Filed by CorpAcq Group Plc pursuant to

Rule 425 under the Securities Act of 1933

and deemed filed pursuant to Rule 14a-12

under the Securities Exchange Act of 1934

Subject Company: Churchill Capital Corp VII

Commission File No.: 001-40051

UNITED

STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

PURSUANT TO SECTION 13 OR 15(d)

OF THE

SECURITIES EXCHANGE ACT OF 1934

Date of Report (Date of earliest event reported): November 17, 2023

CHURCHILL CAPITAL CORP VII

(Exact name of registrant as specified in its

charter)

| Delaware |

001-40051 |

85-3420354 |

(State

or other jurisdiction

of incorporation) |

(Commission

File Number) |

(IRS

Employer

Identification No.) |

640 Fifth Avenue, 12th Floor

New York, NY 10019

(Address of principal

executive offices, including zip code)

Registrant’s telephone number,

including area code: (212) 380-7500

Not Applicable

(Former name or former address, if changed since last report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously

satisfy the filing obligation of the registrant under any of the following provisions:

| |

¨ | Written communications pursuant to Rule 425 under the Securities

Act (17 CFR 230.425) |

| |

| |

| |

x | Soliciting material pursuant to Rule 14a-12 under the Exchange

Act (17 CFR 240.14a-12) |

| |

| |

| |

¨ | Pre-commencement communications pursuant to Rule 14d-2(b) under

the Exchange Act (17 CFR 240.14d-2(b)) |

| |

| |

| |

¨ | Pre-commencement communications pursuant to Rule 13e-4(c) under

the Exchange Act (17 CFR 240.13e-4(c)) |

Securities

registered pursuant to Section 12(b) of the Act:

| Title of each class |

|

Trading

Symbol(s) |

|

Name of each exchange on

which registered |

| Units, each consisting of one share of Class A common stock, $0.0001 par value, and one-fifth of one warrant |

|

CVII.U |

|

New York Stock Exchange |

| |

|

|

|

|

| Shares of Class A common stock |

|

CVII |

|

New York Stock Exchange |

| |

|

|

|

|

| Warrants |

|

CVII WS |

|

New York Stock Exchange |

Indicate by check mark whether the registrant

is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the

Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging growth company ¨

If an emerging growth company, indicate by check

mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting

standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Churchill Capital Corp VII (“CCVII”),

CorpAcq Holdings Limited, a private limited company incorporated under the laws of England and Wales (“CorpAcq”)

and CorpAcq Group Plc, a public limited company incorporated under the laws of England and Wales ("CorpAcq Group") issued a

joint press release (the “Press Release”) on November 17, 2023

announcing the filing of a registration statement of CorpAcq Group on Form F-4 (the “Registration

Statement”) with the U.S. Securities and Exchange Commission (“SEC”)

on November 17, 2023.

The Registration Statement contains a preliminary proxy statement/prospectus

in connection with the proposed business combination between CCVII, CorpAcq Group and CorpAcq (together with the other transactions contemplated

thereby, the “Transactions”). While the Registration Statement has not yet become effective and the information contained

therein is subject to change, it provides important information about CCVII, CorpAcq Group, CorpAcq, and the Transactions. The Press Release

is attached hereto as Exhibit 99.1 and incorporated by reference herein.

Attached as Exhibit 99.2 and incorporated by reference herein is an

investor presentation, dated November 2023 (“Investor Presentation”), that will be used by CCVII, CorpAcq

Group and CorpAcq with respect to the Transactions.

Additional Information and Where to Find It

This current report on Form 8-K (this "Current Report") does

not contain all the information that should be considered concerning the Transactions and is not intended to form the basis of any investment

decision or any other decision in respect of the Transactions. CorpAcq Group has filed the Registration Statement with the SEC, which

includes a proxy statement/prospectus to be distributed to CCVII’s shareholders and warrantholders in connection with CCVII’s

solicitation for proxies for the vote by CCVII’s shareholders and warrantholders in connection with the Transactions and other matters

described in the Registration Statement, as well as the prospectus relating to the offer of the securities to be issued by CorpAcq Group

to CCVII’s shareholders and warrantholders in connection with the completion of the Transactions. Before making any voting or other

investment decisions, CCVII’s shareholders and warrantholders and other interested persons are advised to read the Registration

Statement and any amendments thereto and, once available, the definitive proxy statement/prospectus, in connection with CCVII’s

solicitation of proxies for its special meeting of shareholders and its special meeting of warrantholders to be held to approve, among

other things, the Transactions, as well as other documents filed with the SEC by CCVII or CorpAcq Group in connection with the Transactions,

as these documents will contain important information about CorpAcq, CorpAcq Group, CCVII and the Transactions. After the Registration

Statement has been declared effective, Churchill VII will mail a definitive proxy statement/prospectus and other relevant documents to

its shareholders and warrantholders as of the record date established for voting on the Transactions. Shareholders and warrantholders

may also obtain a copy of the Registration or definitive proxy statement/prospectus, once available, as well as other documents filed

by CCVII with the SEC, without charge, at the SEC’s website located at www.sec.gov or by directing a written request to Churchill

Capital Corp VII at 640 Fifth Avenue, 12th Floor, New York, NY 10019.

Forward-Looking Statements

This Current Report includes “forward looking

statements” within the meaning of the “safe harbor” provisions of the United States Private Securities Litigation

Reform Act of 1995. Forward looking statements may be identified by the use of words such as “estimate,”

“plan,” “project,” “forecast,” “intend,” “will,” “expect,”

“anticipate,” “believe,” “seek,” “target,” “continue,”

“could,” “may,” “might,” “possible,” “potential,” “predict”

or other similar expressions that predict or indicate future events or trends or that are not statements of historical matters.

CCVII and CorpAcq have based these forward looking statements on each of its current expectations and projections about future

events. These forward looking statements include, but are not limited to, statements regarding estimates and forecasts of financial

and operational metrics. These statements are based on various assumptions, whether or not identified in this Current Report, and on

the current expectations of CorpAcq’s and CCVII’s respective management teams and are not predictions of actual

performance. Nothing in this Current Report should be regarded as a representation by any person that the forward looking statements

set forth herein will be achieved or that any of the contemplated results of such forward looking statements will be achieved. These

forward looking statements are provided for illustrative purposes only and are not intended to serve as and must not be relied on by

any investor as, a guarantee, an assurance, a prediction or a definitive statement of fact or probability. Actual events and

circumstances are difficult or impossible to predict and may materially differ from assumptions. Many actual events and

circumstances are beyond the control of CCVII and CorpAcq. These forward looking statements are subject to known and unknown risks,

uncertainties and assumptions about CCVII and CorpAcq that may cause each of its actual results, levels of activity, performance or

achievements to be materially different from any future results, levels of activity, performance or achievements expressed or

implied by such forward looking statements. Such risks and uncertainties include changes in domestic and foreign business changes in

the competitive environment in which CorpAcq operates; CorpAcq's ability to manage its growth prospects, meet its operational and

financial targets, and execute its strategy; the impact of any economic disruptions, decreased market demand and other macroeconomic

factors, including the effect of the a global pandemic, to CorpAcq's business, projected results of operations, financial

performance or other financial metrics; expectations as to future growth in demand for CorpAcq's products and services; CorpAcq's

reliance on its senior management team and key employees; risks related to liquidity, capital resources and capital expenditures;

failure to comply with applicable laws and regulations or changes in the regulatory environment in which CorpAcq operates; the

outcome of any potential litigation, government and regulatory proceedings, investigations and inquiries that CorpAcq may face;

assumptions or analyses used for CorpAcq's forecasts proving to be incorrect and causing its actual operating and financial results

to be significantly below its forecasts; CorpAcq failing to maintain its current level of acquisitions or an acquisition not

occurring as planned and negatively affecting operating results; the inability of the parties to successfully or timely consummate

the Transactions, including the risk that any required regulatory approvals are not obtained, are delayed or are subject to

unanticipated conditions that could adversely affect the CorpAcq Group or the expected benefits of the Transactions or that the

approval of the shareholders of CCVII is not obtained; the risk that shareholders of CCVII could elect to have their shares redeemed

by CCVII, thus leaving the CorpAcq Group insufficient cash to complete the Transactions or grow its business; the outcome of any

legal proceedings that may be instituted against CorpAcq or CCVII; failure to realize the anticipated benefits of the Transactions;

risks relating to the uncertainty of the projected financial information with respect to CorpAcq; the effects of competition;

changes in applicable laws or regulations; the ability of CorpAcq to manage expenses and recruit and retain key employees; the

ability of CCVII or the CorpAcq Group to issue equity or equity linked securities in connection with the Transactions or in the

future; the outcome of any potential litigation, government and regulatory proceedings, investigations and inquiries; the potential

U.S. government shutdown; the impact of certain geopolitical events, including wars in Ukraine and the surrounding region and between Israel and Hamas; the impact of a current or future pandemic on CorpAcq, CCVII, the CorpAcq Group’s projected results of

operations, financial performance or other financial metrics, or on any of the foregoing risks; those factors discussed under the

heading “Risk Factors” in the Registration Statement, 2023, as may be amended from time to time, and other documents

filed, or to be filed, with the SEC by CCVII or CorpAcq Group. If any of these risks materialize or CorpAcq’s, CorpAcq

Group’s or CCVII’s assumptions prove incorrect, actual results could differ materially from the results implied by these

forward looking statements. There may be additional risks that neither CorpAcq, CorpAcq Group nor CCVII presently know or that

CorpAcq, CorpAcq Group and CCVII currently believe are immaterial that could also cause actual results to differ materially from

those contained in the forward looking statements. In addition, forward looking statements reflect CorpAcq’s, CorpAcq

Group’s and CCVII’s expectations, plans or forecasts of future events and views as of the date of this Current Report.

