FYfalse00002029472024-03-31http://fasb.org/us-gaap/2023#CostsAndExpenseshttp://fasb.org/us-gaap/2023#CostsAndExpenses0000202947us-gaap:CustomerConcentrationRiskMember2022-01-012022-12-3100002029472021-12-310000202947cptp:LandImprovementsOnLeaseOrHeldForLeaseMember2023-12-310000202947us-gaap:SubsequentEventMember2024-01-242024-01-2400002029472023-06-300000202947cptp:MetroparkLtdMember2023-12-310000202947cptp:BAnkRIMembersrt:MinimumMemberus-gaap:LineOfCreditMember2021-03-012021-03-310000202947us-gaap:BuildingAndBuildingImprovementsMember2022-12-310000202947us-gaap:SubsequentEventMembercptp:MetroparkLtdMember2024-01-092024-01-090000202947us-gaap:CustomerConcentrationRiskMembercptp:LamarOutdoorAdvertisingLlcMember2023-01-012023-12-310000202947cptp:LamarLeaseMember2023-12-310000202947cptp:TripleNetLeaseMembersrt:MinimumMember2023-12-310000202947us-gaap:USTreasurySecuritiesMember2023-01-012023-12-310000202947cptp:ParcelsMember2022-01-012022-12-310000202947cptp:TerminalMembercptp:SaleOfPetroleumStorageFacilityAndRelatedAssetsMember2017-01-312017-01-310000202947cptp:SaleOfPetroleumSegmentMember2019-11-012019-11-300000202947cptp:PropertiesOnLeaseOrHeldForLeaseLandAndLandImprovementsMember2022-12-310000202947cptp:EnvironmentalIncidentNineteenNinetyFourMember2022-12-310000202947cptp:EnvironmentalIncidentNineteenNinetyFourMember2023-12-310000202947cptp:MetroparkLtdMember2020-06-300000202947cptp:LandImprovementsOnLeaseOrHeldForLeaseMember2022-12-3100002029472022-12-310000202947us-gaap:SubsequentEventMember2024-01-250000202947us-gaap:SubsequentEventMember2024-01-252024-01-250000202947us-gaap:SubsequentEventMembercptp:MetroparkLtdMember2024-01-090000202947srt:MaximumMembercptp:BAnkRIMemberus-gaap:SecuredOvernightFinancingRateSofrOvernightIndexSwapRateMemberus-gaap:LineOfCreditMember2023-01-012023-12-310000202947cptp:LamarLeaseMember2022-06-012023-05-310000202947cptp:PropertiesOnLeaseOrHeldForLeaseSteepleStreetPropertyMember2022-12-310000202947us-gaap:CustomerConcentrationRiskMembercptp:MetroparkLtdMember2022-01-012022-12-310000202947cptp:BAnkRIMembersrt:MinimumMemberus-gaap:LineOfCreditMemberus-gaap:FirstMortgageMember2021-03-012021-03-310000202947cptp:MetroparkLtdMember2022-01-012022-12-310000202947cptp:ParcelsMember2023-01-012023-12-310000202947us-gaap:BuildingAndBuildingImprovementsMember2023-12-310000202947cptp:ParcelsMember2022-10-012022-12-310000202947cptp:ParcelTwoMember2022-01-012022-12-310000202947us-gaap:CustomerConcentrationRiskMembercptp:LamarOutdoorAdvertisingLlcMember2022-01-012022-12-310000202947cptp:CityOfProvidenceMember2022-01-012022-12-310000202947cptp:BAnkRIMemberus-gaap:SecuredOvernightFinancingRateSofrOvernightIndexSwapRateMemberus-gaap:LineOfCreditMember2023-01-012023-12-310000202947cptp:SaleOfPetroleumSegmentMembercptp:TerminalMember2021-07-3100002029472022-01-012022-12-310000202947cptp:LamarLeaseMember2021-06-012022-05-310000202947us-gaap:CustomerConcentrationRiskMembercptp:HGITCenterPlaceMember2023-01-012023-12-3100002029472023-12-310000202947srt:MaximumMembercptp:BAnkRIMemberus-gaap:LineOfCreditMember2021-03-012021-03-310000202947cptp:SaleOfPetroleumSegmentMember2017-02-102017-02-100000202947cptp:PropertiesOnLeaseOrHeldForLeaseLandAndLandImprovementsMember2023-12-310000202947cptp:ParcelTwoMember2023-01-012023-12-310000202947us-gaap:CustomerConcentrationRiskMembercptp:OneSevenZeroOneRCSarasotaInvestLLCMember2022-01-012022-12-310000202947us-gaap:CustomerConcentrationRiskMembercptp:WaterplaceCondominiumsMember2022-01-012022-12-310000202947cptp:BAnkRIMemberus-gaap:LineOfCreditMember2021-03-012021-03-310000202947us-gaap:USTreasurySecuritiesMember2023-12-310000202947cptp:SaleOfPetroleumSegmentMember2023-01-012023-12-310000202947cptp:LamarLeaseMember2023-01-012023-12-3100002029472024-02-1600002029472023-01-012023-12-310000202947us-gaap:CustomerConcentrationRiskMembercptp:HGITCenterPlaceMember2022-01-012022-12-310000202947us-gaap:CustomerConcentrationRiskMembercptp:MetroparkLtdMember2023-01-012023-12-310000202947cptp:BAnkRIMemberus-gaap:LineOfCreditMember2021-03-310000202947us-gaap:CustomerConcentrationRiskMember2023-01-012023-12-310000202947srt:MaximumMember2023-01-012023-12-310000202947cptp:BAnkRIMemberus-gaap:LineOfCreditMember2023-01-012023-12-310000202947srt:MinimumMember2023-01-012023-12-310000202947srt:MaximumMembercptp:BAnkRIMemberus-gaap:LineOfCreditMemberus-gaap:FirstMortgageMember2021-03-012021-03-310000202947us-gaap:CustomerConcentrationRiskMembercptp:WaterplaceCondominiumsMember2023-01-012023-12-310000202947cptp:PropertiesOnLeaseOrHeldForLeaseSteepleStreetPropertyMember2023-12-310000202947us-gaap:CustomerConcentrationRiskMembercptp:OneSevenZeroOneRCSarasotaInvestLLCMember2023-01-012023-12-310000202947cptp:SaleOfPetroleumSegmentMember2022-01-012022-12-31cptp:Locationxbrli:purecptp:Parcelutr:sqftxbrli:sharescptp:LandLeasecptp:Billboard_Facecptp:Installmentiso4217:USDcptp:Subsidiary

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-K

|

|

|

☒ |

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2023

OR

|

|

|

☐ |

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 001-08499

CAPITAL PROPERTIES, INC.

(Exact name of registrant as specified in its charter)

|

|

|

Rhode Island |

|

05-0386287 |

(State or other jurisdiction of |

|

(IRS Employer |

incorporation or organization) |

|

identification No.) |

|

|

|

5 Steeple Street, Unit 303 |

|

|

Providence, Rhode Island |

|

02903 |

(Address of principal executive offices) |

|

(Zip Code) |

Registrant’s telephone number, including area code: (401) 435-7171

Securities registered pursuant to Section 12 (g) of the Act:

|

|

|

Title of each class |

Trading Symbol(s) |

Name of each exchange on which registered |

Class A Common Stock, $.01 par value |

CPTP |

OTCQX |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files.) Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of the "large accelerated filer," "accelerated filer," "smaller reporting company" and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

|

|

|

|

|

|

Large Accelerated Filer |

☐ |

Accelerated Filer |

☐ |

|

Emerging Growth Company |

☐ |

Non-Accelerated Filer |

☐ |

Smaller reporting company |

☒ |

|

|

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404 (b) of the Sarbanes-Oxley Act (15 U.S.C.7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of June 30, 2023, the aggregate market value of the Class A voting stock held by non-affiliates of the Company was $23,000,000 which excludes voting stock held by directors, executive officers and holders of 5% or more of the voting power of the Company’s common stock (without conceding that such persons are “affiliates” of the Company for purposes of federal securities laws). The Company has no outstanding non-voting common equity.

