false

0001162896

0001162896

2023-11-17

2023-11-17

iso4217:USD

xbrli:shares

iso4217:USD

xbrli:shares

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM

8-K

CURRENT

REPORT

Pursuant

to Section 13 or 15(d) of

the

Securities Exchange Act of 1934

Date

of Report (Date of earliest event reported): November 17, 2023

Prairie

Operating Co.

(Exact

name of registrant as specified in its charter)

| Delaware |

|

000-33383 |

|

98-0357690 |

(State

or other jurisdiction

of

incorporation) |

|

(Commission

File

Number) |

|

(IRS

Employer

Identification

No.) |

602

Sawyer Street, Suite 710

Houston,

TX |

|

77007 |

| (Address

of principal executive offices) |

|

(Zip

Code) |

Registrant’s

telephone number, including area code: (713) 424-4247

N/A

(Former

Name or Former Address, If Changed Since Last Report)

Check

the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under

any of the following provisions (see General Instruction A.2. below):

| ☐ |

Written

communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| |

|

| ☐ |

Soliciting

material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| |

|

| ☐ |

Pre-commencement

communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| |

|

| ☐ |

Pre-commencement

communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Securities

registered pursuant to Section 12(b) of the Act:

| Title

of each class |

|

Trading

Symbol(s) |

|

Name

of each exchange on which registered |

| None |

|

N/A |

|

N/A |

Indicate

by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405)

or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2).

Emerging

Growth Company ☐

If

an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Item

8.01 Other Events.

In

connection with the filing of an amendment to the registration statement on Form S-1 (File No. 333-272743) registering the resale of

certain securities, Prairie Operating Co. (the “Company”) is filing (i) updated business disclosures set forth in Exhibit

99.1 and (ii) updated risk factors set forth in Exhibit 99.2 and to update the disclosures previously provided in the Company’s

Annual Report on Form 10-K for the year ended December 31, 2022 and Quarterly Report on Form 10-Q for the quarterly period ended September

30, 2023, each as filed with the Securities and Exchange Commission, and as may be further updated by the Company’s Current Reports

on Form 8-K. In addition, the Company is filing as Exhibit 99.3 Unaudited Pro Forma Condensed Combined Financial Information as of and

for the nine months ended September 30, 2023 and for the year ended December 31, 2022. The disclosures set forth in Exhibits 99.1, 99.2

and 99.3 are incorporated herein by reference.

Item

9.01 Financial Statements and Exhibits.

(d)

Exhibits

SIGNATURES

Pursuant

to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by

the undersigned hereunto duly authorized.

| |

Prairie

Operating Co. |

| Date:

November 20, 2023 |

|

|

| |

By: |

/s/

Edward Kovalik |

| |

|

Edward

Kovalik |

| |

|

Chief

Executive Officer |

Exhibit 99.1

Business

Background

On

May 3, 2023, the Company completed its previously announced Merger with Prairie LLC pursuant to the terms of the Merger Agreement, pursuant

to which, among other things, Merger Sub merged with and into Prairie LLC, with Prairie LLC surviving and continuing to exist as a Delaware

limited liability company and a wholly-owned subsidiary of the Company.

Upon

consummation of the Merger, the Company changed its name from “Creek Road Miners, Inc.” to “Prairie Operating Co.”

The Company traded under its former name and ticker symbol “CRKR” until October 16, 2023. From October 16, 2023 to November

12, 2023, the Company traded under symbol “CRKRD,” a transitionary ticker symbol. The Company began trading under

its current ticker symbol, “PROP,” on November 13, 2023. On November 16, 2023, the closing price of

our Common Stock was $14.00.

Prior

to the consummation of the Merger, the Company effectuated the Restructuring Transactions in the following order and issued an aggregate

of 3,375,288 shares of Common Stock (excluding shares reserved for issuance and unissued subject to certain beneficial ownership

limitations) and 4,423 shares of Series D Preferred Stock:

(i)

the Series A Preferred Stock, Series B Preferred Stock and Series C Preferred Stock, plus accrued dividends, were converted, in the

aggregate, into shares of Common Stock;

(ii)

the Original Debentures, plus accrued but unpaid interest and a 30% premium, were exchanged, in the aggregate, for (a) the AR

Debentures in the principal amount of $1,000,000 in substantially the same form as their respective Original Debentures, (b) shares

of Common Stock and (c) shares of Series D Preferred Stock;

(iii)

accrued fees payable to the Board in the amount of $110,250 were converted into shares of Common Stock;

(iv)

accrued consulting fees of the Company in the amount of $318,750 payable to Bristol Capital were converted into shares of Common

Stock; and

(v)

all amounts payable pursuant to certain convertible promissory notes were converted into shares of Common Stock.

Prior

to the Closing, the Company’s then-existing warrants to purchase shares of Common Stock, warrants to purchase shares

of Series B Preferred Stock and options to purchase shares of Common Stock were cancelled and retired and ceased to exist without

the payment of any consideration to the holders thereof.

At

the Effective Time, all membership interests in Prairie LLC were converted into the right to receive each member’s pro rata share

of 2,297,669 shares of Common Stock.

At

the Effective Time, the Company assumed and converted options to purchase membership interests of Prairie LLC outstanding and unexercised

as of immediately prior to the Effective Time into Non-Compensatory Options to acquire an aggregate of 8,000,000 shares of Common

Stock for $0.25 per share, which are only exercisable if specific production hurdles are achieved, and the Company entered into the Option

Agreements with each of Gary C. Hanna, Edward Kovalik, Paul Kessler and a third-party investor. An aggregate of 2,000,000 Non-Compensatory

Options are subject to be transferred to the PIPE Investors, based on their then percentage ownership of Series D Preferred

Stock to the aggregate Series D Preferred Stock outstanding and held by all PIPE Investors as of the Closing Date, if the

Company does not meet certain performance metrics by May 3, 2026.

In

addition, in connection with the Closing of the Merger, the Company consummated the purchase of oil and gas

leases, including all of Exok’s right, title and interest in, to and under certain undeveloped oil and gas leases located in Weld

County, Colorado, together with certain other associated assets, data and records, consisting of approximately 3,157 net mineral acres

in, on and under approximately 4,494 gross acres from Exok for $3,000,000 pursuant to the Exok Agreement.

On

August 1, 2023, all compensatory options that survived the Merger expired.

On

August 30, 2023, the Company, Gary C. Hanna, Edward Kovalik, Bristol Capital and Georgina Asset Management, LLC (“Georgina Asset

Management”) entered into a non-compensatory option purchase agreement, pursuant to which Georgina Asset Management agreed to purchase,

and each of Gary C. Hanna, Edward Kovalik and Bristol Capital (collectively, the “Sellers”) agreed to sell to Georgina Asset

Management Non-Compensatory Options to acquire an aggregate of 200,000 shares of Common Stock for an aggregate purchase price of $2,000

(the “Option Purchase”). The Option Purchase closed on August 30, 2023. In connection with the Option Purchase, the Company

entered into an amendment to the Option Agreements with each of the Sellers (or an assignee thereof) to reflect that each Seller owns

a lesser number of Non-Compensatory Options after the Option Purchase.

On

September 18, 2023, the Company submitted its initial permit application with the Colorado Energy and Carbon Management Commission for

the Genesis Oil & Gas Development Plan (“OGDP”) in Weld County, Colorado. The Genesis OGDP encompasses seventy-two (72)

wells on two (2) pads, developing 9-square miles of subsurface minerals in rural Weld County, Colorado. The two (2) pads, the Burnett

and Oasis, will develop eighteen (18) three-mile lateral wells and fifty-four (54) two-mile lateral wells, respectively.

On

October 13, 2023, the holders of the AR Debentures elected to convert their AR Debentures into an aggregate of 400,667 shares of Common

Stock.

