UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

____________________________________________

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d) of the Securities

Exchange Act of 1934

____________________________________________

Date of Report (Date of earliest event reported): December

1, 2015

QS Energy, Inc.

(Exact Name of Registrant as Specified in

Charter)

| Nevada |

|

0-29185 |

|

52-2088326 |

|

(State or other jurisdiction

of incorporation) |

|

(Commission File Number) |

|

(IRS Employer

Identification No.) |

| |

|

|

|

735 State Street, Suite 500

Santa Barbara,

CA |

|

93101 |

|

| (Address of principal executive offices) |

|

(Zip Code) |

|

Registrant’s telephone number, including

area code: (805) 845-3581

| |

| (Former name or former address, if changed since last report) |

| |

Check the appropriate

box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the

following provisions:

| o |

Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| o |

Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| o |

Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| o |

Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Item 8.01 Other Events.

On December 1, 2015,

QS Energy, Inc. (the “Company”) posted a presentation of its Business Plan on the Company’s website, a copy of

which is attached as Exhibit 99.1 hereto.

Item 9.01. Financial Statements and Exhibits.

(d) Exhibits:

Exhibit

Number |

|

Description |

| |

|

|

| 99.1 |

|

Presentation of Business Plan |

SIGNATURES

Pursuant to the requirements of the Securities

Exchange Act of 1934, the Registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

| |

|

|

|

|

| Date: December 1, 2015 |

QS ENERGY, INC.

|

|

| |

By: |

/s/ Greggory Bigger |

|

| |

|

Name: Greggory Bigger |

|

| |

|

Title: Chief Executive Officer |

|

| |

|

|

|

|

|

EXHIBIT

99.1

QS

Energy, Inc.

Optimizing

the Efficiency and Safety

of

the Global Crude Oil Pipeline Infrastructure

BUSINESS

PLAN

December

2015

Greggory

M. Bigger, CEO

QS

Energy, Inc.

735

State Street, Suite 500

Santa

Barbara, CA 93101

|

Tel:

(805) 845-3581

E-mail:

gregg.bigger@qsenergy.com

Web:

www.qsenergy.com

|

No

offering is made or intended by this document. Any offering of interests in QS Energy, Inc. will be made only in compliance with

Federal and State securities laws.

This

document includes confidential and proprietary information of and regarding QS Energy, Inc. This document is provided for informational

purposes only. You may not use this document except for informational purposes, and you may not reproduce this document in whole

or in part, or divulge any of its contents without the prior written consent of QS Energy, Inc. By accepting this document, you

agree to be bound by these restrictions and limitations.

FORWARD

LOOKING STATEMENTS

This

presentation is neither an offer to sell nor a solicitation of offers to purchase securities. This presentation is the confidential

intellectual property of QS Energy, Inc. (“Company”). Any use or redistribution of this document or its contents without

the express written consent of the Company is prohibited. All statements other than statements of historical fact included in

this presentation, including, without limitation, statements regarding the Company’s anticipated financial position, business

strategy and plans and objectives of management of the Company for future operations are forward-looking statements. When used

in this presentation, words such as “anticipate,” “believe,” “estimate,” “expect,”

“intend,” and similar expressions, as they relate to the Company or its management, identify forward-looking statements.

Such forward-looking statements are based on the beliefs of the Company’s management as well as assumptions made by and

information currently available to the Company’s management. Actual results could differ materially from those contemplated

by the forward-looking statements as a result of certain factors not limited to, general economic and business conditions, competitive

factors, changes in business strategy or development plans, the ability to attract and retain qualified personnel, and changes

in legal and regulatory requirements. Such forward-looking statements reflect the current views of the Company with respect to

future events and are subject to these and other risks, uncertainties and assumptions relating to the operations, results of operations,

growth strategy and liquidity of the Company. All subsequent written and oral forward-looking statements attributable to the Company

or persons acting on its behalf are expressly qualified in their entirety by this paragraph.

Contents

| Executive

Summary |

1 |

| Technology |

1 |

| Acquisition

Strategy |

1 |

| Market

Opportunity |

2 |

| Funding

Strategy |

3 |

| Company

Overview |

4 |

| QS

Energy, Inc. |

4 |

| Special-Purpose

Subsidiary |

4 |

| Innovative

High Value Technologies |

5 |

| AOT

(Applied Oil Technology) |

5 |

| JHT

(Joule Heat Technology) |

9 |

| Product

Development and Commercialization |

11 |

| Published

Papers and Studies |

14 |

| Market

Overview |

17 |

| Market

Size |

17 |

| Projected

Pipeline Infrastructure Investment |

18 |

| Target

Markets |

22 |

| Upstream

Producers |

22 |

| Midstream

Transporters |

23 |

| Midstream

Gathering Transporters |

24 |

| Downstream

Refineries / Offloading Facilities |

24 |

| Our

Team |

25 |

| Executive

Management |

25 |

| Board

of Directors |

26 |

| QS

Energy Pool Board of Advisors |

27 |

| Pro

Forma Financials |

28 |

| General

Discussion |

28 |

| Pro

forma Income Statement |

30 |

| Pro

forma Balance Sheet |

31 |

| Pro

forma Cash Flow |

32 |

| Notes |

33 |

Executive

Summary

QS

Energy, Inc. (QS Energy) provides cutting-edge technologies

to companies active in the gathering, upstream and midstream crude oil industry to optimize the efficiency and safety of transporting

conventional and unconventional production to refineries. QS Energy's intellectual property portfolio includes 48 domestic and

international patents and patents pending, which have been developed independently and in conjunction with and exclusively licensed

from Temple University. Through its wholly owned subsidiary, QS Energy Pool, QS Energy looks to make accretive acquisitions of

complementary entities and assets in the oil and gas sector. QS Energy, Inc. is a publicly traded U.S. corporation (OTCQX symbol:

QSEP)1.

Technology

QS

Energy’s AOT and Joule Heat technologies comprise a suite of commercial crude oil pipeline flow assurance products designed

to reduce operating costs and increase capacity of upstream, gathering and midstream pipeline operations. AOT delivers viscosity

reduction by coagulating particulate matter found in crude oil into nanoscale particle clusters. Joule Heat is a highly energy-efficient

feedstock heating system that delivers optimal heat conductivity and performance using less power than other traditional heat

systems.

Acquisition

Strategy

QS

Energy has identified multiple attractive opportunities to acquire producing oil and gas field operations. Our strategy is to

acquire producing oil and gas fields with production profiles of at least ten years, proven long-term development rights, and

demonstrated positive cash flow at commodity prices as low as $25/barrel of oil and $2.00/MCF of gas. While commodity prices stay

low, QS Energy will continue to seek opportunistic acquisitions. As commodity prices rise and acquisition opportunities become

more expensive, QS Energy would be in a position to profit from increased operating revenues while redeploying acquisition capital

to drilling of proved, undeveloped well sites (PUDs) on its previously acquired properties.

Initial

Acquisition: Subject to funding availability, QS Energy is

currently pursuing the acquisition of profitable joint venture gas well operations and drilling rights within the Haynesville

Shale region, one of the largest onshore gas fields in the United States with an estimated 251 trillion cubic feet of recoverable

gas. Located in northwest Louisiana, these assets consist of joint venture interests in 7,000+ gross acres in four field areas,

21 producing wells and 38 Proved Undeveloped (PUD) and Probable wells. At today’s low gas prices, these assets continue

to generate positive cash flows of $100,000 per month, and are expected to operate profitably at gas prices as low as $2.00/MCF;

break-even operations estimated at $1.70/MCF. In 2014, when wellhead gas prices averaged $3.95/MCF, the properties generated $4.6M

in cash.

1

QS Energy was incorporated on February 18, 1998, as a Nevada corporation, under the name Mandalay Capital Corporation. The

Company originally branded itself as Save the World Air, Inc. in 1999 in anticipation of its entry into the “clean tech”

sector of industrial equipment. In 2015, the Company was renamed and re-branded as an energy technology and operations company

under the name QS Energy, Inc.