As of February 16, 2024, the Company had 6,599,912 shares of Class A Common Stock outstanding.

|

|

|

|

|

|

Auditor Firm Id: |

577 |

Auditor Name: |

Stowe & Degon, LLC |

Auditor Location: |

Westborough, MA, USA |

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Company’s Proxy Statement for the 2024 Annual Meeting of Shareholders to be held on April 24, 2024, are incorporated by reference into Part III of this Form 10-K.

CAPITAL PROPERTIES, INC.

FORM 10-K

FOR THE YEAR ENDED DECEMBER 31, 2023

TABLE OF CONTENTS

PART I

FORWARD-LOOKING STATEMENTS

Certain portions of this report, and particularly the Management’s Discussion and Analysis of Financial Condition and Results of Operations, contain forward-looking statements within the meaning of Sections 27A of the Securities Act of 1933, as amended, and Sections 21E of the Securities Exchange Act of 1934, as amended, which represent the Company’s expectations or beliefs concerning future events. The Company cautions that these statements are further qualified by important factors that could cause actual results to differ materially from those in the forward-looking statements, including, without limitation, the following: the ability of the Company to generate adequate amounts of cash; the collectability of the excess of straight-line over contractual rent when due over the terms of the long-term leases; the commencement of additional long-term land leases; changes in economic conditions that may affect either the current or future development on the Company’s parcels; cyber-penetrations; the long-term impact of the COVID-19 pandemic on the economy, parking operations, and the Company’s financial performance, and exposure to remediation and other costs associated with its former ownership of a petroleum storage facility. The Company does not undertake the obligation to update forward-looking statements in response to new information, future events or otherwise.

Item 1. Business

Organizational History

The Company was organized as a business corporation under the laws of Rhode Island in 1983 as Providence and Worcester Company and is the successor by merger in 1983 to a corporation also named Providence and Worcester Company which was organized under the laws of Delaware in 1979. In 1984, the Company’s name was changed to Capital Properties, Inc.

Business:

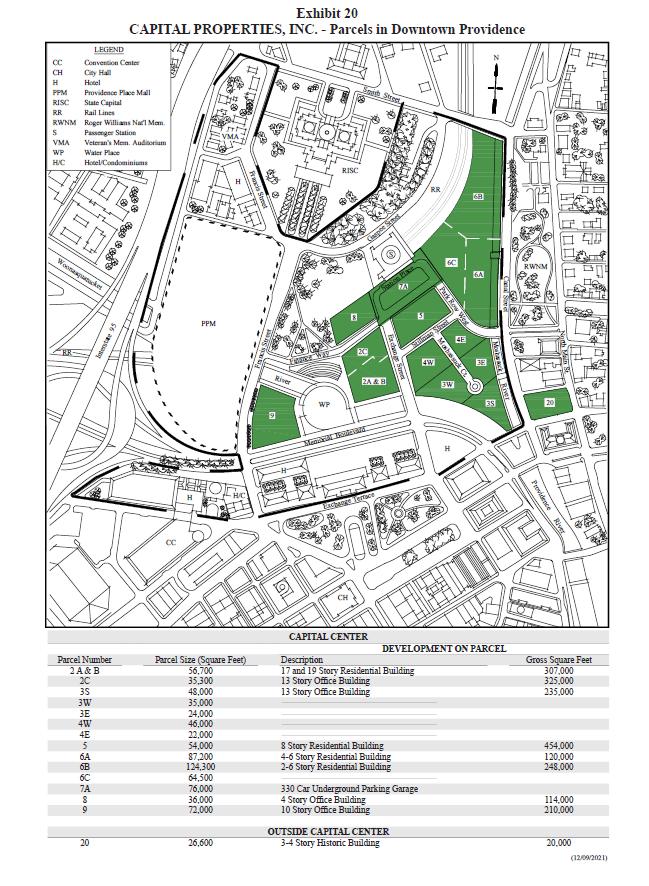

The Company’s principal business is the leasing of Company-owned land in Capital Center (“Capital Center”) and property adjacent to Capital Center (Parcel 20) in downtown Providence, Rhode Island under long-term ground leases with terms of 99 years or more.* (Hereinafter, the land in Capital Center and Parcel 20 are referred to as parcels within the “Capital Center Area”). The Company owns approximately 18 acres in Capital Center consisting of 13 individual parcels. Capital Center (approximately 77 acres of land) is the result of a development project undertaken by the State of Rhode Island, the City of Providence, the National Railroad Passenger Corporation (“Amtrak”) and the Company during the 1980’s in which two rivers, the Moshassuck and the Woonasquatucket, were moved, Amtrak’s Northeast Corridor rail line was relocated, a new Amtrak/commuter railroad station was constructed and significant public improvements were made to improve pedestrian and vehicular traffic in the area. The Company has not acted, and does not intend to act, as a developer with respect to any Company-owned parcels.

Under the Company’s standard Ground Leases, the tenant is responsible for all property related operating expenses, such as real estate taxes, maintenance and insurance as well as all costs associated with the development and construction of the related improvements. Each Ground Lease contains provisions permitting the tenant to develop the parcel under certain terms and conditions and provides for periodic rent increases based on either a specific percentage, consumer price index (“CPI”), appraisal or combination thereof and sometimes includes percentage rent participation (contingent rent). The Ground Leases also provide that the tenants are responsible for insuring the Company against various hazards and events as well as indemnifying the Company with respect to all of the tenant’s activities on the land. The Ground Leases contain other terms and conditions customary to such instruments.

While seeking developers, the Company also leases Parcels 3E, 3W, 4E, 4W and a portion of Parcel 20 in the Capital Center Area for public parking purposes to Metropark, Ltd.

Parcel 20

Parcel 20 consists of a parcel of land adjacent to the Capital Center, part of which is undeveloped and part of which contains a three/four-story 20,000 square foot building (the “Steeple Street Building”).

On January 25, 2024, the Company entered into a long-term ground lease of Parcel 20. Under the terms of the lease, tenant's possession will not occur until such time as the tenant has received all necessary approvals for construction of not less than 100,000 square feet of mixed use improvements. Prior to transfer of possession, no rent is being paid by the tenant and the Company receives all rents from existing tenants and parking lease revenue and remains responsible for all expenses, including real estate taxes, related to Parcel 20. Following tenant's possession, tenant is obligated to pay ground rent for the parcel and to purchase the building presently located on the premises for an additional amount payable monthly over twenty years.

*Generally speaking, a ground lease is a lease by the owner of the land (in this case, the Company) to the owners/operators of the real estate improvements built thereon by such owners/operators (“Ground Leases”).

All of the properties described above are shown on the map contained in Exhibit 20.

