Exhibit 99.1

SANDSTORM GOLD LTD.

MANAGEMENT’S DISCUSSION AND ANALYSIS

Q3 / 2017

For The Period Ended September 30, 2017

This management’s discussion and analysis (“MD&A”) for Sandstorm Gold Ltd. and its subsidiary entities (“Sandstorm”, “Sandstorm Gold” or the “Company”) should be read in conjunction with the unaudited condensed consolidated interim financial statements of Sandstorm for the three and nine months ended September 30, 2017 and related notes thereto which have been prepared in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”), applicable to preparation of interim financial statements including International Accounting Standard 34—Interim Financial Reporting ("IAS 34"). Readers are encouraged to consult the Company’s audited consolidated financial statements for the year ended December 31, 2016 and the corresponding notes to the financial statements which are available on SEDAR at www.sedar.com. The information contained within this MD&A is current to November 1, 2017 and all figures are stated in U.S. dollars unless otherwise noted.

COMPANY HIGHLIGHTS

Operating Results

|

|

|

|

|

|

|

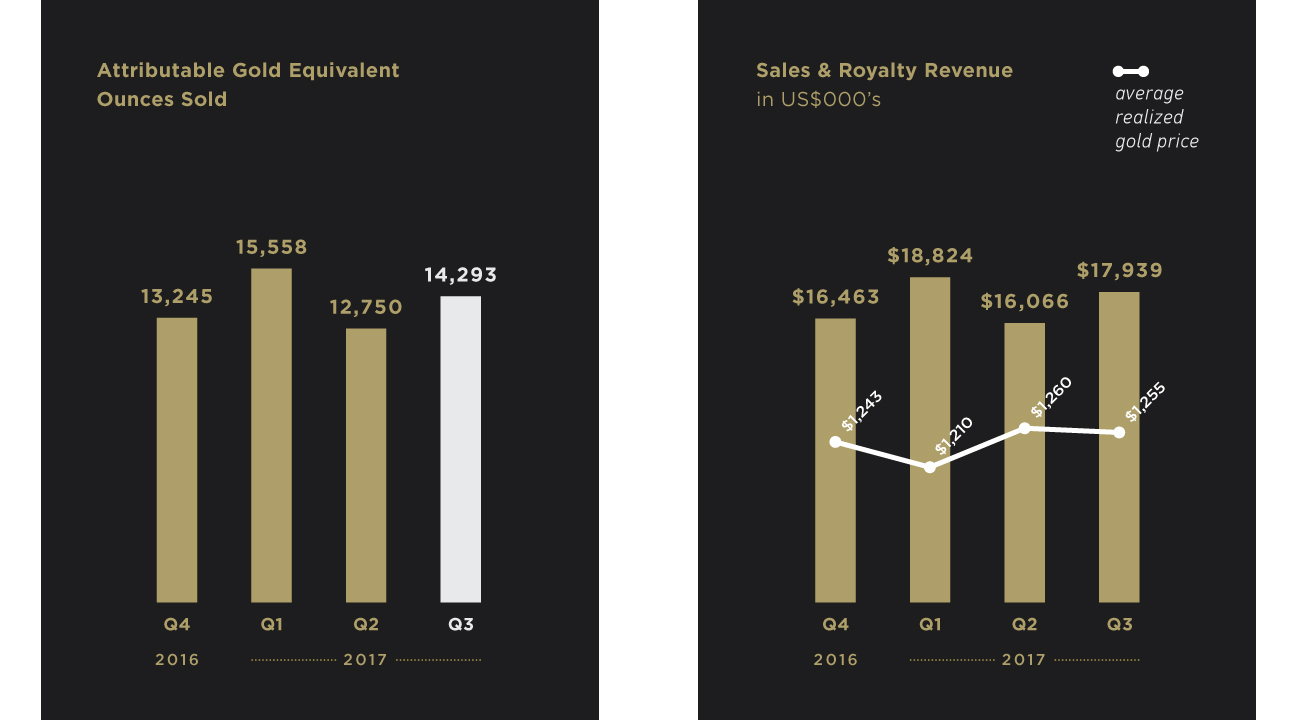

Attributable Gold Equivalent ounces sold (as defined hereinafter), for the three and nine months ended September 30, 2017 were 14,293 ounces and 42,601 ounces, respectively, compared with 12,588 and 36,486 ounces for the comparable periods in 2016.

|

|

|

|

|

|

|

|

Revenue for the three and nine months ended September 30, 2017 was $17.9 million and $52.8 million, respectively, compared with $16.8 million and $45.9 million for the comparable periods in 2016.

|

|

|

|

|

|

|

|

Cash flows from operating activities for the three and nine months ended September 30, 2017 were $11.9 million and $34.9 million, respectively, compared with $10.3 million and $28.9 million for the comparable periods in 2016.

|

|

|

|

|

|

|

|

Cost of sales, excluding depletion for the three and nine months ended September 30, 2017 were $3.5 million and $11.2 million, respectively, compared with $3.2 million and $9.5 million for the comparable periods in 2016.

|

|

|

|

|

|

|

|

Average cash costs1 for the three and nine months ended September 30, 2017 of $246 and $264 per Attributable Gold Equivalent ounce, respectively, compared with $255 and $261 per Attributable Gold Equivalent ounce for the comparable periods in 2016.

|

|

|

|

|

|

|

1.

|

Refer to section on non-IFRS and other measures of this MD&A.

|

New Anchor Asset

|

|

|

|

|

|

|

On July 3, 2017, Sandstorm completed its previously announced arrangement to acquire all the issued and ordinary share capital of Mariana Resources Ltd. (that Sandstorm did not already own). Under the terms of the arrangement and as consideration for the acquisition, the Company issued 32,685,228 common shares and paid an additional $47.3 million in cash. The transaction and the addition of the 30% Hot Maden interest to the Company’s portfolio of royalties provides for:

|

|

|

|

|

|

|

o

|

approximately 100% increase in estimated future production for only 19% dilution;

|

|

|

|

|

|

|

o

|

an anchor asset that is high-grade and low-cost with significant exploration upside;

|

|

|

|

|

|

|

o

|

a strong local partner with experience in exploring, developing, permitting and operating projects in Turkey; and

|

|

|

|

|

|

|

o

|

exploration properties in Côte d’Ivoire, Turkey, and Argentina. Sandstorm has begun the process to sell the exploration properties and expects to retain NSR royalties as well as equity in the spin-out.

|

Monetization of Securities

|

·

| |

On October 25, 2017, the Company agreed to sell $18.2 million in debt and equity securities of Trek Mining Inc. to Mr. Ross Beaty. The sale is conditional upon the closing of the announced business combination between Trek Mining, NewCastle Gold Ltd. and Anfield Gold Corp. The combined entity intends to operate under the name Equinox Gold Corp. and will be led by Mr. Ross Beaty as Chairman. The announced combination between Trek, NewCastle and Anfield is an encouraging development for Sandstorm shareholders. Sandstorm has existing royalties on properties that would be part of the Equinox Gold entity, and the combined company would be well financed to advance their assets into production. In addition, the monetization of a significant portion of Sandstorm’s debt and equity investments is a part of the Company’s strategy of selling non-core assets and using the capital raised to continue growing the stream and royalty portfolio. |

Gold Stream Amendment

|

·

| |

During the third quarter, the Company amended the Bachelor Lake gold stream with Metanor Resources Inc. Beginning October 1, 2017, Sandstorm will purchase 20% of the gold produced from the Bachelor Lake mine at an ongoing cost of $500 per ounce, until 12,000 ounces of gold have been purchased by the Company at which time the gold stream will convert into a 3.9% NSR royalty. As part of the amendment, Metanor has agreed it will sell a minimum of 1,500 ounces of gold to Sandstorm on a quarterly basis until the 12,000 ounce threshold has been reached. In consideration for the amendment, Sandstorm received: |

|

o

| |

a 3.9% NSR royalty on Metanor’s Barry project; and |

|

o

| |

$2.0 million in the common shares of Metanor. |

The amendment allows Sandstorm to maintain meaningful exposure to production from the Bachelor Lake mine while adding a royalty on the Barry project, an advanced exploration-stage asset located in the emerging Urban-Barry camp.

