As filed with the United States Securities

and Exchange Commission on May 10, 2024

Registration No. 333-272488

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

POST EFFECTIVE AMENDMENT NO. 1

TO

FORM S-1

REGISTRATION STATEMENT UNDER THE SECURITIES

ACT OF 1933

TENON

MEDICAL, inc.

(Exact name of registrant as specified in its charter)

| Delaware | | 3841 | | 45-5574718 |

(State or Other Jurisdiction of

Incorporation or Organization) | | (Primary Standard Industrial

Classification Code Number) | | (I.R.S. Employer

Identification No.) |

104 Cooper Court

Los Gatos, CA 95032

(408) 649-5760

(Address, including zip code, and telephone number,

including area code,

of registrant’s principal executive offices)

Steven M. Foster

Chief Executive Officer and President

Tenon Medical, Inc.

104 Cooper Court

Los Gatos, CA 95032

(408) 649-5760

(Name, address, including zip code, and telephone

number, including area code, of agent for service)

Copies to:

Ross D. Carmel, Esq.

Jeffrey P. Wofford, Esq.

Sichenzia Ross Ference Carmel LLP

1185 Avenue of the Americas, 31st Floor

New York, New York 10036

Telephone: (212) 930-9700

Approximate date of commencement of proposed sale

to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this

Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box. ☒

If this Form is filed to register additional securities

for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration

statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed

pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of

the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed

pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of

the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant

is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large

accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Securities

Exchange Act of 1934.

| Large accelerated filer ☐ | Accelerated filer ☐ |

| Non-accelerated filer ☒ | Smaller reporting company ☒ |

| | Emerging growth company ☒ |

If an emerging growth company, indicate by check

mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting

standards provided to Section 7(a)(2)(B) of the Securities Act. ☐

The Registrant hereby amends this Registration

Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment

which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities

Act of 1933 or until the Registration Statement shall become effective on such date as the Commission acting pursuant to said Section

8(a), may determine.

EXPLANATORY

NOTE

This Post-Effective Amendment No. 1 on Form S-1

to the Registration Statement on Form S-1 (Registration No. 333-272488) (the “Original Registration Statement”), which was

declared effective by the Commission on June 13, 2023, is being filed to serve as a Section 10(a)(3) update to the Original

Registration Statement and to make certain other updates to the prospectus that forms a part of this Post-Effective Amendment. Pursuant

to Rule 416 under the Securities Act, there are also being registered such securities that may be issued because of events such as

recapitalizations, stock dividends, stock splits and reverse stock splits, and similar transactions. All applicable registration fees

were paid at the time of the filing of the Original Registration Statement.

The information in

this prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the

Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and is not soliciting an offer

to buy these securities in any state or other jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION,

DATED MAY 10, 2024

PRELIMINARY PROSPECTUS

2,000,000 Shares of Common Stock Underlying

the Warrants

Tenon Medical, Inc.

This prospectus relates to the issuance by Tenon

Medical, Inc. (the “Company”) of 2,000,000 shares of common stock, par value $0.001 per share upon the exercise of warrants

(the “Tradeable Warrants”) issued in a public offering on June 16, 2023.

On June 16, 2023, we completed our public offering

of 1,000,000 units (the “Units”), each Unit consisting of one share of our common stock, $0.001 par value per share, and two

warrants (each, a “Warrant”), each to purchase one share of our common stock, at an offering price of $5.60 per Unit. The

Units had no stand-alone rights and were not certificated or issued as stand-alone securities. Each Tradeable Warrant was immediately

exercisable on the date of issuance at an exercise price of $5.60 per share (100% of the offering price per Unit) and expires five years

from the date of issuance.

We

will receive the proceeds from any exercise of the Warrants, the Placement Agent Warrants and Representative’s Warrants for cash.

See “Use of Proceeds” on page 45 of this prospectus. On May 9, 2024, the last reported sale price of (i) our common

stock on Nasdaq was $0.8432 per share, and (ii) our Tradeable Warrants on Nasdaq was $0.0341 per Tradeable Warrant.

Our common stock and Tradeable Warrants are listed

on The Nasdaq Capital Market under the symbols “TNON” and “TNONW,” respectively.

Investing in our securities involves a high

degree of risk. See “Risk Factors” beginning on page 10 of this prospectus for a discussion of information that should

be considered in connection with an investment in our securities.

Neither the Securities and Exchange Commission

(“SEC”) nor any state securities commission has approved or disapproved of these securities or determined if this prospectus

is truthful or complete. Any representation to the contrary is a criminal offense.

We are an “emerging growth company”

as that term is used in the Jumpstart Our Business Startups Act of 2012, and we have elected to comply with certain reduced public company

reporting requirements.

The date of this prospectus is ______________,

2024.

TABLE OF CONTENTS

You should rely only on the information contained

in this prospectus or any prospectus supplement or amendment. Neither we, nor the placement agent, have authorized any other person to

provide you with information that is different from, or adds to, that contained in this prospectus. If anyone provides you with different

or inconsistent information, you should not rely on it. Neither we nor the placement agent take responsibility for, and can provide no

assurance as to the reliability of, any other information that others may give you. You should assume that the information contained in

this prospectus, or any free writing prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery

of this prospectus or of any sale of our common stock. Our business, financial condition, results of operations and prospects may have

changed since that date. We are not making an offer of any securities in any jurisdiction in which such offer is unlawful.

No action is being taken in any jurisdiction outside

the United States to permit a public offering of our securities or possession or distribution of this prospectus in that jurisdiction.

Persons who come into possession of this prospectus in jurisdictions outside the United States are required to inform themselves about

and to observe any restrictions as to this public offering and the distribution of this prospectus applicable to that jurisdiction.

ABOUT

THIS PROSPECTUS

Throughout this prospectus, unless otherwise designated

or the context suggests otherwise,

| ● | all

references to the “Tenon,” the “Company,” the “registrant,” “we,” “our,”

or “us” in this prospectus mean Tenon Medical, Inc.; |

| ● | “year”

or “fiscal year” means the year ending December 31st; and |

| ● | all

dollar or $ references, when used in this prospectus, refer to United States dollars. |

Market

Data

Market data and certain industry data and forecasts

used throughout this prospectus were obtained from internal company surveys, market research, consultant surveys, publicly available information,

reports of governmental agencies and industry publications and surveys. Industry surveys, publications, consultant surveys and forecasts

generally state that the information contained therein has been obtained from sources believed to be reliable, but the accuracy and completeness

of such information is not guaranteed. To our knowledge, certain third-party industry data that includes projections for future periods

does not consider the effects of any future coronavirus outbreaks or any geopolitical conflicts. Accordingly, those third-party projections

may be overstated and should not be given undue weight. We have not independently verified any of the data from third party sources, nor

have we ascertained the underlying economic assumptions relied upon therein. Similarly, internal surveys, industry forecasts and market

research, which we believe to be reliable based on our management’s knowledge of the industry, have not been independently verified.

Forecasts are particularly likely to be inaccurate, especially over long periods of time. In addition, we do not necessarily know what

assumptions regarding general economic growth were used in preparing the forecasts we cite. Statements as to our market position are based

on the most currently available data. While we are not aware of any misstatements regarding the industry data presented in this prospectus,

our estimates involve risks and uncertainties and are subject to change based on various factors, including those discussed under the

heading “Risk Factors” in this prospectus. We are, however, liable for the information in the prospectus related to

the market and industry data.

