November 18, 2015

Dear Alcatel Lucent Security Holder,

On behalf of Alcatel

Lucent’s board of directors, I am pleased to inform you that Nokia Corporation today commenced an offer to exchange all Alcatel Lucent’s outstanding ordinary shares held by U.S. holders, American depositary shares representing ordinary

shares, wherever located, and OCEANEs held by U.S. holders, for Nokia Corporation ordinary shares or American depositary shares, as applicable. The remainder of Alcatel Lucent’s outstanding ordinary shares and OCEANEs, which are held by persons

outside the U.S., are the subject of a parallel public exchange offer in France. The U.S. offer and French offer are being made pursuant to a Memorandum of Understanding, dated April 15, 2015, as amended, between Alcatel Lucent and Nokia

Corporation.

At their meeting of October 28, 2015 and as a result of the matters described in the section entitled “Item 4. The

Solicitation or Recommendation—Reasons for Alcatel Lucent’s Board Recommendation” in the enclosed Alcatel Lucent Solicitation / Recommendation Statement on Schedule 14D-9, the participating members of the Alcatel Lucent board of

directors, taking into account the factors described in that section, unanimously:

| |

(i) |

determined that the exchange offer is in the best interest of Alcatel Lucent, its employees and its stakeholders (including the holders of the Alcatel Lucent ordinary shares and

holders of other Alcatel Lucent securities); |

| |

(ii) |

recommended that all holders of Alcatel Lucent ordinary shares and holders of Alcatel Lucent American depositary shares tender their Alcatel Lucent ordinary shares and/or their

Alcatel Lucent American depositary shares pursuant to the exchange offer; and |

| |

(iii) |

recommended that all holders of OCEANEs tender their OCEANEs pursuant to the exchange offer. |

A copy of the Alcatel Lucent Solicitation / Recommendation Statement on Schedule 14D-9 is enclosed. It contains additional information relating to the exchange offer in the United States, including a description of

the reasons for the determination and recommendation described above. Also enclosed are Nokia Corporation’s U.S. Exchange Offer / Prospectus, dated November 12, 2015, letters of transmittal for use in tendering your Alcatel Lucent securities

and other related documents. These documents set forth the terms and conditions of the exchange offer in the United States. We urge you to read the enclosed information and consider it carefully before tendering any of your Alcatel Lucent

securities.

On behalf of Alcatel Lucent’s board of directors, we thank you for your support.

Sincerely,

Philippe Camus

Chairman and Chief Executive Officer

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14D-9

(RULE 14d-101)

SOLICITATION/RECOMMENDATION STATEMENT

UNDER SECTION 14(d)(4) OF THE SECURITIES EXCHANGE ACT OF 1934

Alcatel Lucent

(Name of Subject Company)

Alcatel Lucent

(Name of Persons Filing Statement)

Ordinary shares,

nominal value EUR 0.05 per ordinary share

American Depositary Shares, each representing one ordinary share, nominal value

EUR 0.05 per ordinary share

(Title of Class of Securities)

FR0000130007

013904305

(CUSIP Number of Class of Securities)

Jean Raby

Chief Financial and Legal Officer

Alcatel Lucent

148/152 Route de la Reine

92100 Boulogne-Billancourt

France

Telephone Number +33

(1) 55 14 10 10

Facsimile Number +33 (1) 55 14 14 05

(Name, address and telephone numbers of person authorized to receive notices and

communications on behalf of the persons filing statement)

With copies to:

|

|

|

| Gauthier Blanluet Sullivan & Cromwell LLP 24, rue Jean-Goujon

75008 Paris

France Facsimile Number +33

(1) 73 04 10 10 |

|

Richard C. Morrissey Sullivan & Cromwell LLP 1 New Fetter Lane

London EC4A 1AN United

Kingdom Facsimile Number +44 (0) 20 7959 8950 |

| ¨ |

Check the box if the filing relates solely to preliminary communications made before the commencement of a tender offer. |

TABLE OF CONTENTS

|

|

|

|

|

| |

|

Page |

|

| Item 1. Subject Company Information. |

|

|

1 |

|

| Item 2. Identity and Background of Filing Person. |

|

|

1 |

|

| Item 3. Past Contacts, Transactions, Negotiations and Agreements. |

|

|

4 |

|

| Item 4. The Solicitation or Recommendation. |

|

|

27 |

|

| Item 5. Persons/Assets, Retained, Employed, Compensated or Used. |

|

|

86 |

|

| Item 6. Interest in Securities of the Subject Company. |

|

|

87 |

|

| Item 7. Purposes of the Transaction and Plans or Proposals. |

|

|

88 |

|

| Item 8. Additional Information. |

|

|

88 |

|

| Item 9. Exhibits. |

|

|

96 |

|

| ANNEX A: Opinion of Zaoui & Co. S.A., dated April 14, 2015. |

|

|

A-1 |

|

| ANNEX B: Opinion of Zaoui & Co. S.A., dated October 28, 2015. |

|

|

B-1 |

|

| ANNEX C: Unofficial English Translations of Independent Expert Report of Associés en Finance, dated October 28,

2015, and Addendum, dated November 9, 2015. |

|

|

C-1 |

|

Item 1. Subject Company Information.