Newly Acquired Royalties

|

·

| |

Since September 2017, the Company has acquired 10 separate royalties on properties located in Peru, Botswana and South Africa. These royalties, which were purchased for an aggregate of $2.3 million, cover more than 1,000,000 hectares of property. |

Share Buy-Back Update

|

·

| |

Under the Company’s normal course issuer bid, the Company is able until April 4, 2018, to purchase approximately 7.6 million common shares. During the nine months ended September 30, 2017, the Company purchased approximately 3.3 million common shares. |

OVERVIEW

Sandstorm is a growth-focused company that seeks to acquire gold and other metals purchase agreements (“Gold Streams” or “Streams”) and royalties from companies that have advanced stage development projects or operating mines. In return for making upfront payments to acquire a Gold Stream, Sandstorm receives the right to purchase, at a fixed price per ounce or at a variable price based on spot, a percentage of a mine’s gold, silver, or other commodity ("Gold Equivalent") 1 production for the life of the mine. Sandstorm helps other companies in the resource industry grow their businesses, while acquiring attractive assets in the process. The Company is focused on acquiring Gold Streams and royalties from mines with low production costs, significant exploration potential and strong management teams. The Company currently has 171 Streams and net smelter returns royalties (“NSR”s), of which 20 of the underlying mines are producing.

|

|

|

|

1.

|

Refer to section on non-IFRS and other measures of this MD&A.

|

OUTLOOK

Based on the Company’s existing Gold Streams and NSRs, attributable Gold Equivalent production (individually and collectively referred to as “Attributable Gold Equivalent”) for 2017 is forecasted to be between 53,000 – 55,000 Attributable Gold Equivalent ounces. The Company is forecasting Attributable Gold Equivalent production of approximately 130,000 ounces per annum in 2022.

KEY PRODUCING ASSETS

|

|

|

|

Yamana Silver Stream

|

YAMANA GOLD INC.

|

The Company has a silver stream on Yamana Gold Inc.’s (“Yamana”) gold-silver Cerro Moro project, located in Santa Cruz, Argentina (the “Cerro Moro Project” or “Cerro Moro”) and an agreement to receive interim silver deliveries through 2018 from a number of Yamana’s currently operating mines.

Silver deliveries

Under the terms of the Yamana silver stream, Sandstorm has agreed to purchase, beginning January 1, 2019, for on-going per ounce cash payments equal to 30% of the spot price of silver, an amount of silver from Cerro Moro equal to 20% of the silver produced (up to an annual maximum of 1.2 million ounces of silver), until Yamana has delivered to Sandstorm 7.0 million ounces of silver; then 9% of the silver produced thereafter.

As part of the Yamana silver stream, through 2018, Sandstorm has also agreed to purchase, for on-going per ounce cash payments equal to 30% of the spot price of silver, an amount of silver from:

|

|

|

|

|

|

i.

|

the Minera Florida mine in Chile equal to 38% of the silver produced (up to an annual maximum of 200,000 ounces of silver); and

|

|

|

|

|

|

|

ii.

|

the Chapada mine in Brazil equal to 52% of the silver produced (up to an annual maximum of 100,000 ounces of silver).

|

Downside protection

If by January 1, 2019, the Cerro Moro processing facility has not averaged 80% of its daily nameplate production capacity over a 30-day period (the "Commencement of Production"), then Yamana´s producing El Peñon mine in Chile will provide a 24 month backstop until the Commencement of Production has begun. During the 24 month backstop, if applicable, Sandstorm will purchase, for on-going per ounce cash payments equal to 30% of the spot price of silver, an amount of silver equal to 16% of El Peñon´s silver production up to a maximum of 1.2 million ounces per annum.

About Cerro Moro

The Cerro Moro project is located approximately 70 kilometers southwest of the coastal port city of Puerto Deseado in the Santa Cruz province of Argentina. Cerro Moro contains a number of high grade epithermal gold and silver deposits, some of which will be mined via open pit and some via underground mining methods. The current plan indicates average annual production in the first three years of production of 150,000 ounces of gold and 7.2 million ounces of silver, with the life of mine annual production averaging approximately 130,000 ounces of gold and 6.4 million ounces of silver at a throughput of 1,000 tonnes per day.

|

|

|

|

|

|

»

|

Yamana recently reported that it is progressing well with respect to site construction activities and it anticipates the mechanical installation of the processing plant will be completed by the end of 2017.

|

|

|

|

|

|

|

»

|

Yamana’s 2017 exploration plan, which is anticipated to be part of a four year $30 million program, is aimed at expanding the Cerro Moro mineral resource. As part of that program, it was recently discovered that a 1,500 meter mineralized structure links the Esperanza and Escondida northwest mineral systems, with follow up drilling indicating that mineralization remains open along strike and down dip.

|

|

|

|

|

Chapada Copper Stream

|

YAMANA GOLD INC.

|

The Company has a copper stream on Yamana’s open pit gold-copper Chapada mine located 270 kilometers northwest of Brasília in Goiás State, Brazil (“Chapada” or the “Chapada Mine”). Under the terms of the Yamana copper stream, Sandstorm has agreed to purchase, for on-going per pound cash payments equal to 30% of the spot price of copper, an amount of copper from the Chapada Mine equal to:

|

|

|

|

|

|

i.

|

4.2% of the copper produced (up to an annual maximum of 3.9 million pounds of copper) until Yamana has delivered 39 million pounds of copper to Sandstorm (the “First Chapada Delivery Threshold”); then

|

|

|

|

|

|

|

ii.

|

3.0% of the copper produced until, on a cumulative basis, Yamana has delivered 50 million pounds of copper to Sandstorm (the “Second Chapada Delivery Threshold”); then

|

|

|

|

|

|

|

iii.

|

1.5% of the copper produced thereafter, for the life of the mine.

|

Downside protection

If Cerro Moro has not achieved the Commencement of Production and Sandstorm has not received cumulative pre-tax cash flow equal to $70 million from the Yamana silver stream, then the First Chapada Delivery Threshold and the Second Chapada Delivery Threshold will cease to be in effect and Sandstorm will continue to purchase 4.2% of Chapada’s payable copper production (up to an annual maximum of 3.9 million pounds of copper), until such time as Sandstorm has received cumulative pre-tax cash flow equal to $70 million, or Cerro Moro has achieved the Commencement of Production.

About Chapada

Chapada has been in production since 2007 and is a relatively low-cost South American operation. The ore is treated through a flotation plant with capacity of 22 million tonnes per annum. Yamana has benefitted from significant discoveries at Chapada in the past and in 2016 it announced an updated reserve statement which increased proven and probable copper mineral reserves to 3.25 billion pounds of copper contained in 559.5 million tonnes at 0.26% copper (see www.yamana.com for more information on this and recent drill results). Yamana recently announced positive results from its exploration program which is primarily focused on increasing mineral resources and mineral reserves by testing near mine and district targets including Baru, Suruca, Buriti and Formiga. Some of the highlights include: (i) the identification of a near surface, higher grade core to the Baru deposit that lies above Sucupira, a northeast to southwest trending mineral body immediately adjacent to the north wall of the main Chapada pit; (ii) at Suruca, current drilling has discovered a higher grade core to the mineralization that is at or above current life of mine grades with metallurgy similar to the Chapada deposit; (iii) a new copper-gold mineralization identified three kilometers from the Chapada mine, called the Buriti target which adds another near surface discovery at Chapada; and (iv) given the proximity of the Baru and Sucupira deposits to plant infrastructure, studies are underway to review a larger open pit scenario that would include both these deposits.

|

|

|

|

Diavik Diamond Royalty

|

RIO TINTO PLC

|

The Company has a 1% gross proceeds royalty based on the production from the Diavik mine located in Lac de Gras, Northwest Territories, Canada (“Diavik” or the “Diavik Mine”) which is operated by Rio Tinto PLC (“Rio Tinto”).

The Diavik Mine is Canada’s largest diamond mine. The mine began producing diamonds in January 2003, and has since produced more than 100 million carats from three kimberlite pipes (A154 South, A154 North, and A418). Rio Tinto has approved the development of an open pit mine on a fourth pipe (A21) which is targeted for production in 2018. Recent public announcements have indicated that the development of A21 pipe continues to progress according to plan.

|

|

|

|

|

|

»

|

A year end reserve was filed for the Diavik Mine which when compared to the 2015 technical report, adds approximately 6.7 million carats to the mineral reserves. For more information refer to www.ddcorp.ca.

|

|

|

|

|

|

|

»

|

In accordance with the project plan, the completion of the A21 dike and the start of dewatering are expected by the end of 2017.

|

|

|

|

|

Santa Elena Gold Stream

|

FIRST MAJESTIC SILVER CORP.

|

The Company has a Gold Stream to purchase 20% of the life of mine gold produced from First Majestic Silver Corp.’s (“First Majestic”) open-pit and underground Santa Elena mine, located in Mexico (the “Santa Elena Mine”), for a per ounce cash payment equal to the lesser of $450 and the then prevailing market price of gold.