PROSPECTUS

SUMMARY

This summary provides a brief overview of the

key aspects of our business and our securities. The reader should read the entire prospectus carefully, especially the risks of investing

in our common stock discussed under “Risk Factors.” Some of the statements contained in this prospectus, including statements

under “Summary” and “Risk Factors” as well as those noted in the documents incorporated herein by reference, are

forward-looking statements and may involve a number of risks and uncertainties. Our actual results and future events may differ significantly

based upon a number of factors. The reader should not put undue reliance on the forward-looking statements in this document, which speak

only as of the date on the cover of this prospectus.

Unless the context otherwise requires, references

in this prospectus to “Tenon,” “Tenon Medical,” “the Company,” “our Company,” “we,”

“us” and “our” refer to Tenon Medical, Inc.

Introduction

Tenon Medical, Inc. (the “Company”),

was incorporated in the State of Delaware on June 19, 2012 and was headquartered in San Ramon, California until June 2021 when it relocated

to Los Gatos, California. The Company is a medical device company that has developed The Catamaran™ SI Joint Fusion System (“The

CATAMARAN System”) that offers a novel, less invasive approach to the sacroiliac joint (the “SI Joint”) using a single,

robust, titanium implant for treatment of the most common types of SI Joint disorders that cause lower back pain. The Company received

U.S. Food and Drug Administration (“FDA”) clearance in 2018 for The CATAMARAN System and is currently focused on the US market.

Since the national launch of The CATAMARAN System in October 2022, the Company is focused on three commercial opportunities: 1) Primary

SI Joint procedures, 2) Revision procedures of failed SI Joint implants and 3) SI Joint fusion adjunct to a spine fusion construct.

The Opportunity

We estimate that over 30 million American adults

have chronic lower back pain. Published clinical studies have shown that 15% to 30% of all chronic lower back pain is associated with

the SI-Joint. For patients whose chronic lower back pain stems from the Sacroiliac Joint (“SI-Joint”), our experience in both

clinical trials and commercial settings indicates the system to be introduced by Tenon could be beneficial for patients who are properly

diagnosed and screened for surgery by trained healthcare providers.

In 2019, approximately 475,000 patients in the

United States were estimated to have received an aesthetic injection to temporarily alleviate pain emanating from the SI-Joint and/or

to diagnose SI-Joint pain. Additionally, several non-surgical technologies have been introduced in the past 10 years to address patients

who do not respond to conservative options, including systemic oral medications, opioids, physical therapy and injection therapy.

To date, the penetration of a surgical solution

for this market has been relatively low (5-7%). We believe this is due to complex surgical approaches and suboptimal implant design of

existing options. The penetration of this market with an optimized surgical solution is Tenon’s focus.

We believe the SI-Joint is the last major joint

to be successfully addressed by the spine implant industry. Studies have shown that disability resulting from disease of the SI-Joint

is comparable to the disability associated with a number of other serious spine conditions, such as knee and hip arthritis and degenerative

disc disease, each of which has surgical solutions where an implant is used, and a multi-billion-dollar market exists.

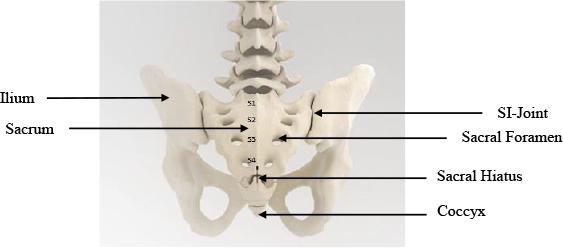

The SI-Joint

The SI-Joint is a strong weight bearing synovial

joint situated between the lumbar spine and the pelvis and is aligned along the longitudinal load bearing axis of the human spine when

in an upright posture. It functions as a force transfer conduit where it transfers axial loads bi-directionally from the spine to the

pelvis and lower extremities and allows forces to be transmitted from the extremities to the spine. It also provides load sharing between

the hip and spine to contribute towards attenuation of impact shock and stress from activities of daily living.

The SI-Joint is a relatively immobile joint that

connects the sacrum (the spinal segment that is attached to the base of the lumbar spine at the L5 vertebra) and the ilium of the pelvis.

Each SI-Joint is approximately 2-4mm wide and irregularly shaped.

Motion of the SI-Joint features vertical shear

and rotation. Although the rotational forces about the SI-Joint are relatively low, repetitive motions created by daily activities such

as walking, jogging, twisting at the hips, and jumping can increase the stresses on the SI-Joint. If the SI-Joint is compromised through

injury or degeneration, the load bearing and motion restraints from the surrounding anatomical structures of the SI-Joint will be compromised

resulting in abnormal stress transfers across the joint to these structures, thereby further augmenting the degenerative cascade of the

SI-Joint. Eventual pain and cessation of an individual’s normal activities due to a painful and unstable SI-Joint have led to an

increase in the recent development of SI-Joint stabilization devices.

Non-Surgical Treatment of Sacroiliac Joint Disease

Several non-surgical treatments exist

for suspected sacroiliac joint pain. These conservative steps often provide desired relief for the patient. Non-surgical treatments include:

| |

● |

Drug Therapy: including opiates and non-steroidal anti-inflammatory medications. |

| |

● |

Physical Therapy: which can involve exercises as well as massage. |

| |

● |

Intra-Articular Injections of Steroid Medications: which are typically performed by physicians who specialize in pain treatment or anesthesia. |

| |

● |

Radiofrequency Ablation: or the cauterizing of the lateral branches of the sacral nerve roots. |

When conservative steps fail to deliver sustained

pain relief and return to quality of life, specific diagnostic protocols are utilized to explore if a surgical option should be considered.

Diagnosis

Historically, diagnosing pain from the SI-Joint

was not routinely a focus of orthopedic or neurosurgery training during medical school or residency programs. Due to its invasiveness,

post-operative pain, and muscle disruption along with a difficult procedure overall, the open SI-Joint fusion procedure was rarely taught

in these settings.

The emergence of various SI-Joint surgical technologies

has generated a renewed discussion of SI-Joint issues. Of particular focus is the diagnostic protocol utilized to properly select patients

for SI-Joint surgery. Patients with low back pain typically start with primary care physicians who often refer to pain specialists. Here,

the patient will undergo traditional physical therapy combined with oral medications (anti-inflammatory, narcotic, etc.). If the patient

fails to respond to these steps the pain specialist may move to therapeutic injections of the SI-Joint. These injections may serve to

lessen inflammation to the point that the patient is satisfied. However, the impact from these injections is often transient. In this

case the patient is often referred to a clinician to determine if the patient may be a candidate for surgical intervention. A series of

provocative tests in clinic, combined with a specific injection protocol to isolate the SI-Joint as the pain generator is then utilized

to confirm the need for surgical intervention. Published literature has shown this technique to be a very effective step to determine

the best treatment to alleviate pain.

Limitations of Existing Treatment Options

Surgical fixation and fusion of the SI-Joint with

an open surgical technique was first reported in 1908, with further reports in the 1920s. The open procedure uses plates and screws, requires

a 6 to 12-inch incision and is extremely invasive. Due to the high invasiveness and associated morbidity, the use

of this procedure is limited to cases involving significant trauma, tumor, etc.