Name and Address

The name of the subject company is

Alcatel Lucent, a French société anonyme (“Alcatel Lucent”). The address of Alcatel Lucent’s principal office is 148/152 route de la Reine, 92100 Boulogne-Billancourt, France. The telephone number of

Alcatel Lucent’s principal executive office is +33 (1) 55 14 10 10.

Securities

This Solicitation/Recommendation Statement on Schedule 14D-9 (this “Schedule 14D-9”) relates to:

| |

(i) |

Alcatel Lucent’s ordinary shares, nominal value EUR 0.05 per share (“Alcatel Lucent Shares”); |

| |

(ii) |

American Depositary Shares, evidenced by American Depositary Receipts, each representing one Alcatel Lucent Share (“Alcatel Lucent ADSs”);

|

| |

(iii) |

EUR 628 946 424 Alcatel Lucent bonds convertible/exchangeable into new Alcatel Lucent Shares or exchangeable for existing Alcatel Lucent Shares due on July 1, 2018

(“2018 OCEANEs”); |

| |

(iv) |

EUR 688 425 000 Alcatel Lucent bonds convertible/exchangeable into new Alcatel Lucent Shares or exchangeable for existing Alcatel Lucent Shares due on January 30,

2019 (“2019 OCEANEs”); and |

| |

(v) |

EUR 460 289 979.90 Alcatel Lucent bonds convertible/exchangeable into new Alcatel Lucent Shares or exchangeable for existing Alcatel Lucent Shares due on

January 30, 2020 (“2020 OCEANEs” and, together with the 2018 OCEANEs and the 2019 OCEANEs, “OCEANEs” and the OCEANEs, together with the Alcatel Lucent Shares and the Alcatel Lucent ADSs, “Alcatel Lucent

Securities”). |

The Alcatel Lucent Shares and the Alcatel Lucent ADSs are registered pursuant to the U.S. Securities Exchange Act

of 1934, as amended (the “Exchange Act”). The OCEANEs are not registered pursuant to the Exchange Act.

As of October 31, 2015, the

latest practicable date before the date of this Schedule 14D-9, there were 2 841 508 155 Alcatel Lucent Shares issued (including 472 058 361 Alcatel Lucent ADSs issued), of which 40 115 700 Alcatel Lucent Shares

were held in treasury by Alcatel Lucent or its subsidiaries, EUR 349 413 670 2018 OCEANEs outstanding, EUR 167 500 000 2019 OCEANEs outstanding and EUR 114 499 995 2020 OCEANEs outstanding.

For further information on Alcatel Lucent Securities outstanding as of October 31, 2015, see the section entitled “Item 8.

Additional Information—Alcatel Lucent Shares on a Fully Diluted Basis” below, which is incorporated herein by reference.

Item 2. Identity and Background of Filing Person.

Name and Address

Alcatel Lucent, the subject company, is the person filing this Schedule 14D-9. The name, business address and business telephone number of

Alcatel Lucent are set forth in the section entitled “Item 1. Subject Company Information—Name and Address” above.

1

Exchange Offer

This Schedule 14D-9 relates to an exchange offer comprised of two offers (separately, the “U.S. Offer” and the “French Offer” and collectively, the “Exchange

Offer”) by Nokia Corporation, a Finnish Corporation (“Nokia”), as disclosed in the Tender Offer Statement on Schedule TO (together with the exhibits thereto, as amended, the “Schedule TO”), filed by Nokia

with the U.S. Securities and Exchange Commission (the “SEC”) on November 18, 2015, the date of this Schedule 14D-9.

