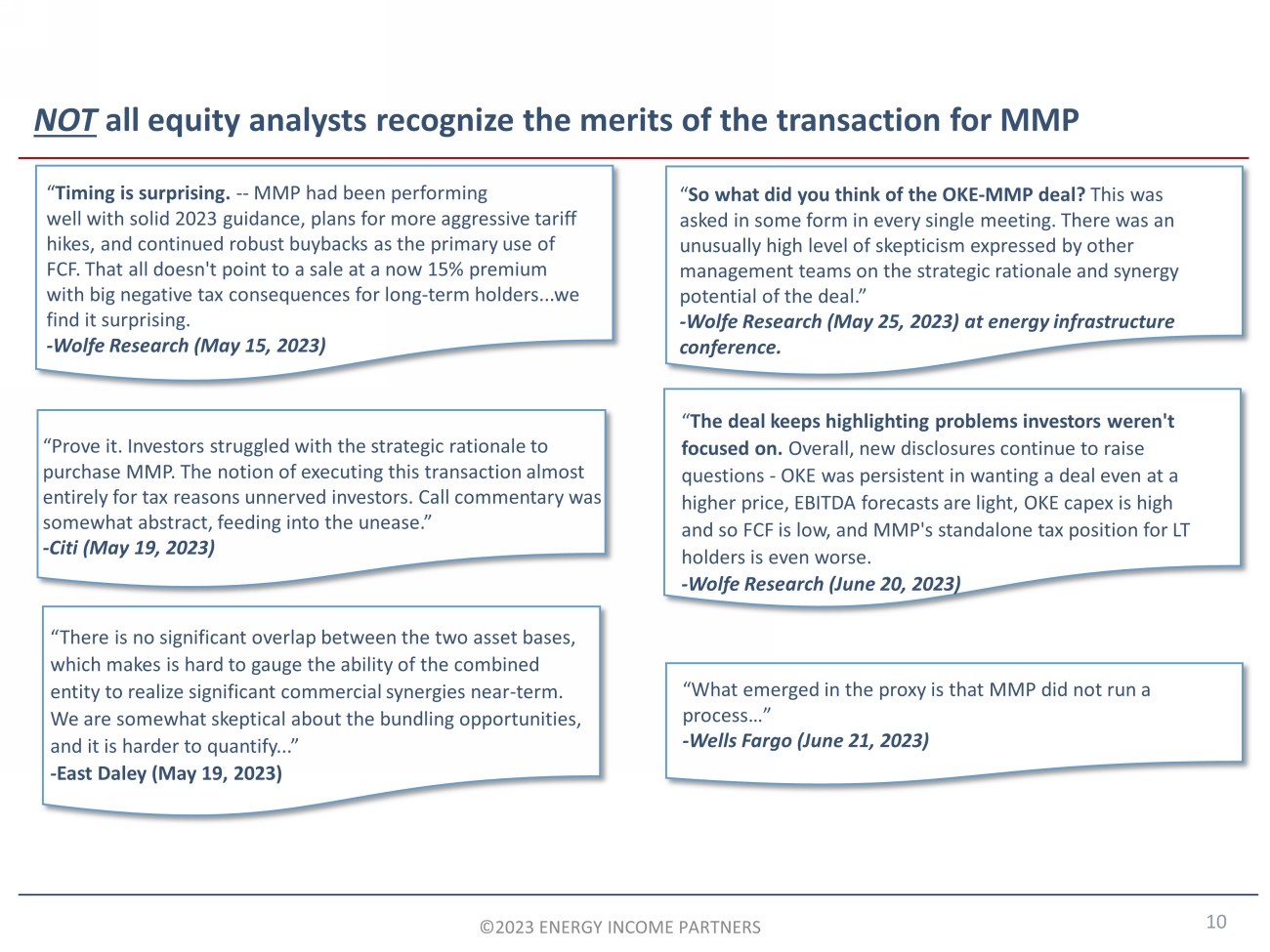

If Management decided selling out is the best option, why didn’t they run a proper sales process? ©2023 ENERGY INCOME PARTNERS 9 • Management gives no reason for its sudden reversal in its view of Magellan’s future business prospects. • However, once Management adopted this negative view, why didn’t they suspend discussions with ONEOK and pursue a full - blown strategic review conducted with the help of an investment bank and outside industry consultants and solicit bids from all potentially interested parties? • Instead, Management is using scare tactics and offering a false choice of a stand - alone company that remains a partnership for tax purposes versus a merger with ONEOK treated as a sale for tax purposes that triggers an immediate payment of a $2.7 billion deferred tax liability for unitholders. • While ONEOK and Magellan have made clear that without purchase treatment and the resulting cost - basis step up for ONEOK, ONEOK would not pursue the proposed merger, Magellan offers no evidence that they pursued a more tax - efficient option. • Moreover, Management has still not provided a complete analysis of the benefits of a stand - alone SEC. 351 conversion to a C - Corporation that would not trigger an up - front $2.7 billion payment and would cut unitholder tax payments dramatically by lowering the taxes due on this deferred tax liability from ordinary income rates to capital gains rates. “What emerged in the proxy is that MMP did not run a process…” - Wells Fargo (June 21, 2023)