On

October 16, 2023, the Company effected the Reverse Stock Split at a ratio of 1:28.5714286. The share counts listed above have been

retroactively adjusted to reflect the Reverse Stock Split. The following table shows the share counts before and after the Reverse

Stock Split:

Source

of shares | |

Shares prior to Reverse Stock

Split | | |

Shares following Reverse Stock

Split | |

| Restructuring Transaction | |

| 96,436,808 | | |

| 3,375,288 | |

| Merger Consideration | |

| 65,647,676 | | |

| 2,297,669 | |

| Shares underlying Series D Preferred Stock | |

| 99,292,858 | | |

| 3,475,250 | |

| Shares underlying Series D A Warrants | |

| 99,292,858 | | |

| 3,475,250 | |

| Shares underlying Series D B Warrants | |

| 99,292,858 | | |

| 3,475,250 | |

| Shares issued to Exok in the Exok Option Purchase | |

| 19,157,123 | | |

| 670,499 | |

| Shares underlying Exok Warrants | |

| 19,157,123 | | |

| 670,499 | |

| Shares issued to the Series E PIPE Investor | |

| 1,131,856 | | |

| 39,614 | |

| Shares underlying Series E Preferred Stock | |

| 114,285,714 | | |

| 4,000,000 | |

| Shares underlying Series E A Warrants | |

| 114,285,714 | | |

| 4,000,000 | |

| Shares underlying Series E B Warrants | |

| 114,285,714 | | |

| 4,000,000 | |

| Shares issued upon conversion of AR Debentures | |

| 11,447,619 | | |

| 400,667 | |

In

addition, the exercise prices and conversion rates of the Preferred Stock and Warrants were adjusted pursuant to their respective terms

to reflect the Reverse Stock Split. The following table shows the applicable exercise prices and conversion rates before and after the

Reverse Stock Split:

Securities | |

Pre-Split

Conversion Rate or Exercise Price, as applicable | | |

Post-Split Conversion Rate or Exercise Price, as applicable | |

| Series D A Warrant | |

$ | 0.21 | | |

$ | 6.00 | |

| Series D B Warrant | |

$ | 0.21 | | |

$ | 6.00 | |

| Series D Preferred Stock | |

$ | 0.175 | | |

$ | 5.00 | |

| Exok Warrant | |

$ | 0.2620 | | |

$ | 7.4857 | |

| Series E A Warrant | |

$ | 0.21 | | |

$ | 6.00 | |

| Series E B Warrant | |

$ | 0.21 | | |

$ | 6.00 | |

| Series E Preferred Stock | |

$ | 0.175 | | |

$ | 5.00 | |

On

November 13, 2023, the O’Neill Trust delivered notice to the Company of the exercise of Series D B Warrants to purchase 2,000,000

shares of Common Stock at an exercise price of $6.00 per share for total proceeds to the Company of $12 million (the “Warrant Exercise”).

The Company intends to use the proceeds from the Warrant Exercise for general working capital purposes, which may include drilling activity

or opportunistic acquisitions. Each of the warrants held by the O’Neill Trust, as well as the Series D Preferred Stock and Series

E Preferred Stock was subject to a limitation on exercise or conversion, as applicable, if as a result of such exercise or conversion,

the holder would own more than 4.99% of the outstanding shares of Common Stock (the “Beneficial Ownership Limitation”), which

may be increased by the holder upon written notice to the Company, to any specified percentage not in excess of 9.99% (the “Beneficial

Ownership Limitation Ceiling”). In connection with the Warrant Exercise, the O’Neill Trust entered into an agreement with

the Company pursuant to which it amended the terms of each of its Series D Warrants and Series E Warrants to increase the Beneficial

Ownership Limitation Ceiling from 9.99% to 25% and gave notice to the Company that it was increasing its Beneficial Ownership Limitation

to 25% with respect to each of its remaining warrants. The Beneficial Ownership Limitation Ceiling on the Series D Preferred Stock and

Series E Preferred Stock remains at 9.99%.

Nature

of Business

E&P

We

are engaged in the development, exploration and production of oil, natural gas, and NGLs with operations focused on unconventional oil

and natural gas reservoirs located in Colorado focused on the Niobrara and Codell formations. All of the Company’s E&P assets

were acquired in the Exok Transaction and Exok Option Purchase and consist of certain oil and gas leasehold interests with no existing

oil and gas production or revenue. Our current activities are focused on obtaining requisite permits to begin drilling wells and, as

such, we have no current drilling or completion operations.

The Exok Assets

Prairie acquired

the following assets from Exok in the Exok Transaction and the Exok Option Purchase:

| |

● |

all of Exok’s right, title and interest in, to and under the

fee oil and gas leases described more particularly in the Exok Agreement, including all working interests, operating rights, record

title interests and other interests of every kind and character (the “Fee Leases”), that include and convey no less than

a 75% net revenue interest (“NRI,” being the share of production of all hydrocarbons produced, saved and sold, after

all burdens, such as royalty and overriding royalty, have been deducted from the working interest) in each Fee Lease; |

| |

|

|

| |

● |

all of Exok’s right, title and interest in, to and under the

State of Colorado Oil and Gas Lease described more particularly in the Exok Agreement, including all working interests, operating

rights, record title interests and other interests of every kind and character (the “State Leases”), that include and

convey no less than a 77.5% NRI in the State Leases; |

| |

|

|

| |

● |

100% of Exok’s leasehold interest (Fee Leases and State Leases

collectively referred to as the “Leases”) in approximately 23,485 net mineral acres in, on and under approximately 37,189

gross acres located in Weld County, Colorado, as described more particularly in the Exok Agreement (the “Lands”); |

| |

|

|

| |

● |

to the extent transferable, Exok’s interests in and under

all contracts, agreements and instruments by which the other Exok Assets are bound or that relate to or are used or useful in connection

with the ownership, development or operation of the Leases or the Lands, to the extent applicable to the Leases or Lands, including

all surface use agreements, surface rights, surface permits and other similar rights and instruments; and |

| |

● |

all of Exok’s records, files and geological and geophysical

data directly related to the Exok Assets, including without limitation all seismic data and interpretations thereof, logs, core analyses,

formation tests, films, surveyors’ notes, plane table sheets, shot point data bases, land files, contract files, lease files,

title files (including title reports, title opinions, runsheets, abstracts, evidence of bonus and rental payments), maps, surveys

and data sheets. |

The

assets are undeveloped oil and gas leasehold acreage located in northern Colorado, in Weld County covering approximately 4,494 gross

acres and 3,157 net acres. The operating area is rural and free of development. Access to the leases is by paved and dirt country roads

and private road access. Approximately 70% of the net leasehold is held under fee leases, with the remaining 30% held under State of

Colorado leases. Prairie does not hold any interest in federal oil and gas leases. All of the acreage is held by crude oil and natural

gas leases with varying expiration dates, some with options to extend ranging from 1 to 4 years. The fee leases are burdened with total

royalties of 25%. The State of Colorado leases are burdened with total royalties of 22.5%. The leases can be held indefinitely by production.

Unless production is established within the spacing units covering the undeveloped acreage, the leases for such acreage will eventually

expire. There are no lease expirations prior to July 23, 2025.

The

Exok Assets are located in and around wells drilled in both the Niobrara Shale and the Codell Sandstone formations within the D-J Basin.

While production activities in the D-J Basin date back to the 1970s, production within the D-J Basin has increased rapidly since the

horizontal drilling boom in 2009, with both the Niobrara and Codell formations contributing to this activity. Within the D-J Basin operating

area, there are over 1,300 legacy vertical wells, with Noble Energy, Inc. (now Chevron Corporation), Civitas Resources, Inc., EOG Resources,

Inc. and Samson Energy Company, LLC operating a substantial number of such wells.