These

assets, if acquired, would be purchased post-bankruptcy, with clean title, free and clear of all debt and encumbrances. At current

and forecast gas prices, the joint venture interest in producing wells (PDP) are projected to provide a 12% to 17% return on investment

based solely on cash flow generated by producing wells; we would effectively be acquiring future development rights for free.

In

a 2014 year-end financial audit, EY Global Financial Services, reported the joint venture’s reserves under SEC rules of

Oil and Gas Compliance and Disclosure Interpretations2. This audit

valued the estimated ultimate recovery (EUR) of the producing wells (PDP) at 6.3 billion cubic feet of natural gas (BCF); and

identified 19 proved undeveloped sites (PUD), each with a EUR of more than 6 BCF. A summary of the audit SEC evaluation is as

follows:

Haynesville

Acquisition Target

Year End 2014 Audit

SEC Evaluation |

Reserve

Category |

Net

Reserves

(BCF) |

Gross

EUR

(BCF) |

| Proved |

6.3 |

84.6 |

| Probable |

34.8 |

196.0 |

| Possible |

8.3 |

42.4 |

| Contingent |

27.4 |

194.3 |

Despite

falling gas prices, we expect the fluidity of supply and demand forces within the global energy sector will result in commodity

prices rising in the near future. Data compiled by the U.S. Energy Information Agency, shows oil and natural gas rigs in the U.S.

dropped by 58% and 41%, respectively during the 12 months ending October 20153.

The potential loss of natural gas byproduct over the next year has been estimated to be as high as 1 billion cubic feet per day

as oil wells continue to shut down in the Bakken and Eagle Ford regions4.

Acquisition

Pipeline: QS Energy has identified several other oil and gas

asset targets and will proceed pursuant to funding availability.

Market

Opportunity

The

recent surge in oil and gas production and resultant oversupply and industry downturn have created a remarkable buy-opportunity

for companies positioned to acquire distressed assets out of bankruptcy, at auction, through direct purchase and other quick-strike

opportunities. Prior to the recent drop in oil and gas commodity prices, U.S. exploration and production companies drilled wells

at historic rates, capitalized through highly leveraged secured bank loans. As commodity prices fell, so did corporate valuations

and borrowing base. As reported by Business Insider, analysis of the Federal Reserve’s 2015 Shared National Credits exam

reveals that, “one in seven loans to oil and gas companies are edging toward default.”5

2

See https://www.sec.gov/divisions/corpfin/guidance/oilandgas-interp.htm

3

“Drilling Productivity Report for key tight oil

and shale gas regions”, Oct. 2015, U.S. Energy Information Administration, http://www.eia.gov/petroleum/drilling/archive/dpr_oct15.pdf

4

“EIA expects near-term decline in natural gas production

in major shale regions”, Aug. 26, 2015, U.S. Energy Information Administration, https://www.eia.gov/todayinenergy/detail.cfm?id=22672

5

“TROUBLING: Oil and gas companies are edging toward

default”, Business Insider, Nov. 13, 2015; http://www.businessinsider.com/banks-oil-and-gas-classified-loans-2015-11

Target Market: Initially, we plan to target small to mid-market operations valued at

$5MM - $25MM with annual revenues ranging from $1.5MM to $8MM. We have identified our first target acquisition, valued at $4MM

with debt-free positive annual cash flow of $1MM and long-term proven development rights.

Short-term:

Our first acquisitions will target cash flow positive oil and gas production operations, acquired debt-free, either through

direct asset purchase or bankruptcy. Operations must have demonstrated cash flow and should be able to operate profitably at gas

prices at or below $2.00/MCF or oil prices at or $25/bbl.

Although

we do intend to build a balanced oil and gas portfolio, our initial preference leans towards gas assets over oil due to lower

volatility and greater domestic influence on commodity prices.

Long-term:

We will continue to pursue opportunistic acquisitions while

commodity prices remain low. As commodity prices rise and acquisition opportunities become less attractive, QS Energy will turn

its focus to drilling proved, undeveloped well sites (PUDs) on its previously acquired properties.

Funding

Strategy

QS

Energy intends to fund acquisitions through the private placement of a $25 million convertible note, convertible to shares of

common stock of QS Energy, Inc. In advance of the private placement, we intend to raise additional working capital of approximately

$1 million in the form of convertible debt, and approximately $4 million in the form of a secured bridge loan for the sole purpose

of funding our first acquisition. The bridge loan will be settled in cash with funds raised through the convertible note. All

acquired properties will be held and operated by QS Energy Pool, a wholly owned subsidiary of QS Energy Inc., formed for the sole

purpose of acting as QS Energy’s acquisition vehicle. Cash flow from acquired properties will fund QS Energy working capital

and final commercialization of its oil pipeline flow assurance technologies.

Company

Overview

QS

Energy, Inc.

QS

Energy was originally incorporated on February 18, 1998, as a Nevada corporation, under the name Mandalay Capital Corporation.

In 1999, the Company changed its name to Save the World Air, Inc. in anticipation of its entry into the “clean tech”

sector of industrial equipment. In 2015, the Company was renamed and re-branded as an energy technology and operations company

under the name QS Energy, Inc.

QS

Energy is a developer and vendor of patent-protected industrial equipment designed to improve the operational and economic efficiencies

of the global crude oil pipeline infrastructure. Working in partnership with scientists at Temple University in Philadelphia and

in collaboration with petroleum engineers at leading production and transportation entities, QS Energy is establishing a strong

leadership position within the $6 trillion global energy industry. The Company specializes in technologies that favorably affect

the viscosity and flow of a wide spectrum of crude oil products by treating feedstock with electrical charges while in transit,

increasing operational efficiencies and providing “clean tech” benefits by helping to reduce CO2 emissions for the

upstream and midstream sectors.

Over

the past three years QS Energy has undergone an extensive corporate restructuring, significantly reducing expenses, while focusing

corporate activities on the final stages of technology commercialization and revenue growth through the execution of an opportunistic

acquisition strategy. In addition, operations were restructured to meet the demands of Sarbanes-Oxley compliance, all while reducing

administrative overhead. All of these initiatives were done with one purpose in mind: enhancing shareholder value.

Special-Purpose

Subsidiary

QS

Energy Pool is a wholly owned subsidiary of QS Energy, Inc., newly formed for the sole purpose of taking advantage of asset acquisition

opportunities in the oil and gas operations market. QS Energy Pool is specifically targeting the acquisition of one or more operating

companies or properties with proven positive cash flow, providing operating income and bottom line revenue which are both accretive

to and synergistic with QS Energy, Inc.’s current operations.

As

a wholly owned subsidiary of QS Energy, Inc., QS Energy Pool is managed and operated by QS Energy’s executive management

team and Board of Directors. QS Energy Pool has a clean balance sheet and no direct expenses.

We

have identified our first target acquisition, valued at $4MM with positive annual cash flow of $1MM and substantial long-term

development rights. Follow-on acquisitions are targeted at values of $5MM - $25MM with annual revenues ranging from $1.5MM to

$8MM.

To

expedite funding of its initial acquisition, QS Energy Pool intends to secure a $4MM short-term bridge loan, 100% secured by the

acquired assets. The bridge loan will be settled in cash with funds raised through the private placement of a $25MM convertible

note, convertible to common shares of QS Energy Pool’s parent company, QS Energy, Inc. Follow-on acquisitions will be funded

primarily with the balance of funds raised through QS Energy, Inc.’s convertible note.

QS

Energy Pool has formed an Advisory Board comprised of energy industry veterans, each providing a depth of knowledge and strategic

relationships within the oil and gas industry and capable of pre-vetting acquisition targets. See QS Energy Pool Board of Advisors

section below for details.

Innovative

High Value Technologies

Our

current product portfolio is comprised of two lines of patent-protected industrial equipment designed and fabricated entirely

in the U.S. and extensively field tested with leading midstream and upstream producers and pipeline operators.

