0001426506

false

0001426506

2023-07-06

2023-07-06

iso4217:USD

xbrli:shares

iso4217:USD

xbrli:shares

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K/A

CURRENT REPORT

Pursuant to Section 13 or Section 15(d) of the

Securities Exchange Act of 1934

Date of Report (Date of

earliest event reported): September 15, 2023 (July 6, 2023)

SMG INDUSTRIES INC.

(Exact name of registrant as specified in

its charter)

| Delaware |

|

000-54391 |

|

51-0662991 |

| (State or other jurisdiction |

|

(Commission |

|

(IRS Employer |

| of incorporation) |

|

File Number) |

|

Identification No.) |

| 20475 State Hwy 249, Suite 450 |

|

|

| Houston, Texas |

|

77070 |

| (Address of principal executive offices) |

|

(Zip Code) |

Registrant’s telephone number, including

area code:

(713-955-3497)

Check the appropriate box below if the Form 8-K

filing is intended to simultaneously satisfy the filing obligation to the registrant under any of the following provisions:

| ¨ |

Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| ¨ |

Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| ¨ |

Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| ¨ |

Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

| Title of each class |

|

Ticker symbol(s) |

|

Name of each exchange on which registered |

| None |

|

N/A |

|

N/A |

Indicate by check mark whether the registrant

is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the

Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging growth

company ¨

If

an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

EXPLANATORY NOTE

As

previously disclosed in the Current Report on Form 8-K filed by SMG Industries Inc. (the

“Company”) with the Securities and Exchange Commission on July 12, 2023 (the “Original

Report”), on July 7, 2023, the Company acquired all of the membership interests of: (i) Barnhart Fleet Maintenance, LLC,

a Pennsylvania limited liability company, (ii) Barnhart Transportation, LLC, a Pennsylvania limited liability company, (iii) Lake Shore

Global Solutions LLC, a Pennsylvania limited liability company, (iv) Lake Shore Logistics, LLC, a Pennsylvania limited liability company,

(v) Legend Equipment Leasing, LLC, a Pennsylvania limited liability company, and (vi) Route 20 Tank Wash LLC, a Pennsylvania limited liability

company (collectively, the “Barnhart Companies”), from Bryan S. Barnhart, Timothy W. Barnhart, Timothy W. Barnhart, as Trustee

of the Timothy W. Barnhart 2017 Irrevocable Trust, and certain affiliates.

This

Amendment No. 1 on Form 8-K/A is being filed by the Company to amend the Original Report solely to provide the financial statements and

pro forma financial information required by Item 9.01 of the Form 8-K that were not previously filed with the Original Report. Except

as provided herein, the disclosures made in the Original Report remain unchanged.

Item 9.01. Financial

Statements and Exhibits.

| (a) |

Financial Statements of Businesses Acquired.

The audited combined financial statements

of Barnhart Transportation, LLC and Affiliates as of and for the years ended December 31, 2022 and 2021 are filed herewith as Exhibit

99.1 and incorporated herein by reference.

The unaudited combined financial statements

of Barnhart Transportation, LLC and Affiliates as of June 30, 2023 and December 31, 2022 and for the six months ended June 30, 2023 and

2022 are filed herewith as Exhibit 99.2 and incorporated herein by reference. |

| (b) |

Pro Forma Financial Information.

The unaudited pro forma combined balance sheet of the Company as of

June 30, 2023 and unaudited pro forma combined statements of operations for the Company for the six months ended June 30, 2023 and for

the year ended December 31, 2022, and the notes to the unaudited pro forma combined financial statements, all giving effect to the acquisition

by the Company of the Barnhart Companies, are filed herewith as Exhibit 99.3 and incorporated herein by reference. |

SIGNATURES

Pursuant to the requirements

of the Securities Exchange Act of 1934, the Registrant has duly caused this Current Report to be signed on its behalf by the undersigned

hereunto duly authorized.

| Dated: September 15, 2023 |

SMG Industries Inc. |

| |

|

|

| |

By: |

/s/ Bryan S. Barnhart |

| |

Name: |

Bryan S. Barnhart |

| |

Title: |

Chief Executive Officer |

Exhibit 99.1

BARNHART TRANSPORTATION, LLC AND AFFILLIATES

North East, Pennsylvania

Combined

Financial Statements

For the years ended December 31, 2022 and 2021

and

Independent Auditor’s Report Thereon

| CONTENTS |

| |

|

|

|

| |

|

|

PAGE |

| |

|

|

|

| INDEPENDENT AUDITOR'S REPORT |

1 |

| |

|

|

|

| COMBINED FINANCIAL STATEMENTS |

3 |

| |

|

|

|

| |

Balance Sheets, December 31, 2022 and 2021 |

3 |

| |

|

|

|

| |

Statements for the years ended December 31, 2022 and 2021 |

4 |

| |

|

|

|

| |

|

Income and Members' Equity |

4 |

| |

|

|

|

| |

|

Cash Flows |

5 |

| |

|

|

|

| |

Notes to the Combined Financial Statements |

7 |

INDEPENDENT AUDITOR’S REPORT

Board of Directors

Barnhart Transportation, LLC and Affiliates

North East, Pennsylvania

Opinion

We have audited the accompanying combined financial

statements of Barnhart Transportation, LLC and Affiliates (Company), which comprise the combined balance sheets as of December 31, 2022

and 2021, and the related combined statements of income and members’ equity and cash flows for the years then ended, and the related

notes to the combined financial statements.

In our opinion, the combined financial statements

referred to above present fairly, in all material respects, the combined financial position of the Company as of December 31, 2022 and

2021, and the results of its combined operations and its combined cash flows for the years then ended in accordance with accounting principles

generally accepted in the United States of America.

Basis for Opinion

We conducted our audits in accordance with auditing

standards generally accepted in the United States of America. Our responsibilities under those standards are further described in the

Auditor’s Responsibilities for the Audit of the Combined Financial Statements section of our report. We are required to be independent

of the Company and to meet our other ethical responsibilities in accordance with the relevant ethical requirements relating to our audits.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Responsibilities of Management for the Combined

Financial Statements

Management is responsible for the preparation

and fair presentation of the combined financial statements in accordance with accounting principles generally accepted in the United States

of America, and for the design, implementation and maintenance of internal control relevant to the preparation and fair presentation of

combined financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the combined financial statements,

management is required to evaluate whether there are conditions or events, considered in the aggregate, that raise substantial doubt about

the Company’s ability to continue as a going concern within one year after the date that the combined financial statements are available

to be issued.

Auditor’s Responsibilities for the Audit

of the Combined Financial Statements

Our objectives are to obtain reasonable assurance

about whether the combined financial statements as a whole are free from material misstatement, whether due to fraud or error, and to

issue an auditor’s report that includes our opinion. Reasonable assurance is a high level of assurance but is not absolute assurance

and therefore is not a guarantee that an audit conducted in accordance with generally accepted auditing standards will always detect a

material misstatement when it exists. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting

from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations or the override of internal control. Misstatements,

including omissions, are considered material if there is a substantial likelihood that, individually or in the aggregate, they would influence

the judgment made by a reasonable user based on the combined financial statements.

In performing an audit in accordance with generally

accepted auditing standards, we:

| · | Exercise professional judgment and maintain professional skepticism throughout the audit. |

| · | Identify and assess the risks of material misstatement of the combined financial statements, whether due

to fraud or error, and design and perform audit procedures responsive to those risks. Such procedures include examining, on a test basis,

evidence regarding the amounts and disclosures in the combined financial statements. |

| · | Obtain an understanding of internal control relevant to the audit in order to design audit procedures

that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s

internal control. Accordingly, no such opinion is expressed. |

| · | Evaluate the appropriateness of accounting policies used and the reasonableness of significant accounting

estimates made by management, as well as evaluate the overall presentation of the combined financial statements. |

| · | Conclude whether, in our judgment, there are conditions or events, considered in the aggregate, that raise

substantial doubt about the Company’s ability to continue as a going concern for a reasonable period of time. |

We are required to communicate with those charged

with governance regarding, among other matters, the planned scope and timing of the audit, significant audit findings and certain internal

control related matters that we identified during the audit.

