UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

PROXY

STATEMENT PURSUANT TO SECTION 14(a) OF THE

SECURITIES EXCHANGE ACT OF 1934

Filed by the Registrant ☒

Filed by a party

other than the Registrant ☐

Check the appropriate box:

| ☐ |

Preliminary Proxy Statement |

| ☐ |

Confidential, for Use of the Commission Only (as permitted by

Rule 14a-6(e)(2)) |

| ☐ |

Definitive Proxy Statement |

| ☒ |

Definitive Additional Materials |

| ☐ |

Soliciting Material Pursuant to §240.14a-12 |

Forte Biosciences, Inc.

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| ☐ |

Fee paid previously with preliminary materials. |

| ☐ |

Fee computed on table in exhibit required by Item 25(b) per Exchange Act Rules

14a-6(i)(1) and 0- |

In connection with the 2023 Annual Meeting of Stockholders (as it may be adjourned or

postponed from time to time), to be held on Tuesday, September 19, 2023 at 10:00 a.m., Pacific Time, Forte Biosciences, Inc. issued an investor presentation (the “Investor Presentation”) on September 1, 2023. A copy of the

Investor Presentation can be found below:

FORTE BIOSCIENCES CORPORATE OVERVIEW PRESENTATION SEPT 1, 2023

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS ¡ Certain

statements contained in this presentation regarding matters that are not historical facts, are forward-looking statements within the meaning of Section 21E of the Securities and Exchange Act of 1934, as amended, and the Private Securities Litigation

Act of 1995, known as the PSLRA. These include statements regarding management’s intention, plans, beliefs, expectations or forecasts for the future, and, therefore, you are cautioned not to place undue reliance on them. No forward-looking

statement can be guaranteed, and actual results may differ materially from those projected. Forte Biosciences, Inc. (“we”, the “Company” or “Forte”) undertakes no obligation to publicly update any forward-looking

statement, whether as a result of new information, future events or otherwise, except to the extent required by law. We use words such as “anticipates,” “believes,” “plans,” “expects,”

“projects,” “intends,” “may,” “will,” “should,” “could,” “estimates,” “predicts,” “potential,” “continue,”

“guidance,” and similar expressions to identify these forward-looking statements that are intended to be covered by the safe-harbor provisions of the PSLRA. ¡ Such forward-looking statements are based on our expectations and involve

risks and uncertainties; consequently, actual results may differ materially from those expressed or implied in the statements due to a number of factors, including, but not limited to, risks relating to the business and prospects of the Company;

Forte’s plans to develop and potentially commercialize its product candidates, including FB-102; the risk that results from early-preclinical studies may not be predictive of results from later-stage studies or clinical trials; the timing of

initiation of Forte’s planned clinical trials; the timing of the availability of data from Forte’s clinical trials; the timing of any planned investigational new drug application or new drug application; Forte’s plans to research,

develop and commercialize its current and future product candidates; Forte’s projections of the size of the market for FB-102; Forte’s ability to successfully enter into collaborations, and to fulfill its obligations under any such

collaboration agreements; the clinical utility, potential benefits and market acceptance of Forte’s product candidates; Forte’s commercialization, marketing and manufacturing capabilities and strategy; developments and projections

relating to Forte’s competitors and its industry; the impact of government laws and regulations; Forte’s ability to protect its intellectual property position; Forte’s estimates regarding future revenue, expenses, capital

requirements and need for additional financing; and the impact of global events on the Company, the Company’s industry or the economy generally. ¡ We have based these forward-looking statements largely on our current expectations and

projections about future events and trends that we believe may affect our financial condition, results of operations, business strategy and financial needs, and these statements represent our views as of the date of this presentation. We may not

actually achieve the plans, intentions or expectations disclosed in these forward-looking statements, and you should not place undue reliance on these forward-looking statements. Forward-looking statements are inherently subject to risks and

uncertainties, some of which cannot be predicted or quantified. Information regarding certain risks, uncertainties and assumptions may be found in our filings with the Securities and Exchange Commission, including under the caption “Risk

Factors” and elsewhere in our Annual Report on Form 10-K for the year ending December 31, 2022 and subsequent filings with the Securities and Exchange Commission. New risk factors emerge from time to time and it is not possible for our

management team to predict all risk factors or assess the impact of all factors on the business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in, or implied by, any

forward-looking 2 statements. While we may elect to update these forward-looking statements at some point in the future, we specifically disclaim any obligation to do so. These forward-looking statements should not be relied upon as representing our

views as of any date subsequent to the date of this presentation.