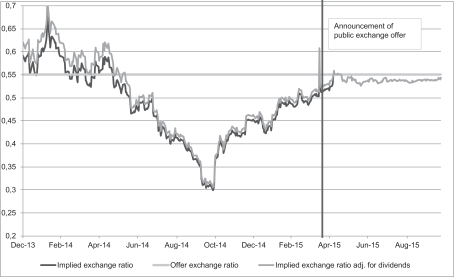

For every one

Alcatel Lucent Share validly tendered into, and not withdrawn from, the U.S. Offer, holders will receive, 0.5500 of a share of Nokia (a “Nokia Share”). For every one Alcatel Lucent ADS validly tendered into, and not withdrawn from,

the U.S. Offer, holders will receive 0.5500 of a Nokia American depositary share (a “Nokia ADS”), each Nokia ADS representing one Nokia Share. The ratio of 0.5500 Nokia Shares per one Alcatel Lucent Share is referred to as the

“exchange ratio”. For every one 2018 OCEANE validly tendered into, and not withdrawn from, the U.S. Offer, holders will receive 0.6930 Nokia Shares, for every one 2019 OCEANE validly tendered into, and not withdrawn from, the U.S.

Offer, holders will receive 0.7040 Nokia Shares, and for every one 2020 OCEANE validly tendered into, and not withdrawn from, the U.S. Offer, holders will receive 0.7040 Nokia Shares.

The U.S. Offer is being made on the terms and subject to the conditions set forth in section entitled “The Exchange Offer” in Nokia’s exchange offer/prospectus (the “exchange

offer/prospectus”), which is part of a Registration Statement on Form F-4 filed by Nokia with the SEC on August 14, 2015, as amended from time to time (the “Form F-4”), and is incorporated by reference into the

Schedule TO. A copy of the exchange offer/prospectus is included as Exhibit (a)(1) to this Schedule 14D-9 and the section entitled “The Exchange Offer” is incorporated herein by reference.

The French Offer to exchange 0.5500 Nokia Shares for every Alcatel Lucent Share, 0.6930 Nokia Shares for every 2018 OCEANE, 0.7040 Nokia Shares for every 2019

OCEANE and 0.7040 Nokia Shares for every 2020 OCEANE is being made pursuant to separate offer documentation available to holders of Alcatel Lucent Shares and OCEANEs located in France (holders of Alcatel Lucent Shares and OCEANEs located outside of

France may not participate in the French Offer except if, pursuant to the local laws and regulations applicable to those holders, they are permitted to participate in the French Offer).

The Exchange Offer is being made pursuant to a Memorandum of Understanding, dated as of April 15, 2015 (as such agreement may be amended, supplemented or otherwise modified from time to time, the

“Memorandum of Understanding”), by and between Alcatel Lucent and Nokia. A more complete description of the Memorandum of Understanding, including the Amendment to the Memorandum of Understanding, dated October 28, 2015, by and

between Alcatel Lucent and Nokia (the “Memorandum of Understanding Amendment”), is included in the section entitled “The Memorandum of Understanding” in the exchange offer/prospectus. A copy of the exchange

offer/prospectus is included as Exhibit (a)(1) to this Schedule 14D-9 and the section entitled the “Memorandum of Understanding” is incorporated herein by reference. The summary of Memorandum of Understanding and the Memorandum of

Understanding Amendment included in the section entitled “The Memorandum of Understanding” in the exchange offer/prospectus does not purport to be complete and is qualified in its entirety by reference to the Memorandum of

Understanding and the Memorandum of Understanding Amendment, copies of which are included as Exhibits (e)(1) and (e)(2), respectively, to this Schedule 14D-9 and are incorporated herein by reference.

Holders of Alcatel Lucent ADSs located outside of the United States may participate in the U.S. Offer only to the extent the local laws and regulations applicable

to those holders permit them to participate in the U.S. Offer. Holders of Alcatel Lucent Securities who are restricted from participating in the U.S. Offer pursuant to Sanctions (as defined in the exchange offer/prospectus) may not participate in

the U.S. Offer.

2

No fractional Nokia Shares or fractional Nokia ADSs will be issued. Holders of Alcatel Lucent Securities tendering

into the U.S. Offer or the French Offer will receive cash in lieu of any fractional Nokia Shares or Nokia ADSs to which such holders may otherwise be entitled, following the implementation of a mechanism to resell such fractional Nokia Shares or

Nokia ADSs.

Holders of options to acquire Alcatel Lucent Shares (“Alcatel Lucent Stock Options”) who wish to tender in the Exchange

Offer or the subsequent offering period, if any, must exercise their Alcatel Lucent Stock Options, and Alcatel Lucent Shares must be issued to such holders prior to the Expiration Date (as defined below) or the expiration of the subsequent offering

period, as applicable. Pursuant to the Memorandum of Understanding, Alcatel Lucent agreed to accelerate or waive certain terms of the Alcatel Lucent Stock Options, subject to certain conditions.

