false

2024

Q1

--12-31

0001985840

0001985840

2024-01-01

2024-03-31

0001985840

2024-05-13

0001985840

2024-03-31

0001985840

2023-12-31

0001985840

defi:HashdexBitcoinETFMember

2024-03-31

0001985840

defi:HashdexBitcoinETFMember

2023-12-31

0001985840

defi:BitcoinMember

2024-03-31

0001985840

defi:CryptocurrencyMember

2024-03-31

0001985840

defi:MoneyMarketFundsFirstAmericanGovernmentObligationsFundClassXMember

2024-03-31

0001985840

us-gaap:CashEquivalentsMember

2024-03-31

0001985840

defi:CMEMicroBitcoinFuturesApril2024DerivativeAssetMember

2024-03-31

0001985840

defi:CryptocurrencyFuturesContractsDerivativeAssetMember

2024-03-31

0001985840

defi:CMEMicroBitcoinFuturesApril2024DerivativeLiabilityMember

2024-03-31

0001985840

defi:CryptocurrencyFuturesContractsDerivativeLiabilityMember

2024-03-31

0001985840

defi:MoneyMarketFundsUSBankDepositAccountMember

2023-12-31

0001985840

us-gaap:CashEquivalentsMember

2023-12-31

0001985840

defi:CMEMicroBitcoinFuturesJan2024DerivativeAssetMember

2023-12-31

0001985840

defi:CryptocurrencyFuturesContractsDerivativeAssetMember

2023-12-31

0001985840

defi:CMEMicroBitcoinFuturesFeb2024DerivativeLiabilityMember

2023-12-31

0001985840

defi:CryptocurrencyFuturesContractsDerivativeLiabilityMember

2023-12-31

0001985840

defi:HashdexBitcoinETFMember

defi:BitcoinMember

2024-03-31

0001985840

defi:HashdexBitcoinETFMember

defi:CryptocurrencyMember

2024-03-31

0001985840

defi:HashdexBitcoinETFMember

defi:MoneyMarketFundsFirstAmericanGovernmentObligationsFundClassXMember

2024-03-31

0001985840

defi:HashdexBitcoinETFMember

us-gaap:CashEquivalentsMember

2024-03-31

0001985840

defi:HashdexBitcoinETFMember

defi:CMEMicroBitcoinFuturesApril2024DerivativeAssetMember

2024-03-31

0001985840

defi:HashdexBitcoinETFMember

defi:CryptocurrencyFuturesContractsDerivativeAssetMember

2024-03-31

0001985840

defi:HashdexBitcoinETFMember

defi:CMEMicroBitcoinFuturesApril2024DerivativeLiabilityMember

2024-03-31

0001985840

defi:HashdexBitcoinETFMember

defi:CryptocurrencyFuturesContractsDerivativeLiabilityMember

2024-03-31

0001985840

defi:HashdexBitcoinETFMember

defi:MoneyMarketFundsUSBankDepositAccountMember

2023-12-31

0001985840

defi:HashdexBitcoinETFMember

us-gaap:CashEquivalentsMember

2023-12-31

0001985840

defi:HashdexBitcoinETFMember

defi:CMEMicroBitcoinFuturesJan2024DerivativeAssetMember

2023-12-31

0001985840

defi:HashdexBitcoinETFMember

defi:CryptocurrencyFuturesContractsDerivativeAssetMember

2023-12-31

0001985840

defi:HashdexBitcoinETFMember

defi:CMEMicroBitcoinFuturesFeb2024DerivativeLiabilityMember

2023-12-31

0001985840

defi:HashdexBitcoinETFMember

defi:CryptocurrencyFuturesContractsDerivativeLiabilityMember

2023-12-31

0001985840

2023-01-01

2023-03-31

0001985840

defi:HashdexBitcoinETFMember

2024-01-01

2024-03-31

0001985840

defi:HashdexBitcoinETFMember

2023-01-01

2023-03-31

0001985840

2022-12-31

0001985840

2023-03-31

0001985840

defi:HashdexBitcoinETFMember

2022-12-31

0001985840

defi:HashdexBitcoinETFMember

2023-03-31

0001985840

us-gaap:FairValueInputsLevel1Member

2024-03-31

0001985840

us-gaap:FairValueInputsLevel2Member

2024-03-31

0001985840

us-gaap:FairValueInputsLevel3Member

2024-03-31

0001985840

us-gaap:FairValueInputsLevel1Member

defi:CryptocurrencyMember

2024-03-31

0001985840

us-gaap:FairValueInputsLevel2Member

defi:CryptocurrencyMember

2024-03-31

0001985840

us-gaap:FairValueInputsLevel3Member

defi:CryptocurrencyMember

2024-03-31

0001985840

us-gaap:FairValueInputsLevel1Member

us-gaap:MoneyMarketFundsMember

2024-03-31

0001985840

us-gaap:FairValueInputsLevel2Member

us-gaap:MoneyMarketFundsMember

2024-03-31

0001985840

us-gaap:FairValueInputsLevel3Member

us-gaap:MoneyMarketFundsMember

2024-03-31

0001985840

us-gaap:MoneyMarketFundsMember

2024-03-31

0001985840

us-gaap:FairValueInputsLevel1Member

defi:BitcoinFuturesContractsMember

2024-03-31

0001985840

us-gaap:FairValueInputsLevel2Member

defi:BitcoinFuturesContractsMember

2024-03-31

0001985840

us-gaap:FairValueInputsLevel3Member

defi:BitcoinFuturesContractsMember

2024-03-31

0001985840

defi:BitcoinFuturesContractsMember

2024-03-31

0001985840

us-gaap:FairValueInputsLevel1Member

2023-12-31

0001985840

us-gaap:FairValueInputsLevel2Member

2023-12-31

0001985840

us-gaap:FairValueInputsLevel3Member

2023-12-31

0001985840

us-gaap:FairValueInputsLevel1Member

us-gaap:CashEquivalentsMember

2023-12-31

0001985840

us-gaap:FairValueInputsLevel2Member

us-gaap:CashEquivalentsMember

2023-12-31

0001985840

us-gaap:FairValueInputsLevel3Member

us-gaap:CashEquivalentsMember

2023-12-31

0001985840

us-gaap:FairValueInputsLevel1Member

defi:BitcoinFuturesContractsMember

2023-12-31

0001985840

us-gaap:FairValueInputsLevel2Member

defi:BitcoinFuturesContractsMember

2023-12-31

0001985840

us-gaap:FairValueInputsLevel3Member

defi:BitcoinFuturesContractsMember

2023-12-31

0001985840

defi:BitcoinFuturesContractsMember

2023-12-31

0001985840

defi:TeucriumTradingLLCMember

2024-01-02

2024-01-03

0001985840

defi:HashdexBitcoinFuturesETFMember

2024-01-02

2024-01-03

0001985840

2024-01-03

0001985840

defi:HashdexBitcoinETFMember

defi:SpotBitcoinMember

2024-03-26

0001985840

defi:HashdexBitcoinETFMember

defi:CMETradedBitcoinFuturesContractsCashAndCashEquivalentsMember

2024-03-26

iso4217:USD

xbrli:shares

iso4217:USD

xbrli:shares

xbrli:pure

defi:Contract

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM

10-Q

| ☒ |

Quarterly

report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

| |

|

| for the

quarterly period ended March 31, 2024 |

| |

OR

| ☐ |

Transition report

pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

| |

|

| for

the transition period from _________ to _________ |

Commission

File Number: 001-41900

| Tidal

Commodities Trust I |

| |

(Exact name of registrant as specified in its charter) |

|

| Delaware |

|

92-6468665 |

(State

or other jurisdiction of

incorporation

or organization)

|

|

(I.R.S.

Employer

Identification

No.)

|

234

West Florida Street, Suite 203 Milwaukee, WI 53204

(Address

of principal executive offices) (Zip code)

(844)

986-7700

(Registrant’s

telephone number, including area code)

Securities

registered pursuant to Section 12(b) of the Act:

| Title

of each Class |

|

Trading

Symbol |

|

Name

of each exchange on which registered |

Shares

of beneficial interest, no par value, of

Hashdex Bitcoin ETF, a series of the Registrant |

|

DEFI |

|

NYSE Arca, Inc. |

Indicate

by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports),

and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes ☐ No

Indicate

by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted and posted

pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period

that the registrant was required to submit such files). ☒ Yes ☐ No

Indicate

by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting

company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,”

“smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large

accelerated filer |

☐ |

Accelerated

filer |

☐ |

| Non-accelerated

Filer |

☒ |

Smaller

reporting company |

☒ |

| |

|

Emerging

growth company |

☒ |

If

an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for

complying with any new or revised financial accounting standards provided pursuant to Section 13 (a) of the Exchange Act.