¡ About Forte: Forte Biosciences, Inc. (NASDAQ: FBRX)

(“Forte” or the “Company”) is a biopharmaceutical company that is advancing its product candidate, FB-102, which is a proprietary molecule with potentially broad autoimmune applications including in such indications as

graft-versus-host disease, vitiligo and alopecia areata. ¡ Important Additional Information and Where to Find It: Forte has filed a definitive proxy statement (the “Proxy Statement”) and other documents with the U.S. Securities and

Exchange Commission (the “SEC) in connection with its solicitation of proxies from stockholders in respect of the 2023 Annual Meeting of Stockholders to be held on September 19, 2023 (the “2023 Annual Meeting”). BEFORE MAKING ANY

VOTING DECISION, INVESTORS AND SECURITY HOLDERS ARE URGED TO READ ALL RELEVANT DOCUMENTS, INCLUDING FORTE’S PROXY STATEMENT AND ANY AMENDMENTS AND SUPPLEMENTS THERETO AND THE ACCOMPANYING BLUE PROXY CARD, FILED WITH THE SEC WHEN THEY BECOME

AVAILABLE BECAUSE THEY CONTAIN, OR WILL CONTAIN, IMPORTANT INFORMATION ABOUT FORTE. Stockholders may obtain free copies of the Proxy Statement and other relevant documents that Forte files with the SEC and on Forte’s website at

https://www.fortebiorx.com or from the SEC’s website at http://www.sec.gov. ¡ Participants to the Solicitation: Forte, its directors and executive officers and other members of management and employees may be deemed to be participants in

the solicitation of proxies with respect to a solicitation by Forte in connection with matters to be considered at the 2023 Annual Meeting. Information about Forte’s executive officers and directors, including information regarding the direct

and indirect interests, by security holdings or otherwise, is available in the Proxy Statement for the 2023 Annual Meeting, which was filed with the SEC on August 24, 2023. To the extent holdings of Forte securities reported in the Proxy Statement

for the 2023 Annual Meeting have changed, such changes have been or will be reflected on Statements of Change in Ownership on Forms 3, 4 or 5 filed with the SEC. These documents are or will be available free of charge at the SEC’s website at

www.sec.gov. 3

WHAT IS THIS PROXY ABOUT? Camac is attempting to co-opt cash from Forte

which we believe destroys value for shareholders. Forte and our investors believe that FB-102, our lead development compound, has the potential to create significant value for stockholders as validated by $25 m investment by leading healthcare

investment funds in early August. Camac is nominating 2 directors to the Forte board, Mr. Hacke and Mr. McIntyre, who are not qualified as they have no biotechnology/drug development experience, no science or medical background and have never served

on the board of a public company. The Forte nominees. Dr. Paul Wagner and Dr. Lawrence Eichenfield, are highly qualified with 4 deep biotechnology and drug development experience

CAMAC LIQUIDATION DEMANDS WILL DESTROY VALUE FOR SHAREHOLDERS From Camac

Proxy On March 9, 2023, Camac's counsel again had a telephone call with the Company's counsel in an attempt to reach a mutually agreeable resolution. Through its counsel, Camac suggested multiple potential frameworks to reach an agreement, including

options where one director candidate would be appointed to the Board with one incumbent director resigning, the formation of a committee to explore strategic alternatives and the Company agreeing to immediately return $25.3 million of capital, or

alternatively, two new director candidates being appointed to the Board and two incumbent directors resigning.“ • As of the end of March the Company has ~$36 m in cash and were utilizing ~$6.7 m per quarter. By co-opting $25.3 m in cash

the Company would have been left with just over 1 quarter of cash and could not have continued options (would be liquidated) From Camac August 17, 2022 Press release: “Urges the Board to Reverse Course and Return Capital to Long-Suffering

Shareholders – or Risk Facing Action from Camac” “…the Board should promptly announce a plan to return capital to shareholders. 5

WHAT DOES FORTE BIOSCIENCES DO? Forte is a biotechnology company developing

FB-102 to help quiet down key cells in the immune system to keep them from attacking healthy tissue We are developing FB-102 for treating diseases like graft-versus-host disease (GvHD) • Acute graft-versus-host-disease (aGvHD) has a 70%

mortality rate in 2 years (grade 3 and 4). • Acute graft-versus-host-disease is a high unmet medical need with only one drug approved that shows moderate activity and potential significant toxicity ruxolitinib (Jakafi) • FB-102 has

beaten ruxolitinib (Jakafi) head to head in validated animal models • The market opportunity in GvHD is greater than $1 billion Mechanism of FB-102 also shows activity in vitiligo and alopecia areata (diseases where the immune system attacks

skin pigmentation cells and hair follicles respectively) • $6 billion potential market with limited treatment options 6

BIOTECHNOLOGY SECTOR DYNAMICS Drug development is very challenging with a

~10% probability of success from preclinical through commercialization. As a result, it is common in the biotechnology sector to have drugs in development fail and then to move forward with other development candidates to create value 90% of drugs

tested in biotech companies fail. A failure of a molecule in development is not a failure of management. Healthcare and biotechnology investors are accustomed to this cycle of lead drug failures and refocusing on pipeline candidates. In fact many

view this cycle as significant opportunities for investment during the transition. 7