Billboard Lease

The Company, through its wholly-owned subsidiary Tri-State Displays, Inc. leases 23 outdoor advertising locations containing 44 billboard faces along interstate and primary highways in Rhode Island and Massachusetts to Lamar Outdoor Advertising, LLC (“Lamar”) under a lease which expires in 2053 (the “Lamar Lease”). All but one of these locations are controlled by the Company through permanent easements granted to the Company pursuant to an agreement between the Company and the Providence & Worcester Railroad Company (“Railroad”); the remaining location is leased by the Company from a third party with a remaining term of two years.

Lamar has a right of first refusal for additional billboard location sites acquired by the Company in New England and Metropolitan New York City.

The Lamar lease provides, among other things, for annual base rent increases of 2.75% in June for each leased billboard location and participation in the revenue generated by each billboard, as defined in the agreement. The Lamar lease contains other terms and conditions customary to such instruments.

A summary of the long-term leases is as follows:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Parcels in Capital Center Area |

|

Parcel Number |

|

Type of Building (s) |

|

Building Gross Square Feet |

|

|

Number of Residential Units |

|

Term of

Lease

(Years) |

|

Termination

Date |

|

Options

to Extend

Lease |

|

Current

Annual Contractual

Rent |

|

|

|

Next Periodic

Rent

Adjustment |

|

Annual Rent After Next Adjustment or Type of Next Adjustment |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2 |

|

17-story & 19-story Residential and |

|

|

307,000 |

|

|

193 |

|

103 |

|

2108 |

|

Two 75-Year |

|

$ |

609,000 |

|

|

|

2028 |

|

COLA |

|

|

|

13-story Office |

|

|

325,000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3S |

|

13-story Office |

|

|

235,000 |

|

|

|

|

99 |

|

2087 |

|

None |

|

$ |

618,000 |

|

|

|

2024 |

|

$ |

788,000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5 |

|

8-story Residential |

|

|

454,000 |

|

|

225 |

|

149 |

|

2142 |

|

None |

|

$ |

540,000 |

|

* |

|

2033 |

|

Appraisal |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6A |

|

4-6 story Residential |

|

|

120,000 |

|

|

96 |

|

99 |

|

2107 |

|

Two 50-Year |

|

$ |

367,000 |

|

|

|

2024 |

|

$ |

404,000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6B |

|

2-6 story Residential |

|

|

248,000 |

|

|

169 |

|

99 |

|

2107 |

|

Two 50-Year |

|

$ |

214,000 |

|

|

|

2024 |

|

$ |

235,000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7A |

|

Underground Public Parking Garage |

|

|

|

|

330 parking spaces |

|

99 |

|

2104 |

|

Two 75-Year |

|

$ |

200,000 |

|

|

|

2027 |

|

COLA |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8 |

|

4-story Office |

|

|

114,000 |

|

|

|

|

99 |

|

2090 |

|

None |

|

$ |

290,000 |

|

* |

|

2025 |

|

COLA |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

9 |

|

10-Story Office |

|

|

210,000 |

|

|

|

|

149 |

|

2153 |

|

None |

|

$ |

397,000 |

|

|

|

2026 |

|

$ |

417,000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Billboard Lease |

|

NA |

|

Billboard |

|

|

|

|

|

|

39 |

|

2053 |

|

** |

|

$ |

1,051,000 |

|

*** |

|

2024 |

|

$ |

1,080,000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

COLA |

|

Cost-of-living adjustment |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

* |

|

Lease provides for rent participation (contingent rent) equal to 1% of Gross Revenue. |

|

** |

|

Lease term is extended for four (4) years if an electronic billboard is constructed on a leased location. |

|

*** |

|

Lease provides for rent participation equal to 30% of Revenue, as defined in the agreement for each standard billboard and 20% of Revenue for each electronic billboard. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Major tenants:

The following table sets forth those major tenants whose revenues exceed 10 percent of the Company’s leasing revenues for the years ended December 31, 2023 and 2022:

|

|

|

|

|

|

|

|

|

|

|

Parcel |

|

|

|

2023 |

|

|

2022 |

|

NA |

|

Lamar Outdoor Advertising, LLC |

|

$ |

1,231,000 |

|

|

$ |

1,255,000 |

|

NA |

|

Metropark |

|

|

726,000 |

|

|

|

411,000 |

|

Parcel 5 |

|

HGIT Center Place |

|

|

641,000 |

|

|

|

625,000 |

|

Parcel 3S |

|

1701 R.C. Sarasota Invest, LLC |

|

|

618,000 |

|

|

|

618,000 |

|

Parcel 2 |

|

Waterplace Condominiums |

|

|

574,000 |

|

|

|

503,000 |

|

|

|

|

|

$ |

3,790,000 |

|

|

$ |

3,412,000 |

|

Competition

The Company competes for tenants with other owners of undeveloped real property in downtown Providence. The Company maintains no listing of other competitive properties and will not engage in a competitive bid arrangement with proposed developers. The Company’s refusal to sell the land that it owns may restrict the number of interested developers.

Employees

As of December 31, 2023, the Company has two full-time and one part-time employee.

Environmental

Prior to February 2017, the Company operated a petroleum storage facility (“Terminal”) through two of its wholly owned subsidiaries. On February 10, 2017, the Terminal was sold to Sprague Operating Resources, LLC (“Sprague”) which results in the Terminal’s operations being classified as discontinued operations for all periods presented. As part of the Terminal Sale Agreement, the Company agreed to complete the environmental remediation and pay for the costs related to a 1994 storage tank fuel oil leak which allowed the escape of a small amount of fuel oil. In February 2020, the Company filed a revised Remediation Action Work Plan (“RAWP”) with Rhode Island Department of Environmental Management (“RIDEM”) to incorporate technical details associated with the preferred remedial activities and to update the 2018 RAWP. During 2022, the remediation system was modified to address operational issues which impeded remediation activities. For the year ended December 31, 2023, the Company incurred costs of $79,000 of which $4,000 was charged against the environmental remediation accrual resulting in a liability of $402,000 at December 31, 2023 with the balance charged to other liabilities. Any subsequent increases or decreases to the expected cost of remediation will be recorded in the Company’s consolidated income statements as gain or loss on sale of discontinued operations.

Insurance

The Company maintains what management believes to be adequate levels of insurance.

Item 1C. Cybersecurity

Risk Management

The Company’s corporate information technology, communication networks, and accounting and financial reporting platforms are necessary for the operation of its business. The Company uses these systems, along with others, to manage its tenant and vendor relationships, for internal and external communications and for accounting to operate recordkeeping and reporting functions. The Company has implemented and maintains various information security processes designed to identify, assess and manage material risks from cybersecurity threats to its critical computer networks, third-party hosted services, communications systems, hardware and software, and our critical data, including confidential information.

Management works primarily with third parties (principally professional services and consulting firms) that assist management in identifying, assessing, and managing cybersecurity risks. To operate its business, the Company utilizes certain third-party service providers to perform a variety of functions and seeks to engage reliable, reputable service providers that maintain cybersecurity programs. The Company is not aware of any risks from cybersecurity threats, including as a result of any cybersecurity incidents, which have materially affected or are reasonably likely to materially affect it, including its business strategy, results of operations, or financial condition.

Governance:

The Board of Directors oversees the Company’s strategy and risk management, including material risks related to cybersecurity threats. The Board has delegated to the Audit Committee oversight of cybersecurity matters.

Management is responsible for day-to-day assessment and management of cybersecurity risks. The Treasurer has primary oversight of material risks from cybersecurity threats and works primarily with third parties to identify, assess, and manage cybersecurity risks. The Treasurer meets with the Audit Committee periodically to review the Company’s information technology systems and discuss key cybersecurity risks.