CorpAcq, CorpAcq Group and CCVII anticipate that subsequent events and developments will cause CorpAcq’s, CorpAcq

Group’s and CCVII’s assessments to change. However, while CorpAcq, CorpAcq Group and CCVII may elect to update these

forward looking statements at some point in the future, CorpAcq, CorpAcq Group and CCVII specifically disclaim any obligation to do

so. These forward looking statements should not be relied upon as representing CorpAcq’s, CorpAcq Group’s and

CCVII’s assessments as of any date subsequent to the date of this Current Report. Accordingly, undue reliance should not be

placed upon the forward looking statements. An investment in CorpAcq, CorpAcq Group or CCVII is not an investment in any of

CorpAcq’s, CorpAcq Group’s or CCVII’s founders’ or sponsors’ past investments or companies or any

funds affiliated with any of the foregoing. The historical results of these investments are not indicative of future performance of

CorpAcq, CorpAcq Group or CCVII, which may differ materially from the performance of past investments, companies or affiliated

funds.

No Offer or Solicitation

This Current Report does not constitute an offer to sell or the solicitation

of an offer to buy any securities, or a solicitation of any vote or approval, nor shall there be any sale of securities in any jurisdiction

in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such

jurisdiction. This Current Report is not, and under no circumstances is to be construed as, a proxy statement or solicitation of a proxy,

a prospectus, an advertisement or a public offering of the securities described herein in the United States or any other jurisdiction.

No offer of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the Securities Act of 1933,

as amended, or exemptions therefrom. INVESTMENT IN ANY SECURITIES DESCRIBED HEREIN HAS NOT BEEN APPROVED BY THE SEC OR ANY OTHER REGULATORY

AUTHORITY NOR HAS ANY AUTHORITY PASSED UPON OR ENDORSED THE MERITS OF THE OFFERING OR THE ACCURACY OR ADEQUACY OF THE INFORMATION CONTAINED

HEREIN. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

Participants in the Solicitation

CorpAcq, CorpAcq Group, CCVII, Churchill Sponsor VII LLC and

their respective directors and executive officers may be deemed participants in the solicitation of proxies from CCVII’s

shareholders and warrantholders with respect to the Transactions. A list of the names of CCVII’s directors and executive

officers and a description of their interests in CCVII is set forth in CCVII’s filings with the SEC (including the

Registration Statement and Annual Reports and Quarterly Reports filed by CCVII with the SEC on Forms 10-K and 10-Q, respectively and

any other documents filed in connection with the Transactions) and are available free of charge at the SEC’s website located

at www.sec.gov, or by directing a written request to Churchill Capital Corp VII at 640 Fifth Avenue, 12th Floor, New York, NY 10019.

Additional information regarding the participants in the proxy solicitation and a description of their direct and indirect interests

will be included in the definitive proxy statement/prospectus when it becomes available. Shareholders, potential investors and other

interested persons should read each of the Registration Statement, and the definitive proxy statement/prospectus carefully when it

becomes available before making any voting or investment decisions. You may obtain free copies of these documents from the sources

indicated above.

| Item 9.01 |

Financial Statements and Exhibits |

(d) Exhibits

SIGNATURE

Pursuant to the requirements of the Securities

Exchange Act of 1934, the registrant has duly caused this Current Report to be signed on its behalf by the undersigned hereunto duly authorized.

Dated: November 17, 2023

| |

Churchill Capital Corp VII |

| |

|

| |

By: |

/s/ Jay Taragin |

| |

|

Name: |

Jay Taragin |

| |

|

Title: |

Chief Financial Officer |

Exhibit 99.1

CorpAcq and Churchill Capital Corp VII Announce

Filing of Registration Statement on Form F-4 in Connection with Proposed Business Combination and CorpAcq’s First Half 2023 Results

ALTRINCHAM, England and NEW YORK, November 17, 2023 – CorpAcq

Holdings Limited ("CorpAcq"), a corporate compounder with a proven track record of acquiring and supporting founder-led businesses,

Churchill Capital Corp VII ("Churchill VII") (NYSE: CVII), a special purpose acquisition company, and CorpAcq Group Plc, a public

limited company incorporated under the laws of England and Wales ("CorpAcq Group"), announced today the filing of a registration

statement of CorpAcq Group on Form F-4 (the "Registration Statement") with the U.S. Securities and Exchange Commission (the

“SEC”) on November 17, 2023.

The Registration Statement contains a proxy statement/prospectus in

connection with the definitive agreement entered into between Churchill VII, CorpAcq and CorpAcq Group with respect to the proposed business

combination (the “Merger Agreement”, and the transactions contemplated thereby, the “Transactions”). While the

Registration Statement has not yet become effective and the information contained therein is subject to change, it provides important

information about CorpAcq, CorpAcq Group, Churchill VII and the Transactions.

As announced on August 1, 2023, CorpAcq intends to go public

through a business combination with Churchill VII. Upon closing, CorpAcq Group will be a publicly traded corporate compounder with a

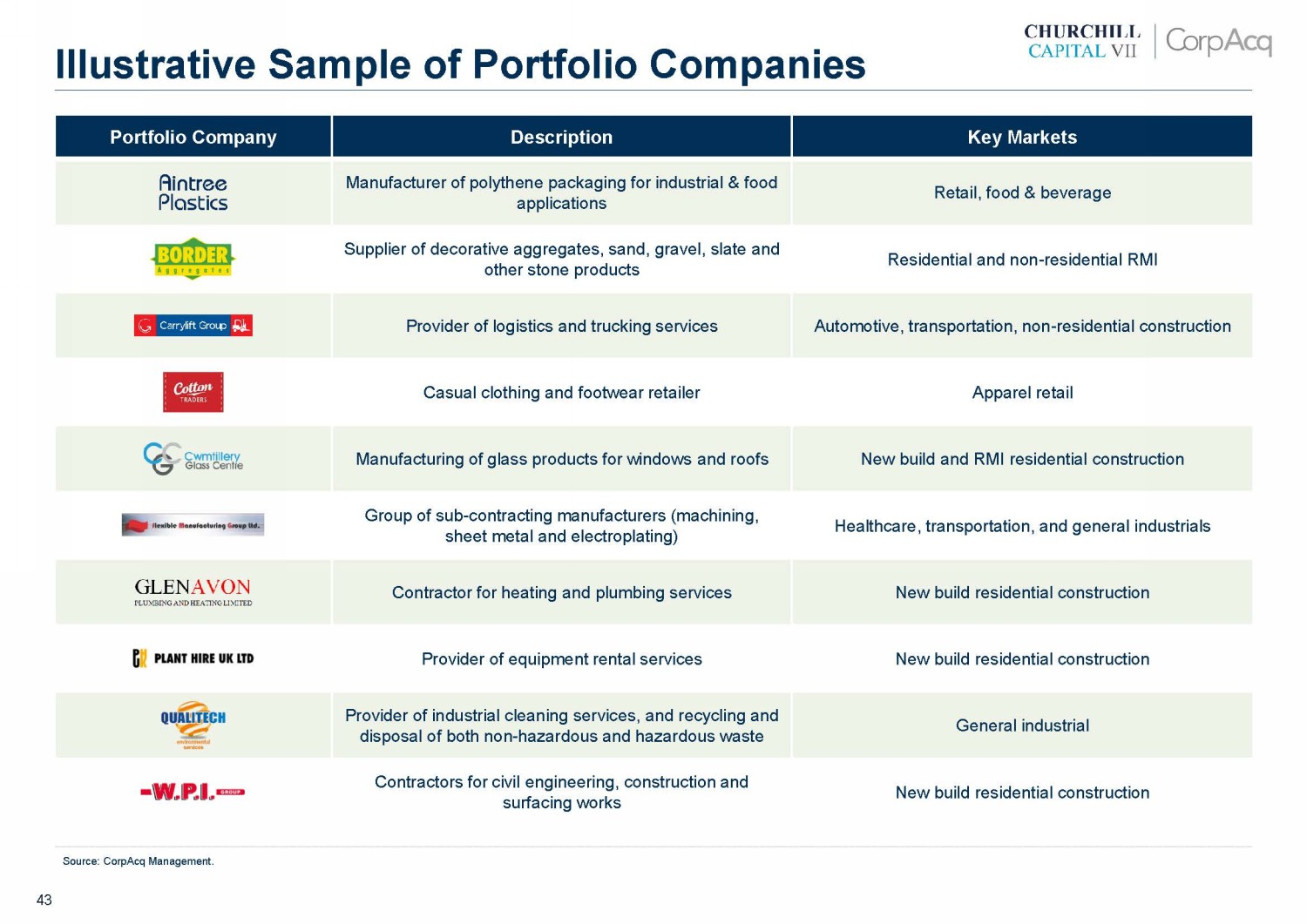

portfolio of 42 businesses (as of September 30, 2023) that have strong asset bases, operate in resilient industries with high barriers

to entry, and generate strong growth and free cash flow.