Indicate

by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐ Yes ☒ No

As

of May 13,

2024, there were 160,000 shares

of beneficial interest, no par value, of Hashdex Bitcoin ETF issued and outstanding.

Part I. FINANCIAL INFORMATION

Part II. OTHER INFORMATION

Part

I. FINANCIAL INFORMATION

Item

1. Financial Statements.

Index

to Financial Statements

TIDAL COMMODITIES TRUST I

Combined Statements of Assets and Liabilities at March 31, 2024 (Unaudited) and December 31, 2023

|

F-1 |

| Combined Schedule of Investments at March 31, 2024 (Unaudited) and December 31, 2023 |

F-2 |

| Combined Statements of Operations (Unaudited) for the three months ended March 31, 2024 and 2023 |

F-4 |

| Combined Statements of Changes in Net Assets (Unaudited) for the three months ended March 31, 2024 and 2023 |

F-5 |

| Combined Statements of Cash Flows (Unaudited) for the three months ended March 31, 2024 and 2023 |

F-6 |

| Notes to Combined Financial Statements |

F-8 |

HASHDEX

BITCOIN ETF

Statements of Assets and Liabilities at March 31, 2024 (Unaudited) and December 31, 2023

|

F-20

|

| Schedule of Investments at March 31, 2024 (Unaudited) and December 31, 2023 |

F-21 |

| Statements of Operations (Unaudited) for the three months ended March 31, 2024 and 2023 |

F-23 |

| Statements of Changes in Net Assets (Unaudited) for the three months ended March 31, 2024 and 2023 |

F-24 |

| Statements of Cash Flows (Unaudited) for the three months ended March 31, 2024 and 2023 |

F-25 |

| Notes to Financial Statements |

|

TIDAL

COMMODITIES TRUST I

COMBINED

STATEMENTS OF ASSETS AND LIABILITIES

| | |

March 31, 2024 (Unaudited) | | |

December

31, 2023 | |

| Assets | |

| | | |

| | |

| Investments (Cost $10,578,023) | |

$ | 10,837,413 | | |

$ | — | |

| Cash and cash equivalents | |

| 237,786 | | |

| 1,867,663 | |

| Interest receivable | |

| 59,811 | | |

| 10,297 | |

| Equity in trading accounts: | |

| | | |

| | |

| Cryptocurrency futures contracts | |

| 14,259 | | |

| 129,519 | |

| Due from broker | |

| 233,247 | | |

| 582,908 | |

| Total equity in trading accounts | |

| 247,506 | | |

| 712,427 | |

| Total assets | |

$ | 11,382,516 | | |

$ | 2,590,387 | |

| | |

| | | |

| | |

| Liabilities | |

| | | |

| | |

| Management fee payable to Sponsor | |

| 19,207 | | |

| 2,053 | |

| Equity in trading accounts: | |

| | | |

| | |

| Cryptocurrency futures contracts | |

| 13,475 | | |

| 51,376 | |

| Total liabilities | |

$ | 32,682 | | |

$ | 53,429 | |

| | |

| | | |

| | |

| Net assets | |

$ | 11,349,834 | | |

$ | 2,536,958 | |

| | |

| | | |

| | |

| Shares authorized | |

| 140,000 | | |

| 50,000 | |

| | |

| | | |

| | |

| Net asset value per share | |

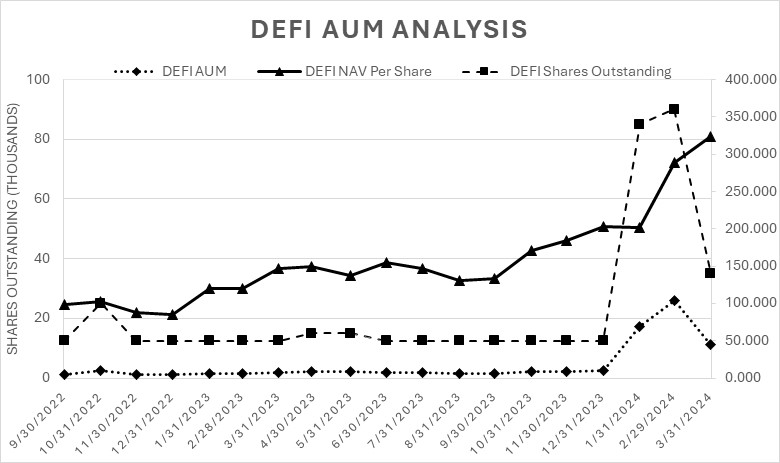

$ | 81.07 | | |

$ | 50.74 | |

| | |

| | | |

| | |

| Market value per share | |

$ | 81.50 | | |

$ | 50.73 | |

The

accompanying notes are an integral part of these financial statements.

TIDAL

COMMODITIES TRUST I

COMBINED

SCHEDULE OF INVESTMENTS

March

31, 2024

(Unaudited)

| Description: Assets |

|

|

|

|

|

|

|

|

|

|

Fair Value | | |

Percentage of Net

Assets | | |

Shares | |

| | |

| | |

| | |

| |

| Cryptocurrency | |

| | | |

| | | |

| | |

| Bitcoin | |

$ | 10,837,413 | | |

| 95.49 | % | |

| 15,331 | |

| Total Cryptocurrency (cost $10,578,023) | |

$ | 10,837,413 | | |

| 95.49 | % | |

| | |

| | |

| | | |

| | | |

| | |

| Cash equivalents | |

| | | |

| | | |

| | |

| Money market funds | |

| | | |

| | | |

| | |

| First American Government Obligations Fund - Class X, 5.29% | |

$ | 237,786 | | |

| 2.10 | % | |

| 237,786 | |

| Total Cash Equivalents (cost $237,786) | |

$ | 237,786 | | |

| 2.10 | % | |

| | |

| | |

| | | |

| | | |

| | |

| | |

| | | |

Percentage of | | |

Notional Amount | |

| Description: Assets |

|

|

|

|

|

|

|

|

|

|

Fair Value | | |

Net Assets | | |

(Long Exposure) | |

| | |

| | | |

| | | |

| | |

| Cryptocurrency futures contracts | |

| | | |

| | | |

| | |

| United States CME Bitcoin Futures contracts | |

| | | |

| | | |

| | |

| CME Micro Bitcoin Futures April 2024 (21 contracts) | |

$ | 14,259 | | |

| `0.13 | % | |

$ | 150,213 | |

| Total cryptocurrency futures contracts | |

$ | 14,259 | | |

| 0.13 | % | |

$ | 150,213 | |

| | |

| | | |

| | | |

| | |

| Description: Liabilities |

|

|

|

|

|

|

|

|

|

|

| | | |

| | | |

| | |

| | |

| | | |

| | | |

| | |

| Cryptocurrency futures contracts | |

| | | |

| | | |

| | |

| United States CME Bitcoin Futures contracts | |

| | | |

| | | |

| | |

| CME Bitcoin Futures April 2024 (1 contract) | |

$ | 13,475 | | |

| 0.12 | % | |

$ | 357,650 | |

| Total cryptocurrency futures contracts | |

$ | 13,475 | | |

| 0.12 | % | |

$ | 357,650 | |

The

accompanying notes are an integral part of these financial statements.

TIDAL

COMMODITIES TRUST I

(FORMERLY

TEUCRIUM COMMODITIES TRUST)

SCHEDULE

OF INVESTMENTS

December

31, 2023

| Description: Assets |

|

|

|

|

|

| |

Yield | | |

Fair Value | | |

Percentage of Net Assets | | |

Shares | |

| |

| Cash equivalents | |

| | | |

| | | |

| | | |

| | |

| Money market funds | |

| | | |

| | | |

| | | |

| | |

| U.S. Bank Deposit Account (cost $1,867,663) | |

| 5.27 | % | |

$ | 1,867,663 | | |

| 73.62 | % | |

| 1,867,663 | |

| Total Cash Equivalents (cost $1,867,663) | |

| | | |

$ | 1,867,663 | | |

| 73.62 | % | |

| | |

| | |

| | | |

| | | |

| | | |

| | |

| Description: Assets |

|

|

|

|

|

| |

| | | |

Fair Value | | |

Percentage of

Net Assets

| | |

Notional Amount

(Long Exposure)

| |

| | |

| | | |

| | | |

| | | |

| | |

| Cryptocurrency futures contracts | |

| | | |

| | | |

| | | |

| | |

| United States CME Bitcoin Futures contracts | |

| | | |

| | | |

| | | |

| | |

| CME Bitcoin Futures JAN 24 (6 contracts) | |

| | | |

$ | 129,519 | | |

| 5.11 | % | |

$ | 1,274,500 | |

| Total cryptocurrency futures contracts | |

| | | |

$ | 129,519 | | |

| 5.11 | % | |

$ | 1,274,500 | |

| | |

| | | |

| | | |

| | | |

| | |

| Description: Liabilities |

|

|

|

|

|

| |

| | | |

| | | |

| | | |

| | |

| | |

| | | |

| | | |

| | | |

| | |

| Cryptocurrency futures contracts | |

| | | |

| | | |

| | | |

| | |

| United States CME Bitcoin Futures contracts | |

| | | |

| | | |

| | | |

| | |

| CME Bitcoin Futures FEB 24 (6 contracts) | |

| | | |

| 51,376 | | |

| 2.03 | % | |

$ | 1,288,500 | |

| Total cryptocurrency futures contracts | |

| | | |

$ | 51,376 | | |

| 2.03 | % | |

$ | 1,288,500 | |

The

accompanying notes are an integral part of these financial statements.

