UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 13E-3

RULE 13e-3 TRANSACTION STATEMENT

PURSUANT TO SECTION 13(e)

OF THE SECURITIES EXCHANGE ACT OF 1934

(Amendment No. 2)

Pardes

Biosciences, Inc.

(Name of the Issuer)

Pardes

Biosciences, Inc.

(Name of Person(s) Filing Statement)

Common Stock, par value $0.0001 per share

(Title of Class of Securities)

69945Q 105

(CUSIP Number

of Common Stock)

Thomas G. Wiggans

Chief Executive Officer

Pardes Biosciences, Inc.

2173 Salk Avenue, Suite 250

PMB#052

Carlsbad,

California 92008

(415) 649-8758

(Name, Address and Telephone Number of Person Authorized to Receive Notices and Communications on Behalf of the Person(s) Filing Statement)

With copies to:

|

|

|

| Douglas N. Cogen, Esq.

Ethan A. Skerry, Esq. Ran

D. Ben-Tzur, Esq. Jennifer J. Hitchcock, Esq.

Michael S. Pilo, Esq.

Fenwick & West LLP

555 California Street, 12th Floor

San Francisco, California 94104

(415) 875-2300 |

|

Elizabeth H. Lacy

General Counsel and Corporate Secretary

Pardes Biosciences, Inc.

2173 Salk Avenue, Suite 250

PMB#052 Carlsbad,

California 92008 (415) 649-8758 |

This statement is filed in connection with (check the appropriate box):

|

|

|

|

|

| a. |

|

☐ |

|

The filing of solicitation materials or an information statement subject to Regulation 14A, Regulation 14C or Rule 13e-3(c) under the Securities Exchange Act of 1934. |

|

|

|

| b. |

|

☐ |

|

The filing of a registration statement under the Securities Act of 1933. |

|

|

|

| c. |

|

☒ |

|

A tender offer. |

|

|

|

| d. |

|

☐ |

|

None of the above. |

Check the following box if the soliciting materials or information statement referred to in checking box (a) are

preliminary copies: ☐

Check the following box if the filing is a final amendment reporting the results of the

transaction: ☐

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES COMMISSION HAS APPROVED OR DISAPPROVED OF THIS

TRANSACTION, PASSED UPON THE MERITS OR FAIRNESS OF THIS TRANSACTION, OR PASSED UPON THE ADEQUACY OR ACCURACY OF THE DISCLOSURE IN THIS SCHEDULE 13E-3. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL

OFFENSE.

INTRODUCTION

This Amendment No. 2 (“Amendment No. 2”) amends and supplements

the Rule 13e-3 Transaction Statement on Schedule 13E-3 previously filed by Pardes Biosciences, Inc., a Delaware corporation

(“Pardes” or the “Company”), with the United States Securities and Exchange Commission (the “SEC”) on July 28, 2023 (as amended and restated on August 17, 2023, and as

may be further amended, restated or supplemented from time to time, the “Schedule 13E-3”). This Amendment No. 2 relates to the offer to purchase by MediPacific Sub, Inc., a

Delaware corporation (“Purchaser”), and wholly owned subsidiary of MediPacific, Inc. (“Parent”), all of the issued and outstanding shares (the “Shares”) of common stock, par

value $0.0001 per share (“Common Stock”), of Pardes that is the subject of the Rule 13e-3 transaction described below (other than (i) Shares held in the

treasury of Pardes immediately prior to the effective time of the Merger (as defined below), and (ii) Shares owned, directly or indirectly, by the Foresite Stockholders (as defined in that certain Agreement and Plan of Merger, dated as of

July 16, 2023, by and among Pardes, Purchaser and Parent (the “Merger Agreement”)), Parent, Purchaser or any other subsidiary of Parent at the commencement of the Offer and that are owned by Parent, Purchaser or any

other subsidiary of Parent immediately prior to the effective time of the Merger), for a price of (i) $2.13 per Share and (ii) one non-transferable contingent value right per Share, upon the

terms and subject to the conditions set forth in the Offer to Purchase dated July 28, 2023 (as amended and restated on August 17, 2023, further amended on August 28, 2023, and as may be further amended or supplemented from time to

time, the “Offer to Purchase”) and in the related Letter of Transmittal, dated July 28, 2023, which, together with any further amendments or supplements thereto, collectively constitute the

“Offer.” The Offer is being made pursuant to the Merger Agreement. The Merger Agreement provides, among other things, for the terms and conditions of the Offer and the subsequent merger of Purchaser with and into Pardes (the

“Merger”) in accordance with Section 251(h) of the Delaware General Corporation Law.

The information contained in the Tender

Offer Statement filed under cover of Schedule TO by Parent with the SEC on July 28, 2023 (as amended and restated on August 17, 2023, further amended on August 28, 2023, and as may be further amended or supplemented from time to time,

the “Schedule TO”), including the Offer to Purchase, and the Solicitation/Recommendation Statement on Schedule 14D-9 filed by Pardes with the SEC on July 28,

2023 (as amended and restated on August 17, 2023, further amended on August 28, 2023, and as may be further amended or supplemented from time to time, the

“Schedule 14D-9”), is incorporated herein by reference.

All information contained in this Statement concerning Purchaser, Parent or their affiliates has been provided by such person and not by any other person.

Item 16 is hereby amended and supplemented by adding the following exhibits:

|

|

|

| Exhibit No. |

|

Description |

| (a)(1)(I) |

|

Supplement No. 1 to Amended and Restated Offer to Purchase, dated August 28, 2023 (incorporated herein by reference to Exhibit (a)(1)(H) to the Schedule TO). |

|

|

| (a)(1)(J) |

|

Solicitation/Recommendation Statement (Amendment No. 2) on Schedule 14D-9 (incorporated herein by reference to the Schedule 14D-9). |

|

|

| (a)(1)(K) |

|

Press Release issued by Purchaser on August 28, 2023 (incorporated herein by reference to Exhibit (a)(1)(I) to the Schedule TO). |

|

|

| (c)(10)+ |

|

Discussion Materials, dated April 13, 2023, from Leerink Partners LLC. |

|

|

| (c)(11)+ |

|

Discussion Materials, dated May 2023, from Leerink Partners LLC. |

|

|

| (c)(12)+ |

|

Discussion Materials, dated May 24, 2023, from Leerink Partners LLC. |

|

|

| (c)(13)+ |

|

Discussion Materials, dated May 25, 2023, from Leerink Partners LLC. |

|

|

| (c)(14)+ |

|

Discussion Materials, dated June 10, 2023, from Leerink Partners LLC. |

|

|

| (c)(15)+ |

|

Discussion Materials, dated June 11, 2023, from Leerink Partners LLC. |

| + |

Certain portions of this exhibit have been redacted and separately filed with the Securities and Exchange

Commission pursuant to a request for confidential treatment. |

SIGNATURES

After due inquiry and to the best of my knowledge and belief, I certify that the information set forth in this Statement is true, complete and correct.

|

|

|

|

|

|

|

| Dated: August 28, 2023 |

|

|

|

PARDES BIOSCIENCES, INC. |

|

|

|

|

|

|

|

|

By: |

|

/s/ Thomas G. Wiggans |

|

|

|

|

|

|

Name: Thomas G. Wiggans |

|

|

|

|

|

|

Title: Chief Executive Officer and |

|

|

|

|

|

|

Chair of the Board of Directors |

$1'5(3/$&(':,7+³>;<=@´68&+,'(17,),(',1)250$7,21

+$6%((1(;&/8'(')5207+,6(;+,%,7%(&$86(,7 , ,61270$7(5,$/$1' ,, ,67+(7<3(7+$77+(5(*,675$1775($76$635,9$7(25&21),'(17,$/ Exhibit (c)(10) &(57$,1&21),'(17,$/3257,2162)7+,6(;+,%,7+$9(%((120,77(' PROJECT PACIFIC STRATEGIC

ALTERNATIVES CONSIDERATIONS APRIL 13, 2023 Confidential

PROJECT PACIFIC SITUATION OVERVIEW • Pardes Biosciences is

evaluating its strategic options following the decision to suspend the clinical development of pomotrelvir, reduce headcount by 85% and conserve its current cash balance of ~$172 million. • Pardes’ attractive cash balance and the current

weakness in the capital markets provide Pardes with a range of strategic alternatives to optimize value for shareholders. – Merge with a private company – In-license or acquire clinical assets or new technologies – Merge with a

public company – Return capital to shareholders • Private company merger counterparties could have complementary assets and operating synergies or could be in different therapeutic areas that the board believes will create a compelling

story for new and existing investors. • In-licensing or acquiring assets should be explored but can be challenging given both the competitive intensity and funding requirements to acquire and develop high-quality, clinical-stage assets through

to value inflecting milestones. • Public-to-public mergers are rare for pre-commercial biopharma companies as public company targets with attractive assets often have financing options that are more efficient and feasible than a merger with a

cash-rich fallen angel. • The return of capital option may be more efficient than in the past given the emergence of parties willing to acquire cash-rich companies for up to 80-90% of their net cash balance plus CVRs via a tender offer that

can close in ~45 days vs the traditional dissolution process that can take up to three years to complete. • The typical private merger process can take approximately two to three months to announcement and can take up to another three to four

months to close in the event the transaction does not qualify for a sign-and-close. • Our experience as a leading strategic advisor, history of screening and sourcing select targets for a number of similarly situated clients, differentiated

knowledge resources and deep relationships with potential merger partners make us an ideal advisor for the board as it navigates options and executes potential strategic transactions. Confidential 1

PROJECT PACIFIC PUBLIC / PRIVATE MERGERS CAN WORK AS A GO PUBLIC

ALTERNATIVE FOR HIGH-QUALITY COMPANIES $ IN MILLIONS; SORTED BY ANNOUNCEMENT DATE (NEWEST TO OLDEST) RECENTLY Private Company Private Company Private Company Private Company Private Company ANNOUNCED Merger with Merger with Merger with Merger with

Merger with PUBLIC / PRIVATE MERGERS: March 2023 February 2023 December 2022 November 2022 November 2022 HIGH QUALITY COMPANIES CURRENTLY TRADING ON NASDAQ VIA A PUBLIC / PRIVATE MERGER: Private Company Private Company Private Company Private

Company Private Company Private Company Merger with Merger with Merger with Merger with Merger with Merger with Celtrix Pharmaceuticals May 2000 October 2020 October 2020 January 2018 November 2016 July 2016 • $98MM follow-on (Sep. 2021)

• $184MM follow-on (Nov. 2021) • $84MM follow-on (Jan. 2018) • $52MM follow-on (May 2017) • $144MM follow-on (Dec. 2017) • $403MM follow-on (Sep. 2017) • $450MM convertible debt • $270MM follow-on (Aug.2022)

• $121MM follow-on (May 2022) • $63MM follow-on (Nov. 2018) • $75MM follow-on (Jan. 2018) • $440MM follow-on (Jun. 2018) (Jan. 2018) • $91MM follow-on (Apr. 2019) • $46MM follow-on (Jan. 2020) • $159MM

proceeds under • $287MM follow-on (May 2019) $200M ATM (Dec. 2022) • $98MM follow-on (Dec. 2019) • $160MM follow-on (Sep. 2020) • $259MM follow-on (May 2020) • $288MM follow-on / $575MM • $299MM follow-on (Dec.