Pittsburgh, Pennsylvania

August 21, 2023

BARNHART TRANSPORTATION, LLC AND AFFILIATES

COMBINED

BALANCE SHEETS

| | |

December 31 | |

| | |

2022 | | |

2021 | |

| ASSETS | | |

| CURRENT ASSETS | |

| | | |

| | |

| Cash and cash equivalents | |

$ | 5,198,950 | | |

$ | 1,569,109 | |

| Investments | |

| 1,455,890 | | |

| 518,168 | |

| Accounts receivable, net | |

| 8,751,540 | | |

| 11,950,027 | |

| Other receivables | |

| 376,613 | | |

| 242,116 | |

| Notes receivable | |

| 60,514 | | |

| 31,663 | |

| Inventories | |

| 779,835 | | |

| 724,956 | |

| Prepaid and other | |

| 564,660 | | |

| 392,482 | |

| | |

| | | |

| | |

| Total Current Assets | |

| 17,188,003 | | |

| 15,428,520 | |

| | |

| | | |

| | |

| Tractors and transport equipment | |

| 11,091,411 | | |

| 9,721,352 | |

| Trailers | |

| 13,669,558 | | |

| 11,982,130 | |

| Leasehold improvements | |

| 1,171,775 | | |

| 1,171,775 | |

| Machinery and equipment | |

| 1,338,490 | | |

| 1,041,969 | |

| | |

| 27,271,234 | | |

| 23,917,227 | |

| Less - Accumulated depreciation | |

| (17,031,108 | ) | |

| (14,318,327 | ) |

| | |

| 10,240,126 | | |

| 9,598,900 | |

| | |

| | | |

| | |

| Intangible assets, net | |

| 79,096 | | |

| 56,363 | |

| Accounts receivable - related parties | |

| 6,956,072 | | |

| 5,846,292 | |

| Notes receivable | |

| 14,317 | | |

| 18,089 | |

| Operating right-of-use assets | |

| 2,211,742 | | |

| - | |

| | |

| | | |

| | |

| | |

$ | 36,689,357 | | |

$ | 30,948,163 | |

| | |

| | | |

| | |

| LIABILITIES AND MEMBERS' EQUITY | | |

| | |

| | | |

| | |

| CURRENT LIABILITIES | |

| | | |

| | |

| Accounts payable | |

$ | 2,554,060 | | |

$ | 3,252,672 | |

| Other liabilities | |

| 1,657,217 | | |

| 1,268,700 | |

| Current portion of operating lease liability | |

| 643,424 | | |

| - | |

| Current portion of long-term debt | |

| 2,783,226 | | |

| 2,663,795 | |

| | |

| | | |

| | |

| Total Current Liabilities | |

| 7,637,927 | | |

| 7,185,167 | |

| | |

| | | |

| | |

| OPERATING LEASE LIABILITY | |

| 1,568,319 | | |

| - | |

| | |

| | | |

| | |

| LONG-TERM DEBT | |

| 2,517,904 | | |

| 2,272,404 | |

| | |

| | | |

| | |

| MEMBERS' EQUITY | |

| 24,965,207 | | |

| 21,490,593 | |

| | |

| | | |

| | |

| | |

$ | 36,689,357 | | |

$ | 30,948,163 | |

See notes to combined financial statements.

BARNHART TRANSPORTATION, LLC AND AFFILIATES

COMBINED STATEMENTS OF INCOME AND MEMBERS' EQUITY

FOR

THE YEARS ENDED DECEMBER 31, 2022 AND 2021

| | |

2022 | | |

2021 | |

| REVENUE | |

$ | 81,749,226 | | |

$ | 61,797,013 | |

| | |

| | | |

| | |

| COST OF REVENUE | |

| 67,980,193 | | |

| 52,018,504 | |

| | |

| | | |

| | |

| Gross Profit | |

| 13,769,033 | | |

| 9,778,508 | |

| | |

| | | |

| | |

| OPERATING EXPENSES | |

| 8,332,154 | | |

| 6,687,908 | |

| | |

| | | |

| | |

| Income From Operations | |

| 5,436,879 | | |

| 3,090,601 | |

| | |

| | | |

| | |

| OTHER INCOME (EXPENSE) | |

| | | |

| | |

| Interest expense | |

| (142,532 | ) | |

| (133,774 | ) |

| Gain on sale of equipment | |

| 632,524 | | |

| 277,595 | |

| Other | |

| 68,770 | | |

| 1,319,532 | |

| Interest income | |

| 46,225 | | |

| 21,401 | |

| | |

| 604,987 | | |

| 1,484,755 | |

| | |

| | | |

| | |

| Net Income | |

| 6,041,865 | | |

| 4,575,355 | |

| | |

| | | |

| | |

| MEMBERS' EQUITY | |

| | | |

| | |

| Beginning of year | |

| 21,490,593 | | |

| 16,935,305 | |

| | |

| | | |

| | |

| Members' distributions | |

| (2,567,251 | ) | |

| (20,068 | ) |

| | |

| | | |

| | |

| End of year | |

$ | 24,965,207 | | |

$ | 21,490,593 | |

See notes to combined financial statements.

BARNHART TRANSPORTATION, LLC AND AFFILIATES

COMBINED STATEMENTS OF CASH FLOWS

FOR

THE YEARS ENDED DECEMBER 31, 2022 AND 2021

| | |

2022 | | |

2021 | |

| CASH FLOWS FROM OPERATING ACTIVITIES | |

| | | |

| | |

| Net income | |

$ | 6,041,866 | | |

$ | 4,575,355 | |

| Adjustments to reconcile net income to net cash provided by | |

| | | |

| | |

| operating activities: | |

| | | |

| | |

| Depreciation and amortization | |

| 4,382,647 | | |

| 3,994,876 | |

| Extinguishment of Paycheck Protection Program loan | |

| - | | |

| (1,214,124 | ) |

| Gain on sale of property and equipment | |

| (632,524 | ) | |

| (277,595 | ) |

| Net realized and unrealized losses (gains) on investments | |

| 62,278 | | |

| (106,645 | ) |

| Change in allowance for doubtful accounts | |

| 5,592 | | |

| (18,168 | ) |

| Changes in assets and liabilities: | |

| | | |

| | |

| Accounts receivable | |

| 3,172,157 | | |

| (5,674,071 | ) |

| Other receivables | |

| - | | |

| (5,993 | ) |

| Inventories | |

| (54,879 | ) | |

| (223,118 | ) |

| Prepaids and other | |

| (285,939 | ) | |

| (116,692 | ) |

| Accounts payable | |

| (510,486 | ) | |

| 579,941 | |

| Other liabilities | |

| 200,391 | | |

| 1,517,684 | |

| Net Cash Provided By Operating Activities | |

| 12,381,103 | | |

| 3,031,450 | |

| | |

| | | |

| | |

| CASH FLOWS FROM INVESTING ACTIVITIES | |

| | | |

| | |

| Purchases of property and equipment | |

| (1,687,107 | ) | |

| (694,699 | ) |

| Proceeds from sale of property and equipment | |

| 1,067,627 | | |

| 484,687 | |

| Purchases of intangible assets | |

| (22,481 | ) | |

| - | |

| Payments on notes receivable | |

| 52,405 | | |

| 28,613 | |

| Additions to notes receivable | |

| (77,484 | ) | |

| (79,599 | ) |

| Purchase of investments | |

| (1,000,000 | ) | |

| (500,000 | ) |

| Loans and advances to related parties, net | |

| (1,109,781 | ) | |

| (1,454,991 | ) |

| Net Cash Used In Investing Activities | |

| (2,776,821 | ) | |

| (2,215,989 | ) |

| | |

| | | |

| | |

| CASH FLOWS FROM FINANCING ACTIVITIES | |

| | | |

| | |

| Payments on long-term debt | |

| (3,407,191 | ) | |

| (3,161,244 | ) |

| Proceeds from Paycheck Protection Program loan | |

| - | | |

| 1,214,124 | |

| Member distributions | |

| (2,567,249 | ) | |

| (20,068 | ) |

| Net Cash Used In Financing Activities | |

| (5,974,440 | ) | |

| (1,967,188 | ) |

| | |

| | | |

| | |

| Net Increase (Decrease) in Cash and Cash Equivalents | |

| 3,629,842 | | |

| (1,151,727 | ) |

| | |

| | | |

| | |

| CASH AND CASH EQUIVALENTS | |

| | | |

| | |

| Beginning of year | |

| 1,569,109 | | |

| 2,720,836 | |

| | |

| | | |

| | |

| End of year | |

$ | 5,198,951 | | |

$ | 1,569,109 | |

| | |

2022 | | |

2021 | |

| SUPPLEMENTAL DISCLOSURES OF CASH FLOW INFORMATION | |

| | | |

| | |

| Cash paid during the year for interest | |

$ | 142,532 | | |

$ | 133,774 | |

| | |

| | | |

| | |

| SUPPLEMENTAL SCHEDULE OF NONCASH INVESTING AND FINANCING ACTIVITIES | |

| | | |

| | |

| Capital expenditures funded by issuance of long-term debt | |

$ | 3,772,122 | | |

$ | 2,951,110 | |

See notes to combined financial statements.