AOT

(Applied Oil Technology)

AOT

(Applied Oil Technology), is a solid-state hardware system that reduces the viscosity of crude oil by applying a high intensity

electric field within one or more ASME6-certified pressure vessels.

Designed for installation at pump stations within the midstream sector. Independent third-party testing has proven the efficacy

of AOT to: 1) improve flow, 2) increase the volume of transported oil, 3) mitigate bottlenecks, 4) reduce the amount of energy

used to operate the line and, 5) lower operating pressure.

The

AOT is currently the industry’s only commercially available hardware solution utilizing electricity to reduce the viscosity

of crude oil in order to optimize pipeline performance. Protected by 48 worldwide patents, AOT uses electrorheology to change

the mechanical behavior of a variety of oils, liquid gases and other fluids. AOT is uniquely positioned as a cost-efficient, low

maintenance solution with documented efficacy that improves pipeline flow capacity, reduces pipeline operating pressure, unlocks

pipeline chokepoints and lowers pump station energy requirements.

6

American Society of Mechanical Engineers (ASME) is an engineering society and developer

of codes, standards, and certification programs associated with the art,

science, and practice of mechanical engineering.

Although

pipelines are by far the safest, most economical and most preferred method for transporting crude oil and petroleum products7,

a significant amount of energy and pressure is required to operate them – primarily due to the low mobility and high viscosity

characteristic of most grades of crude oil. To counter the inherent resistance of crude oil to flow, and to mitigate drag caused

by turbulence, pipeline operators rely upon chemical additives (diluents and DRA) and the use of heat (trace heating, bulk heating)

to reduce viscosity. While the use of drag reducing agents (DRAs) and heat can reliably achieve the desired viscosity reduction

(resulting in a higher Reynolds number8), lower friction factor

and reduced pump station power requirements, additives are costly, displace a percentage of the volume of feedstock being transported,

and must be removed during the final refinement process. Traditionally, additives dilute the oil by as much as 25 to 30 percent,

effectively reducing pipeline capacity by the same ratio.

Trace

heating systems require extensive wiring and insulation modifications to the pipeline and require a parallel power supply network

supported by control cabinets, temperature detectors and distribution boxes. Heat loss and other inefficiencies result in substantial

electricity/fuel consumption which adds significantly to operating overhead.

Fig.

1: Industrial design schematic and photo of AOT four-vessel viscosity reduction system. Following fabrication and pressure

testing, this 110-ton unit was ASME-certified, approved for use in hazardous location Class 1, Div. I. rated areas, and installed

on a 500,000 barrel per day mid-continent pipeline operated by a $36 billion North American energy company.

Unlike

diluents and DRAs, AOT does not require consumables and operates as a solid-state system while delivering an equivalent viscosity

reduction effect compared to those methods. By subjecting the flow to an electrical field as the crude oil moves through one or

more ASME-certified pressure vessels installed on an isolated skid at the pumping station, the AOT is able to coalesce microscopic

particles within the crude and reduce viscosity. This is accomplished by applying an electrical charge to a series of disk-shaped

metal plates positioned at intervals within the AOT vessel(s). Each plate is perforated with hundreds of round apertures that

allow continuous movement of the crude oil with minimal resistance.

7

“Pipelines are Safest for Transportation of Oil

and Gas”, The Manhattan Institute, June 2013:

http://www.manhattan-institute.org/html/ib_23.htm#.VT1_IiHBzRY

8

In fluid mechanics the Reynolds number (Re) is used to define

the ratio of resistant (inertial) forces to viscous forces to help predict flow patterns and drag.

Through

a process known as dielectrophoresis9, the electrical charge causes

a conformational change to the molecular structure of the naturally occurring paraffin and asphaltene content in the crude oil.

These randomly distributed particles bundle together into tight packets aligned in chains. By aggregating the suspended particles

into short chains traveling in the direction of flow, AOT decreases viscosity and increases pipeline flow rate, optimizing performance

for operators and transporters while lowering their capital requirements.

Fig.

2: Viscosity reduction test results documented by U.S. Department of Energy researchers during a test deployment of a single-vessel

AOT prototype conducted on a 4.4 mile, 6 inch, schedule 80 metal closed loop pipeline at the Rocky Mountain Oil Field Test Center

in Wyoming. The original viscosity of 81.6 centipoise (cP) was reduced by 40 percent,

to 48.95 cP.

In

addition to decreasing viscosity along the direction of flow, this unique chain formation also increases viscosity perpendicular

to the direction of flow which seems to suppress the onset of turbulence. Suppressed turbulence reduces turbulent friction and

substantially increases flow rate, far beyond the benchmark set by reduced viscosity alone. These factors combine to minimize

costs and increase throughput, while mitigating energy loss.

The

impact of viscosity reduction for pipeline transportation systems is well known and, in fact, a large portion of the products

serving the midstream sector seek to achieve this goal. Fluid viscosity plays an important role in the function of any hydraulics

system. It is one of the main sources of internal fluid friction that creates major friction loss, which must be overcome by a

strong pressure gradient created by a pump. Reduction of friction enables the reduction of pressure, thereby improving the efficiency

of the system as a whole. The reduction of power required for flow reduces demand on pump station motors, directly reducing the

amount of carbon dioxide (CO2) emitted. Provided that the pipeline system remains in the same flow condition (laminar or turbulent),

the reduction in viscosity delivered by AOT also leads to a reduction in power consumed per day.

9

Dielectrophoresis (DEP) occurs when a dielectric particle is subjected to a non-uniform electric field. When fields of a

specific frequency are tested for scientific or industrial applications, it becomes possible to manipulate particles selectivity

according to the effect desired.

Many

companies choose to operate their pipelines at a constant pressure or power level. In that case, viscosity reduction will effectively

increase pipeline capacity. Decreases in viscosity will, if strategically deployed, increase throughput and revenues significantly.

Lower viscosity also relieves bottlenecks, and provides companies with the ability to unload crude storage more quickly. This

allows for a more flexible schedule, shorter load times, and more time for maintenance. Reduced wax deposition and suppressed

pour point, two effects currently being studied and confirmed in laboratory testing, may also provide substantial ancillary benefits

to certain customers.

Whether

deployed in a single-vessel or multi-vessel configuration, each AOT pressure vessel can process up to 5,000 gallons of oil per

minute, up to a capacity of 150,000 barrels per day. Depending on customer need, AOT pressure vessels can be connected in parallel,

increasing cumulative capacity. The first commercial skid deployed on an operating pipeline used four pressure vessels in parallel

for a cumulative capacity of 600,000 barrels per day. The Company currently owns five AOT pressure vessels; one of which was recently

deployed in South Texas under lease with options to extend the lease or purchase the equipment (see IV: AOT and JHT Customer Deployments

section on page 23). The remaining four AOT pressure vessels will be re-deployed either separately or together depending on the

target pipeline infrastructure.

In

the 24-months following fabrication of the first AOT prototype in May 2013, two lease agreements resulted in an installation on

a 500,000 barrel per day mid-continent pipeline operated by a $36 billion company, as well as a deployment on a 100,000 barrel

per day pipeline serving the Eagle Ford Formation and operated by a $93 billion entity.

QS

Energy is currently in non-disclosure level discussions with pipeline operators in six of the world’s primary oil transportation

corridors. The Company has also furnished detailed engineering proposals to entities in the Middle East, Europe, Africa and Canada,

while engaging in active engineering and business discussions. Several configurations of single- and multi-vessel AOT systems

have also been extensively field tested by globally recognized independent testing organizations including the U.S. Department

of Energy10, ATS RheoSystems11

and PetroChina/The China Petroleum Pipeline Bureau (CPP)12.