The Transactions, which have been approved by the Boards of Directors

of CorpAcq and Churchill VII, are expected to close in early 2024 and is subject to approval by Churchill VII's shareholders, the Registration

Statement being declared effective by the SEC, Churchill VII having available cash at closing of at least $350 million, net of transaction

fees, and other customary closing conditions. Upon completion of the Transactions, the combined company will operate as CorpAcq Group

Plc and is expected to be listed on the New York Stock Exchange under the ticker “CPGR”.

In addition, CorpAcq’s performance in the first six months of

2023 has been strong, with organic revenue growth of approximately 9% and organic adjusted EBITDA growth of approximately 11%. For the

six months ended June 30, 2023, CorpAcq had total revenues and adjusted EBITDA of approximately £341.6 million and £60.6 million,

respectively. Further information on CorpAcq’s financial performance for the first six months of 2023 is available in the Registration

Statement.

UBS Investment Bank is serving as financial advisor to CorpAcq. Citigroup

Global Markets Inc. is serving as capital markets advisor to Churchill VII. Reed Smith LLP is serving as legal counsel to CorpAcq. Weil,

Gotshal & Manges LLP is serving as legal counsel to Churchill VII.

About CorpAcq Holdings Limited

CorpAcq is a corporate compounder founded in 2006 with deep commercial

experience and a diversified portfolio of 42 companies (as of September 30, 2023) across multiple large industries. CorpAcq has a track

record of unlocking business potential and long-term growth for small and medium-sized enterprises through its established M&A playbook

and decentralized operational approach. CorpAcq's executive team develops close relationships with their subsidiaries’

management to support them with financial and strategic expertise while allowing them to retain independence to continue to operate their

business successfully. CorpAcq is headquartered in the United Kingdom.

About Churchill Capital Corp VII

Churchill Capital Corp VII was formed for the purpose of effecting

a merger, capital stock exchange, asset acquisition, stock purchase, reorganization or similar business combination with one or more businesses.

Important Notices Relating to Financial Advisors

UBS AG London Branch ("UBS") is authorized and regulated

by the Financial Market Supervisory Authority in Switzerland. It is authorized by the PRA and subject to regulation by the FCA and limited

regulation by the PRA in the United Kingdom. UBS provided financial advice to CorpAcq and no one else in connection with the process or

contents of this announcement. In connection with such matters, UBS will not regard any other person as its client, nor will it be responsible

to any other person for providing the protections afforded to its clients or for providing advice in relation to the process, contents

of this announcement or any other matter referred to herein.

Forward-Looking Statements

This communication includes “forward-looking statements”

within the meaning of the “safe harbor” provisions of the United States Private Securities Litigation Reform Act of 1995.

Forward-looking statements may be identified by the use of words such as “estimate,” “plan,” “project,”

“forecast,” “intend,” “will,” “expect,” “anticipate,” “believe,”

“seek,” “target,” “continue,” “could,” “may,” “might,” “possible,”

“potential,” “predict” or other similar expressions that predict or indicate future events or trends or that are

not statements of historical matters. Churchill VII and CorpAcq have based these forward-looking statements on each of its current expectations

and projections about future events. These forward-looking statements include, but are not limited to, statements regarding estimates

and forecasts of financial and operational metrics. These statements are based on various assumptions, whether or not identified in this

communication, and on the current expectations of CorpAcq’s and Churchill VII’s respective management teams and are not predictions

of actual performance. Nothing in this communication should be regarded as a representation by any person that the forward-looking statements

set forth herein will be achieved or that any of the contemplated results of such forward-looking statements will be achieved. These forward-looking

statements are provided for illustrative purposes only and are not intended to serve as and must not be relied on by any investor as,

a guarantee, an assurance, a prediction or a definitive statement of fact or probability. Actual events and circumstances are difficult

or impossible to predict and may materially differ from assumptions. Many actual events and circumstances are beyond the control of Churchill

VII and CorpAcq. These forward-looking statements are subject to known and unknown risks, uncertainties and assumptions about Churchill

VII and CorpAcq that may cause each of its actual results, levels of activity, performance or achievements to be materially different

from any future results, levels of activity, performance or achievements expressed or implied by such forward-looking statements. Such

risks and uncertainties include changes in domestic and foreign business changes in the competitive environment in which CorpAcq operates;

CorpAcq's ability to manage its growth prospects, meet its operational and financial targets, and execute its strategy; the impact of

any economic disruptions, decreased market demand and other macroeconomic factors, including the effect of a global pandemic, to CorpAcq's

business, projected results of operations, financial performance or other financial metrics; CorpAcq's reliance on its senior management

team and key employees; risks related to liquidity, capital resources and capital expenditures; failure to comply with applicable laws

and regulations or changes in the regulatory environment in which CorpAcq operates; the outcome of any potential litigation, government

and regulatory proceedings, investigations and inquiries that CorpAcq may face; assumptions or analyses used for CorpAcq's forecasts proving

to be incorrect and causing its actual operating and financial results to be significantly below its forecasts; CorpAcq failing to maintain

its current level of acquisitions or an acquisition not occurring as planned and negatively affecting operating results; the inability

of the parties to successfully or timely consummate the Transactions, including the risk that any required regulatory approvals are not

obtained, are delayed or are subject to unanticipated conditions that could adversely affect CorpAcq Group, which will be the combined

company upon closing of the Transactions, or the expected benefits of the Transactions or that the approval of the shareholders of Churchill

VII is not obtained; the risk that shareholders of Churchill VII could elect to have their shares redeemed by Churchill VII, thus leaving

CorpAcq Group insufficient cash to complete the Transactions or grow its business; the outcome of any legal proceedings that may be instituted

against CorpAcq or Churchill VII; failure to realize the anticipated benefits of the Transactions; risks relating to the uncertainty of

the projected financial information with respect to CorpAcq; the effects of competition; changes in applicable laws or regulations; the

ability of CorpAcq to manage expenses and recruit and retain key employees; the ability of Churchill VII or CorpAcq Group to issue equity

or equity linked securities in connection with the Transactions or in the future; the outcome of any potential litigation, government

and regulatory proceedings, investigations and inquiries; a potential U.S. government shutdown; the impact of certain geopolitical events,

including wars in Ukraine and the surrounding region and the Middle East; the impact of a current or future pandemic on CorpAcq, Churchill

VII or CorpAcq Group's projected results of operations, financial performance or other financial metrics, or on any of the foregoing risks;

those factors discussed in under the heading “Risk Factors” in the Registration Statement, as may be amended from time to

time, and other documents filed, or to be filed, with the SEC by Churchill VII or CorpAcq Group. If any of these risks materialize or

CorpAcq’s or Churchill VII’s assumptions prove incorrect, actual results could differ materially from the results implied

by these forward-looking statements. There may be additional risks that neither CorpAcq nor Churchill VII presently know or that CorpAcq

and Churchill VII currently believe are immaterial that could also cause actual results to differ materially from those contained in the

forward-looking statements. In addition, forward-looking statements reflect CorpAcq’s and Churchill VII’s expectations, plans

or forecasts of future events and views as of the date of this communication. CorpAcq and Churchill VII anticipate that subsequent events

and developments will cause CorpAcq’s and Churchill VII’s assessments to change. However, while CorpAcq and Churchill VII

may elect to update these forward-looking statements at some point in the future, CorpAcq and Churchill VII specifically disclaim any

obligation to do so. These forward-looking statements should not be relied upon as representing CorpAcq and Churchill VII’s assessments

as of any date subsequent to the date of this communication. Accordingly, undue reliance should not be placed upon the forward-looking

statements. An investment in CorpAcq, CorpAcq Group, or Churchill VII is not an investment in any of CorpAcq’s, CorpAcq Group's,

or Churchill VII’s respective founders’ or sponsors’ past investments or companies or any funds affiliated with any

of the foregoing. The historical results of these investments are not indicative of future performance of CorpAcq, CorpAcq Group, or Churchill

VII, which may differ materially from the performance of past investments, companies or affiliated funds.

Non-GAAP Financial Measures

This communication includes certain financial measures not presented

in accordance with UK GAAP or IFRS including, but not limited to, Adjusted EBITDA, Free Cash Flow, EBITDA Margin, ROIC and certain ratios

and other metrics derived therefrom. These non-GAAP financial measures are not measures of financial performance in accordance with UK

GAAP, or IFRS or any other GAAP and may exclude items that are significant in understanding and assessing CorpAcq’s financial results.

Therefore, these measures should not be considered in isolation or as an alternative to net income, cash flows from operations or other

measures of profitability, liquidity or performance under UK GAAP, IFRS, or any other GAAP. You should be aware that CorpAcq’s presentation

of these measures may not be comparable to similarly-titled measures used by other companies.