The Santa Elena Mine was successfully transitioned from an open pit heap leach operation to an underground mining and milling operation and commercial production for the 3,000 tonne per day processing plant was declared in 2014.

|

|

|

|

|

|

»

|

First Majestic recently announced that it had successfully completed the connection of the San Salvador ramp to the Main vein which has resulted in a reduction in haulage bottlenecks and has improved mine planning logistics. In addition, the new ramp is expected to support future exploration activities around the Tortuga vein.

|

|

|

|

|

Black Fox Gold Stream

|

MCEWEN MINING INC.

|

The Company has a Gold Stream to purchase 8% of the life of mine gold produced from McEwen Mining Inc.’s (“McEwen”) open pit and underground Black Fox mine, located in Ontario, Canada (the “Black Fox Mine”), and 6.3% of the life of mine gold produced from McEwen’s Black Fox Extension, which includes a portion of McEwen’s Pike River concessions, for a per ounce cash payment equal to the lesser of $531 and the then prevailing market price of gold.

The Black Fox Mine began operating as an open pit mine in 2009 (depleted in 2015) and transitioned to underground operations in 2011. On October 6, 2017, McEwen completed its previously announced acquisition of the Black Fox Mine from the previous owner, Primero Mining Corp.

|

|

|

|

Bachelor Lake Gold Stream

|

METANOR RESOURCES INC.

|

On September 29, 2017, the Company amended its Gold Stream with Metanor Resources Inc (“Metanor”). Beginning October 1, 2017, Sandstorm will purchase 20% of the gold produced from Metanor’s Bachelor Lake gold mine located in Quebec, Canada (the “Bachelor Lake Mine”), for a per ounce cash payment equal to the lesser of $500 and the then prevailing market price of gold, until 12,000 ounces of gold have been purchased by the Company at which time the Gold Stream will convert into a 3.9% NSR royalty. As part of the amendment, Metanor has agreed it will sell a minimum of 1,500 ounces of gold to Sandstorm on a quarterly basis until the 12,000 ounce threshold has been reached. Under the previous Gold Stream, there were no requirements for minimum deliveries nor was there a subsequent conversion of the Gold Stream into a NSR royalty. In consideration for entering into the amendment, Sandstorm received:

|

o

| |

a 3.9% NSR royalty on Metanor’s Barry project; and |

|

o

| |

$2.0 million in the common shares of Metanor. |

Metanor may elect to reduce the 3.9% NSR royalty on the Bachelor Lake or Barry projects by making a $2.0 million payment to Sandstorm in each case (the “Purchase Option”). Upon exercising either of the Purchase Options, the respective Sandstorm NSR royalty will decrease to 1.8%. In addition to the Gold Stream, Sandstorm has an already existing 1% NSR royalty on the Bachelor Lake gold mine, which remains unaffected by the amendment. In connection with the amendment, the Company recognized a gain of $3.0 million during the three months ended September 30, 2017.

The Bachelor Lake Mine is an underground mining operation with an operating mill and surface infrastructure, which began production in early 2013. The amendment not only allows Sandstorm to maintain meaningful exposure to the production from the Bachelor Lake mine, but it also adds a royalty on the Barry project, which is an advanced exploration-stage asset located in the emerging Urban-Barry camp. Metanor is currently conducting exploration drilling at the Barry project and has plans to complete a pre-feasibility study as it continues the permitting process.

|

The Bachelor Lake Mine is an underground mining operation with an operating mill and surface infrastructure, which began production in early 2013.

|

|

|

|

|

|

|

|

|

|

|

Karma Gold Stream

|

ENDEAVOUR MINING CORP.

|

The Company has a Gold Stream which entitles it to purchase 25,000 ounces of gold over a five year period and thereafter 1.625% of the gold produced from Endeavour Mining Corporation’s (“Endeavour”) open-pit heap leach Karma gold mine located in Burkina Faso, West Africa (“Karma” or the “Karma Mine”) for on-going per ounce cash payment equal to 20% of the spot price of the gold.

The Gold Stream, which on a gross basis requires Endeavour to deliver 100,000 ounces of gold over a five year period starting March 31, 2016 and thereafter 6.5% of the equivalent gold production at the Karma Mine, is syndicated 75% and 25% between Franco-Nevada Corp. and Sandstorm, respectively (together the “Stream Syndicate”).

The Karma Mine has five defined mineral deposits that make up the Karma project. Based on recent drilling, Endeavour has extended the mine life beyond 10 years.

|

|

|

|

|

|

»

|

A 60,000 meter exploration drilling program, at Kao North, was completed in 2016, which confirmed the continuity of the previous inferred resource, identified resources amenable to heap leach processing and converted mineral resources into mineral reserves. For more information refer to www.endeavourmining.com .

|

|

|

|

|

|

|

»

|

Endeavour has a $4 million exploration program to drill near-mill targets such as Rambo West and Yabonsgo.

|

|

|

|

|

Bracemac-McLeod Royalty

|

GLENCORE PLC

|

Sandstorm has a 3% NSR based on 100% of the production from the Bracemac-McLeod property located in Matagami, Quebec, Canada (“Bracemac-McLeod” or the “Bracemac-McLeod Mine”) which is owned and operated by a subsidiary of Glencore plc (“Glencore”).

The Bracemac-McLeod Mine is a high grade volcanogenic massive sulphide deposit located in the historic and prolific Matagami mining district of Quebec. Continuous mining and milling operations have been active in the Matagami district for over fifty years with ten previously operating mines and one other currently producing mine. The Bracemac-McLeod Mine began initial production in the second half of 2013.

|

|

|

|

Ming Gold Stream

|

RAMBLER METALS & MINING PLC

|

The Company has a Gold Stream to purchase approximately 25% of the first 175,000 ounces of gold produced and 12% of the life of mine gold produced thereafter, from Rambler Metals & Mining PLC’s (“Rambler”) Ming Copper-Gold mine, located in Newfoundland, Canada (the “Ming Mine”). There are no ongoing per ounce payments required by Sandstorm in respect of the Ming Mine Gold Stream. In the event that the metallurgical recoveries of gold at the Ming Mine are below 85%, the percentage of gold that Sandstorm shall be entitled to purchase shall be increased proportionally. Based on 2016 metallurgical recoveries, Sandstorm’s 2017 gold purchase entitlement was adjusted to 32%.

|

|

|

|

|

|

»

|

Rambler has begun a surface diamond drilling program targeting the depth extension of both the Lower Footwall Zone and the high grade Ming Massive Sulphides. For more information refer to www.ramblermines.com

|

OTHER PRODUCING ASSETS

|

|

|

|

Emigrant Springs

|

NEWMONT MINING CORP.

|

The Company has a 1.5% NSR on the Emigrant Springs mine (the “Emigrant Springs Mine”) which is located in the Carlin Trend in Nevada, U.S.A. and is owned and operated by Newmont Mining Corp. (“Newmont”). The Emigrant Springs Mine is an open pit, heap leach operation that has been in production since the third quarter of 2012.

|

|

|

|

Gualcamayo Royalty

|

YAMANA GOLD INC.

|

The Company has a 1% NSR on the Gualcamayo gold mine (the “Gualcamayo Mine”) which is located in San Juan province, Argentina and owned and operated by Yamana. The Gualcamayo Mine is an open pit, heap leach operation encompassing three substantial zones of gold mineralization. Yamana recently announced exploration success in near pit targets of Cerro Condor and Potenciales which, Yamana believes, provides support for extending the life of the open pit.

|

|

|

|

Mine Waste Solutions Royalty

|

ANGLOGOLD ASHANTI LTD.

|

The Company has a 1% NSR on the gold produced from Mine Waste Solutions tailings recovery operation (“MWS”) which is located near Stilfontein, South Africa, and is owned and operated by AngloGold Ashanti Ltd. (“AngloGold”). MWS is a gold and uranium tailings recovery operation. The operation re-processes multiple tailings dumps in the area through three production modules, the last of which was commissioned in 2011.

|

|

|

|

San Andres Royalty

|

AURA MINERALS INC.

|

The Company has a 1.5% NSR on the San Andres mine (the “San Andres Mine”) which is located in La Únion, Honduras and is owned and operated by Aura Minerals Inc. (“Aura Minerals”). The San Andres Mine is an open pit, heap leach operation. The mine has been in production since 1983 and has well-developed infrastructure, which includes power and water supply, warehouses, maintenance facilities, assay laboratory and on-site camp facilities.