10

“Project Test Results Report; QS Energy, Inc. Viscosity

Reduction Technology”, U.S. Department of Energy, April 4, 2012: https://qsenergy.box.com/DOE-STWA-RMOTC-Report

11

Based in State College, Pennsylvania, ATS

RheoSystems provides industry with rheological, viscoelastic, flow profile, and mechanical property testing capabilities: http://www.atsrheosystems.com

12

“AOT Viscosity Reduction Tests in China”,

PetroChina, China Petroleum Pipeline Bureau (CPP) Flow Assurance Research and Development Facility, June 26, 2012: https://qsenergy.box.com/PetroChina-STWA-Report

Designed

for installation at pump stations on a gravel or concrete substratum, AOT can optimize virtually any midstream infrastructure,

regardless of pipeline length, diameter, flow rating, volume or grade of crude oil carried.

Summary

of AOT Viscosity Reduction System Benefits:

| · | Increased

maximum flow rates for given MAOP (maximum allowable operating pressure) ratings. |

| · | Increased

safety margins via reduced pressure required to achieve constant flow rates. |

| · | Reduced

power consumption and operating expenses at each midstream pump station. |

| · | Reduced

pour point and wax appearance temperatures. |

| · | Reduced

reliance on bulk heating systems. |

| · | Reduced

reliance on chemical pour point WAT depressants and additives. |

JHT

(Joule Heat Technology)

JHT

(Joule Heat Technology)13 is a highly energy-efficient, electrically-powered

heating system that applies an electric current directly to crude oil within an ASME-certified pressure vessel to efficiently

elevate oil temperature, substantially mitigating the high pour point nature of heavy, waxy feedstock and the flow challenges

caused by cold weather environments.

The

Company’s patent-pending Joule Heat Technology takes a unique approach to upstream oil heating. Specifically developed to

treat a wide spectrum of crude oil types, and designed to withstand cold weather conditions, JHT is electrically powered, compact

and adaptable to a variety of environments, from pipelines and oilfields to marine, rail and truck offloading facilities.

Due

to a variety of factors such as high viscosity, density, poor mobility and cold ambient temperatures, the energy industry invests

heavily in trace heating and other electrical and natural gas powered systems to ensure the safe, reliable and cost effective

transport of crude oil. Although the use of heat is common throughout the energy sector, it has traditionally been extremely inefficient

and therefore costly. Existing trace heating systems rely on an electrical resistor to heat the oil, which results in inefficiencies

through heat loss to the ambient environment. Despite the obvious need for a better, energy-efficient heating system, there has

not been a significant technological innovation in crude oil heating in many years – until now.

Developed

and designed in-house by QS Energy engineers and Dr. Carl Meinhart, a prominent researcher in the field of fluid mechanics at

the micro- and nano-scale, JHT is positioned to emerge as the most efficient and adaptable heat solution available for the upstream

and midstream sectors. The primary motivation for our research and development in service of providing innovative heat solutions

for the oil sector was a direct result of lengthy discussions with exploration and production (E&P) entities, pipeline operators

and government officials. Many state governments are scrutinizing activities such as drilling, flaring (the burning off of gas

at the well hole) and the transport of oil and natural gas because they contribute significantly to CO2 (greenhouse gas or GHG)

emissions. A significant portion of the blame for these emissions is centered on the inefficiencies of existing heat technologies.

13

Joule heating is the process by which the passage of an electric current through a resistive conductor releases heat and

is also known as ohmic heating and resistive heating.

JHT

achieves its superior efficiencies by subjecting oil diverted to the JHT vessel to a direct electric field that increases oil

temperature uniformly without interruption of flow. Instead of using energy to heat the pipe wall as seen in trace and direct-fired

(bulk) heaters, JHT creates heat within the oil itself by directly applying an electric field and pumping heat in the form of

electric work, creating a warm core of oil that diffuses heat more evenly. Existing trace heating systems require high levels

of maintenance, for example through the replacement of glycol, a non-corrosive fluid commonly used in convective heat transfer

systems.

Fig.

3: Traditional trace heating generates heat via a resistive heating element which transfers energy into the oil. In

contrast, JHT applies an electrical charge directly to the oil, generating heat within the feedstock itself.

JHT

is a standalone system, designed to function maintenance-free for long periods of time in remote locations. The system can also

interface with any extant SCADA (Supervisory Control and Data Acquisition) infrastructure and can be customized for large, high

volume transmission pipelines or low-flow "feeder" pipelines which are ubiquitous throughout the massive upstream sector.

The

first fully functional JHT unit was recently fabricated by one of our ISO/TS 29001-certified14

supply chain partners and is undergoing laboratory testing by Southern Research Institute15.

Once final calibration and pressure testing has been completed, the system will be installed on a primary pipeline serving the

Greater Monument Butte oilfield located in the Uintah Basin in Utah and operated by Newfield Exploration Company. Newfield is

Utah’s largest oil producer, responsible for approximately 40 percent of the state’s total output.

14

ISO/TS 29001:2010 is a globally

recognized standard that defines the quality management system for product and service supply organizations serving the petroleum,

petrochemical and natural gas industries: http://www.iso.org/iso/home/store/catalogue_tc/catalogue_detail.htm?csnumber=55499

15

An incorporated affiliate of The

University of Alabama at Birmingham (UAB), Southern Research Institute provides environmental and energy research and laboratory

services to government and commercial organizations around the world.

Summary

of JHT Benefits:

| · | Delivers

optimal heat conductivity and performance with less power and in a smaller form factor. |

| · | Achieves

upwards of 60 percent energy efficiency compared to an average of 30 percent seen in

electrical resistor systems. |

| · | Reduces

demand on existing bulk heaters on pipelines, storage tanks or offloading facilities

by preheating the oil and improving the overall system assurance. |

| · | Reduces

back pressure by lowering pipeline operating pressure. |

| · | Avoids

excessive buildup or corking due to poor mobility. |

| · | Drives

overall operational efficiencies by providing greater control over pour point temperatures. |

| · | Runs

on electricity from the available grid. |

| · | Produces

less local emissions, reducing environmental impact. |

Product

Development and Commercialization

At

its inception in 1998, the Company’s research and development focused on improving the fuel efficiency and reducing CO2

and other emissions of gasoline and diesel combustion engines. It was through these preliminary product development efforts that

in 2007 the research of Dr. Rongjia Tao, professor and chair of physics at Temple University

in Philadelphia, came to the attention of QS Energy leadership.

Recognized

as a leading expert in the use of electric and magnetic fields for industrial applications, Dr. Tao had published several technical

papers proposing that electrorheological principles could be useful in improving the performance of land-based and undersea oil

pipelines. Coincidentally, following a decade of declining domestic crude oil production, enhanced oil recovery (EOR) techniques

had sparked intensive new E&P activity and upstream output was soaring to historic highs. The resultant pipeline capacity

challenges were becoming well documented in energy industry trade publications, providing a strong case for commercializing hardware

based on Dr. Tao’s studies.

In

2008, the Company pivoted away from the automotive and truck aftermarket and began underwriting research at Temple University

to develop industrial equipment capable of optimizing pipeline performance through advanced fluid mechanics. Within months, QS

Energy-funded projects at the Physics Department at Temple had shown strong evidence that the

effects of a high intensity electric field could significantly reduce the viscosity of a wide range of crude oils. Newly launched

business development efforts by QS Energy procured oil samples from around the world that, once tested, provided data useful for

the construction of small-scale AOT prototypes.

During

the next two years the joint R&D program resulted in 48 worldwide patents related to the use of electrical fields to treat

crude oil, liquid natural gas and other petroleum products. QS Energy is the sole worldwide licensee of these patents and holds

exclusive rights for their use in commercial applications, in perpetuity, under a royalty agreement with Temple University. The

core functionality of AOT is centered on delivering an electrical “bath” to crude oil in transit based on principles

of electrorheology identified and pioneered by Dr. Tao.

Beginning

in the second quarter of 2011, the Company initiated engineering and supply chain contracting protocols necessary to transition

from prototype testing of our patented industrial-grade technologies to full scale commercial production. Since that time, QS

Energy has been working in close collaboration with leading energy companies and has leveraged its resources as a publicly traded

entity to underwrite the successful development of two distinct categories of pipeline optimization technology. With the expertise

and collaboration of Industrial Screen & Maintenance in Casper, Wyoming, the first functional AOT vessel was fabricated and

shipped to the Rocky Mountain Oilfield Testing Center (RMOTC) for rigorous testing and analysis on a functioning closed loop pipeline.