CorpAcq believes these non-GAAP measures of financial results provide

useful information to management and investors regarding certain financial and business trends relating to CorpAcq’s financial condition

and results of operations. CorpAcq believes that the use of these non-GAAP financial measures provides an additional tool for investors

to use in evaluating ongoing operating results and trends and in comparing CorpAcq’s financial measures with other similar companies,

many of which present similar non-GAAP financial measures to investors. These non-GAAP measures are subject to inherent limitations as

they reflect the exercise of judgments by management about which expense and income are excluded or included in determining these non-GAAP

financial measures.

Additional Information and Where to Find It

This communication does not contain all the information that should

be considered concerning the Transactions and is not intended to form the basis of any investment decision or any other decision in respect

of the Transactions.

The Registration Statement includes a proxy statement/prospectus to

be distributed to Churchill VII’s shareholders and warrantholders in connection with Churchill VII’s solicitation for proxies

for the vote by Churchill VII’s shareholders and warrantholders in connection with the Transactions and other matters described

in the Registration Statement, as well as the prospectus relating to the offer of the securities to be issued by CorpAcq Group to Churchill’s

shareholders and warrantholders in connection with the completion of the Transactions. Before making any voting or other investment decisions,

Churchill VII’s shareholders and warrantholders and other interested persons are advised to read the Registration Statement and

any amendments thereto and, once available, the definitive proxy statement/prospectus, in connection with Churchill VII’s solicitation

of proxies for its special meeting of shareholders and its special meeting of warrantholders to be held to approve, among other things,

the Transactions, as well as other documents filed with the SEC by Churchill VII or CorpAcq Group in connection with the Transactions,

as these documents will contain important information about CorpAcq, CorpAcq Group, Churchill VII and the Transactions. After the Registration

Statement has been declared effective, Churchill VII will mail a definitive proxy statement/prospectus and other relevant documents to

its shareholders and warrantholders as of the record date established for voting on the proposed transaction. Shareholders and warrantholders

may also obtain a copy of the Registration Statement or definitive proxy statement/prospectus, once available, as well as other documents

filed by Churchill VII with the SEC, without charge, at the SEC’s website located at www.sec.gov or by directing a written request

to Churchill Capital Corp VII at 640 Fifth Avenue, 12th Floor, New York, NY 10019.

Participants in the Solicitation

CorpAcq, CorpAcq Group, Churchill VII, Churchill Sponsor VII LLC and

their respective directors and executive officers may be deemed participants in the solicitation of proxies from Churchill VII’s

shareholders and warrantholders with respect to the Transactions and other matters described in the Registration Statement. A list of

the names of Churchill VII’s directors and executive officers and a description of their interests in Churchill VII is set forth

in Churchill VII’s filings with the SEC (including the Registration Statement and Annual Reports and Quarterly Reports filed by

Churchill VII with the SEC on Forms 10-K and 10-Q, respectively) and are available free of charge at the SEC’s website located at

www.sec.gov, or by directing a written request to Churchill Capital Corp VII at 640 Fifth Avenue, 12th Floor, New York, NY 10019. Additional

information regarding the participants in the proxy solicitation and a description of their direct and indirect interests will be included

in the definitive proxy statement/prospectus when it becomes available. Shareholders, potential investors and other interested persons

should read the definitive proxy statement/prospectus carefully when it becomes available before making any voting or investment decisions.

You may obtain free copies of these documents from the sources indicated above.

No Offer or Solicitation

This communication does not constitute an offer to sell or the solicitation

of an offer to buy any securities, or a solicitation of any vote or approval, nor shall there be any sale of securities in any jurisdiction

in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such

jurisdiction. This communication is not, and under no circumstances is to be construed as, a proxy statement or solicitation of a proxy,

a prospectus, an advertisement or a public offering of the securities described herein in the United States or any other jurisdiction.

No offer of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the Securities Act of 1933,

as amended, or exemptions therefrom. INVESTMENT IN ANY SECURITIES DESCRIBED HEREIN HAS NOT BEEN APPROVED BY THE SEC OR ANY OTHER REGULATORY

AUTHORITY NOR HAS ANY AUTHORITY PASSED UPON OR ENDORSED THE MERITS OF THE OFFERING OR THE ACCURACY OR ADEQUACY OF THE INFORMATION CONTAINED

HEREIN. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

Media Contact

Christina Stenson / Michael Landau

Gladstone Place Partners

(212) 230-5930

Exhibit 99.2

November 2023 Investor Presentation

2 About This Presentation This presentation is provided

for informational purposes only and has been prepared to assist interested parties in making their own evaluation with respect to a proposed

business combination (together with the related transactions, the “proposed transaction”) between CorpAcq Holdings Limited

(“ CorpAcq ”) and Churchill Capital Corp VII (“Churchill”) . The information contained herein does not purport

to be all inclusive and no representations or warranties, express or implied, are given in, or in respect of, this presentation or any

other written or oral communication communicated to the recipient in the course of the recipient’s evaluation of CorpAcq and Churchill

and their respective affiliates . The information contained in this presentation is preliminary in nature and is subject to change, and

any such changes may be material . This presentation does not constitute ( i ) a solicitation of a proxy, consent or authorization with

respect to any securities or in respect of the proposed transaction or (ii) an offer to sell, a solicitation of an offer to buy, or a

recommendation to purchase any security of Churchill, CorpAcq, or any of their respective affiliates . You should not construe the contents

of this presentation as legal, tax, accounting or investment advice or a recommendation . You should consult your own counsel and tax

and financial advisors as to legal and related matters concerning the matters described herein, and, by accepting this presentation,

you confirm that you are not relying upon the information contained herein to make any decision . The recipient shall not rely upon any

statement, representation or warranty made by any other person, firm or corporation in making its investment or decision to invest in

CorpAcq or Churchill or their respective affiliates . To the fullest extent permitted by law, in no circumstances will CorpAcq, Churchill

or any of their respective subsidiaries, interest holders, affiliates, representatives, partners, directors, officers, employees, advisers

or agents be responsible or liable for any direct, indirect or consequential loss or loss of profit arising from the use of this presentation,

its contents, its omissions, reliance on the information contained within it, or on opinions communicated in relation thereto or otherwise

arising in connection therewith . In addition, this presentation does not purport to be all - inclusive or to contain all of the information

that may be required to make a full analysis of CorpAcq, Churchill or the proposed transaction . Please refer to the definitive merger

agreement and other related transaction documents, when available, for the full terms of the proposed transaction . The general explanations

included in this presentation cannot address, and are not intended to address, your specific investment objectives, financial situations

or financial needs . The distribution of this presentation may also be restricted by law and persons into whose possession this presentation

comes should inform themselves about and observe any such restrictions . The recipient acknowledges that it is (a) aware that the United

States securities laws prohibit any person who has material, non - public information concerning a company from purchasing or selling

securities of such company or from communicating such information to any other person under circumstances in which it is reasonably foreseeable

that such person is likely to purchase or sell such securities, and (b) familiar with the United States Securities Exchange Act of 1934

, as amended, and the rules and regulations promulgated thereunder (collectively, the “Exchange Act”), and that the recipient

will neither use, nor cause any third party to use, this presentation or any information contained herein in contravention of the Exchange

Act, including, without limitation, Rule 10 b - 5 thereunder . Forward Looking Statements This presentation includes “forward looking

statements” within the meaning of the “safe harbor” provisions of the United States Private Securities Litigation Reform

Act of 1995 . Forward looking statements may be identified by the use of words such as “estimate,” “plan,” “project,”

“forecast,” “intend,” “will,” “expect,” “anticipate,” “believe,”

“seek,” “target,” “continue,” “could,” “may,” “might,” “possible,”

“potential,” “predict” or other similar expressions that predict or indicate future events or trends or that

are not statements of historical matters . Churchill and CorpAcq have based these forward looking statements on each of its current expectations

and projections about future events . These forward looking statements include, but are not limited to, statements regarding estimates

and forecasts of financial and operational metrics . These statements are based on various assumptions, whether or not identified in

this presentation, and on the current expectations of CorpAcq’s and Churchill’s respective management teams and are not predictions

of actual performance . Nothing in this presentation should be regarded as a representation by any person that the forward looking statements

set forth herein will be achieved or that any of the contemplated results of such forward looking statements will be achieved . These

forward looking statements are provided for illustrative purposes only and are not intended to serve as and must not be relied on by

any investor as, a guarantee, an assurance, a prediction or a definitive statement of fact or probability . Actual events and circumstances

are difficult or impossible to predict and may materially differ from assumptions . Many actual events and circumstances are beyond the

control of Churchill and CorpAcq . These forward looking statements are subject to known and unknown risks, uncertainties and assumptions

about Churchill and CorpAcq that may cause each of its actual results, levels of activity, performance or achievements to be materially

different from any future results, levels of activity, performance or achievements expressed or implied by such forward looking statements