2020) • Acquisition by Ipsen (closed convertible debt (May 2021) March 2023) • Renovacor Acquisition • $275MM follow-on / $500MM (Dec. 2022) term loan/royalty (Oct. 2022) • $100MM follow-on (Oct. 2022) Acquired for Mkt. Cap:

$1.5B Mkt. Cap: $1.7B Mkt. Cap: $1.4B Mkt. Cap: $5.6B Mkt. Cap: $2.3B (1) $1.0B by Ipsen (1) Does not include $10/share CVRs. Note: Data as of 04/06/23. Recently announced transactions include private company mergers that have not yet closed.

Confidential 2 Source: FactSet, Dealogic, SEC filings and press releases.

PROJECT PACIFIC SELECTION METHODOLOGY FOR A PRIVATE COMPANY MERGER

TRANSACTION Leverage SVB Securities' relationships with high-quality private biopharma companies with stated interest in alternative go-public transactions MEDACorp knowledge resource enables diligence of potential opportunities Relationships with

100+ high quality private biopharma companies help expedite screening process Focused list of attractive target companies for Pardes to pursue Confidential 3

PROJECT PACIFIC CRITERIA FOR DETERMINING ATTRACTIVENESS OF A PRIVATE

COMPANY MERGER COUNTERPARTY ILLUSTRATIVE SCREENING CRITERIA USED BY PARDES BIOSCIENCES Attractiveness of target’s lead asset, pipeline, technology, and business case 1. 2. Near-term, value-driving catalysts within pro forma cash runway

Management, board and existing investor quality 3. 4. Readiness to be a U.S. publicly traded company Need for additional financing and commitment from private company investors to provide such 5. 6. Proposed valuation and ownership split including

premium assigned to private company over expected cash at close Fit and value assigned to public company’s programs 7. ILLUSTRATIVE SCREENING CRITERIA USED BY PRIVATE COMPANY 1. Sufficient cash on balance sheet to fund activities through key

value-driving catalysts 2. Quality of public company investor base – overlap with private company is often helpful Material litigation, liabilities or sustained operational commitments 3. Personnel with complementary domain expertise

(scientific, development, or commercial) 4. Confidential 4

PROJECT PACIFIC COMPONENTS OF VALUE IN A PRIVATE COMPANY MERGER PARDES

BIOSCIENCES PRIVATE TARGET Estimated net cash at close Base value is post-money valuation of last private financing • Primary value driver • Value may be adjusted based on market conditions • Ability to maximize cash preservation

via operational • Meaningful data generation or update since last streamlining financing could justify a value adjustment • Target valuation may be more negotiable in the absence of a high-quality institutional shareholder Valuation

supported by: Listing value Clinical programs / Intrinsic valuation Market based valuation other assets • Key analysis to inform • Crossover to IPO step- • Additional value driver • Potential for right inherent value of

future up, comparable partner to ascribe value cash flows • Dependent on equity companies analysis capital market • CVRs can be employed • Sensitive to changes in • Reference point to conditions to retain value for

assumptions inform value shareholders • Less reliable for earlier- • Dependent on market stage companies conditions Relative value, informed by the above metrics, will be determined via negotiation of the exchange ratio Confidential

5

CVRS CAN BE EMPLOYED TO RETAIN VALUE FOR PROJECT PACIFIC SHAREHOLDERS

Mechanism of Special dividend to Aduro shareholders of record prior Special dividend to OncoMed shareholders of record in to merger becoming effective March 2019 CVR Issuance Terminates at earlier of: • Payment by Mereo of each milestone

eligible to be 10 years Period attained • Expiration of period for each trigger event Non-tradable Non-tradable Tradability • Celgene exercises its option to license Oncomed’s etigilimab and pays associated $35mm milestone •

Disposition or license of Aduro’s non-renal assets before 12/31/19 Trigger • Revenue resulting from ownership of subsidiary Event(s) • Mereo enters partnership or other agreement established to hold any non-renal assets regarding

navicixizumab within 18 months of the merger closing • Additional Mereo ADRs based on exchange ratio calculated by dividing the milestone received by the • Any consideration paid to Aduro with respect to the Mereo’s 10-day VWAP

following announcement disposition or license of any non-renal assets that Celgene exercised its option (subject to issuance limitation of 40% of issued share capital) • Proceeds resulting from ownership in any Payment subsidiary established

by Aduro before the six- • 70% of net proceeds of milestone payments month anniversary of the closing date to hold any received by Mereo within 5 years of merger from non-renal assets future partnership or investment transactions in relation

to navicixizumab (subject to aggregate cap of $79.7mm) Confidential 6

PROJECT PACIFIC CASE STUDY: CONCENTRA’S ACQUISITION OF JOUNCE

POST REDX MERGER ANNOUNCEMENT TIMELINE • 02/23: Jounce announced an all-stock merger with Redx Pharma (37% / 63% split, respectively) • 03/14: Concentra offered to acquire Jounce for $1.80 cash per share + a CVR • 03/27: Jounce

announced acquisition by Concentra for $1.85 cash per share + CVRs TRANSACTION DETAILS • On 04/07, Concentra will commence a tender offer to acquire all outstanding shares of Jounce for $1.85 per share + CVRs ‒ Estimated / minimum Jounce

net cash at close: $115M / $110M ‒ Upfront cash of $1.85 per share represents 61% of current net cash per share, 85% of estimated net cash at close and 89% of minimum net cash ‒ Jounce’s liquidation analysis suggested distribution

would result in proceeds of 61% of current net cash and 89% of merger minimum cash • CVRs are for proceeds from (1) a transaction for Jounce’s programs and (2) certain specified cost savings (1) 80% of proceeds from a transaction for

Jounce’s programs within two years of merger close; 10-year tail on payments (2) 100% of the potential aggregate value of certain specified potential cost savings, including: o Any reduction in the amount of the expected lease obligation o Any

increase in net working capital • Concurrent with the merger, Jounce announced an 84% RIF (compared to a 57% RIF with the Redx merger) and restructuring costs of $6.5M • Jounce’s board also recommended not moving forward with the

Redx merger, causing Redx shares to decline 11% TRADING PERFORMANCE PERFORMANCE RELATIVE TO CASH PER SHARE Share TANGCAPITALMANAGEMENT Price 03/27: Announced $3.00 acquisition by Concentra Merger (2/23) + Offer (3/14): Merger (3/27): (1) Current Net

Cash Per Share: $3.01 57% RIF $1.80 + CVR $1.85 + CVRs $2.50 T-0 +1 Day T-0 +1 Day T-0 +1 Day (2) 03/14: Announced Est. Net Cash at Close Per Share: $2.16 Concentra’s offer to acquire $2.00 Jounce Share Price $0.99 $1.10 $1.06 $1.49 $1.51

$1.83 (3) Merger Min. Net Cash Per Share: $2.07 Change 11% 41% 21% $1.50 Share Price as a % of Net Cash Share Price as % of: $1.00 (1) Latest Net Cash 33% 37% 35% 50% 50% 61% (2) Est. Net Cash at Close 46% 51% 49% 69% 70% 85% $0.50 02/23: Announced

merger 03/06: Tang Capital acquired (3) with Redx a 9.7% stake in Jounce Merger Min. Net Cash 48% 53% 51% 72% 73% 88% $0.00 1/3 1/10 1/17 1/24 1/31 2/7 2/14 2/21 2/28 3/7 3/14 3/21 (1): Net cash per share of $3.01, assuming $160M last reported net

cash and 53.1 fully diluted shares outstanding using treasury stock methodology. (2): Net cash per share of $2.16, assuming $115M net cash at close and 53.1 fully diluted shares outstanding using treasury stock methodology. Confidential 7 (3): Net

cash per share of $2.07, assuming $110M net cash at close and 53.1 fully diluted shares outstanding using treasury stock methodology.

PROJECT PACIFIC ILLUSTRATIVE POTENTIAL MERGER CANDIDATES Oncology

Autoimmune & Inflammation (1) (1) (1) Vida Ventures (1) (1) (1) Portfolio Company (2) (1): Public company. (2): Highest stage of development not disclosed. Inbound Interest Source: Company websites. Confidential 8 Preclinical Phase 1 & 1/2

Phase 2 & 3

PROJECT PACIFIC ILLUSTRATIVE POTENTIAL MERGER CANDIDATES (CONT.)

Cardiology / X (1) (2) Cardio- CNS Anti-Viral Genetic Medicines Rare Diseases Others metabolic (4) (3) (4) (4) Project Nuage (5) (1): Excludes oncology focused companies. (2): Other therapeutics areas includes endocrinology, gastrointestinal

diseases, HCS therapies, hepatology, ophthalmology, pulmonology, xenotransplantation, companies with multiple therapeutic areas as well as a healthcare information technology platform. (3): Commercial-stage. (4): Public company. (5): Highest stage

of development not disclosed. Inbound Interest Source: Company websites. Confidential 9 Preclinical Phase 1 & 1/2 Phase 2 & 3 or Later

PROJECT PACIFIC ILLUSTRATIVE PRIVATE COMPANY MERGER PROCESS TIMELINE

THROUGH ANNOUNCEMENT MONTH APRIL MAY JUNE JULY WEEK OF 10 17 24 1 8 15 22 29 5 12 19 26 3 10 17 24 Weekly reoccurring meeting to track process Private company target selection Formally initiate outreach to selected parties Send process letter and

receive initial proposals Evaluate proposals and advance parties to further diligence Due diligence Management presentations Receipt of final proposals Negotiate final terms and definitive documentation If Nasdaq agrees no shareholder approval is

required, the merger can close shortly after announcement. Confidential 10

PROJECT PACIFIC Disclosures This information (including, but not

limited to, prices, quotes and statistics) has been obtained from sources that we believe reliable, but we do not represent that it is accurate or complete and it should not be relied upon as such. All information is subject to change without

notice. The information is intended for Institutional Use Only and is not an offer to sell or a solicitation to buy any product to which this information relates. SVB Securities LLC (“Firm”), its officers, directors, employees,

proprietary accounts and affiliates may have a position, long or short, in the securities referred to in this report, and/or other related securities, and from time to time may increase or decrease the position or express a view that is contrary to

that contained in this report. The Firm's research analysts, salespeople, traders and other professionals may provide oral or written market commentary or trading strategies that are contrary to opinions expressed in this report. The Firm's asset

management group and proprietary accounts may make investment decisions that are inconsistent with the opinions expressed in this document. The past performance of securities does not guarantee or predict future performance. Transaction strategies

described herein may not be suitable for all investors. This document may not be reproduced or circulated without SVB Securities’ written authority. Additional information is available upon request by contacting the Editorial Department, SVB