Restricted stock granted by Alcatel Lucent (“Performance Shares”) cannot be tendered in the Exchange Offer or the subsequent offering period, if

any, unless such Performance Shares have vested and are not subject to transfer restrictions prior to the Expiration Date (as defined below) or the expiration of the subsequent offering period, as applicable. Pursuant to the Memorandum of

Understanding, Nokia and Alcatel Lucent agreed to implement a mechanism with respect to unvested Performance Shares granted before April 15, 2015 pursuant to which the beneficiaries may waive their rights to receive Performance Shares in

exchange for Alcatel Lucent Shares, subject to certain conditions.

The U.S. Offer and withdrawal rights for tenders of Alcatel Lucent Shares and

OCEANEs in the U.S. Offer will expire at 11:00 a.m., New York City time (5:00 p.m. Paris time), on December 23, 2015 (as such time and date may be extended, the “Expiration Date”), unless the Exchange Offer is extended.

The deadline for validly tendering and withdrawing Alcatel Lucent ADSs in the U.S. Offer is 5:00 p.m., New York City time, on the U.S. business day immediately

preceding the Expiration Date, which will be December 22, 2015 (as such time and date may be extended, the “ADS Tender Deadline”), unless the U.S. Offer is extended.

The purpose of the Exchange Offer is for Nokia to acquire all of the Alcatel Lucent Securities in order to combine the businesses of Nokia and Alcatel Lucent.

Nokia’s obligation to accept, and to exchange, any Alcatel Lucent Securities validly tendered into the U.S. Offer is subject only to:

| |

• |

|

the number of Alcatel Lucent Securities validly tendered in accordance with the terms of the Exchange Offer representing, on the date of announcement by the

French stock market authority (Autorité des marchés financiers) (the “AMF”) of the results of the French Offer taking into account the results of the U.S. Offer, more than 50% of the Alcatel Lucent Shares on a

fully diluted basis (the “Minimum Tender Condition”); and |

| |

• |

|

Nokia shareholders having approved the authorization for the Nokia board of directors to issue such number of new Nokia Shares as may be necessary for delivering

the Nokia Shares offered in consideration for the Alcatel Lucent Securities tendered into the Exchange Offer and for the completion of the Exchange Offer (the “Nokia Shareholder Approval”). |

Subject to applicable SEC and AMF rules and regulations, Nokia reserves the right, in its sole discretion, to waive the Minimum Tender Condition to any level at or

above a number of Alcatel Lucent Shares representing more than 50% of the Alcatel Lucent share capital or voting rights, taking into account, if necessary, the Alcatel Lucent Shares resulting from the conversion of the OCEANEs validly tendered into

the Exchange Offer (the “Mandatory Minimum Acceptance Threshold”).

3

Nokia, Alcatel Lucent and the holders of Alcatel Lucent Securities will not know whether the Minimum Tender Condition

is satisfied before the publication by the AMF of the results of the French Offer (taking into account the results of the U.S. Offer). At such time, Nokia would determine, in its sole discretion, whether to waive the Minimum Tender Condition to any

level at or above the Mandatory Minimum Acceptance Threshold.

The foregoing summary of the Exchange Offer does not purport to be complete and is

qualified in its entirety by the more detailed description and explanations contained in the section entitled “The Exchange Offer” in the exchange offer/prospectus which is incorporated herein by reference.

Nokia’s registered office and its principal executive office is Karaportti 3, FI-02610 Espoo, Finland, and the telephone number is +358 (0) 10 448 8000,

as set forth in the exchange offer/prospectus.

Information relating to the Exchange Offer, including this Schedule 14D-9 and related documents, can be

found on the SEC’s website at www.sec.gov, or on Alcatel Lucent’s website at www.alcatel-lucent.com. Neither these websites nor the information on or available through them are a part of this Schedule 14D-9 or incorporated herein by

reference, and should not be considered a part of this Schedule 14D-9.

Item 3. Past Contacts, Transactions,

Negotiations and Agreements.

Except as described in this Schedule 14D-9, including documents incorporated herein by reference and the exhibits

hereto, to the knowledge of Alcatel Lucent, as of the date of this Schedule 14D-9, there exists no material agreement, arrangement or understanding, nor any actual or potential conflict of interest, between Alcatel Lucent or its affiliates, on the

one hand, and (i) any of Alcatel Lucent’s executive officers, directors or affiliates, or (ii) Nokia or any of Nokia’s executive officers, directors or affiliates, on the other hand.