TIDAL

COMMODITIES TRUST I

COMBINED

STATEMENTS OF OPERATIONS

(Unaudited)

| | |

Three Months Ended March 31, 2024 | | |

Three Months Ended March 31, 2023 | |

| | |

| | |

| |

| Income | |

| | | |

| | |

| Realized and unrealized gain (loss) on trading of cryptocurrency futures contracts: | |

| | | |

| | |

| Realized gain (loss) on cryptocurrency futures contracts | |

$ | 7,635,018 | | |

$ | 629,551 | |

| Net change in unrealized appreciation/depreciation on investments | |

| 259,390 | | |

| — | |

| Net change in unrealized appreciation/depreciation on cryptocurrency futures contracts | |

| (77,359 | ) | |

| 128,468 | |

| Broker interest income | |

| 59,803 | | |

| — | |

| Interest income | |

| 118,946 | | |

| 13,448 | |

| Total income (loss) | |

| 7,995,798 | | |

| 771,467 | |

| | |

| | | |

| | |

| Expenses | |

| | | |

| | |

Management fees

| |

| 42,381 | | |

| 3,395 | |

| Professional fees | |

| — | | |

| 58,820 | |

| Distribution and marketing fees | |

| — | | |

| 1,362 | |

| Custodian fees and expenses | |

| — | | |

| 259 | |

| Business permits and license fees | |

| — | | |

| 10,129 | |

| General and administrative expenses | |

| — | | |

| — | |

| Broker expenses | |

| 16,148 | | |

| — | |

| Total expenses | |

| 58,529 | | |

| 73,965 | |

| | |

| | | |

| | |

| Expenses waived by the Sponsor | |

| — | | |

| (70,570 | ) |

| | |

| | | |

| | |

| Total expenses, net | |

| 58,529 | | |

| 3,395 | |

| | |

| | | |

| | |

| Net

income (loss) | |

$ | 7,937,269 | | |

$ | 768,072 | |

The

accompanying notes are an integral part of these financial statements.

TIDAL

COMMODITIES TRUST I

COMBINED

STATEMENTS OF CHANGES IN NET ASSETS

(Unaudited)

| | |

Three Months Ended March 31, 2024 | | |

Three Months Ended March 31, 2023 | |

| | |

| | |

| |

| Operations | |

| | | |

| | |

| Net income (loss) | |

$ | 7,937,269 | | |

$ | 768,072 | |

| Capital transactions | |

| | | |

| | |

| Issuance of Shares | |

| 17,089,625 | | |

| 367,689 | |

| Redemption of Shares | |

| (16,214,018 | ) | |

| — | |

| Net change in the cost of the Underlying Funds | |

| — | | |

| — | |

| Total capital transactions | |

| 875,607 | | |

| 367,689 | |

| Net change in net assets | |

| 8,812,876 | | |

| 1,135,761 | |

| | |

| | | |

| | |

| Net assets, beginning of period | |

$ | 2,536,958 | | |

$ | 1,070,263 | |

| | |

| | | |

| | |

| Net assets, end of period | |

$ | 11,349,834 | | |

$ | 2,206,024 | |

The

accompanying notes are an integral part of these financial statements.

TIDAL

COMMODITIES TRUST I

STATEMENTS

OF CASH FLOWS

(Unaudited)

| | |

Three Months Ended

March 31, 2024 | | |

Three Months Ended

March 31, 2023 | |

| Cash flows from operating activities | |

| | | |

| | |

| Net income (loss) | |

$ | 7,937,269 | | |

$ | 768,072 | |

| Adjustments to reconcile net income (loss) to net cash provided by (used in) operating activities: | |

| | | |

| | |

| Net change in unrealized appreciation (depreciation) on cryptocurrency futures contracts | |

| 77,359 | | |

| (128,468 | ) |

| Changes in operating assets and liabilities: | |

| | | |

| | |

| Investments | |

| (10,837,413 | ) | |

| — | |

| Due from broker | |

| 349,661 | | |

| (109,824 | ) |

| Interest receivable | |

| (49,514 | ) | |

| (2,124 | ) |

| Other assets | |

| — | | |

| — | |

| Due to broker | |

| — | | |

| — | |

| Management fee payable to Sponsor | |

| 17,154 | | |

| 408 | |

| Other liabilities | |

| — | | |

| — | |

| Net cash provided by (used in) operating activities | |

| (2,505,484 | ) | |

| 528,064 | |

| Cash flows from financing activities: | |

| | | |

| | |

| Proceeds from sale of Shares | |

| 17,089,625 | | |

| — | |

| Redemption of Shares | |

| (16,214,018 | ) | |

| — | |

| Net change in cost of the Underlying Funds | |

| — | | |

| — | |

| Net cash provided by (used in) financing activities | |

| 875,607 | | |

| — | |

| | |

| | | |

| | |

| Net change in cash and cash equivalents | |

| (1,629,877 | ) | |

| 528,064 | |

| Cash and cash equivalents, beginning of period | |

| 1,867,663 | | |

| 701,969 | |

| Cash and cash equivalents, end of period | |

$ | 237,786 | | |

$ | 1,230,033 | |

The

accompanying notes are an integral part of these financial statements.

TIDAL

COMMODITIES TRUST I

FINANCIAL

HIGHLIGHTS

| | |

Three Months Ended | | |

Three Months Ended | |

| | |

March 31, 2024 | | |

March 31, 2023 | |

| Per Share Operation Performance | |

| | | |

| | |

| Net asset value at beginning of period | |

$ | 50.74 | | |

$ | 21.40 | |

| Income (loss) from investment operations: | |

| | | |

| | |

| Investment income | |

| 0.62 | | |

| 0.27 | |

| Net realized and unrealized gain (loss) on cryptocurrency futures contracts | |

| 29.91 | | |

| 15.16 | |

| Total expenses | |

| (0.20 | ) | |

| (0.07 | ) |

| Net increase (decrease) in net asset value | |

| 30.33 | | |

| 15.36 | |

| Net asset value at end of period | |

$ | 81.07 | | |

$ | 36.76 | |

| Total Return | |

| 59.78 | % | |

| 71.79 | % |

| Ratios to Average Net Assets (Annualized) | |

| | | |

| | |

| Total expenses | |

| 1.30 | % | |

| 20.48 | % |

| Total expenses, net | |

| 1.30 | % | |

| 0.94 | % |

| Net investment income (loss) | |

| 2.67 | % | |

| 2.78 | % |

The

accompanying notes are an integral part of these financial statements.

NOTES TO FINANCIAL STATEMENTS

March 31, 2024 (Unaudited)

Note 1 – Organization and

Significant Accounting Policies

These footnotes represent the footnotes to Hashdex

Bitcoin ETF’s Statement of Assets and Liabilities and the Combined Financial Statements of Tidal Commodities Trust I.

Hashdex Bitcoin ETF (the “Fund”) is a

series of Tidal Commodities Trust I (“Trust”), a Delaware statutory trust organized on February 10, 2023. The Fund operates

pursuant to the First Amended and Restated Declaration of Trust and Trust Agreement (“Trust Agreement”), dated March 10, 2023.