Less invasive surgical options along with implant

design began to emerge over the past 15 years. These options feature a variety of approaches and implant designs and have been met with

varying degrees of adoption. Lack of a standard and accepted diagnostic approach, complexity of approach, high morbidity of approach,

abnormally high complication rates and inability to radiographically confirm fusion have all been cited as reasons for low adoption of

these technologies.

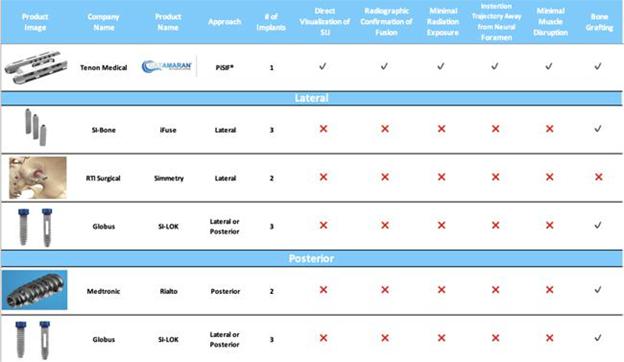

Commercialization

Tenon initiated its national commercial launch

of The CATAMARAN System in October 2022 to address what we believe is a large market opportunity. The CATAMARAN System includes instruments

and implants designed to prepare and fixate the SI-Joint for fusion. The CATAMARAN System is distinct from other competitive offerings

in the following ways:

| |

● |

Transfixes the SI-Joint |

| |

● |

Inferior / Posterior Sacroiliac Fusion Approach |

| |

● |

Reduced Approach Morbidity |

| |

● |

Direct And Visualized Approach to the SI-Joint |

| |

● |

Single Implant Technique |

| |

● |

Insertion Trajectory Away from the Neural Foramen |

| |

● |

Insertion Trajectory Away from Major Lateral Vascular Structures |

| |

● |

Autologous Bone Grafting in the Ilium, Sacrum and Bridge |

| |

● |

Radiographic Confirmation of Bridging Bone Fusion of the SI-Joint |

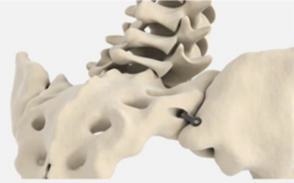

The fixation device and its key features are shown

below:

|

|

Key Features

“Pontoon” in the ilium

“Pontoon” in the sacrum

“Pontoons and Bridge” filled with autologous bone from

drilling process

Leading edge osteotome creates defect and facilitates ease of insertion

|

The CATAMARAN System is a singular implant designed

with several proprietary components which allow for it to be explicitly formatted to address the SI-Joint with a single approach and implant.

This contrasts with several competitive implant systems that require multiple approach pathways and implants to achieve fixation. In addition,

the inferior-posterior approach is designed to be direct to the joint and through limited anatomical structures which may minimize the

morbidity of the approach. The implant features a patented dual pontoon open cell design which enables the clinician to pack the pontoons

with the patient’s own autologous bone designed to promote bone fusion across the joint. The CATAMARAN System is designed specially

to resist vertical shear and rotation of the joint in which it was implanted, helping stabilize the joint in preparation for eventual

fusion.

The instruments we have developed are proprietary

to The CATAMARAN System and specifically designed to transfix the SI-Joint and facilitate an inferior-posterior approach that is unique

to the system.

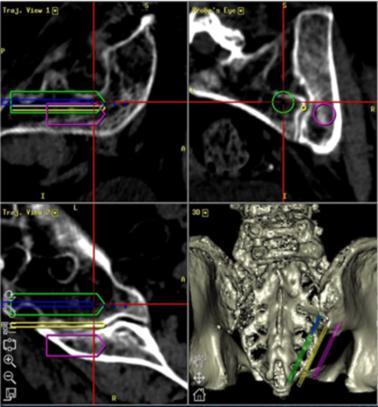

Tenon also has developed a proprietary 2D placement

protocol as well as a protocol for 3D navigation utilizing the latest techniques in spine surgery. These Tenon advancements are intended

to further enhance the safety of the procedure and encourage more physicians to adopt the procedure.

In October 2022, we received Institutional Review

Board (“IRB”) approval from WCG IRB for two separate Tenon-sponsored post market clinical studies of The CATAMARAN System.

The approval by WCG allows designated Catamaran study centers to begin recruiting and enrolling patients into the clinical studies. The

first approval from WCG IRB will support a prospective, multi-center, single arm post market study that will evaluate the clinical outcomes

of patients with sacroiliac joint disruptions or degenerative sacroiliitis treated with The CATAMARAN System. Patients will be followed

out to 24 months assessing various patient reported outcomes, radiographic assessments, and adverse events. The second prospective, multi-center,

Catamaran study will evaluate 6-to-12-month radiographic outcomes to assess fusion of patients that have already undergone treatment with

The CATAMARAN System. In addition, retrospective and prospective clinical outcomes will be evaluated. We anticipate completing enrollment

by the end of the second quarter of 2024.

For a description of the challenges, we face and

the risks and limitations that could harm our prospects, see “Summary Risk Factors” and “Risk Factors.”

Recent Developments

Nasdaq Notice of Failure to Comply with

Continued Listing Standards

On May 7, 2024, we received a letter from

the Nasdaq Listing Qualifications Staff of The Nasdaq Stock Market LLC (“Nasdaq”) stating that for the 30 consecutive business

day period between March 25, 2024 and May 6, 2024, our common stock had not maintained a minimum closing bid price of $1.00 per share

required for continued listing on The Nasdaq Capital Market pursuant to Nasdaq Listing Rule 5550(a)(2) (the “Bid Price Rule”).

Pursuant to Nasdaq Listing Rule 5810(c)(3)(A), we were provided an initial period of 180 calendar days, or until November 4, 2024 (the

“Compliance Period”), to regain compliance with the Bid Price Rule.

To regain compliance, the closing bid price

of our common stock must meet or exceed $1.00 per share for a minimum of 10 consecutive trading days, unless extended by Nasdaq

under Nasdaq Rule 5810(c)(3)(H), prior to November 4, 2024.

If we do not regain compliance with the Bid

Price Rule by November 4, 2024, we may be eligible for an additional 180-day period to regain compliance if we meet all of the other

Nasdaq listing criteria and if Nasdaq does not believe we will not be able to regain compliance within such 180-day period. If we cannot

regain compliance during the Compliance Period or any subsequently granted compliance period, our common stock will be subject to delisting.

Our common stock continues to be listed on

The Nasdaq Capital Market under the symbol “TNON”. We are currently evaluating our options for regaining compliance.

The notice from Nasdaq has no immediate effect

on the listing or trading of our common stock on The Nasdaq Capital Market and does not affect our business, operations or reporting

requirements with the SEC.

Exchange Offer

On April 8, 2024, we launched a one-time stock

option exchange program (the “Option Exchange”) pursuant to which eligible participants were able to exchange outstanding

stock options for a lesser amount of new restricted stock units (“RSUs”). Our executive officers, non-employee directors

and consultants were eligible to participate in the Option Exchange. Employees, non-employee directors and consultants received one RSU

for every two shares of our common stock underlying the eligible options surrendered. This “exchange ratio” (2-for-1) was

applied on a grant-by-grant basis. The Option Exchange expired on May 6, 2024 at 11:59 p.m., Eastern Time. At that time, stock options

to purchase 83,391 shares of our common stock were surrendered and 41,698 new RSUs were issued under the Tenon Medical, Inc. 2022 Equity

Incentive Plan (the “2022 Plan”).