Securities LLC, 53 State Street, 40th Floor, Boston, MA 02109. Like all Firm employees, research analysts receive compensation that is impacted by, among other factors, overall firm profitability, which includes revenues from, among other business

units, Institutional Equities, Research, and Investment Banking. Research analysts, however, are not compensated for a specific investment banking services transaction. To the extent SVB Securities' research reports are referenced in this material,

they are either attached hereto or information about these companies, including prices, rating, market making status, price charts, compensation disclosures, Analyst Certifications, etc. is available on

https://svbsecurities.bluematrix.com/bluematrix/Disclosure2. SVB MEDACorp LLC (MEDACorp), an affiliate of SVB Securities LLC, is a global network of independent healthcare professionals (Key Opinion Leaders and consultants) providing industry and

market insights to SVB Securities and its clients. © 2023 SVB Securities LLC. All Rights Reserved. Member FINRA/SIPC. SVB Securities LLC is a member of SVB Financial Group. Confidential

Exhibit (c)(11) PROJECT PACIFIC PROPOSED HIGH PRIORITY PRIVATE COMPANY

TARGETS MAY 2023 Confidential

PROJECT PACIFIC ANHEART THERAPEUTICS INC. Business Description

Management • Clinical-stage global biopharmaceutical company developing Name Title novel precision oncology therapeutics Junyuan Jerry Wang, • Operating in the U.S. and China Chief Executive Officer & Co-Founder Ph.D. • Lead

program, taletrectinib, is ROS1 inhibitor currently in Bing Yan, M.D. Co-Founder & Chief Medical Officer Phase 2 trials for ROS1 fusion-positive NSCLC • Second program, AB-218, is a mIDH1 inhibitor in Phase 2 Lihua Zheng, Ph.D. Co-Founder

& Chief Strategy Officer Headquarters: New York, NY trials for multiple solid tumors with mIDH1 mutations Shuanglian Lian Li, SVP & Chief Medical Officer (US) • Pipeline also includes AB-329, an AXL inhibitor in Phase 1 M.D., Ph.D.

Date of Last Raise: 12/14/2021 combination studies for NSCLC or other solid tumors Edward Lang Jr. Chief Business Officer Amount Raised: $60.9M Company Highlights Taletrectinib Overview • Taletrectinib in-licensed from Daiichi Sankyo in

worldwide • Next-generation, CNS-active ROS1 tyrosine kinase inhibitor exclusive agreement in 2018 (TKI) with selectivity over TRKB • Co-development and co-commercialization agreement with • Ongoing global pivotal Phase 2 trial for

ROS1 TKI-naïve and Innovent in Greater China for $189 million upfront fees and TKI-pretreated patients with ROS1 fusion-positive NSCLC Select Key Investors milestones plus tiered royalties • TRUST-1 Phase 2 trial in China showed

proof-of-concept in • Development and commercialization agreement with NewG NSCLC patients with ~1.5-year follow-up time Lab in Korea for $7 million milestone payments and double- ‒ cORR of 92.5% (62/67) in ROS1 TKI-naïve patients

and digit royalties and 52.6% (20/38) in crizotinib-pretreated patients • Breakthrough Therapy Designation granted in both the U.S. ‒ Median PFS of 33.2 months in ROS1 TKI-naïve patients and China for ROS1+ NSCLC and 11.8 months in

crizotinib-pretreated patients ‒ Well-tolerable with low incidence of neurological AEs Fuzhou Investment Recent News Product Pipeline Early Late Clinical / • April 3, 2023: Appointed Edward Lang, Jr. as Chief Business Drug Indication

Preclinical Clinical Pivotal Trial Officer 1L ROS1 fusion- • March 31, 2023: Presented updated efficacy and safety data Taletrectinib / positive NSCLC AB-106 from taletrectinib Phase 2 study in patients with ROS1+ 2L ROS1 fusion- (ROS1 TKI)

NSCLC that continued to demonstrate clinically meaningful positive NSCLC efficacy outcomes 1L & 2L lower grade Safusidenib / glioma • February 2, 2023: Announced collaboration with Guardant AB-218 (mIDH1 Cholangiocarcinoma Health to

develop Guardant360 CDx and Guardant360 inhibitor) Other solid tumors TissueNext as companion diagnostics for taletrectinib in PD1 combo NSCLC advanced or metastatic ROS1+ NSCLC AB-329 Chemo combo for (AXL inhibitor) solid tumors Undisclosed

Undisclosed Assets Source: Company website, press releases, Pitchbook. Confidential 1

PROJECT PACIFIC ASHER BIOTHERAPEUTICS, INC. Business Description

Management • Biotechnology company developing cis-targeted Name Title immunotherapies for cancer, chronic viral infections, and Craig Gibbs, Ph.D. Chief Executive Officer autoimmune disorders • Cis-targeting platform improves selectivity

and overcomes Ivana Djuretic, Ph.D. Founder, Chief Scientific Officer pleiotropy seen in traditional targeted immunotherapies Kyle Elrod Chief Operating Officer • Cis-targeted candidates consist of an antibody connected to a Andy Yeung, Ph.D.

Founder, Chief Technology Officer Headquarters: S. San Francisco, CA modified immunomodulatory protein, such as a cytokine, Andrea Pirzkall, M.D. Chief Medical Officer designed to only activate specific immune cells with clinically Date of Last

Raise: 09/01/2021 validated function Don O’Sullivan, Ph.D Chief Business Officer Amount Raised: $108.0M – Engineered antibody directs binding with high specificity to immune cell of interest AB248 Overview – Attenuated

immunomodulatory protein avoids activation of off-target immune cells • Engineered IL-2 immunotherapy designed to specifically target CD8+ effector T cells, overcoming native IL-2’s side effects seen with clinical use Company Highlights

• Demonstrated superior selectivity and efficacy in multiple Select Key Investors • Lead program, AB248, has demonstrated preclinical PoC for preclinical models compared to other cytokine therapeutics cis-targeting platform • Dosed

first patient in Phase 1a/1b trial in January 2023 for the • Preclinical studies of AB248 murine surrogate show: treatment of locally advanced or metastatic solid tumors – Therapeutic profile differentiated from first- and second-

• Initial clinical data expected in 2H 2023 generation (non-alpha) IL-2-based therapies – Improved anti-tumor activity and tolerability Product Pipeline – Strong antitumor activity as mono- and combination- Candidate Indication

Discovery IND Enabling Phase 1 therapy AB248 (CD8+ T • Highly modular platform allows for efficient generation of new cell cis-targeted IL- Oncology 2 2) product candidates by reusing the already optimized AB821 (CD8+ T components of existing

candidates cell cis-targeted IL- Oncology 21) CAR-T (cis- Oncology targeted IL-2) Recent News CAR-T (cis- Oncology targeted IL-21) • January 17, 2023: Announced dosing of first patient in Phase Myeloid (targeted 1a/1b clinical trial of AB248,

a cis-targeted il-2 immunotherapy Oncology immune agonist) product candidate, for the treatment of locally advanced or AB359 (CD8+ T Chronic viral metastatic solid tumors cell cis-targeted IL- infections 2) • January 5, 2023: Appointed

independent director Elaine Sun Treg (cis-targeted Autoimmune to Board of Directors cytokine) disease Source: Company website, press releases, Pitchbook. Confidential 2

PROJECT PACIFIC BOUNDLESS BIO, INC. Business Description Management

• Next-generation precision oncology company advancing four Name Title first-in-class or best-in-class programs targeting Zachary Hornby President, Chief Executive Officer extrachromosomal DNA (ecDNA) in aggressive cancers Neil Abdollahian

Chief Business Officer • Company’s Spyglass platform combines proprietary ecDNA model systems with bespoke analytical tools to enable the Chris Hassig, Ph.D. Chief Scientific Officer interrogation of ecDNA cancer Klaus Wagner, M.D.,

Headquarters: San Diego, CA Chief Medical Officer • Developing proprietary software system, ecDNA Harboring Ph.D. Oncogenes (ECHO™), for detecting presence of ecDNA Date of Last Raise: 04/28/2021 Jessica Oien General Counsel oncogene,

which is the first portable precision medicine tool for Amount Raised: $105.0M identifying ecDNA oncogenes and built to be deployable at David Hinkle Vice President, Finance & Controller clinical trial sties or commercial labs • Initial

therapeutic programs will pursue specific solid tumor types where ecDNA are highly prevalent Spyglass Platform Overview • Consists of a comprehensive suite of proprietary ecDNA+/- Company Highlights models across tumor types and oncogene

amplifications Select Key Investors • Company is developing the first ever ecDNA-directed • Enables characterization of ecDNA in cancer cells and provides therapeutics (ecDTx) for ecDNA-driven cancers a synthetic lethality-based approach

to targeting ecDNA-bearing cancers • ecDNA are circles of DNA outside the chromosomes but still within the nucleus of a cell and can be rapidly replicated within • Preclinical results demonstrate ecDNA-enabled colorectal the cell,

causing high numbers of oncogene copies cancer cells have intrinsically elevated levels of replication stress and are hypersensitive to replication stress inducing - ecDNA frequently harbor oncogene amplifications and agents promote resistance by

enhancing genomic diversity, thereby enabling cancer cells to rapidly adapt under • Platform will be essential in understanding how ecDNA drives therapeutic pressure cancer progression and therapeutic resistance - More than half of all high

copy number amplifications in cancer occur on ecDNA Product Pipeline - Company developed directed-assembly techniques using short-read sequencing data to reconstruct ecDNA ecDNA Target Lead IND- Drug Discovery Phase 1/2 Validation Optimization

Enabling - Addressing 400k+ patients in the US with oncogene amplified cancers each year BBI-355 CHK1 BBI-825 Undisclosed Recent News ecDTx 3 Undisclosed • May 9, 2023: Announced first patient dosed in first-in-human ecDTx 4 Undisclosed Phase

1/2 clinical trial of BBI-355 in patients with solid tumors Diagnostic candidate ECHO Undisclosed harboring oncogene amplification • April 17, 2023: Presented data on the novel discovery of CHK1 as an ecDNA essential target in oncogene

amplified cancers at AACR 2023 Source: Company website, press releases, Pitchbook. Confidential 3

PROJECT PACIFIC DTX PHARMA, INC. Business Description Management

• Clinical-stage biotechnology company leveraging RNA-based Name Title therapeutics to treat genetic conditions Arthur T. Suckow, Ph.D. Chief Executive Officer • Initially applying FALCON platform technology to peripheral nervous system,

muscular and CNS disorders Bryan Laffitte, Ph.D. Chief Scientific Officer • R&D strategy is to select targets underlying the genetic cause Peter Condon Chief Business Officer Headquarters: San Diego, CA of the disease and engineer FALCON

siRNAs to repress the disease-causing gene Charles Allerson, Ph.D. SVP of Chemistry Date of Last Raise: 03/01/2021 • Lead program, DTX-1252, is a first-in-class FALCON siRNA Alan Joelson VP, Finance and Operations Amount Raised: $115.0M

therapeutic for Charcot-Marie-Tooth Disease Type 1A (CMT1A) Company Highlights DTX-1252 Overview • FALCON (Fatty Acid Ligand Conjugated OligoNucleotides) • First-in-class FALCON siRNA therapeutic platform conjugates combinations of fatty

acids to siRNAs to • In development for CMT1A, the most common inherited improve cellular uptake and biodistribution Select Key Investors neuromuscular disease affecting 150,000 patients in the US • Fatty acids improve biodistribution in

marketed diabetes drugs and EU such as insulin detemir, degludec, liraglutide and semaglutide • Reversed CMT1A in a mouse model by repressing PMP22 • Small size of fatty acids relative to siRNA keeps doses low • Induced

remyelination of axons to normal levels and increased relative to other delivery mechanisms muscle mass, grip strength, coordination and agility • FALCON siRNAs silence disease-causing genes in tissues • Progressing to clinical

development in 2023 beyond the liver to address disease throughout the body Product Pipeline Recent News • June 28, 2022: Appointed Peter Condon as Chief Business Drug Indication Discovery Preclinical Phase 1 Phase 2 Officer DTX-1252 CMT1A