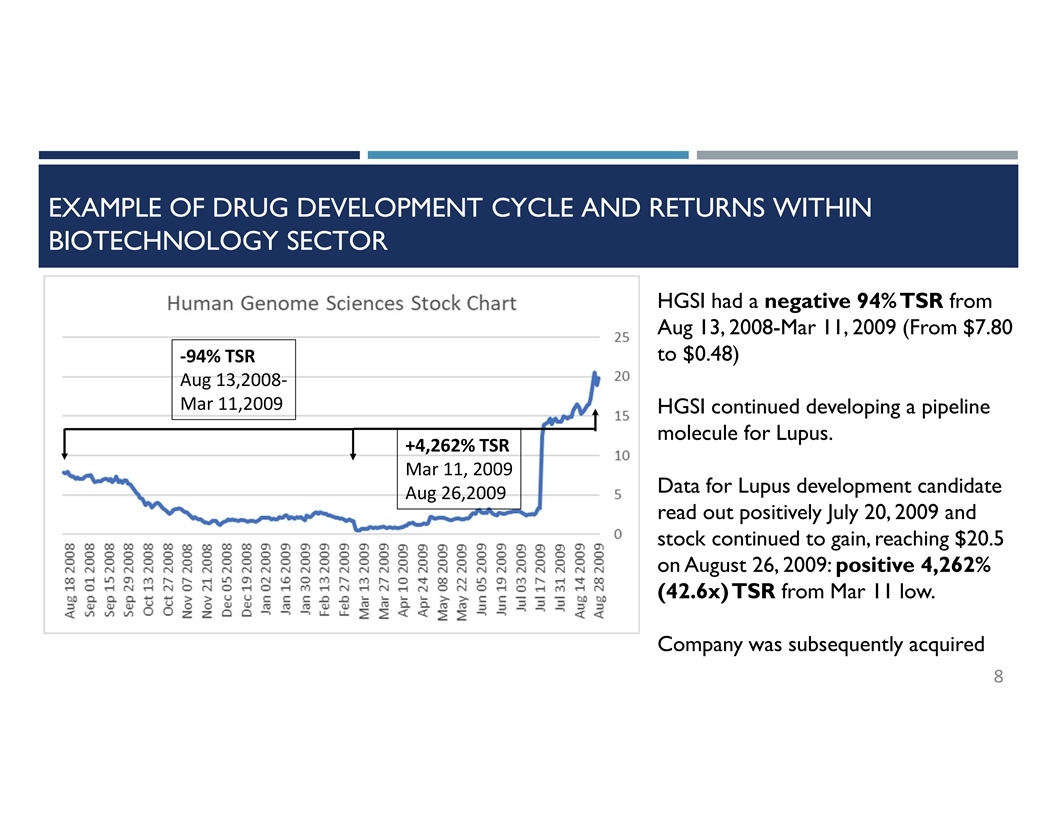

EXAMPLE OF DRUG DEVELOPMENT CYCLE AND RETURNS WITHIN BIOTECHNOLOGY SECTOR

HGSI had a negative 94% TSR from Aug 13, 2008-Mar 11, 2009 (From $7.80 to $0.48) -94% TSR Aug 13,2008- Mar 11,2009 HGSI continued developing a pipeline molecule for Lupus. +4,262% TSR Mar 11, 2009 Data for Lupus development candidate Aug 26,2009

read out positively July 20, 2009 and stock continued to gain, reaching $20.5 on August 26, 2009: positive 4,262% (42.6x) TSR from Mar 11 low. Company was subsequently acquired 8

FORTE TIMELINE • June 2020 Forte went public through a reverse merger

with Tocagen • Lead program FB-401, in-licensed from NIH, was focused on autoimmune skin disease (atopic dermatitis) • Sept 2021 Forte ran robust phase 2 study for FB-401 and announced negative outcome • Following the phase 2

FB-401 failure • Company ran a reverse merger process (150 companies initially, down to 5 finalists) • Assessed liquidation • Reviewed in-licensing options • Evaluation internal candidate, FB-102 • May 2022 after

thorough assessment of options announced plan to advance FB-102 in autoimmune indications • Strengthened team by adding Chief Scientific Officer with translational medicine and drug approval experience • Added new board members with

development and scientific expertise to further support FB-102 development • July 2022 Camac makes first acquisition of Forte common stock 9 • August 2023 Company announced key new data for FB-102 and on basis of solid data, top-tier

institutional healthcare funds invested $25 m, validating the significant value creation potential for FB-102

FORTE TIMELINE Forte announces key R&D updates for FB-102 and on based

of strong data, top-tier healthcare Forte institutional funds invested $25 m completes Company and board review including: reverse merger reverse merger, in-licensing and Alger with Tocagen internal compound, FB-102 and BVF to become announces

advancement of FB-102 Farallon publicly listed Lead candidate Perceptive company in FB-401 fails in Camac buys shares Tybourne June 2020 phase 2 development Stock is up ~30% in aftermarket following announcement until Camac dumps shares (500k) 10

including in illiquid aftermarket to negatively impact performance

ON THE BASIS OF STRONGLY VALIDATING DATA AND LARGE MARKET OPPORTUNITY,

SIGNIFICANT INSTITUTIONAL FUNDS INVESTED $25 MILLION AT THE BEGINNING OF AUGUST $25 m invested from Alger, BVF Partners, Farallon Capital Management, Perceptive Advisors and Tybourne Capital Management validating significant value creation potential

for FB-102 Investment included $1.2 m from management and the board, underscoring our belief in FB-102 value creation potential Offering had no discount to market price and no dilutive warrant coverage which speaks to the strength that offering in

the current challenging market facing biotechnology 11 companies.