DEVELOPMENT ASSETS

|

|

|

|

Hot Maden

|

LYDIA MADENCILIK A.S

|

The Company has a 30% interest and a 2% NSR on the Hot Maden gold-copper project which is located in the Artvin Province, northeastern Turkey (the “Hot Maden Project” or “Hot Maden”). The project is operated and co-owned by a Turkish partner, Lidya Madencilik Sanayi ve Ticaret A.S. (“Lydia”), which owns the remaining 70% interest in the project. Lydia is an experienced Turkish company who is also a joint-venture partner with Alacer Gold Corp. on the producing Çöpler mine in Turkey. The Hot Maden Project is envisaged as a conventional underground mine and processing facility producing concentrates without the use of cyanide.

On July 3, 2017, Sandstorm completed its previously announced arrangement to acquire all the issued and ordinary share capital of Mariana Resources Ltd. (“Mariana”) (that Sandstorm did not already own) (the “Arrangement”). Under the terms of the Arrangement and as consideration for the acquisition, the Company issued 32,685,228 common shares and paid an additional $47.3 million in cash. The highlights of the transaction and the addition of the 30% Hot Maden interest to the Company’s portfolio include:

|

|

|

|

|

|

|

100% increase in expected future production for 19% dilution;

|

|

|

|

|

|

|

o

|

Hot Maden is an anchor asset that is expected to increase the Company’s attributable gold equivalent ounces to approximately 130,000 in 2022.

|

|

|

|

|

|

|

|

Hot Maden is a high-grade, low-cost asset with significant exploration upside;

|

|

|

|

|

|

|

o

|

The Preliminary Economic Assessment (effective date of March 1, 2017) demonstrated robust estimated economics with estimated all-in-sustaining costs of less than $400 per gold equivalent ounce. The high-grade nature of the orebody and the wide intercepts of mineralization provide the potential for low-cost mining methods.

|

|

|

|

|

|

|

o

|

Total land package is 74 square kilometers in size with the current focus being a 7.0 kilometer long north-south alteration zone. The majority of the exploration drilling has been within a 1.0 kilometer strike length of this alteration zone with several exploration targets identified along strike and parallel to the identified orebody.

|

|

|

|

|

|

|

|

Majority operator Lydia is a strong local partner with experience exploring, developing, permitting and operating projects in Turkey.

|

|

|

|

|

|

|

o

|

Lidya is part of a large Turkish conglomerate called Çalik Holding and is currently partnered with Alacer Gold Corp. on several projects in Turkey including the producing Çöpler mine and the development-stage Gediktepe and Kartaltepe projects.

|

|

|

|

|

|

|

|

Acquisition of Mariana includes exploration properties in Côte d’Ivoire, Turkey, and Argentina. Sandstorm has begun the process to sell the exploration properties and expects to retain NSR royalties as well as equity in the spin-out.

|

|

|

|

|

Aurizona Gold Royalty

|

TREK MINING INC.

|

The Company has a 3% – 5% sliding scale NSR on the production from Trek Mining Inc.’s (“Trek”) open-pit Aurizona mine, located in Brazil (“Aurizona” or the “Aurizona Mine”). At gold prices less than or equal to $1,500 per ounce, the royalty is a 3% NSR. In addition, Sandstorm holds a 2% NSR on Trek’s 190,073 hectares of greenfields exploration ground. At any time prior to the commencement of commercial production, Trek has the ability to purchase one-half of the greenfields NSR for a cash payment of $10 million.

On July 31, 2017, Trek released results of a feasibility study including proven and probable mineral reserves of 971,000 ounces of gold (contained in 19.8 million tonnes at 1.5 grams per tonne gold with a cut-off grade of 0.4 grams per tonne from Boa Esperanza and 0.6 grams per tonne from Piaba) with expected annual production of 136,000 ounces. Trek recently announced that it had intersected two new zones of gold mineralization at the near mine target of Genipapo. In addition, Trek has commenced a second phase of exploration drilling at Aurizona with five diamond drill rigs working to complete a 12,000 meter drill campaign. The focus of the campaign is to test several near mine targets including follow-up drilling at Genipapo and additional infill drilling at Piaba West. For more information refer to www.trekmining.com . Trek also has an exploration agreement with AngloGold covering the greenfields exploration property. Sandstorm holds a right of first refusal on any future streams or royalties on the Aurizona project and greenfields property.

On March 31, 2017, Luna Gold Inc. (“Luna”) completed its previously announced merger with JDL Gold Corp creating Trek, a new multi-asset company with over C$110 million in cash. Concurrent with the closing of the transaction, the term debt facility that was owed to Sandstorm, in the amount of $20 million plus accrued interest, was settled in the equity of Trek. The Company recognized a gain of $1.8 million on the settlement of the debt. On October 25, 2017, Trek announced that it had entered into an agreement to acquire NewCastle Gold Ltd. and Anfield Gold Corp. The combined entity intends to operate under the name Equinox Gold Corp. and will be led by Mr. Ross Beaty as Chairman. The announced combination is an encouraging development for Sandstorm shareholders as Sandstorm has existing royalties on properties that would be part of the Equinox Gold Corp entity and the combined company would be well financed to advance their assets into production. In conjunction with the transaction, Sandstorm agreed to sell $18.2 million in debt and equity securities of Trek to Mr. Ross Beaty. The sale is conditional upon the closing of the announced business combination between Trek, NewCastle Gold Ltd. and Anfield Gold Corp. The monetization of a significant portion of Sandstorm’s debt and equity investments is a part of the Company’s strategy of selling non-core assets and using the capital raised to continue growing the stream and royalty portfolio.

|

|

|

|

Hugo North Extension & Heruga Gold Stream

|

ENTRÉE RESOURCES LTD

|

The Company has a Gold Stream with Entrée Resources Ltd. (“Entrée”) to purchase an amount equal to 5.62% and 4.26% of the gold and silver by-products produced from the Hugo North Extension and Heruga deposits located in Mongolia, (the “Hugo North Extension” and “Heruga”, respectively) for per ounce cash payments equal to the lesser of $220 per ounce of gold and $5 per ounce of silver and the then prevailing market price of gold and silver, respectively. Additionally, Sandstorm has a copper stream to purchase an amount equal to 0.42% of the copper produced from Hugo North Extension and Heruga for per pound cash payments equal to the lesser of $0.50 per pound of copper and the then prevailing market price of copper.

The Company is not required to contribute any further capital, exploration, or operating expenditures to Entrée.

The Hugo North Extension is a rich copper-gold porphyry deposit and Heruga is a copper-gold-molybdenum porphyry deposit. Both projects are located in the South Gobi desert of Mongolia, approximately 570 kilometers south of the capital city of Ulaanbaatar and 80 kilometers north of the border with China. The Hugo North Extension and Heruga are part of the Oyu Tolgoi mining complex and are managed by Oyu Tolgoi LLC, a subsidiary of Turquoise Hill Resources Ltd. (“Turquoise Hill”) and the Government of Mongolia, and its project manager Rio Tinto PLC. Entrée retains a 20% interest in the resource deposits of the Hugo North Extension and Heruga.

Entrée recently announced that a 43-101 technical report relating to its interests in the Hugo North Extension and Heruga is underway and expected to be released in 2018. Once completed, the report will allow Entrée to discuss preliminary economics for the potential future phases of the Oyu Tolgoi mine, beyond Lift 1, including Lift 2 and Heruga.

|

|

|

|

Hackett River Royalty

|

GLENCORE PLC

|

The Company has a 2% NSR on the Hackett River property located in Nunavut, Canada (the “Hackett River Project” or “Hackett River”) which is owned by a subsidiary of Glencore.

Hackett River is a silver-rich volcanogenic massive sulphide deposit and is one of the largest undeveloped projects of its kind. The property contains four massive sulphide bodies that occur over a 6.6 kilometer strike length. A preliminary economic assessment updated in 2010 evaluated a possible large-scale open pit and underground operation, processing up to 17,000 tonnes per day. The most recent technical report, completed in 2013, reported 25.0 million tonnes of indicated resources containing 4.2% zinc and 130.0 grams per tonne silver plus 57.0 million tonnes of inferred resources with 3.0% zinc and 100.0 grams per tonne silver. For more information refer to the technical reports dated July 26, 2010 and July 31, 2013 under Sabina Gold & Silver Corp’s profile on www.sedar.com. Glencore has recently disclosed that a pre-feasibility study is currently underway and that they are revisiting both the mining methods and boundaries between open pit and underground.

|

|

|

|

Lobo-Marte Royalty

|

KINROSS GOLD CORP.

|

The Company has a 1.05% NSR on production from the Lobo-Marte project located in the Maricunga gold district of Chile (the “Lobo-Marte Project” or “Lobo-Marte”) which is owned by Kinross Gold Corp. (“Kinross”).

