The hurricane season continues in the Atlantic Ocean, forcing the National Hurricane Center to issue an alert for residents of the northern Gulf Coast given the projected path of Tropical Storm Sally. Tropical Storm Sally could hit somewhere along the Mississippi Coast by Tuesday morning. France is once again facing Yellow Vests protests in Paris and a number of other French cities. Finally, heavy showers and thunderstorms have hit Ankara (Turkey) and California’s fire activity elevated, destroying over 4,000 structures.

The stock market roller coaster is back, with the money flowing from the FAANG stocks to other sectors. Curiously, traders’ decision to adjust derivative positions wasn’t unanimous, thus not spreading to other risk assets, neither creating a shift to safe havens.

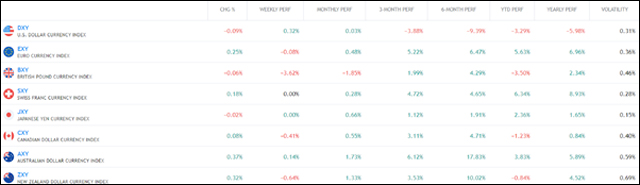

In the case of the euro, at the last policy meeting, European Central Bank President Christine Lagarde said the euro appreciation must be monitored for its impact on prices, but she didn’t signal any pressing need to adjust monetary policy. As a result, the currency continued its rally against the dollar for a third straight session. On the other hand, it should be mentioned that coronavirus cases in Europe continue to grow, but the number of deaths remained low.

Talking about policy meetings, the Bank of Canada announced it will leave rates unchanged at 0.25% and will continue to buy at least CAD 5 billion per week of government bonds. The ECB, on the other hand, left rates unchanged at 0% and Christine Lagarde said they aren’t targeting the value of the Euro, but will continue to buy 1.35 trillion Euros worth of debt through June 2021. Besides that, ECB revised its GDP forecasts higher as well as inflation to 0.9% next year and 1.1% in 2022.

Brexit talks resumed but the confidence in reaching the divorce agreement is looking less and less likely. The UK presented draft legislation that upends some of the Brexit Withdrawal Agreement, and the EU didn’t like it. In this context, investment bank Morgan Stanley has increased the risk of Britain and the European Union flopping onto World Trade Organization terms to 40% from 25%. The Pound meanwhile continues to fall.

In terms of macroeconomic data, The Consumer Price Index for All Urban Consumers (CPI-U) increased 0.4 percent in August on a seasonally adjusted basis after rising 0.6 percent in July. Over the last 12 months, the all items index increased 1.3 percent before seasonal adjustment. The number of Americans applying for unemployment benefits, on the other hand, stayed at 884,000.

Finally, the oil market fell as investors expect a global economy to continue suffering from the COVID-19 and the rising production levels of the OPEC+ group, and the possibility of more lockdowns. The inventory levels in the US from the American Petroleum Institute (API) and the Department of Energy (DoE) were slightly higher than expectations but not enough to inspire such a sell-off.

Chart of the week

Macroeconomic Data & Events

This week, we will keep an eye on the Fed, BOJ, and the BOE meetings. The FED will announce its decision on the interest rate, the BOJ will let the market know if any change to the monetary policy will be applied, meanwhile, the Bank of England will announce its decision on interest rates and monetary policy. Besides that, we will know industrial output and import, export prices, retail sales, business inventories, homebuilder sentiment, weekly jobless claims, housing starts, business conditions, and consumer sentiment data. On Friday, the Federal Reserve Bank of St. Louis President James Bullard speaks.

September 14: China house price index (Aug), Japan industrial output (Final, Jul), Euro area industrial output (Jul), and China vehicle sales.

September 15: RBA meeting minutes, China fixed-asset investment, industrial output, retail sales, unemployment rate (Aug), UK employment change (Jun), jobless rate, average earnings (Jul), France and Italy inflation (Final, Aug), Euro area and Germany ZEW survey (Sep), NY Empire State manufacturing index (Sep) and Japan trade (Aug).

September 16: Australia new home sales (Aug), UK inflation, retail price index (Aug), Euro area trade balance (Jul), US retail sales (Aug), business inventories (Jul), and US NAHB housing market index (Sep).

September 17: Australia jobless rate, employment change (Aug), BoJ interest rate decision, BoE interest rate decision, Hong Kong unemployment rate (Aug), Italy trade balance (Jul), Euro area inflation (Final, Aug), US housing starts, building permits (Aug), Philly Fed manufacturing index (Sep), jobless claims (12-Sep) Japan inflation (Aug).

September 18: Germany wholesale prices (Aug), UK retail sales (Aug), Russia GDP (Aug), interest rate decision US current account (Q2), and University of Michigan consumer confidence survey.