FORTE TRANSACTION FAVORABLE VS COMPARABLE RECENT BIOTECH TRANSACTIONS Stock

price vs CPS in Company Name Gossamer Evelo Biosciences Forte Biosciences range of comparable Ticker GOSS EVLO FBRX biotech companies Cash per Share (Last 10Q/K prior to transaction) $2.13 $8.72 $1.71 Stock Price Ave (5 day prior to transaction

date) $1.60 $2.87 $1.01 that conducted recent Pre-transaction Stock discount to CPS 25% 67% 41% transactions Transaction announced 20-Jul-23 10-Jul-23 1-Aug-23 Size of transactions vs Amount raised ($ m) $212 $25.5 $25 market cap less vs Market cap

(5 day prior to transaction date) ($ m) $143 $15.7 $21.2 comparable biotech Raise amount vs market cap 149% 162% 118% transaction Terms FBRX transaction had Price per share of transactoin $1.63 $2.19 $1.01 no discount to stock Share price day before

announcement $1.82 $2.31 $1.01 price day before Discount of transaction price to day prior announcement 10% 5% 0% Warrant coverage 25% transaction and no 12 dilutive warrant coverage

FORTE MANAGEMENT – NEARLY 140 YEARS OF COMBINED EXPERIENCE

Forte’s management has 140 years of combined experience in manufacturing, quality, regulatory and clinical development Paul Wagner, Ph.D., CFA – Chief Executive Officer Tony Riley, MBA – Chief Financial Officer • 24 years of

experience in the biotechnology industry • 30 years of experience 15 in the life sciences industry • Institutional Investor recognized Biotechnology • CFO at Krystal Biotechnology Analyst at Lehman Brothers (now Barclays)•

Founding Partner of CFO Network • Head of Development Licensing at Protein Design • Acting CFO Avanex Labs• Corporate Controller at Kosan • Portfolio Manager of Biotechnology Investment Fund • MBA from University of

Chicago at Allianz Global Investors Chris Roenfeldt – Chief Operating Officer • Chief Financial Officer at Pfenex (biotech arm of • 22 years of experience in the biotechnology industry Dow) • Project and alliance management

at Halozyme • Head of Corporate Strategy and Development at • Head of project management at Pfenex CANBridge • CMC project management at Amgen • Founder and CEO of Forte Biosciences • Project management at Genentech

• Ph.D in Chemistry from Caltech • BS in Chemical Engineering from University of Co 1l3 orado • CFA Charterholder

FORTE MANAGEMENT – NEARLY 140 YEARS OF COMBINED EXPERIENCE

Forte’s management has 140 years of combined experience in manufacturing, quality, regulatory and clinical development Hubert Chen, MD – Chief Scientific Officer Steven Ruhl – Chief Technical Officer • 20 years of experience

in the biotechnology industry • 43 years of experience in the biotechnology industry • Chief Medical Officer at Metacrine • Head of downstream processing for warp speed • Chief Scientific and Medical Officer at Pfenex COVID

antibody at ThermoFisher • Led NDA/MAA approval of teriparatide • Director of Technical and Commercial Supply at injectable protein for osteoporosis IDEC Pharmaceuticals • VP of clinical development at Aileron • Commercial

Drug Product Exec Director – Amgen • VP of translational medicine at Regulus • Site Head Amgen Ireland manufacturing facility • Sr. director of clinical development at Amylin • BS in microbiology and chemistry from BYU

• MD from Columbia University • Medical training at UCSF and Massachusetts General 14

STRONG INDEPENDENT BOARD COMPRISED OF LEADERS IN THE BIOTECHNOLOGY AND

PHARMACEUTICAL INDUSTRY • Steven Kornfeld: Represents investor perspective and interest having previously led healthcare investments for Franklin Templeton • Scott Brun, MD: Headed product development and venture investments for Abbvie.