NOT a ll equity a nalysts recognize the merits of the transaction for MMP ©2023 ENERGY INCOME PARTNERS 10 “What emerged in the proxy is that MMP did not run a process…” - Wells Fargo (June 21, 2023) “Prove it. Investors struggled with the strategic rationale to purchase MMP. The notion of executing this transaction almost entirely for tax reasons unnerved investors. Call commentary was somewhat abstract, feeding into the unease.” - Citi (May 19, 2023) “ The deal keeps highlighting problems investors weren't focused on. Overall, new disclosures continue to raise questions - OKE was persistent in wanting a deal even at a higher price, EBITDA forecasts are light, OKE capex is high and so FCF is low, and MMP's standalone tax position for LT holders is even worse. - Wolfe Research (June 20, 2023) “ Timing is surprising. -- MMP had been performing well with solid 2023 guidance, plans for more aggressive tariff hikes, and continued robust buybacks as the primary use of FCF. That all doesn't point to a sale at a now 15% premium with big negative tax consequences for long - term holders...we find it surprising. - Wolfe Research (May 15, 2023) “There is no significant overlap between the two asset bases, which makes is hard to gauge the ability of the combined entity to realize significant commercial synergies near - term. We are somewhat skeptical about the bundling opportunities, and it is harder to quantify...” - East Daley (May 19, 2023) “ So what did you think of the OKE - MMP deal? This was asked in some form in every single meeting. There was an unusually high level of skepticism expressed by other management teams on the strategic rationale and synergy potential of the deal.” - Wolfe Research (May 25, 2023) at energy infrastructure conference.

EIP Stands By its Analysis ©2023 ENERGY INCOME PARTNERS 11 • EIP stands by its financial analysis of the proposed synergies and growth projections for the combined entity as it is all based on financial data provided in the S - 4. • EIP’s analysis of the merger’s tax implications is based on Magellan’s disclosure from their June 2023 presentation and presentation from February 2, 2021 “Corporate Conversion Analysis”. • MMP mischaracterized or misunderstood EIP’s analysis of the tax deferral and payment due if the merger goes through: EIP has never said that taxes were not payable by the unitholders except for those that hold their shares until death. Rather, EIP made an attempt at quantifying the time value of the tax deferral using Magellan’s own guidance on share turnover by age cohort and a 10% cost of equity capital. • Magellan slide 38 adulterates EIP’s analysis by applying a 5 - year holding period rather than its own guidance on share turnover. • Magellan has repeatedly failed to quantify and present the benefits of a SEC. 351 C - Corp conversion on reducing the tax rate unitholders would pay on the existing $2.7 billion deferred liability by lowering the tax to capital gains rates from ordinary rates. Instead, it offers up adjectives against a conversion such as “complex” or “uneconomic” while advocating for triggering this liability this year, payable at ordinary income rates and eliminating the value of continuing to defer this payment. EIP’s objection to this merger is based primarily on its lack of strategic merit and the negative deal premium.

Taxes are Important, But They Are Not Primary Reason for No Vote ©2023 ENERGY INCOME PARTNERS 12 EIP’s tax liability is lower than the average MMP unitholder due to the younger holding period of the shares held in the funds and accounts it advises and sub - advises. EIP’s objection to this merger is based primarily on its lack of strategic merit and the inadequate deal premium under the current transaction structure. Source: EIP, Magellan’s June 2023 Tax Presentation

Questions Magellan Still Hasn’t Answered ©2023 ENERGY INCOME PARTNERS 13 • Why was there not a fulsome sales process? • Why has Magellan’s Board not responded to nor engaged in any way with EIP to address these concerns? • Where is a comprehensive financial analysis of the alternatives including the benefits of C - Corporation conversion (not just the costs at the corporate entity Management provided)? • Why merge with ONEOK - a company that standalone has a forecast return of only 5% on planned growth capital over the next 5 years? • Why can’t the ONEOK merger synergies be achieved commercially without a merger? EIP continues to believe the transaction should be rejected. VOTE “NO”

Disclosure ©2023 ENERGY INCOME PARTNERS 14 This is not a solicitation of authority to vote your proxy. Please DO NOT send us your proxy card. Energy Income Partners, LLC is not able to vote your proxies, nor does this communication contemplate such an event. The proponent urges shareholders to vote against the proposed merger or not vote which will have the same effect as voting no. The views expressed are those of Energy Income Partners, LLC as of the date referenced and are subject to change at any time based on market or other conditions. These views are not intended to be a forecast of future events or a guarantee of future results. These views may not be relied upon as investment advice. The information provided in this material should not be considered a recommendation to buy or sell any of the securities mentioned. It should not be assumed that investments in such securities have been or will be profitable. This piece is for informational purposes and should not be construed as a research report. Energy Income Partners, LLC conducted its own analysis based upon information available to it at the time of the analysis which may change at any time without notice and does not make any warranty as to the accuracy or completeness of any analysis, data point, assumption or opinion presented herein. Distribution of this letter, regardless of the means or format of its delivery, does not constitute the provision of tax advice by EIP, nor should any general analysis piece be relied upon for the formulation of any targeted tax strategy. For more information regarding specific personal or corporate tax matters, including, but not limited to, personal tax implications relating to specific portfolio transactions, please consult a qualified tax professional.

Magellan Midstream Partn... (NYSE:MMP)

Historical Stock Chart

From Apr 2024 to May 2024

Magellan Midstream Partn... (NYSE:MMP)

Historical Stock Chart

From May 2023 to May 2024