BARNHART TRANSPORTATION, LLC AND AFFILIATES

NOTES TO COMBINED FINANCIAL STATEMENTS

DECEMBER 31, 2022 AND 2021

NOTE 1 - ORGANIZATION

Barnhart Transportation,

LLC and Affiliates (collectively, the Company) is a transportation solution provider offering a diversified range of services to clients

and their specific transportation needs. The Company specializes in pneumatic dry bulk sand and cement, flatbed, step-deck, double-drop,

RGN, over-dimensioned, heavy haul, dry van, nonhazardous liquids, intermodal drayage and LTL shipments within the United States, Canada

and Mexico. The Company also has a fleet maintenance division that handles most of the maintenance required on its equipment along with

a freight brokerage division that works with partner carriers to provide innovative freight solutions. Additionally, the Company has integrated

international freight forwarding, commercial tank cleaning, warehousing and transloading services that allow for comprehensive solutions,

that cater to diverse customer needs.

NOTE 2 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

A summary of

significant accounting policies consistently applied by management in the preparation of the accompanying combined financial statements

are as follows:

Basis of Combination

- The accompanying combined financial statements include the financial position, results of operations and cash flows of Barnhart Transportation,

LLC; Lake Shore Logistics, LLC; Legend Equipment Leasing, LLC; Barnhart Fleet Maintenance, LLC; Lake Shore Global Solutions, LLC; and

Route 20 Tank Wash, LLC, all of which are under common control and ownership. All intercompany balances and transactions have been eliminated

in combination.

Use of Estimates

- The preparation of combined financial statements in conformity with accounting principles generally accepted in the United States of

America (U.S. GAAP) requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and

disclosure of contingent assets and liabilities at the date of the combined financial statements and the reported amounts of revenues

and expenses during the reporting period. Actual results could differ from those estimates.

Cash and Cash

Equivalents - Cash and cash equivalents include all cash balances and highly liquid investments with an initial maturity of three months

or less. The Company places its cash with high-credit quality financial institutions. At times, such investments may be in excess of the

Federal Deposit Insurance Corporation insurance limit.

Investments -

Valued at the daily closing price as reported by the fund, investments in marketable securities with readily determinable fair values

are stated at fair value based on quoted prices in active markets. The Company discloses the category of assets and liabilities measured

at fair value into one of three different levels, depending on the assumptions (i.e., inputs) used in the valuation. Level 1 provides

the most reliable measure of fair value, whereas Level 3 generally requires significant management judgment. Financial assets and liabilities

are classified in their entirety based on the lowest level of input significant to the fair value measurement, and generally approximate

fair value either due to their short-term nature or terms the Company could obtain in the current market. The Company does not have any

Level 3 financial assets or liabilities as of December 31, 2022 and 2021.

BARNHART TRANSPORTATION, LLC AND AFFILIATES

NOTES TO COMBINED FINANCIAL STATEMENTS

DECEMBER 31, 2022 AND 2021

NOTE 2 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

The following

table presents the cost basis and fair value of the Company’s major categories of investments:

| | |

December 31, 2022 | | |

December 31, 2021 | |

| | |

Cost Basis | | |

Fair Value | | |

Cost Basis | | |

Fair Value | |

| Investments: | |

| | | |

| | | |

| | | |

| | |

| Cash and bank deposits | |

$ | 71,565 | | |

$ | 71,565 | | |

$ | 12,243 | | |

$ | 12,243 | |

| Mutual funds and exchange-traded funds | |

$ | 1,428,435 | | |

$ | 1,384,325 | | |

$ | 487,757 | | |

$ | 505,925 | |

| Total | |

$ | 1,500,000 | | |

$ | 1,455,890 | | |

$ | 500,000 | | |

$ | 518,168 | |

The following

table depicts the level in the fair value hierarchy of the input used to estimate fair value of investments measured on a recurring basis

as of December 31, 2022 and 2021:

| | |

Fair Value | | |

Level 1 Inputs | | |

Level 2 Inputs | | |

Level 3 Inputs | |

| As of December· 31, 2022 | |

| | | |

| | | |

| | | |

| | |

| Cash and bank deposits | |

$ | 71,565 | | |

$ | 71,565 | | |

$ | - | | |

$ | - | |

| Mutual funds and exchange-traded funds | |

$ | 1,384,325 | | |

$ | 1,384,325 | | |

$ | - | | |

$ | - | |

| | |

| | | |

| | | |

| | | |

| | |

| As of December· 31, 2021 | |

| | | |

| | | |

| | | |

| | |

| Cash and bank deposits | |

$ | 12,243 | | |

$ | 12,243 | | |

$ | - | | |

$ | - | |

| Mutual funds and exchange-traded funds | |

$ | 505,925 | | |

$ | 505,925 | | |

$ | - | | |

$ | - | |

The following table

presents the detail of income (loss) from investments for the years ended December 31:

| | |

2022 | | |

2021 | |

| Interest income | |

$ | 29,352 | | |

$ | 3,049 | |

| Unrealized gain (loss) on investment | |

| (73,617 | ) | |

| 17,552 | |

| Realized gain (loss) on investment | |

| (30,758 | ) | |

| - | |

| Total | |

$ | (75,023 | ) | |

$ | 20,601 | |

BARNHART TRANSPORTATION, LLC AND AFFILIATES

NOTES TO COMBINED FINANCIAL STATEMENTS

DECEMBER 31, 2022 AND 2021

NOTE 2 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

Realized and unrealized

gains and losses, interest and dividends are recognized in other income in the combined statements of income and members’ equity.

Accounts Receivable

- Accounts receivable are reported at the amount management expects to collect from outstanding balances. The Company performs ongoing

credit evaluations of its customers and generally does not require collateral. Provisions are made for estimated uncollectible trade accounts

receivable. The Company’s estimate of the allowance is based on historical collection experience, a review of the current status

of trade receivables and judgment. Decisions to charge off receivables are based on management’s judgment after consideration of

facts and circumstances surrounding potential uncollectible accounts. The allowance for doubtful accounts as of December 31, 2022 and

2021 is approximately $57,000 and $51,000, respectively.

Leases - As of

January 1, 2022, leases are recognized under Accounting Standards Update (ASU) No. 2016-02 Leases (Topic 842) (ASU 2016-02). The Company

evaluates leases based on the underlying asset groups. The assets currently underlying the Company’s leases include real estate

(primarily buildings, office space, land and drop yards). Management’s significant assumptions and judgements include the determination

of the discount rate (discussed below), as well as the determination of whether a contract contains a lease. A contract contains a lease

if there is an identified asset and the Company has the right to control the asset.

Operating lease

right-of-use assets represent the Company’s right to use an underlying asset for the lease term, and the lease liabilities represent

the Company’s obligation to make lease payments arising from the lease. In the accompanying statements of income and members’

equity, rent expense for operating lease payments is recognized on a straight-line basis of the lease term. The Company’s operating

real estate leases all have lease terms of five years and they do not include auto-renewal provisions.

Topic 842 allows

lessees an option to not recognize right-of-use assets and lease liabilities arising from short-term leases. The Company does not have

any leases twelve months or less.

Operating lease right-of-use

assets and lease liabilities are recognized at the commencement date based on the present value of the lease payments over the lease term.

The Company’s lease liabilities are recognized based on the present value of the remaining fixed lease payments, over the lease

term, using a discount rate. The discounted rates for leases were determined based on U.S. Daily Treasury Par Yield Curve rates as of

January 1, 2022.

See Note 9 for

additional disclosures regarding the Company’s operating leases, and adoption of Topic 842.

Concentration

- Revenue recognized from the Company’s two largest customers for the years ended December 31, 2022 and 2021 approximated 33% and

35%, respectively, of total revenue. The balance due from the Company’s largest customer as of December 31, 2022 and 2021 approximated

28% and 43%, respectively, of accounts receivable.