Alcatel Lucent’s board of directors was aware of all such contracts, agreements, arrangements or understandings and any actual or potential conflicts of

interest and considered them along with other matters set forth under “Item 4. The Solicitation or Recommendation—Reasons for Approving the Memorandum of Understanding” below and “Item 4. The Solicitation or

Recommendation—Reasons for Alcatel Lucent’s Board Recommendation” below.

Relationship with Nokia

Memorandum of Understanding

A summary of the material terms

of the Memorandum of Understanding is included in the section entitled “The Memorandum of Understanding” in the exchange offer/prospectus and is incorporated herein by reference. The summary in the exchange offer/prospectus may not

contain all of the information about the Memorandum of Understanding that is important to holders of Alcatel Lucent Securities, and holders of Alcatel Lucent Securities are encouraged to read the Memorandum of Understanding, which is attached as

Annex A to the exchange offer/prospectus, carefully in its entirety. The legal rights and obligations of Alcatel Lucent and Nokia are governed by the specific language of the Memorandum of Understanding and not the summary described in the section

entitled “The Memorandum of Understanding” in the exchange offer/prospectus.

The Memorandum of Understanding contains representations,

warranties and covenants by each of Nokia and Alcatel Lucent. These representations and warranties were (i) made solely for the benefit of the other party to the Memorandum of Understanding; (ii) were not intended to be treated as

4

categorical statements of fact, but rather as a way of allocating the risk to one of the parties if those statements prove to be inaccurate; (iii) may have been qualified in the Memorandum

of Understanding by disclosures that were made to the other party in connection with the negotiation of the Memorandum of Understanding; (iv) may apply contract standards of “materiality” that are different from

“materiality” under the applicable securities laws; and (v) were made only as of the date of the Memorandum of Understanding, the French Offer filing date or such other date or dates as may be specified in the Memorandum of

Understanding. Information concerning the subject matter of the representations, warranties and covenants may change after the date of the Memorandum of Understanding, which subsequent information may or may not be fully reflected in public

disclosures. In addition, such representations, warranties and covenants may have been qualified by certain disclosures not reflected in the text of the Memorandum of Understanding and may apply standards of materiality and other qualifications and

limitations in a way that is different from what may be viewed as material by holders of Alcatel Lucent Securities. Only Alcatel Lucent and Nokia are parties to the Memorandum of Understanding, which does not confer any rights upon or give any

causes of action to the holders of Alcatel Lucent Securities. Neither holders of Alcatel Lucent Securities nor any other third parties should rely on the representations, warranties and covenants or any descriptions thereof as characterizations of

the actual state of facts or conditions of Alcatel Lucent, Nokia, or any of their respective subsidiaries or affiliates.

Alcatel Lucent acknowledges

that, notwithstanding the inclusion of the foregoing cautionary statements, it is responsible for considering whether additional specific disclosures of material information regarding material contractual provisions are required to make the

statements in this Schedule 14D-9 not misleading.

The foregoing summary of Memorandum of Understanding and the Memorandum of Understanding Amendment

does not purport to be complete and is qualified in its entirety by reference to the Memorandum of Understanding and the Memorandum of Understanding Amendment, copies of which are included as Exhibits (e)(1) and (e)(2), respectively, to this

Schedule 14D-9 and are incorporated herein by reference.

Other Arrangements

In 2015, Nokia has reimbursed Alcatel Lucent approximately EUR 124 000 and USD 62 000 for out-of-pocket expenses paid by Alcatel Lucent to third parties for shareholder analysis at the request of Nokia in

connection with the Exchange Offer, including shareholder analysis in accordance with Rule 14d-1 under the Exchange Act.

Arrangements with

Executive Officers and Directors of Alcatel Lucent

Alcatel Lucent’s executive officers and directors may have interests in the Exchange

Offer and the other transactions contemplated by the Memorandum of Understanding that are different from, or in addition to, the interests of the holders of Alcatel Lucent Securities generally. These interests may create potential conflicts of

interest. Alcatel Lucent’s board of directors was aware of these interests and considered them, among other matters, in approving the Memorandum of Understanding and the transactions contemplated by the Memorandum of Understanding, as set forth

under “Item 4. The Solicitation or Recommendation—Reasons for Approving the Memorandum of Understanding” below, and in determining that the Exchange Offer was in the best interest of Alcatel Lucent, its employees and its

stakeholders (including holders of Alcatel Lucent Shares and holders of other Alcatel Lucent Securities) and recommending that all holders of Alcatel Lucent Securities tender their Alcatel Lucent Securities pursuant to the Exchange Offer, as set

forth under “Item 4. The Solicitation or Recommendation—Reasons for Alcatel Lucent’s Board Recommendation” below.