The Trust is registered with the U.S. Securities and Exchange Commission (“SEC”) under the Securities Act of 1933, as amended

(together with the rules and regulations adopted thereunder, as amended, the “1933 Act”), as an exchange-traded fund. The Fund

was formed and is managed and controlled by the Sponsor, a limited liability company formed in Delaware on March 14, 2012. The sponsor

of the Fund is Tidal Investments LLC (f/k/a Toroso Investments, LLC, the “Sponsor”), The Sponsor is registered as a commodity

pool operator (“CPO”) with the Commodity Futures Trading Commission (“CFTC”) and is a member of the National Futures

Association (“NFA”). The Fund intends to be treated as a partnership for U.S. federal income tax purposes.

On January 2,

2024, the initial Form S-1 for DEFI was declared effective by the U.S. Securities and Exchange Commission (“SEC”). The Fund

is the successor and surviving entity from the merger (the “Merger”) of the Hashdex Bitcoin Futures ETF (the “Predecessor

Fund”) into the Fund. The Predecessor Fund was a series of the Teucrium Commodity Trust (the “Predecessor Trust”) sponsored

by Teucrium Trading, LLC (“Prior Sponsor”). The Merger closed on January 3, 2024. In connection with the Merger, the Predecessor

Fund shareholders received one Share for each share of the Predecessor Fund they owned prior to the Merger.

The Fund’s investment objective is for changes

in the Shares’ net asset value (“NAV”) to reflect the daily changes of the price of the Nasdaq Bitcoin Reference Price

- Settlement (NQBTCS) (the “Benchmark”), less expenses from the Fund’s operations. The Benchmark is designed to track

the price performance of bitcoin. The Fund invests in bitcoin, bitcoin futures contracts (“Bitcoin Futures Contracts”) listed

on the Chicago Mercantile Exchange Inc. (“CME”), and cash and cash equivalents. Because the Fund’s investment objective

is to track the price of the Benchmark, changes in the price of the Shares may vary from changes in the spot price of bitcoin.

The accompanying unaudited financial statements have

been prepared in accordance with Rule 10-01 of Regulation S-X promulgated by the SEC and, therefore, do not include all information and

footnote disclosures required under accounting principles generally accepted in the United States of America (“GAAP”). The

financial information included herein is unaudited; however, such financial information reflects all adjustments which are, in the opinion

of management, necessary for the fair presentation of the Fund’s financial statements for the interim period. It is suggested that

these interim financial statements be read in conjunction with the financial statements and related notes included in the Trust’s

Annual Report on Form 10-K, as well as the most recent Form S-1 filing, as applicable. The operating results through March 31, 2023 are

not necessarily indicative of the results to be expected from the full year ended December 31, 2024.

The Fund continuously offers and redeems shares

(“Shares”) in blocks of at least 10,000 Shares

(each such block, a “Creation Unit”) at an initial price per Share of $25.

Only Authorized Participants may purchase and redeem Shares from the Fund and then only in Creation Units. An Authorized Participant

is an entity that has entered into an Authorized Participant Agreement with the Trust and the Sponsor. Shares are offered on a

continuous basis to Authorized Participants in Creation Units at NAV. Authorized Participants may then offer to the public, from

time to time, shares from any Creation Unit they create at a per-share market price. The form of Authorized Participant Agreement

sets forth the terms and conditions under which an Authorized Participant may purchase or redeem a Creation Unit. Authorized

Participants will not receive from the Fund, the Sponsor, or any of their affiliates, any fee or other compensation in connection

with their sale of Shares to the public. An Authorized Participant may receive commissions or fees from investors who purchase

Shares through their commission or fee-based brokerage accounts.

Significant accounting policies of the Fund are as

follows:

Use of Estimates

The preparation

of financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amount

of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements, and the reported

amounts of the revenue and expenses during the reporting period. Actual results could differ from those estimates.

Indemnifications

In the normal

course of business, the Fund enters into contracts that contain a variety of representations which provide general indemnifications. The

Fund’s maximum exposure under these arrangements cannot be known; however, the Fund expects any risk of loss to be remote.

Cash

Cash includes

money market funds held.

Income Taxes

For U.S.

federal income tax purposes, the Fund will be classified as a publicly traded partnership. A publicly traded partnership is

generally taxable as a corporation for U.S. federal income tax purposes unless 90% or more of the publicly traded

partnership’s gross income for each taxable year of its existence consists of qualifying income as defined in section 7704(d)

of the Internal Revenue Code of 1986, as amended (the “Code”). Qualifying income is defined as generally including, in

pertinent part, interest (other than from a financial business), dividends, and gains from the sale or disposition of capital assets

held for the production of interest or dividends. In the case of a partnership of which a principal activity is the buying and

selling of commodities, other than as inventory, or of futures, forwards, and options with respect to commodities, qualifying income

also includes income and gains from commodities and from futures, forwards, options with respect to commodities and, provided the

partnership is a trader or investor with respect to such assets, swaps and other notional principal contracts with respect to

commodities. There is very limited authority on the U.S. federal income tax treatment of bitcoin and no direct authority on bitcoin

derivatives, such as Bitcoin Futures Contracts. Based on an opinion received by Tidal from their independent legal counsel and a

Commodity Futures Trading Commission determination that treats bitcoin as a commodity under the Commodity Exchange Act, the Fund

intends to take the position that bitcoin and Bitcoin Futures Contracts consist of futures on commodities for purposes of the

qualifying income exception under section 7704 of the Code. Accordingly, the Fund expects that at least 90% of the Fund’s

gross income for each taxable year will consist of qualifying income and that the Fund will be taxed as a partnership for U.S.

federal income tax purposes. Therefore, the Fund does not record a provision for income taxes because the shareholders report their

share of the Fund’s income or loss on their income tax returns.

The Fund is

required to determine whether a tax position is more likely than not to be sustained upon examination by the applicable taxing authority,

including resolution of any related appeals or litigation processes, based on the technical merits of the position. The Fund will file

income tax returns in the U.S. federal jurisdiction and may file income tax returns in various U.S. states and foreign jurisdictions.

The Fund may

be subject to potential examination by U.S. federal, U.S. state, or foreign jurisdictional authorities in the area of income taxes. These

potential examinations may include among other things questioning the tax classification of the Fund, the timing and amount of deductions,

the nexus of income among various tax jurisdictions, and compliance with U.S. federal, U.S. state and foreign tax laws.

Creation

and Redemptions

Authorized Purchasers

may purchase Creation Baskets consisting of 10,000 Shares from the Fund. The amount of the proceeds required to purchase a Creation

Basket will be equal to the NAV of the Shares in the Creation Basket determined as of 4:00 p.m. (ET) on the day the order to create the

basket is received in good order.

Authorized Purchasers

may redeem Shares from the Fund only in blocks of 10,000 Shares called “Redemption Baskets.” The amount of the redemption

proceeds for a Redemption Basket will be equal to the NAV of the Shares in the Redemption Basket determined as of 4:00 p.m. (ET) on the

day the order to redeem the basket is received in good order.

The Fund will

receive the proceeds from Shares sold or will pay for redeemed Shares within three business days after the trade date of the purchase

or redemption, respectively. The amounts due from Authorized Purchasers will be

reflected in the Fund’s statements of assets

and liabilities as capital shares receivable. Amounts payable to Authorized Purchasers upon redemption will be reflected in the Fund’s

statements of assets and liabilities as payable for Shares redeemed.

As outlined

in the Trust's Registration Statement on Form S-1, filed with the SEC on March 18, 2024, 10,000 Shares represent five Redemption Baskets for the Fund and a minimum level of Shares.

If the Fund experienced redemptions that caused the number of Shares outstanding to decrease to the minimum level of Shares required to

be outstanding, until the minimum number of Shares is again exceeded through the purchase of a new Creation Basket, there can be no more

redemptions by an Authorized Purchaser.

Calculation

of Net Asset Value

The Fund’s

NAV is calculated by:

| |

● |

Taking the current market value of its total assets; |

| |

● |

Subtracting any liabilities; and |

| |

● |

Dividing the above total by the number of Shares outstanding. |

U.S. Bancorp

Fund Services, LLC, doing business as U.S. Bank Global Fund Services (“Global Fund Services”), the Fund's sub-administrator,

will calculate the NAV of the Fund once each trading day. It will calculate the NAV as of the earlier of the close of the New York Stock

Exchange or 4:00 p.m. (ET). The NAV for a particular trading day will be released after 4:15 p.m. (ET).

