Filed by APA Corporation

Pursuant to Rule 425 of the Securities Act of 1933

and deemed filed Pursuant to Rule 14a-12

of the Securities Exchange Act of 1934

Subject Company: Callon Petroleum Company

Commission File No. 001-14039

Date: January 4, 2024

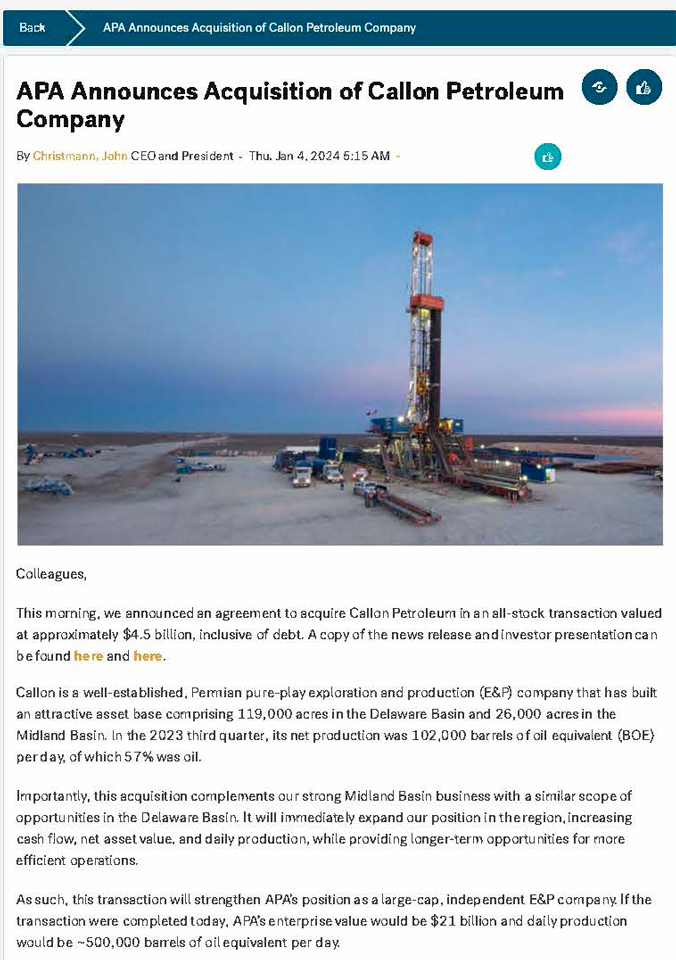

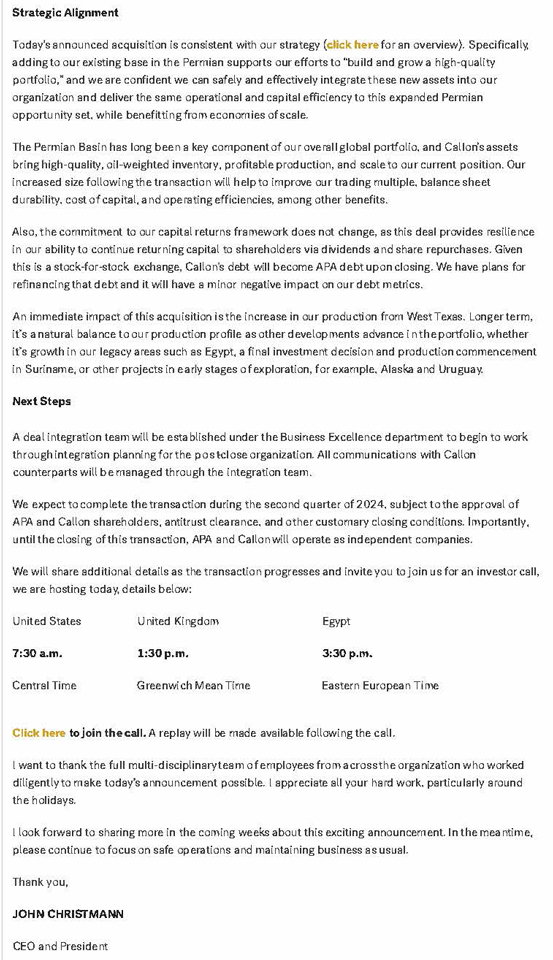

The following are

screenshots from APA’s employee intranet on January 4, 2024.

Forward-Looking Statements

This communication relates to a proposed business combination transaction between APA and Callon and contains “forward-looking statements” within

the meaning of the federal securities laws, including Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking statements relate to future events and

anticipated results of operations, business strategies, the anticipated benefits of the proposed transaction, the anticipated impact of the proposed transaction on the combined company’s business and future financial and operating results, the

expected amount and timing of synergies from the proposed transaction, the anticipated closing date for the proposed transaction, and other aspects of our operations or operating results. Words and phrases such as “anticipate,”

“estimate,” “believe,” “budget,” “continue,” “could,” “intend,” “may,” “might,” “plan,” “potential,” “possibly,” “predict,”

“seek,” “should,” “will,” “would,” “expect,” “objective,” “projection,” “prospect,” “forecast,” “goal,” “guidance,” “outlook,”

“effort,” “target,” and other similar words can be used to identify forward-looking statements. However, the absence of these words does not mean that the statements are not forward-looking. All such forward-looking statements

are based upon current plans, estimates, expectations, and ambitions that are subject to risks, uncertainties, and assumptions, many of which are beyond the control of APA and Callon, that could cause actual results to differ materially from those

expressed or forecast in such forward-looking statements.

The following important factors and uncertainties, among others, could cause actual results or

events to differ materially from those described in these forward-looking statements: the risk that the approval under the Hart-Scott-Rodino Antitrust Improvements Act of 1976 is not obtained or is obtained subject to conditions that are not

anticipated by APA and Callon; uncertainties as to whether the potential transaction will be consummated on the expected time period or at all, or if consummated, will achieve its anticipated benefits and projected synergies within the expected time

period or at all; APA’s ability to integrate Callon’s operations in a successful manner and in the expected time period; the occurrence of any event, change, or other circumstance that could give rise to the termination of the transaction,

including receipt a competing acquisition proposal; risks that the anticipated tax treatment of the potential transaction is not obtained; unforeseen or