The

primary drilling objective in this area is crude oil production from the fractured Codell and Niobrara formations. The area has seen

a renewed interest in drilling activity over the past decade in conjunction with drilling success in the Niobrara in the D-J Basin on

the front range of Colorado. Active operators in the area have included Noble Energy, Inc. (now Chevron Corporation), Civitas Resources,

Inc., EOG Resources, Inc., Samson Energy Company, LLC and others. There is ample takeaway infrastructure in place within several miles

of the Exok Assets, including multiple midstream operators such as Summit Midstream Partners LP, Outrigger Energy II LLC, Rimrock Energy

Partners LLC and Roaring Fork Midstream LLC.

Pursuant

to the Exok Agreement, the Company has the option to purchase, from the Closing Date until the

later of (x) the date that is ninety (90) days following the Closing Date and (y) August 15, 2023, approximately 20,327 net mineral acres

in, on and under approximately 32,695 additional gross acres from Exok for a purchase price of $22,182,000, payable in (a) $18,000,000

in cash and (b) $4,182,000 in total equity consideration, consisting of (1) a number of shares of Common Stock equal to the quotient

of $4,182,000 divided by the volume weighted average price for shares of Common Stock for twenty (20) consecutive trading days ending

on the date such option is exercised by the Company and (2) an equal number of warrants to purchase shares of Common Stock (the “Exok

Option”).

On

August 14, 2023, Prairie LLC exercised the Exok Option and purchased oil and gas leases, including all of Exok’s right, title and

interest in, to and under certain undeveloped oil and gas leases located in Weld County, Colorado, together with certain other associated

assets, data and records, consisting of approximately 20,328 net mineral acres in, on and under approximately 32,695 gross acres from

Exok. The Company paid $18.0 million in cash to Exok and issued equity consideration to certain affiliates of Exok, consisting

of (i) 670,499 shares of Common Stock and (ii) Exok Warrants providing the right to purchase 670,499 shares of Common Stock at $7.43.

To

fund the Exok Option Purchase, the Company entered into a securities purchase agreement with the Series E PIPE Investor on August

15, 2023, pursuant to which the Series E PIPE Investor agreed to purchase, and the Company agreed to sell to the Series E PIPE

Investor, for an aggregate of $20.0 million, securities consisting of (i) 39,614 shares of Common Stock, (ii) 20,000 shares

of Series E Preferred Stock and (iii) Series E PIPE Warrants to purchase 8,000,000 shares of Common Stock, in a private placement.

The

Exok Option Purchase and the Series E PIPE closed on August 15, 2023.

The

Company is currently applying for permits to begin drilling. We expect to begin drilling in the first quarter of 2024, subject to receiving

approvals for the requisite permits and obtaining sufficient financing.

Summary

of Our Possible Reserve Estimates

The

Company’s estimated possible reserves as of August 1, 2023, as shown in the following table, have been prepared by

Collarini Energy Experts, an independent Petroleum Reserve Evaluation Firm, in

accordance with the Society of Petroleum Engineers’ Petroleum Resources Management System guidelines and guidelines

established by the SEC, utilizing NYMEX Strip Pricing as of July 31, 2023. A copy of Collarini’s reserve report as of

August 1, 2023 is included as an exhibit to this Registration Statement.

| Reserve Category | |

Formation | |

Well Count | | |

Net Oil (MBbl) | | |

Net Gas (MMCF) | | |

Net NGL (MGal) | | |

Net Equiv. (MBoe) | | |

PV10 ($000s) | |

| POSS | |

| |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| | |

Codell | |

| 148 | | |

| 45,947 | | |

| 99,806 | | |

| 15,852 | | |

| 78,434 | | |

| 641,081 | |

| | |

Niobrara | |

| 264 | | |

| 96,688 | | |

| 338,511 | | |

| 53,766 | | |

| 206,873 | | |

| 1,722,856 | |

| Total | |

| |

| 412 | | |

| 142,635 | | |

| 438,318 | | |

| 69,618 | | |

| 285,306 | | |

| 2,363,937 | |

Note:

PV-10 is a non-GAAP financial measure. PV-10 is derived from the Standardized Measure of Discounted Future Net Cash Flows (“Standardized

Measure”), which is the most directly comparable GAAP financial measure for proved reserves. PV-10 is a computation of the Standardized

Measure on a pre-tax basis. PV-10 is equal to the Standardized Measure at the applicable date, before deducting future income taxes,

discounted at 10%. We believe that the presentation of PV10 is relevant and useful to our investors as supplemental disclosure to the

standardized measure, or after-tax amount, because it presents the discounted future net cash flows attributable to our possible reserves

before considering future corporate income taxes and our current tax structure. While the standardized measure is dependent on the unique

tax situation of each company, PV10 is based on prices and discount factors that are consistent for all companies. Our possible reserves

were derived from wells of offset operators in the same development area. We have shown possible reserves as we will not have proven

reserves until our development plan commences.

Preparation

of reserves estimates.

Collarini is

a registered d.b.a of Collarini Energy Staffing Inc., a Louisiana S Corporation registered in Louisiana in 1995. It employs

petroleum engineers, geoscientists and other experienced professionals. The report was prepared under the direction of Collarini’s Chairman and Project Supervisor,

Reserves and Economics Expert, Cheryl Collarini, P.E. Ms. Collarini holds a B.S. in civil engineering from Massachusetts Institute

of Technology and an MBA from the University of New Orleans, is a registered professional engineer in the state of Louisiana

(License #PE.0022246) and has approximately 50 years of experience in production engineering, reservoir engineering, acquisitions

and divestments, field operations and management. Ms. Collarini is a member of the Society of Petroleum Engineers, the Society of

Women Engineers, and the Houston Producers’ Forum. She is also a member of the Advisory Board of the University of

Houston’s Petroleum Engineering Department. Ms. Collarini meets or exceeds the education, training and experience requirements

set forth in the Standards Pertaining to the Estimating and Auditing of Oil and Gas Reserves Information promulgated by the Society

of Petroleum Engineers. Ms. Collarini is proficient in judiciously applying industry standard practices to engineering and

geoscience evaluations as well as applying SEC and other industry reserves definitions and guidelines.

Bryan

Freeman, our Executive Vice President of Operations, works closely with our independent reserve engineers to ensure the integrity,

accuracy and timeliness of data furnished to our independent reserve engineers in their preparation of reserve estimates. Mr.

Freeman is primarily responsible for overseeing the preparation of both our internal and external reserve estimates. Mr. Freeman is responsible for reservoir engineering, is a qualified reserve

estimator and auditor and is primarily responsible for overseeing our independent reserve engineers during the preparation of our external

reserve estimates. His professional qualifications meet or exceed the qualifications of reserve estimators and auditors set forth in the

“Standards Pertaining to Estimation and Auditing of Oil and Natural Gas Reserves Information” promulgated by the Society of

Petroleum Engineers. His qualifications include a Masters and Bachelor of Science degrees in Engineering from University of Texas; a member

of the Society of Petroleum Engineers; and more than 19 years of practical experience in estimating and evaluating reserve information

with more than 10 of those years overseeing estimating and evaluating reserves. For additional

discussion of Mr. Freeman’s qualifications, please see Mr. Freeman’s biography in the section entitled

“Management.”

Our

independent reserve engineers were selected for their historical experience and geographic expertise in engineering similar resources.

Under SEC rules, possible reserves are reserves which, by analysis of geoscience and engineering data, are those additional reserves

that are less certain to be recovered than probable reserves. When deterministic methods are used, the total quantities ultimately recovered

from a project have a low probability of exceeding proved plus probable plus possible reserves. When probabilistic methods are used,

there should be at least a 10% probability that the total quantities ultimately recovered will equal or exceed the proved plus probable

plus possible reserves estimates. Possible reserves may be assigned to areas of a reservoir adjacent to probable reserves where data

control and interpretations of available data are progressively less certain. Frequently, this will be in areas where geoscience and

engineering data are unable to define clearly the area and vertical limits of commercial production from the reservoir by a defined project.