To

determine the value of Bitcoin Futures Contracts, Global Fund Services uses the settlement price for the Benchmark Component Futures

Contracts, as reported on the CME. CME Group staff determines the daily settlements for the Benchmark Component Futures Contracts

based on trading activity on CME Globex exchange between 14:59:00 and 15:00:00 Central Time (CT), the settlement period. When a

Bitcoin Futures Contract has closed at its daily price fluctuation limit, that limit price will be the daily settlement price that

the CME publishes. The Fund will use the published settlement price to price its Shares on that day. If the CME halted trading in

Bitcoin Futures Contracts for other reasons, including if trading were halted for an entire trading day or several trading days, the

Fund would value its Bitcoin Futures Contracts by using the settlement price that the CME publishes. Such valuation is generally

deemed a Level 1 valuation.

The value of

the Bitcoin held by the Fund will be determined using a “Futures-Based Spot Price” (or “FBSP”) methodology. This

methodology has been chosen by the Sponsor specifically to calculate the Fund's NAV, isolating it from data from unregulated bitcoin exchanges.

The methodology to derive the settlement prices of Bitcoin Futures Contracts on the CME involves a calculation that is a function of both

the length of time (the tenor) until each Bitcoin Futures Contract is due for settlement, and the final settlement price for each contract

on that day. The calculation is based on estimating a simple quadratic function to fit the prices across the different tenors and extrapolate

this curve to zero days tenor. This approach is designed to give more importance to contracts that are due for settlement in the near

term, considering that the prices of these near-term contracts are more reliable indicators of the current spot price of bitcoin and are

also more heavily traded. Such Valuation is generally deemed a Level 2 valuation.

Fair Value

- Definition and Hierarchy

In accordance

with GAAP, fair value is defined as the price that would be received to sell an asset or paid to transfer a liability (i.e., the “exit

price”) in an orderly transaction between market participants at the measurement date.

In determining

fair value, the Fund uses various valuation approaches. In accordance with GAAP, a fair value hierarchy for inputs is used in measuring

fair value that maximizes the use of observable inputs and minimizes the use of unobservable inputs by requiring that the most observable

inputs be used when available. Observable inputs are those that market participants would use in pricing the asset or liability based

on market data obtained from sources independent of the Fund. Unobservable inputs reflect the Fund’s assumptions about the inputs

market participants would use in pricing the asset or liability developed based on the best information available in the circumstances.

The fair value hierarchy is categorized into three levels based on the inputs as follows:

Level 1 -

Valuations based on unadjusted quoted prices in active markets for identical assets or liabilities that the Fund has the ability to access.

Valuation adjustments and block discounts are not applied to Level 1 financial instruments. Since valuations are based on quoted prices

that are readily and regularly available in an active market, valuation of these financial instruments does not entail a significant degree

of judgment.

Level 2 -

Valuations based on quoted prices in markets that are not active or for which all significant inputs are observable, either directly or

indirectly.

Level 3 -

Valuations based on inputs that are unobservable and significant to the overall fair value measurement.

The availability

of valuation techniques and observable inputs can vary from financial instrument to financial instrument and is affected by a wide variety

of factors including, the type of financial instrument, whether the financial instrument is new and not yet established in the marketplace,

and other characteristics particular to the transaction. To the extent that valuation is based on models or inputs that are less observable

or unobservable in the market, the determination of fair value requires more judgment. Those estimated values do not necessarily represent

the amounts that may be ultimately realized due to the occurrence of future circumstances that cannot be reasonably determined. Because

of the inherent uncertainty of valuation, those estimated values may be materially higher or lower than the values that would have been

used had a ready market for the financial instruments existed. Accordingly, the degree of judgment exercised by the Fund in determining

fair value is greatest for financial instruments categorized in Level 3. In certain cases, the inputs used to measure fair value may fall

into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy, within

which the fair value measurement in its entirety falls, is determined based on the lowest level input that is significant to the fair

value measurement.

Schedule of fair values of investments disaggregated into three levels of fair value hierarchy

March 31, 2024

| | |

Level 1 | | |

Level 2 | | |

Level 3 | | |

Balance as of

March 31, 2024 | |

| Assets: | |

| | | |

| | | |

| | | |

| | |

| Cryptocurrency | |

$ | — | | |

$ | 10,837,413 | | |

$ | — | | |

$ | 10,837,413 | |

| Money market funds | |

| 237,786 | | |

| — | | |

| — | | |

| 237,786 | |

| Bitcoin futures contracts | |

| 14,259 | | |

| — | | |

| — | | |

| 14,259 | |

| Total | |

$ | 252,045 | | |

$ | 10,837,413 | | |

$ | — | | |

$ | 11,089,458 | |

| | |

| | | |

| | | |

| | | |

| | |

| Liabilities: | |

| | | |

| | | |

| | | |

| | |

| Bitcoin futures contracts | |

$ | 13,475 | | |

$ | — | | |

$ | — | | |

$ | 13,475 | |

December 31, 2023

| | |

Level 1 | | |

Level 2 | | |

Level 3 | | |

Balance as of

December 31, 2023 | |

| Assets: | |

| | | |

| | | |

| | | |

| | |

| Cash Equivalents | |

$ | 1,867,663 | | |

$ | — | | |

$ | — | | |

$ | 1,867,663 | |

| Bitcoin futures contracts | |

| 129,519 | | |

| — | | |

| — | | |

| 129,519 | |

| Total | |

$ | 1,997,182 | | |

$ | — | | |

$ | — | | |

$ | 1,997,182 | |

| | |

| | | |

| | | |

| | | |

| | |

| Liabilities: | |

| | | |

| | | |

| | | |

| | |

| Bitcoin futures contracts | |

$ | 51,376 | | |

$ | — | | |

$ | — | | |

$ | 51,376 | |

For the three months ended March 31, 2024 and year

ended December 31, 2023, the Fund did not have any significant transfers between any of the levels of the fair value hierarchy.

Derivative

Investments

In the normal course of business, the Fund utilizes

derivative contracts in connection with its proprietary trading activities. Investments in derivative contracts are subject to additional

risks that can result in a loss of all or part of an investment. The Fund’s derivative activities and exposure to derivative contracts

are classified by the following primary underlying risks: interest rate, credit, commodity price, and equity price risks. In addition

to its primary underlying risks, the Fund is also subject to additional counterparty risk due to inability of its counterparties to meet

the terms of their contracts.

Futures Contracts

The Fund is subject to cryptocurrency price risk in

the normal course of pursuing its investment objectives. A futures contract represents a commitment for the future purchase or sale of

an asset at a specified price on a specified date.

The purchase and sale of futures contracts requires

margin deposits with a Futures Commission Merchant (“FCM”). Subsequent payments (variation margin) are made or received by

the Fund each day, depending on the daily fluctuations in the value of the contract, and are recorded as unrealized gains or losses by

the Fund. Futures contracts may reduce the Fund’s exposure to counterparty risk since futures contracts are exchange-traded; and

the exchange’s clearinghouse, as the counterparty to all exchange-traded futures, guarantees the futures against default.

The Commodity Exchange Act requires an FCM to segregate

all customer transactions and assets from the FCM’s proprietary activities. A customer’s cash and other equity deposited with

an FCM are considered commingled with all other customer funds subject to the FCM’s segregation requirements. In the event of an

FCM’s insolvency, recovery may be limited to the Fund’s pro rata share of segregated customer funds available. It is possible

that the recovery amount could be less than the total of cash and other equity deposited.

The following table discloses information about offsetting

assets and liabilities presented in the statements of assets and liabilities to enable users of these financial statements to evaluate

the effect or potential effect of netting arrangements for recognized assets and liabilities. These recognized assets and liabilities

are presented as defined in the Financial Accounting Standards Board’s (“FASB”) Accounting Standards Update (“ASU”)

No. 2011-11 “Balance Sheet (Topic 210): Disclosures about Offsetting Assets and Liabilities” and subsequently clarified in

FASB ASU 2013-01 “Balance Sheet (Topic 210): Clarifying the Scope of Disclosures about Offsetting Assets and Liabilities.”

The following table also identifies the fair value

amounts of derivative instruments included in the statements of assets and liabilities as derivative contracts, categorized by primary

underlying risk, and held by StoneX as of March 31, 2024.