• May 12, 2022: Announced appointment of Kathie M. Bishop to Muscle ND Board of Directors Disorder • March 1, 2021: Completed $100 million Series B financing to Rare CNS ND Disease advance its FALCON platform and pipeline of RNA

therapeutics ND Other Tissues Source: Company website, press releases, Pitchbook. Confidential 4

PROJECT PACIFIC HUMAN IMMUNOLOGY BIOSCIENCES, INC. Business

Description Management • Clinical-stage biopharmaceutical company leveraging human Name Title genetic and immunological insights to deliver targeted Travis Murdoch, M.D. Chief Executive Officer therapies to patients with severe immune-mediated

diseases Matthew Albert, M.D., • Programs aim to target, modulate or deplete cellular drivers of Chief Translational Officer Ph.D. immune-mediated diseases Carl Henrik Enell Chief Operating Officer • Potential to expand programs into

other indications sharing the Headquarters: S. San Francisco, CA same cellular drivers Uptal Patel, M.D. Chief Medical Officer Date of Last Raise: 11/01/2022 • Cellular approach includes plasma cells, neutrophils and mast cells Amount Raised:

$120.0M Felzartamab Overview Company Highlights • Human mAb directed against CD38 • Obtained exclusive worldwide rights, except for Greater China, • Phase 1b/2a POC trial (n=31) in primary membranous for felzartamab, and rights in

Greater China and South Korea nephropathy (PMN) showed for HIB210 (formerly MOR210) from MorphoSys in 2022 - Dose-dependent reduction in pathogenic antibody levels • MorphoSys received 15% equity in HIBio, $15 million upfront •

Proteinuria remission observed across patient groups, Select Key Investors cash payment for HIB210, and up to $1 billion in milestones including those starting with high aPLA2R titers or across both programs plus single- to low double-digit

royalties refractory to prior immunosuppressive therapies • Launched in November 2022 with $120 million financing • Median reductions of 45% in aPLA2R titers were • Incubated by ARCH Venture Partners and Monograph Capital observed

in most patients as early as one week, with deep responses (>50% reduction) in most patients at six months • Well tolerated with mild to moderate TEAEs Recent News • Currently being evaluated in Phase 2 trials in PMN, • April

18, 2023: Appointed Uptal Patel, M.D. as Chief Medical Immunoglobulin A Nephropathy and for antibody mediated Officer and Sunil Agarwal, M.D. as Board Member rejection (AMR) of renal allograft transplants • April 11, 2023: Announced positive

Phase 2 data on felzartamab for the treatment of primary membranous Product Pipeline nephropathy • November 1, 2022: Launched with $120 Million financing Drug Indication Preclinical Phase 1 Phase 2 Primary membranous • June 14, 2022:

Entered into equity participation and license nephropathy agreements with MorphoSys for felzartamab and MOR210 Felzartamab IgA Nephropathy (CD38) Antibody-mediated transplant rejection HIB210 Undisclosed (C5aR1) Mast cell Undisclosed program Source:

Company website, press releases, Pitchbook. Confidential 5

t PROJECT PACIFIC IMMPACT BIO, INC. Business Description Management

• Clinical-stage biotechnology company dedicated to the Name Title discovery of transformative chimeric antigen receptor (CAR) T- Sumant Ramachandra, M.D., Ph.D. President & CEO cell therapies for various cancers where other treatments

have been exhausted Vikram Lamba Chief Financial Officer • Next generation bispecific CAR T-cell technologies precisely Jonathan Benjamin, M.D, Ph.D. Chief Medical Officer distinguish cancer cells from normal cells, thereby eliminating

Headquarters: West Hills, CA the severe side effects endured by cancer patients Jim Johnston, Ph.D. Chief Scientific Officer Date of Last Raise: 01/20/2022 Venkat Yepuri Chief Operating Officer Amount Raised: $111.0M Sylvain Roy Chief Technical

Officer Company Highlights CD19-CD20 Bispecific CAR-T Overview • The company’s logic-gate-based CAR-T platforms address key • The company’s lead program is a CD19-CD20 bispecific ‘OR- biological challenges in treating

cancer and are specifically gate’ CAR-T designed to address antigen escape, a key designed to prevent antigen escape, prevent ‘on-target – off- challenge for current approved CD19 therapies Select Key Investors tumor’

toxicities, and overcome the immunosuppressive tumor • Updated data from the ongoing Phase 1 trial of patients with microenvironment relapsed or refractory B-cell non-Hodgkin’s lymphoma • OR-gated bispecific CAR-T is based on the

work of pioneering demonstrated a total of seven of eight patients achieved and oncology and immunology scientists from UCLA and the remain in complete remission (12 months median follow-up) MIGAL-Galilee Research Institute • Ongoing

investigational study (UCLA) demonstrated potential best-in-class safety and efficacy data from 10 patients who had received 3 prior lines of treatment - Demonstrated 90% ORR and 70% CR Recent News - Observed limited toxicity (no ICANS/neurotoxicity

and no CRS above grade 1) • February 8, 2023: Appointed Biren Amin to its Board • January 24, 2023: Announced FDA clearance of IND for novel bispecific CAR to treat aggressive B-cell lymphoma Product Pipeline • September 22, 2022:

Appointed Jonathan Benjamin, M.D., Ph.D. as Chief Medical Officer Lead IND Drug Indication Phase 1/1b • August 10, 2022: Appointed Vikram Lamba as Chief Financial Selection Enabling Officer and Head of Business Development CD19-CD20 NHL &

CLL Bispecific CAR-T • May 9, 2022: Appointed Sylvain Roy as Chief Technical Officer LOH Bispecific Lung Cancer CAR-T • April 19, 2022: Appointed Venkat Yepuri as Chief Operating Officer TGF-β x ND Glioblastoma CAR-T Bispecific

Source: Company website, press releases, Pitchbook. Confidential 6

PROJECT PACIFIC MBX BIOSCIENCES, INC. Business Description Management

• Biotechnology company focused on discovery, development, Name Title and commercialization of transformative peptide therapeutics Kent Hawryluk President & Chief Executive Officer • Founded by seasoned industry veterans with

expertise in endocrine drug development, including the development and Mary Jane Geiger, M.D., Chief Medical Officer commercialization of first-in-class endocrine therapeutics such Ph.D. as Forteo® and Humalog® Headquarters: Carmel, IN

Richard DiMarchi, Ph.D. Chief Scientific Officer • Advancing a pipeline of candidates with clinically validated targets, defined regulatory pathways and unmet medical needs Date of Last Raise: 11/14/2022 Richard Bartram Chief Financial Officer

in a variety of endocrine disorders Amount Raised: $115.0M Company Highlights MBX 2109 Overview • World-class technology platform of Precision Endocrine • MBX 2109 is an investigational parathyroid hormone (PTH) Peptides (PEPs),

innovative peptide hormone analogs peptide prodrug in development as a long-acting hormone engineered to have optimized pharmaceutical properties replacement therapy for hypoparathyroidism • Advancing a pipeline of PEPs that have been

selectively • Under physiological conditions, MBX 2109 (prodrug) is Select Key Investors modified using state-of-the-art and proprietary chemical designed to release the active PTH peptide, referred to as modifications to enhance the stability

and pharmacokinetics MBX 2099, at a precisely controlled rate compared to the native peptide hormone • Both MBX 2109 (prodrug) and MBX 2099 (active peptide) are • Aim to extend the duration of action of the PEP thereby designed to have

extended half-lives with the potential to necessitating few administrations enable once-weekly administration • Currently being evaluated in healthy subjects in a Phase 1 trial Product Pipeline Recent News • November 14, 2022: Announced

closing of $115 million Drug Indication Discovery Preclinical Phase 1 Series B financing led by Wellington Management • October 5, 2022: Announced advancements in phase 1 MBX 2109 Hypoparathyroidism clinical trial of MBX 2109 • July 26,

2022: Received Orphan Drug Designation for MBX Post-bariatric 2109 for the treatment of hypoparathyroidism MBX 1416 hypoglycemia (PBH) • April 11, 2022: Appointed Richard Bartram as Chief Financial Officer Additional Lead Undisclosed

Candidates Source: Company website, press releases, Pitchbook. Confidential 7

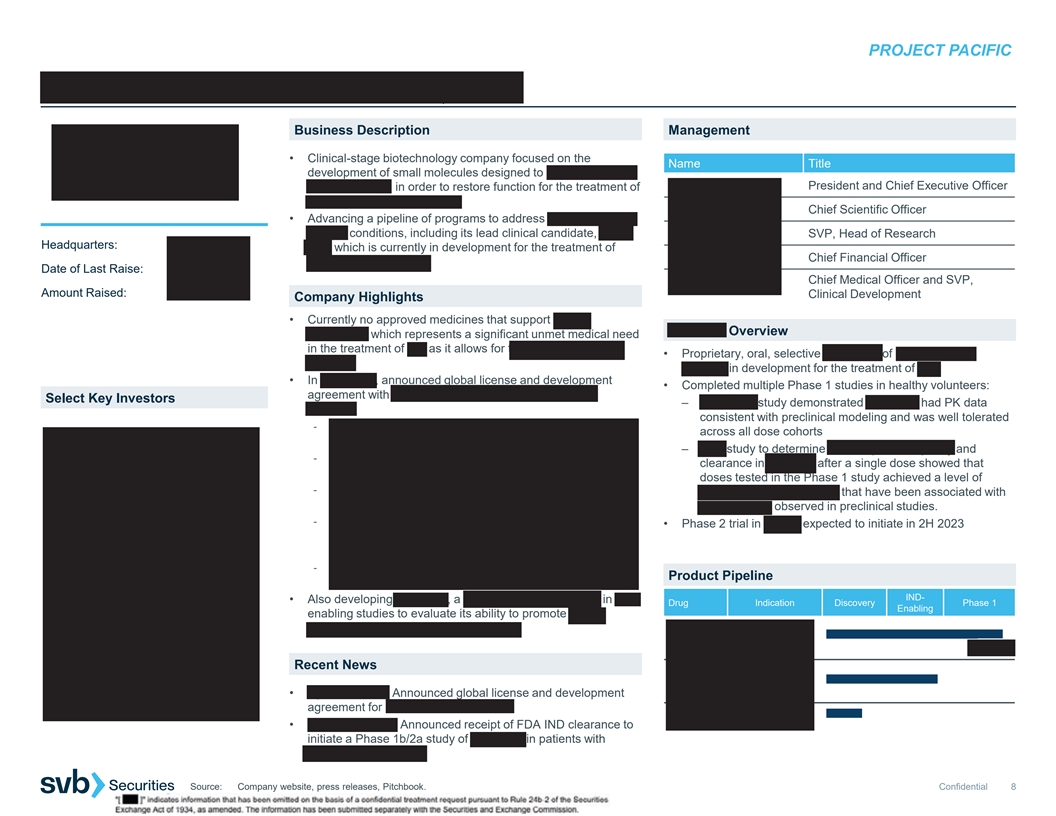

PROJECT PACIFIC PIPELINE THERAPEUTICS, INC. Business Description

Management • Clinical-stage biotechnology company focused on the Name Title development of small molecules designed to reactivate innate Carmine Stengone President and Chief Executive Officer repair pathways in order to restore function for

the treatment of neurodegenerative diseases. Daniel Lorrain, Ph.D. Chief Scientific Officer • Advancing a pipeline of programs to address CNS and neuro- otology conditions, including its lead clinical candidate, PIPE- Austin Chen, Ph.D. SVP,

Head of Research Headquarters: San Diego, CA 307, which is currently in development for the treatment of Peter Slover Chief Financial Officer multiple sclerosis (MS). Date of Last Raise: 4/17/23 Chief Medical Officer and SVP, Stephen Huhn, M.D.