Inventories

- Inventories, consisting mainly of tires and transportation-related supplies, are stated at the lower of cost or net realizable value

determined by the first-in, first-out method. Appropriate consideration is given to obsolescence, excessive levels, deterioration and

other factors in evaluating net realizable value.

BARNHART TRANSPORTATION, LLC AND AFFILIATES

NOTES TO COMBINED FINANCIAL STATEMENTS

DECEMBER 31, 2022 AND 2021

NOTE 2 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

(Continued)

Fixed Assets

- Fixed assets are recorded at the lower of cost or market. Repairs and maintenance that do not extend the lives of the applicable assets

are charged to expense as incurred. Depreciation is provided over the estimated useful lives of the related assets using the straight-line

method. The estimated useful lives of the related assets are as follows:

| Buildings and improvements |

15 - 40 years |

| Transportation equipment |

3 - 10 years |

| Furniture and fixtures |

3 - 7 years |

Depreciation expense for the years then ended December 31,

2022 and 2021 amounted to approximately

$4,366,000 and $3,961,000, respectively.

The Company reviews

the carrying value of fixed assets for impairment whenever events and circumstances indicate that the carrying value of an asset might

not be recoverable from the estimated future cash flows expected to result from its use a eventual disposition. In cases where undiscounted

expected future cash flows are less than the carrying value, an impairment loss is recognized equal to an amount by which the carrying

value exceeds the fair value of assets. The factors considered by management in performing this assessment include current operating results,

trends and prospects, as well as the effects of obsolescence, demand, competition and other economic factors. Based on management’s

evaluation, there was no impairment at December 31, 2022 and 2021.

Intangible assets

subject to amortization consist of software and computer licenses. The Company is amortizing the intangible assets on a straight-line

basis over various periods based on the asset’s future economic benefit. Amortization related to intangible assets for the years

ended December 31, 2022 and 2021 amounted to approximately $17,000 and $34,000, respectively.

Revenue Recognition

- Revenues are recognized over time as control of the promised services is transferred to the Company’s customers in an amount that

reflects the consideration the Company expects to be entitled to in exchange for those services.

The Company generates

revenues from billings for transportation services under contracts with customers, generally on a rate per mile or fixed rate per shipment,

based on origin and destination of the shipment. The Company’s performance obligation arises when it receives a shipment order to

transport a customer’s freight and is satisfied upon delivery of the shipment. The transaction price may be defined in a transportation

services agreement or negotiated with the customer prior to accepting the shipment order. A customer may submit several shipment orders

for transportation services at various times throughout a service agreement term, but each shipment represents a distinct service that

is a separately identified performance obligation. The Company often provides additional or ancillary services as part of the shipment

(such as loading/unloading and stops in transit), which are not distinct or are not material in the context of the contract; therefore,

the revenues for these services are recognized with the freight transaction price. The average transit time to complete a shipment is

approximately two days. Invoices for transportation services are typically generated soon after shipment delivery and, although payment

terms and conditions vary by customer, are generally due within 30 days after the invoice date.

The Company also

generates revenues from equipment leases, to include terminal rental adjustment clause (TRAC) leases. Equipment leases are recognized

and billed monthly and renewed annually. TRAC leases are a set term for anywhere from one to five years with weekly payments and a 20%

balloon payment at the conclusion of the lease term.

BARNHART TRANSPORTATION, LLC AND AFFILIATES

NOTES TO COMBINED FINANCIAL STATEMENTS

DECEMBER 31, 2022 AND 2021

NOTE 2 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

(Continued)

The combined statements

of income and members’ equity reflect recognition of transportation revenues (including fuel surcharge revenues) and related direct

costs over time as the shipment is being delivered. The Company uses distance shipped (for the Truckload segment) and transit time (for

the Logistics segment) to measure progress and the amount of revenues recognized over time, as the customer simultaneously receives and

consumes the benefit. Determining a measure of progress requires the Company to make judgments that affect the timing of revenues recognized.

The Company has determined that the methods described provide a faithful depiction of the transfer of services to the customer.

For shipments

where a third-party capacity provider (including independent contractors under contract with the Company) is utilized to provide some

or all of the service, the Company evaluates whether it is the principal (i.e., report revenues on a gross basis) or the agent (i.e.,

report revenues on a net basis). Generally, the third party reports such revenues on a gross basis; that is, it recognizes both revenues

for the service it bills to the customer and rent and purchased transportation expense for transportation costs it pays to the third-party

provider. Where the Company is the principal, it controls the transportation service before it is provided to the Company’s customers,

which is supported by the Company being primarily responsible for fulfilling the shipment obligation to the customer and having a level

of discretion in establishing pricing with the customer.

Rental income related

to the Company’s leasing arrangements is recognized when earned over the life of the lease agreement. Another source of revenue

is through the Company’s service garage and the repair work that is completed on all of the Company’s assets, including both

tractors and trailers. Service work is performed for outside customers along with the Company’s owner-operators and is recognized

over the term of the service agreement.

Practical

Expedient - The Company has elected to apply the practical expedient in Financial Accounting Standards Board (FASB) ASU No. 2014-09 Revenue

from Contracts with Customers (Topic 606) to not disclose the value of remaining performance obligations for contracts with an original

expected length of one year or less. Remaining performance obligations represent the transaction prices allocated to future reporting

periods for freight shipments started but not completed at the reporting date at which the Company expects to recognize revenues in the

period subsequent to the reporting date. Transit times generally average two days.

Income Taxes

- The combined companies have been formed as limited liability companies under the laws of the Commonwealth of Pennsylvania. The members

of each of the Company’s affiliates, Barnhart Transportation, LLC; Lakeshore Logistics, LLC; Barnhart Fleet Maintenance, LLC; and

Legend Equipment Leasing, LLC, have elected under the Internal Revenue Code to be taxed as an S corporation. The members of each of the

Company’s affiliates, Lake Shore Global Solutions, LLC and Route 20 Tank Wash, LLC, have elected under the Internal Revenue Code

to be taxed as a partnership. In lieu of corporate income taxes, the members of an S corporation and partnership will be taxed on their

appropriate share of the Company's taxable income; therefore, no provision or liability for federal or state income taxes has been included

in the combined financial statements.

A tax

position is a position in a previously filed tax return or a position expected to be taken in a future tax filing that is reflected

in measuring current or deferred income tax assets and liabilities. Tax positions shall be recognized only when it is more likely

than not (likelihood of greater than 50%), based on technical merits, that the position will be sustained. Tax positions that meet

the more-likely-than-not threshold should be measured using a probability-weighted approach as the largest amount of tax benefit

that is greater than 50% likely of being realized upon settlement. Whether the more-likely-than-not recognition threshold is met for

a tax position is a matter of judgement based on the individual facts and circumstances of that position evaluated in light of all

available evidence. If tax is incurred, the Company would accrue interest and penalties related to uncertain tax positions in income

tax expense.

BARNHART TRANSPORTATION, LLC AND AFFILIATES

NOTES TO COMBINED FINANCIAL STATEMENTS

DECEMBER 31, 2022 AND 2021

NOTE 2 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

(Continued)

The Company has

assessed the tax positions it has taken or expects to take in its tax return. As of December 31, 2022 and 2021, no liability for uncertain

tax positions was required to be recorded. The Company’s tax returns are subject to examination by major taxing jurisdictions for

years after 2019.

Advertising - The

Company expenses advertising costs as they are incurred. Advertising expenses for the years ended December 31, 2022 and 2021 are approximately

$77,000 and $25,000, respectively.

NOTE 3 - RELATED-PARTY TRANSACTIONS

Related-party transactions arise in the

ordinary course of business and are summarized as follows:

The Company has recorded

amounts due from related parties of approximately $6,956,000 and $5,846,000 as of December 31, 2022 and 2021, respectively. These balances

are classified as long-term, as repayment is expected beyond one year from the date of the Company’s combined balance sheets. These

balances fluctuate in the normal course of business and do not bear interest.

The Company has recorded

amounts payable to related parties of approximately $426,000 and $815,000 as of December 31, 2022 and 2021, respectively. These balances

are classified as accounts payable on the Company’s combined balance sheets. These balances fluctuate in the normal course of business

and do not bear interest.

The Company leases

office and warehouse space under a noncancelable operating lease from an entity owned by the members. Rent is payable in monthly installments

of approximately $55,000 through December 2026.

Rent expense for related-party leases

was approximately $687,000 and $487,000 for the years ended

December 31, 2022 and 2021, respectively.