Offsetting of Financial Assets and Derivative Assets

as of March 31, 2024

| |

| |

| |

| |

(iv) Gross Amount

Not Offset In the

Statement

of Asset and Liabilities

| |

|

| Description | |

(i)

Gross

Amount

of

Recognized

Assets | |

(ii)

Gross

Amount

Offset in the

Statement of

Assets and | |

(iii)

= (i-ii)

Net

Amount

Presented in

the Statement

of Assets and

Liabilities | |

Futures

Contracts

Available

for

Offset | |

Collateral,

Due to

Broker | |

(v)

= (iii)-(iv)

Net

Amount |

| Cryptocurrency Price | |

| |

| |

| |

| |

| |

|

| Bitcoin futures contracts | |

$ | 14,259 | |

$ | — | |

$ |

14,259 | |

$ |

13,475 | |

$ | — | |

$ |

784 |

Offsetting of Financial Liabilities and Derivative Assets as of

March 31, 2024

| |

|

|

|

|

|

|

|

(iv)

Gross

Amount Not Offset

in the Statement of

Assets and Liabilities |

|

|

| Description |

|

(i)

Gross

Amount

of

Recognized

Assets |

|

(ii)

Gross

Amount

Offset in the

Statement of

Assets

and

Liabilities |

|

(iii)

= (i-ii)

Net

Amount

Presented in

the Statement

of Assets

and

Liabilities |

|

Futures

Contracts

Available

for

Offset |

|

Collateral,

Due to

Broker |

|

(v)

= (iii)-(iv)

Net

Amount |

| Cryptocurrency Price |

|

|

|

|

|

|

|

|

|

|

|

|

| Bitcoin futures contracts |

|

$ |

13,475 |

|

$ |

— |

|

$ |

13,475 |

|

$ |

13,475 |

|

$ |

— |

|

|

— |

Offsetting of Financial Assets and Derivative Assets as of December

31, 2023

| |

|

|

|

|

|

|

|

(iv)

Gross

Amount Not Offset

in the Statement of

Assets and Liabilities |

|

|

| Description |

|

(i)

Gross

Amount

of

Recognized

Assets |

|

(ii)

Gross

Amount

Offset in the

Statement of

Assets and

Liabilities |

|

(iii)

= (i-ii)

Net

Amount

Presented in

the Statement

of Assets and

Liabilities |

|

Futures

Contracts

Available for

Offset |

|

Collateral,

Due to

Broker |

|

(v)

= (iii)-(iv)

Net

Amount |

| Cryptocurrency Price |

|

|

|

|

|

|

|

|

|

|

|

|

| Bitcoin futures contracts |

|

$ |

129,519 |

|

$ |

— |

|

|

129,519 |

|

|

51,376 |

|

$ |

— |

|

|

78,143 |

Offsetting of Financial Liabilities and Derivative Assets as of

December 31, 2023

| |

|

|

|

|

|

|

|

(iv)

Gross Amount Not Offset

in the Statement of

Assets and Liabilities |

|

|

| Description |

|

(i)

Gross

Amount

of

Recognized

Assets |

|

(ii)

Gross

Amount

Offset in the

Statement of

Assets and

Liabilities |

|

(iii)

= (i-ii)

Net

Amount

Presented in

the Statement

of Assets

and

Liabilities |

|

Futures

Contracts

Available

for

Offset |

|

Collateral,

Due to

Broker |

|

(v)

= (iii)-(iv)

Net

Amount |

| Cryptocurrency Price |

|

|

|

|

|

|

|

|

|

|

|

|

| Bitcoin futures contracts |

|

$ |

51,376 |

|

$ |

— |

|

|

51,376 |

|

|

51,376 |

|

$ |

— |

|

$ |

— |

The following tables identify the net gain and loss

amounts included in the statements of operations as realized and unrealized gains and losses on trading of cryptocurrency futures contracts

categorized by primary underlying risk:

Three months ended March 31, 2024.

| | |

Realized Gain (Loss) on Commodity Futures Contracts | | |

Net Change in Unrealized Appreciation/ Depreciation on Commodity Futures Contracts | |

| Cryptocurrency Price | |

| | |

| |

| Bitcoin futures contracts | |

$ | 7,635,018 | | |

| (77,359 | ) |

Three months ended March 31, 2023.

| | |

Realized Gain (Loss) on Commodity Futures Contracts | | |

Net Change in Unrealized Appreciation/ Depreciation on Commodity Futures Contracts | |

| Cryptocurrency Price | |

| | |

| |

| Bitcoin futures contracts | |

$ | 629,551 | | |

$ | 128,468 | |

Volume of

Derivative Activities

The average notional market value categorized by primary

underlying risk for all futures contracts held was $9.4 million and $1.7 million respectively for the three months ended March 31,

2024, and for the three months ended March 31, 2023.

Basis of

Presentation

The preparation

of these financial statements in conformity with U.S. generally accepted accounting principles requires management to make estimates and

assumptions that affect the reported amount of net assets and liabilities and disclosure of contingent assets and liabilities at the balance

sheet date. Actual results could differ from those estimates.

Organizational

and Offering Costs

All organizational

and initial offering costs for the Trust and the Fund were borne directly by the Sponsor. The Trust and the Fund do not have an obligation

to reimburse the Sponsor for organization and offering costs paid on their behalf.

Revenue Recognition

Investment transactions are accounted for on

a trade-date basis. All such transactions are recorded on the identified cost basis and marked to market daily. Unrealized appreciation

or depreciation on investments are reflected in the statements of operations as the difference between the original amount and the fair

market value as of the last business day of the year or as of the last date of the financial statements. Changes in the appreciation or

depreciation between periods are reflected in the statements of operations.

Brokerage

Commissions

The Sponsor recognizes the expense for brokerage commissions

for futures contract trades on a per-trade basis. The below table shows the amounts included on the statements of operations as total

brokerage commissions paid inclusive of unrealized loss.

| Three Months Ended March 31, 2024 |

$ |

5,781 |

|

| Three Months Ended March 31, 2023 |

$ |

609 |

|

Due from/to

Broker

The amount recorded by the Fund for the amount due

from and to the clearing broker includes, but is not limited to, cash held by the broker, amounts payable to the clearing broker related

to open transactions, payables for cryptocurrency futures accounts liquidating to an equity balance on the clearing broker’s records

and amounts of brokerage commissions paid and recognized as unrealized losses.

Margin is the minimum amount of funds that must be

deposited by a cryptocurrency interest trader with the trader’s broker to initiate and maintain an open position in futures contracts.

A margin deposit acts to assure the trader’s performance of the futures contracts purchased or sold. Futures contracts are customarily

bought and sold on initial margin that represents a very small percentage of the aggregate purchase or sales price of the contract. Because

of such low margin requirements, price fluctuations occurring in the futures markets may create profits and losses that, in relation to

the amount invested, are greater than customary in other forms of investment or speculation. As discussed below, adverse price changes

in the futures contract may result in margin requirements that greatly exceed the initial margin. In addition, the amount of margin required

in connection with a particular futures contract is set from time to time by the exchange on which the contract is traded and may be modified

from time to time by the exchange during the term of the contract. Brokerage firms, such as the Fund’s clearing brokers, carrying

accounts for traders in commodity interest contracts generally require higher amounts of margin as a matter of policy to further protect

themselves. Over the counter trading generally involves the extension of credit between counterparties, so the counterparties may agree

to require the posting of collateral by one or both parties to address credit exposure.

When a trader purchases an option, there is no margin

requirement; however, the option premium must be paid in full. When a trader sells an option, on the other hand, he or she is required

to deposit margin in an amount determined by the margin requirements established for the underlying interest and, in addition, an amount

substantially equal to the current premium for the option. The margin requirements imposed on the selling of options, although adjusted

to reflect the probability that out-of-the-money options will not be exercised, can in fact be higher than those imposed in dealing in

the futures markets directly. Complicated margin requirements apply to spreads and conversions, which are complex trading strategies in

which a trader acquires a mixture of options positions and positions in the underlying interest.

Ongoing or “maintenance” margin requirements

are computed each day by a trader’s clearing broker. When the market value of a particular open futures contract changes to a point

where the margin on deposit does not satisfy maintenance margin requirements, a margin call is made by the broker. If the margin call

is not met within a reasonable time, the broker may close out the trader’s position. With respect to the Fund’s trading, the

Fund (and not its shareholders personally) is subject to margin calls. Finally, many major U.S. exchanges have passed certain cross margining

arrangements involving procedures pursuant to which the futures and options positions held in an account would, in the case of some accounts,

be aggregated and margin requirements would be assessed on a portfolio basis, measuring the total risk of the combined positions.

Expenses

Expenses are recorded using the accrual method of

accounting.

Net Income

(Loss) per Share

Net income (loss) per share is the difference between

the NAV per unit at the beginning of each period and at the end of each period. The weighted average number of units outstanding was computed

for purposes of disclosing net income (loss) per weighted average unit. The weighted average units are equal to the number of units outstanding

at the end of the period, adjusted proportionately for units created or redeemed based on the amount of time the units were outstanding

during such period.