Item 2. Properties

The Company owns approximately 18 acres and a historic building in the Capital Center Area of Providence, Rhode Island. With the exception of Parcel 6C and the Steeple Street Building, all of the Company’s real property is leased either under long-term leases or short-term leases as more particularly described in Item 1, Business. The Company also owns or controls 23 locations in Rhode Island and Massachusetts on which 44 billboard faces have been constructed. All but one of these locations are owned by the Company under permanent easements from the Railroad; the remaining location is leased from an unrelated third party with a remaining term of two years.

Item 3. Legal Proceedings

In connection with the sale of the Company’s petroleum storage terminal in 2017, the Company and Sprague entered into an agreement relating to the construction of a breasting dolphin pursuant to which any construction costs incurred in excess of the contract cost of the construction would be shared equally between the Company and Sprague subject to certain limitations. In November 2019, Sprague asserted that it was owed $427,000 and the Company asserted that its obligation under the Agreement could not exceed $104,000. Mediation efforts were unsuccessful and in July 2021, Sprague commenced an action against the Company in the Rhode Island Superior Court (Superior Court) seeking monetary damages of $427,000, interest and attorney’s fees. In December 2022, the Superior Court denied Sprague’s Motion for Summary Judgment filed in September 2022 and granted in part and denied in part the Company’s Cross Motion for Summary Judgment also filed in September 2022. The Company anticipates that the matter will go to trial within the next six months. The Company intends to vigorously defend against the claims being asserted by Sprague.

Item 4. Mine Safety Disclosure – Not applicable

PART II

Item 5. Market for Registrant’s Common Equity and Related Stockholder Matters

The Company’s Class A Common Stock is traded on the OTCQX, symbol “CPTP.” The following table shows the high and low trading prices for the Company’s Class A Common Stock during the quarterly periods indicated as obtained from the OTCQX, together with cash dividends paid per share during such periods.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Trading Prices |

|

|

Dividends |

|

|

|

|

High |

|

|

Low |

|

|

Declared |

|

|

2023 |

|

|

|

|

|

|

|

|

|

|

1st Quarter |

|

$ |

12.20 |

|

|

$ |

10.55 |

|

|

$ |

0.07 |

|

|

2nd Quarter |

|

|

12.00 |

|

|

|

10.70 |

|

|

|

0.07 |

|

|

3rd Quarter |

|

|

13.00 |

|

|

|

11.12 |

|

|

|

0.07 |

|

|

4th Quarter |

|

|

12.52 |

|

|

|

11.35 |

|

|

|

0.07 |

|

|

|

|

|

|

|

|

|

|

|

|

|

2022 |

|

|

|

|

|

|

|

|

|

|

1st Quarter |

|

$ |

13.46 |

|

|

$ |

12.00 |

|

|

$ |

0.07 |

|

|

2nd Quarter |

|

|

12.99 |

|

|

|

11.95 |

|

|

|

0.07 |

|

|

3rd Quarter |

|

|

12.12 |

|

|

|

10.59 |

|

|

|

0.07 |

|

|

4th Quarter |

|

|

12.20 |

|

|

|

11.00 |

|

|

|

0.07 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

At February 16, 2024, there were 322 holders of record of the Company’s Class A Common Stock.

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Our consolidated financial statements are prepared in accordance with accounting principles generally accepted in the United States (“GAAP”). The following discussion of our financial condition and results of operations excludes the results of our discontinued operations unless otherwise noted. See Note 9, “Discontinued operations and environmental incident” in the accompanying Consolidated Financial Statements for further discussion of these operations.

Critical accounting policies:

The Securities and Exchange Commission (“SEC”) has issued guidance for the disclosure of “critical accounting policies.” The SEC defines such policies as those that require application of management’s most difficult, subjective or complex judgments, often as a result of the need to make estimates about the effect of matters that are inherently uncertain and may change in subsequent periods.

The Company’s significant accounting policies are described in Note 2 in the accompanying Consolidated Financial Statements. Not all of these significant accounting policies require management to make difficult, subjective or complex judgments or estimates. Management believes that the Company’s revenue recognition policy for long-term leases with scheduled rent increases meets the SEC definition of “critical.”

The Company’s long-term leases (land and billboard) have original terms of 30 to 149 years. The Company follows GAAP in accounting for its leases by recognizing rental income on the straight-line basis over the term of the leases. Where the straight-line income exceeds the actual contractual payments (“Excess”), the Company evaluates the collectability of the entire stream of remaining lease payments on a lease-by-lease basis. If the remaining lease payments are not deemed to be probable of collection, in accordance with GAAP, lease revenue is recorded at the lower of straight-line rental income or the contractual amount paid.

The number of years remaining on the Company’s leases range from twenty-six (26) years to one hundred-thirty (130) years with total rents yet to be collected from tenants (without regard to CPI and appraisal adjustments) under the lease ranging from $19.2 million to $363.0 million. Given the length of the remaining lease term and the magnitude of the amount yet to be collected, along with the consideration of other factors, the Company has concluded that the remaining stream of lease payments is not probable of collection and as such, reports lease revenue based on the contractual amount paid.

2.Liquidity and capital resources:

Historically, the Company generates adequate liquidity to fund its operations.

Cash and cash commitments:

The Company had cash and cash equivalents of $652,000 and $1,476,000 at December 31, 2023 and 2022, respectively, inclusive of a money market account totaling $461,000 and $1,273,000 in each of the aforementioned years. Additional sources of funds to fund operations include investments that mature in April 2024 totaling $1,244,000 along with a $2,000,000 unused line of credit (see Note 6 in the accompanying Consolidated Financial Statements). The Company and its subsidiary each maintain checking accounts and one money market account in a financial institution which is insured by the Federal Deposit Insurance Corporation to a maximum of $250,000. The Company periodically evaluates the financial stability of the financial institutions at which the Company’s funds are held.

Under the terms of each applicable long-term land lease, the contractual adjustments for the last two years were:

|

|

|

|

|

|

|

Parcel Number |

|

Monthly Increase |

|

Effective Date of Increase |

|

Type of Adjustment |

Parcel 7A |

|

$2,539 |

|

April 1, 2022 |

|

Base ground rent increase |

Parcel 2 |

|

$8,847 |

|

May 1, 2023 |

|

COLA Adjustment |

The City of Providence (“City”) conducted a City-wide property revaluation for 2022. This revaluation increased the assessed value of the Company’s parcels that are available for lease by 26.5%, resulting in an annual property tax increase of $139,000 that was to be borne entirely by the Company. The Company's appeal of the assessed values for certain of its parcels was successful and resulted in a reduction of the assessed value to an amount less than the 2021 assessed value and in an annual property tax reduction in 2022 taxes as originally assessed of $165,000, which amount was recorded in the fourth quarter of 2022.

Through February 16, 2024 all tenants have paid their monthly rent in accordance with their lease agreements.

The COVID-19 pandemic had an adverse impact on Metropark’s parking operations as the move by many companies to a hybrid workplace model (one that mixes in-office and remote work) resulted in lower demand for parking spaces. From June 2020 through December 31, 2023 the Company and Metropark operated under a Revenue Sharing Agreement, dated June 30, 2020, that provided for revenue sharing at various percentages until parking revenues received by Metropark equal or exceed $70,000 per month whereupon Metropark would be obligated to resume regularly scheduled rental payments under its lease. During this time, revenue was recognized on a cash basis with the difference between the regularly scheduled rental payments and amounts paid ("deferred rent") recorded as an accounts receivable and was fully reserved.