NOTE 4 - NOTES RECEIVABLE

The Company has

notes receivable from sale of the services and parts, to include overhauls or placements to owner operators in the normal course of business.

The notes are payable in weekly installments of principal and interest at 12%. The notes receivable have a term of no more than five years

with maturities ranging from

2023 to 2024.

BARNHART TRANSPORTATION, LLC AND AFFILIATES

NOTES TO COMBINED FINANCIAL STATEMENTS

DECEMBER 31, 2022 AND 2021

NOTE 5 - LONG-TERM DEBT

Long-term debt at December 31 consists

of the following:

| | |

2022 | | |

2021 | |

| Various notes payable with Citizens Bank, payable in monthly installments aggregating approximately $287,000, including interest at rates ranging from 1.45% to 6.05%, with expirations ranging from 2023 to 2025. | |

$ | 5,301,130 | | |

$ | 4,936,199 | |

| Less - Current portion of long-term debt | |

| 2,783,226 | | |

| 2,663,795 | |

| | |

$ | 2,517,904 | | |

$ | 2,272,404 | |

Long-term debt is secured by substantially

all corporate assets of the combined companies.

The aggregate annual principal payments required on the long-term

debt subsequent to December 31,

2022 are as follows:

| Year Ending | | |

| |

| December 31 | | |

Amount | |

| | 2023 | | |

$ | 2,783,226 | |

| | 2024 | | |

| 1,876,766 | |

| | 2025 | | |

| 641,138 | |

| | | | |

$ | 5,301,130 | |

NOTE 6 - LINES OF CREDIT

The Company has

a $1,750,000 revolving line of credit. Advances on the line are payable on demand and carry an interest rate of 1.50% above Secured Overnight

Financing Rate (SOFR). The credit line is secured by substantially all corporate assets of the combined companies. There were no outstanding

advances on the line at December 31, 2022 and 2021. The credit line is renewable on an annual basis and is set to expire in October 2023.

BARNHART TRANSPORTATION, LLC AND AFFILIATES

NOTES TO COMBINED FINANCIAL STATEMENTS

DECEMBER 31, 2022 AND 2021

NOTE 6 - LINES OF CREDIT (Continued)

The Company has

a $4,000,000 non-revolving line of credit, which is to be used to finance large equipment purchases. Each advance on the credit line shall

be repaid in equal monthly installments of principal and interest based upon up to a five-year amortization period. The interest rate

payable on each advance outstanding shall be a

fixed rate equal

to the prevailing market rate generally charged by the bank on commercial loans of similar nature, risk and duration as quoted by the

bank to the Company on or before the date of each advance. There were no outstanding advances on the line at December 31, 2022 and 2021.

The credit line is secured by substantially all corporate assets of the Barnhart Transportation, LLC, Lake Shore Logistics, LLC, Legend

Equipment Leasing, LLC, and Barnhart Fleet Maintenance, LLC and is renewable on an annual basis.

The Company’s

credit agreements with the bank contain certain financial covenants. The Company was in compliance with all terms and provisions of the

agreements at December 31, 2022 and 2021.

NOTE 7 - EMPLOYEE BENEFIT PLAN

The Company

sponsors a voluntary 401(k) profit-sharing plan covering substantially all of its employees. The plan provides for Company contributions

to match voluntary employee contributions up to 3% of eligible compensation and to match 50% of eligible compensation between 3% and 5%.

Employer contribution obligations for the years ended December 31, 2022 and 2021 were approximately $196,000 and $144,000, respectively.

NOTE 8 - PAYCHECK PROTECTION PROGRAM

On January 21,

2021, the Company was granted loans from Citizens Bank in the aggregate amount of $1,227,624. All loans were pursuant to the Paycheck

Protection Program (the PPP) under Division A, Title I of the Coronavirus Aid, Relief, and Economic Security Act (the CARES Act), which

was enacted March 27, 2020. Under terms of the PPP, PPP loans and accrued interest are forgivable after 24 weeks as long as the borrower

uses the loan proceeds for eligible purposes, including payroll, benefits, rent and utilities, and maintains its payroll levels. The amount

of loan forgiveness will be reduced if the borrower terminates or reduces salaries during the forgiveness period.

As of December

31, 2021, the Company used the entire loan proceeds to fund its payroll expenses and has received forgiveness for all PPP loans from the

Small Business Administration. The Company recorded these loans in accordance with FASB Accounting Standards Codification (ASC) 470, Debt,

and, as such, the balances were recorded as debt on the combined balance sheets until forgiveness was received. Upon forgiveness, the

Company recognized the entire extinguished amount as other income on the combined statements of income and members’ equity for the

year ended December 31, 2021.

BARNHART TRANSPORTATION, LLC AND AFFILIATES

NOTES TO COMBINED FINANCIAL STATEMENTS

DECEMBER 31, 2022 AND 2021

NOTE 9 - LEASES

The FASB issued

ASU 2016-02 Leases, which sets out the principles for the recognition, measurement, presentation and disclosure of leases for both parties

to a contract (i.e., lessees and lessors). The new standard requires lessees to apply a dual approach, classifying leases as either finance

or operating leases based on the principle of whether or not the lease is effectively a financed purchase by the lessee. This classification

will determine whether lease expense is recognized based on an effective interest method or on a straight-line basis over the term of

the lease. A lessee is also required to record a right-of-use asset and a lease liability for all leases with a term of greater than 12

months regardless of their classification. Leases with a term of 12 months or less will be accounted for similar to existing guidance

for operating leases today. The new standard requires lessors to account for leases using an approach that is substantially equivalent

to existing guidance for sales-type leases, direct financing leases and operating leases. ASU 2016-02 supersedes the previous leases standard,

Leases (ASC 840).

The Company adopted

ASU 2016-02, Leases, which is codified in ASC 842, as of January 1, 2022. The Company elected the optional transition method as a part

of utilizing the modified retrospective approach in applying the new lease standard and have recognized right-of-use assets of approximately

$2,842,000 and long-term lease liabilities of approximately $2,199,000, with current portion of approximately $643,000, as of January

1, 2022.

In addition,

the Company elected the package of practical expedients provided under the guidance. The practice expedient package applies to leases

that commenced prior to adoption of the new standard and permits companies not to reassess whether existing or expired contracts are or

contain a lease, the lease classification, and any initial direct costs for any existing leases.

The Company has

recognized a right-to-use asset on December 31, 2022 in the amount of $2,211,742. The Company has also recognized a long-term lease liability

of $1,568,319 with a current portion of $643,424. Operating lease right-of-use assets and operating lease liabilities are recognized based

on the present value of the future lease payments over the term. The discounted rates for leases were determined based on U.S. Daily Treasury

Par Yield Curve rates as of January 1, 2022. The leases have maturity dates from 2023 through 2026.

The Company’s

leases are solely operating real estate leases that include offices, garage space and drop yards. Each of the Company's operating leases

are leased from related party entities that are under common ownership. The Company’s leases have a fixed cost and do no include

any variable components. None of the Company’s leases contain restrictions or covenants that restrict the Company from incurring

other financial obligations. The Company does not have any finance leases.

Lease Cost - The Company’s

lease expense within the accompanying combined statements of income and members’ equity was approximately $687,000 for the year

ended December 31, 2022.