Kinross completed a pre-feasibility study at Lobo-Marte that contemplated an open-pit/ heap-leach operation. As a result of changes in the plan of operations and other factors, Kinross withdrew its previously submitted permit application. Future development and operations at Lobo-Marte will require the re-initiation of the permitting process. For more information refer to www.kinross.com.

|

|

|

|

Agi Dagi & Kirazli Royalty

|

ALAMOS GOLD INC.

|

The Company has a $10 per ounce royalty based on the production from the Agi Dagi and the Kirazli gold development projects located in the Çanakkale Province of northwestern Turkey (“Agi Dagi” and “Kirazli”, respectively) which are both owned by Alamos Gold Inc. (“Alamos Gold”). The royalty is payable by Newmont and is subject to a maximum of 600,000 ounces from Agi Dagi and a maximum of 250,000 ounces from Kirazli.

A 2017 feasibility study on Agi Dagi and a 2017 feasibility study on Kirazli contemplated both projects as stand-alone open-pit, heap-leach operations. Under the respective studies, Agi Dagi is expected to produce an average of 177,600 ounces of gold per year over a 6 year mine life while Kirazli is expected to produce an average of 104,000 ounces of gold per year over a 5 year mine life. For more information refer to www.alamosgold.com.

|

|

|

|

Prairie Creek Royalty

|

CANADIAN ZINC CORPORATION

|

The Company has a 1.2% NSR on the Prairie Creek project (the “Prairie Creek Project”) located in the Northwest Territories, Canada and owned by Canadian Zinc Corporation (“Canadian Zinc”). The Prairie Creek Project is a zinc, silver and lead project that is 100%-owned by Canadian Zinc and based on a recently announced feasibility study has a proven and probable mineral reserve of 8.1 million tonnes containing 8.6% zinc, 124.2 grams per tonne silver and 8.1% lead. Canadian Zinc recently announced that the Mackenzie Valley Environmental Impact Review Board had recommended approval for the proposed all season road at the Prairie Creek Project. Development of the all season road will enable the transportation of concentrates and supplies throughout the year. For more information, refer to www.canadianzinc.com.

|

|

|

|

Mt. Hamilton Royalty

|

WATERTON PRECIOUS METALS FUND II CAYMAN, LP

|

The Company has a 2.4% NSR on the Mt. Hamilton gold project (the "Mt. Hamilton Project"). The Mt. Hamilton Project is located in White Pine County, Nevada, U.S.A. and is owned by Waterton Precious Metals Fund II Cayman, LP (“Waterton”).

Sandstorm holds a right of first refusal on any future royalty or gold stream financing for the Mt. Hamilton Project.

IMPAIRMENT

While assessing whether any indications of impairment exist for mineral interests and royalties, consideration is given to both external and internal sources of information. A reduction in the mineral resource estimate for the Coringa gold project prompted the Company to evaluate the carrying value of its royalty investment. During the three months ended June 30, 2017 and as a result of this review, the Company recorded an impairment charge of $4.5 million.

OTHER

Under the Company’s normal course issuer bid (“NCIB”), the Company is able until April 4, 2018, to purchase up to 7.6 million common shares. The NCIB provides the Company with the option to purchase its common shares from time to time. During the nine months ended September 30, 2017 and pursuant to the NCIB, the Company purchased and cancelled approximately 3.3 million common shares.

On January 26, 2017, Orezone Gold Corporation (“Orezone”) exercised its option to repurchase the royalty on the Bomboré gold project for $3.6 million, representing a 20% premium to the original upfront payment. Sandstorm retains a right of first refusal on any future stream or royalty financings related to the Bomboré gold project.

SUMMARY OF QUARTERLY RESULTS

Quarters Ended

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

In $000s

|

|

Sep. 30, 2017

|

|

Jun. 30, 2017

|

|

Mar. 31, 2017

|

|

Dec. 31, 2016

|

|

Total revenue

|

|

$

|

17,939

|

|

$

|

16,066

|

|

$

|

18,824

|

|

$

|

16,463

|

|

Attributable Gold Equivalent ounces sold 1

|

|

|

14,293

|

|

|

12,750

|

|

|

15,558

|

|

|

13,245

|

|

Sales

|

|

$

|

11,534

|

|

$

|

11,835

|

|

$

|

12,861

|

|

$

|

10,970

|

|

Royalty revenue

|

|

|

6,405

|

|

|

4,231

|

|

|

5,963

|

|

|

5,493

|

|

Average realized gold price per attributable ounce 1

|

|

|

1,255

|

|

|

1,260

|

|

|

1,210

|

|

|

1,243

|

|

Average cash cost per attributable ounce 1

|

|

|

246

|

|

|

290

|

|

|

258

|

|

|

250

|

|

Cash flows from operating activities

|

|

|

11,864

|

|

|

11,112

|

|

|

11,938

|

|

|

10,058

|

|

Net income (loss)

|

|

|

4,773

|

|

|

(1,909)

|

|

|

6,964

|

|

|

(19)

|

|

Basic income (loss) per share

|

|

|

0.03

|

|

|

(0.01)

|

|

|

0.05

|

|

|

(0.00)

|

|

Diluted income (loss) per share

|

|

|

0.02

|

|

|

(0.01)

|

|

|

0.04

|

|

|

(0.00)

|

|

Total assets

|

|

|

667,185

|

|

|

545,557

|

|

|

550,342

|

|

|

534,882

|

|

Total long-term liabilities

|

|

|

2,915

|

|

|

2,969

|

|

|

3,197

|

|

|

3,288

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

In $000s

|

|

Sep. 30, 2016

|

|

Jun. 30, 2016

|

|

Mar. 31, 2016

|

|

Dec. 31, 2015

|

|

Total revenue

|

|

$

|

16,815

|

|

$

|

15,709

|

|

$

|

13,384

|

|

$

|

9,863

|

|

Attributable Gold Equivalent ounces sold 1

|

|

|

12,588

|

|

|

12,517

|

|

|

11,381

|

|

|

8,951

|

|

Sales

|

|

$

|

11,302

|

|

$

|

10,858

|

|

$

|

8,504

|

|

$

|

6,604

|

|

Royalty revenue

|

|

|

5,513

|

|

|

4,851

|

|

|

4,880

|

|

|

3,259

|

|

Average realized gold price per attributable ounce 1

|

|

|

1,336

|

|

|

1,255

|

|

|

1,176

|

|

|

1,102

|

|

Average cash cost per attributable ounce 1

|

|

|

255

|

|

|

261

|

|

|

267

|

|

|

258

|

|

Cash flows from operating activities

|

|

|

10,313

|

|

|

8,935

|

|

|

9,685

|

|

|

4,987

|

|

Net income (loss)

|

|

|

6,915

|

|

|

5,199

|

|

|

13,159

|

|

|

(24,960)

|

|

Basic income (loss) per share

|

|

|

0.05

|

|

|

0.04

|

|

|

0.10

|

|

|

(0.20)

|

|

Diluted income (loss) per share

|

|

|

0.04

|

|

|

0.04

|

|

|

0.10

|

|

|

(0.20)

|

|

Total assets

|

|

|

540,419

|

|

|

525,353

|

|

|

531,160

|

|

|

496,873

|

|

Total long-term liabilities

|

|

|

3,320

|

|

|

62,854

|

|

|

80,130

|

|

|

86,779

|

|

|

|

|

1.

|

Refer to section on non-IFRS and other measures of this MD&A.

|

|

|

|

Attributable Gold Equivalent Ounces Sold Sales & Royalty Revenue in US$000’s average realized gold price 13,245 15,558 12,750 14,293 Q4 Q1 Q2 Q3 2016 1027 $16,463 $18,824 $16,066 $17,939 $1,243 $1,210 $1,260 $1,255 Gold Equivalent Ounces Sold Sales & Royalty Revenue in US$000’s average realized gold price 13,245 15,558 12,750 14,293 Q4 Q1 Q2 Q3 2016 1027 $16,463 $18,824 $16,066 $17,939 $1,243 $1,210 $1,260 $1,255

|

Changes in sales, net income and cash flow from operating activities from quarter to quarter are affected primarily by fluctuations in production at the mines, the timing of shipments, changes in the price of commodities, as well as acquisitions of Streams and royalty agreements and the commencement of operations of mines under construction. For more information refer to the quarterly commentary discussed below.