Serves on 2 public company boards. • David Gryska: Chief Financial Officer (CFO) at Incyte and Celgene. Served on 6 public company board, including at Seattle Genetics into its acquisition by Pfizer. • Barb Finck, MD: Former Chief

Medical Officer (CMO) at Coherus and led the clinical development of Enbrel (over $4 billion revenue). Serves on board of private biotechnology company. Led clinical development at numerous biotechnology companies Board certified in rheumatology and

internal medicine. 15

STRONG INDEPENDENT BOARD COMPRISED OF LEADERS IN THE BIOTECHNOLOGY AND

PHARMACEUTICAL INDUSTRY • Steve Doberstein, PhD: Former Chief Scientific Officer (CSO) at leading biotechnology company (Nektar). Led R&D at 4 other biotechnology companies. Expert in cell biology and immunology. • Donald Williams:

Former Ernst and Young Partner and Grant Thornton Partner. Serves on 4 public company boards. • Dr. Lawrence Eichenfield. MD: Vice Chairperson of Dermatology Department at UC-San Diego. Prominent key opinion leader in dermatology (including

vitiligo where FB-102 is being developed). • Dr. Paul Wagner, Ph.D: CEO of the Company and has held several senior leadership roles in the biotechnology industry, has been an Institutional Investor recognized biotechnology analyst and has been

a portfolio manager for a biotechnology investment fund. Moreover, Dr. Wagner has extensive scientific knowledge due to his education and work background. 16

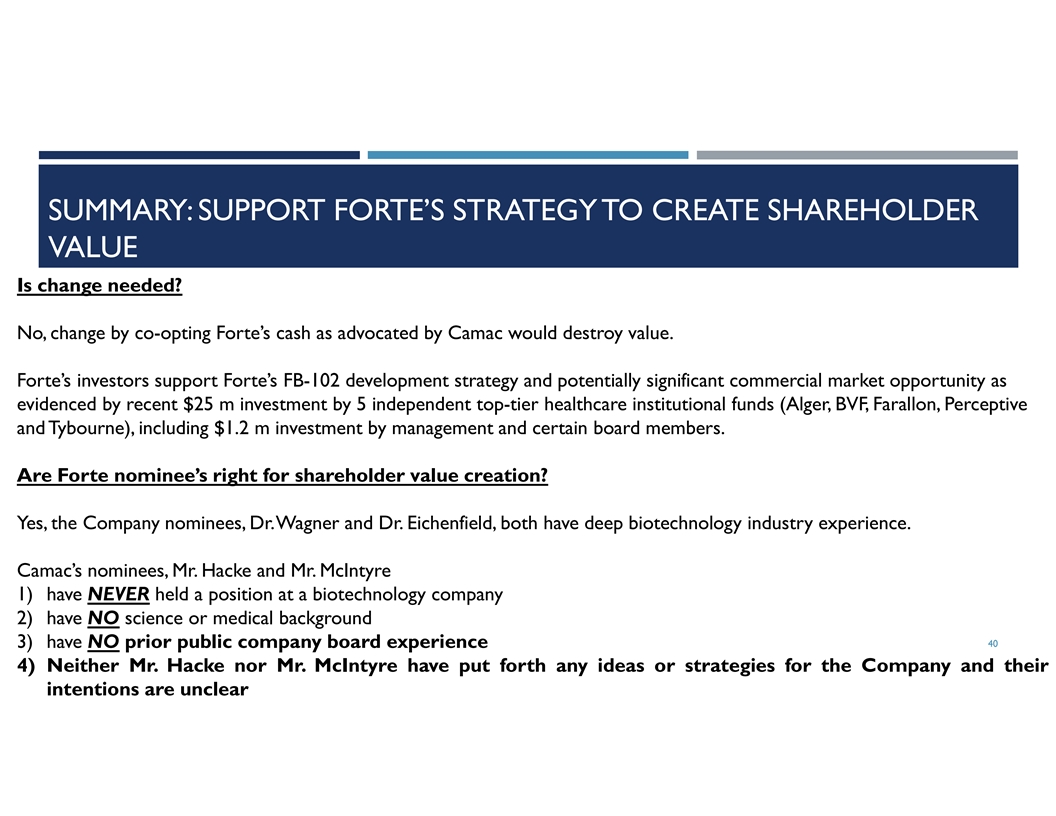

SUMMARY: SUPPORT FORTE’S STRATEGY TO CREATE SHAREHOLDER VALUE Is

change needed? No, change by co-opting Forte’s cash as advocated by Camac would destroy value. Forte’s investors support Forte’s FB-102 development strategy and potentially significant commercial market opportunity as evidenced by

recent $25 m investment by 5 independent top-tier healthcare institutional funds (Alger, BVF, Farallon, Perceptive and Tybourne), including $1.2 m from the management team and certain board members. Are Forte nominee’s right for shareholder

value creation? Yes, the Company nominees, Dr.Wagner and Dr. Eichenfield, both have deep biotechnology industry experience. Camac’s nominees, Mr. Hacke and Mr. McIntyre 1) have NEVER held a position at a biotechnology company 2) have NO

science or medical background 17 3) have NO prior public company board experience 4) Neither Mr. Hacke nor Mr. McIntyre have put forth any ideas or strategies for the Company and their intentions are unclear

CAMAC’S ATTEMPTS TO CO-OPT COMPANY CASH DESTROYS VALUE FOR

STOCKHOLDERS

CAMAC ATTEMPTING TO SUBVERT SHAREHOLDERS’ RIGHT TO VOTE Camac is

actively attempting to prevent new investors from being able to vote in order to subvert the voting rights of the majority of the Forte ownership. •Camac’s meritless lawsuit fails to allege any facts to support the claims of that the

Board of Directors of Forte breached its fiduciaries duties in approving the $25 million financing in an arms-length transaction with bona fide third party institutional investors. •Camac’s motion to expedite a preliminary injunction

hearing was denied by the Court of Chancery in the State of Delaware •The Court ordered the parties to confer to schedule Forte’s motions to dismiss In attempting to subvert shareholders’ right to vote, Camac’s self-serving

purpose is to co- opt the cash for a value potentially below the current share price and destroy value for the 19 majority of stockholders.