.. Such risks and uncertainties include changes in domestic and foreign business changes in the competitive environment in which CorpAcq

operates ; CorpAcq's ability to manage its growth prospects, meet its operational and financial targets, and execute its strategy ; the

impact of any economic disruptions, decreased market demand and other macroeconomic factors, including the effect of a global pandemic,

to CorpAcq's business, projected results of operations, financial performance or other financial metrics ; expectations as to future

growth in demand for CorpAcq's products and services ; CorpAcq's reliance on its senior management team and key employees ; risks related

to liquidity, capital resources and capital expenditures ; failure to comply with applicable laws and regulations or changes in the regulatory

environment in which CorpAcq operates ; the outcome of any potential litigation, government and regulatory proceedings, investigations

and inquiries that CorpAcq may face ; assumptions or analyses used for CorpAcq's forecasts proving to be incorrect and causing its actual

operating and financial results to be significantly below its forecasts ; CorpAcq failing to maintain its current level of acquisitions

or an acquisition not occurring as planned and negatively affecting operating results ; the inability of the parties to successfully

or timely consummate the proposed transaction, including the risk that any required regulatory approvals are not obtained, are delayed

or are subject to unanticipated conditions that could adversely affect CorpAcq Group Plc, (the combined company after the proposed transactions

“CorpAcq Group”), or the expected benefits of the proposed transaction or that the approval of the shareholders of Churchill

is not obtained ; the risk that shareholders of Churchill could elect to have their shares redeemed by Churchill, thus leaving CorpAcq

insufficient cash to complete the proposed transaction or grow its business ; the outcome of any legal proceedings that may be instituted

against CorpAcq or Churchill ; failure to realize the anticipated benefits of the proposed transaction ; risks relating to the uncertainty

of the projected financial information with respect to CorpAcq ; the effects of competition ; changes in applicable laws or regulations

; the ability of CorpAcq to manage expenses and recruit and retain key employees ; the ability of Churchill or CorpAcq Group Plc to issue

equity or equity linked securities in connection with the proposed transaction or in the future ; the outcome of any potential litigation,

government and regulatory proceedings, investigations and inquiries ; the potential U . S . government shutdown ; the impact of certain

geopolitical events, including wars in Ukraine and the surrounding region and between Israel and Hamas ; the impact of a current or future

pandemic or any future pandemic on CorpAcq, Churchill, or the CorpAcq Group Plc’s projected results of operations, financial performance

or other financial metrics, or on any of the foregoing risks ; those factors discussed under the heading “Risk Factors” in

the registration statement on Form F - 4 (the “Registration Statement”) filed by CorpAcq Group Plc on November 17 th , 2023

, as may be amended from time to time, and other documents filed, or to be filed, with the SEC by Churchill or CorpAcq Group Plc . If

any of these risks materialize or CorpAcq’s or Churchill’s assumptions prove incorrect, actual results could differ materially

from the results implied by these forward looking statements . There may be additional risks that neither CorpAcq nor Churchill presently

know or that CorpAcq and Churchill currently believe are immaterial that could also cause actual results to differ materially from those

contained in the forward looking statements . In addition, forward looking statements reflect CorpAcq’s and Churchill’s expectations,

plans or forecasts of future events and views as of the date of this presentation . CorpAcq and Churchill anticipate that subsequent

events and developments will cause CorpAcq’s and Churchill’s assessments to change . However, while CorpAcq and Churchill

may elect to update these forward looking statements at some point in the future, CorpAcq and Churchill specifically disclaim any obligation

to do so . These forward looking statements should not be relied upon as representing CorpAcq and Churchill’s assessments as of

any date subsequent to the date of this presentation . Accordingly, undue reliance should not be placed upon the forward looking statements

.. An investment in CorpAcq or Churchill is not an investment in any of CorpAcq’s or Churchill’s founders’ or sponsors’

past investments or companies or any funds affiliated with any of the foregoing . The historical results of these investments are not

indicative of future performance of CorpAcq or Churchill, which may differ materially from the performance of past investments, companies

or affiliated funds .

3 Financial Information The financial information contained in this presentation has been taken from or prepared based on the historical financial statements of CorpAcq for the periods presented . CorpAcq’s historical financial information prior to 2021 was prepared in accordance with the generally accepted accounting practice in the UK (“UK GAAP”) . Such information has not been audited in accordance with Public Company Accounting Oversight Board (“PCAOB”) standards . Neither Churchill nor CorpAcq can assure you that, had the financial statements been compliant with Regulation S - X under the United States Securities Act of 1933 , as amended (the “Securities Act”), and the regulations of the SEC promulgated thereunder or audited in accordance with PCAOB standards, there would not be differences and such differences could be material . CorpAcq’s financial statements included in the registration statement have been prepared in accordance with IFRS . Furthermore, all financial information of CorpAcq included in this presentation subsequent to June 30 , 2023 is preliminary and unaudited . CorpAcq's independent auditor has not reviewed or performed any procedures on the preliminary, unaudited financial results included in this presentation . Accordingly there may be material differences between the presentation of the financial information included in the presentation and in the registration statement . Certain monetary amounts, percentages and other figures included in this presentation have been subject to rounding adjustments . Certain other amounts that appear in this presentation may not sum due to rounding . Non - GAAP Financial Measures This presentation includes certain financial measures not presented in accordance with UK GAAP or IFRS including, but not limited to, Adjusted EBITDA, Free Cash Flow, EBITDA Margin, ROIC and certain ratios and other metrics derived therefrom . These non - GAAP financial measures are not measures of financial performance in accordance with UK GAAP, or IFRS or any other GAAP and may exclude items that are significant in understanding and assessing CorpAcq’s financial results . Therefore, these measures should not be considered in isolation or as an alternative to net income, cash flows from operations or other measures of profitability, liquidity or performance under UK GAAP, IFRS, or any other GAAP . You should be aware that CorpAcq’s presentation of these measures may not be comparable to similarly - titled measures used by other companies . CorpAcq believes these non - GAAP measures of financial results provide useful information to management and investors regarding certain financial and business trends relating to CorpAcq’s financial condition and results of operations . CorpAcq believes that the use of these non - GAAP financial measures provides an additional tool for investors to use in evaluating ongoing operating results and trends and in comparing CorpAcq’s financial measures with other similar companies, many of which present similar non - GAAP financial measures to investors . These non - GAAP measures are subject to inherent limitations as they reflect the exercise of judgments by management about which expense and income are excluded or included in determining these non - GAAP financial measures . This presentation also includes certain projections of non - GAAP financial measures . Due to the high variability and difficulty in making accurate forecasts and projections of some of the information excluded from these projected measures, together with some of the excluded information not being ascertainable or accessible, CorpAcq is unable to quantify certain amounts that would be required to be included in the most directly comparable GAAP financial measures without unreasonable effort . Consequently, no disclosure of estimated comparable GAAP measures is included and no reconciliation of the forward - looking non - GAAP financial measures is included . Please see the appendix to this presentation for a reconciliation of non - GAAP financial measures used in this presentation to their most directly comparable GAAP metric . Industry and Market Data ; Trademarks This presentation also contains certain statistical data, estimates and forecasts that are based on independent industry publications or other publicly available information, as well as other information based on other third - party or internal sources . This information involves many assumptions and limitations, and you are cautioned not to give undue weight to such information . None of CorpAcq, Churchill or any placement agent has independently verified the accuracy or completeness of the information contained in the industry publications and other publicly available information . Accordingly, none of CorpAcq, Churchill or any placement agent makes any representation as to the accuracy or completeness of that information nor does CorpAcq, Churchill or any placement agent undertake to update such information after the date of this presentation . In addition, this presentation does not purport to be all - inclusive or to contain all of the information that may be required to make a full analysis of CorpAcq or the proposed transaction . You should make your own evaluation of CorpAcq and of the relevance and adequacy of the information and should make such other investigations as you deem necessary . The information contained in the third party citations referenced in this presentation is not incorporated by reference into this presentation . This presentation may contain trademarks, service marks, trade names and copyrights of other companies, which are property of their respective owners . Solely for convenience, some of the trademarks, service marks, trade names and copyrights referred to in this presentation may be listed without the TM, SM, (c) or (r) symbols, but CorpAcq and Churchill will assert, to the fullest extent under applicable law, the right of the applicable owners, if any, to these trademarks, service marks, trade names and copyrights . Additional Information about the Proposed Transaction and Where to Find It This presentation does not contain all the information that should be considered concerning the proposed t ransactions and is not intended to form the basis of any investment decision or any other decision in respect of the proposed transaction . CorpAcq Group Plc has filed the Registration Statement with the SEC, which includes a proxy statement/prospectus to be distributed to Churchill’s shareholders and warrantholders in connection with Churchill’s solicitation for proxies for the vote by Churchill’s shareholders and warrantholders in connection with the proposed transaction and other matters described in the Registration Statement, as well as the prospectus relating to the offer of the securities to be issued by CorpAcq Group Plc to Churchill’s shareholders and warrantholders in connection with the completion of the proposed transaction . Before making any voting or other investment decisions, Churchill’s shareholders and warrantholders and other interested persons are advised to read the Registration Statement and any amendments thereto and, once available, the definitive proxy statement/prospectus, in connection with Churchill’s solicitation of proxies for its special meeting of shareholders and warrantholders to be held to approve, among other things, the proposed transaction, as well as other documents filed with the SEC by Churchill, CorpAcq or CorpAcq Group Plc in connection with the proposed transaction, as these documents will contain important information about CorpAcq, CorpAcq Group Plc, Churchill and the proposed transaction . After the Registration Statement has been declared effective, Churchill will mail a definitive proxy statement/prospectus and other relevant documents to its shareholders and warrantholders as of the record date established for voting on the proposed transaction . Churchill’s shareholders and warrantholders may also obtain a copy of the Registration Statement or definitive proxy statement/prospectus, once available, as well as other documents filed by Churchill with the SEC, without charge, at the SEC’s website located at www . sec . gov or by directing a written request to Churchill Capital Corp VII at 640 Fifth Avenue, 12 th Floor, New York, NY 10019 . About This Presentation