5

Effect of the Exchange Offer on Alcatel Lucent Shares, Alcatel Lucent ADSs, OCEANEs and Share- and Equity-Based

Incentive Plans

Consideration for Alcatel Lucent Shares and Alcatel Lucent ADSs

If Alcatel Lucent’s executive officers and directors were to tender any Alcatel Lucent Shares or Alcatel Lucent ADSs they own for exchange pursuant to the Exchange Offer, they would receive the same

consideration on the same terms and conditions as the other holders of Alcatel Lucent Shares and Alcatel Lucent ADSs generally.

As of April 13,

2015, the date immediately prior to the public announcement of discussions related to a possible business combination between Alcatel Lucent and Nokia, Alcatel Lucent’s executive officers and directors (and their respective affiliates and

affiliated investment entities) as of that date owned 6 785 573 Alcatel Lucent Shares (including Alcatel Lucent Shares represented by Alcatel Lucent ADSs). If Alcatel Lucent’s executive officers and directors (and affiliates and

affiliated investment entities) as of April 13, 2015 had validly tendered all of their outstanding Alcatel Lucent Shares and Alcatel Lucent ADSs held as of that date pursuant to the Exchange Offer, Alcatel Lucent’s executive officers and

directors (and their respective affiliates and affiliated investment entities) as of that date would have received Nokia Shares having an aggregate value of approximately EUR 28 974 397, based on the closing price of the Nokia Shares as of

April 13, 2015 of EUR 7.77.

October 27, 2015, the date before the determination and recommendation by Alcatel Lucent’s board of

directors in respect of the Exchange Offer, Alcatel Lucent’s executive officers and directors (and their respective affiliates and affiliated investment entities) as of that date owned 6 815 005 Alcatel Lucent Shares (including

Alcatel Lucent Shares represented by Alcatel Lucent ADSs). If Alcatel Lucent’s executive officers and directors (and affiliates and affiliated investment entities) as of October 27, 2015, pursuant to the Exchange Offer, were to validly

tender all of their outstanding Alcatel Lucent Shares and Alcatel Lucent ADSs held as of that date, Alcatel Lucent’s executive officers and directors (and their respective affiliates and affiliated investment entities) as of that date would

receive Nokia Shares having an aggregate value of approximately EUR 22 285 066 based on the closing price of the Nokia Shares as of October 27, 2015 of EUR 5.95.

Consideration for OCEANEs

No Alcatel Lucent executive officers or directors hold any OCEANEs. However, if

Alcatel Lucent’s executive officers and directors were to hold OCEANEs and tender any OCEANEs they own for exchange pursuant to the Exchange Offer, they would receive the same consideration on the same terms and conditions as the other holders

of OCEANEs generally.

Distribution of Unrestricted Alcatel Lucent Shares

On October 28, 2015, Alcatel Lucent’s board of directors resolved, on the recommendation of the compensation committee, to grant to Alcatel Lucent employees, in lieu of the Alcatel Lucent Stock Options

Plan (as defined below) that Alcatel Lucent’s board of directors had considered granting in respect of the year ended December 31, 2014 and which has not been granted, unrestricted Alcatel Lucent Shares (representing a maximum total number

of 3 507 185 as of October 31, 2015) according to a ratio of one Alcatel Lucent Share per two Alcatel Lucent Stock Options, subject to the completion of the Exchange Offer, to the presence condition being fulfilled as of the

Expiration Date and to an undertaking to sell the unrestricted Alcatel Lucent Shares on the market no later than two French trading days before the last day of the subsequent offering period. A maximum aggregate amount of 275 000 unrestricted

Alcatel Lucent Shares are expected to be granted to Alcatel Lucent’s executive officers. No unrestricted Alcatel Lucent Shares would be granted to directors who are not executive officers.

6

In certain jurisdictions, the mechanisms described above may be adjusted to comply with possible applicable legal,

regulatory or other local constraints.

The foregoing summary of the distribution of Alcatel Lucent Shares does not purport to be complete and is

qualified in its entirety by reference to the Form of Replacement Share Grant Notification, a copy of which is included as Exhibit (e)(9) to this Schedule 14D-9 and is incorporated herein by reference.

Acceleration of Alcatel Lucent Stock Options

In connection

with its long-term incentive compensation arrangements, Alcatel Lucent grants Alcatel Lucent Stock Options to employees and members of management pursuant to plans in effect from time to time (“Alcatel Lucent Stock Options Plans”).