Operated by the U.S. Department of Energy, the RMOTC was established to provide oilfield infrastructure and SCADA resources to

companies serving the energy industry.

Following

independent verification and validation of viscosity reduction in a range suitable for commercial viability by the research team

at the Department of Engineering at Temple University and U.S. Department of Energy personnel at the RMOTC, the Company initiated

discussions with several leading crude oil producers and transporters. In collaboration with engineering teams at 19 leading energy

industry vendors, including Bechtel, Worley Parsons/Colt Engineering, Kiewit, Gulf Interstate and four Fortune 500 entities, development

of the first industrial-grade AOT system commenced in 2012.

Designed

to the exact specifications of the fourth largest pipeline operator in North America and specifically engineered for beta testing

on their high capacity, north-south, mid-continent pipeline, a four-vessel AOT system was engineered. Under the terms of a six-month

Equipment Lease/Option to Purchase Agreement the 110-ton, solid state, ASME Certified, 600# AOT skid was shipped and installed

in June 2014 on one of the most advanced pipeline infrastructures in the world. Following a series of efficacy tests performed

in conjunction by the Customer, QS Energy personnel, and ATS RheoSystems, AOT was verified to have achieved viscosity reduction

and reduced back pressure. If installed permanently, it would allow pipeline operations to increase throughput or reduce pipeline

operating pressure, and to reduce pumping station power consumption.

This

initial beta installation on a high profile primary pipeline provided the Company with the opportunity to participate in a collaborative

engineering environment with multiple companies, and brought AOT to the attention of the entire industry, including the company

that procured our current deployment. Through beta testing, QS Energy was able to understand and optimize the final details of

the design and installation. As a result of this lengthy, multiyear development effort with several leading entities in the midstream

sector, AOT has been certified to fully comply with the stringent standards and qualification processes as dictated by independent

engineering audit groups and North American industry regulatory bodies.

In

parallel with the development of the AOT system, QS Energy has been working internally to develop a new Joule Heat technology

(JHT). Although research, development and fabrication of JHT hardware is just entering its second year, much progress has been

made in a short amount of time. At the moment JHT has been proven viable in multi-physics models, and confirmed to be market valuable

following research and corroboration with clients and customers. Since market confirmation, QS Energy has built its first prototype,

full-scale installation and hopes to begin testing with a major upstream company within the month.

Applied

Oil Technology (AOT)

From

fiscal year 2013 to the present, QS Energy has executed two AOT Equipment Lease Agreements, both based on limited term leases

with an option to purchase the equipment outright. On August 1, 2013, the Company entered into a four-month Equipment Lease/Option

to Purchase Agreement with a $36 billion pipeline operator for use of a four-vessel AOT system on a 500,000 barrel per day line,

providing QS Energy with its first ever revenues. During the term of the lease, QS Energy successfully tested the AOT technology

on the midstream pipeline, proving its efficacy in reducing viscosity, optimizing pipeline performance, and improving flow. Third-party

ATS RheoSystems was present during the test and confirmed the results using a bench mount viscometer. Although the test periods

were short, QS Energy was also able to see the effects of viscosity reduction in the operational SCADA data.

On

July 15, 2014, the Company entered into a four-month Equipment Lease/Option to Purchase Agreement with an option to extend the

lease for up to a maximum of 84 months for a single-vessel AOT system on a 100,000 barrel per day line with a $96 billion pipeline

operator. This deployment offers the opportunity to optimize AOT for condensate, a super light crude oil that represents the fastest

growing category of feedstock today. In addition to providing useful test data from deployment in the field, these collaborative

opportunities are invaluable in further refining the AOT design and optimizing its performance capabilities.

The

specifics of these agreements are documented in our Company’s Form 10-Q filed with the Securities and Exchange Commission

(SEC) on August 11, 2014 and in various other SEC filings and press announcements since.

Joule

Heat Technology (JHT)

In

October 2014, QS Energy entered into a Joint Development Agreement with Newfield Exploration Company (NYSE: NFX) to test a commercial

prototype of JHT equipment on a crude oil pipeline serving the Greater Monument Butte oilfield located in the Uintah Basin of

Utah. This beta test of JHT provides ideal conditions to demonstrate our heat technology’s efficiency and efficacy. The

Uinta Basin is 5,000 to 10,000 feet above sea level with average low winter temperatures of 16ºF, and the crude oil pumped

from the region is highly paraffinic, with the consistency of shoe polish at room temperature. Uinta's black wax crude must remain

at a minimum temperature of 95°F (yellow wax above 115°F) and therefore requires a substantial amount of heat to keep

it above its high pour point. Newfield, like all other companies in the region, has significant operating expense overhead in

the form of fuel and power used to heat the waxy crude and counter the cold climate conditions characteristic of Utah. This deployment

provides an opportunity to showcase JHT as a cost-effective, low maintenance technology offering the potential to reduce operating

overhead through more efficient heating and transport of the feedstock.

Details

of this engagement are documented in a 10-K filed with the SEC on March 16, 2015.

Published

Papers and Studies

AOT

Video Overview

http://www.qsenergy.com/technology/technology-reports?file=54

Technical

papers published by Dr. Rongjia Tao, co-developer of AOT and Chairman of Temple University's Physics Department:

‘Reducing

viscosity of paraffin base crude oil with electric field for oil production and transportation’, Published in FUEL, The

Science and Technology of Fuel and Energy. Elsevier B.V. (October 25, 2013)

http://qsenergy.box.com/Jfuel-crude-oil

‘Neutron scattering studies of crude oil viscosity reduction with electric field’, Published in FUEL,

The Science and Technology of Fuel and Energy. Elsevier B.V. (June, 2014)

http://qsenergy.box.com/Neutron-Fuel

‘Suppressing Turbulence and Enhancing the Liquid Suspension Flow in Pipeline with Electromagnetic Fields’,

presented at the Tenth International Conference on Flow Dynamics,

November

25-27, 2013, Sendai, Miyagi, Japan.

http://qsenergy.box.com/Turbulence-2013-Tohoku

AOT

CASE STUDY

QS

Energy / ATS RheoSystems Joint Testing of

Commercial

Beta Deployment on Mid-Continent High Volume Pipeline

In

September 2014, a four-vessel AOT system was installed on a newly constructed, high-volume North-South, mid-continent pipeline

under the terms of an Equipment Lease-Option to Purchase Agreement. Fabricated by QS Energy supply chain partners in 2013, the

solid-state, 110-ton AOT system was shipped by freight truck and positioned on a gravel substrate on the equipment’s self-contained

steel skid-mount at a pumping station of the customer’s choosing.

This

commercial deployment and beta test opportunity was the result of extensive collaboration between QS Energy and executives and

engineers from multiple producers, pipeline operators and supply chain partners. Following installation, pressure testing and

calibration, the AOT system was interfaced with the extant SCADA (supervisory control and data acquisition) to provide a detailed

overview of the system’s performance, including real time monitoring of flow rates, back flow pressure and other relevant

metrics. Preliminary tests were conducted over a period of several weeks, under a variety of operating conditions and multiple

grades of crude oil and diluent mixtures.

During

the preliminary test cycle, it was determined that the electric field within the AOT pressure vessel was insufficient to fully

treat heavy crude oils at flow rates expected under full-scale operating conditions. The power supply provided with the AOT device

had been specified and approved by Temple University based on infrastructure and operating parameters, as well as on laboratory

tests performed on crude oil samples provided by the pipeline operator. Detailed investigation verified the AOT power supply had

been manufactured to, and was operating at, specifications as provided by Temple University, but was generating an electric field

approximately 10% of that required to optimize treatment under full-scale operating flow rates16.

It was further determined that replacing the AOT power supply with a more powerful unit would likely correct the situation. However,

due to time constraints, all parties agreed to go forward with the testing using the installed power supply.

