UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM

8-K

CURRENT

REPORT

PURSUANT

TO SECTION 13 OR 15(d)

OF

THE SECURITIES EXCHANGE ACT OF 1934

Date

of Report (Date of earliest event reported): August 29, 2023

MAGELLAN

MIDSTREAM PARTNERS, L.P.

(Exact

Name of Registrant as Specified in Charter)

| Delaware |

|

1-16335 |

|

73-1599053 |

(State

or Other Jurisdiction

of

Incorporation) |

|

(Commission

File Number) |

|

(IRS

Employer

Identification

No.) |

One

Williams Center

Tulsa,

Oklahoma 74172

(Address

of Principal Executive Offices) (Zip Code)

Registrant’s

telephone number, including area code (918) 574-7000

(Former

Name or Former Address, if Changed Since Last Report)

Check

the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under

any of the following provisions:

| ☐ |

Written communications

pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| ☒ |

Soliciting

material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| ☐ |

Pre-commencement

communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| ☐ |

Pre-commencement

communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Indicate

by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405

of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging

growth company ☐

If

an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Securities

registered pursuant to Section 12(b) of the Act:

| Title

of Each Class |

|

Trading

Symbol(s) |

|

Name

of Each Exchange on Which Registered |

| Common

Units |

|

MMP |

|

New

York Stock Exchange |

Item

8.01 Other Events.

As

previously announced, on May 14, 2023, Magellan Midstream Partners, L.P. (NYSE: MMP), a Delaware limited partnership (“Magellan”),

entered into an Agreement and Plan of Merger (the “Merger Agreement”) with ONEOK, Inc., an Oklahoma corporation (NYSE:

ONEOK) (“ONEOK”), and Otter Merger Sub, LLC, a Delaware limited liability company and a newly formed, wholly owned

subsidiary of ONEOK (“Merger Sub”), pursuant to which, upon the terms and subject to the conditions of the Merger

Agreement, Merger Sub will merge with and into Magellan (the “Merger”), with Magellan continuing as the surviving

entity and a wholly owned subsidiary of ONEOK.

On

August 29, 2023, Magellan issued a press release announcing the filing of an investor presentation related to the Merger. A copy of the

press release is attached hereto as Exhibit 99.1 and is incorporated herein by reference.

Cautionary

Statement Regarding Forward-Looking Statements

This

report contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended,

and Section 21E of the Securities Exchange Act of 1934, as amended. All statements, other than statements of historical fact, included

in this report that address activities, events or developments that ONEOK or Magellan expects, believes or anticipates will or may occur

in the future are forward-looking statements. Words such as “estimate,” “project,” “predict,” “believe,”

“expect,” “anticipate,” “potential,” “create,” “intend,” “could,”

“would,” “may,” “plan,” “will,” “guidance,” “look,” “goal,”

“future,” “build,” “focus,” “continue,” “strive,” “allow” or

the negative of such terms or other variations thereof and words and terms of similar substance used in connection with any discussion

of future plans, actions, or events identify forward-looking statements. However, the absence of these words does not mean that the statements

are not forward-looking. These forward-looking statements include, but are not limited to, statements regarding the Merger, the expected

closing of the Merger and the timing thereof and as adjusted descriptions of the post-transaction company and its operations, strategies

and plans, integration, debt levels and leverage ratio, capital expenditures, cash flows and anticipated uses thereof, synergies, opportunities

and anticipated future performance, including maintaining current ONEOK management, enhancements to investment-grade credit profile,

an expected accretion to earnings and free cash flow, dividend payments and potential share repurchases, increase in value of tax attributes

and expected impact on EBITDA. Information adjusted for the Merger should not be considered a forecast of future results. There are a

number of risks and uncertainties that could cause actual results to differ materially from the forward-looking statements included in

this report. These include the risk that ONEOK’s and Magellan’s businesses will not be integrated successfully; the risk

that cost savings, synergies and growth from the Merger may not be fully realized or may take longer to realize than expected; the risk

that the credit ratings of the combined company or its subsidiaries may be different from what the companies expect; the possibility

that shareholders of ONEOK may not approve the issuance of new shares of ONEOK common stock in the Merger or that unitholders of Magellan

may not approve the Merger; the risk that a condition to closing of the Merger may not be satisfied, that either party may terminate

the Merger Agreement or that the closing of the Merger might be delayed or not occur at all; potential adverse reactions or changes to