The Company’s operating segments for the three months ended

September 30, 2017 are summarized in the table below:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

In 000s

|

|

Attributable Gold Equivalent ounces sold

|

|

Sales and

royalty

revenues

|

|

Cost of sales, excluding depletion

|

|

Depletion expense

|

|

Impairment of mineral, royalty

and other interests

|

|

Income (loss)

before taxes

|

|

Cash flow

from operating

activities

|

|

Bachelor Lake

|

|

1,264

|

|

$

|

1,578

|

|

$

|

599

|

|

$

|

973

|

|

$

|

-

|

|

$

|

6

|

|

$

|

861

|

|

Black Fox

|

|

1,383

|

|

|

1,716

|

|

|

735

|

|

|

653

|

|

|

-

|

|

|

328

|

|

|

1,115

|

|

Chapada

|

|

2,107

|

|

|

2,644

|

|

|

774

|

|

|

931

|

|

|

-

|

|

|

939

|

|

|

1,870

|

|

Diavik

|

|

1,785

|

|

|

2,240

|

|

|

-

|

|

|

1,244

|

|

|

-

|

|

|

996

|

|

|

1,840

|

|

Karma

|

|

1,068

|

|

|

1,351

|

|

|

268

|

|

|

671

|

|

|

-

|

|

|

412

|

|

|

974

|

|

Ming

|

|

237

|

|

|

291

|

|

|

-

|

|

|

125

|

|

|

-

|

|

|

166

|

|

|

291

|

|

Santa Elena

|

|

2,307

|

|

|

2,922

|

|

|

840

|

|

|

265

|

|

|

-

|

|

|

1,817

|

|

|

2,013

|

|

Yamana silver stream

|

|

781

|

|

|

981

|

|

|

285

|

|

|

561

|

|

|

-

|

|

|

135

|

|

|

695

|

|

Other Royalties

|

|

3,253

|

|

|

4,082

|

|

|

-

|

|

|

1,704

|

|

|

-

|

|

|

2,378

|

|

|

3,818

|

|

Other

|

|

108

|

|

|

134

|

|

|

11

|

|

|

42

|

|

|

-

|

|

|

81

|

|

|

124

|

|

Corporate

|

|

-

|

|

|

-

|

|

|

-

|

|

|

-

|

|

|

-

|

|

|

(464)

|

|

|

(1,737)

|

|

Consolidated

|

|

14,293

|

|

$

|

17,939

|

|

$

|

3,512

|

|

$

|

7,169

|

|

$

|

-

|

|

$

|

6,794

|

|

$

|

11,864

|

The Company’s operating segments for the three months ended

September 30, 2016 are summarized in the table below:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

In 000s

|

|

Attributable Gold Equivalent ounces sold

|

|

Sales and

royalty

revenues

|

|

Cost of sales,

excluding depletion

|

|

Depletion expense

|

|

Impairment of mineral, royalty

and other interests

|

|

Income (loss)

before taxes

|

|

Cash flow

from operating activities

|

|

Bachelor Lake

|

|

1,988

|

|

$

|

2,657

|

|

$

|

958

|

|

$

|

1,023

|

|

$

|

-

|

|

$

|

676

|

|

$

|

1,898

|

|

Black Fox

|

|

983

|

|

|

1,314

|

|

|

515

|

|

|

439

|

|

|

-

|

|

|

360

|

|

|

578

|

|

Chapada

|

|

1,230

|

|

|

1,643

|

|

|

489

|

|

|

707

|

|

|

-

|

|

|

447

|

|

|

1,154

|

|

Diavik

|

|

1,175

|

|

|

1,570

|

|

|

-

|

|

|

1,070

|

|

|

-

|

|

|

500

|

|

|

1,670

|

|

Karma

|

|

1,250

|

|

|

1,669

|

|

|

333

|

|

|

785

|

|

|

-

|

|

|

551

|

|

|

1,336

|

|

Ming

|

|

598

|

|

|

802

|

|

|

-

|

|

|

282

|

|

|

-

|

|

|

520

|

|

|

802

|

|

Santa Elena

|

|

1,951

|

|

|

2,601

|

|

|

704

|

|

|

359

|

|

|

-

|

|

|

1,538

|

|

|

1,897

|

|

Yamana silver stream

|

|

533

|

|

|

712

|

|

|

212

|

|

|

306

|

|

|

-

|

|

|

194

|

|

|

500

|

|

Other Royalties

|

|

2,880

|

|

|

3,847

|

|

|

-

|

|

|

2,354

|

|

|

1,139

|

|

|

354

|

|

|

3,595

|

|

Corporate

|

|

-

|

|

|

-

|

|

|

-

|

|

|

-

|

|

|

-

|

|

|

3,282

|

|

|

(3,117)

|

|

Consolidated

|

|

12,588

|

|

$

|

16,815

|

|

$

|

3,211

|

|

$

|

7,325

|

|

$

|

1,139

|

|

$

|

8,422

|

|

$

|

10,313

|

|

|

|

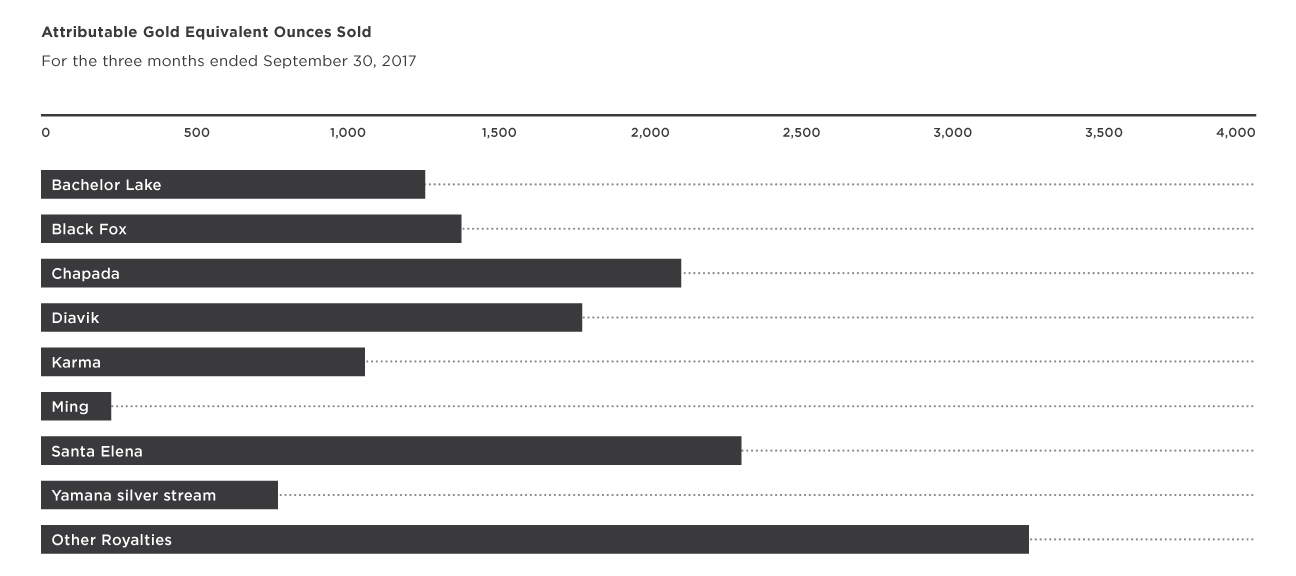

Attributable Gold Equivalent Ounces Sold For the three months ended September 30, 2017 0 500 1,000 1,500 2,000 2,500 3,000 3,500 4,000 Bachelor Lak Black Fox Chapada Diavik Karma Min Santa Elena Yamana Silver stream Other Royalties

|

|

|

|

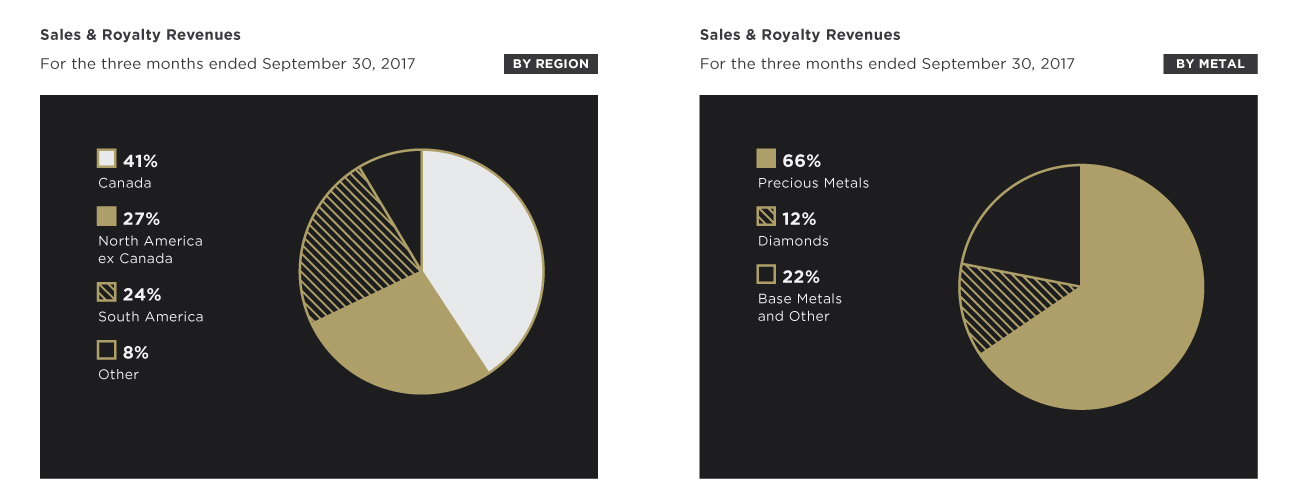

Sales & Royalty Revenues For the three months ended September 30, 2017 By Region By Metal 41% Canada 27% North America ex Canada 24% South America 8% Other 66% Precious Metals 12% Diamonds 22% Base Metals and Other