CAMAC ATTEMPTING TO SUBVERT SHAREHOLDERS’ RIGHT TO VOTE Additionally,

Camac has stated that they will demand other Forte stockholders foot the bill for its self-serving campaign by seeking recovery from the Company of its expenses, which Camac has indicated will be in excess of $750,000 and growing, yet another

wasteful and unnecessary expenditure of stockholder resources To highlight Camac’s self-serving purposes, following the Company announcement of the financing and R&D update after the market closed on August 1, Forte’s stock price was

significantly outperforming – However, Camac then aggressively sold nearly 500,000 shares, including in the illiquid aftermarket, opportunistically driving down the share price, calling into question Camac’s intentions. Additionally,

Camac’s partner, ATG sold calls on Forte’s stock and has a direct interest in keeping the stock from outperforming to prevent their effective short position from losing them money. 20

CAMAC GROUP’S SELF-SERVING AND SHORT-SIGHTED CAMPAIGN IS AN ATTEMPT

TO CO-OPT THE COMPANY’S CASH AND DESTROY POTENTIAL FUTURE VALUE FROM STOCKHOLDERS Camac Group’s self-serving and short-sighted campaign is an attempt to co-opt the Company’s cash and destroy potential future value from

stockholders. • Camac only purchased shares AFTER the Company announced its FB-102 strategy with full knowledge of the FB-102 strategy and purchased shares after obtaining that information because they believe they can agitate their way to a

liquidation of the company. • To be clear Forte believes it is a not in the interest of shareholders to destroy value by liquidating the company for the benefit of a minority of opportunistic 13D filers. • The future liquidation value,

including expenses, could be below the current share price and destroys stockholder value. 21

IN SPITE OF CAMAC’S SELF-SERVING EFFORTS THE COMPANY’S COUNSEL

MADE GOOD FAITH EFFORTS TO COME TO AGREEMENT WITH CAMAC In spite of Camac’s self-serving efforts to co-opt the company cash and destroy stockholder value, the Company’s counsel made good faith efforts to come to agreement with Camac.

§ On March 9, 2023, Forte’s counsel again engaged with Camac Fund’s counsel to explore various avenues to a negotiated resolutions that would avoid a costly and distracting proxy fight. However, counsel for Camac Fund indicated that

their client was not open to any negotiated solution that did not include a complete shift of operational focus and depleting the Company’s cash reserves to fund a large share repurchase program.” § On August 7, 2023 and August 8,

2023, Forte’s counsel engaged with Camac Fund’s counsel to explore various avenues to a negotiated resolution that would avoid a proxy fight and litigation threatened by Camac Fund against Forte. However, following 22 discussions,

counsel for Camac Fund indicated that their client was no longer interested in pursuing discussions with respect to a negotiated resolution.

FB-102 PROGRAM OVERVIEW

FB-102 OVERVIEW + • FB-102 (Forte’s anti-CD122 antibody) is

designed to quiet down key immune cells (NK and CD 8 T cells) that are responsible for attacking healthy tissue • FB-102 has demonstrated significant preclinical activity in validated graft versus host (GvHD) studies, beating the standard of

care drug for GvHD, Jakafi, in head-to-head studies • Expect FB-102 to be in the clinic in early 2024 • We believe FB-102 has demonstrated potentially best-in-class activity for the treatment of GvHD and addresses a significant unmet

need that could allow for abbreviated development path • Mechanism of FB-102 also shows activity in vitiligo and alopecia areata (diseases where the immune system attacks skin pigmentation cells and hair follicles respectively) 24 •

FB-102 has significant immediate and long term value based on recent acquisitions (Villaris and Kadmon)

INCYTE PURCHASES VILLARIS THERAPEUTICS AND AUREMOLIMAB (ANTI CD-122

ANTIBODY) FOR $70M UPFRONT AND UP TO $1.36B IN POTENTIAL MILESTONES • Villaris developed a preclinical CD-122 antibody (same target as FB-102) • Acquired by Incyte for $70 m upfront and $1.4 billion in milestones We see this deal as

potentially strengthening INCY's vitiligo franchise and incrementally • FB-102 is more advanced than Villaris was adding to efforts to offset JAKAFI's LOE later in the decade. – Mizuho Securities when it was acquired, highlighting

significant The acquisition makes sense to us given INCY’s increasing pipeline focus on current value in FB-102 program. dermatology – Guggenheim This acquisition complements INCY's transition to a dermatology-focused company as oral