In

its most extensive testing during this deployment, the AOT was operated under full-scale commercial operating conditions over

a two-day period. Operations were overseen by the pipeline operator and QS Energy engineers, while engineers from ATS RheoSystems,

a division of the CANNON Instrument Company (“ATS”), were on-site collecting data for subsequent analysis. Oil samples

were taken from the pipeline both before and after treatment by the AOT. Viscosity measurements were conducted on three grades

of heavy crude oils over the two-day testing period. Data collected and analyzed before and after AOT treatment demonstrated a

decrease in viscosity of approximately 23 percent 3 hours after treatment, and a decrease in viscosity of approximately 11 percent

13 hours after treatment; 22 hours after treatment, the crude oil had returned to its original pre-treated viscosity. Viscosity

reductions measured in these tests fell short of reductions experienced in the lab. Given the insufficiency of installed power

supply, we are very encouraged by these results. It is important to note that due the small size of data set collected, these

results cannot be relied upon to provide statistically significant proof of AOT efficacy.

In

consideration of non-discloser agreements, ATS RheoSystems provided a report summarizing test procedures and general findings

which excluded details of operations and results. A copy of this report, compiled by Jeshwanth Rameshwaram, Ph.D., Principal Rheologist,

ATS RheoSystems is available online in PDF format at:

https://qsenergy.box.com/ATS-AOT-SummaryRpt

16

Flow rate and treatment time are inversely proportional; as flow rate increases, the time crude oil particles spend within

the electric field decreases. As a result, higher flow rates require a stronger electric field to optimize AOT treatment.

U.S.

Department of Energy Field Test:

Save

the World Air, Inc. Viscosity Reduction Technology, Casper, Wyoming

Abstract:

The Rocky Mountain Oilfield Testing Center (RMOTC) conducted a field test on a prototype of the QS Energy in-line viscosity

reduction device at the Naval Petroleum Reserve No. 3 (NPR-3) located 35 miles north of Casper in Natrona County, Wyoming. The

in-line viscosity reduction device is designed to reduce the line-loss and increase the flow rate of crude oil traveling through

a commercial pipeline, thereby reducing the energy required for crude oil transportation. Reductions in line-loss and gains in

pump operation efficiency (i.e., reduced power consumption) were observed on the 4.4 mile 6” schedule 80 metal buried pipeline

test loop.

Test

Results:

Viscosity

Reduction The original viscosity was 81.6 cp. After the AOT device was turned on, it was reduced by 56.12 percent down to

48.95cp. After the AOT device was turned off, the crude oil in the section was gradually replaced by untreated crude oil and the

viscosity returned to the original value.

Pressure

Loss When the AOT device is turned on, the pressure loss is reduced by 56.12 percent, from 24.8 psi/mile (pounds per square

inch per mile) down to 14.87 psi/mile. After the device turned off, the crude oil in the section was replaced by untreated crude

oil and the pressure loss returns to the original value.

Conclusion:

Test

results indicate that the viscosity reduction device operated successfully and that the AOT 1.2H prototype delivers improved performance

over the original AOT prototype tested in October 2011. Pipeline line-loss and pump motor power consumption were reduced for a

given flow rate during the observed test. The device may hold potential for energy savings and increased pipeline flow rates for

the oil production and transportation industry.

Available

online at: https://qsenergy.box.com/DOE-STWA-RMOTC-Report

Market

Overview

The

energy sector continues to operate in a period of both rapid change and expansion. Due to the relatively recent and widespread

adoption of advanced oilfield drilling and completion technologies, known as enhanced oil recovery (EOR) techniques, enormous

reserves of “tight” oil and gas are now recoverable from shale formations throughout North America and the world.

This historic surge in upstream crude oil production has resulted in costly and persistent transportation bottlenecks when moving

upstream production to downstream storage, offloading facilities and refineries. This persistent and severe industrywide problem

is stimulating investments in new and existing pipeline infrastructure and a reliance on less desirable alternate forms of transport,

including rail and freight truck.

Since

the initial use of EOR or tertiary recovery techniques in the 1970s, oil and gas producers have progressively relied more heavily

on the application of gas and chemical injection as well as thermal recovery. These extraction techniques, coupled with a much

greater number of new wells in active oilfields, has raised the output of reservoirs by 30 to 60 percent above traditional primary

and secondary recovery practices17. Due to the rapid adoption of

advanced extraction technologies throughout the U.S. energy industry, a 34-year decline in domestic oil and gas production was

reversed in 2006. Historically high output from massive shale formations such as North Dakota’s Bakken, Texas’ Eagle

Ford and Permian Basin, Colorado’s Green River and Utah’s Uintah Basin continues to the present day.

Other

nations with significant exploitable shale formations include Russia, China, Argentina, Libya, Australia, Venezuela, Mexico and

dozens of others, providing a ready market for crude oil pipeline optimization technologies as production comes online. All told,

the U.S. Energy Information Administration estimates there to be 345 billion barrels of identified and recoverable shale oil worldwide.

Consequently,

oil production greatly exceeds the capacity of existing pipelines in the U.S., Canada and many other regions of the world, often

resulting in delivery delays to refineries, as well as reliance on less desirable rail and tanker truck transport. In the U.S.,

billions of dollars in lost revenue opportunities in leading oil producing states such as Texas, North Dakota, Alaska, California,

Colorado, Wyoming and Utah18 are attributed to production takeaway

constraints.

Market

Size

Industry

data and research by independent agencies such as the International Energy Agency (IEA) and IHS Global estimate that the world's

population currently consumes approximately 15 terawatts of energy in all forms annually. To put this into perspective, a terawatt

is equal to 1,000 gigawatts or roughly one thousand times the output of the largest coal-fired plants operating today. Based on

the known cost of sourcing, processing and transporting oil, gas, coal and other forms of usable energy, this places the value

of the global energy sector at roughly $6 trillion per year, or ten percent of the world’s collective economic output. By

2050, global power consumption is forecast to double to 30 terawatts.

17

EOR overview by the U.S. Dept. of Energy, Office of Fossil

Energy:

http://energy.gov/fe/science-innovation/oil-gas-research/enhanced-oil-recovery

18

“Pipeline Capacity; Ensuring the Resiliency the

US Requires”, Defense Transportation Journal, February, 2014:

http://www.ndtahq.com/documents/PipelineCapacity.pdf

According

to multiple studies, the primary drivers behind the continued worldwide increase in demand for energy are population and income

growth. World population is projected to reach 8.3 billion by 2030, adding 1.3 billion more consumers of oil, natural gas, coal

and other forms of energy. During the same time frame, world income is expected to effectively double from 2011 level. Primary

energy consumption is estimated to grow 2.1 percent annually between 2010 and 2020 and 1.3 percent per year from 2020 to 2030,

resulting in a 36 percent increase to global consumption by 203019.

Domestically,

the energy sector is the third largest industry, and the U.S. is one of the largest producers and consumers of energy. Since the

mid-1950s, oil has been the world’s leading energy source and today fossil fuel provides for around 36 percent of U.S. energy

demand with 70 percent refined into fuels used in transportation (gasoline, diesel, jet fuel, etc.)20.

The vast majority of U.S. crude oil production is transported by a network of pipelines, ranging from short “feeder”

lines to transmission lines stretching for hundreds or thousands of miles.

On

the demand side, the IEA forecasts that global oil markets will

remain strong as the market continues to rebalance following the precipitous drop in oil prices

from $110 in July to $40.00 as of November 2015. In its ‘Oil Market Report for April 2015’, IEA analysts have

revised upward global demand by 90,000 barrels per day to 93.6 million barrels per day (mbpd), a gain of 1.1 mbpd over last year.

Projected

Pipeline Infrastructure Investment

Among

the challenges facing the global crude oil production and transportation sectors, few are as intransigent or detrimental to the

industry as the transportation bottlenecks and well-to-market delivery delays that are endemic here in North America and overseas.