2024 Series A Offering

On February 20, 2024, we entered into a Securities

Purchase Agreement (the “Series A Purchase Agreement”) with certain investors (the “Series A Investors”), pursuant

to which the Company agreed to sell, issue and deliver to the Series A Investors, in a private placement offering (the “Series

A Offering”), a total of 172,239 shares of the Company’s Series A Preferred Stock (the “Series A Preferred Stock”)

and warrants (the “Series A Warrants”) to purchase 258,374 shares of common stock, par value $0.001 per share, of the Company

(“Common Stock”) at an exercise price equal to $1.2705 per share for an aggregate offering price of $2,605,000. Under the

Series A Purchase Agreement, each Series A Investor paid $15.125 for each share of Series A Preferred Stock. In addition, each investor

received Series A Warrants to purchase a number of shares of our common stock equal to 15% of the number of shares of our common stock

underlying the shares of Series A Preferred Stock purchased by such investor. In connection with the offering of the Series A Preferred

Stock the Company exchanged the Notes (as defined below) for 84,729 shares of Series A Preferred Stock and Series A Warrants to purchase

157,094 shares of our common stock. There are a total of 256,968 shares of Series A Preferred Stock outstanding as of May 10, 2024.

2023 Note Offering

On November 21, 2023, we entered into securities purchase agreements

with certain investors (the “Note Investors”), pursuant to which we agreed to sell, issue and deliver to the Note Investors,

in a private placement offering (the “Note Offering”), a total of $1,250,000 in secured notes (the “Notes”) and

warrants (the “Note Warrants”) to purchase 45,000 shares of our common stock at an exercise price equal to $1.94 per share.

The Company received $1,125,000 from the Note Offering after payment of investor expenses.

The Notes beared an interest rate of 10% per annum

with a default rate of 12% per annum and have a maturity date of November 21, 2024. All principal and accrued interest is payable at maturity.

However, at any time during the term of the Notes, the principal amount of the Notes together with all accrued and unpaid principal thereon

(the “Prepayment Amount”) may be paid in full, but not in part, by us. The Prepayment Amount may be paid by us in cash or

by the issuance to the Investors in shares of Series A Preferred Stock. The Notes are secured by a first priority security interest in

all of our assets. The principal balance of the Note, including any accrued interest, was paid in full in shares of Series A Preferred

Stock on February 20, 2024 and the security interest has been released.

The Note Warrants expire five (5) years from the

issuance date of the Note Warrants. The Note Warrants contain a “cashless exercise” feature and contain anti-dilution rights

on subsequent issuances of equity or equity equivalents.

November 2023 Stock Split

On November 2, 2023, the Company effected a 1-for-10

reverse stock split (the “2023 Reverse Stock Split”) by filing an amendment to the Company’s Second Amended and Restated

Certificate of Incorporation, as amended, with the Delaware Secretary of State. The 2023 Reverse Stock Split combined every ten shares

of our common stock issued and outstanding immediately prior to effecting the 2023 Reverse Stock Split into one share of common stock.

No fractional shares were issued in connection with the 2023 Reverse Stock Split. All historical share and per share amounts reflected

throughout this document have been adjusted to reflect the 2022 Reverse Stock Split and the 2023 Reverse Stock Split. The authorized number

of shares and the par value per share of the Company’s common stock were not affected by the 2023 Reverse Stock Split.

Summary Risk Factors

Our business is subject to numerous risks and

uncertainties, any one of which could materially adversely affect our results of operations, financial condition or business. These risks

include, but are not limited to, those listed below. This list is not complete, and should be read together with the section titled “Risk

Factors” below:

| ● | We

have incurred losses in the past, our financial statements have been prepared on a going concern basis and we may be unable to achieve

or sustain profitability in the future; |

| ● | Practice

trends or other factors, including the COVID-19 pandemic, may cause procedures to shift from the hospital environment to ambulatory surgical

centers (“ASCs”), where pressure on the prices of our products is generally more acute; |

| ● | If

hospitals, clinicians, and other healthcare providers are unable to obtain and maintain coverage and reimbursement from third-party payors

for procedures performed using our products, adoption of our products may be delayed, and it is unlikely that they will gain further

acceptance; |

| ● | We

may not be able to convince physicians that The CATAMARAN System is an attractive alternative to our competitors’ products and

that our procedure is an attractive alternative to existing surgical and non-surgical treatments of the SI-Joint; |

| ● | Clinicians

and payors may not find our clinical evidence to be compelling, which could limit our sales, and ongoing and future research may prove

our products to be less safe and effective than initially anticipated; |

| |

● |

Pricing pressure from our competitors, changes in third-party coverage and reimbursement, healthcare provider consolidation, payor consolidation and the proliferation of “physician-owned distributorships” may impact our ability to sell our product at prices necessary to support our current business strategies; |

| |

● |

We operate in a very competitive business environment and if we are unable to compete successfully against our existing or potential competitors, our sales and operating results may be negatively affected and we may not grow; |

| |

● |

We currently manufacture (through third parties) and sell products used in a single procedure, which could negatively affect our operations and financial condition; |

| |

● |

Our sales volumes and our operating results may fluctuate over the course of the year; |

| ● | Various

factors outside our direct control may adversely affect manufacturing and distribution of our product; |

| ● | We

are dependent on a limited number of contract manufacturers, some of them single-source and some of them in single locations, for our

product, and the loss of any of these contract manufacturers, or their inability to provide us with an adequate supply of products in

a timely and cost-effective manner, could materially adversely affect our business; |

| ● | As

our sales grow, our contract manufacturers may encounter problems or delays in the manufacturing of our product or fail to meet certain

regulatory requirements which could result in an adverse effect on our business and financial results; |

| ● | The

size and future growth in the market for the SI-Joint fixation market have not been established based on market reports and our estimates

are based on our own review and analysis of public information and may be smaller than we estimate, possibly materially. In addition,

our estimates of cost savings to the economy and healthcare system as a result of The CATAMARAN System procedure are based on our internal

estimates and market research and could also be smaller than we estimate, possibly materially. If our estimates and projections overestimate

the size of this market or cost savings, our sales growth may be adversely affected; |

| ● | If

we experience significant disruptions in our information technology systems, our business, results of operations, and financial condition

could be adversely affected; |

| ● | We

may seek to grow our business through acquisitions of or investments in new or complementary businesses, products or technologies, and

the failure to manage acquisitions or investments, or the failure to integrate them with our existing business, could have a material

adverse effect on us; |

| ● | We

may enter into collaborations, in-licensing arrangements, joint ventures, strategic alliances, or partnerships with third-parties that

may not result in the development of commercially viable products or the generation of significant future revenue; |

| ● | We

are increasingly dependent on information technology, and our systems and infrastructure face certain risks, including cybersecurity

and data leakage risks; |

| ● | Geopolitical

conditions, including trade disputes and direct or indirect acts of war or terrorism, could have an adverse effect on our operations

and financial results; |

| ● | Inflation

may adversely affect our operations and financial results; |

| |

● |

We and our contract manufacturers are subject to extensive governmental regulation both in the United States and abroad, and failure to comply with applicable requirements could cause our business to suffer; |

| |

● |

Our employees, independent contractors, consultants, contract manufacturers, and our independent sales representatives may engage in misconduct or other improper activities, relating to regulatory standards and requirements; |

| |

● |

We are subject to environmental laws and regulations that can impose significant costs and expose us to potential financial liabilities; |

| |

● |

Our ability to protect our intellectual property and proprietary technology is uncertain; |

| |

● |

We may not be able to protect our intellectual property rights throughout the world; |

| |

● |

The sale or issuance of our common stock to Lincoln Park may cause dilution and the sale of the shares of common stock acquired by Lincoln Park, or the perception that such sales may occur, could cause the price of our common stock to fall; and |

| |

● |

Our management will have broad discretion over the use of the net proceeds from our sale of shares of common stock to Lincoln Park, and you may not agree with how we use the proceeds and the proceeds may not be invested successfully. |

Corporate Information

Our principal executive offices are located at

104 Cooper Court, Los Gatos, CA 95032. Our website address is www.tenonmed.com. The information included on our website is not

part of this prospectus.