Amount Raised: $50.0M Clinical Development Company Highlights • Currently no approved medicines that support myelin PIPE-307 Overview restoration, which represents a significant unmet medical need in the treatment of MS as it allows for the

repair of neuronal • Proprietary, oral, selective antagonist of muscarinic M1 damage. receptor in development for the treatment of MS. • In April 2023, announced global license and development • Completed multiple Phase 1 studies

in healthy volunteers: agreement with Janssen Pharmaceutica of Johnson & Select Key Investors – SAD/MAD study demonstrated PIPE-307 had PK data Johnson. consistent with preclinical modeling and was well tolerated - Janssen granted

exclusive license to research, develop across all dose cohorts and commercialize PIPE-307 in all indications – PET study to determine M1 receptor occupancy and - Pipeline retains ability to develop PIPE-307 for relapsing- clearance in the

brain after a single dose showed that remitting multiple sclerosis (RRMS) doses tested in the Phase 1 study achieved a level of - Pipeline received $50M upfront cash payment and $25M uptake in the human brain that have been associated with equity

investment from Johnson & Johnson Innovation remyelination observed in preclinical studies. - Pipeline eligible for ~$1B in clinical, regulatory and • Phase 2 trial in RRMS expected to initiate in 2H 2023 commercial milestones, as well as

tiered double-digit royalty payments - Additionally, Pipeline also received $25M equity Product Pipeline investment from Pipeline’s existing investors IND- • Also developing PIPE-791, a LPA1 receptor antagonist in IND- Drug Indication

Discovery Phase 1 Enabling enabling studies to evaluate its ability to promote myelin PIPE-307 restoration and treat neuroinflammation. (M1R Myelin Restoration antagonist) Recent News PIPE-791 Myelin Restoration, (LPA1R Neuroinflammation antagonist)

• April 17, 2023: Announced global license and development agreement for PIPE-307 with Janssen Discovery Axonal Repair • March 28, 2022: Announced receipt of FDA IND clearance to initiate a Phase 1b/2a study of PIPE-307 in patients with

relapsing-remitting MS Source: Company website, press releases, Pitchbook. Confidential 8

PROJECT PACIFIC Q32 BIO INC. Business Description Management •

Clinical-stage company pioneering a new approach to treating Name Title complement-mediated diseases Jodie Morrison Acting Chief Executive Officer • Lead candidate, ADX-097, is a tissue targeted CD3 antibody Shelia Violette, Ph.D. Chief

Scientific Officer fH1-5 fusion protein for the treatment of complement alternative pathway driven disease Jason Campagna, Chief Medical Officer M.D., Ph.D. • Most advanced program, ADX-914, is a potent IL-7Rα Headquarters: Waltham, MA

antagonist with the potential to be a best-in-class modulator of Adam Cutler Chief Financial Officer IL-7 signaling that is being developed in collaboration with Date of Last Raise: 10/29/2020 Horizon Therapeutics Amount Raised: $60.0M ADX-097

Overview Company Highlights • A bifunctional fusion protein containing two moieties of the first five consensus repeats of human factor H (fH1-5) linked to a • ADX-914 is currently being evaluated in a Phase 2 trial for humanized

anti-C3d antibody atopic dermatitis (AD) with an additional Phase 2 trial, in • Designed to target diseased tissue via binding to C3d, which is another indication, to be initiated in 2023 deposited at sites of complement activation, and

provide • Under the Horizon agreement, Horizon will fund development localized blockade Select Key Investors through the two Phase 2 trials of ADX-914 with Q32 being • ADX-097 may potently and durably block complement activity in

operationally responsible humans, while preserving the body’s ability to fight infection - Horizon has an option to acquire the program – exercisable effectively, thereby avoiding the potentially damaging effects of through a period

following the completion of the Phase 2 systemic complement inhibition trials • Preclinical models showed potent, durable, and efficacious local - Q32 received $55mm in upfront payment and, if the option alternative pathway complement blockade

at low doses that is exercised, is eligible to receipt up to an additional avoid systemic complement inhibition $645mm in closing and milestone payments plus tiered • Currently conducting a first-in-human, Phase 1, ascending dose royalties

(SAD/MAD) clinical study of ADX-097 for the treatment of complement disorders Recent News • October 27, 2022: Announced dosing of first patient in Phase 2 Product Pipeline trial of ADX-914 of atopic dermatitis with Horizon Therapeutics Drug

Indication Discovery Preclinical Phase 1 Phase 2 • September 20, 2022: Appointed Jodie Morrison, a Venture Complement Platform Partner at Atlas Venture, as Board of Director and acting Chief Executive Officer ADX-097 Complement • August

15, 2022: Entered into a collaboration and option mAb-CR1a disorders agreement with Horizon to develop ADX-914 for the treatment fAb-fH/CR1 of autoimmune diseases Partnered Program • May 26, 2022: Initiated first-in-human Phase 1 trial of

ADX-097 for the treatment of complement disorders ADX-914 AD Source: Company website, press releases, Pitchbook. Confidential 9

PROJECT PACIFIC Disclosures This information (including, but not

limited to, prices, quotes and statistics) has been obtained from sources that we believe reliable, but we do not represent that it is accurate or complete and it should not be relied upon as such. All information is subject to change without

notice. The information is intended for Institutional Use Only and is not an offer to sell or a solicitation to buy any product to which this information relates. SVB Securities LLC (“Firm”), its officers, directors, employees,

proprietary accounts and affiliates may have a position, long or short, in the securities referred to in this report, and/or other related securities, and from time to time may increase or decrease the position or express a view that is contrary to

that contained in this report. The Firm's research analysts, salespeople, traders and other professionals may provide oral or written market commentary or trading strategies that are contrary to opinions expressed in this report. The Firm's asset

management group and proprietary accounts may make investment decisions that are inconsistent with the opinions expressed in this document. The past performance of securities does not guarantee or predict future performance. Transaction strategies

described herein may not be suitable for all investors. This document may not be reproduced or circulated without SVB Securities’ written authority. Additional information is available upon request by contacting the Editorial Department, SVB

Securities LLC, 53 State Street, 40th Floor, Boston, MA 02109. Like all Firm employees, research analysts receive compensation that is impacted by, among other factors, overall firm profitability, which includes revenues from, among other business

units, Institutional Equities, Research, and Investment Banking. Research analysts, however, are not compensated for a specific investment banking services transaction. To the extent SVB Securities' research reports are referenced in this material,

they are either attached hereto or information about these companies, including prices, rating, market making status, price charts, compensation disclosures, Analyst Certifications, etc. is available on

https://svbsecurities.bluematrix.com/bluematrix/Disclosure2. SVB MEDACorp LLC (MEDACorp), an affiliate of SVB Securities LLC, is a global network of independent healthcare professionals (Key Opinion Leaders and consultants) providing industry and

market insights to SVB Securities and its clients. © 2023 SVB Securities LLC. All Rights Reserved. Member FINRA/SIPC. SVB Securities LLC is a member of SVB Financial Group. Confidential

Exhibit (c)(12) PROJECT PACIFIC STRATEGIC PROCESS UPDATE MAY 24, 2023

Confidential

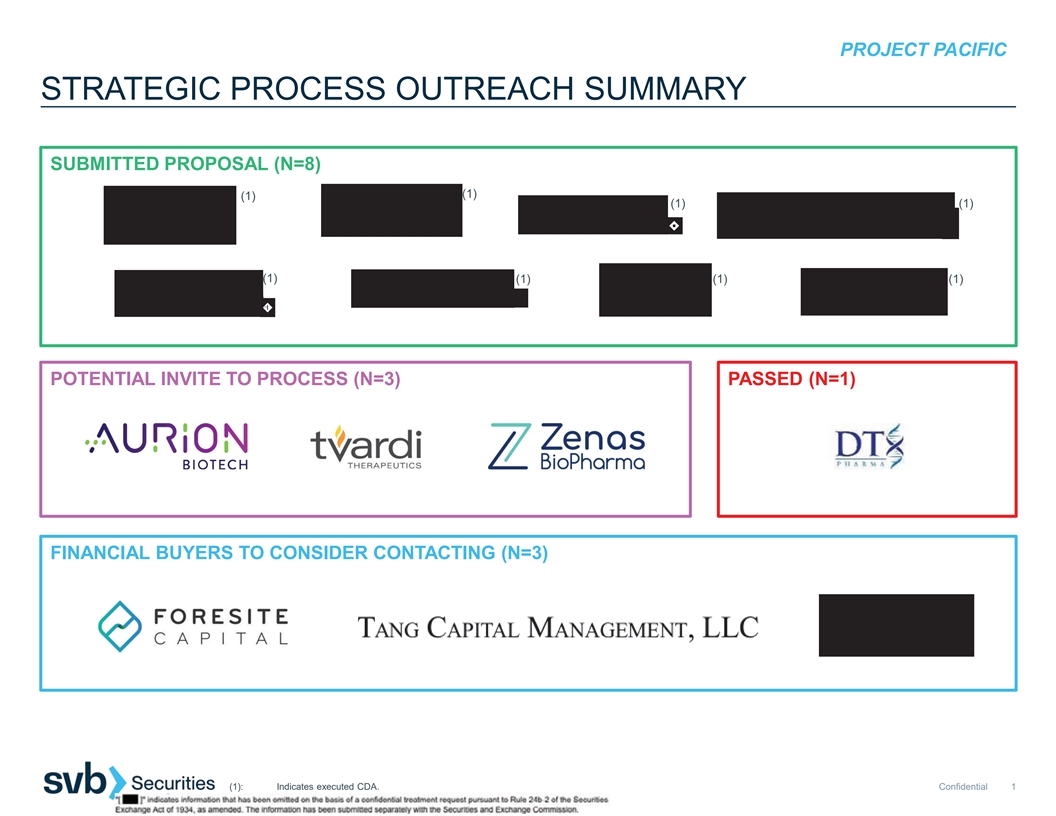

PROJECT PACIFIC STRATEGIC PROCESS OUTREACH SUMMARY SUBMITTED PROPOSAL

(N=8) (1) (1) (1) (1) (1) (1) (1) (1) POTENTIAL INVITE TO PROCESS (N=3) PASSED (N=1) FINANCIAL BUYERS TO CONSIDER CONTACTING (N=3) (1): Indicates executed CDA. Confidential 1