Possible reserves also include incremental quantities associated with a greater percentage recovery of the hydrocarbons in place than

the recovery quantities assumed for probable reserves. The technical and economic data used in the estimation of our possible reserves

include, but are not limited to, lease positions, estimated working and net revenue interests, indicative drilling and completion costs,

facility and pipeline costs, expected operating expenses and schedules for proposed drilling and permitting, as well as regional production,

well information and directional surveys from the Enverus PRISM data service. Our independent reserve engineers use this technical data,

together with standard engineering and geoscience methods, or a combination of methods, including performance analysis, volumetric analysis

and analogy. The reserve volumes and their respective classifications and categorizations were estimated by performance

methods, volumetric methods, analogy, or combination of methods. Performance methods generally included decline-curve analysis and material

balance analysis where representative data was available. Volumetric estimates generally included a combination of geological and engineering

interpretations, while analogy methods included reserve estimates from historical performance of similar wells and reservoirs in the field

or nearby fields. Regional production, well information, and directional surveys were sourced from Enverus PRISM data service.

We

maintain adequate and effective internal controls over our reserve estimation process as well as the underlying data upon which reserve

estimates are based. The primary inputs to the reserve estimation process were technical information, financial data, ownership interest

and third-party production data. The reserve estimates prepared by our independent reserve engineers were reviewed and compared to our

internal estimates by Mr. Freeman and our technical staff. Material reserve estimation differences were reviewed between our independent

reserve engineers and us, and additional data was provided to address the differences. If the supporting documentation did not justify

additional changes, our independent reserve engineers reserves were accepted.

The

accuracy of any reserve estimate is a function of the quality of available data and of engineering and geological interpretation. As

a result, the estimates of different engineers often vary. In addition, the results of drilling, testing and production may justify revisions

of such estimates. Accordingly, reserve estimates often differ from the quantities of oil, natural gas and NGLs that are ultimately recovered.

See “Risk Factors—Our estimated natural gas, NGL and oil reserve are based on many assumptions that may prove to be inaccurate.

Any material inaccuracies in the reserve estimates or the underlying assumptions will materially affect the quantities and present value

of our reserves.” for more information.

Cryptocurrency

Mining

During

2022, the Company participated in mining pools that pool the resources of groups of miners and split cryptocurrency rewards earned according

to the “hashing” capacity each miner contributes to the mining pool. Cryptocurrency mined by the Company has historically

been held short-term and sold to fund operations. As described further in the table provided below, the Company earned approximately

19 Bitcoin, net of fees, from its mining operations during the fourth quarter of 2021 and first half of 2022. Substantially all such

Bitcoin was sold during the second quarter of 2022 in order to fund operations. The average period between receipt of crypto assets and

the subsequent sale date from October 2021, when the Company began holding cryptocurrency, to December 2022, when the Company sold the

last of its cryptocurrency, was 136 days. Historically, the Company’s liquidity and value of its Bitcoin held was subject to the

risks associated with the volatility in Bitcoin pricing. The Company ceased its cryptocurrency mining operations in mid-2022

and began the process to reinitiate such operations upon the entering of the Master Services Agreement in March 2023 as described below.

The Company measures its

operations by the number and U.S. Dollar (US$) value of the cryptocurrency rewards it earns from its cryptocurrency mining activities.

The following table presents additional information regarding our cryptocurrency mining operations:

| | |

Quantity of Bitcoin | | |

US$

Amounts | |

| Balance September 30, 2021 | |

| — | | |

$ | — | |

| Revenue recognized from cryptocurrency mined | |

| 6.7 | | |

| 369,804 | |

| Mining pool operating fees | |

| (0.1 | ) | |

| (7,398 | ) |

| Impairment of cryptocurrencies | |

| — | | |

| (59,752 | ) |

| Balance December 31, 2021 | |

| 6.6 | | |

$ | 302,654 | |

| Revenue recognized from cryptocurrency mined | |

| 8.3 | | |

| 343,055 | |

| Mining pool operating fees | |

| (0.2 | ) | |

| (6,868 | ) |

| Impairment of cryptocurrencies | |

| — | | |

| (106,105 | ) |

| Balance March 31, 2022 | |

| 14.7 | | |

$ | 532,736 | |

| Revenue recognized from cryptocurrency mined | |

| 4.6 | | |

| 166,592 | |

| Mining pool operating fees | |

| (0.1 | ) | |

| (3,428 | ) |

| Proceeds from the sale of cryptocurrency | |

| (18.9 | ) | |

| (564,205 | ) |

| Realized loss on the sale of cryptocurrency | |

| — | | |

| (131,075 | ) |

| Impairment of cryptocurrencies | |

| — | | |

| (34 | ) |

| Balance June 30, 2022 (1) | |

| 0.3 | | |

$ | 586 | |

| Revenue recognized from cryptocurrency mined | |

| 0.3 | | |

| 7,955 | |

| Mining pool operating fees | |

| — | | |

| (156 | ) |

| Impairment of cryptocurrencies | |

| — | | |

| (1,035 | ) |

| Balance September 30, 2022 (1) | |

| 0.6 | | |

$ | 7,350 | |

| | |

| | | |

| | |

| Revenue recognized from cryptocurrency mined | |

| — | | |

| — | |

| Mining pool operating fees | |

| — | | |

| — | |

| Proceeds from the sale of cryptocurrency | |

| (0.6 | ) | |

| (11,203 | ) |

| Realized gain on the sale of cryptocurrency | |

| — | | |

| 3,853 | |

| | |

| | | |

| | |

| Balance December 31, 2022 (1) | |

| — | | |

$ | — | |

| (1) |

After June 30, 2022 and

through December 31, 2022 the Company did not receive meaningful cryptocurrency awards nor generate meaningful revenue from cryptocurrency

mining. |

On March 2, 2023, the Company

entered into the Master Services Agreement with Atlas and began the process of reinitiating its cryptocurrency mining operations. Currently, we generate

all our revenue through our cyptocurrency mining activities from assets we acquired in the Merger. We currently do not expect to receive

rewards in the form of cryptocurrency in the future. We do not own, control or take custody of Bitcoin, and we currently do not have

any policies regarding how long the Company holds any crypto assets it receives as payment or when the Company will sell any such received

crypto assets. Atlas, our service provider, retains all Bitcoin rewards, deducts a hosting service fee from the monthly total mined currency

produced by our miners and remits the net mined currency to us in cash. We currently do not intend to mine crypto assets other than Bitcoin.

The Company currently does not have, and does not intend to enter into, any agreements with mining

pool operators.

All

of our miners were manufactured by Bitmain, and incorporate application-specific integrated circuit chips specialized to solve blocks

on the Bitcoin blockchains using the 256-bit secure hashing algorithm in return for Bitcoin cryptocurrency rewards. At May 3, 2023,

the assets acquired by the Company in the Merger included 606 Bitmain S19 XP miners for which deposits had been made and were located

in Asia. On May 31, 2023, the Company paid a shipping fee of $54,000 and the miners were delivered

to the Company on June 17, 2023. All of the miners are newly manufactured. Upon delivery of the last batch of products to the Company

on June 17, 2023, the Bitmain Agreement terminated pursuant to its terms.