In January 2024, the Company entered into a Second Amendment to its Lease Agreement whereby Metropark agreed to return to a fixed monthly rental payment of $57,000 per month effective January 1, 2024 subject to adjustment in accordance with the Lease Agreement. Additionally, the Company and Metropark settled the Company’s claim for deferred rent for all prior periods which amounted to $1,127,000 (fully reserved on the Company’s books) for $150,000 payable by Metropark in twenty (20) equal quarterly installments commencing on April 1, 2024 together with interest on the unpaid balance in the amount of 4.73% per annum. At December 31, 2023, the $150,000 settlement is included in Prepaid and other and in Leasing revenue in the accompanying consolidated balance sheets and statements of income and retained earnings.

The Terminal Sale Agreement and related documentation provides that the Company is required to secure an approved remediation plan and to remediate contamination caused by a leak in 1994 from a storage tank at the Terminal. At December 31, 2023, the Company’s accrual for the remaining cost of remediation was $402,000 of which $132,000 is expected to be expended in 2024. The Terminal Sale Agreement also contained a cost sharing provision for a breasting dolphin whereby any construction costs in excess of the contract cost of construction would be borne equally by Sprague and the Company subject to certain limitations, including, in the Company’s opinion, a 20% cap on the increase from the initial estimate subject to the sharing arrangement. In November 2019, Sprague asserted that it was owed $427,000 and the Company asserted that its obligation under the Agreement could not exceed $104,000. Mediation efforts were unsuccessful and in July 2021, Sprague commenced an action against the Company in the Rhode Island Superior Court (Superior Court) seeking monetary damages of $427,000, plus interest and attorney’s fees. In December 2022, the Superior Court denied Sprague’s Motion for Summary Judgment filed in September 2022 and granted in part and denied in part the Company’s Cross Motion for Summary Judgment also filed in September 2022. The Company anticipates that the matter will go to trial within the next six months. The Company intends to vigorously defend against the claims being asserted by Sprague. See Note 9, “Discontinued operations and environmental incident” in the accompanying Consolidated Financial Statements.

In 2023, the Company declared and paid dividends of $1,848,000 or $0.28 per share.

The declaration of future dividends will depend on future earnings and financial performance.

Year Ended December 31, 2023 Compared to Year Ended December 31, 2022:

Leasing revenue increased $450,000 from 2022 due principally to an increase in cash collections from Metropark along with the $150,000 deferred rent settlement ($315,000) and a net increase in rent (contractual and contingent) from tenants ($135,000).

Operating expenses decreased $40,000 in 2023 as there were no professional fees associated with the property tax appeal that occurred in 2022.

General and administrative expense increased $57,000 due principally to an increase in payroll and payroll related costs.

For the years ended December 31, 2023 and 2022, the Company’s effective income tax rate from continuing operations is 27%.

Item 8. Financial Statements and Supplementary Data

CAPITAL PROPERTIES, INC. AND SUSIDIARY

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Directors and Shareholders of

Capital Properties, Inc.

Providence, Rhode Island

Opinion on the Financial Statements

We have audited the accompanying consolidated balance sheets of Capital Properties, Inc. (the “Company”) as of December 31, 2023 and 2022, and the related consolidated statements of income and retained earnings, and cash flows for each of the years in the two-year period ended December 31, 2023, and the related notes (collectively referred to as the “consolidated financial statements”). In our opinion, the consolidated financial statements present fairly, in all material respects, the financial position of the Company as of December 31, 2023 and 2022, and the results of its operations and its cash flows for each of the years in the two-year period ended December 31, 2023, in conformity with accounting principles generally accepted in the United States of America.

Basis for Opinion

These consolidated financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on the Company’s consolidated financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Company in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Company is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. As part of our audits, we are required to obtain an understanding of internal control over financial reporting, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audits included performing procedures to assess the risks of material misstatement of the consolidated financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the consolidated financial statements. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements. We believe our audits provide a reasonable basis for our opinion.

Critical Audit Matter

The critical audit matter communicated below is a matter arising from the current period audit of the consolidated financial statements that was communicated or required to be communicated to the audit committee and that: (1) relates to accounts or disclosures that are material to the consolidated financial statements and (2) involved our especially challenging, subjective, or complex judgments. The communication of a critical audit matter does not alter in any way our opinion on the consolidated financial statements taken as a whole, and we are not, by communicating the critical audit matter below, providing a separate opinion on the critical audit matter or on the accounts or disclosures to which it relates.

Revenue Recognition – Refer to Note 2 to the Consolidated Financial Statements

Critical Audit Matter Description

The Company derives revenue from long-term leases with original terms ranging from 30 years to 149 years. Effective January 1, 2019 the Company adopted ASC 842, Leases, and elected the “package of practical expedients” which permits the Company not to reassess under the new standard prior conclusions about lease identification, lease classification, and initial indirect costs and determined that all pre-existing leases were properly accounted for as operating. The long-term leases contain periodic rent increases based on either a specific percentage, market appraisals, changes in the consumer price index or combination thereof. In accordance with generally accepted accounting principles, lease income should be recognized on a straight-line basis. Where

straight-line income exceeds the actual contractual payments (the “Excess”), the Excess should only be recognized to the extent it is collectable. In accordance with ASC 842, if collectability of the lease payments is not probable, lease income shall be limited to the lesser of the income that would be recognized in accordance with ASC 842 (straight-line basis) or the actual lease payment, including variable payments that have been collected from the lessee. The Company evaluates the entire stream of remaining lease payments on a lease-by-lease basis. Analysis of collectability from the lessee (tenant) is subjective and complex and is dependent on many factors including historical experience and the creditworthiness of the tenant. The creditworthiness of the tenant can, and often is, significantly influenced by major factors including the creditworthiness of multiple sub-tenants. The inability to access reliable credit information on all parties impacting the probability of collection creates a collectability constraint. Management updates its collectability analysis of long-term leases annually and has determined that collection of the entire remaining stream of remaining lease payments is not probable. Accordingly lease revenue, including variable payments, is recorded when received from the lessee.

How the Critical Audit Matter was Addressed in the Audit

Our audit procedures related to the recognition of long-term lease revenue on a straight-line basis included the following, among others:

•We evaluated the effectiveness of controls over lease revenue recognition, including management's analysis of and conclusions regarding collection probability.

•We evaluated the application of the Company’s accounting policies in the context of the applicable accounting standards (ASC842) as adopted on January 1, 2019.

•We evaluated the appropriateness and consistency of methods and assumptions used by management to determine and support its collection probability conclusion.

•We considered changes in the lease terms, including tenant payment patterns or other information, and determined such information was properly considered by management in its analysis.

/s/ Stowe & Degon, LLC

We have served as the Company’s auditor since 2016.