While new pipeline infrastructure projects are underway here in the U.S., Canada and in foreign markets, gaining legislative approval

is a lengthy process and their construction is highly capital-intensive.

19

“BP Energy Outlook 2030”, January 2013,

and “BP Statistical Review of World Energy”, June 2013, British Petroleum (BP p.l.c.):

https://www.bp.com/content/dam/bp/pdf/energy-economics/statistical-review-2015/

bp-statistical-review-of-world-energy-2015-full-report.pdf

20

Energy Information Administration, Monthly Energy Review,

July 2014:

http://www.eia.gov/totalenergy/data/monthly/previous.cfm

Although

pipelines are by far the safest and most economical transportation method21,

outmoded pipeline infrastructure constructed primarily in the 1950s and 1960s cannot provide the capacity necessary to move production

downstream to storage, refinery and offloading facilities. Consequently, delivery delays to refineries and reliance on less desirable

rail and tanker truck transport have increased exponentially since 2008 when the shale boom began in earnest. Data compiled by

the U.S. Energy Information Administration, IHS Global and the American Petroleum Institute identify billions in lost revenue

opportunities for E&P companies and tax collection agencies in leading oil producing states such as Texas, North Dakota, Alaska,

California, Colorado, Wyoming and Utah directly attributable to production takeaway constraints.

As

of 2013, the U.S. and Canadian midstream oil market was serviced by a total of 60,911 miles of crude oil pipelines, up 3,448 miles

or 6 percent over 2012 and up 11,647 miles or 23 percent over the past decade22.

Planned midstream pipeline projects are expected to bring an additional 20,000 miles of pipeline capacity over the 5 to 10 years.

However, the bulk of the active pipelines in the U.S. were constructed several decades ago, necessitating enormous capital investments

to maintain and update the aging pipeline infrastructure. Studies by research firm IHS Global Inc. estimate that between 2014

and 2020, an average of greater than $80 billion will be invested annually in U.S. midstream and downstream petroleum infrastructure23.

Despite

the recently depressed price level of the global oil benchmark (North Sea Brent crude, now trading between $50 and $60 a barrel,

roughly half the price of a year ago), experts forecast continued growth in crude oil pipeline capital expenditures. For example,

a study published by GlobalData in February of this year, ‘North America and

Russia to Dominate Global Oil and Gas Pipeline Construction by 2018’, estimates that U.S. oil and gas pipeline capital expenditures

for new construction will exceed $500 billion, resulting in the construction of 24,000 miles of new oil and gas pipeline capacity.

21

“Pipelines are Safest for Transportation of Oil

and Gas”, The Manhattan Institute, June 2013:

http://www.manhattan-institute.org/html/pipelines-are-safest-transportation-oil-and-gas-5716.html

22

“U.S. Liquids Pipeline Usage and Mileage Report”,

Association of Oil Pipe Lines, October 2014:

http://www.api.org/~/media/files/oil-and-natural-gas/pipeline/whats-new/us-liquids-pipeline-usage-mileage-report-oct-2014.pdf

23

“Oil & Natural Gas Transportation & Storage

Infrastructure: Status, Trends, & Economic Benefits”, IHS Global Inc., December 2013, page 20: http://www.api.org/~/media/Files/Policy/SOAE-2014/API-Infrastructure-Investment-Study.pdf

Fig.

4: Data from the International Energy Agency shows that the U.S. shale boom will continue to drive strong upstream

oil and gas output until at least 2020. QS Energy has diversified its target market by calibrating AOT functionality for a wide

spectrum of crude oil and condensate, an ultra-lightweight oil and the fastest growing segment of upstream production. Chart courtesy

of IEA Oil Market Report, February 2015.

QS

Energy’s AOT and Joule Heat Technologies are strategically aligned with the major requirements and challenges facing the

petroleum economy.

First,

AOT allows the midstream sector to increase capacity while remaining within maximum pressure requirements. The technology can

increase capacity for the industry and reduce reliance on truck and train transport, which has proven inefficient and often dangerous.

Second, AOT and JHT help to reduce operating expenses for pipeline operators. These technologies optimize per barrel energy expenditure,

which is especially important given the current oil price environment.

On

a global basis, the IEA projects that the energy sector will require $38 trillion of investment capital in existing and new capacity

by 2035 simply to meet growing demand for energy due to population growth24.

With the oil production boom in North America and overseas expected to continue to outstrip pipeline takeaway capacity, and downward

pressure on oil prices driving the need for ever greater operational efficiencies, AOT and JHT are uniquely positioned within

the industry as solutions capable of addressing both challenges.

24

“World Energy Outlook 2011”, International

Energy Agency, page 40:

https://www.iea.org/publications/freepublications/publication/WEO2011_WEB.pdf

Recently,

the softening of oil prices worldwide has incentivized producers and transporters to reduce costs and seek technologies that can

provide greater operational efficiencies. Industry analysts such as Rick Carr, principal and leader of Deloitte LLP’s oil

& gas operations and supply chain group, note that the drive to squeeze out better margins began in late 2013 when oil prices

fell to the $100 per barrel mark after a price expansion cycle that had been in place since 200025.

Capital-intensive extraction techniques necessary for unlocking tight oil and gas have boosted costs across the industry since

the shale boom began in earnest in 2008, and today’s low spot prices serve as a painful wakeup call for upstream and midstream

companies unaccustomed to scrutinizing overhead.

Research

conducted by IHS Global on behalf of the American Petroleum Institute shows that investment in the oil and gas midstream and downstream

infrastructure jumped 60 percent from 2010 to 2013, increasing from $56.3 billion to $89.6 billion. The report also estimates

that upwards of $90 billion of direct capital will be spent on oil and gas infrastructure this year alone. Data from the U.S.

Department of Energy suggests that developers of the nation’s midstream facilities will need to invest $200 billion to accommodate

expected shale-driven industry output by 2035.

In

answer to the energy industry’s pressing challenges, QS Energy is commercializing cost-efficient and proven “clean

tech” solutions for increasing the number of barrels of oil transported per day through existing pipeline gathering and

transmission systems. Our patent-protected product portfolio is dedicated to providing producers and transporters with highly

customizable industrial hardware capable of reducing operational overhead, increasing margins and delivering measurable competitive

advantages.

25

“Deloitte: Low Oil Prices Creating Need for More

Efficient Operations”, Rigzone.com, February 5, 2015:

http://www.rigzone.com/news/oil_gas/a/137095/Deloitte_Low_Oil_Prices_Creating_Need_for_More_Efficient_Operations

Target

Markets

The

oil and gas sector market can be segmented into three primary categories: Upstream Producers, Midstream Transporters and Downstream

Refiners:

| · | The

Upstream segment is involved in the exploration and production (E&P) of oil and gas. |

| · | Midstream

companies and partnerships transport oil and gas to markets via pipelines, rail and shipping,

and provide storage in the field and at the destination location. |

| · | The

Downstream sector refines oil and gas into finished products and, in cooperation with

manufacturers and retailers, markets and distributes fuels and other refined petroleum

products. |

Upstream

Producers

The

Upstream segment has the greatest exposure to commodity prices. When prices fall as has been the case recently, they feel the

brunt of this realignment. They also have the most to gain from additional flow throughput capacity and therefore would see immediate

benefit from QS Energy’s AOT and JHT solutions.

This

sector is typically more nimble and faces fewer barriers to entry. With clear financial upside for every additional barrel of

crude oil that they are able to transport, these companies are often open to new and innovative technology that will result in

greater efficiencies, lower costs and better cash flow. Upstream producers physically move the most volume of product. They are

customers to the Midstream transporters and enter into long-term contractual shipping obligations (tariff-based transportation

contracts) with them to secure the movement of product from their fields to the refiners and markets downstream.

Producers

make the spot market price for every barrel delivered to refinery, minus the transport costs, tariffs, and marketing discounts

associated with bringing the product to market. A rough rule of thumb for this market is that the further away they are from the

refinery, the higher the transport costs to deliver the product. Discussions with Upstream entities has uncovered strong interest

in solutions that unlock chokepoints from their field equipment to the transmission line loading terminals through viscosity reduction

(AOT) and optimizing flow by directly heating feedstock (JHT). In addition, this group would also benefit from transporters implementing

our AOT transmission-line series due to its ability to increase the overall flow capacity of pipelines transporting product from

loading terminals to market.