Jakafi approaches loss of exclusivity and topical JAK agents assume a greater Payment strategic role. – SVB securities Upfront Payment $70 M This deal fits in well with management's recent comments on BD to seek early, high Development and

regulatory milestones $310 M science assets in derm, and auremolimab's potentially durable mechanism of action Commercial milestones on net sales of the product $1,050 M could nicely complement Incyte's existing vitiligo portfolio. - Cowen 25

Potential Total $1,430 M

KADMON PURCHASED BY SANOFI FOR $1.9B FOR GVHD DRUG Sanofi acquired Kadmon

for $1.9 Billion for their GvHD drug highlighting value creating potential for FB-102. 26

GRAFT VS HOST DISEASE

GRAFT VS HOST DISEASE (GVHD): A SERIOUS COMPLICATION OF ALLOGENEIC STEM

CELL TRANSPLANTATION – HIGH UNMET NEED AND BILLION DOLLAR MARKET POTENTIAL Cause: donor immune cells attack host tissues Classification Acute (~5K US prevalence - NIH) - Occurs in up to 50% of recipients. - Onset typically within 3 months of

transplant - Usually combination or organs involved: skin (rash), GI tract (vomiting, diarrhea), liver (jaundice) Chronic (~14K US prevalence - NIH) - Develops in up to 40% of recipients. - In addition to skin, GI tract and liver, may involve lungs,

mucosal surfaces (eyes, mouth, GU tract), muscle, joints (connective tissue) 28 https://www.lls.org/booklet/graft-versus-host-disease

ACUTE GVHD: TREATMENT PARADIGM AND DEVELOPMENT PIPELINE • Only one

approved drug for steroid resistant GvHD, Jakafi, and it has significant toxicity and modest activity • High unmet medical need in billion dollar GvHD market for safer more effective treatments 29

https://www.lls.org/booklet/graft-versus-host-disease https://www.jakafi.com/pdf/prescribing-information.pdf

APPROVAL OF RUXOLITINIB (JAKAFI) IN ACUTE GVHD WAS BASED ON THE RESULTS

FROM AN OPEN-LABEL, SINGLE-ARM STUDY • Jakafi was approved based on single arm study and showed a modest 57% response rate and only 30% complete response Efficacy is based on Day 28 overall response rate as defined by CIBMTR criteria. •

Potential for small open label trial for approval given high unmet need could mean faster and less expensive https://www.jakafi.com/pdf/prescribing-information.pdf development of FB-102 30

LARGE UNMET NEED IN VITILIGO AND ALOPECIA AREATA (COMBINED $6 BILLION

MARKET BY 2026) Vitiligo Vitiligo is an autoimmune disease of the skin mediated primarily by NK and CD8+ T cells that kill melanocytes and create white spots. In the US there are approximately 2 m people with vitiligo. The global vitiligo treatment

market size was valued at $1.2 billion in 2018 and is projected to reach $1.9 billion by 2026, exhibiting a CAGR of 5.8% (Fortune Business Insights) Alopecia Areata (AA) AA is an autoimmune disease in which immune cells attack and damage hair

follicles and is mediated primarily by CD8+ T cells and NK cells The global alopecia treatment market was valued at $2.7 billion in 2018, and is projected to reach $3.9 billion by 2026, registering a CAGR of 4.6% from 2019 to 2026 (Allied Mkt

Research) While JAK inhibitors have demonstrated efficacy in AA and vitiligo, regulatory scrutiny of the JAK 31 class including black box warnings has dampened enthusiasm for this class and as a result there remains a significant unmet need for safe

and effective therapies for treating AA and vitiligo

FB-102 IN GRAFT VS HOST DISEASE

DOSE-RANGING INVESTIGATION OF FB102 IN A HUMANIZED MOUSE MODEL OF ACUTE

GVHD: THERAPEUTIC MODE Irradiation & End of PBMC transplantation treatment Day 1 2 3 4 5 6 7 8 9 10 11 12 13 14 FB102 Once-daily IP administration Start dosing on Day 5, (75, 125, 175 mpk) once daily Vehicle Once-daily IP administration

Twice-daily oral administration Ruxolitinib Start dosing on Day 5, (60 mpk) twice daily Twice-daily oral administration Vehicle N=10 per cohort 33

FB102 SURVIVAL BENEFITS: FB-102 BEAT RUXOLITINIB HEAD-TO- HEAD Start of

daily treatment 1 1 1 1 10 0 0 0 00 0 0 0 0% % % % % FB102(75): 90% FB102(175): 90% 8 8 8 8 80 0 0 0 0% % % % % FB102(125): 80% 6 6 6 6 60 0 0 0 0% % % % % Ruxolitinib: 60% 4 4 4 4 40 0 0 0 0% % % % % 2 2 2 2 20 0 0 0 0% % % % % 0 0 0 0 0% % % % %