Factors

Affecting Profitability

Our

business is heavily dependent on the market price of Bitcoin. The prices of cryptocurrencies, specifically Bitcoin, have experienced

substantial volatility and dropped throughout 2022 and Bitcoin reached its lowest price since December 2020 in late 2022. As of September

30, 2023, the market price of Bitcoin was approximately $26,911, which reflects a decrease of approximately 43% from

the beginning of 2022, and a decrease of approximately 60% from its all-time high of approximately $67,000. Further affecting

the industry, and particularly for the Bitcoin blockchain, the cryptocurrency reward for solving a block is subject to periodic incremental

halving. Halving is a process designed to control the overall supply and reduce the risk of inflation in cryptocurrencies using a Proof-of-Work

consensus algorithm. At a predetermined block, the mining reward is cut in half, hence the term “halving.” For Bitcoin the

reward was initially set at 50 Bitcoin currency rewards per block. The Bitcoin blockchain has undergone halving three times since its

inception as follows: (1) on November 28, 2012 at block 210,000; (2) on July 9, 2016 at block 420,000; and (3) on May 11, 2020 at block

630,000, when the reward was reduced to its current level of 6.25 Bitcoin per block. While a precise date for the next halving of the

Bitcoin blockchain is not known, based on industry data, we anticipate this to occur in the first half of 2024 at block 840,000, when

the reward will be reduced to 3.125 Bitcoin per block. This process will reoccur until the total amount of Bitcoin currency rewards issued

reaches 21 million and the theoretical supply of new Bitcoin is exhausted, which is currently estimated to occur in 2140. While Bitcoin

prices have historically increased around these halving events, which increases in price have correspondingly mitigated the decrease

in mining reward, there is no guarantee that the price change would be favorable or would compensate for the reduction in mining reward.

If a corresponding and proportionate increase in the trading price of Bitcoin or a proportionate decrease in mining difficulty does not

follow these anticipated halving events, the revenue we earn from our bitcoin mining operations would see a corresponding decrease. Many

factors influence the price of Bitcoin, and potential increases or decreases in prices in advance of, or following, a future halving

is unknown.

In addition to the

market price of Bitcoin, the price of electricity can impact the profitability of Bitcoin mining operations. We use special cryptocurrency

mining computers to solve complex cryptographic algorithms to support the Bitcoin blockchain and, in return, received Bitcoin as our

reward through the third quarter of 2022 and beginning in March 2023, we receive the dollar value of Bitcoin net of costs as our reward.

Miners measure their processing power, which is known as “hashing” power, in terms of the number of hashing algorithms solved

per second, which is the miner’s “hash rate.” A miner with a higher hash rate consumes more electricity to run than

a miner with a lower hash rate. The “hash rate”

capacity of our miners was 159.5 PH/s as of September 30, 2023.

Adverse movements

in Bitcoin market price, electricity costs and “hash rate” can result in decreased cryptocurrency mining revenue and increased

cryptocurrency mining costs, each of which has had a material adverse effect on our business, financial condition and results of operations

for certain periods, most notably in June 2022 when we decided to pause Bitcoin mining activities due to an inability to source power

at rates that would justify ongoing mining activity during that period. After entering into the Master Services Agreement and relocating

our miners to the Atlas facility, we re-initiated Bitcoin mining activities in 2023. We continue to monitor the economic benefits and

risks of our cryptocurrency mining operations and may reduce or pause such operations from time to time, or may exit such operations

altogether, if we determine that such operations are no longer beneficial to the Company.

The term “hashing”

power also relates to the total Bitcoin network’s mining difficulty of a given blockchain. When a new blockchain is launched, it

sets a specific time frame to produce new blocks. If new miners join the network or performance of miners increases, the hash rate goes

up, and blocks are mined faster than the set time. In such cases, the network increases the mining difficulty. The inverse is also true

– if there are fewer miners, the hash rate decreases, blocks take longer to mine and the difficulty is lowered. When the Bitcoin

network’s difficulty goes up, it takes every mining machine longer and requires more “hashing” power to maintain the

same level of mining profits. We do not control nor attempt to forecast the Bitcoin network’s difficulty or the resulting network

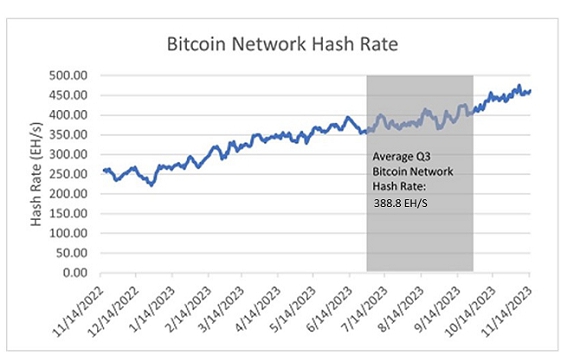

“hashing” rate. In general, the Bitcoin network hash rate has increased over time due to both additional miners coming online

as well as increased efficiencies in mining technology. For the third quarter of 2023, the average hash rate of the Bitcoin network

was approximately 388.8 EH/s. For the twelve-month period ended November 14, 2023, the average hash rate of the Bitcoin

network was approximately 348.1 EH/s. The following graph shows the Bitcoin network hash rate for the twelve months ended November

14, 2023, according to Blockchain.com:

The Company’s cost

to earn a Bitcoin is predominantly driven by the cost of power or electricity which fluctuates based on many factors, including the impacts

of weather and the price of natural gas. Through the third quarter of 2022, the Company paid the prevailing market rate for power without

the benefit of a fixed cost. The price of natural gas can be volatile and increased substantially from the beginning of 2022 through

the end of the year which increased the Company’s cost of power. This increase when coupled with the decrease in the price of Bitcoin

throughout 2022 resulted in decreased cryptocurrency mining revenue, increased cryptocurrency mining costs and negative operating margins

all of which had a material adverse effect on our business, financial condition and results of operations leading to the Company’s

cessation of cryptocurrency mining operations in mid-2022.

In

March 2023 and as described below, we entered into a Master Services Agreement with Atlas and began the process to reinitiate our cryptocurrency

mining operations. Through this contract, we sought to normalize our mining costs and agreed to pay Atlas a flat fee of $20.00 per miner

to cover set-up costs and thereafter pay a monthly fee to Atlas for the quantity of electricity consumed by the miners at a rate of $0.08

per kWh. As such, the Company’s per unit cost of electricity is currently fixed through the term of the contract which expires

on March 2, 2025. However, the cost that Atlas is required to pay its electricity provider may not be fixed and could be greater than

$0.08 per kWh or $80 per MW. In such cases, it can and does shut down the Company’s miners thereby reducing both our ability to

earn revenue and our electricity costs. During the third quarter of 2023 there were six days whereby Atlas shut down miners due to its cost of electricity. As such, the Company’s operations

continue to have exposure to increased power costs driven by market factors.

Our

Bitcoin mining business breaks even so long as it

is economically beneficial for us to continue to operate our mining machines, and that is essentially when the mining machines contribute

positive cash flow (i.e., when the variable cost to mine one Bitcoin, namely the electricity cost, equals the market price of a Bitcoin).

Based on this overarching principle, our assumed cash cost to mine one Bitcoin is approximately $11,000 on go-forward basis (or

$37,000 inclusive of hardware costs). Such estimates are based on the following inputs: (i) a Bitcoin network hash rate of

344.15 EH/s, which was the approximate network hash rate as of April 14, 2023, the date we reinitiated our Bitcoin mining business, according

to Blockchain.com and is also a close approximation to both the average Bitcoin network hash rate of 388.8 EH/s for the three

months ended September 30, 2023 and the trailing twelve month average Bitcoin network hash rate of 348.1 EH/s as of November

14, 2023, according to Blockchain.com; (ii) our average mining machine energy consumption at 27.1 joules/terahash, which

represents the average mining machine energy consumption as of September 30, 2023; (iii) electricity cost at $0.08 kWh, which

is the contracted price we pay per kWh under the Master Services Agreement and (iv) depreciation cost of our investment in mining

equipment, which is described in more detail below. We believe using the April 14, 2023 hash rate, which also reflects an approximate

network hash rate over the past year, is appropriate currently and we will continue to monitor historical rates and reassess the network

hash rate used in our breakeven forecast going forward. As a result, $11,000 represents our “shutdown Bitcoin price” for

our Bitcoin mining business, indicating that as long as the Bitcoin price is higher than $11,000 on average, we would continue to operate

our existing mining machines and such operation would be economically beneficial to us.