Midstream

Transporters

Midstream

entities move oil and gas from gathering lines to downstream storage and refineries. Functioning as “toll collectors”,

they earn fees whether oil prices are rising or falling. Their income is normally based on fixed-fee contracts, providing a great

deal more stability and predictability than in the upstream sector. Industry data shows ample evidence that upstream producers

are often caught with oversupply in relation to the takeaway capacity available to them. Inadequate pipeline infrastructure prompts

them to pull back their output (run fewer rigs) or suffer lower margins by using rail or freight truck to move production.

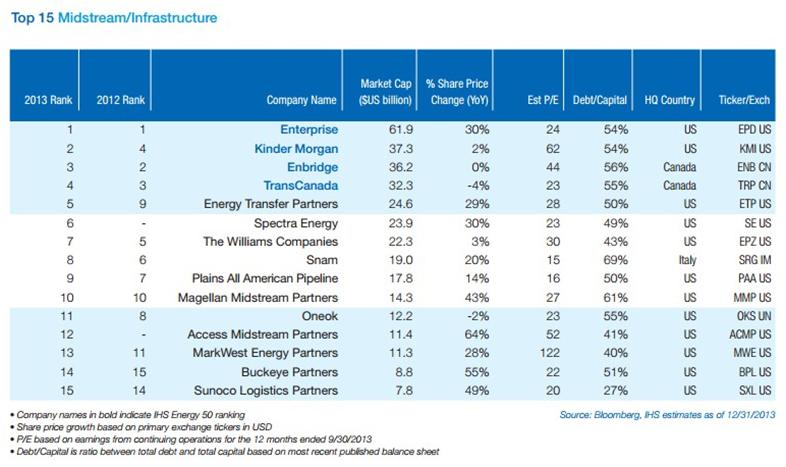

Fig.

5: Rankings of leading companies active in the North American Midstream sector, the principle target customer group for AOT.

Although primarily engaged in the operation of crude oil and natural gas pipelines, many are becoming vertically integrated and

are involved in the processing, storage and marketing of oil, gas, condensates and natural gas liquids. Chart courtesy of Bloomberg

and IHS Global.

Midstream

entities transport the bulk of the world’s crude oil output via the 400,000 miles of crude oil pipelines globally. Domestically,

they deliver a large percentage of the U.S. daily production of 9.2 million barrels per day through 160,000 miles of crude pipelines.

Midstream operators represent a strong and ready market for both AOT and JHT, and field test deployments for both solutions are

underway.

The

pipeline transport operators’ business model is to charge a tariff to transport each barrel of oil through their pipeline.

Due to the high daily volume of oil being transported and its value as a commodity, even incremental performance efficiencies

such as the 8 to 12 percent viscosity reduction demonstrated through a recent AOT beta field test is of high appeal from both

an overhead reduction and toll income increase perspective.

The

AOT and JHT performance enhancing capabilities that can be delivered to this market segment are derived from their ability to

increase flow, lower pipeline operating pressure and reduce the friction loss per mile of the crude oil as it passes through the

hundreds, or thousands, of miles of pipeline from the Upstream producers en route to the downstream refineries. Bottom line and

regulatory benefits can also be realized through increased volume rate capacities, higher toll rate income, reduced BTU per ton-mile

and reduced carbon emissions (CO2).

Midstream

Gathering Transporters

A

subset of the Midstream transporters sector is the gathering line operators, this group often functions as a part of the Upstream

producers’ operations, or within the Midstream transporter’s operations. Midstream gathering lines are the regional

transportation infrastructure that connect the upstream oilfields’ gathering lines to the Midstream long distance transporters’

main trunk lines. They are typically relatively short distance pipelines (20-100 miles) and have diameters between 6” and

12”.

Downstream

Refineries / Offloading Facilities

The

third market category of the industry that can potentially benefit from our solutions is the downstream refineries and rail, truck

and marine offloading sectors. The benefits of AOT viscosity reduction technology and JHT advanced heating equipment could be

significant, both from direct deployment and efficiencies realized in the upstream and midstream segments. Advantages for the

Downstream market sector would be generated through energy savings, reduced reliance on chemical based flow assurance additives,

reduced friction from turbulent pipelines, reduced Reid Vapor Pressures,26

and subsequent evaporation mitigation practices and hardware requirements as mandated by the U.S. Environmental Protection Agency27.

26

Reid vapor pressure (RVP) measures of the volatility of crude

oil and nonviscous petroleum liquids and is defined by the absolute vapor pressure exerted by a liquid at 100 °F (37.8 °C).

27

Oil and Natural Gas Air Pollution Standards, U.S. Environmental

Protection Agency: http://www.epa.gov/airquality/oilandgas/index.html

Our

Team

Executive

Management

Greggory

M. Bigger, Chairman of the Board, President and CEO was most

recently a Founding Partner of Rocfin Advisors, a strategic management consulting company providing advice and direction to a

variety of clients including companies in the energy, clean tech, and emerging technology markets. Prior, Mr. Bigger was Founder

and Board Member of The Bank of Santa Barbara, a regional California bank. Earlier in his career Mr. Bigger held a variety of

key management and leadership positions including U.S. Trust as a Vice President in the Private Client Group, and First Republic

Bank as a Vice President and Manager in the Private Banking Group. Mr. Bigger served in the United States Marine Corps Special

Operations Unit.

Under

Mr. Bigger’s leadership, QS Energy has established relationships with leading oil and gas producers and transporters in

North America, Europe, Africa and the Middle East. In driving the commercialization of the company’s technologies, he negotiated

equipment lease agreements with two $40+B market cap producers and transporters for testing of QSE’s viscosity reduction

technology on high-volume crude oil pipelines serving the largest crude oil transportation corridors in North America. Mr. Bigger

established all supply chain relationships for QSE, including vendor agreements with heavy equipment fabricators for the oil and

gas industry.

During

testing of a prototype of the Company’s AOT viscosity reduction system at the U.S. Department of Energy’s Rocky Mountain

Oil Field Testing Center (RMOTC), Mr. Bigger was instrumental in the rehabilitation of an existing pipeline at the Teapot

Dome oil field in Casper, Wyoming, which was developed into a 4.4 mile, 6-inch closed testing loop. He participated

in the installation and testing of the AOT using a SCADA system to monitor its performance, where significant viscosity reduction

was confirmed by RMOTC personnel. Working in cooperation with PetroChina and the China Petroleum Pipeline Bureau (CPP),

Mr. Bigger also managed a series of laboratory tests in the CPP test center in Shandong Province, near Beijing on crude oil from

the Daqing oil field, mainland China’s largest and most active reservoir.

Michael

McMullen, Controller, is responsible for financial and operational

leadership and establishing and implementing policies relevant to strategic planning and internal controls. Mr. McMullen has extensive

managerial and oversight experience with proven expertise in the areas of corporate governance, private and public capitalization,

asset valuation, risk assessment and in-depth understanding of operational and financial compliance and controls. In 2013, Mr.

McMullen designed, implemented and managed certification of the company’s Sarbanes-Oxley 404 compliant internal controls

and reporting procedures.

Prior

to joining QS Energy, Mr. McMullen served in senior executive capacities across a variety of industries. As a management consultant

and financial advisor to mid-market healthcare and technology entities, he specialized in providing growth and transition management

oversight to companies serving hospitals and cancer centers. In his role as Director of Strategic Development at Leema Energy

Resources he managed acquisition, valuation and due diligence cycles for the purchase and resale of energy-related assets acquired

from distressed savings and loan institutions, resulting in sale-leaseback, leveraged buyout and resale transactions totaling

$150 million. At FloWind Corporation Mr. McMullen negotiated domestic power plant contracts, international joint venture agreements