The Alcatel Lucent Stock Option Plans have the following terms:

| |

• |

|

the vesting of Alcatel Lucent Stock Options generally occurs: |

| |

• |

|

for Alcatel Lucent Stock Options Plans for beneficiaries located in France, over three successive periods (an initial 2-year vesting period after which

beneficiaries acquire 50% of the entitlement, a second 1-year vesting period after which the beneficiaries acquire an additional 25% of the entitlement, and a third 1-year vesting period after which the beneficiaries acquire the remaining 25% of the

entitlement); and |

| |

• |

|

for Alcatel Lucent Stock Options Plans for beneficiaries located outside of France, over four successive 1-year periods (beneficiaries acquire 25% of the

entitlement at the end of each period); |

| |

• |

|

vesting at the end of each period is subject to: |

| |

• |

|

presence conditions, which are satisfied if the relevant beneficiary maintains his or her position as an employee at Alcatel Lucent (or one of its subsidiaries)

at the expiration date of each relevant period; and |

| |

• |

|

for executive directors and members of the leadership team only, performance conditions related to free cash flow. |

As of October 31, 2015, there were 81 040 440 Alcatel Lucent Stock Options issued, out of which 67 452 250 Alcatel Lucent Stock Options

were exercisable and the Alcatel Lucent Shares which may be issued pursuant to their exercise were transferable.

In connection with the Exchange Offer,

on April 14, 2015 Alcatel Lucent’s board of directors, on the recommendation of the compensation committee, resolved to offer to accelerate or waive any vesting periods, vesting conditions, performance conditions and presence conditions

and lock-up periods for Alcatel Lucent Stock Options granted prior to the date of the Memorandum of Understanding (a maximum amount of approximately 13 588 190 Alcatel Lucent Stock Options as of October 31, 2015), subject to:

| |

• |

|

the completion of the Exchange Offer; |

| |

• |

|

applicable presence conditions being fulfilled on the Expiration Date; |

| |

• |

|

holders of accelerated Alcatel Lucent Stock Options undertaking to exercise all of their unvested Alcatel Lucent Stock Options as well as all of their vested

Alcatel Lucent Stock Options (except, as the case may be, those that are subject to a tax lock-up period provided by French or Belgian law); and |

7

| |

• |

|

holders of accelerated Alcatel Lucent Stock Options authorizing the Alcatel Lucent Stock Options Plan administrator to sell on the market all the resulting

Alcatel Lucent Shares on their behalf no later than two French trading days before the last day of the subsequent offering period. |

Holders of Alcatel Lucent Stock Options will not be required to exercise any of their Alcatel Lucent Stock Options and to sell the resulting Alcatel Lucent Shares

where the sum of the exercise price and the related costs and expenses relating to the exercise and sale of the resulting Alcatel Lucent Shares will exceed the Alcatel Lucent Share price. Instead, by accepting the acceleration of their Alcatel

Lucent Stock Options, such holders will be required to irrevocably accept to be bound by an Underwater Stock Options Liquidity Agreement with respect to the Alcatel Lucent Stock Options not exercised pursuant to the preceding sentence, as further

described in the section entitled “—Liquidity Agreement Offered to Holders of Underwater Stock Options” below. In addition, holders will be required to irrevocably accept to be bound by a Lock-Up Liquidity Agreement, as further

described in the section entitled “—Liquidity Agreements Offered to Holders of Alcatel Lucent Stock Options and Beneficiaries of Performance Shares Granted Before 2015 and Subject to a Lock-Up Period” below, with respect to the

Alcatel Lucent Stock Options subject to a tax lock-up period provided by French or Belgian law, unless the holder elects to accelerate such Alcatel Lucent Stock Options.

In respect of holders of Alcatel Lucent Stock Options who elect not to accept the acceleration, the terms and conditions of their Alcatel Lucent Stock Options will remain unchanged, including the presence

conditions and, as applicable, performance conditions. Certain holder of Alcatel Lucent Stock Options will be offered the Lock-Up Liquidity Agreement, as further described in the section entitled “—Liquidity Agreements Offered to

Holders of Alcatel Lucent Stock Options and Beneficiaries of Performance Shares Granted Before 2015 and Subject to a Lock-Up Period” below.

In

certain jurisdictions, the mechanisms described above may be adjusted to comply with possible applicable legal, regulatory or other local constraints.