|

THREE MONTHS ENDED SEPTEMBER 30, 2017

COMPARED TO THE THREE MONTHS ENDED SEPTEMBER 30, 2016

For the three months ended September 30, 2017, net income and cash flow from operating activities were $4.8 million and $11.9 million, respectively, compared with net income and cash flow from operating activities of $6.9 million and $10.3 million for the comparable period in 2016. The change is attributable to a combination of factors including:

|

NSR

|

|

|

|

A $3.4 million gain primarily resulting from the Bachelor Lake Gold Stream amendment for which Sandstorm received consideration consisting of $2.0 million in the common shares of Metanor and a 3.9% NSR on Metanor’s Barry project;

|

|

|

|

|

|

|

|

An increase of $0.8 million in administration expenses partly driven by the acquisition of Mariana and related operating costs. The Company expects these costs to decline as it executes on its strategy of selling the exploration properties which were acquired as part of the Mariana acquisition; and

|

|

|

|

|

|

|

|

|

|

|

|

Certain items recognized during the three months ended September 30, 2016 did not occur during the three months ended September 30, 2017 including a $5.8 million gain on the revaluation of the Company’s investments largely driven by the change in fair value of the Trek convertible debenture and Trek warrants; partially offset by a $1.1 million non-cash impairment charge relating to certain of the Company’s mineral interests.

|

For the three months ended September 30, 2017, revenue was $17.9 million compared with $16.8 million for the comparable period in 2016. The increase is largely attributed to a number of factors including:

|

|

|

|

|

|

|

14% increase in the number of Attributable Gold Equivalent ounces sold consisting of:

|

|

|

|

|

|

|

i.

|

An additional 1,125 Attributable Gold Equivalent ounces sold from the Company’s Yamana silver stream and Chapada copper stream. The increase was largely related to the timing of shipments; whereby, under the terms of the agreements, the time period over which the calculation of the maximum thresholds for deliveries was revised. These revisions resulted in the production thresholds being calculated on a quarterly basis as opposed to a monthly basis; thereby, reducing the variability of deliveries and annual true ups;

|

|

|

|

|

|

|

ii.

|

An increase in the number gold ounces sold from the Santa Elena Mine; and

|

|

|

|

|

|

|

iii.

|

An increase in the number of gold ounces sold from the Black Fox Mine;

|

|

|

|

|

|

Partially offset by:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A 6% decrease in the average realized selling price of gold.

|

NINE MONTHS ENDED SEPTEMBER 30, 2017

COMPARED TO THE NINE MONTHS ENDED SEPTEMBER 30, 2016

For the nine months ended September 30, 2017, net income and cash flow from operating activities were $9.8 million and $34.9 million, respectively, compared with net income and cash flow from operating activities of $25.3 million and $28.9 million for the comparable period in 2016. The change is attributable to a combination of factors including:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A $5.6 million gain primarily consisting of (i) $3.0 million, which was recognized during the three months ended September 30, 2017, arising from the Bachelor Lake Gold Stream amendment; (ii) a $1.8 million gain relating to the settlement of the Trek (previously Luna) debt and a $0.6 million gain relating to the 20% premium associated with Orezone exercising its option to repurchase the royalty on the Bomboré gold project, both of which were recognized during the three months ended March 31, 2017;

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

During the three months ended June 30, 2017, the Company recognized a $1.9 million foreign exchange gain primarily driven from currency trades and the resulting cash held in escrow which were required to meet the cash commitments under Sandstorm’s bid to acquire Mariana; and

|

|

|

|

|

|

|

|

|

|

|

|

During the nine months ended September 30, 2017, the Company recognized a $0.6 million decrease in project evaluation costs primarily driven by cost reduction strategies;

|

Offset by:

|

|

|

|

|

|

|

The recognition of a $4.5 million non-cash impairment charge, during the three months ended June 30, 2017, relating to the Company’s royalty on the Coringa gold project;

|

|

|

|

|

|

|

|

During the nine months ended September 30, 2017, the Company recognized a $3.4 million increase in depletion expense largely driven by an increase in the number of Attributable Gold Equivalent ounces sold;

|

|

|

|

|

|

|

|

During the nine months ended September 30, 2017, the Company recognized an increase of $1.2 million in administration expenses partly driven by the acquisition of Mariana and related operating costs. The Company expects these costs to decline as it executes on its strategy of selling the exploration properties which were acquired as part of the Mariana acquisition; and

|

|

|

|

|

|

|

|

A decrease in the gains recognized on the revaluation of the Company’s investments; whereby, a gain of $1.4 million was recognized during the nine months ended September 30, 2017 which was $23.8 million less when compared to the nine months ended September 30, 2016.

|

For the nine months ended September 30, 2017, revenue was $52.8 million compared with $45.9 million for the comparable period in 2016. The increase is largely attributed to a 17% increase in the number of Attributable Gold Equivalent ounces sold, due to:

|

|

|

|

|

|

i.

|

An additional 4,107 Attributable Gold Equivalent ounces sold from the Company’s Yamana silver stream and Chapada copper stream. The increase was largely related to the timing of shipments; whereby, under the terms of the agreements, the time period over which the calculation of the maximum thresholds for deliveries was revised. These revisions resulted in the production thresholds being calculated on a quarterly basis as opposed to a monthly basis; thereby, reducing the variability of deliveries and annual true ups;

|

|

|

|

|

|

|

ii.

|

An additional 1,484 gold ounces sold from the Karma Mine, which announced its first gold production in April 2016;

|

|

|

|

|

|

|

iii.

|

A 23% increase in gold ounces sold from the Black Fox Mine largely driven by increased gold production from the mine in 2017. In addition, the Company received 887 gold ounces by September 30, 2017 that were not sold until after quarter end.

|

Partially offset by:

|

|

|

|

|

|

iv.

|

A 13% decrease in gold ounces sold from the Santa Elena Mine primarily related to the timing of shipments whereby 1,335 ounces were received by September 30, 2017, but were sold subsequent to quarter end.

|

THREE MONTHS ENDED SEPTEMBER 30, 2017

COMPARED TO THE OTHER QUARTERS PRESENTED

When comparing net income of $4.8 million and cash flow from operating activities of $11.9 million for the three months ended September 30, 2017 with net income/loss and operating cash flow for the remaining quarters, the following items impact comparability of analysis:

|

|

|

|

|

|

|

|

|

|

|

|

|

A $3.0 million gain resulting from the Bachelor Lake Gold Stream amendment for which Sandstorm received consideration consisting of $2.0 million in the common shares of Metanor and a 3.9% NSR on Metanor’s Barry project was recognized during the three months ended September 30, 2017;

|

|

|

|

|

|

|

|

A $4.5 million non-cash impairment charge relating to the Company’s royalty on the Coringa gold project was recognized during the three months ended June 30, 2017;

|

|

|

|

|

|

|

|

The Company recognized gains and losses with respect to the revaluation of its investments, which were primarily driven by changes in the fair value of the Trek (previously Luna) convertible debenture. For the three months ended September 30, 2017 and the three months ended June 30, 2017, these losses amounted to $0.5 million and $0.9 million, respectively, while for the three months ended March 31, 2017 these gains amounted to $2.7 million. In the first three quarters of 2016 these gains amounted to $13.4 million, $6.0 million and $5.8 million, respectively and in the fourth quarter of 2016, the Company recognized a loss of $3.1 million on revaluation;

|

|

|

|

|

|

|

|

During the three months ended March 31, 2017, the Company recognized a $2.2 million gain primarily resulting from (i) the settlement of the Trek (previously Luna) debt and (ii) the 20% premium associated with Orezone exercising its option to repurchase the royalty on the Bomboré gold project;

|

|

|

|

|

|

|

|

Non-cash impairment charges of $1.4 million and $1.1 million were recorded during the three months ended March 31, 2016 and the three months ended September 30, 2016, respectively;

|

|

|

|

|

|

|

|

A general decrease in finance expenses when compared to previous quarters primarily driven by the repayment of revolving credit facility; and

|

|

|

|

|

|

|

|

Overall, Gold Attributable Equivalent ounces sold have increased over the course of the last three years as a result of the acquisition of various assets including the Teck Resources Limited (“Teck”) royalty package which consists of 52 royalties and was purchased during the three months ended March 31, 2016.