business or employee relationships, including those resulting from the announcement or completion of the Merger; the occurrence of any

other event, change or other circumstances that could give rise to the termination of the Merger Agreement relating to the Merger; the

risk that changes in ONEOK’s capital structure and governance could have adverse effects on the market value of its securities;

the ability of ONEOK and Magellan to retain customers and retain and hire key personnel and maintain relationships with their suppliers

and customers and on ONEOK’s and Magellan’s operating results and business generally; the risk the Merger could distract

management from ongoing business operations or cause ONEOK and/or Magellan to incur substantial costs; the risk of any litigation relating

to the Merger; the risk that ONEOK may be unable to reduce expenses or access financing or liquidity; the impact of a pandemic, any related

economic downturn and any related substantial decline in commodity prices; the risk of changes in governmental regulations or enforcement

practices, especially with respect to environmental, health and safety matters; and other important factors that could cause actual results

to differ materially from those projected. All such factors are difficult to predict and are beyond ONEOK’s or Magellan’s

control, including those detailed in the joint proxy statement/prospectus (as defined below). All forward-looking statements are based

on assumptions that ONEOK and Magellan believe to be reasonable but that may not prove to be accurate. Any forward-looking statement

speaks only as of the date on which such statement is made, and neither ONEOK nor Magellan undertakes any obligation to correct or update

any forward-looking statement, whether as a result of new information, future events or otherwise, except as required by applicable law.

Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof.

Important

Additional Information and Where to Find It

In

connection with the Merger, on July 25, 2023, ONEOK and Magellan each filed with the Securities and Exchange Commission (the “SEC”)

a definitive joint proxy statement/prospectus (the “joint proxy statement/prospectus”), and each party has and will file

other documents regarding the Merger with the SEC. Each of ONEOK and Magellan commenced mailing copies of the joint proxy statement/prospectus

to shareholders of ONEOK and unitholders of Magellan, respectively, on or about July 25, 2023. This report is not a substitute for the

joint proxy statement/prospectus or for any other document that ONEOK or Magellan has filed or may file in the future with the SEC in

connection with the Merger. INVESTORS AND SECURITY HOLDERS OF ONEOK AND MAGELLAN ARE URGED TO CAREFULLY AND THOROUGHLY READ THE JOINT

PROXY STATEMENT/PROSPECTUS, INCLUDING ALL AMENDMENTS AND SUPPLEMENTS THERETO, AND OTHER RELEVANT DOCUMENTS FILED OR THAT WILL BE FILED

BY ONEOK AND MAGELLAN WITH THE SEC BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT ONEOK AND MAGELLAN, THE MERGER, THE RISKS RELATED

THERETO AND RELATED MATTERS.

Investors

can obtain free copies of the joint proxy statement/prospectus and other relevant documents filed by ONEOK and Magellan with the SEC

through the website maintained by the SEC at www.sec.gov. Copies of documents filed with the SEC by ONEOK, including the joint proxy

statement/prospectus, are available free of charge from ONEOK’s website at www.oneok.com under the “Investors” tab.

Copies of documents filed with the SEC by Magellan, including the joint proxy statement/prospectus, are available free of charge from

Magellan’s website at www.magellanlp.com under the “Investors” tab.

Item

9.01. Financial Statements and Exhibits.

SIGNATURES

Pursuant

to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by

the undersigned hereunto duly authorized.

| |

Magellan

Midstream Partners, L.P. |

| |

|

|

| |

By: |

Magellan

GP, LLC, |

| |

|

its

general partner |

| |

|

|

| Date:

August 29, 2023 |

By: |

/s/

Jeff L. Holman |

| |

Name: |

Jeff

L. Holman |

| |

Title: |

Executive

Vice President,

Chief Financial Officer and Treasurer |

3

Exhibit

99.1

NYSE:

MMP

| Date: |

Aug. 29, 2023 |

|

| |

|

|

| Contact: |

Investors: |

Media: |

| |

|

|

| |

Paula Farrell |

Bruce Heine |

| |

(918) 574-7650 |

(918) 574-7010 |

| |

paula.farrell@magellanlp.com |

bruce.heine@magellanlp.com |

Magellan

Midstream Files Investor Presentation Highlighting Benefits of Pending ONEOK Transaction

Transaction

delivers full value to Magellan unitholders and provides unitholders with ownership in a stronger combined company

Combined

company better positioned to address secular risks and achieve strong growth and value creation over the long term

Board

carefully considered alternative opportunities, structures and tax implications

Magellan

urges unitholders to vote “FOR” the pending merger today

TULSA,

Okla. – Magellan Midstream Partners, L.P. (NYSE: MMP) (“Magellan”) today announced the filing of an investor presentation

with the U.S. Securities and Exchange Commission in connection with our pending merger with ONEOK, Inc. (NYSE: OKE) (“ONEOK”).