Implications of Being an Emerging Growth

Company and a Smaller Reporting Company

We are an “emerging growth company,”

as defined in the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”). We will remain an emerging growth company

until the earlier of (i) the last day of the fiscal year following the fifth anniversary of the date of the first sale of our common stock

pursuant to an effective registration statement under the Securities Act; (ii) the last day of the fiscal year in which we have total

annual gross revenues of $1.235 billion or more; (iii) the date on which we have issued more than $1 billion in nonconvertible debt during

the previous three years; or (iv) the date on which we are deemed to be a large accelerated filer under applicable SEC rules. We expect

that we will remain an emerging growth company for the foreseeable future, but cannot retain our emerging growth company status indefinitely

and will no longer qualify as an emerging growth company on or before the last day of the fiscal year following the fifth anniversary

of the date of the first sale of our common stock pursuant to an effective registration statement under the Securities Act. For so long

as we remain an emerging growth company, we are permitted and intend to rely on exemptions from specified disclosure requirements that

are applicable to other public companies that are not emerging growth companies.

These exemptions include:

| |

● |

being permitted to provide only two years of audited financial statements, in addition to any required unaudited interim financial statements, with correspondingly reduced “Management’s Discussion and Analysis of Financial Condition and Results of Operations” disclosure; |

| |

● |

not being required to comply with the requirement of auditor attestation of our internal controls over financial reporting; |

| ● | not

being required to comply with any requirement that may be adopted by the Public Company Accounting Oversight Board regarding mandatory

audit firm rotation or a supplement to the auditor’s report providing additional information about the audit and the financial

statements; |

| ● | reduced

disclosure obligations regarding executive compensation; and |

| ● | not

being required to hold a nonbinding advisory vote on executive compensation and shareholder approval of any golden parachute payments

not previously approved. |

We have taken advantage of certain reduced reporting

requirements in this prospectus. Accordingly, the information contained herein may be different than the information you receive from

other public companies in which you hold stock.

An emerging growth company can take advantage

of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act for complying with new or revised accounting standards.

This allows an emerging growth company to delay the adoption of certain accounting standards until those standards would otherwise apply

to private companies. We have irrevocably elected to avail ourselves of this extended transition period and, as a result, we will not

be required to adopt new or revised accounting standards on the dates on which adoption of such standards is required for other public

reporting companies.

We are also a “smaller reporting company”

as defined in Rule 12b-2 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and have elected to take

advantage of certain of the scaled disclosure available for smaller reporting companies.

SUMMARY

OF THE OFFERING

| Securities

offered |

|

2,000,000

shares of common stock issuable upon the exercise of the Tradeable Warrants, subject to adjustment as set forth therein. The Warrants

will be immediately exercisable and will expire on the fifth anniversary of the original issuance date. |

| |

|

|

| Use of Proceeds |

|

We will receive proceeds from the exercise of the Tradeable Warrants for cash. We intend to use any net proceeds from the exercise of the Tradeable Warrants for general corporate purposes. See “Use of Proceeds” on page 45 of this prospectus. |

| |

|

|

| Listing |

|

Our common stock and Tradeable Warrants trade on The Nasdaq Capital Market under the symbols “TNON” and “TNONW,” respectively. |

| |

|

|

| Risk Factors |

|

See “Risk Factors” on page 10 and other information included in this prospectus for a discussion of factors to consider carefully before deciding to invest in shares of our common stock. |

| |

|

|

| Transfer Agent and Warrant Agent |

|

Vstock Transfer, LLC. |

RISK

FACTORS

Our business is subject to many risks and uncertainties,

which may affect our future financial performance. If any of the events or circumstances described below occur, our business and financial

performance could be adversely affected, our actual results could differ materially from our expectations, and the price of our stock

could decline. The risks and uncertainties discussed below are not the only ones we face. There may be additional risks and uncertainties

not currently known to us or that we currently do not believe are material that may adversely affect our business and financial performance.

You should carefully consider the risks described below, together with all other information included in this prospectus including our

financial statements and related notes, before making an investment decision. The statements contained in this prospectus that are not

historic facts are forward-looking statements that are subject to risks and uncertainties that could cause actual results to differ materially

from those set forth in or implied by forward-looking statements. If any of the following risks actually occurs, our business, financial

condition or results of operations could be harmed. In that case, the trading price of our common stock could decline, and investors in

our securities may lose all or part of their investment.

Risks Related to Our Business and Operations

We have incurred losses in the past, our

financial statements have been prepared on a going concern basis and we may be unable to achieve or sustain profitability in the future.

To date, we have financed our operations primarily

through the issuance of public and private equity and convertible notes. We have devoted substantially all of our resources to research

and development, creating the infrastructure for a publicly traded medical device company, preparing for our national commercial launch,

and clinical and regulatory matters for our products. There can be no assurances that we will be able to generate sufficient revenue from

our existing products or from any future product candidates to transition to profitability and generate consistent positive cash flows.

We expect that our operating expenses will continue to increase as we continue to build our commercial infrastructure, develop, enhance,

and commercialize our existing and new products and incur additional operating and reporting costs associated with being a public company.

As a result, we expect to continue to incur operating losses for the foreseeable future and may never achieve profitability. Furthermore,

even if we do achieve profitability, we may not be able to sustain or increase profitability on an ongoing basis. If we do not achieve

profitability, it will be more difficult for us to finance our business and accomplish our strategic objectives.

Our recurring losses from operations and negative

cash flows raise substantial doubt about our ability to continue as a going concern. As a result, our independent registered public accounting

firm included an explanatory paragraph in its report on our financial statements for the fiscal year ended, December 31, 2023, describing

the existence of substantial doubt about our ability to continue as a going concern. Our expected future capital requirements may depend

on many factors including expanding our clinician base, increasing the rate at which we train clinicians, the number of additional clinical

papers initiated, and the timing and extent of spending on the development of our technology to increase our product offerings. We may

need additional funding to fund our operations but additional funds may not be available to us on acceptable terms on a timely basis,

if at all. We may seek funds through borrowings or through additional rounds of financing, including private or public equity or debt

offerings. If we raise additional funds by issuing equity securities, our stockholders may experience dilution. Any future debt financing

into which we enter may impose upon us additional covenants that restrict our operations, including limitations on our ability to incur

liens or additional debt, pay dividends, repurchase our common stock, make certain investments, and engage in certain merger, consolidation

or asset sale transactions. Any future debt financing or additional equity that we raise may contain terms that are not favorable to us

or our stockholders. Furthermore, we cannot be certain that additional funding will be available on acceptable terms, if at all. If we

are unable to raise additional capital or generate sufficient cash from operations to adequately fund our operations, we will need to

curtail planned activities to reduce costs, which will likely harm our ability to execute on our business plan and continue operations.