Note 2 – Sponsor

Fee Allocation of Expenses and Related Party Transactions

The Fund pays

the Sponsor a Management Fee, monthly in arrears, in an amount equal to 0.90% per annum of the daily NAV of the Fund. The Management

Fee is paid in consideration of the Sponsor’s services related to the management of the Fund’s business and affairs, including

the provision of commodity futures trading advisory services. Purchases of creation units with cash may cause the Fund to incur certain

costs including brokerage commissions and redemptions of creation units with cash may result in the recognition of gains or losses that

the Fund might not have incurred if it had made redemptions in-kind. The Fund pays all of its respective brokerage commissions, including

applicable exchange fees, National Futures Association fees and give-up fees, and other transaction related fees and expenses charged

in connection with trading activities for the Fund’s investments in Commodity Futures Trading Commission regulated investments.

The Fund bears other transaction costs related to the futures commission merchants capital requirements on a monthly basis. The Sponsor

pays all of the routine operational, administrative and other ordinary expenses of the Fund, generally as determined by the Sponsor, including

but not limited to, fees and expenses of the Administrator, Sub-Administrator, Custodian, Distributor, Transfer Agent, licensors, accounting

and audit fees and expenses, tax preparation expenses, legal fees, ongoing SEC registration fees, individual Schedule K-1 preparation

and mailing fees, and report preparation and mailing expenses. The Fund pays all of its non-recurring and unusual fees and expenses, if

any, as determined by the Sponsor. Non-recurring and unusual fees and expenses are unexpected or unusual in nature, such as legal claims

and liabilities and litigation costs or indemnification or other unanticipated expenses. Extraordinary fees and expenses also include

material expenses which are not currently anticipated obligations of the Fund. Routine operational, administrative and other ordinary

expenses are not deemed extraordinary expenses.

The Sponsor has the ability to elect to pay certain

expenses on behalf of the Fund or waive the management fee. This election is subject to change by the Sponsor, at its discretion. Expenses

paid by the Sponsor or the Prior Sponsor are, if applicable, presented as waived expenses in the statements of operations for the Fund:

| Three Months Ended March 31, 2024 |

$ |

— |

|

| Three Months Ended March 31, 2023 |

|

70,570 |

|

For the three months ending March 31, 2024, the Sponsor

did not waive expenses. For the three months ending March 31, 2023 the Prior Sponsor waived the above expenses.

Administrator

The

Fund employs Tidal ETF Services LLC as the Fund’s administrator (the “Administrator”). In turn, the Administrator has

engaged U.S. Bancorp Fund Services, LLC, doing business as U.S. Bank Global Fund Services (“Global Fund Services”) to act

as sub-administrator. The Administrator is a wholly-owned subsidiary of Sponsor. The Administrator also assists the Fund and the Sponsor

with certain functions and duties relating to marketing, which include the following: marketing and sales strategy and marketing related

services.

Cash

Custodian, Registrar, Transfer Agent, Fund Sub-Administrator

In

its capacity as the Fund’s custodian, the Custodian, currently U.S. Bank, N.A., holds the Fund’s securities, cash and/or cash

equivalents pursuant to a custodial agreement. Global Fund Services, an entity affiliated with U.S. Bank, N.A., is the registrar and transfer

agent for the Fund’s Shares. In addition, Global Fund Services also serves as sub-administrator for the Fund, performing certain

sub-administrative, and accounting services, and support in preparing certain SEC and CFTC reports on behalf of the Fund.

Bitcoin

Custodian

Holdings

of the Fund also includes bitcoin. Such investments are held by BitGo Trust Company, Inc. (the “Bitcoin Custodian”)

on behalf of the Fund. The Bitcoin Custodian will keep custody of all of the Fund’s bitcoin in a multi-layer, multi-party cold storage

or similarly secure technology. The Bitcoin Custodian is responsible for safekeeping passwords, keys or phrases that allow transfers of

digital assets (“Security Factors”) safe, secure and confidential. 100% of the private keys will be held in cold storage.

The Bitcoin Custodian will establish the Bitcoin Accounts on the Bitcoin Network solely for the Fund. The Bitcoin Custodian will follow

valid instructions given by the Sponsor to use the Fund’s Security Factors to effect transfers to and from the Bitcoin Accounts.

The Fund’s bitcoin will be held in segregated wallets and will not be commingled with the assets of other customers. The Bitcoin

Custodian has an insurance policy that covers, at least partially, risks such as the loss of client assets held in cold storage, including

from employee collusion or fraud, physical loss including theft, damage of key material, security breach or hack, and fraudulent transfer.

Marketing

Agent

The

Fund employs Foreside Fund Services, LLC, a wholly-owned subsidiary of Foreside Financial Group, LLC (d/b/a ACA Group) as the Marketing

Agent for the Fund. The Marketing Agent Agreement among the Marketing Agent and the Trust calls for the Marketing Agent to work with the

Custodian in connection with the receipt and processing of orders for Creation Baskets and Redemption Baskets and the review and approval

of all Fund sales literature and advertising material. The Marketing Agent’s principal business address is Three Canal Plaza, Suite

100, Portland, Maine 04101. The Marketing Agent is a broker-dealer registered with the SEC and a member of FINRA.

Support

Agent

The

Administrator also assists the Fund and the Sponsor with certain functions and duties relating to administration and marketing, which

include the following: marketing and sales strategy and marketing related services.

Digital

Asset Adviser

Hashdex

Asset Management Ltd. (“Hashdex” or the “Digital Asset Adviser”) is a Cayman Islands investment manager (and an

Exempt Reporting Advisor under SEC rules) that specializes in, among other things, the management, research, investment analysis and other

investment support services of funds and ETFs with investment strategies involving bitcoin and other crypto assets. As Digital Asset Adviser,

Hashdex is responsible for providing the Sponsor and the Administrator with research and analysis regarding bitcoin and bitcoin markets

for use in the operation and marketing of the Fund. Hashdex has no role in maintaining, calculating or publishing the Benchmark. Hashdex

also has no responsibility for the investment or management of the Fund’s portfolio or for the overall performance or operation

of the Fund.

Note 3 – Transactions

with Affiliates

The Trust has no directors, officers or employees and is managed by the Sponsor. The Administrator

is a wholly-owned subsidiary of the Sponsor.

Note 4 – Financial

Highlights

The following table presents per unit performance

data and other supplemental financial data for the three months ended March 31, 2024. This information has been derived from information

presented in the financial statements and is presented with total expenses gross of expenses waived by the Sponsor and with total expenses

net of expenses waived by the Sponsor, as appropriate.

HASHDEX BITCOIN ETF

FINANCIAL HIGHLIGHTS

| | |

Three Months Ended | | |

Three Months Ended | |

| | |

March 31, 2024 | | |

March 31, 2023 | |

| Per Share Operation Performance | |

| | |

| |

| Net asset value at beginning of period | |

$ | 50.74 | | |

$ | 21.40 | |

| Income (loss) from investment operations: | |

| | | |

| | |

| Investment income | |

| 0.62 | | |

| 0.27 | |

| Net realized and unrealized gain (loss) on cryptocurrency futures contracts | |

| 29.91 | | |

| 15.16 | |

| Total expenses | |

| (0.20 | ) | |

| (0.07 | ) |

| Net increase (decrease) in net asset value | |

| 30.33 | | |

| 15.36 | |

| Net asset value at end of period | |

$ | 81.07 | | |

$ | 36.76 | |

| Total Return | |

| 59.78 | % | |

| 71.79 | % |

| Ratios to Average Net Assets (Annualized) | |

| | | |

| | |

| Total expenses | |

| 1.30 | % | |

| 20.48 | % |

| Total expenses, net | |

| 1.30 | % | |

| 0.94 | % |

| Net investment income (loss) | |

| 2.67 | % | |

| 2.78 | % |

Note 5 – Merger

with Hashdex Bitcoin Futures ETF

As reported by the Tidal Commodities Trust I on a

Form 8-K filed with the Securities and Exchange Commission on January 3, 2024 (File No. 001-41900), the Fund completed the successful

acquisition by merger (the “Merger”) of the Hashdex Bitcoin Futures ETF, a series of the Teucrium Commodity Trust (the “Acquired

Fund”).

Under the terms of the Merger, each shareholder of

the Acquired Fund received one share of the Fund for every one share of the Acquired Fund held on January 3, 2024 based on the net asset

value per share of the Fund being equal to the net asset value per share of the Acquired Fund determined immediately prior to the Merger

closing. The share price used for the delivery of shares of the Acquired Fund was the net asset value per share of the Acquired Fund determined

after the close of business of NYSE Arca on January 2, 2024. Consequently, the Merger resulted in a one-for-one exchange of shares between

the Acquired Fund and the Fund. Upon the Merger closing, the Fund acquired all the assets of the Acquired Fund and assumed all the liabilities

of the Acquired Fund. Upon the Merger closing, all of the Acquired Fund’s shares were cancelled and the Acquired Fund was liquidated.