BARNHART TRANSPORTATION, LLC AND AFFILIATES

NOTES TO COMBINED FINANCIAL STATEMENTS

DECEMBER 31, 2022 AND 2021

NOTE 9 - LEASES (Continued)

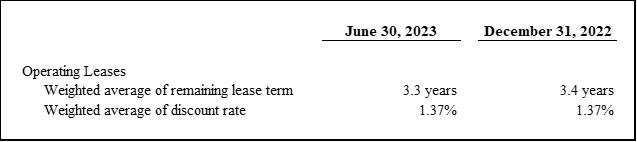

Lease Liability

Calculation Assumptions - The assumptions underlying the calculation of the Company’s right-to-use assets and lease liabilities

are disclosed below:

| |

2022 |

| Operating Leases |

|

| Weighted average of remaining lease term |

3.4 years |

| Weighted average of discount rate |

1.37% |

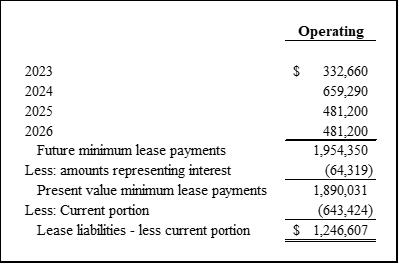

Maturity analysis

of lease liabilities (as lessee) - As of December 31, 2022, estimated annual maturities of lease liabilities for the year ending December

31, 2023 and thereafter were as follows:

| | |

Operating | |

| 2023 | |

$ | 665,320 | |

| 2024 | |

| 659,290 | |

| 2025 | |

| 481,200 | |

| 2026 | |

| 481,200 | |

| Future minimum lease payments | |

| 2,287,010 | |

| Less: amounts representing interest | |

| (75,267 | ) |

| Present value minimum lease payments | |

| 2,211,743 | |

| Less: Current portion | |

| (643,424 | ) |

| Lease liabilities - less current portion | |

$ | 1,568,319 | |

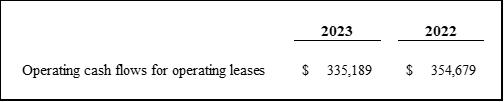

The following

table sets forth approximate cash paid for amounts included in the measurement of lease liabilities for the year ended December 31, 2022:

| | |

2022 | |

| Operating cash flows for operating leases | |

$ | 687,000 | |

BARNHART TRANSPORTATION, LLC AND AFFILIATES

NOTES TO COMBINED FINANCIAL STATEMENTS

DECEMBER 31, 2022 AND 2021

NOTE 9 - LEASES (Continued)

Prior period

amounts were not adjusted and will continue to be reported under ASC 840. The below table was the schedule of minimum lease payments required

as of December 31, 2021:

| Year Ending | | |

| |

| December 31 | | |

Amount | |

| 2022 | | |

$ | 701,320 | |

| 2023 | | |

| 701,320 | |

| 2024 | | |

| 695,290 | |

| 2025 | | |

| 677,200 | |

| 2026 | | |

| 677,200 | |

| Thereafter | | |

| 117,000 | |

| | | |

$ | 3,569,330 | |

During the year ended December 31,

2021, the Company's operating lease expense was approximately $487,000.

NOTE 10 - CONTIGENCIES AND COMMITMENTS

The Company, from time to time, is involved in

legal and other proceedings arising in the ordinary course of business. The Company believes that there are no significant claims or litigation

pending that could, individually or in the aggregate, have a material adverse effect on its combined financial statements.

NOTE 11 - SUBSEQUENT EVENTS

Management has evaluated subsequent events through

July 20, 2023, the date on which the combined financial statements were available to be issued. On July 7, 2023, the Company was acquired

by SMG Industries, Inc., a Texas based transportation company. The acquisition was complete for a total consideration of approximately

$55,750,000 in cash, stock and other assets. As a result of the acquisition, the Company, is now a wholly owned subsidiary of SMG Industries,

Inc. There are no other subsequent events that have occurred that would require adjustments to disclosures in the financial statements.

Exhibit 99.2

| BARNHART TRANSPORTATION, LLC AND AFFILLIATES |

| North East, Pennsylvania |

| |

| Combined Financial Statements |

| As of June 30, 2023 and December 31, 2022 and |

| for the six-month periods ended June 30, 2023 and 2022 |

| |

| and Independent Accountant's Review Report Thereon |

INDEPENDENT ACCOUNTANT’S REVIEW REPORT

Board of Directors

Barnhart Transportation, LLC and Affiliates

North East, Pennsylvania

We have reviewed the accompanying combined financial

statements of Barnhart Transportation, LLC and Affiliates (Company), which comprise the combined balance sheets as of June 30, 2023 and

December 31, 2022, and the related combined statements of income and members’ equity and cash flows for the six-month periods ended

June 30, 2023 and 2022, and the related notes to the combined financial statements (financial statements). A review includes primarily

applying analytical procedures to management’s financial data and making inquiries of company management. A review is substantially

less in scope than an audit, the objective of which is the expression of an opinion regarding the financial statements as a whole. Accordingly,

we do not express such an opinion.

Management’s Responsibility for the Financial

Statements

Management is responsible for the preparation

and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of

America (U.S. GAAP); this includes the design, implementation and maintenance of internal control relevant to the preparation and fair

presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Accountant’s Responsibility

Our responsibility is to conduct the review engagement

in accordance with Statements on Standards for Accounting and Review Services promulgated by the Accounting and Review Services Committee

of the American Institute of Certified Public Accountants. Those standards require us to perform procedures to obtain limited assurance

as a basis for reporting whether we are aware of any material modifications that should be made to the financial statements for them to

be in accordance with U.S. GAAP. We believe that the results of our procedures provide a reasonable basis for our conclusion.

We are required to be independent of the Company

and to meet our other ethical responsibilities, in accordance with the relevant ethical requirements related to our review.

Accountant’s Conclusion

Based on our reviews, we are not aware of any

material modifications that should be made to the accompanying financial statements in order for them to be in accordance with U.S. GAAP.