Practice trends or other factors, including

the COVID-19 pandemic, may cause procedures to shift from the hospital environment to ambulatory surgical centers (“ASCs”),

where pressure on the prices of our products is generally more acute.

To protect health care professionals involved

in surgical care and their patients, we anticipate that more outpatient eligible procedures will be performed in ASCs during the COVID-19

pandemic, and as its acuity declines and the healthcare system returns to a more normalized state. Since patients do not stay overnight

in ASCs and COVID-19 patients would not otherwise be treated in ASCs, it is likely that the ASC will be viewed as a safer site of service

for patients and health care providers, where the risk of transmission of COVID-19 can be more effectively controlled. Because ASC facility

fee reimbursement is typically less than facility fee reimbursement for hospitals, we typically experience more pressure on the pricing

of our products by ASCs than by hospitals, and the average price for which we sell our products to ASCs is less than the average prices

we charge to hospitals. An accelerated shift of procedures using our products to ASCs as a result of any future COVID-19 outbreak could

adversely impact the average selling prices of our products and our revenues could suffer as a result.

If hospitals, clinicians, and other healthcare

providers are unable to obtain coverage and reimbursement from third-party payors for procedures performed using our products, adoption

of our products may be delayed, and it is unlikely that they will gain further acceptance.

Growing sales of our product depends on the availability

of adequate coverage and reimbursement from third-party payors, including government programs such as Medicare and Medicaid, private insurance

plans, and managed care programs. Hospitals, clinicians, and other healthcare providers that purchase or use medical devices generally

rely on third-party payors to pay for all or part of the costs and fees associated with the procedures performed with these devices.

Adequate coverage and reimbursement for procedures

performed with our products is central to the acceptance of our current and future products. We may be unable to sell our products on

a profitable basis if third-party payors deny coverage, continue to deny coverage or reduce their current levels of payment, or if our

costs for the product increase faster than increases in reimbursement levels.

Many private payors refer to coverage decisions

and payment amounts determined by the Centers for Medicare and Medicaid Services, or CMS, which administers the Medicare program, as guidelines

for setting their coverage and reimbursement policies. By June 30, 2016, all Medicare Administrative Contractors were regularly reimbursing

for minimally invasive and/or open SI-Joint fusion. Private payors that do not follow the Medicare guidelines may adopt different coverage

and reimbursement policies for procedures performed with our products. Private commercial payors have been slower to adopt positive coverage

policies for minimally invasive and/or open SI-Joint fusion, and many private payors still have policies that treat the procedure as experimental

or investigational and do not regularly reimburse for the procedure. Future action by CMS or third-party payors may further reduce the

availability of payments to physicians, outpatient surgery centers, and/or hospitals for procedures using our products.

The healthcare industry in the United States has

experienced a trend toward cost containment as government and private insurers seek to control healthcare costs. Payors are imposing lower

payment rates and negotiating reduced contract rates with service providers and being increasingly selective about the technologies and

procedures they choose to cover. There can be no guarantee that we will be able to provide the scientific and clinical data necessary

to overcome these policies. Payors may adopt policies in the future restricting access to medical technologies like ours and/or the procedures

performed using such technologies. Therefore, we cannot be certain that the procedures performed with each of our products will be reimbursed.

There can be no guarantee that, should we introduce additional products in the future, payors will cover those products or the procedures

in which they are used.

If the reimbursement provided by third-party

payors to hospitals, clinicians, and other healthcare providers for procedures performed using our products is insufficient, adoption

and use of our products and the prices paid for our implants may decline.

When a Tenon procedure utilizing The CATAMARAN

System is performed, both the clinician and the healthcare facility, a hospital (inpatient or outpatient clinic), submit claims for reimbursement

to the patient’s insurer. Generally, the facility obtains a lump sum payment, or facility fee, for SI-Joint fusions. Our products

are purchased by the facility, along with other supplies used in the procedure. The facility must also pay for its own fixed costs of

operation, including certain operating room personnel involved in the procedure, and other medical services care. If these costs exceed

the facility reimbursement, the facility’s managers may discourage or restrict clinicians from performing the procedure in the facility

or using certain technologies, such as The CATAMARAN System, to perform the procedure.

The Medicare 2022 national average hospital inpatient

payment ranges from approximately $25,000 to approximately $59,000 depending on the procedural approach and the presence of Complication

and Comorbidity (CC)/Major Complication and Comorbidity (MCC).

The Medicare 2022 national average hospital outpatient

clinic payment is $21,897. We believe that insurer payments to facilities are generally adequate for these facilities to offer The CATAMARAN

System. However, there can be no guarantee that these facility payments will not decline in the future. The number of procedures

performed, and the prices paid for our implants may in the future decline if payments to facilities for SI-Joint fusions decline.

Clinicians are reimbursed separately for their

professional time and effort to perform a surgical procedure. Depending on the surgical approach, the incision size, type and extent of

imaging guidance, indication for procedure, and the insurer, The CATAMARAN System procedure may be reported by the clinician using any

one of the applicable following CPT® codes 27279, 27280, 27299. The Medicare 2022 national average payment for CPT® 27279 is $807

and $1,325 for 27280. CPT® 27299 has no national valuation. Clinicians, however, can present a crosswalk to another procedure believed

to be fairly equivalent and/or comparison to a code for which there is an existing valuation.

For some governmental programs, such as Medicaid,

coverage and reimbursement differ from state to state, and some state Medicaid programs may not pay an adequate amount for the procedures

performed with our products, if any payment is made at all. Similar to Medicaid, many private payors’ coverage and payment may differ

from one payer to another as well.

We believe that some clinicians view the current

Medicare reimbursement amount as insufficient for the procedure, given the work effort involved with the procedure, including the time

to diagnose the patient and obtain prior authorization from the patient’s health insurer when necessary. Many private payors require

extensive documentation of a multi-step diagnosis before authorizing SI-Joint fusion for a patient. We believe that some private payors

apply their own coverage policies and criteria inconsistently, and clinicians may experience difficulties in securing approval and coverage

for sacroiliac fusion procedures. Additionally, many private payors limit coverage for open SI-Joint fusion to trauma, tumors or extensive

spine fusion procedures involving multiple levels. The perception by physicians that the reimbursement for SI-Joint fusion is insufficient

to compensate them for the work required, including diagnosis, documentation, obtaining payor approval for the procedure, and burden on

their office staff, may negatively affect the number of procedures performed and may therefore impede the growth of our revenues or cause

them to decline.

We may not be able to convince physicians

that The CATAMARAN System is an attractive alternative to our competitors’ products and that our procedure is an attractive alternative

to existing surgical and non-surgical treatments of the SI-Joint.

Clinicians play the primary role in determining

the course of treatment in consultation with their patients and, ultimately, the product that will be used to treat a patient. In order

for us to sell The CATAMARAN System successfully, we must convince clinicians through education and training that treatment with The CATAMARAN

System is beneficial, safe, and cost-effective for patients as compared to our competitors’ products. If we are not successful in

convincing clinicians of the merits of The CATAMARAN System, they may not use our product, and we will be unable to increase our sales

and achieve or grow profitability.