Westborough, Massachusetts

February 16, 2024

CAPITAL PROPERTIES, INC. AND SUBSIDIARY

CONSOLIDATED BALANCE SHEETS

|

|

|

|

|

|

|

|

|

|

|

December 31, |

|

|

|

2023 |

|

|

2022 |

|

ASSETS |

|

|

|

|

|

|

|

|

|

|

|

|

|

Properties and equipment (net of accumulated depreciation) (Note 4) |

|

$ |

6,498,000 |

|

|

$ |

6,584,000 |

|

Cash and cash equivalents |

|

|

652,000 |

|

|

|

1,476,000 |

|

Investments |

|

|

1,244,000 |

|

|

|

- |

|

Prepaid and other |

|

|

387,000 |

|

|

|

224,000 |

|

Prepaid income taxes |

|

|

57,000 |

|

|

|

21,000 |

|

Deferred income taxes, discontinued operations |

|

|

109,000 |

|

|

|

110,000 |

|

|

|

$ |

8,947,000 |

|

|

$ |

8,415,000 |

|

|

|

|

|

|

|

|

LIABILITIES AND SHAREHOLDERS’ EQUITY |

|

|

|

|

|

|

|

|

|

|

|

|

|

Liabilities: |

|

|

|

|

|

|

Property taxes |

|

$ |

340,000 |

|

|

$ |

260,000 |

|

Other |

|

|

330,000 |

|

|

|

366,000 |

|

Deferred income taxes, net |

|

|

284,000 |

|

|

|

271,000 |

|

Environmental remediation accrual, discontinued operations (Note 9) |

|

|

402,000 |

|

|

|

406,000 |

|

|

|

|

1,356,000 |

|

|

|

1,303,000 |

|

|

|

|

|

|

|

|

Shareholders’ equity: |

|

|

|

|

|

|

Class A common stock, $.01 par; authorized 10,000,000 shares; issued and

outstanding 6,599,912 shares |

|

|

66,000 |

|

|

|

66,000 |

|

Capital in excess of par |

|

|

782,000 |

|

|

|

782,000 |

|

Retained earnings |

|

|

6,743,000 |

|

|

|

6,264,000 |

|

|

|

|

7,591,000 |

|

|

|

7,112,000 |

|

|

|

$ |

8,947,000 |

|

|

$ |

8,415,000 |

|

See accompanying notes to Consolidated Financial Statements.

CAPITAL PROPERTIES, INC. AND SUBSIDIARY

CONSOLIDATED STATEMENTS OF INCOME AND RETAINED EARNINGS

|

|

|

|

|

|

|

|

|

|

|

December 31, |

|

|

|

2023 |

|

|

2022 |

|

|

|

|

|

|

|

|

Leasing revenue |

|

$ |

5,525,000 |

|

|

$ |

5,075,000 |

|

|

|

|

|

|

|

|

Expenses: |

|

|

|

|

|

|

Operating |

|

|

882,000 |

|

|

|

922,000 |

|

General and administrative |

|

|

1,394,000 |

|

|

|

1,337,000 |

|

|

|

|

2,276,000 |

|

|

|

2,259,000 |

|

|

|

|

|

|

|

|

Income from continuing operations before income taxes |

|

|

3,249,000 |

|

|

|

2,816,000 |

|

|

|

|

|

|

|

|

Income tax expense: |

|

|

|

|

|

|

Current |

|

|

885,000 |

|

|

|

765,000 |

|

Deferred |

|

|

13,000 |

|

|

|

9,000 |

|

|

|

|

898,000 |

|

|

|

774,000 |

|

|

|

|

|

|

|

|

Income from continuing operations |

|

|

2,351,000 |

|

|

|

2,042,000 |

|

|

|

|

|

|

|

|

Loss on sale of discontinued operations, net of tax (Note 9) |

|

|

(24,000 |

) |

|

|

(255,000 |

) |

|

|

|

|

|

|

|

Net income |

|

|

2,327,000 |

|

|

|

1,787,000 |

|

Retained earnings, beginning |

|

|

6,264,000 |

|

|

|

6,325,000 |

|

Dividends on common stock based on 6,599,912 shares outstanding |

|

|

(1,848,000 |

) |

|

|

(1,848,000 |

) |

Retained earnings, ending |

|

$ |

6,743,000 |

|

|

$ |

6,264,000 |

|

Basic income (loss) per common share based upon 6,599,912 shares

outstanding: |

|

|

|

|

|

|

Continuing operations |

|

$ |

0.35 |

|

|

$ |

0.31 |

|

Discontinued operations |

|

|

(0.00 |

) |

|

|

(0.04 |

) |

Total basic income per common share |

|

$ |

0.35 |

|

|

$ |

0.27 |

|

See accompanying notes to Consolidated Financial Statements.

CAPITAL PROPERTIES, INC. AND SUBSIDIARY

CONSOLIDATED STATEMENTS OF CASH FLOWS

|

|

|

|

|

|

|

|

|

|

|

December 31, |

|

|

|

2023 |

|

|

2022 |

|

Cash flows from operating activities: |

|

|

|

|

|

|

Continuing operations: |

|

|

|

|

|

|

Income from continuing operations |

|

$ |

2,351,000 |

|

|

$ |

2,042,000 |

|

Adjustments to reconcile income from continuing operations to net

cash provided by operating activities, continuing operations: |

|

|

|

|

|

|

Depreciation |

|

|

86,000 |

|

|

|

86,000 |

|

Deferred income taxes |

|

|

13,000 |

|

|

|

9,000 |

|

Changes in assets and liabilities: |

|

|

|

|

|

|

Prepaid income taxes |

|

|

(36,000 |

) |

|

|

64,000 |

|

Prepaid and other |

|

|

(163,000 |

) |

|

|

(102,000 |

) |

Property taxes |

|

|

80,000 |

|

|

|

(17,000 |

) |

Other |

|

|

(36,000 |

) |

|

|

16,000 |

|

Net cash provided by operating activities, continuing operations |

|

|

2,295,000 |

|

|

|

2,098,000 |

|

|

|

|

|

|

|

|

Cash flows from investing activities: |

|

|

|

|

|

|

Purchase of Investments |

|

|

(1,244,000 |

) |

|

|

- |

|

Discontinued operations: |

|

|

|

|

|

|

Loss on sale of discontinued operation |

|

|

(24,000 |

) |

|

|

(255,000 |

) |

Cash used to settle obligations |

|

|

(4,000 |

) |

|

|

(112,000 |

) |

Adjustment to loss on sale of discontinued operations |

|

|

1,000 |

|

|

|

150,000 |

|

|

|

|

(27,000 |

) |

|

|

(217,000 |

) |

Net cash (used in) investing activities |

|

|

(1,271,000 |

) |

|

|

(217,000 |

) |

|

|

|

|

|

|

|

Cash flows from financing activities, payment of dividends |

|

|

(1,848,000 |

) |

|

|

(1,848,000 |

) |

|

|

|

|

|

|

|

Increase (decrease) in cash and cash equivalents |

|

|

(824,000 |

) |

|

|

33,000 |

|

Cash and cash equivalents, beginning |

|

|

1,476,000 |

|

|

|

1,443,000 |

|

Cash and cash equivalents, ending |

|

$ |

652,000 |

|

|

$ |

1,476,000 |

|

|

|

|

|

|

|

|

Supplemental disclosures: |

|

|

|

|

|

|

Cash paid for income taxes |

|

$ |

913,000 |

|

|

$ |

619,000 |

|

|

|

|

|

|

|

|

See accompanying notes to Consolidated Financial Statements.

CAPITAL PROPERTIES, INC. AND SUBSIDIARY

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

YEARS ENDED DECEMBER 31, 2023 AND 2022

1.Description of business:

The operations of Capital Properties, Inc. and its wholly-owned subsidiary, Tri-State Displays, Inc. (collectively “the Company”) consist of the long-term leasing of certain of its real estate interests in the Capital Center area in downtown Providence, Rhode Island (upon the commencement of which the tenants have been required to construct buildings thereon, with the exception of the parking garage and Parcel 20) and the leasing of locations along interstate and primary highways in Rhode Island and Massachusetts to Lamar Outdoor Advertising, LLC (“Lamar”) on which Lamar has constructed outdoor advertising boards. The Company anticipates that the future development of its remaining properties in the Capital Center area will consist primarily of long-term ground leases. Pending this development, the Company leases these undeveloped parcels (other than Parcel 6C) for public parking to Metropark, Ltd.