4 Participants in the Solicitation CorpAcq, CorpAcq Group Plc, Churchill, Churchill Sponsor VII LLC and their directors and executive officers may be deemed participants in the solicitation of proxies from Churchill’s shareholders and warrantholders with respect to the proposed transaction . A list of the names of Churchill’s directors and executive officers and a description of their interests in Churchill is set forth in Churchill’s filings with the SEC (including the Registration Statement and Annual Reports and Quarterly Reports filed by Churchill with the SEC on Forms 10 - K and 10 - Q, respectively and any other documents filed in connection with the proposed transaction) and are available free of charge at the SEC’s website located at www . sec . gov, or by directing a written request to Churchill Capital Corp VII at 640 Fifth Avenue, 12 th Floor, New York, NY 10019 . Additional information regarding the participants in the proxy solicitation and a description of their direct and indirect interests will be included in the definitive proxy statement/prospectus when it becomes available . Shareholders, potential investors and other interested persons should read each of the Registration Statement, and the definitive proxy statement/prospectus carefully when it becomes available before making any voting or investment decisions . You may obtain free copies of these documents from the sources indicated above . No Offer or Solicitation This presentation does not constitute an offer to sell or the solicitation of an offer to buy any securities, or a solicitation of any vote or approval, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction . This presentation is not, and under no circumstances is to be construed as, a proxy statement or solicitation of a proxy, a prospectus, an advertisement or a public offering of the securities described herein in the United States or any other jurisdiction . No offer of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the Securities Act of 1933 , as amended, or exemptions therefrom . INVESTMENT IN ANY SECURITIES DESCRIBED HEREIN HAS NOT BEEN APPROVED BY THE SEC OR ANY OTHER REGULATORY AUTHORITY NOR HAS ANY AUTHORITY PASSED UPON OR ENDORSED THE MERITS OF THE OFFERING OR THE ACCURACY OR ADEQUACY OF THE INFORMATION CONTAINED HEREIN . ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE . Risk Factors For a non - exhaustive description of certain risks relating to CorpAcq and CorpAcq Group Plc, including its business and operations, and the proposed transaction, we refer you to “Risk Factors” at the end of this presentation . Please also see the section titled “Risk Factors” in the Registration Statement for more information . Use of Projections This presentation contains certain financial forecast information of CorpAcq, including, but not limited to, estimated results for fiscal year 2023 , including Adjusted EBITDA, revenue and gross margin, and the Company's long - term business model . Such financial forecast information constitutes forward - looking information, and is for informational purposes only and should not be relied upon as necessarily being indicative of future results . The assumptions and estimates underlying such financial forecast information are inherently uncertain and are subject to a wide variety of significant business, economic, competitive and other risks and uncertainties . See "Forward - Looking Statements“ above and “Selected Risk Factors” at the end of this presentation . Actual results may differ materially from the results contemplated by the financial forecast information contained in this presentation, and inclusion of such information in this presentation should not be regarded as a representation by any person that the results reflected in such forecasts will be achieved . None of CorpAcq's or Churchill's independent auditors have audited, reviewed, compiled or performed any procedures with respect to the projections for the purpose of their inclusion in this presentation, and, accordingly, neither of them have expressed an opinion or provided any other form of assurance with respect thereto for the purpose of this presentation . In addition, the analyses of the CorpAcq and Churchill contained herein are not, and do not purport to be, appraisals of the securities, assets or business of CorpAcq or Churchill . About This Presentation

5 Simon Orange David Martin Michael Klein • Established CorpAcq in 2006 • Current role includes identifying and negotiating acquisitions in conjunction with CorpAcq partners and driving funding, strategic development and partnership • Has been involved in funding and managing businesses and has overseen the creation and growth of several ventures that have exited successfully • Also a Founder, Investor, and Director of BOL Foods (a company supplying food products to major retailers) • Joined CorpAcq as the Finance Director in 2007 and was appointed as Chief Executive Officer in 2011 • Leads all operational matters for CorpAcq and is actively involved with subsidiary businesses • Has had extensive involvement with the management and financial control of UK manufacturing businesses across numerous sectors • Prior to joining CorpAcq, held a number of key positions within Nestle UK, Frank Roberts & Sons, Volex, and GEC • Founder and CEO of Churchill I - VII which have completed four business combinations to date • Founder and managing partner of M. Klein and Company, which he founded in 2012 • Background in strategic advisory work was built during his 30+ year career, including more than two decades at Citi and its predecessors • Previously CEO of Citi’s institutional businesses, which had aggregate revenues of approximately $20 billion and 65,000 employees • Served as a private advisor to the Government of the United Kingdom in responding to the financial market crisis Founder & Chairman Chief Executive Officer Head of Acquisitions Chairman and CEO CorpAcq Churchill • Joined CorpAcq in 2019 as Acquisitions Manager • Current role includes leading new business origination alongside structuring, negotiating, and executing acquisitions • Began career at Goldman Sachs followed by 11 years at Glencore, ultimately as Head of Sugar Trading Globally • Garnered commercial experience at Glencore managing a global physical and paper trading book as well as leading contract negotiations alongside complementary M&A activities Stuart Kissen Source: CorpAcq and Churchill Capital Corp VII Management. Today’s Presenters

6 1 2 3 4 5 6 CorpAcq to go public via a business combination with Churchill Capital Corp VII (NYSE: CVII) in a transaction anticipated to create a differentiated acquisition platform that offers a compelling combination of earnings growth and attractive risk - adjusted returns with a valuation of approximately 10x 2023E Adjusted EBITDA CorpAcq is a corporate compounder anchored by a diversified portfolio of 42 (1) small - to - medium sized enterprises (“SMEs”) (2) within the UK that has stable and profitable asset - rich businesses which from 2018 - 2022 delivered organic subsidiary - level Adj. EBITDA growth (3) of 7% and total Adj. EBITDA (4) growth of 17%, with 15% year - over - year Adj. EBITDA growth in 1H’23 In partnership with Churchill Capital Corp VII, CorpAcq expects to be able to accelerate its successful platform strategy by increasing its capital deployment and acquisition pace Since 2006, CorpAcq has developed a track record as a “preferred buyer” for well - established, founder - led SMEs across the UK by maintaining autonomy within the businesses and investing for long - term performance This attractive transaction structure aligns interests between CorpAcq’s management team and shareholders of the post - closing combined company and offers the potential opportunity for the newly public company to pay a regular dividend from closing at an intended yield of approximately 4% at current valuation Business combination is expected to close in early 2024 resulting in the opportunity for Churchill Capital Corp VII investors to become CorpAcq shareholders (1) As of 9/30/2023. (2) SME defined by CorpAcq as business with 10 - 249 employees. (3 ) Organic growth is calculated as the aggregate growth of s ubsidiary - level Adj. EBITDA of subsidiaries that have been in the portfolio for the entirety of the compared periods. Subsidiary - level Adj. EBITDA is measured as net profit before interest, tax, depreciation and amortization and excludes management fees to CorpAcq. Management fees are fixed amounts charged by CorpAcq Limited to its subsidiaries for general corporate services. Subsidiary - level Adj. EBITDA growth figures are based on UK GAAP audits and have no t been audited in accordance with PCAOB standards. (4) See appendix for definition of Adj. EBITDA and reconciliation to its most directly comparable GAAP metric. (5) Assumes sponsor to forfeit 15mm founder shares and unvest 7.4mm and 4.7mm founder shares at close that are subject to vesting share prices at or above $11.50 per share and $15.00 per share, respectively. 7 Strong shareholder alignment as sponsors are expected to forfeit and unvest more than 75% (5) of founder shares on day one with additional revesting and earn - in hurdles significantly above deal price CorpAcq to Go Public in Partnership With Churchill Capital VII

7 A diversified platform underpinned by a foundation of proven assets and supplemented by an acquisition engine that is expecte d t o drive shareholder returns Current Key Company Statistics (1) CorpAcq Engine For Value Creation Acquisition Engine Stable, Cash - Generative Companies Consistent and Accretive Acquisition Engine ~$25mm+ EBITDA acquired per year Stable Retained proven management team Profitable with ~15% EBITDA margin Accretive with +20% (2) returns on investment Source: CorpAcq Management. Note: Financials based on IFRS audits . LTM financials as of 6/30/2023. Assumes USD:GBP exchange ratio of 1.286:1 (5 - day vwap from time of merger announcement on 8/1/2023) (1) Company statistics are as of 9/30/2023. (2) Returns on investment for acquisitions are defined as operating income minus tax, interest and debt service divided by CorpAcq’s cash in ves tment. Return metrics for target acquisition are based on seven of CorpAcq’s recently completed acquisitions between 2019 - 2023. (3) CorpAcq sold 3 businesses (Regency, Vista, M&S) for more than 10x total cash invested. Acquisition Targets Self Funding Alcentra Capital / Asset Finance Goldman Sachs Pref Go Public CorpAcq’s Funding Path 42 Total Subsidiaries ~$860mm LTM Revenue >3.5k Total Employees Across Subsidiaries >30 years Average Age of Subsidiaries >6 Average Number of Years in Portfolio Across Subsidiaries 46 Companies acquired 3 Sold at strong returns (3) 4 Management changes The CorpAcq Platform