|

CHANGE IN TOTAL ASSETS

Total assets increased by $121.6 million from June 30, 2017 to September 30, 2017 primarily resulting from the acquisition of Mariana and operating cash flow; partially offset by depletion expense. Total assets decreased by $4.8 million from March 31, 2017 to June 30, 2017 primarily resulting from a decrease in the value of the Company’s investments and a non-cash impairment charge relating to the Company’s royalty on the Coringa gold project; partially offset by operating cash flow. Total assets increased by $15.5 million from December 31, 2016 to March 31, 2017 primarily resulting from an increase in the value of the Company’s investments and operating cash flow; partially offset by depletion expense. Total assets decreased by $5.5 million from September 30, 2016 to December 31, 2016 primarily resulting from depletion expense and a decrease in the value of the Company’s investments; partially offset by operating cash flow. Total assets increased by $15.1 million from June 30, 2016 to September 30, 2016 primarily resulting from operating cash flow and an increase in the value of the Company’s investments; partially offset by depletion expense. Total assets decreased by $5.8 million from March 31, 2016 to June 30, 2016 primarily resulting from depletion expense; partially offset by an increase in the value of the Company’s investments. Total assets increased by $34.3 million from December 31, 2015 to March 31, 2016 primarily resulting from the acquisition of the Teck royalty package and an increase in the fair value of the Company’s investments, partially offset by depletion expense and a non-cash impairment charge on certain mineral interests.

NON-IFRS AND OTHER MEASURES

The Company has included, throughout this document, certain performance measures, including (i) average cash cost per attributable ounce and (ii) average realized gold price per attributable ounce. The presentation of these non-IFRS measures is intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. These non-IFRS measures do not have any standardized meaning prescribed by IFRS, and other companies may calculate these measures differently.

|

|

|

|

|

|

i.

|

Average cash cost per attributable ounce is calculated by dividing the Company’s cost of sales, excluding depletion by the number of Attributable Gold Equivalent ounces sold. The Company presents average cash cost per ounce as it believes that certain investors use this information to evaluate the Company’s performance in comparison to other streaming companies in the precious metals mining industry who present results on a similar basis. Figure 1.1 provides a reconciliation of average cash cost of gold on a per ounce basis.

|

Figure 1.1

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3 Months Ended

|

|

3 Months Ended

|

|

9 Months Ended

|

|

9 Months Ended

|

|

|

|

September 30, 2017

|

|

September 30, 2016

|

|

September 30, 2017

|

|

September 30, 2016

|

|

Cost of Sales, excluding depletion1

|

|

$

|

3,512

|

|

$

|

3,211

|

|

$

|

11,230

|

|

$

|

9,518

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Cash cost of sales is comprised of:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total cash cost of gold sold

|

|

$

|

3,512

|

|

$

|

3,211

|

|

$

|

11,230

|

|

$

|

9,518

|

|

Divided by:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Attributable Gold Equivalent ounces sold 2

|

|

|

14,293

|

|

|

12,588

|

|

|

42,601

|

|

|

36,486

|

|

Equals:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Average cash cost of gold (per attributable ounce)

|

|

$

|

246

|

|

$

|

255

|

|

$

|

264

|

|

$

|

261

|

|

|

|

|

1.

|

Cost of Sales, excluding depletion, includes cash payments made for Gold Equivalent ounces associated with commodity streams.

|

|

2.

|

The Company’s royalty and other commodity stream income is converted to an Attributable Gold Equivalent ounce basis by dividing the royalty and other commodity income for that period by the average realized gold price per ounce from the Company’s Gold Streams for the same respective period. These Attributable Gold Equivalent ounces when combined with the gold ounces sold from the Company’s Gold Streams equal total Attributable Gold Equivalent ounces sold.

|

|

|

|

|

|

|

ii.

|

Average realized gold price per attributable ounce is calculated by dividing the Company’s sales by the number of Attributable Gold Equivalent ounces sold. The Company presents average realized gold price per attributable ounce as it believes that certain investors use this information to evaluate the Company’s performance in comparison to other streaming companies in the precious metals mining industry that present results on a similar basis. Figure 1.2 provides a reconciliation of average realized gold price per ounce.

|

Figure 1.2

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3 Months Ended

|

|

3 Months Ended

|

|

9 Months Ended

|

|

9 Months Ended

|

|

|

|

September 30, 2017

|

|

September 30, 2016

|

|

September 30, 2017

|

|

September 30, 2016

|

|

Total Revenue

|

|

$

|

17,939

|

|

$

|

16,815

|

|

$

|

52,829

|

|

$

|

45,908

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Divided by:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Attributable Gold Equivalent ounces sold

|

|

|

14,293

|

|

|

12,588

|

|

|

42,601

|

|

|

36,486

|

|

Equals:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Average realized gold price (per attributable ounce)

|

|

$

|

1,255

|

|

$

|

1,336

|

|

$

|

1,240

|

|

$

|

1,258

|

LIQUIDITY AND CAPITAL RESOURCES

As of September 30, 2017, the Company had cash and cash equivalents of $6.1 million (December 31, 2016 – $21.4 million) and working capital of $20.4 million (December 31, 2016 – $23.8 million). In addition, the Company has an undrawn $110 million revolving credit facility available for future acquisitions.

During the nine months ended September 30, 2017, the Company generated cash flows from operating activities of $34.9 million compared with $28.9 million during the comparable period in 2016, with the increase being primarily attributable to an increase in the number of Attributable Gold Equivalent ounces sold.

During the nine months ended September 30, 2017, the Company had net cash outflows from investing activities of $38.3 million which were primarily the result of: (i) $48.3 million in cash outflows relating to the Mariana acquisition which included the cash consideration of the transaction and associated acquisition costs, which were partially offset by the cash Mariana had on acquisition; (ii) the acquisition of investments and other assets; and (iii) $3.6 million in payments related to the acquisition of royalty interests; partially offset by: (i) $13.8 million of cash inflows largely resulting from the sale of investments as the Company continues to monetize its non-core investments and (ii) $3.6 million relating to Orezone exercising its option to repurchase its royalty on the Bomboré gold project. During the nine months ended September 30, 2016, the Company had net cash inflows from investing activities of $0.9 million which were primarily the result of: (i) $18.4 million cash inflow largely consisting of the disposition of a portion of the Company’s investments and the receipt of $5.5 million related to the Company’s amendment of the Entrée commodity streams; which were partially offset by (ii) the acquisition of investments and other assets; (iii) the payment of $4.0 million and $5.2 million in connection with the Yamana commodity streams and the Karma Gold Stream, respectively; and (iv) a $1.4 million payment related to the Teck royalty transaction.

During the nine months ended September 30, 2017, the Company drew down $16 million on its revolving credit facility to fund a portion of the cash consideration required for the Mariana acquisition. The $16 million drawn down was subsequently repaid within the same period utilizing cash flow from operating activities and the proceeds from the sale of non-core investments. In addition, the Company had cash out flows of $14.2 million related to the redemption of the Company’s common shares under the NCIB. During the nine months ended September 30, 2016, the Company had net cash outflows from financing activities of $25.3 million largely related to $83.5 million in the repayment of debt under the Company’s revolving credit facility; partially offset by (i) $57.5 million raised in gross proceeds from the Company’s July 2016 equity financing and (ii) $5.1 million in proceeds from the exercise of stock options.

CONTRACTUAL OBLIGATIONS

In connection with its commodity streams, the Company has committed to purchase the following:

|

|

|

|

|

|

|

|

|

|

|

|

|

Stream

|

|

% of Life of Mine Gold

or Relevant Commodity 5,6,7,8,9

|

|

Per Ounce Cash Payment:

lesser of amount below and the then prevailing market price of the commodity (unless otherwise noted) 1, 2, 3, 4

|

|

Bachelor Lake

|

|

20%

|

|

$500

|

|

Black Fox

|

|

8%

|

|

$531

|

|