The investor presentation is also available at MaximizingValueforMMPunitholders.com.

“We

are confident the pending merger with ONEOK is the best path forward for Magellan and is in the best interests of Magellan unitholders,”

said Aaron Milford, chief executive officer. “The merger provides significant premium value to Magellan unitholders, with a meaningful

upfront cash consideration as well as substantial ownership in a stronger combined company that has greater growth opportunities, scale,

diversification and resilience. We urge all Magellan unitholders to vote ‘FOR’ the pending merger today to receive full value

for their units.”

Highlights

of the presentation include:

| ● | Magellan

believes the transaction delivers full value to Magellan unitholders |

| | |

| ○ | Transaction

multiple and premium exceed precedent industry transactions, representing the highest enterprise

value to adjusted EBITDA (“EV / EBITDA”) multiple of comparable midstream energy

transactions since 2016, an EV / EBITDA multiple that is 2.5x higher than Magellan’s

publicly traded peers1, and, at 22%, the

highest premium of comparable midstream transactions since the pandemic induced a sector

re-rating |

| ○ | Implied

value of merger consideration exceeds Magellan’s trading value at any point in approximately

5 years |

| ○ | Board

negotiated 4 price increases, fiduciary out, lower termination fee, ability to pay pre-closing

special distributions and significant cash component – and carefully evaluated ONEOK

assets, strategy and track record before determining transaction maximized value |

| ○ | As

shown below, the proposed transaction premium adds to Magellan’s already premium EV

/ EBITDA trading multiple. If the transaction fails to close, Magellan’s unit price

could decline to a multiple in line with our peers, which would result in a 28% decline to

the implied transaction value |

Exhibit

1: Transaction premium adds to an already premium trading multiple12345

Exhibit

2: Potential risk of multiple re-rating if transaction does not close1

| 1 | Analysis

based on market data and street consensus estimates as of May 12, 2023 (last trading day

prior to transaction announcement). Peer group includes ENB, TRP, WMB, EPD, KMI and ET |

| 2 | Represents

EV / 2023E EBITDA multiple implied by transaction |

| 3 | Reflects

average EV / EBITDA multiple of ENB, TRP, WMB, EPD, KMI and ET |

| 4 | Weighted

average after-tax value |

| 5 | Analysis

based on market data and street consensus estimates as of May 12, 2023 (last trading day prior to

transaction announcement) |

| ● | Magellan

could face long-term secular risks as a standalone company; Magellan believes that the valuation

offered in the merger captures fair value for unitholders and that the transaction mitigates

these risks, creating a diversified, scaled and resilient combined company that is well-positioned

for the long term |

| | |

| ○ | Many respected

third parties forecast demand for U.S. refined products to decline more than 40% from 2022

to 2050; if correct, these forecasts represent lower demand than we currently expect and

than is represented in the value received in the merger |

| ○ | Crude

oil production to remain below existing pipeline capacity, placing downward pressure on utilization

and re-contracted rates |

| ○ | There

are more limited attractive growth opportunities in crude oil and refined products segments |

| ○ | Significant

sector consolidation leaves fewer viable M&A and other strategic opportunities |

| ○ | Implementing

inorganic growth opportunities would likely result in paying (rather than receiving) transaction

premiums and issuing equity that we believe has been consistently undervalued absent this

merger |

| ○ | With enhanced

scale and diversification, the combined company will have greater growth opportunities and

be better positioned across industry cycles |

| ■ | Combined

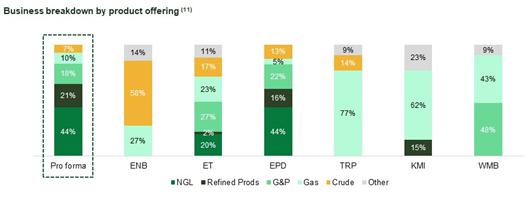

company to have resilient product mix, mirroring that of larger-scale peers |

| ■ | Potential

uplift of approximately $6.1 billion (approximately $7 per Magellan unit pro-rata6)

from capitalized risked synergies and significant tax deferral |

| ■ | Global

demand for natural gas and NGL-related products is expected to increase more than 20% through