As

of September 30, 2023, we have invested approximately $12 million to acquire our miners. We paid for these miners in cash and

have not historically financed the miners and do not have any current plans to finance miners we may purchase in the future. Our

mining equipment is expected to have a useful life of 2 to 5 years and depreciation of $132,851 and $425,468 was recognized

with respect to our mining equipment for the three months ended June 30, 2023 and September 30, 2023,

respectively. Since all of our mining equipment is fully paid, we do not take into account the replacement or depreciation

costs of such machines in determining our “shutdown Bitcoin price” for our existing equipment. In addition, since

the AR Debentures were fully extinguished in October 2023, we do not have debt or financing costs to allocate to our

breakeven analysis. While we do not consider sunk costs, depreciation of existing equipment or replacement costs in our forecasted

breakeven analysis or in our decisions to continue or

to pause existing mining operations, such costs are substantial and will

be an important factor in determining whether to invest in new mining equipment to replace our existing equipment as it

ages. For the three months ended June 30, 2023 and September

30, 2023, we estimate that such hardware costs were $20,427 and $25,877, respectively, per Bitcoin based upon our depreciation

expense in each period. Such costs fluctuate due to the timing of placing equipment into service and amount of Bitcoin mined in a

given period among other factors. Based on our current mining equipment, estimates of useful lives, network hash rate and other factors, we expect

approximately $26,000 per Bitcoin to be representative of such cost in our forecast. In addition, based on current prices for

miners with comparable hashing capacity as our existing miners and an assumed useful life of 36 months, we estimate that the

replacement costs of our existing equipment would be approximately $345,000 per quarter, or $21,044 per Bitcoin based on the

amount of Bitcoin mined in the third quarter of 2023. Such replacement costs are based on assumptions that are subject to

significant uncertainty. For example, miners currently available for purchase from Bitmain have a hashing capacity 123% higher than

the weighted average hashing capacity of our existing equipment. Such technology developments may result in higher efficiency and

lower electricity cost per Bitcoin in the future. However, pricing of such new miners may fluctuate significantly over time based on

both demand and efficiency. In addition, we are not able to predict at this time the actual useful life of our existing miners or

any miners we may acquire in the future, each of which could have a material effect on the breakeven cost of maintaining our mining

operations. For information regarding the

inherent uncertainties in our breakeven analysis, please see “Risk Factors—Our breakeven costs are based on a number of assumptions, including the price of Bitcoin, which are subject to inherent

uncertainty, may prove to be inaccurate or may not be sustained over time. Such factors could

adversely our business and results of operations.”

During the three

months ended June 30, 2023, our cash operating cost was $14,872 per Bitcoin. Our cash operating costs during this period

reflected inefficiencies related to re-initiating our mining operations and continued deployment of additional miners into Atlas’

facility that are not expected to recur in subsequent periods. Despite these cash operating costs being higher than our assumed

costs, our Bitcoin mining operations were still profitable on a cash basis due to the price of Bitcoin far exceeding our “shutdown

Bitcoin price.” As expected, mining costs per Bitcoin normalized during the third quarter of 2023 after the Company brought

the remaining miners online at the end of June 2023. Average cash operating costs per Bitcoin were $11,005 per Bitcoin

in the three months ended September 30, 2023 in line with our expectations.

A breakeven analysis of the

Company’s Bitcoin mining operations in terms of one Bitcoin for the three months ended June 30, 2023 and three months ended

September 30, 2023 and key inputs for our breakeven forecast follows:

| | |

Average Second Quarter 2023 | | |

Average Third Quarter 2023 | |

| Bitcoin price | |

$ | 28,053 | | |

$ | 27,852 | |

| Power cost per Bitcoin | |

| (14,872 | ) | |

| (11,005 | ) |

| Cash operating margin per Bitcoin | |

| 13,181 | | |

| 16,847 | |

| Hardware cost per Bitcoin | |

| (20,427 | ) | |

| (25,877 | ) |

| Total operating margin per Bitcoin | |

$ | (7,246 | ) | |

$ | (9,029 | ) |

| | |

| | | |

| | |

| Key inputs to power cost: | |

| | | |

| | |

| Approximate average network hash rate (EH/s) | |

| 356.8 | | |

| 388.8 | |

| Average energy consumption per miner (watts) (1) | |

| 3,098 | | |

| 3,112 | |

| Electricity cost ($ per kWh) | |

$ | 0.08 | | |

$ | 0.08 | |

| Approximate average energy consumption per Bitcoin (kWh) | |

| 185,900 | | |

| 137,563 | |

(1)

This value represents the weighted average energy consumption per miner. This is a rated value as measured by the manufacturer of our

miners, Bitmain.

Our electricity

costs are determined by multiplying the price per kWh by the number of hours in the month by the metered rated power consumption of our

miners hosted by Atlas. The more miners we have hosted by Atlas, the higher our electricity costs in total are. Conversely, when the

price of electricity rises to the point where Atlas shuts off our miners, we experience lower electricity costs. The cost of electricity

under the Master Services Agreement ranged from a low of $9,772 per Bitcoin to a high of $34,123 per Bitcoin for the three months

ended June 30, 2023 and $9,213 per Bitcoin to a high of $18,608 per Bitcoin for the three months ended September 30, 2023

The average trading price of

Bitcoin was $28,053 and $27,852 for the three months ended June 30, 2023 and September 30, 2023, respectively. Our

cash costs averaged $14,872 per Bitcoin and $11,005 per Bitcoin in these periods, respectively, and was solely from the

power cost of $0.08 per kWh. On average, our miners used 185,900 kWh and 137,563 kWh to mine one Bitcoin. There were no set-up

or other costs under the Master Services Agreement incurred during these periods. This resulted in an average cash operating

margin of $13,181 per Bitcoin and $16,847 per Bitcoin during the three months ended June 30, 2023 and three months ended

September 30, 2023, respectively. This cost is based on the following factors: (i) the average Bitcoin network hash rate of approximately

356.8 EH/s in the second quarter of 2023 and 388.8 EH/s in the third quarter of 2023 (4612.0 EH/s as of November 14, 2023),

(ii) our average mining machine energy consumption of 3,098 watts and 3,112 watts, respectively, and (iii) electricity cost of

$0.08 per kWh. As a result, the Company’s average cash breakeven cost to mine one Bitcoin was equal to $14,872 per Bitcoin

and $11,005 per Bitcoin in the three months ended June 30, 2023 and September 30, 2023, respectively. We experienced some inefficiencies

in the second quarter of 2023, such as beginning operations on April 14, 2023, that affected results for this quarter. We do not expect

such inefficiencies to occur in future quarters. When including the cost of hardware, the Company’s total costs to mine one

Bitcoin was $35,299 and $36,882 in the three months ended June 30, 2023 and September 30, 2023, respectively, and resulted in a total

operating loss of $7,246 per Bitcoin and $9,029 per Bitcoin in these periods, respectively.

Recent

industry-wide developments, including the continued industry-wide fallout from the recent Chapter 11 bankruptcy filings of cryptocurrency

exchange FTX (including its affiliated hedge fund Alameda Research), crypto hedge fund Three Arrows, crypto miners Compute North and

Core Scientific and crypto lenders Celsius Network, Voyager Digital and BlockFi are beyond our control. We are not directly affected

by these recent incidents, as we do not have any counterparty credit exposure to the above-mentioned firms nor expect their potential

bankruptcy to have any direct impact on our business or operations. We do not believe that our share price has been adversely affected

by such incidents since June 30, 2023, but likely was adversely impacted in 2022 and the first half of 2023. The Company has no exposure

to any of the cryptocurrency market participants that recently filed for Chapter 11 bankruptcy or any other counterparties, customers,

custodians or other participants in crypto asset markets, or who are known to have experienced excessive redemptions, suspended redemptions,

withdrawals of crypto assets or have crypto assets of their customers unaccounted for or material corporate compliance failures; and

the Company does not have any assets, material or otherwise, that may not be recovered due to these bankruptcies or excessive or suspended

redemptions. The price of Common Stock may still not be immune to unfavorable investor sentiment resulting from these recent developments

in the broader cryptocurrency industry and you may experience depreciation of the price of Common Stock.