Pittsburgh, Pennsylvania

September 14, 2023

| BARNHART TRANSPORTATION, LLC AND AFFILIATES |

| |

| COMBINED BALANCE SHEETS |

| |

| | |

| | |

| |

| | |

June 30 | | |

December 31 | |

| | |

2023 | | |

2022 | |

| ASSETS |

| | |

| | |

| |

| CURRENT ASSETS | |

| | |

| |

| Cash and cash equivalents | |

| 5,599,435 | | |

$ | 5,198,950 | |

| Investments | |

| 1,158,974 | | |

| 1,455,890 | |

| Accounts receivable, net | |

| 6,621,281 | | |

| 8,751,540 | |

| Other receivables | |

| 518,632 | | |

| 376,612 | |

| Notes receivable | |

| 40,521 | | |

| 60,514 | |

| Inventories | |

| 762,164 | | |

| 779,835 | |

| Prepaid and other | |

| 1,030,822 | | |

| 564,660 | |

| | |

| | | |

| | |

| Total Current Assets | |

| 15,731,829 | | |

| 17,188,003 | |

| | |

| | | |

| | |

| Tractors and transport equipment | |

| 11,031,433 | | |

| 11,091,411 | |

| Trailers | |

| 13,891,981 | | |

| 13,669,558 | |

| Leasehold improvements | |

| 1,225,496 | | |

| 1,171,775 | |

| Machinery and equipment | |

| 802,730 | | |

| 1,338,490 | |

| | |

| 26,951,640 | | |

| 27,271,234 | |

| Less - Accumulated depreciation | |

| (18,014,460 | ) | |

| (17,031,108 | ) |

| | |

| 8,937,180 | | |

| 10,240,126 | |

| | |

| | | |

| | |

| Intangible assets, net | |

| 68,041 | | |

| 79,096 | |

| Accounts receivable - related parties | |

| 7,076,672 | | |

| 6,956,072 | |

| Notes receivable | |

| 7,820 | | |

| 14,317 | |

| Operating right-of-use assets | |

| 1,890,030 | | |

| 2,211,742 | |

| | |

| | | |

| | |

| | |

| 33,711,572 | | |

$ | 36,689,357 | |

| | |

| | | |

| | |

| LIABILITIES AND MEMBERS' EQUITY |

| | |

| | | |

| | |

| CURRENT LIABILITIES | |

| | | |

| | |

| Accounts payable | |

| 2,544,190 | | |

$ | 2,554,060 | |

| Other liabilities | |

| 1,314,231 | | |

| 1,657,217 | |

| Current portion of operating lease liability | |

| 643,423 | | |

| 643,424 | |

| Current portion of long-term debt | |

| 2,646,406 | | |

| 2,783,226 | |

| | |

| | | |

| | |

| Total Current Liabilities | |

| 7,148,250 | | |

| 7,637,927 | |

| | |

| | | |

| | |

| OPERATING LEASE LIABILITY | |

| 1,246,607 | | |

| 1,568,319 | |

| | |

| | | |

| | |

| LONG-TERM DEBT | |

| 2,163,342 | | |

| 2,517,904 | |

| | |

| | | |

| | |

| MEMBERS' EQUITY | |

| 23,153,373 | | |

| 24,965,207 | |

| | |

| | | |

| | |

| | |

| 33,711,571 | | |

$ | 36,689,357 | |

| | |

| | | |

| | |

| The accompanying notes and independent accountant's review report | |

| | | |

| | |

| should be read with these combined financial statements | |

| | | |

| | |

| BARNHART TRANSPORTATION, LLC AND AFFILIATES |

| |

| COMBINED STATEMENTS OF INCOME AND MEMBERS’ EQUITY |

| FOR THE SIX-MONTH PERIODS ENDED JUNE 30, 2023 AND 2022 |

| | |

| | |

| |

| | |

| | |

| |

| | |

2023 | | |

2022 | |

| | |

| | |

| |

| REVENUE | |

$ | 31,757,180 | | |

$ | 42,024,144 | |

| | |

| | | |

| | |

| COST OF REVENUE | |

| 27,789,479 | | |

| 35,110,834 | |

| | |

| | | |

| | |

| Gross Profit | |

| 3,967,701 | | |

| 6,913,310 | |

| | |

| | | |

| | |

| OPERATING EXPENSES | |

| 4,246,596 | | |

| 3,952,713 | |

| | |

| | | |

| | |

| (Loss) Income From Operations | |

| (278,895 | ) | |

| 2,960,597 | |

| | |

| | | |

| | |

| OTHER INCOME (EXPENSE) | |

| | | |

| | |

| Interest expense | |

| (112,950 | ) | |

| (61,682 | ) |

| Gain on sale of equipment | |

| 179,365 | | |

| 307,725 | |

| Other | |

| 1,624,026 | | |

| (24,488 | ) |

| Interest income | |

| 131,100 | | |

| 12,034 | |

| | |

| 1,821,541 | | |

| 233,589 | |

| | |

| | | |

| | |

| Net Income | |

| 1,542,646 | | |

| 3,194,186 | |

| | |

| | | |

| | |

| MEMBERS' EQUITY | |

| | | |

| | |

| Beginning of period | |

| 24,965,207 | | |

| 21,490,593 | |

| | |

| | | |

| | |

| Members' distributions | |

| (3,354,479 | ) | |

| (11,250 | ) |

| | |

| | | |

| | |

| End of period | |

$ | 23,153,373 | | |

$ | 24,673,530 | |

| | |

| | | |

| | |

| | |

| | | |

| | |

| The accompanying notes and independent accountant's review report | |

| | | |

| | |

| should be read with these combined financial statements | |

| | | |

| | |

| BARNHART TRANSPORTATION, LLC AND AFFILIATES |

| | |

| | |

| |

| COMBINED STATEMENTS OF CASH FLOWS |

| FOR THE SIX-MONTH PERIODS ENDED JUNE 30, 2023 AND 2022 |

| | |

| | |

| |

| | |

| | |

| |

| | |

2023 | | |

2022 | |

| | |

| | |

| |

| CASH FLOWS FROM OPERATING ACTIVITIES | |

| | |

| |

| Net income | |

$ | 1,542,645 | | |

$ | 3,194,186 | |

| Adjustments to reconcile net income to net cash provided by | |

| | | |

| | |

| operating activities: | |

| | | |

| | |

| Depreciation and amortization | |

| 2,171,403 | | |

| 2,119,046 | |

| Noncash lease expense | |

| 321,710 | | |

| 308,817 | |

| Gain on sale of property and equipment | |

| (179,365 | ) | |

| (307,725 | ) |

| Net realized and unrealized (gains) losses on investments | |

| (66,084 | ) | |

| 77,634 | |

| Change in allowance for doubtful accounts | |

| 9,979 | | |

| 18,527 | |

| Changes in assets and liabilities: | |

| | | |

| | |

| Accounts receivable | |

| 2,120,280 | | |

| (571,170 | ) |

| Other receivables | |

| (20,737 | ) | |

| (20,737 | ) |

| Inventories | |

| 17,672 | | |

| (157,012 | ) |

| Prepaids and other | |

| (587,443 | ) | |

| (622,934 | ) |

| Accounts payable | |

| (9,869 | ) | |

| 1,300,712 | |

| Operating lease liability | |

| (321,712 | ) | |

| (308,817 | ) |

| Other liabilities | |

| (342,986 | ) | |

| 407,728 | |

| Net Cash Provided By Operating Activities | |

| 4,655,493 | | |

| 5,438,255 | |

| | |

| | | |

| | |

| CASH FLOWS FROM INVESTING ACTIVITIES | |

| | | |

| | |

| Purchases of property and equipment | |

| (107,764 | ) | |

| (475,882 | ) |

| Proceeds from sale of property and equipment | |

| 610,489 | | |

| 573,070 | |

| Purchases of intangible assets | |

| - | | |

| 9,270 | |

| Payments on notes receivable | |

| 39,014 | | |

| 40,618 | |

| Additions to notes receivable | |

| (12,525 | ) | |

| (24,700 | ) |

| Purchase of investments | |

| - | | |

| (1,000,000 | ) |

| Proceeds from the sale of investments | |

| 363,000 | | |

| - | |

| Loans and advances to related parties, net | |

| (120,599 | ) | |

| (267,541 | ) |

| Net Cash Provided By (Used In) Investing Activities | |

| 771,615 | | |

| (1,145,165 | ) |

| | |

| | | |

| | |

| CASH FLOWS FROM FINANCING ACTIVITIES | |

| | | |

| | |

| Payments on long-term debt | |

| (1,672,147 | ) | |

| (1,688,333 | ) |

| Member distributions | |

| (3,354,477 | ) | |

| (11,252 | ) |

| Net Cash Used In Financing Activities | |

| (5,026,624 | ) | |

| (1,699,585 | ) |

| | |

| | | |

| | |

| Net Increase in Cash and Cash Equivalents | |

| 400,484 | | |

| 2,593,505 | |

| | |

| | | |

| | |

| CASH AND CASH EQUIVALENTS | |

| | | |

| | |

| Beginning of period | |

| 5,198,951 | | |

| 1,569,109 | |

| | |

| | | |

| | |

| End of period | |

$ | 5,599,435 | | |

$ | 4,162,614 | |

| | |

| | |

| |

| | |

2023 | | |

2022 | |

| | |

| | |

| |

| SUPPLEMENTAL DISCLOSURES OF CASH FLOW INFORMATION | |

| | |

| |

| Cash paid during the period for interest | |

$ | 112,950 | | |

$ | 61,682 | |

| | |

| | | |

| | |

| SUPPLEMENTAL SCHEDULE OF NONCASH INVESTING AND FINANCING ACTIVITIES | |

| | | |

| | |

| Capital expenditures funded by issuance of long-term debt | |

$ | 1,180,764 | | |

$ | 2,145,242 | |

| | |

| | | |

| | |

| | |

| | | |

| | |

| The accompanying notes and independent accountant's review report | |

| | | |

| | |

| should be read with these combined financial statements | |

| | | |

| | |

BARNHART TRANSPORTATION, LLC AND AFFILIATES

NOTES TO COMBINED FINANCIAL STATEMENTS

AS OF JUNE 30, 2023 AND DECEMBER 31, 2022 AND

FOR THE SIX-MONTH PERIODS ENDED JUNE 30, 2023 AND 2022

NOTE 1 - ORGANIZATION

Barnhart Transportation,

LLC and Affiliates (collectively, the Company) is a transportation solution provider offering a diversified range of services to clients

and their specific transportation needs. The Company specializes in pneumatic dry bulk sand and cement, flatbed, step-deck, double-drop,

RGN, over-dimensioned, heavy haul, dry van, nonhazardous liquids, intermodal drayage, and LTL shipments within the United States, Canada

and Mexico. The Company also has a fleet maintenance division that handles most of the maintenance required on its equipment along with

a freight brokerage division that works with partner carriers to provide innovative freight solutions. Additionally, the Company has integrated

international freight forwarding, commercial tank cleaning, warehousing and transloading services that allow for comprehensive transportation

solutions, that cater to diverse customer needs.

NOTE 2 - SUMMARY OF SIGNIFICANT ACCOUNTING

POLICIES

A summary of

significant accounting policies consistently applied by management in the preparation of the accompanying combined financial statements

are as follows:

Basis of Combination

- The accompanying combined financial statements include the financial position, results of operations and cash flows of Barnhart Transportation,

LLC; Lake Shore Logistics, LLC; Legend Equipment Leasing, LLC; Barnhart Fleet Maintenance, LLC; Lake Shore Global Solutions, LLC; and

Route 20 Tank Wash, LLC, all of which are under common control and ownership. All intercompany balances and transactions have been eliminated

in combination.

Use of Estimates

- The preparation of combined financial statements in conformity with accounting principles generally accepted in the United States of

America (U.S. GAAP) requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and

disclosure of contingent assets and liabilities at the date of the combined financial statements and the reported amounts of revenues

and expenses during the reporting period. Actual results could differ from those estimates.