PROJECT PACIFIC HOW COUNTERPARTIES ARE VALUING PACIFIC AND THEMSELVES

$ IN USD MILLIONS. SORTED ALPHABETICALLY. PACIFIC VALUATION COUNTERPARTY PF OWNERSHIP ASSETS / PRO FORMA TARGET PIPE PARTY CASH LISTING TECHNOLOGY TOTAL VALUATION STEP-UP CASH RUNWAY (INSIDER COMMITMENT) PACIFIC PARTY PIPE (1) (2) $40 $5 - $45 $155

ND Through 2024 - 22.5% 77.5% - (3) (4) 140 10 - 150 250 1.25x Through 2024 $40 (100%) 34.1% 56.8% 9.1% Through 1H 140 5 - 145 357 1.10x - 28.9% 71.1% - 2025 140 - - 140 402-434 1.50-1.62x Into 2H 2026 - 24.4-25.8% 74.2-75.6% - 140 7 - 147 325 1.50x

Into 2026 75-125 (ND) 24.6-26.9% 54.4-59.4% 13.7-20.9% (5) (5) Through early 40 10 - 50 257 1.00x 110 (68%) 12.0% 61.6% 26.4% 2026 (6) 140 15 - 155 310 1.00x Through 2027 - 33.3% 66.7% - (7) 140 15 - 155 250 1.35x Into 2H 2026 - 38.3% 61.7% - (1):

PACIFIC net cash at close in excess of $40M to be returned to pre-transaction PACIFIC shareholders. (2): Pro forma runway includes ~$280M in non-dilutive funding from BARDA. (3): Runway through 2024 requires only $100M. (4): Concurrent PIPE not

required. Insiders and licensing partner have indicated $40M commitment to any potential PIPE. (5): IMMPACT BIO plans to announce a share buyback upon announcement of the transaction for up to $100M to provide liquidity to PACIFIC stockholders

seeking to exit the transaction. (6): Ongoing discussions with investors to extend Series C by $25-50M, which would increase post-money for Series C and valuation for proposed transaction accordingly. (7): Existing Q32 shareholders have a signed a

letter committing at least $30 million for PIPE financing. This funding could be used to extend runway further or potentially return a portion of PACIFIC's cash to its shareholders. Confidential 2

PROJECT PACIFIC COUNTERPARTY CATALYSTS IN PRO FORMA CASH RUNWAY SORTED

ALPHABETICALLY. PF runway: Through 2024 PF runway: Through 2024 PF runway: Through 1H 2025 PF runway: Into 2H 2026 • BARDA contract (~$280M) • Taletrectinib/AB-106 in non-small cell lung • AB248 in solid tumors • BBI-355 in

oncogene amplified cancers – June 2023: Submit proposal cancer – 3Q23: Phase 1a monotherapy PD data – Mid-2024: Phase 1/2 clinical POC data – July-August 2023: Funding signal – 2H23: Global Phase 2 TRUST-II interim

– 2H23: Initiate Phase 1a/b anti-PD1 • BBI-825 in oncogene amplified cancers – September 2023: Contract data combination trial – 4Q23: IND filing • AER003 / AER004 / AER005 – 4Q23: Complete enrollment of global

– Late 2023 / early 2024: initiate Phase 1b – 2Q24: Initiate Phase 1/2 trial – 4Q23: Initiate Phase 1/2 trial Phase 2 TRUST-II monotherapy expansion cohorts – 2H25: Phase 1/2 clinical POC data – 1Q24: Initiate Phase 3

trial – 1H24: Initiate global Phase 3 TRUST-III – June 2024: Phase 1a/b preliminary • ecDTx 3 in oncogene amplified cancers – 4Q24: EUA /=and commercial launch confirmatory study monotherapy activity data – 4Q23: In

vivo POC – 2Q24: Pre-NDA type B meeting with FDA – 2H24 / 1Q25: Phase 1a/b anti-PD1 – 1H24: Development candidate selection (6-month follow up data) combination activity data – 2Q25: IND filing – 3Q24: Global Phase 2

TRUST-II final data • AB821 in solid tumors – 3Q25: Initiate Phase 1/2 trial – 4Q24: NDA submission in the US – 3Q23: GLP tox • ecDTx 4 in oncogene amplified cancers – 2Q25: US NDA approval – 3Q23: GMP

manufacturing and pilot – 1Q24: In vivo POC • Safusidenib/AB-218 in lower grade glioma, batch – 2H24: Development candidate selection cholangiocarcinoma – Q423: IND filing – 4Q25: IND filing – Ongoing: Enrollment

for Phase 2 global – 1Q24: Initiate Phase 1 trial – 1H26: Initiate Phase 1/2 trial studies – 2H24: Preliminary Phase 1 PD data • ECHO Platform – 2H23: IDE filing – 1Q24: CTA filing Note: Pro forma cash runway

includes concurrent PIPE proceeds where applicable. Bold indicates catalysts that could fall within the transaction window. Confidential 3

PROJECT PACIFIC COUNTERPARTY CATALYSTS IN PRO FORMA CASH RUNWAY

(CONT.) SORTED ALPHABETICALLY. PF runway: Into 2026 PF runway: Through early 2026 PF runway: Through 2027 PF runway: Into 2H 2026 • Felzartamab – 2Q23: reproductive tox data • IMPT-314 in ≥3L CAR-T naïve ABCL •

PIPE-307 in r/r MS • ADX-097 in complement-mediated renal • Felzartamab in PMN – 2H23: Phase 1 data – 2H23: Phase 2 POC initiation diseases – 2H23: Interim data from POC study in – 4Q24: Phase 2 pivotal data

– 2Q25: Phase 2 POC study completion – 2024 and 2025: Phase 2 AAV 12-week aCD20-refractory population – 3Q25: Phase 2 pivotal data update • PIPE-307 in other neurological disorders, safety/efficacy and topline data, –

1H24: Phase 3 initiation – 1Q26: BLA submission including MDD respectively • Felzartamab in IgAN – 2Q23: Clinical POC • IMPT-314 in CAR-T experienced ABCL – 2023 and 2024: initiate multiple Phase 2 – 2024 and

2025: Phase 2 renal basket trial • Felzartamab in LN – 1Q24: Phase 1 data POC studies 4-week / biomarker topline data and – 2H23: Phase 1 initiation – 2Q24: EOP1 meeting – 1Q25: Phase 2 POC studies completion

interim12-week data, respectively – 2H24: Clinical POC – 2H24: Phase 2 data update • PIPE-791 – 2H25-1H26: Phase 2/3 trial initiations in – 2024 and 2025: Phase 1b readouts – 1H25: BLA submission – 1H23: IND

filing complement-mediated renal diseases • Felzartamab in AMR • IMPT-314 in 2L HCT unintended ABCL – 1H24: Phase 1 HV study completion • ADX-096 – 1H25: IND submission – 1Q24: Clinical POC – 1Q25: Patient

data – 4Q24: Phase 1 PET study completion • Novel nanobodies – 2024: DC nomination – 1Q24: Phase 2 investigator sponsored trial – 1H26: BLA submission – 2Q25: Chronic tox studies • ADX-914 in atopic

dermatitis readout in AMR • IMPT-314 – 1Q26: patient data in 2L HCT – 3Q25: Biomarker studies completion – 2H23: Receipt of all additional • HIB210 in severe IMDs eligible ABCL – 3Q25: Phase 2a trial initiation

development funding from Horizon – 3Q23: Preclinical data supporting • IMPT-514 in r/r lupus nephritis • Calpain – 2H23: Phase 2 study completion superiority to avacopan – Mid 2023: IND clearance – 4Q25: IND

submission – 2H24: Phase 2 study completion in second – 1H23: Phase 1 trial initiation in healthy – 3Q24: Phase 1 first cohort data – 1Q26: Phase 1 study initiation (undisclosed) indication volunteers – 1Q25: EOP1

meeting – Late 2024 – early 2025: Horizon option – 1Q24: NHP chronic tox study readout – 3Q25: Phase 2 pivotal data exercise window (subject to a significant – 1H24: Subcutaneous formulation – 2Q26: BLA submission

option exercise fee) for the acquisition of developments insights • IMPT-514 in severe systemic lupus all of Q32’s assets related to ADX-914 – 1H24: Phase 2 study initiation in AAV erythematosus with extrarenal disease –

1H24: Phase 1 readout in healthy – 1Q24: IND amendment volunteers – 4Q24: Patient data • Advanced discovery programs – 2023: – 3Q26: BLA submission development candidate nomination • IMPT-514 in ANCA-associated

vasculitis – 2Q24: IND amendment – 1H25: Patient data – 4Q26: BLA submission • IMPT-514 in secondary progressive MS – 3Q24: IND amendment – Mid 2025: Patient data – 4Q26: BLA submission Note: Pro forma cash

runway includes concurrent PIPE proceeds where applicable. Bold indicates catalysts that could fall within the transaction window. Confidential 4

PROJECT PACIFIC INITIAL INDICATIONS OF INTEREST: AERIUM | ANHEART

Transaction Structure • Reverse triangular merger • Reverse triangular merger (2) • Assumes closing 09/30/23 • Prepared to sign merger agreement and close transaction in 2H 2023 and Timing • AERIUM: $155M (includes $2M

current cash position and ongoing insider-led round which will fund • ANHEART: $250M (includes $5M of cash expected at 09/30/23 and $5M from ANHEART strategic AERIUM through September 2023) partnership) Implied Valuation (1) • PACIFIC:

$45M (based on $40M net cash at close + $5M for Nasdaq listing) • PACIFIC: $150M (based on $140M net cash at close + $10M for Nasdaq listing) Post-$ Last Round / • AERIUM’S post-money from last private round (Series A, 2022): ND

• ANHEART’S post-money from last private round (Series B, September 2021): $200M • Step-up: ND • Step-up: 1.25x Step-up • (Incl. optional $40M PIPE 100% covered by insiders and licensing partner) ANHEART: 56.8% /

Implied Ownership Split • (Excl. PIPE) AERIUM: 77.5% / PACIFIC: 22.5% PACIFIC: 34.1% / PIPE: 9.1% • (Excl. PIPE) ANHEART: 62.5% / PACIFIC: 37.5% • Concurrent PIPE not required • Concurrent PIPE not contemplated •