8CorpAcq'sAcquisition Structure Focuses onLowering Risk and Driving ReturnsCorpAcq achieves consistently attractive returns on its deployed capital partially through its acquisition structuresAcquisition Structure BenefitsAcquisition Cost(MidSingle Digits EV / EBITDA multiple)Entry to public markets can provide the potential for equitylinked compensation to help drive returnsIllustrative Sample Acquisition StructureAbility to drive +20%20%( return on cash investment from Day 1Status as a"preferred enables CorpAcq topurchase founder led SMEs for attractivemultiplesImmediate and growingfree cash flow( for dividendPotential to add attractive returnson deployed capitalSource: CorpAcq Management.(1) Return on cash investment for acquisitions is defined as operating income minus tax, interest and debt service divided byCorpAcq's cash investment. Return metrics for target acquisition are based on seven of CorpAcq's recently completedacquisitions between 2019 2023 and do not represent the performance of entire portfolio. Past performance is not indicative of f uture results. (2) Free cash flow is defined as cash flow from operations minus net CapEx. See reconciliation inappendix for definition of net CapEx.Acquisition Funding Sources~25%~50%Cash~25%Debt (atSubsidiary Level)PerformanceLinked DeferredCompensation

9 Historical Roadmap for Achieving Compounding Free Cash Flow & Dividend Growth Combining its diversified portfolio of stable companies and a low - risk, high cash return acquisition strategy has provided the b ase for dividend capacity (2) growth Organic GDP + top - line growth combined with operational support and exposure to essential UK end - markets Organic + Acquisition - driven growth Source: CorpAcq Management. (1) Free Cash Flow is defined as Cash Flow from Operations minus net CapEx. See reconciliation in appendix for definition of net CapEx. (2) Dividend capacity is defined as Free Cash Flow. CorpAcq’s Compounding Platform Strategy Has Delivered FCF Growth and Dividend Capacity Organic EBITDA Growth Long - Term EBITDA Growth Attractive M&A Platform Strong Free Cash Flow (1) Growth & Dividend (2) Potential Deep pool of founder - led SMEs in the UK

10 Source: CorpAcq Management. Note: Financial information prior to 2021 based on UK GAAP audits and has not been audited in accordance with PCAOB standards. Financial information beginning in 2021 is presented based on both UK GAAP and IFRS audits. LTM as of 6/30/2023. FY2023E financials are estimates from CorpAcq Management. Assumes USD:GBP exchange ratio of 1.286:1. (1) Past performance is not an indication of future results. (2) Organic growth is calculated as the aggregate growth of revenue or s ubsidiary - level Adj. EBITDA , as applicable, of subsidiaries that have been in the portfolio for the entirety of the compared periods. Subsidiary - level Adj. EBITDA is measu red as net profit before interest, tax, depreciation and amortization and excludes management fees to CorpAcq. Management fees are fixed amounts charged by CorpAcq Limited to its sub sid iaries for general corporate services. (3) CAGR and organic growth are measured from FY2018 – FY2022 and based on UK GAAP audits. (4) Adj. EBITDA definition and reconciliation provided in appendix. (5) Adjusted ROIC calculated as Adjusted Net Operating Profit After Taxes / Total Invested Capital; reconciliation provided in appendix. (6) Adj. EBITDA is based on IFRS audits and is measured as earnings before interest, tax, depreciation and amortization and excludes m ana gement fees to CorpAcq. (7) Includes costs allocated to corporate overhead. Adjusted EBITDA (6) (2022) Attractive and Diversified Business Mix Key Financial Metrics (UK GAAP) ~17% Adjusted EBITDA Margin (4) (LTM) 16% / 4% Revenue CAGR / Organic Revenue Growth (2,3) (2018 – 2022) 17% / 7% Adj. EBITDA CAGR / Organic Subsidiary - Level Adj. EBITDA Growth (2,3) (2018 – 2022) Historical Financial Performance Revenue (2,3) ( $ mm) Adj. EBITDA (2,3) ( $ mm) Resilience through COVID Top 10 subsidiaries accounted for less than two - thirds of total 2022 Adj. EBITDA (6) Top 10 Subsidiaries Other Subsidiaries (7) CorpAcq Financial Overview (1) CorpAcq has a record of organic top - line growth and cash flow generation driven by its acquisition strategy ~16% Adjusted Return on Invested Capital (5) (LTM) $717 $938 $814 $127 $162 $139 UK GAAP IFRS UK GAAP IFRS 12% / 15% 1H’23 Revenue / Adj. EBITDA Growth $860 $149 Key Financial Metrics (IFRS) $451 $615 $615 $722 $820 $863 $951 18A 19A 20A 21A 22A LTM 23E $70 $86 $84 $118 $129 $139 $152 18A 19A 20A 21A 22A LTM 23E

11 FY2022 Reported Incremental Contribution From FY2022 Acquisitons (1,3,6) FY2022 Run Rate Metrics (1) Acquisitions Signed YTD (2,3,6) Revenue (£mm) 814 25 839 80 Adj. EBITDA (£mm) 139 5 144 12 Adj. EBITDA Margin 17% 19% 17% 15% Source: CorpAcq Management. Note: 2022 reported financial information based on IFRS audits. Assumes USD:GBP exchange ratio of 1.286:1. (1) Assumes financials as if companies were acquired as of January 1, 2022. (2) Financials for 2023 acquisitions are based on FY2022 figures. (3) Subsidiary - level Adj. EBITDA is measured as net profit before interest, tax, depreciation and amortization a nd excludes management fees to CorpAcq. Management fees are fixed amounts charged by CorpAcq Limited to its subsidiaries for general corporate services. (4) Adj. EBITDA definition and reconciliation provided in appendix. (5) Revenue and subsidiary - level Adj. EBITDA are based on CorpAc q management estimates. (6) Sum of FY2022 Adj. EBITDA for CorpAcq and incremental subsidiary - level Adj . EBITDA from 2022 acquisitions. (4) (3) (3) (6) Portfolio Companies: 34 (as of January 1 st ) + 3 (acquired during year) Portfolio Companies: 37 CorpAcq’s Current Portfolio Performance