Historically, most spine clinicians did not include

SI-Joint pain in their diagnostic work-up because they did not have an adequate surgical procedure to perform for patients diagnosed with

the condition. As a result, some patients with lower back pain resulting from SI-Joint dysfunction are misdiagnosed. We believe that educating

clinicians and other healthcare professionals about the clinical merits and patient benefits of The CATAMARAN System is an important element

of our growth. If we fail to effectively educate clinicians and other medical professionals, they may not include a SI-Joint evaluation

as part of their diagnosis and, as a result, those patients may continue to receive unnecessary or only non-surgical treatment.

Clinicians may also hesitate to change their medical treatment practices

for other reasons, including the following:

| |

● |

lack of experience with minimally invasive procedures; |

| |

● |

perceived liability risks generally associated with the use of new products and procedures; |

| |

● |

costs associated with the purchase of new products; and |

| |

● |

time commitment that may be required for training. |

Furthermore, we believe clinicians may not widely

adopt The CATAMARAN System unless they determine, based on experience, clinical data, and published peer-reviewed publications, that surgical

intervention provides benefits or is an attractive alternative to non-surgical treatments of SI-Joint dysfunction. In addition, we believe

support of our products relies heavily on long-term data showing the benefits of using our product. If we are unable to provide that data,

clinicians may not use our product. In such circumstances, we may not achieve expected sales and may be unable to achieve profitability.

Clinicians and payors may not find our clinical

evidence to be compelling, which could limit our sales, and on-going and future research may prove our product to be less safe and effective

than initially anticipated.

All of the component parts of The CATAMARAN System

have either received premarket clearance under Section 510(k) of the U.S. federal Food, Drug, and Cosmetic Act, or FDCA, or are exempt

from premarket review. The 510(k) clearance process of the U.S. Food and Drug Administration, or FDA, requires us to document that our

product is “substantially equivalent” to another 510(k) -cleared product. The 510(k) process is shorter and typically requires

the submission of less supporting documentation than other FDA approval processes, such as a premarket approval, or PMA, and does not

usually require pre-clinical or clinical studies. Additionally, to date, we have not been required to complete clinical studies in connection

with the sale of our product. For these reasons, clinicians may be slow to adopt our product, third-party payors may be slow to provide

coverage, and we may be subject to greater regulatory and product liability risks. Further, future patient studies or clinical experience

may indicate that treatment with our product does not improve patient outcomes. Such results would slow the adoption of our product by

clinicians, significantly reduce our ability to achieve expected sales, and could prevent us from achieving profitability. Moreover, if

future results and experience indicate that our product causes unexpected or serious complications or other unforeseen negative effects,

we could be subject to mandatory product recalls, suspension, or withdrawal of FDA clearance.

Pricing pressure from our competitors, changes

in third-party coverage and reimbursement, healthcare provider consolidation, payor consolidation and the proliferation of “physician-owned

distributorships” may impact our ability to sell our product at prices necessary to support our current business strategies.

If competitive forces drive down the prices we

are able to charge for our product, our profit margins will shrink, which will adversely affect our ability to invest in and grow our

business. The SI-Joint fusion market has attracted numerous new companies and technologies. As a result of this increased competition,

we believe there will be continued and increased pricing pressure, resulting in lower gross margins, with respect to our product.

Even to the extent our product and procedures

using our product are currently covered and reimbursed by third-party private and public payors, adverse changes in coverage and reimbursement

policies that affect our product, discounts, and number of implants used may also drive our prices down and harm our ability to market

and sell our product.

We are unable to predict what changes will be

made to the reimbursement methodologies used by third-party payors. We cannot be certain that under current and future payment systems,

in which healthcare providers may be reimbursed a set amount based on the type of procedure performed, such as those utilized by Medicare

and in many privately managed care systems, the cost of our product will be justified and incorporated into the overall cost of the procedure.

In addition, to the extent there is a shift from inpatient setting to outpatient settings, we may experience pricing pressure and a reduction

in the number of The CATAMARAN System procedures performed.

Consolidation in the healthcare industry, including

both third-party payors and healthcare providers, could lead to demands for price concessions or to the exclusion of some suppliers from

certain of our markets, which could have an adverse effect on our business, results of operations, or financial condition. Because healthcare

costs have risen significantly over the past several years, numerous initiatives and reforms initiated by legislators, regulators, and

third-party payors to curb these costs have resulted in a consolidation trend in the healthcare industry to aggregate purchasing power.

As the healthcare industry consolidates, competition to provide products and services to industry participants has become and will continue

to become more intense. This in turn has resulted and will likely continue to result in greater pricing pressures and the exclusion of

certain suppliers from important market segments as group purchasing organizations, independent delivery networks, and large single accounts

continue to use their market power to consolidate purchasing decisions for hospitals. We expect that market demand, government regulation,

third-party coverage, and reimbursement policies and societal pressures will continue to change the worldwide healthcare industry, resulting

in further business consolidations and alliances among our customers, which may reduce competition, exert further downward pressure on

the price of our product, and adversely impact our business, results of operations, or financial condition. As we continue to expand into

international markets, we will face similar risks relating to adverse changes in coverage and reimbursement procedures and policies in

those markets.

We operate in a very competitive business

environment and if we are unable to compete successfully against our existing or potential competitors, our sales and operating results

may be negatively affected and we may not grow.

The CATAMARAN System is subject to intense competition.

Many of our competitors are major medical device companies that have substantially greater financial, technical, and marketing resources

than we do, and they may succeed in developing products that would render our product obsolete or non-competitive. In addition, many of

these competitors have significantly longer operating histories and more established reputations than we do. Our field is intensely competitive,

subject to rapid change and highly sensitive to the introduction of new products or other market activities of industry participants.

Our ability to compete successfully will depend on our ability to develop proprietary products that reach the market in a timely manner,

receive adequate coverage and reimbursement from third-party payors, and are safer, less invasive, and more effective than alternatives

available for similar purposes as demonstrated in peer-reviewed clinical publications. Because of the size of the potential market, we

anticipate that other companies will dedicate significant resources to developing competing products.

In the United States, we believe that our primary

competitors are currently SI-bone, Inc., Globus Medical, Inc., Medtronic plc, XTant Medical Holdings, Inc., and RTI Surgical, Inc. At

any time, these or other industry participants may develop alternative treatments, products or procedures for the treatment of the SI-Joint

that compete directly or indirectly with our product. If alternative treatments are, or are perceived to be, superior to our product,

sales of our product and our results of operations could be negatively affected. Some of our larger competitors are either publicly traded

or divisions or subsidiaries of publicly traded companies. These competitors may enjoy several competitive advantages over us, including:

| |

● |

greater financial, human, and other resources for product research and development, sales and marketing, and legal matters; |

| |

● |

significantly greater name recognition; |

| |

● |

established relationships with clinicians, hospitals, and other healthcare providers; |

| |

● |

large and established sales and marketing and distribution networks; |

| |

● |

greater experience in obtaining and maintaining domestic and international regulatory clearances or approvals, or CE Certificates of Conformity for products and product enhancements; |

| |

● |

more expansive portfolios of intellectual property rights; and |

| |

● |

greater ability to cross-sell their products or to incentivize hospitals or clinicians to use their products. |

New participants have increasingly entered the

medical device industry. Many of these new competitors specialize in a specific product or focus on a particular market segment, making

it more difficult for us to increase our overall market position. The frequent introduction by competitors of products that are or claim

to be superior to our product or that are alternatives to our existing or planned products may make it difficult to differentiate the

benefits of our product over competing products. In addition, the entry of multiple new products and competitors may lead some of our

competitors to employ pricing strategies that could adversely affect the pricing of our product and pricing in the market generally.