The sponsor of the Acquired Fund, Teucrium Trading,

LLC (“Teucrium”), is not receiving any compensation dependent on the consummation of the Merger. Pursuant to a certain Amended

and Restated ’33 Act Fund Platform Support Agreement, as amended (the “Support Agreement”) among Tidal, Administrator,

Hashdex, and Teucrium, Tidal has agreed to provide Teucrium after the Merger with a monthly amount equal to seven percent (7%)

of the Management Fee paid to Tidal from the Fund; provided, however, that such fee will never be less than 0.04% of monthly average

net assets of the Fund (“Teucrium Compensation”). Any payment of the Teucrium Compensation will be made from the resources

of Tidal and not from the assets of the Fund.

On January 3, 2024, the Fund issued 50,000 shares

at net asset value of $2,708,819 for 50,000 shares the Acquired Fund, representing $2,708,819 of net assets.

The combined net assets and shares outstanding of the Fund immediately after the Merger were $2,708,819 and 50,000, respectively,

representing a net asset value per share of $54.18.

Note 6 – Conversion

to Spot Bitcoin ETF

On March 26, 2024, the Sponsor announced the renaming

of the Fund from the Hashdex Bitcoin Futures ETF to the Hashdex Bitcoin ETF. The renaming of the Fund corresponds to its completion of

the conversion of its investment strategy to allow the Fund to provide spot bitcoin holdings and its tracking of a new benchmark index

effective March 27, 2024.

The Fund’s new benchmark index is the Nasdaq

Bitcoin Reference Price - Settlement (NQBTCS), which better reflects the Fund’s new strategy of direct bitcoin investment. Going

forward and under normal market conditions, the Fund’s investment policy is to maximize its holdings of physical bitcoin such that

it is expected that at least 95% of the Fund’s assets will be invested in spot bitcoin. Up to 5% of the Fund’s remaining

assets may be invested in CME-traded bitcoin futures contracts and in cash and cash equivalents.

Note 7 – Subsequent

Events

In preparing

these financial statements, Management has evaluated the financial statements for the three months ended March 31, 2024 for subsequent

events through the date of this filing and noted no material events requiring either recognition through the date of the filing or disclosure

herein for the Fund.

HASHDEX

BITCOIN ETF

STATEMENTS

OF ASSETS AND LIABILITIES

| | |

March

31, 2024 (Unaudited) | |

December

31, 2023 |

| Assets | |

| |

|

| Investments

(Cost $10,578,023) | |

$ | 10,837,413 | | |

$ | — | |

| Cash

and cash equivalents | |

| 237,786 | | |

| 1,867,663 | |

| Interest

receivable | |

| 59,811 | | |

| 10,297 | |

| Equity

in trading accounts: | |

| | | |

| | |

| Cryptocurrency

futures contracts | |

| 14,259 | | |

| 129,519 | |

| Due

from broker | |

| 233,247 | | |

| 582,908 | |

| Total

equity in trading accounts | |

| 247,506 | | |

| 712,427 | |

| Total

assets | |

$ | 11,382,516 | | |

$ | 2,590,387 | |

| | |

| | | |

| | |

| Liabilities | |

| | | |

| | |

| Management

fee payable to Sponsor | |

| 19,207 | | |

| 2,053 | |

| Equity

in trading accounts: | |

| | | |

| | |

| Cryptocurrency

futures contracts | |

| 13,475 | | |

| 51,376 | |

| Total

liabilities | |

$ | 32,682 | | |

$ | 53,429 | |

| | |

| | | |

| | |

| Net

assets | |

$ | 11,349,834 | | |

$ | 2,536,958 | |

| | |

| | | |

| | |

| Shares

authorized | |

| 140,000 | | |

| 50,000 | |

| | |

| | | |

| | |

| Net

asset value per share | |

$ | 81.07 | | |

$ | 50.74 | |

| | |

| | | |

| | |

| Market

value per share | |

$ | 81.50 | | |

$ | 50.73 | |

The

accompanying notes are an integral part of these financial statements.

HASHDEX

BITCOIN ETF

SCHEDULE

OF INVESTMENTS

March

31, 2024

(Unaudited)

| Description: Assets | |

Fair Value | | |

Percentage of

Net Assets | | |

Shares | |

| | |

| | |

| | |

| |

| Cryptocurrency | |

| | | |

| | | |

| | |

| Bitcoin | |

$ | 10,837,413 | | |

| 95.49 | % | |

| 15,331 | |

| Total Cryptocurrency (cost $10,578,023) | |

$ | 10,837,413 | | |

| 95.49 | % | |

| | |

| | |

| | | |

| | | |

| | |

| Cash equivalents | |

| | | |

| | | |

| | |

| Money market funds | |

| | | |

| | | |

| | |

| First American Government Obligations Fund - Class X, 5.29% | |

$ | 237,786 | | |

| 2.10 | % | |

| 237,786 | |

| Total Cash Equivalents (cost $237,786) | |

$ | 237,786 | | |

| 2.10 | % | |

| | |

| Description: Assets | |

Fair Value | | |

Percentage of

Net Assets | | |

Notional Amount

(Long Exposure) | |

| | |

| | |

| | |

| |

| Cryptocurrency futures contracts | |

| | | |

| | | |

| | |

| United States CME Bitcoin Futures contracts | |

| | | |

| | | |

| | |

| CME Micro Bitcoin Futures April 2024 (21 contracts) | |

$ | 14,259 | | |

| 0.13 | % | |

$ | 150,213 | |

| Total cryptocurrency futures contracts | |

$ | 14,259 | | |

| 0.13 | % | |

$ | 150,213 | |

| Description: Liabilities | |

| | | |

| | | |

| | |

| | |

| | | |

| | | |

| | |

| Cryptocurrency futures contracts | |

| | | |

| | | |

| | |

| United States CME Bitcoin Futures contracts | |

| | | |

| | | |

| | |

| CME Bitcoin Futures April 2024 (1 contract) | |

$ | 13,475 | | |

| 0.12 | % | |

$ | 357,650 | |

| Total cryptocurrency futures contracts | |

$ | 13,475 | | |

| 0.12 | % | |

$ | 357,650 | |

The

accompanying notes are an integral part of these financial statements.

HASHDEX

BITCOIN ETF

(FORMERLY

HASHDEX BITCOIN FUTURES ETF)

SCHEDULE

OF INVESTMENTS

December

31, 2023

| Description: Assets | |

Yield | | |

Fair Value

| | |

Percentage of Net

Assets | | |

Shares | |

| | |

| | |

| | |

| | |

| |

| Cash equivalents | |

| | | |

| | | |

| | | |

| | |

| Money market funds | |

| | | |

| | | |

| | | |

| | |

| U.S. Bank Deposit Account (cost $1,867,663) | |

| 5.27 | % | |

$ | 1,867,663 | | |

| 73.62 | % | |

| 1,867,663 | |

| Total Cash Equivalents (cost $1,867,663) | |

| | | |

$ | 1,867,663 | | |

| 73.62 | % | |

| | |

|

|

|

|

| |

Fair Value | | |

Percentage of

Net Assets | | |

Notional

Amount (Long Exposure) | |

| Description: Assets |

|

|

|

| |

| | |

| | |

| |

| |

|

|

|

| |

| | |

| | |

| |

| Cryptocurrency futures contracts |

|

|

|

| |

| | | |

| | | |

| | |

| United States CME Bitcoin Futures contracts |

|

|

|

| |

| | | |

| | | |

| | |

| CME Bitcoin Futures JAN 24 (6 contracts) |

|

|

|

| |

$ | 129,519 | | |

| 5.11 | % | |

$ | 1,274,500 | |

| Total cryptocurrency futures contracts |

|

|

|

| |

$ | 129,519 | | |

| 5.11 | % | |

$ | 1,274,500 | |

| Description: Liabilities |

|

|

|

| |

| | | |

| | | |

| | |

| |

|

|

|

| |

| | | |

| | | |

| | |

| Cryptocurrency futures contracts |

|

|

|

| |

| | | |

| | | |

| | |

| United States CME Bitcoin Futures contracts |

|

|

|

| |

| | | |

| | | |

| | |

| CME Bitcoin Futures FEB 24 (6 contracts) |

|

|

|

| |

| 51,376 | | |

| 2.03 | % | |

$ | 1,288,500 | |