Master

Services Agreement – Atlas

On

March 2, 2023, the Company entered into the Master Services Agreement with Atlas pursuant to which Atlas will provide the Company with

cryptocurrency mining services for the Company’s cryptocurrency miners at its facility in North Dakota for a term of two years.

The Company has approximately 750 miners at the Atlas Facility and approximately 600 additional miners were shipped to the Company and

deployed to the Atlas Facility on June 28, 2023.

Under

the Master Services Agreement, the Company agreed to pay an initial flat fee of $20.00 per miner to cover set-up costs and thereafter

pay a monthly fee to Atlas for the quantity of electricity consumed by the miners at a rate of $0.08 per kWh. Under the Master Services

Agreement, the Company’s electricity costs are determined by multiplying the price per kWh by the number of hours in the month

by the metered rated power consumption of the Company’s miners hosted by Atlas. In exchange for such payment, Atlas hosts the miners

at its North Dakota facility, including providing rack space, electrical power, internet connectivity, physical security, installation,

configuration and monitoring of the miners for any downtime, with a guarantee to maintain a minimum of 95% uptime for all of our miners,

not including any power outages or other force majeure events.

The

electricity fee is invoiced monthly, within five (5) business days following the end of each calendar month. Any mined cryptocurrency

produced by the Company’s miners is deposited directly to wallets in the custody and control of Atlas on a daily basis.

In exchange, the Company receives a corresponding credit to its account on a daily basis for any mined cryptocurrency that was deposited

to the wallets in the custody and control of Atlas. The Company does not maintain any cryptocurrency assets or wallets and does not take

possession of any cryptocurrency mined. Instead, Atlas maintains an account for the credit of the Company. Within five (5) business

days following the end of each calendar month, Atlas first deducts the electricity fee from the monthly total mined currency produced

by the miners, and then remits to the Company the net mined currency in cash. As a result, the Master Services Agreement does not

contain any contractual arrangements for Atlas to store the Company’s crypto assets and does not address any security precautions

Atlas is required to undertake, any inspection rights the Company has or what type of insurance Atlas is required to have to protect

the Company from loss.

The

term of the Master Services Agreement is two years. The Company has the right to terminate the Master Services Agreement if (a) Atlas

fails to perform any of its obligations under the Master Services Agreement in any material respect that is not cured within 30 business

days of receiving written notice from the Company or (b) Atlas enters into bankruptcy, dissolution, financial failure or insolvency which

is not dismissed or otherwise remedied within thirty (30) days.

Atlas

has the right to terminate the Master Services Agreement if the Company (a) (i) fails to deliver miners to Atlas; (ii) fails to make

any payment(s) when due pursuant to the Master Services Agreement; (iii) breaches any of its representations or warranties in the Master

Services Agreement; (iv) violates, or fails to perform or fulfill any covenant or provision of the Master Services Agreement, and any

such breach of (a) is not cured within ten (10) business days after receipt of written notice from Atlas; or (b) enters into bankruptcy,

dissolution, financial failure or insolvency which is not dismissed or otherwise remedied within thirty (30) days.

Upon

expiration or termination of the Master Services Agreement and upon payment of all undisputed amounts owed under the Master Services

Agreement, Atlas shall decommission and return all of the Company’s miners to the Company.

Government

Regulation

Cryptocurrency

is increasingly becoming subject to governmental regulation, both in the U.S. and internationally. State and local regulations also may

apply to our activities and other activities in which we may participate in the future. Numerous regulatory bodies have shown an interest

in regulating blockchain or cryptocurrency activities. For example, on March 9, 2022, President Biden signed an executive order on cryptocurrencies.

While the executive order does not mandate any specific regulations, it instructs various federal agencies to consider potential regulatory

measures, including the evaluation of the creation of a U.S. Central Bank digital currency. Future changes to existing regulations or

entirely new regulations may affect our business in ways it is not presently possible for us to predict with any reasonable degree of

reliability. As the regulatory and legal environment evolves, we may become subject to new laws and regulation which may affect our mining

and other activities. For additional discussion regarding our belief about the potential risks existing and future regulation pose to

our business, see the Section entitled “Risk Factors.”

Intellectual

Property

We

do not currently own any patents in connection with our existing and planned blockchain and cryptocurrency related operations.

Environmental

and Occupational Health and Safety Regulations

Our

planned oil, natural gas, and NGL exploration and production operations will be subject to stringent federal, regional, state and local

laws and regulations regulating worker health and safety, the release or disposal of materials into the environment, or otherwise relating

to protection of the environmental and natural resources. These laws and regulations may impose significant obligations on our operations,

including the need to obtain permits to conduct drilling or other regulated activities; limit or prohibit drilling activities on certain

lands lying within wilderness, wetlands and other protected areas; restrict the types, quantities and concentration of materials that

can be released into the environment in the performance of drilling and production activities; apply workplace health and safety standards

for the benefit of employees; require remedial activities or corrective actions to mitigate environmental impacts from former or current

operations, such as restoration of drilling pits and plugging of abandoned wells; and impose substantial liabilities for pollution or

unauthorized releases of hazardous materials resulting from our operations.

The

following is a summary of the more significant existing federal environmental and occupational health and safety laws and regulations,

as amended from time to time, to which our planned oil, natural gas and NGL operations will be subject to.

| |

● |

The

Clean Air Act (“CAA”), which restricts the emission of air pollutants from many sources, imposes various pre-construction,

operational, monitoring and reporting requirements and has been relied upon by the EPA as authority for adopting climate change regulatory

initiatives relating to GHG emissions. |

| |

|

|

| |

● |

The

Federal Water Pollution Control Act, also known as the “Clean Water Act,” which regulates discharges of pollutants from

facilities to state and federal waters and establishes the extent to which waterways are subject to federal jurisdiction and rulemaking

as protected waters of the United States. |

| |

|

|

| |

● |

The

Comprehensive Environmental Response Compensation and Liability Act (“CERCLA”), which imposes strict liability on generators,

transporters, disposers and arrangers of hazardous substances at sites where hazardous substance releases have occurred or are threatening

to occur. |

| |

|

|

| |

● |

The

Resource Conservation and Recovery Act (“RCRA”), which governs the generation, treatment, storage, transport and disposal

of non-hazardous and hazardous wastes. |

| |

|

|

| |

● |

The

Oil Pollution Act (“OPA”), which subjects owners and operators of vessels, onshore facilities and pipelines, as well

as lessees or permittees of areas in which offshore facilities are located, to strict liability for removal costs and damages arising

from an oil spill in waters of the United States. |

| |

|

|

| |

● |

The

Safe Drinking Water Act (“SDWA”), which ensures the quality of the nation’s public drinking water through adoption

of drinking water standards and controlling the injection of waste fluids into below-ground formations that may adversely affect

drinking water sources. |

| |

|

|

| |

● |

The

Occupational Safety and Health Act (“OSH Act”), which establishes workplace standards for the protection of the health

and safety of employees, including the implementation of hazard communications programs designed to inform employees about hazardous

substances in the workplace, potential harmful effects of these substances, and appropriate control measures. |

| |

|

|

| |

● |

The

Emergency Planning and Community Right-to-Know Act (“EPCRA”), which requires reporting on the storage, use, and release

of certain chemicals to federal, state, tribal, and/or local governments to help protect communities from potential risks. |

| |

|

|

| |

● |

The

Endangered Species Act (“ESA”), which restricts activities that may affect federally identified endangered and threatened

species or their habitats through the implementation of operating restrictions or a temporary, seasonal, or permanent ban in affected

areas. |

Additionally,

Colorado, where our operations are conducted, has analogous environmental and occupational health and safety laws and regulations governing

many of these same types of activities. In some cases these regulations may impose additional or more stringent conditions or controls

that can significantly restrict, delay or cancel the permitting, development or expansion of our operations or substantially increase

the cost of doing business. In 2019, Colorado passed SB 19-181, which changed Colorado Oil & Gas Conservation Commission’s

mission from “fostering” oil and gas development to “regulating oil and gas development in a manner than protects public

health, safety, welfare, the environment and wildlife resources.” The agency has since promulgated, and continues to develop, a

number of rulemakings reflecting that mission change and imposing additional and stricter regulations on oil and natural gas operations

throughout the state.