As a result, without the timely introduction of

new products and enhancements, our product may become obsolete over time. If we are unable to develop innovative new products, maintain

competitive pricing, and offer products that clinicians and other physicians perceive to be as reliable as those of our competitors, our

sales or margins could decrease, thereby harming our business.

We currently manufacture (through third

parties) and sell products used in a single procedure, which could negatively affect our operations and financial condition.

Presently we do not sell any products other than

The CATAMARAN System and related tools and instruments. Therefore, we are solely dependent on widespread market adoption of The CATAMARAN

System and we will continue to be dependent on the success of this single product for the foreseeable future. There can be no assurance

that The CATAMARAN System will gain a substantial degree of market acceptance among clinicians, patients or healthcare providers. Our

failure to successfully increase sales of The CATAMARAN System or any other event impeding our ability to sell The CATAMARAN System would

result in a material adverse effect on our results of operations, financial condition and continuing operations.

We have a limited operating history and

may face difficulties encountered by early-stage companies in new and rapidly evolving markets.

Even though we were formed in 2012 we have just

built the infrastructure necessary to commercially launch The CATAMARAN System. Accordingly, we have a limited operating history upon

which to base an evaluation of our business and prospects. In assessing our prospects, you must consider the risks and difficulties frequently

encountered by early-stage companies in new and rapidly evolving markets, particularly companies engaged in the development and sales

of medical devices. These risks include our inability to:

| |

● |

obtain coverage by third-party, private, and government payors; |

| |

● |

establish and increase awareness of our brand and strengthen customer loyalty; |

| |

● |

attract and retain qualified personnel; |

| |

● |

find and develop relationships with contract manufacturers that can manufacture the necessary volume of product; |

| |

● |

manage our independent sales representatives to achieve our sales growth objectives; |

| |

● |

commercialize new products and enhance our existing product; |

| |

● |

manage rapidly changing and expanding operations; |

| |

● |

implement and successfully execute our business and marketing strategy; |

| |

● |

respond effectively to competitive pressures and developments. |

We can also be negatively affected by general

economic conditions. Because of our limited operating history, we may not have insight into trends that could emerge and negatively affect

our business. As a result of these or other risks, our business strategy might not be successful.

Our sales volumes and our operating results

may fluctuate over the course of the year.

Since we had our first sales in April 2021 and

our official national launch commenced in October 2022, we have limited history with respect to how rapidly adoption of The CATAMARAN

System will occur. Sales growth could be slower than we have projected. Our sales and results of operations will be affected by numerous

factors, including, among other things:

| |

● |

payor coverage and reimbursement; |

| |

● |

maintaining our training schedule with clinicians; |

| |

● |

the number of procedures performed in the quarter and our ability to drive increased sales of our product; |

| |

● |

our ability to identify and sign-up independent sales representatives and their performance; |

| |

● |

pricing pressure applicable to our product, including adverse third-party coverage and reimbursement outcomes; |

| |

● |

timing of new product offerings, acquisitions, licenses or other significant events by us or our competitors; |

| |

● |

our ability to find and develop relationships with contract manufacturers and their ability to timely provide us with an adequate supply of products; |

| |

● |

the evolving product offerings of our competitors; |

| |

● |

the demand for, and pricing of, our product and the products of our competitors; |

| |

● |

factors that may affect the sale of our product, including seasonality and budgets of our customers; |

| |

● |

ability of clinicians to do our procedure given possible COVID restrictions; |

| |

● |

interruption in the manufacturing or distribution of our product; |

| |

● |

the effect of competing technological, industry and market developments; |

| |

● |

our ability to expand the geographic reach of our sales and marketing efforts; |

| |

● |

the costs of maintaining adequate insurance coverage, including product liability insurance; |

| |

● |

the availability and cost of components and materials needed by our contract manufacturers; |

| |

● |

the number of selling days in the quarter; and |

| |

● |

impairment and other special charges. |

Some of the products we may seek to develop and

introduce in the future will require FDA clearance or approval before commercialization in the United States. As a result, it will be

difficult for us to forecast demand for these products with any degree of certainty. In addition, we will be increasing our operating

expenses as we expand our commercial capabilities. Accordingly, we may experience significant, unanticipated quarterly losses. If our

quarterly or annual operating results fall below the expectations of investors or securities analysts, the price of our common stock could

decline substantially. Furthermore, any quarterly or annual fluctuations in our operating results may, in turn, cause the price of our

common stock to fluctuate substantially. Quarterly comparisons of our financial results may not always be meaningful and should not be

relied upon as an indication of our future performance.

If we do not successfully implement our

business strategy, our business and results of operations will be adversely affected.

Our business strategy was based on assumptions

about the market that might prove wrong. We believe that various demographics and industry-specific trends will help drive growth in the

market and our business, but these demographics and trends have been and will continue to be uncertain. Actual demand for our product

could differ materially from projected demand if our assumptions regarding these factors prove to be incorrect or do not materialize,

or if alternative treatments to those offered by our product gains widespread acceptance. Also, our strategy of focusing exclusively on

the SI-Joint market may limit our ability to grow. In addition, in order to increase our sales, we will need to identify and contract

with independent sales representatives in existing and new regions as well, and in the future, commercialize new products. Moreover, we

may decide to alter or discontinue aspects of our business strategy and may adopt different strategies due to business or competitive

factors not currently foreseen, such as new medical technologies that would make our product obsolete. Any failure to implement our business

strategy may adversely affect our business, results of operations, and financial condition.

Our business could suffer if we lose the

services of key members of our senior management, key advisors or personnel.

We are dependent upon the continued services of

key members of our senior management and a number of key advisors and personnel. The loss of members of our senior management team, key

advisors or personnel, or our inability to attract or retain other qualified personnel or advisors, could have a material adverse effect

on our business, results of operations, and financial condition. We do not maintain “key person” insurance for any of our

executives or employees. In addition, several of the members of our executive management team are not subject to non-competition agreements

that restrict their ability to compete with us. Accordingly, the adverse effect resulting from the loss of certain executives could be

compounded by our inability to prevent them from competing with us.

Various factors outside our direct control

may adversely affect manufacturing and distribution of our product.

The manufacture and distribution of our product

is challenging. Changes that our contract manufacturers may make outside the purview of our direct control can have an impact on our processes,

quality of our product, and the successful delivery of products to our customers. Mistakes and mishandling are not uncommon and can affect

supply and delivery. Some of these risks include:

| |

● |

failure to manufacture in compliance with the required regulatory standards; |

| |

● |

the cost and availability of components and supplies required by our contract manufacturers to manufacture our products; |

| |

● |

delays in analytical results or failure of analytical techniques that we will depend on for quality control and release of products; |

| |

● |

natural disasters, labor disputes, financial distress, raw material availability, issues with facilities and equipment, or other forms of disruption to business operations affecting our manufacturers or their suppliers; and |

| |

● |

latent defects that may become apparent after products have been released and that may result in a recall of such products. |

If any of these risks were to materialize, our

ability to provide our product to customers on a timely basis would be adversely impacted.

We are dependent on a limited number of