2.Summary of significant accounting policies:

Principles of consolidation:

The accompanying consolidated financial statements include the accounts and transactions of the Company and its wholly-owned subsidiary. All significant intercompany accounts and transactions have been eliminated in consolidation.

Use of estimates:

The preparation of consolidated financial statements in conformity with accounting principles generally accepted in the United States (“GAAP”) requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements. Estimates also affect the reported amounts of income and expenses during the reporting period. Actual results could differ from those estimates.

Fair value of financial instruments:

The Company believes that the fair values of its financial instruments, including cash and cash equivalents and payables, approximate their respective book values because of their short-term nature. The fair values described herein were determined using significant other observable inputs (Level 2) as defined by GAAP.

Properties and equipment:

Properties and equipment are stated at cost. Acquisitions and additions are capitalized while routine maintenance and repairs, which do not improve the asset or extend its life, are charged to expense when incurred. Depreciation is being provided by the straight-line method over the estimated useful lives of the respective assets.

The Company reviews properties and equipment for impairment whenever events or changes in circumstances indicate that the net book value of the asset may not be recoverable. An impairment loss will be recognized if the sum of the expected future cash flows (undiscounted and before interest) from the use of the asset is less than the net book value of the asset. Generally, the amount of the impairment loss is measured as the difference between the net book value and the estimated fair value of the asset.

Cash and cash equivalents:

The Company considers all highly liquid investments with a maturity of three months or less when purchased to be cash equivalents. Cash equivalents include money market accounts totaling $461,000 and $1,273,000, at December 31, 2023 and 2022, respectively. The Company and its subsidiary each maintain a checking account and one money market account in a bank, all of which are insured by the Federal Deposit Insurance Corporation to a maximum of $250,000. The Company has not experienced any losses in such accounts.

Environmental incidents:

The Company accrues a liability when an environmental incident has occurred and the costs are estimable. The Company does not record a receivable for recoveries from third parties for environmental matters until it has determined that the amount of the collection is reasonably assured. The accrued liability is relieved when the Company pays the liability or a third party assumes the liability. Upon determination that collection is reasonably assured or a third party assumes the liability, the Company records the amount as a reduction of expense.

Revenues:

The Company’s properties leased to others are under operating leases. The Company reports leasing revenue when earned under the operating method.

Certain of the Company’s long-term leases (land and billboard) provide for presently known scheduled rent increases over the remaining terms (26 to 130 years). The Company follows GAAP in accounting for leases whereby revenue is recognized on the straight-line basis over the terms of the leases when management is able to conclude that all remaining lease payments are collectable. To date, management has recognized revenue on a contractual basis as it has been unable to conclude that the remaining lease payments are realizable (collectable) due to the magnitude of the remaining lease payments to be collected, the length of the lease terms and other related uncertainties.

The Company reports contingent revenue in the period in which the factors occur on which the contingent payments are predicated.

Income taxes:

The Company and its subsidiary file consolidated income tax returns.

The Company provides for income taxes based on income reported for financial reporting purposes.

Based on its evaluation, the Company has concluded that there are no significant uncertain tax positions requiring recognition in the consolidated financial statements. The Company will report any tax-related interest and penalties related to uncertain tax positions as a component of income tax expense. The Company’s federal and state income tax returns are generally open for examination for the past three years.

Legal fees:

The Company recognizes legal fees as incurred.

Basic earnings per common share:

Basic earnings per common share are computed by dividing net income by the weighted average number of common shares outstanding during the period.

Recently issued accounting pronouncements

In December 2023, the FASB issued ASU 2023-09, “Income Taxes (Topic 740): Improvements to Income Tax Disclosures.” This update requires additional disclosures including greater disaggregation of information in the reconciliation of the statutory rate to the effective rate and income taxes paid disaggregated by jurisdiction. The ASU is effective for fiscal years ending after December 15, 2024. We will not early adopt the standard and are currently evaluating the effect on our financial statements.

Investments consist of U.S. Treasury securities that yield 5.04% and mature in April 2024. The Company classifies its U. S. Treasury securities as held-to-maturity in accordance with ASC 320 "Investments - Debt and Equity Securities". Held-to-maturity securities are those securities which the Company has the ability and intent to hold until maturity. Held-to-maturity treasury securities are recorded at amortized cost on the accompanying consolidated balance sheet and adjusted for the amortization or accretion of premiums or discounts.

4.Properties and equipment:

Properties and equipment consist of the following:

|

|

|

|

|

|

|

|

|

|

|

|

|

Estimated

Useful |

|

December 31, |

|

|

|

Life in Years |

|

2023 |

|

|

2022 |

|

|

|

|

|

|

|

|

|

|

Land and land improvements on lease or held for lease |

|

|

|

$ |

4,439,000 |

|

|

$ |

4,439,000 |

|

Building and improvements, Steeple Street (Note 7) |

|

30 |

|

|

2,582,000 |

|

|

|

2,582,000 |

|

|

|

|

|

|

7,021,000 |

|

|

|

7,021,000 |

|

Less accumulated depreciation: |

|

|

|

|

|

|

|

|

Land improvements on lease or held for lease |

|

|

|

|

93,000 |

|

|

|

93,000 |

|

Steeple Street property (Note 7) |

|

|

|

|

430,000 |

|

|

|

344,000 |

|

|

|

|

|

|

523,000 |

|

|

|

437,000 |

|

|

|

|

|

$ |

6,498,000 |

|

|

$ |

6,584,000 |

|

Liabilities, other consist of the following:

|

|

|

|

|

|

|

|

|

|

|

December 31, |

|

|

|

2023 |

|

|

2022 |

|

Accrued professional fees |

|

$ |

157,000 |

|

|

$ |

155,000 |

|

Deposits and prepaid rent |

|

|

146,000 |

|

|

|

93,000 |

|

Accrued payroll and related costs |

|

|

- |

|

|

|

75,000 |

|

Other |

|

|

27,000 |

|

|

|

43,000 |

|

|

|

$ |

330,000 |

|

|

$ |

366,000 |

|

6.Note Payable - Revolving Credit Line:

In March 2021, the Company entered into a financing agreement (“Agreement”) with BankRI that provides for a revolving line-of-credit (the “Line”) with a maximum borrowing capacity of $2,000,000 through March 2024. Amounts outstanding under the Agreement bear interest at the rate of the Secured Overnight Financing Rate ("SOFR") plus the one-month SOFR Spread Adjustment of .11448%, but not less than 3.25% or, at the option of the Company, the Wall Street Journal Prime Rate. Borrowings under the Line are secured by a First Mortgage on Parcel 5 in the Capital Center District in Providence, Rhode Island (the “Property”). The Line requires the maintenance of a debt service coverage ratio of not less than 1.25 to 1.0 on the Property and 1.20 to 1.0 for the Company. The Agreement contains other restrictive covenants, including, among others, a $250,000 limitation on the purchase of its outstanding capital stock in any twelve-month period. No advances have been made under the Line.

7.Description of leasing arrangements and subsequent event:

Long-term land leases:

Through December 31, 2023 the Company had entered into eight long-term land leases, all of which have completed construction of improvements thereon. The leases generally have a term of 99 years or more, are triple net, and provide for periodic adjustment in rent of various types depending on the particular lease, and otherwise contain terms and conditions normal for such instruments.