Cash and Cash

Equivalents - Cash and cash equivalents include all cash balances and highly liquid investments with an initial maturity of three months

or less. The Company places its cash with high-credit quality financial institutions. At times, such investments may be in excess of the

Federal Deposit Insurance Corporation insurance limit.

Investments -

Valued at the daily closing price as reported by the fund, investments in marketable securities with readily determinable fair values

are stated at fair value based on quoted prices in active markets. The Company discloses the category of assets and liabilities measured

at fair value into one of three different levels, depending on the assumptions (i.e., inputs) used in the valuation. Level 1 provides

the most reliable measure of fair value, whereas Level 3 generally requires significant management judgment. Financial assets and liabilities

are classified in their entirety based on the lowest level of input significant to the fair value measurement, and generally approximate

fair value either due to their short-term nature or terms the Company could obtain in the current market. The Company does not have any

Level 3 financial assets or liabilities as of June 30, 2023 and December 31, 2022.

BARNHART TRANSPORTATION, LLC AND AFFILIATES

NOTES TO COMBINED FINANCIAL STATEMENTS

AS OF JUNE 30, 2023 AND DECEMBER 31, 2022 AND

FOR THE SIX-MONTH PERIODS ENDED JUNE 30, 2023 AND 2022

NOTE 2 - SUMMARY OF SIGNIFICANT ACCOUNTING

POLICIES (Continued)

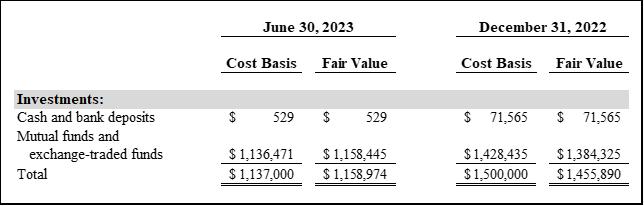

The following

table presents the cost basis and fair value of the Company’s major categories of investments:

The following

table depicts the level in the fair value hierarchy of the input used to estimate fair value of investments measured on a recurring basis

as of June 30, 2023 and December 31, 2022:

The following table

presents the detail of income (loss) from investments for the periods ended June 30, 2023 and 2022:

BARNHART TRANSPORTATION, LLC AND AFFILIATES

NOTES TO COMBINED FINANCIAL STATEMENTS

AS OF JUNE 30, 2023 AND DECEMBER 31, 2022 AND

FOR THE SIX-MONTH PERIODS ENDED JUNE 30, 2023 AND 2022

NOTE 2 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

(Continued)

Realized and unrealized

gains and losses, interest and dividends are recognized in other income in the combined statements of income and members’ equity.

Accounts Receivable

- Accounts receivable are reported at the amount management expects to collect from outstanding balances. The Company performs ongoing

credit evaluations of its customers and generally does not require collateral. Provisions are made for estimated uncollectible trade accounts

receivable. The Company’s estimate of the allowance is based on historical collection experience, a review of the current status

of trade receivables and judgment. Decisions to charge off receivables are based on management’s judgment after consideration of

facts and circumstances surrounding potential uncollectible accounts. The allowance for doubtful accounts as of June 30, 2023 and December

31, 2022 is approximately $67,000 and $57,000, respectively.

Leases - As of

January 1, 2022, leases are recognized under Accounting Standards Update (ASU) No. 2016-02 Leases (Topic 842) (ASU 2016-02). The Company

evaluates leases based on the underlying asset groups. The assets currently underlying the Company’s leases include real estate

(primarily buildings, office space, land and drop yards). Management’s significant assumptions and judgements include the determination

of the discount rate (discussed below), as well as the determination of whether a contract contains a lease. A contract contains a lease

if there is an identified asset and the Company has the right to control the asset.

Operating lease

right-of-use assets represent the Company’s right to use an underlying asset for the lease term, and the lease liabilities represent

the Company’s obligation to make lease payments arising from the lease. In the accompanying statements of income and members’

equity, rent expense for operating lease payments is recognized on a straight-line basis of the lease term. The Company’s operating

real estate leases all have lease terms of five years and they do not include auto-renewal provisions.

Topic 842 allows

lessees an option to not recognize right-of-use assets and lease liabilities arising from short-term leases. The Company does not have

any leases twelve months or less.

Operating lease right-of-use

assets and lease liabilities are recognized at the commencement date based on the present value of the lease payments over the lease term.

The Company’s lease liabilities are recognized based on the present value of the remaining fixed lease payments, over the lease

term, using a discount rate. The discounted rates for leases were determined based on U.S. Daily Treasury Par Yield Curve rates as of

January 1, 2022, which was the adoption date of Topic 842.

See Note 9 for

additional disclosures regarding the Company’s operating leases.

Concentration

- Revenue recognized from the Company’s largest customer for the periods ended June 30, 2023 and 2022 approximated 29% and 24%,

respectively, of total revenue. The balance due from the Company’s largest customer as of June 30, 2023 and December 31, 2022 approximated

27% and 28%, respectively, of accounts receivable.

Inventories

- Inventories, consisting mainly of tires and transportation-related supplies, are stated at the lower of cost or net realizable value

determined by the first-in, first-out method. Appropriate consideration is given to obsolescence, excessive levels, deterioration and

other factors in evaluating net realizable value.

BARNHART TRANSPORTATION, LLC AND AFFILIATES

NOTES TO COMBINED FINANCIAL STATEMENTS

AS OF JUNE 30, 2023 AND DECEMBER 31, 2022 AND

FOR THE SIX-MONTH PERIODS ENDED JUNE 30, 2023 AND 2022

NOTE 2 - SUMMARY OF SIGNIFICANT

ACCOUNTING POLICIES (Continued)

Fixed Assets

- Fixed assets are recorded at the lower of cost or market. Repairs and maintenance that do not extend the lives of the applicable assets

are charged to expense as incurred. Depreciation is provided over the estimated useful lives of the related assets using the straight-line

method. The estimated useful lives of the related assets are as follows:

| |

Buildings and improvements |

15 - 40 years |

|

| |

Transportation equipment |

3 - 10 years |

|

| |

Furniture and fixtures |

3 - 7 years |

|

Depreciation expense

for the periods ended June 30, 2023 and 2022 amounted to approximately $2,149,000 and $2,120,000, respectively.

The Company reviews

the carrying value of fixed assets for impairment whenever events and circumstances indicate that the carrying value of an asset might

not be recoverable from the estimated future cash flows expected to result from its use a eventual disposition. In cases where undiscounted

expected future cash flows are less than

the carrying value, an impairment

loss is recognized equal to an amount by which the carrying value exceeds the fair value of assets. The factors considered by management

in performing this assessment include current operating results, trends, and prospects, as well as the effects of obsolescence, demand,

competition and other economic factors. Based on management’s evaluation, there was no impairment at June 30, 2023 and December

31, 2022.

Intangible assets

subject to amortization consist of software and computer licenses. The Company is amortizing the intangible assets on a straight-line

basis over various periods based on the asset’s future economic benefit. Amortization related to intangible assets for the periods

ended June 30, 2023 and 2022 amounted to approximately $11,000 and $9,000, respectively.

Revenue Recognition

- Revenues are recognized over time as control of the promised services is transferred to the Company’s customers in an amount that

reflects the consideration the Company expects to be entitled to in exchange for those services.

The Company generates

revenues from billings for transportation services under contracts with customers, generally on a rate per mile or fixed rate per shipment,

based on origin and destination of the shipment. The Company’s performance obligation arises when it receives a shipment order to

transport a customer’s freight and is satisfied upon delivery of the shipment. The transaction price may be defined in a transportation

services agreement or negotiated with the customer prior to accepting the shipment order. A customer may submit several shipment orders

for transportation services at various times throughout a service agreement term, but each shipment represents a distinct service that

is a separately identified performance obligation. The Company often provides additional or ancillary services as part of the shipment

(such as loading/unloading and stops in transit), which are not distinct or are not material in the context of the contract; therefore,

the revenues for these services are recognized with the freight transaction price. The average transit time to complete a shipment is

approximately two days. Invoices for transportation services are typically generated soon after shipment delivery and, although payment

terms and conditions vary by customer, are generally due within 30 days after the invoice date.

The Company also

generates revenues from equipment leases, to include terminal rental adjustment clause (TRAC) leases. Equipment leases are recognized