Vehicle: 0% 1 1 1 1 1 3 3 3 3 3 5 5 5 5 5 7 7 7 7 7 9 9 9 9 9 1 1 1 1 11 1 1 1 1 1 1 1 1 13 3 3 3 3 1 1 1 1 15 5 5 5 5 Study day 34 P=0.0001 for FB102 (75, 175) vs Vehicle on Day 14 P=0.0007 for FB102 (125) vs Vehicle on Day 14 P=0.01 for

Ruxolitinib vs Vehicle on Day 14

MONO VS COMBINATION THERAPIES WITH FB102, RUXOLITINIB OR CORTICOSTEROIDS

Irradiation & End of study PBMC injection (D18) Day 1 5 8 12 15 18 Ruxolitinib Twice-daily oral (60 mpk) FB102+Ruxolitinib Once-daily IP + twice-daily oral (75 mpk+60 mpk) Placebo Once-daily IP + twice-daily oral (Combination of vehicles) N=10

per cohort 35

FB102 SURVIVAL BENEFITS: FB-102 COMBINATION WITH RUXOLITINIB SIGNIFICANTLY

SUPERIOR VS RUXOLITINIB Start of daily treatment 100% 1 10 00 0% % FB102+Rux: 90% 80% 8 80 0% % 6 6 60 0 0% % % 4 4 40 0 0% % % Ruxolitinib: 30% 2 2 20 0 0% % % Vehicle: 0% 0 0 0% % % 1 1 1 3 3 3 5 5 5 7 7 7 9 9 9 1 1 11 1 1 1 1 13 3 3 1 1 15 5 5 1

1 17 7 7 Study day 36 P=0.0001 for FB102+Rux vs Vehicle on Day 18 P=0.02 for FB102+Rux vs Ruxolitinib Mono on Day 18

TRANSLATION OF HUMANIZED ACUTE GVHD MOUSE FINDINGS INTO PATIENT RESPONSE:

PROMISING FB102 RESULTS Magnitude of FB102 preclinical efficacy correlates with positive clinical response. Preclinical Data Indication/ Clinical Data Company Candidate Mechanism (survival in humanized Phase (Day 28 ORR) GVHD model)

Second/Third-line Forte Biosciences FB102 Anti-CD122 90% (vs 0% for control) TBD Preclinical Second-line 1 4 Incyte Ruxolitinib JAK 1/2 inhibition 90% (vs 0% for control) 62% Commercial First-line 2 5 Equillium/Ono Itolizumab Anti-CD6 50% (vs 10%

for control) >50% Phase 3 First-line 3 Incyte Itacitinib JAK 1 inhibition 20% (vs 0% for control) N.S. vs PBO Terminated 1. Huarte E et al. Immunotherapy. 2021;13:977. 2. Ng CT et al. Blood. 2019;134 (Supp 1):5063. 3. Courtois J et al. Bone

Marrow Transplant. 2021;56:2672. Day 60 results shown. 4. Zeiser R et al. N Engl J Med. 2020;382:1800. 37 5. Equillium Corporate Presentation, September 2022. 6. Zeiser R et al. Lancet Haematol. 2022;9:e14.

CAMAC’S ATTMEPTS TO CO-OPT COMPANY CASH DESTROYS VALUE FOR

STOCKHOLDERS

WHAT IS THIS PROXY ABOUT? Camac is attempting to co-opt cash from Forte

which we believe destroys value for shareholders. Forte and our investors believe that FB-102, our lead development compound, has the potential to create significant value for stockholders as validated by $25 m investment by leading healthcare

investment funds in early August. Camac is nominating 2 directors to the Forte board, Mr. Hacke and Mr. McIntyre, who are not qualified as they have no biotechnology/drug development experience, no science or medical background and have never served

on the board of a public company. The Forte nominees. Dr. Paul Wagner and Dr. Lawrence Eichenfield, are highly qualified with 39 deep biotechnology and drug development experience

SUMMARY: SUPPORT FORTE’S STRATEGY TO CREATE SHAREHOLDER VALUE Is

change needed? No, change by co-opting Forte’s cash as advocated by Camac would destroy value. Forte’s investors support Forte’s FB-102 development strategy and potentially significant commercial market opportunity as evidenced by

recent $25 m investment by 5 independent top-tier healthcare institutional funds (Alger, BVF, Farallon, Perceptive and Tybourne), including $1.2 m investment by management and certain board members. Are Forte nominee’s right for shareholder

value creation? Yes, the Company nominees, Dr.Wagner and Dr. Eichenfield, both have deep biotechnology industry experience. Camac’s nominees, Mr. Hacke and Mr. McIntyre 1) have NEVER held a position at a biotechnology company 2) have NO

science or medical background 40 3) have NO prior public company board experience 4) Neither Mr. Hacke nor Mr. McIntyre have put forth any ideas or strategies for the Company and their intentions are unclear

Forte Biosciences (NASDAQ:FBRX)

Historical Stock Chart

From Apr 2024 to May 2024

Forte Biosciences (NASDAQ:FBRX)

Historical Stock Chart

From May 2023 to May 2024