20407 |

| ■ | Adds

more than $1.5 billion of diversified annual EBITDA, more than 85% of which is fee-based,

reducing commodity exposure and cash flow volatility |

| ■ | Increases

EBITDA CAGR by approximately 170% through 2025, with pro forma growth expected to outpace

midstream peers8 |

| ■ | 4.0x

step-up in free cash flow after distributions to approximately $1 billion average annually

(2024 to 2027), enabling increased spending on value-creating organic growth projects |

| ■ | Strong

pro forma balance sheet creates financial flexibility to increase capital deployment at attractive

returns, while also returning capital to shareholders through substantial dividends and share

repurchases |

| ■ | Increased

scale provides more trading liquidity, a broader investor base and inclusion in the S&P

500 index |

| 6 | Total

potential uplift of approximately $6.1 billion (calculated as $415 million annual pre-tax

synergies (the upper end of estimated risked synergies) capitalized at 11x plus $1.5 billion

present value of tax deferrals) multiplied by Magellan’s approximately 23% pro forma

ownership in the combined company divided by Magellan’s fully diluted units outstanding

at time of transaction announcement |

| 7 | Source:

EIA and Wood Mackenzie |

| 8 | EBITDA

CAGR for MMP and OKE based on financial projections as disclosed in the definitive joint

proxy statement / prospectus filed with the SEC on July 25, 2023 (the “joint proxy

statement / prospectus”), including $415 million of run-rate synergies (high case for

risk-weighted synergies); peer EBITDA forecast reflects street consensus estimates as of

May 12, 2023 (last trading day prior to transaction announcement) |

Exhibit

3: Combined company has stronger growth outlook than standalone MMP910

Exhibit

4: MMP unitholders will gain exposure to a resilient asset profile, with higher growth than standalone MMP11

Exhibit

5: Risk-weighted synergy opportunities12

| 9 | EBITDA

CAGR for MMP and OKE based on financial projections as disclosed in the joint proxy statement

/ prospectus; peer EBITDA forecast reflects street consensus estimates as of May 12, 2023

(last trading day prior to transaction announcement) |

| 10 | Based

on pro forma financial projections as disclosed in the joint proxy statement / prospectus,

including $415 million of synergies (the upper end of estimated risked synergies) in 2025E |

| 11 | Reflects

the pro forma entity’s 2022A operating income plus equity earnings; reflects 2022E

EBITDA breakdown for peers |

| 12 | Source:

ONEOK Second Quarter 2023 Earnings Presentation |

| ● | Magellan

board carefully reviewed alternative opportunities, structures and tax implications |

| ○ | Transaction

offers greater net proceeds than an open-market sale prior to announcement would have and

greater certainty than holding out for a higher open-market price in the future |

| ○ | Merger

is likely superior to a future Magellan sale when considered in present value terms: future

after-tax proceeds are not likely to be as high and a comparable market premium may not be

available |

| ○ | Transaction

is also superior to converting Magellan to a C-Corp. as a standalone strategy due to the

merger’s known premium and inclusion in S&P 500, versus the uncertain results of

a C-corp. conversion |

| ○ | One investor

has publicly opposed the transaction, but its analysis is flawed: |

| ■ | Misconstrues

the true current tax situation by assuming all longer-tenured unitholders never sell |

| ■ | Ignores

prospective market value and related upside of stronger combined company |

| ■ | Focuses

mainly on a near-term dividend model with no terminal value and ignores the high present

value of the after-tax cash consideration offered |

| ■ | Determines

after-tax value for Magellan standalone of just $29.50 per unit, based on its long-term dividend discount

model– less than 55% of the after-tax merger consideration |

| ○ | The same

investor has misrepresented the tax implications of the transaction: |

| ■ | The

merger does not create any new tax liability (beyond that associated with the premium) –

the return on MLP units is tax-deferred, not tax-free |

| ■ | This

analysis generally ignores the existing tax liability of Magellan unitholders or alternatively

references the amount today as relevant in the future when in fact this liability will continue

to grow (estimated to more than double to approximately $20 per unit on average by 2027) |