Our

operations will also be subject to a variety of local environmental and regulatory requirements, including land use, zoning, building,

and transportation requirements. Any failure to comply with these laws, regulations and regulatory initiatives or controls may result

in the assessment of sanctions, including administrative, civil, and criminal penalties; the imposition of investigatory, remedial, and

corrective action obligations or the incurrence of capital expenditures; the occurrence of restrictions, delays or cancellations in the

permitting, development or expansion of projects; and issuance of injunctions restricting or prohibiting some or all of our activities

in a particular area.

The

trend in environmental and occupational health and safety laws and regulations over time has been the imposition of increasingly restrictive

and limiting regulations on activities that may adversely affect the environment and natural resources or expose workers to injury. If

existing regulatory requirements or enforcement policies change or new executive action or regulatory or enforcement initiatives are

developed and implemented in the future, we may be required to make significant, unanticipated capital and operating expenditures which

could have a material adverse impact on our financial condition or results of operations.

Additionally,

the federal OSH Act and analogous state occupational safety and health laws that impose rigorous standards to prevent or mitigate workers’

exposure to injury will require us to organize information about materials, some of which may be hazardous or toxic, that are used, released

or produced in our planned oil, natural gas, and NGL exploration and production operations. Moreover, the OSHA hazard communication standard,

the EPA community right-to-know regulations under Title III of the federal Superfund Amendment and Reauthorization Act and comparable

state statutes require that information be maintained concerning hazardous materials used or produced in our operations and that this

information be provided to employees, state, local and other applicable government authorities and citizens.

Employees

As

of November 17, 2023, we have eleven

employees. We have never experienced a work stoppage, and believe we maintain positive relationships with our employees.

Facilities

Our

primary office is located at 602 Sawyer Street, Suite 710, Houston, Texas 77007.

Legal

Proceedings

The

Company is not involved in any disputes and does not have any litigation matters pending which the Company believes could have a materially

adverse effect on the Company’s financial condition or results of operations. There is no action, suit, proceeding, inquiry or

investigation before or by any court, public board, government agency, self-regulatory organization or body pending or, to the knowledge

of the executive officers of our Company or any of our subsidiaries, threatened against or affecting our Company, our Common Stock, any

of our subsidiaries or of our Company’s or our Company’s subsidiaries’ officers or directors in their capacities as

such, in which an adverse decision could have a material adverse effect.

Exhibit 99.2

Risk Factors

Investing

in our securities involves risks. Before you make a decision to buy our securities, in addition to the risks and uncertainties discussed

above under “Cautionary Statement Regarding Forward-Looking Statements,” you should carefully consider the specific risks

set forth herein, the risks set forth in our Annual Report on Form 10-K, filed with SEC on March 31, 2023 under the heading “Risk

Factors” and the risks set forth in our subsequent Quarterly Reports on Form 10-Q and other filings we make with the SEC from time

to time, which are incorporated by reference herein, together with other information in this prospectus and the information

incorporated by reference herein. If any of these risks actually occur, it may materially harm our business, financial condition,

liquidity and results of operations. As a result, the market price of our securities could decline, and you could lose all or part of

your investment. Additionally, the risks and uncertainties described in this prospectus or any prospectus supplement and any document

incorporated by reference are not the only risks and uncertainties that we face. Additional risks and uncertainties not presently

known to us or that we currently believe to be immaterial may become material and adversely affect our business.

Risks

Related to Our Company

We

have historically incurred significant losses, and may be unable to generate profitability. If we continue to incur significant

losses, we may have to curtail our operations, which may prevent us from successfully operating and expanding our business.

Historically, we have relied

upon cash from financing activities to fund substantially all of the cash requirements of our activities and have incurred significant

losses and experienced negative cash flow. For the nine months ended September 30, 2023, we incurred a net loss of $55,626,937,

and for the year ended December 31, 2022, we incurred a net loss of $13,783,198. We had stockholders’ equity of $(64,047,831)

and members’ deficit of $381,520 as of September 30, 2023 and December 31, 2022, respectively. We cannot predict if

we will be profitable. We may continue to incur losses for an indeterminate period of time and may be unable to sustain profitability.

An extended period of losses and negative cash flow may prevent us from successfully operating and expanding our business. We may be

unable to sustain or increase our profitability on a quarterly or annual basis.

We

may not achieve the perceived benefits of the Merger and the market price of our Common Stock following the Merger may decline.

The

market price of our Common Stock may decline as a result of the Merger for a number of reasons, including if: investors react negatively

to the prospects of the Company’s business; the effect of the Merger on the Company’s business and prospects is not consistent

with the expectations of our management or of financial or industry analysts; or the Company does not achieve the perceived benefits

of the Merger as rapidly or to the extent anticipated by our management or financial or industry analysts.

Our

stockholders may not realize a benefit from the Merger commensurate with the ownership dilution they will experience in connection with

the Merger.

If

the Company is unable to realize the strategic and financial benefits currently anticipated from the Merger, our pre-closing stockholders

will have experienced substantial dilution of their ownership interests without receiving the expected commensurate benefit, or only

receiving part of the commensurate benefit to the extent the Company is able to realize only part of the expected strategic and financial

benefits currently anticipated from the Merger.

We

may require significant additional capital to fund our growing operations; we may not be able to obtain sufficient capital and

may be forced to limit the scope of our operations.

We

may not have sufficient capital to fund our future operations without significant additional capital investments, including the planned

drilling of oil and gas wells. If adequate additional financing is not available on reasonable terms or at all, we may not be able to

carry out our corporate strategy and we would be forced to modify our business plans (e.g., limit our growth, and/or decrease or eliminate

capital expenditures), any of which may adversely affect our financial condition, results of operations and cash flow. Such reduction

could materially adversely affect our business and our ability to compete. There can be no assurance that financing will be available

in a timely manner or in amounts or on terms acceptable to the Company, or at all.

The

Company’s ability to obtain external financing in the future may be subject to a variety of uncertainties, including its future

financial condition, results of operations, cash flows and the liquidity of international capital and lending markets. In light of conditions

impacting the industry, it may be more difficult for the Company to obtain equity or debt financing currently and/or in the future. Specifically,

the crypto assets industry has been negatively impacted by recent events such as the bankruptcies of Compute North LLC (“Compute

North”), Core Scientific Inc. (“Core Scientific”), Alameda Research LLC (“Alameda Research”), BlockFi Inc.

(“BlockFi”), Celsius Network LLC (“Celsius Network”), Voyager Digital Ltd. (“Voyager Digital”), Three

Arrows Capital (“Three Arrows”) and FTX Trading Ltd. (“FTX”). In response to these events, the digital asset

markets, including the market for Bitcoin specifically, have experienced extreme price volatility and several other entities in the digital

asset industry have been, and may continue to be, negatively affected, further undermining confidence in the digital assets markets and

in Bitcoin. We may need to undertake equity, equity-linked

or debt financings to secure additional funds. If we raise additional funds through future issuances of equity or convertible debt securities,

our existing stockholders could suffer significant dilution, and any new equity securities we issue could have rights, preferences and

privileges superior to those of holders of our Common Stock. Any debt financing that we secure in the future could involve restrictive

covenants relating to our capital raising activities and other financial and operational matters, including the ability to pay dividends.

This may make it more difficult for us to obtain additional capital and to pursue business opportunities. A

large amount of bank borrowings and other debt may result in a significant increase in interest expense while at the same time exposing

the Company to increased interest rate risks.

We