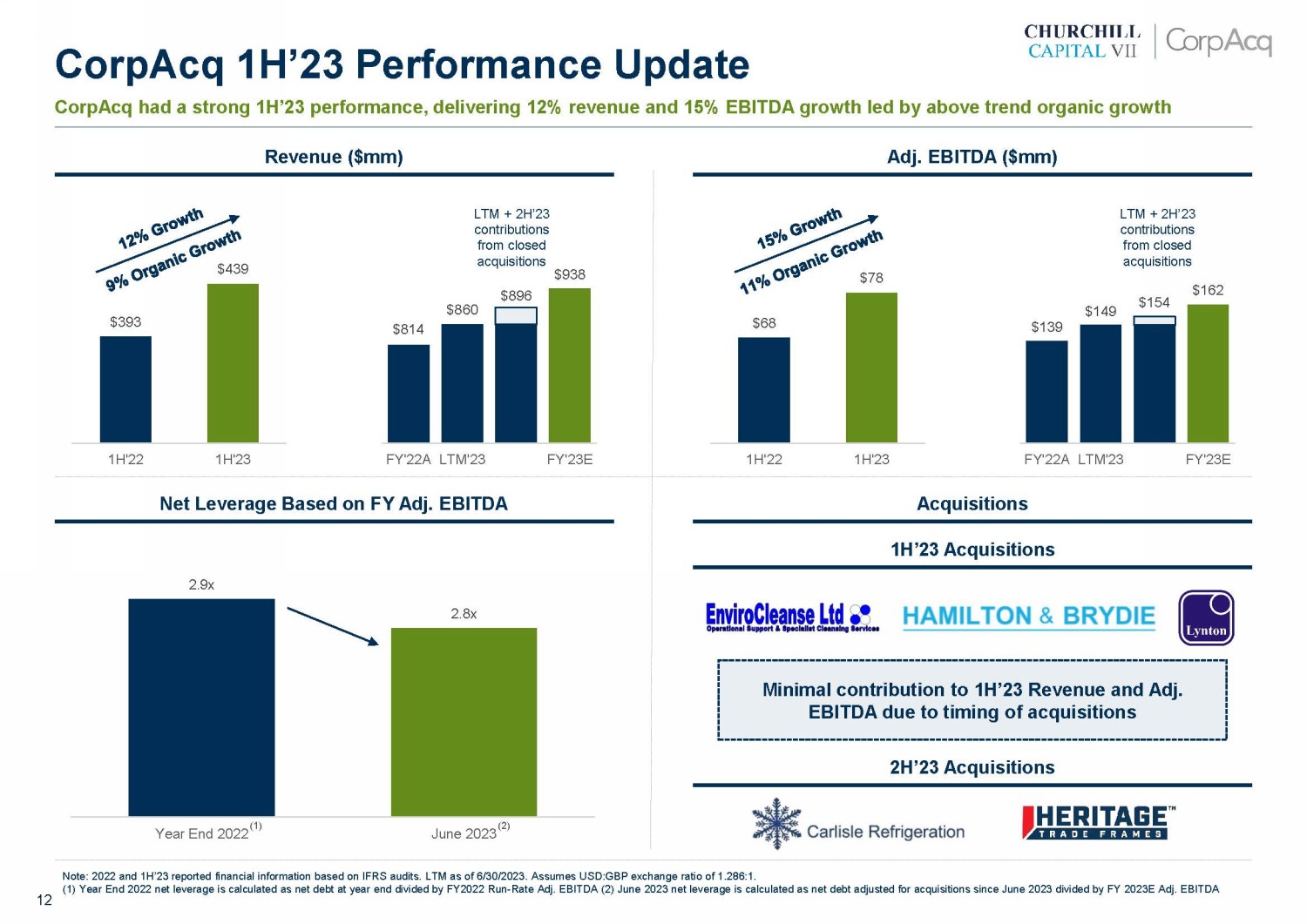

12 $68 $78 1H'22 1H'23 $814 $860 $938 $896 FY'22A LTM'23 FY'23E $393 $439 1H'22 1H'23 Note: 2022 and 1H’23 reported financial information based on IFRS audits. LTM as of 6/30/2023. Assumes USD:GBP exchange ratio of 1.286:1. (1) Year End 2022 net leverage is calculated as net debt at year end divided by FY2022 Run - Rate Adj. EBITDA (2) June 2023 net le verage is calculated as net debt adjusted for acquisitions since June 2023 divided by FY 2023E Adj. EBITDA Revenue ($mm) Adj. EBITDA ($mm) Net Leverage Based on FY Adj. EBITDA Acquisitions 2.9x 2.8x Year End 2022 June 2023 Minimal contribution to 1H’23 Revenue and Adj. EBITDA due to timing of acquisitions LTM + 2H’23 contributions from closed acquisitions LTM + 2H’23 contributions from closed acquisitions 1H’23 Acquisitions 2H’23 Acquisitions (1) (2) CorpAcq 1H’23 Performance Update CorpAcq had a strong 1H’23 performance, delivering 12% revenue and 15% EBITDA growth led by above trend organic growth

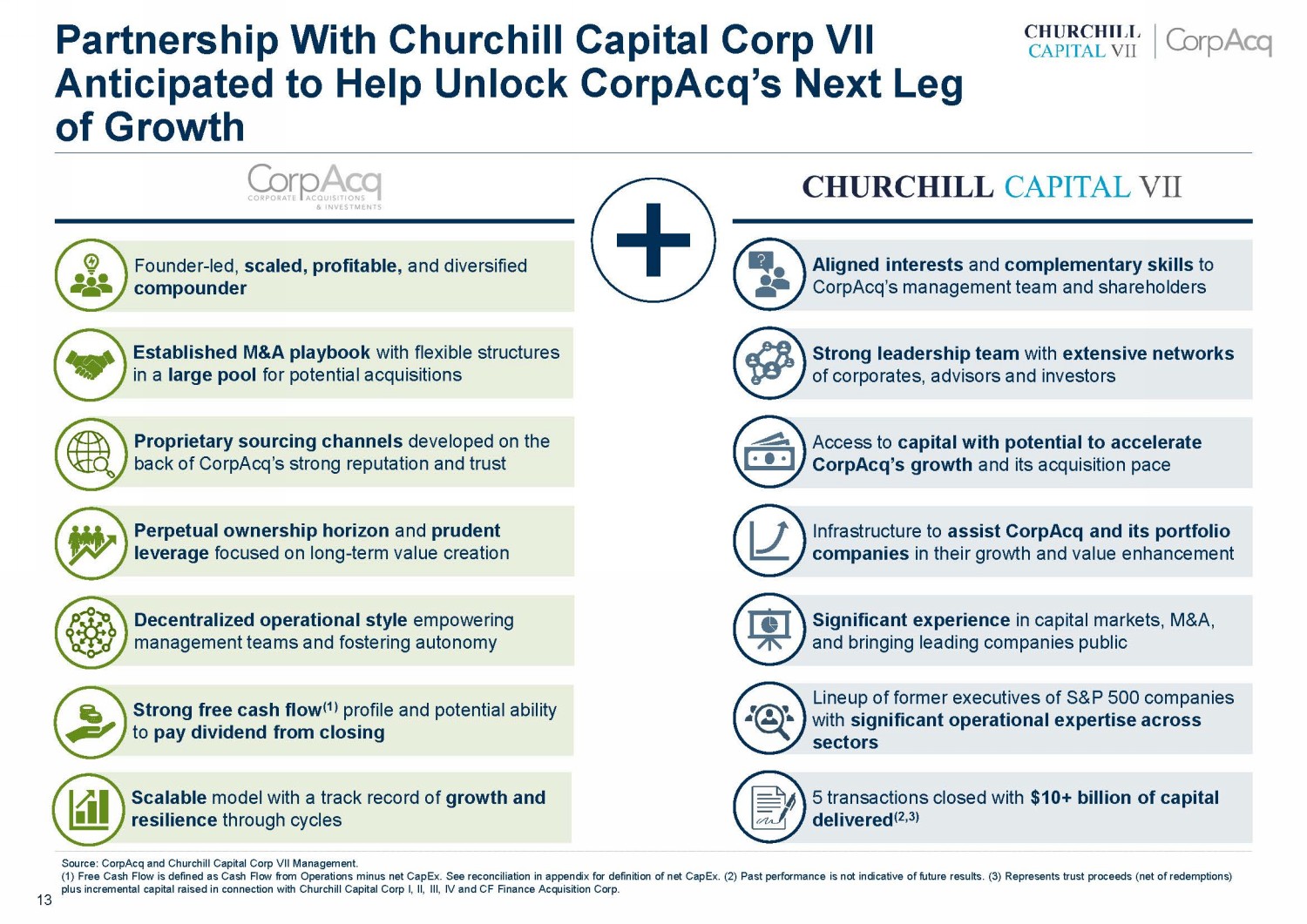

13 Founder - led, scaled, profitable, and diversified compounder 3 Strong free cash flow (1) profile and potential ability to pay dividend from closing 3 Established M&A playbook with flexible structures in a large pool for potential acquisitions 3 Decentralized operational style empowering management teams and fostering autonomy 3 Perpetual ownership horizon and prudent leverage focused on long - term value creation 3 Proprietary sourcing channels developed on the back of CorpAcq’s strong reputation and trust 3 Scalable model with a track record of growth and resilience through cycles 3 Significant experience in capital markets, M&A, and bringing leading companies public 3 Access to capital with potential to accelerate CorpAcq’s growth and its acquisition pace 3 Strong leadership team with extensive networks of corporates, advisors and investors 3 Aligned interests and complementary skills to CorpAcq’s management team and shareholders 3 Infrastructure to assist CorpAcq and its portfolio companies in their growth and value enhancement 3 Source: CorpAcq and Churchill Capital Corp VII Management. (1) Free Cash Flow is defined as Cash Flow from Operations minus net CapEx. See reconciliation in appendix for definition of net CapEx. (2) Past performance is not indicative of future results. (3) Represents trust proceeds (net of redemptions) plus incremental capital raised in connection with Churchill Capital Corp I, II, III, IV and CF Finance Acquisition Corp. Lineup of former executives of S&P 500 companies with significant operational expertise across sectors 3 5 transactions closed with $10+ billion of capital delivered (2,3) 3 Partnership With Churchill Capital Corp VII Anticipated to Help Unlock CorpAcq’s Next Leg of Growth

14 Compelling financial profile designed to deliver compounding returns Attractive entry point with a differentiated story Potential strong dividend yield from closing Potential fo r h igh risk - adjusted return on cash investment (2) Management “skin in the game” ensures alignment of interest post - closing Consistent organic growth tied to essential end - markets Established playbook and tight parameters for acquisitions Increase target size and extend geographic reach to US Access to capital designed to accelerate acquisition pace Deep near - & long - term pipeline of attractive local UK businesses Portfolio of 42 companies and growing 2. Tangible Growth Drivers 3. Compelling Profile for Compounding Returns 1. Platform For Value Creation L4Y Adj . EBITDA CAGR of 17% (1) Adj. EBITDA Growth + Acquisitions + Dividends = Long - Term Shareholder Value Low - risk strategy of acquiring businesses to drive shareholder value A Existing diversified portfolio of UK SMEs B Systematic approach for targeted support C “Preferred buyer” status with targets drives accretive values D Established, reputable owner - manager sinc e 2006 E A B C D E A B C D E Source: CorpAcq Management. (1) B ased on UK GAAP audits and has not been audited in accordance with PCAOB standards. (2) Return on cash investment for acquisitions a re defined as operating income minus tax, interest and debt service divided by CorpAcq’s cash investment. Return metrics for target acquisition are based on seven of CorpAcq’s recently completed acquisitions between 2019 - 2023 and do not represent the performance of entire portfolio. Past performance is not indicative of future results. Opportunity to Own a Differentiated Growth Story CorpAcq’s profitable track record, growth runway, current industry positioning, lower - risk acquisition strategy, and cash flow generation to support dividends represent a differentiated investment opportunity

15 1 Platform for value creation 01