| ■ | The

transaction premium, like any premium, increases a unitholder’s overall tax liability

to reflect a higher gain than the unitholder would have incurred absent the transaction,

but also delivers a greater after-tax return than an open-market sale |

| ■ | Comparing

after-tax merger proceeds with pre-tax trading prices is misleading – any monetization

triggers a taxable event and more than 60% of Magellan unitholders typically sell within

five years |

| ■ | Comparing

the higher after-tax proceeds of the merger to the lower after-tax proceeds of an open-market

sale prior to the merger being announced is a more meaningful analysis than comparing premium

received to taxes owed |

The

special meeting of unitholders will be held virtually on Sept. 21, 2023 at 10:00 a.m. Central Time. Magellan unitholders of record at

the close of business on July 24, 2023 are entitled to vote at, or submit proxies in advance of, the special meeting. The Magellan board

of directors unanimously recommends that Magellan unitholders vote “FOR” the proposals related to Magellan's merger with

ONEOK.

| Magellan

unitholders who need assistance in completing the proxy card, need additional copies of the

proxy materials or have questions regarding the upcoming special meeting should contact Magellan’s

proxy solicitors:

|

| |

|

| Morrow

Sodali, LLC |

MacKenzie

Partners, Inc. |

| Phone: (800)

662-5200 or (203) 658-9400 |

Phone: (800) 322-2885 or (212)

929-5500 |

| Email:

MMP@info.morrowsodali.com |

Email:

proxy@mackenziepartners.com |

About

Magellan Midstream Partners, L.P.

Magellan

Midstream Partners, L.P. (NYSE: MMP) is a publicly traded partnership that primarily transports, stores and distributes refined petroleum

products and crude oil. Magellan owns the longest refined petroleum products pipeline system in the country, with access to nearly 50%

of the nation’s refining capacity, and can store more than 100 million barrels of petroleum products such as gasoline, diesel fuel

and crude oil. More information is available at www.magellanlp.com.

###

CAUTIONARY

STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This communication

contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section

21E of the Securities Exchange Act of 1934, as amended. All statements, other than statements of historical fact, included in this communication

that address activities, events or developments that ONEOK or Magellan expects, believes or anticipates will or may occur in the future

are forward-looking statements. Words such as “estimate,” “project,” “predict,” “believe,”

“expect,” “anticipate,” “potential,” “create,” “intend,” “could,”

“would,” “may,” “plan,” “will,” “guidance,” “look,” “goal,”

“future,” “build,” “focus,” “continue,” “strive,” “allow” or

the negative of such terms or other variations thereof and words and terms of similar substance used in connection with any discussion

of future plans, actions, or events identify forward-looking statements. However, the absence of these words does not mean that the statements

are not forward-looking. These forward-looking statements include, but are not limited to, statements regarding the proposed transaction

between ONEOK and Magellan (the “Proposed Transaction”), the expected closing of the Proposed Transaction and the timing

thereof and as adjusted descriptions of the post-transaction company and its operations, strategies and plans, integration, debt levels

and leverage ratio, capital expenditures, cash flows and anticipated uses thereof, synergies, opportunities and anticipated future performance,

including maintaining current ONEOK management, enhancements to investment-grade credit profile, an expected accretion to earnings and

free cash flow, dividend payments and potential share repurchases, increase in value of tax attributes and expected impact on EBITDA.

Information adjusted for the Proposed Transaction should not be considered a forecast of future results. There are a number of risks

and uncertainties that could cause actual results to differ materially from the forward-looking statements included in this communication.

These include the risk that ONEOK’s and Magellan’s businesses will not be integrated successfully; the risk that cost savings,

synergies and growth from the Proposed Transaction may not be fully realized or may take longer to realize than expected; the risk that

the credit ratings of the combined company or its subsidiaries may be different from what the companies expect; the possibility that

shareholders of ONEOK may not approve the issuance of new shares of ONEOK common stock in the Proposed Transaction or that unitholders

of Magellan may not approve the Proposed Transaction; the risk that a condition to closing of the Proposed Transaction may not be satisfied,

that either party may terminate the merger agreement or that the closing of the Proposed Transaction might be delayed or not occur at

all; potential adverse reactions or changes to business or employee relationships, including those resulting from the announcement or

completion of the Proposed Transaction; the occurrence of any other event, change or other circumstances that could give rise to the