Under the eight land leases, the tenants may negotiate tax stabilization treaties or other arrangements, appeal any changes in real property assessments, and pay real property taxes assessed on land and improvements under these arrangements. Accordingly, real property taxes payable by the tenants are excluded from leasing revenues and leasing expenses on the accompanying consolidated statements of income and retained earnings. For each of the years ended December 31, 2023 and 2022, the real property taxes attributable to the Company’s land under leases, exclusive of Parcel 2 which is a condominium, were $944,000.

Under two of the long-term land leases, the Company receives contingent rentals (based on a fixed percentage of gross revenue received by the tenants) which totaled $118,000 and $99,000 for the years ended December 31, 2023 and 2022, respectively.

On January 25, 2024, the Company entered into a long-term ground lease of Parcel 20. Under the terms of the lease, tenant's possession will not occur until such time as the tenant has received all necessary approvals for construction of not less than 100,000 square feet of mixed use improvements. Prior to transfer of possession, no rent is being paid by the tenant and the Company receives all rents from existing tenants and parking lease revenue and remains responsible for all expenses, including real estate taxes, related to Parcel 20. Following tenant's possession, tenant is obligated to pay ground rent for the parcel and to purchase the historic building presently located on the premises for an additional amount payable monthly over twenty years.

The City of Providence (“City”) conducted a City-wide property revaluation for 2022. This revaluation increased the assessed value of the Company’s parcels that are available for lease by 26.5%, resulting in an annual property tax increase of $139,000. The Company’s appeal of the assessed values for certain of its parcels was successful and resulted in a reduction of the assessed value to an amount less than the 2021 assessed value and in an annual property tax reduction in 2022 taxes as originally assessed of $165,000, which amount was recorded in the fourth quarter of 2022. Property tax expense associated with the Company's parcels that are available for lease was $579,000 for each of the years ended December 31, 2023 and 2022 and are included in operating expenses on the accompanying consolidated statements of income and retained earnings.

Lamar lease:

Tri-State Displays, Inc., leases 23 outdoor advertising locations containing 44 billboard faces along interstate and primary highways in Rhode Island and Massachusetts to Lamar under a lease which expires in 2053. The Lamar lease provides, among other things, for the following: (1) the base rent will increase annually at the rate of 2.75% for each leased billboard location on June 1 of each year, and (2) in addition to base rent, for each 12-month period commencing each June 1, Lamar must pay to the Company within thirty days after the close of the lease year 30% of the gross revenues from each standard billboard and 20% of the gross revenues from each electronic billboard for such 12-month period, reduced by the sum of (a) commissions paid to third parties and (b) base monthly rent for each leased billboard display for each 12-month period. For the lease years ended May 31, 2023 and 2022, the percentage rent totaled $188,000 and $235,000, respectively, which amounts are included in Leasing revenue on the accompanying consolidated statements of income and retained earnings for the years ended December 31, 2023 and 2022.

Parking lease:

The Company leases the undeveloped parcels of land in or adjacent to the Capital Center area (other than Parcel 6C) for public parking purposes to Metropark under a ten-year lease dated January 1, 2017. The lease is cancellable as to all or any portion of the leased premises at any time on thirty day’s written notice in order for the Company or any new tenant of the Company to develop all or any portion of the leased premises. The parking lease provides for contingent rent based on a fixed percentage of gross revenue in excess of the base rent as defined in the agreement.

The COVID-19 pandemic had an adverse impact on Metropark’s parking operations as the move by many companies to a hybrid workplace model (one that mixes in-office and remote work) resulted in lower demand for parking spaces. From June 2020 through December 31, 2023 the Company and Metropark operated under a Revenue Sharing Agreement, dated June 30, 2020, that provided for revenue sharing at various percentages until parking revenues received by Metropark equal or exceed $70,000 per month whereupon Metropark would be obligated to resume regularly scheduled rental payments under its lease. During this time, revenue was recognized on a cash basis with the difference between the regularly scheduled rental payments and amounts paid ("deferred rent") recorded as an accounts receivable and was fully reserved.

On January 9, 2024, Capital Properties, Inc. (the “Company”) entered into a Second Amendment to its Lease Agreement whereby Metropark agreed to return to a fixed monthly rental payment of $57,000 per month effective January 1, 2024 subject to adjustment in accordance with the Lease Agreement. Additionally, the Company and Metropark settled the Company’s claim for deferred rent for all prior periods which amounted to $1,127,000 (fully reserved on the Company’s books) for $150,000 payable by Metropark in twenty (20) equal quarterly installments commencing on April 1, 2024 together with interest on the unpaid balance in the amount of 4.73% per annum. At December 31, 2023, the $150,000 settlement is included in Prepaid and other and in Leasing revenue in the accompanying consolidated balance sheets and statements of income and retained earnings.

Minimum future contractual rental payments, inclusive of presently known scheduled rent increases to be received from non-cancellable long-term leases as of December 31, 2023 are:

|

|

|

|

|

Year ending December 31, |

|

|

|

2024 |

|

$ |

4,248,000 |

|

2025 |

|

|

4,435,000 |

|

2026 |

|

|

4,480,000 |

|

2027 |

|

|

4,511,000 |

|

2028 |

|

|

4,511,000 |

|

2028-2153 |

|

|

730,997,000 |

|

|

|

$ |

753,182,000 |

|

Consistent with prior conclusions, the Company has determined that, at this time, the excess of straight-line rentals over contractual payments is not probable of collection. Accordingly, the Company has not included any part of that amount in revenue. As a matter of information only, as of December 31, 2023 the excess of straight-line rentals (calculated by excluding variable payments) over contractual payments was $92,728,000.

In the event of tenant default, the Company has the right to reclaim its leased land together with any improvements thereon, subject to the right of any leasehold mortgagee to enter into a new lease with the Company with the same terms and conditions as the lease in default.

The following table sets forth those major tenants whose revenues exceed 10 percent of the Company’s revenues for the years ended December 31, 2023 and 2022:

|

|

|

|

|

|

|

|

|

|

|

2023 |

|

|

2022 |

|

Lamar Outdoor Advertising, LLC |

|

$ |

1,231,000 |

|

|

$ |

1,255,000 |

|

Metropark |

|

|

726,000 |

|

|

|

411,000 |

|

HGIT Center Place |

|

|

641,000 |

|

|

|

625,000 |

|

1701 R.C. Sarasota Invest, LLC |

|

|

618,000 |

|

|

|

618,000 |

|

Waterplace Condominiums |

|

|

574,000 |

|

|

|

503,000 |

|

|

|

$ |

3,790,000 |

|

|

$ |

3,412,000 |

|

8.Income taxes, continuing operations:

For the years ended December 31, 2023 and 2022, income tax expense from continuing operations is comprised of the following components:

|

|

|

|

|

|

|

|

|

|

|

2023 |

|

|

2022 |

|

Current: |

|

|

|

|

|

|

Federal |

|

$ |

637,000 |

|

|

$ |

557,000 |

|

State |

|

|

248,000 |

|

|

|

208,000 |

|

|

|

|

885,000 |

|

|

|

765,000 |

|

Deferred: |

|

|

|

|

|

|

Federal |

|

|

8,000 |

|

|

|

7,000 |

|

State |

|

|

5,000 |

|

|

|

2,000 |

|

|

|

|

13,000 |

|

|

|