Insiders and licensing partner have indicated $40M commitment to any potential PIPE • AERIUM pursuing ~$280M BARDA contract to fund development to EUA and launch Concurrent Financing • ANHEART has also explored entering $30M investment

from SDIC at $250M pre-money (not included • AERIUM ongoing insider-led round to fund company through September 2023 in $40M of commitments from insiders and licensing partner) (2) • Pro forma cash (excl. ~$280M BARDA contract): $40M

(AERIUM: $0M expected at 09/30/23 ; (1) PACIFIC: $40M ) • Pro forma cash (incl. optional PIPE): $190M (ANHEART: $10M, including $5M expected at 09/30/23 Pro Forma Cash and (2) • Pro forma cash (incl. ~$280M BARDA contract): $320M

(AERIUM: $0M expected at 09/30/23 ; and $5M from licensing partner; PACIFIC: $140M; PIPE: $40M) Runway (1) PACIFIC: $40M ) • Runway: $100M funds through 2024 • Runway: through 2024 (with BARDA funding) • AER003 (preclinical)

– mAb antiviral treatment against SARS-CoV-2 occupying ACE2 footprint • Taletrectinib/AB-106 (Pivotal Phase 2) – ROS1 inhibitor for ROS1 fusion-positive NSCLC • AER004 (preclinical) – mAb antiviral treatment against

SARS-CoV-2 • Safusidenib/AB-218 (Phase 2) – mIDH1 inhibitor for lower grade glioma, cholangiocarcinoma and • AER005 (preclinical) – mAb antiviral treatment against SARS-CoV-2 binding outside Receptor Binding other tumors Key

Asset(s) Domain • AB-329 (Phase 1) – AXL inhibitor for combination with checkpoint inhibitors or chemotherapy in • Two mAbs planned to be developed in combination; third to be developed as contingency for viral NSCLC and other

solid tumors evolution • 5 undisclosed assets (Preclinical) • Taletrectinib/AB-106 in non-small cell lung cancer • BARDA contract (~$280M) – 2H23: Global Phase 2 TRUST-II interim data – June 2023: Submit proposal

– 4Q23: Complete enrollment of global Phase 2 TRUST-II – July-August 2023: Funding signal – 1H24: Initiate global Phase 3 TRUST-III confirmatory study Timing of Key – September 2023: Contract – 2Q24: Pre-NDA type B

meeting with FDA (6-month follow up data) • AER003 / AER004 / AER005 – 3Q24: Global Phase 2 TRUST-II final data Milestones – 4Q23: Initiate Phase 1/2 trial – 4Q24: NDA submission in the US – 1Q24: Initiate Phase 3 trial

– 2Q25: US NDA approval – 4Q24: EUA /=and commercial launch • Safusidenib/AB-218 in lower grade glioma, cholangiocarcinoma – Ongoing: Enrollment for Phase 2 global studies Plans for PACIFIC’s • Open to discussing

retaining PACIFIC employees for open positions, including CFO, GC and CBO, as • Open to discussions retention of certain personnel, particularly those in the finance and accounting well as PACIFIC’s public company infrastructure and

capabilities functions, during a transition period or full-time following a Transaction Employees • N/A • N/A Exclusivity • Financial: Piper Sandler Advisors • N/A • Legal: WilmerHale • Auditor: Deloitte •

Board Composition: 10 members; 6 designated by ANHEART and 4 designated by PACIFIC • ANHEART does not assume reliance on PACIFIC non-cash assets, facilities or business • Board Composition: 8 board members; 5 designated by AERIUM (one of

which could potentially be • Audit Status: Have completed audits in China for 2021 and 2022; in process of initiating conversion to independent director from PACIFIC board) and 3 designated by PACIFIC US GAAP standards with completion in mid

2023 • AERIUM would consider CVR for development or out licensing of PACIFIC assets Additional Information • Out-licensed Japanese commercial rights for taletrectinib to global pharmaceutical partner. Licensing • Audit Status: ND

will close concurrently with reverse merger; ANHEART to receive $15M in equity and non-dilutive (1) • Proposal allows most PACIFIC cash to be returned to pre-transaction shareholders upfront payments upon closing, $63M in potential milestone

payments, and high double-digit royalties on net sales • Octagon Investments, Decheng Capital, Laurion Capital, Sage Partners, Innovent Biologics and Select Investors • Omega Funds, F-Prime Capital Cenova (1): PACIFIC net cash at close

in excess of $40M to be returned to pre-transaction PACIFIC shareholders. (2): Based on assumption that ongoing insider-led round funds company through September 2023. Note: Bold indicates catalysts that could fall within the transaction window.

Confidential 5

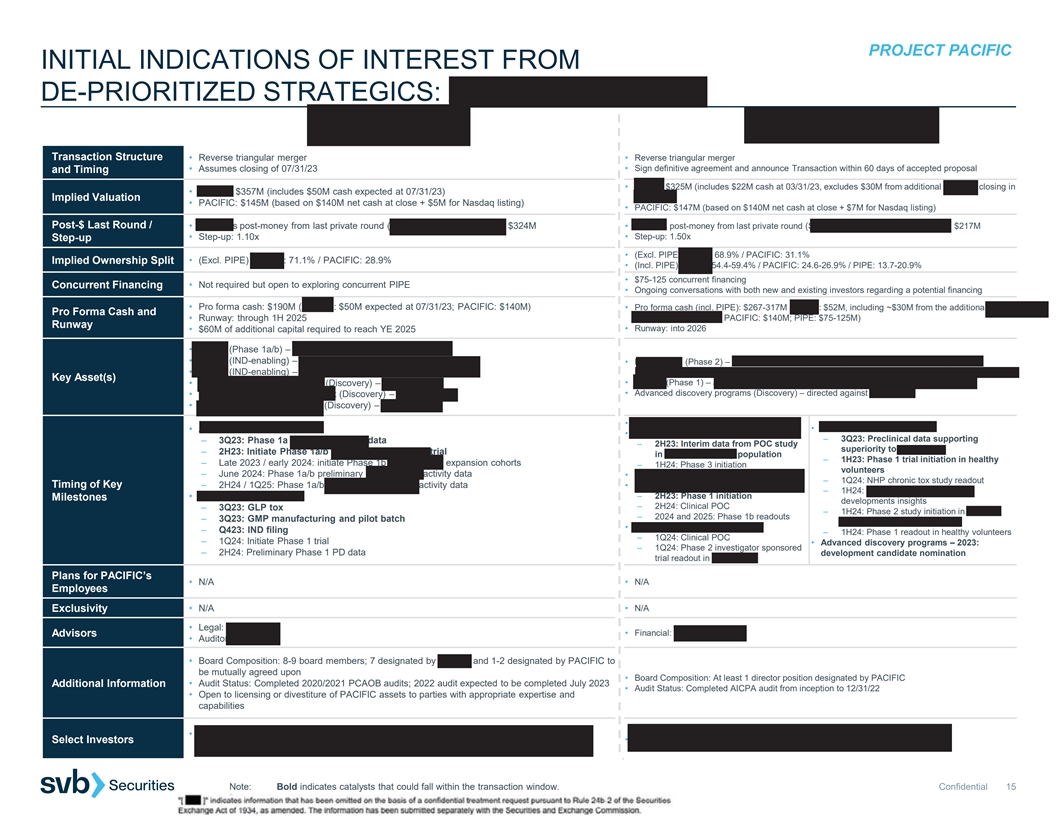

PROJECT PACIFIC INITIAL INDICATIONS OF INTEREST: ASHER BIO | BOUNDLESS

BIO Transaction Structure • Reverse triangular merger • Reverse triangular merger • Assumes closing of 07/31/23 • Entry into a definitive merger agreement within 30-45 days of being selected to move forward and Timing •

ASHER: $357M (includes $50M cash expected at 07/31/23) • BOUNDLESS: $402-434M (includes $142M of cash expected at 06/30/23) Implied Valuation • PACIFIC: $145M (based on $140M net cash at close + $5M for Nasdaq listing) • PACIFIC:

$140M (based on $140M net cash at close + $0M for Nasdaq listing) Post-$ Last Round / • ASHER’s post-money from last private round (Series B, September 2021): $324M • BOUNDLESS’ post-money from last private round (Series C,

May 2023): $268M • Step-up: 1.10x • Step-up: 1.50x-1.62x Step-up • (Excl. PIPE) ASHER: 71.1% / PACIFIC: 28.9% • (Excl. PIPE) BOUNDLESS: 74.2-75.6% / PACIFIC: 24.4-25.8% Implied Ownership Split Concurrent Financing • Not

required but open to exploring concurrent PIPE • No planned financing concurrent with the transaction • Pro forma cash: $190M (ASHER: $50M expected at 07/31/23; PACIFIC: $140M) Pro Forma Cash and • Pro forma cash: $282M (BOUNDLESS:

$142M expected at 06/30/23; PACIFIC: $140M) • Runway: through 1H 2025 • Runway: into 2H 2026 Runway • $60M of additional capital required to reach YE 2025 • AB248 (Phase 1a/b) – CD8-targeted IL2 for solid tumors •

BBI-355 (Phase 1/2) – oral CHK1 inhibitor for oncogene amplified cancers • AB821 (IND-enabling) – CD8-targeted IL21 for solid tumors • BBI-825 (IND-enabling) – extrachromosomal DNA directed therapies (exDTx) for

oncogene • AB359 (IND-enabling) – CD8-targeted IL2 for chronic viral infection amplified cancers Key Asset(s) • Cell therapy-targeted IL-2 / 21 (Discovery) – for cancer • ecDTx 3 (Discovery) – for oncogene

amplified cancers • Myeloid-targeted immune agonist (Discovery) – for cancer • ecDTx 4 (Discovery) – for oncogene amplified cancers • CD4+ T cell-targeted cytokine (Discovery) – for cancer • ECHO / ecDNA

Harboring Oncogenes (IND-enabling) – patient selection diagnostic assay • AB248 in solid tumors • BBI-355 in oncogene amplified cancers – 3Q23: Phase 1a monotherapy PD data – Mid-2024: Phase 1/2 clinical POC data

– 2H23: Initiate Phase 1a/b anti-PD1 combination trial • ecDTx 4 in oncogene amplified cancers • BBI-825 in oncogene amplified cancers – Late 2023 / early 2024: initiate Phase 1b monotherapy expansion cohorts – 1Q24: In

vivo POC – 4Q23: IND filing – June 2024: Phase 1a/b preliminary monotherapy activity data – 2H24: Development candidate selection – 2Q24: Initiate Phase 1/2 trial Timing of Key – 2H24 / 1Q25: Phase 1a/b anti-PD1

combination activity data – 4Q25: IND filing – 2H25: Phase 1/2 clinical POC data • AB821 in solid tumors – 1H26: Initiate Phase 1/2 trial Milestones • ecDTx 3 in oncogene amplified cancers – 3Q23: GLP tox •

ECHO Platform – 4Q23: In vivo POC – 3Q23: GMP manufacturing and pilot batch – 2H23: IDE filing – 1H24: Development candidate selection – Q423: IND filing – 1Q24: CTA filing – 2Q25: IND filing – 1Q24:

Initiate Phase 1 trial – 3Q25: Initiate Phase 1/2 trial – 2H24: Preliminary Phase 1 PD data Plans for PACIFIC’s • N/A • N/A Employees Exclusivity • N/A • N/A • Legal: Goodwin • Legal: Latham

& Watkins Advisors • Auditor: PWC • Auditor: KPMG • Board Composition: 8-9 board members; 7 designated by ASHER and 1-2 designated by PACIFIC to be mutually agreed upon • Audit Status: Completed 2020/2021 PCAOB audits;

2022 audit expected to be completed July • Board Composition: 10 members; 9 designated by BOUNDLESS and 1 designated by PACIFIC Additional Information 2023 • Audit Status: 5 years of audited financials, including 2022 • Open to

licensing or divestiture of PACIFIC assets to parties with appropriate expertise and capabilities • Leaps by Bayer, RA Capital, Sectoral, Piper Heartland, ARCH Venture, Nextech Invest, Fidelity, • Third Rock Ventures, Wellington, RA

Capital, Invus Public Equities, Boxer Capital, Mission Bay Wellington, Boxer, Redmile, Surveyor, PFM, Vertex Ventures, Logos, City Hill, GT Healthcare Select Investors Capital, Janus Henderson, Logos, Marshall Wace, Y-Combinator Capital, Alexandria

Venture Investments Note: Bold indicates catalysts that could fall within the transaction window. Confidential 6

PROJECT PACIFIC INITIAL INDICATIONS OF INTEREST: HI-BIO | IMMPACT BIO

Transaction Structure • Reverse triangular merger • Reverse merger; proposing a simultaneous sign and close transaction • Sign definitive agreement and announce Transaction within 60 days of accepted proposal • Intends to

execute a definitive merger agreement within 45 days of signing term sheet and exclusivity agreement and Timing Financial: • HI-BIO: $325M (includes $22M cash at 03/31/23, excludes $30M from additional Series A • IMMPACT BIO: $257M

(includes $65M of cash expected at 06/30/23) closing in May 2023) Implied Valuation (1) • PACIFIC: $50M (based on $40M net cash at close + $10M for Nasdaq listing) • PACIFIC: $147M (based on $140M net cash at close + $7M for Nasdaq

listing) Post-$ Last Round / • HI-BIO’s post-money from last private round (Series A extension, November 2022): $217M • IMMPACT BIO’s post-money from last private round (Series B, January 2022): $257M • Step-up: 1.50x

• Step-up: 1.00x Step-up • (Excl. PIPE) HI-BIO: 68.9% / PACIFIC: 31.1% • (Excl. PIPE and share buyback) IMMPACT BIO: 63.1% / PACIFIC: 36.9% Implied Ownership Split • (Incl. PIPE) HI-BIO: 54.4-59.4% / PACIFIC: 24.6-26.9% /

PIPE: 13.7-20.9% • (Incl. PIPE and share buyback) IMMPACT BIO: 61.6% / PACIFIC: 12.0% / PIPE: 26.4% • $110M concurrent PIPE with support from existing investors for over $75M (term sheet signed with anchor investor); • $75-125

concurrent financing 30 additional investors in data room Concurrent Financing • Ongoing conversations with both new and existing investors regarding a potential financing • Concurrent share buyback of up to $100M • Pro forma cash

(incl. PIPE): $267-317M (HI-BIO: $52M, including ~$30M from the additional Pro Forma Cash and • Pro forma cash: $215M (IMMPACT: $65M; PACIFIC: $140M; PIPE: $110M; Share repurchase of $100M) Series A closing in May 2023; PACIFIC: $140M; PIPE:

$75-125M) • Runway: through early 2026 Runway • Runway: into 2026 • Felzartamab (Phase 2) – anti-CD38 antibody for primary membranous nephropathy (PMN), • IMPT-314 (Ph. 1) – CD19/CD20 bispecific CAR T cell therapy

for aggressive B-cell lymphoma (ABCL) immunoglobulin A nephropathy (IgAN), antibody-mediated rejection (AMR) and lupus • IMPT-514 (IND-enabling) – CD19/CD20 bispecific CAR T cell therapy for autoimmune diseases nephritis (LN) Key

Asset(s) • TGF-β platform (Discovery) – TGF-β in combination with a binder for IL13 receptor α2 (IL13Ra2) for glioblastoma • HIB210 (Phase 1) – anti-C5aR1 antibody for severe immune-mediated diseases (IMDs)

multiforme • Advanced discovery programs (Discovery) – directed against mast cells • IMPT-514 in r/r lupus nephritis – Mid 2023: IND clearance • IMPT-314 in ≥3L CAR-T naïve ABCL • Felzartamab –

2Q23: reproductive tox data • HIB210 in severe IMDs – 3Q24: Phase 1 first cohort data – 2H23: Phase 1 data • Felzartamab in PMN – 3Q23: Preclinical data supporting – 1Q25: EOP1 meeting – 4Q24: Phase 2

pivotal data – 2H23: Interim data from POC study in superiority to avacopan – 3Q25: Phase 2 pivotal data – 3Q25: Phase 2 pivotal data update aCD20-refractory population – 1H23: Phase 1 trial initiation in – 2Q26: BLA

submission – 1Q26: BLA submission – 1H24: Phase 3 initiation healthy volunteers • IMPT-514 in severe SLE with extrarenal disease • IMPT-314 in CAR-T experienced ABCL • Felzartamab in IgAN – 2Q23: Clinical POC

– 1Q24: NHP chronic tox study readout – 1Q24: IND amendment – 1Q24: Phase 1 data • Felzartamab in LN – 1H24: Subcutaneous formulation – 4Q24: Patient data – 2Q24: EOP1 meeting Timing of Key Milestones

– 2H23: Phase 1 initiation developments insights – 3Q26: BLA submission – 2H24: Phase 2 data update – 2H24: Clinical POC – 1H24: Phase 2 study initiation in • IMPT-514 in ANCA-associated vasculitis – 1H25:

BLA submission – 2024 and 2025: Phase 1b readouts ANCA-associated vasculitis (AAV) – 2Q24: IND amendment • IMPT-314 in 2L hematopoietic cell transplant (HCT) • Felzartamab in AMR – 1H24: Phase 1 readout in healthy

– 1H25: Patient data unintended ABCL – 1Q24: Clinical POC volunteers – 4Q26: BLA submission – 1Q25: Patient data – 1Q24: Phase 2 investigator sponsored • Advanced discovery programs – 2023: • IMPT-514

in secondary progressive MS – 1H26: BLA submission trial readout in AMR development candidate nomination – 3Q24: IND amendment • IMPT-314 – 1Q26: patient data in 2L HCT eligible ABCL – Mid 2025: Patient data –

4Q26: BLA submission Plans for PACIFIC’s • N/A • If specific PACIFIC employees fulfill open roles, they can be considered for combined company Employees • N/A • N/A Exclusivity • Financial: Jefferies •

Financial: Goldman Sachs • Legal: Cooley Advisors • Audit: Deloitte • Board Composition: Proportionate to the equity split and include combined company’s CEO (or as agreed upon in sign and close structure to not require vote

until post-close) • Board Composition: At least 1 director position designated by PACIFIC • Audit Status: 2 years of audited statements can be available within 3 months Additional Information • Audit Status: Completed AICPA audit

from inception to 12/31/22 • Proposes announcing PACIFIC share buyback upon announcement of transaction for up to $100M • May assign value to PACIFIC’s assets on case-by-case basis; open to PACIFIC monetizing assets prior to

transaction close • Bukwang Pharmaceutical, Decheng Capital, Foresite Capital Management, FutuRx, Hayan Health Networks, JJDC, • ARCH Venture Partners, Monograph Capital, Jeito Capital, MorphoSys JVC Investment Partners, Novartis Venture

Fund, OrbiMed, RM Global Partners, RMGLOBAL Healthcare Fund, Select Investors Surveyor Capital, Takeda Ventures, venBio (1): IMMPACT BIO plans to announce a share buyback upon announcement of the transaction for up to $100M to provide liquidity to

PACIFIC stockholders seeking to exit the transaction. Note: Bold indicates catalysts that could fall within the transaction window. Confidential 7

PROJECT PACIFIC INITIAL INDICATIONS OF INTEREST: PIPELINE THERAPEUTICS

| Q32 BIO Transaction Structure • Reverse triangular merger • Reverse triangular merger • Due diligence could be completed by both parties in 45 days and Timing • Q32: $250M (includes $31M cash at 03/31/23, excl. upcoming

payment of $22.5M from Horizon by the • PIPELINE: $310M (includes $130M cash expected at 06/30/23) Implied Valuation end of 3Q23 and $25M debt facility, of which $5M will be used to refinance debt with SVB) • PACIFIC: $155M (based on

$140M net cash at close + $15M for Nasdaq listing) • PACIFIC: $155M (based on $140M net cash at close + $15M for Nasdaq listing) • Q32’s post-money from last private round (Convertible note, 2022; post-$ assumes conversion of the

Post-$ Last Round / • PIPELINE’s post-money from last private round (Series C, April 2023): $310M note at Series B price and 5% interest): $185M, including current option pool • Step-up: 1.00x Step-up • Step-up: 1.35x •

(Excl. PIPE) PIPELINE: 66.7% / PACIFIC: 33.3% • (Excl. PIPE) Q32: 61.7% / PACIFIC: 38.3% Implied Ownership Split • No planned financing concurrent with the transaction, however, PIPELINE is in discussions to extend • Not required

but open to exploring concurrent PIPE Series C by $25-50M, which would increase post-money for Series C and valuation for proposed • Existing shareholders have signed a letter committing at least $30M to a PIPE, which could be used to

Concurrent Financing transaction accordingly extend runway or return a portion of PACIFIC cash to shareholders • Pro forma cash: $213.5M (Q32: $73.5M, based on 1Q23 cash, $22.5M from Horizon and $20M of new Pro Forma Cash and • Pro forma

cash: $270M (PIPELINE: $130M; PACIFIC: $140M) debt; PACIFIC: $140M) • Runway: through 2027, not including potential milestones payments from Janssen related to PIPE-307 Runway • Runway: into 2H 2026 • ADX-097 (Phase 1) –

C3d-mAb fH complement inhibitor for multiple complement-mediated diseases 1-5 • PIPE-791 (IND-enabling) – LPA1 antagonist for multiple sclerosis (MS) and neuroinflammation of the kidney and IgG4 • PIPE-307 (Phase 1 complete)

– oral M1 antagonist for MS and major depressive disorder (MDD) • ADX-096 (Preclinical) – C3d-mAb CR1 complement inhibitor for complement-mediated diseases 1-10 – Entered into a global license and development agreement with

Janssen in April 2023 for $50M • Novel nanobodies (Discovery) – C3d-fab fH/CR1 complement inhibitors and next-gen targeted Key Asset(s) upfront plus $1B milestones and tiered double-digit royalties as well as $25M equity investment

complement inhibitors for neuromuscular and neurodegenerative diseases from JJDC • ADX-914 (Phase 2) – IL-7/TSLP receptor mAb for atopic dermatitis (collaboration and option deal with – PIPELINE retained ability to develop in r/r