termination of the merger agreement relating to the Proposed Transaction; the risk that changes in ONEOK’s capital structure and

governance could have adverse effects on the market value of its securities; the ability of ONEOK and Magellan to retain customers and

retain and hire key personnel and maintain relationships with their suppliers and customers and on ONEOK’s and Magellan’s

operating results and business generally; the risk the Proposed Transaction could distract management from ongoing business operations

or cause ONEOK and/or Magellan to incur substantial costs; the risk of any litigation relating to the Proposed Transaction; the risk

that ONEOK may be unable to reduce expenses or access financing or liquidity; the impact of a pandemic, any related economic downturn

and any related substantial decline in commodity prices; the risk of changes in governmental regulations or enforcement practices, especially

with respect to environmental, health and safety matters; and other important factors that could cause actual results to differ materially

from those projected. All such factors are difficult to predict and are beyond ONEOK’s or Magellan’s control, including those

detailed in the joint proxy statement/prospectus (as defined below). All forward-looking statements are based on assumptions that ONEOK

and Magellan believe to be reasonable but that may not prove to be accurate. Any forward looking statement speaks only as of the date

on which such statement is made, and neither ONEOK nor Magellan undertakes any obligation to correct or update any forward-looking statement,

whether as a result of new information, future events or otherwise, except as required by applicable law. Readers are cautioned not to

place undue reliance on these forward-looking statements, which speak only as of the date hereof.

NON-GAAP

FINANCIAL MEASURES

This communication

includes certain projections of non-GAAP financial measures. Due to the high variability and difficulty in making accurate forecasts

and projections of some of the information excluded from these projected measures, together with some of the excluded information not

being ascertainable or accessible, Magellan and ONEOK are unable to quantify certain amounts that would be required to be included in

the most directly comparable GAAP financial measures without unreasonable effort. Consequently, no disclosure of estimated comparable

GAAP measures is included, and no reconciliation of the forward-looking non-GAAP financial measures is included.

IMPORTANT

ADDITIONAL INFORMATION AND WHERE TO FIND IT

In connection

with the Proposed Transaction, on July 25, 2023, ONEOK and Magellan each filed with the Securities and Exchange Commission (the “SEC”)

a definitive joint proxy statement/prospectus (the “joint proxy statement/prospectus”), and each party has and will file

other documents regarding the Proposed Transaction with the SEC. Each of ONEOK and Magellan commenced mailing copies of the joint proxy

statement/prospectus to shareholders of ONEOK and unitholders of Magellan, respectively, on or about July 25, 2023. This communication

is not a substitute for the joint proxy statement/prospectus or for any other document that ONEOK or Magellan has filed or may file in

the future with the SEC in connection with the Proposed Transaction. INVESTORS AND SECURITY HOLDERS OF ONEOK AND MAGELLAN ARE URGED TO

CAREFULLY AND THOROUGHLY READ THE JOINT PROXY STATEMENT/PROSPECTUS, INCLUDING ALL AMENDMENTS AND SUPPLEMENTS THERETO, AND OTHER RELEVANT

DOCUMENTS FILED OR THAT WILL BE FILED BY ONEOK AND MAGELLAN WITH THE SEC BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT ONEOK

AND MAGELLAN, THE PROPOSED TRANSACTION, THE RISKS RELATED THERETO AND RELATED MATTERS.

Investors

can obtain free copies of the joint proxy statement/prospectus and other relevant documents filed by ONEOK and Magellan with the SEC

through the website maintained by the SEC at www.sec.gov. Copies of documents filed with the SEC by ONEOK, including the joint proxy

statement/prospectus, are available free of charge from ONEOK’s website at www.oneok.com under the “Investors” tab.

Copies of documents filed with the SEC by Magellan, including the joint proxy statement/prospectus, are available free of charge from

Magellan’s website at www.magellanlp.com under the “Investors” tab.

NO ADVICE

This communication

has been prepared for informational purposes only and is not intended to provide, and should not be relied on for, tax, legal or accounting

advice. Magellan unitholders should consult their own tax and other advisors before making any decisions regarding the Proposed Transaction.

7

Magellan Midstream Partn... (NYSE:MMP)

Historical Stock Chart

From Apr 2024 to May 2024

Magellan Midstream Partn... (NYSE:MMP)

Historical Stock Chart

From May 2023 to May 2024