The foregoing summary of the Alcatel Lucent Stock Options does not purport to be complete and is qualified in its entirety by reference to the Form of Stock Option

Acceleration Agreement, a copy of which is included as Exhibit (e)(7) and is incorporated herein by reference, and to the Alcatel Lucent Stock Options Plans, copies of which are included as Exhibits (e)(14) to (e)(21) to this Schedule 14D-9 and are

incorporated herein by reference.

As of April 13, 2015, Alcatel Lucent’s executive officers and directors (and their respective affiliates

and affiliated investment entities) as of that date owned Alcatel Lucent Stock Options (including unvested Alcatel Lucent Stock Options which may be accelerated as described above) exercisable into approximately 841 777 Alcatel Lucent Shares at

a weighted average exercise price of EUR 2.262 per Alcatel Lucent Share. If Alcatel Lucent’s executive officers and directors (and affiliates and affiliated investment entities) as of April 13, 2015, had exercised all Alcatel Lucent

Stock Options (including unvested Alcatel Lucent Stock Options which may be accelerated as described above) held as of that date and had validly tendered all of the resulting Alcatel Lucent Shares pursuant to the Exchange Offer, Alcatel

Lucent’s executive officers and directors (and their respective affiliates and affiliated investment entities) as of that date would have received Nokia Shares having an aggregate value (net of the exercise price of the Alcatel Lucent Stock

Options) of approximately EUR 1 690 288, based on the closing price of the Nokia Shares as of April 13, 2015 of EUR 7.77.

As of

October 27, 2015, Alcatel Lucent’s executive officers and directors (and their respective affiliates and affiliated investment entities) as of that date owned Alcatel Lucent Stock Options (including unvested Alcatel Lucent Stock Options

which may be accelerated as described above) exercisable into 849 100 Alcatel Lucent Shares at a weighted average exercise price of EUR 2.406 per Share. If Alcatel

8

Lucent’s executive officers and directors (and affiliates and affiliated investment entities) as of October 27, 2015, were to exercise all Alcatel Lucent Stock Options (including

unvested Alcatel Lucent Stock Options which may be accelerated as described above) held as of that date and validly tender all of the resulting Alcatel Lucent Shares pursuant to the Exchange Offer, Alcatel Lucent’s executive officers and

directors (and their respective affiliates and affiliated investment entities) as of that date would receive Nokia Shares having an aggregate value (net of the exercise price of the Alcatel Lucent Stock Options) of approximately EUR 733 622,

based on the closing price of the Nokia Shares as of October 27, 2015 of EUR 5.95.

Acceleration of Performance Shares

In connection with its long-term incentive compensation arrangements, Alcatel Lucent grants Performance Shares to employees and members of management pursuant to

plans in effect from time to time (“Performance Share Plans”). The Performance Share Plans have the following terms:

| |

• |

|

Performance Shares entitle the recipient to receive Alcatel Lucent Shares upon vesting; |

| |

• |

|

the vesting of Performance Shares generally occurs: |

| |

• |

|

for Performance Share Plans adopted in 2014 and later, over two successive 2-year periods (an initial 2-year vesting period after which beneficiaries acquire 50%

of the entitlement and a second 2-year vesting period after which beneficiaries acquire the remaining 50% of the entitlement); |

| |

• |

|

for Performance Share Plans for beneficiaries located in France adopted prior to 2014, after a 2-year period and with an additional 2-year holding period; and

|

| |

• |

|

for Performance Share Plans for beneficiaries located outside of France adopted prior to 2014, after a 4-year period; |

| |

• |

|

vesting is subject to the assessment at the end of each relevant period of: |

| |

• |

|

presence conditions, which are satisfied if the relevant beneficiary maintains his or her position as an employee at Alcatel Lucent (or one of its subsidiaries)

at the expiration date of each relevant period; and |

| |

• |

|

performance conditions. |

As of

October 31, 2015, there are 28 188 080 unvested Performance Shares and 2 506 385 vested Performance Shares that remain subject to a holding period which is not expected to expire prior to the closing date of the Exchange Offer.

In connection with the Exchange Offer, on April 14, 2015 Alcatel Lucent’s board of directors, on the recommendation of the compensation

committee, resolved to allow beneficiaries of Performance Shares granted prior to the date of the Memorandum of Understanding to exchange each of their unvested Performance Shares (a total maximum number of 18 217 530 Alcatel Lucent

Performance Shares to Alcatel Lucent’s knowledge as of October 31, 2015) for an unrestricted Alcatel Lucent Share, minus, in the relevant countries, the number of Alcatel Lucent Shares which have to be sold in order to cover payable tax

charges, subject to:

| |

• |

|

the completion of the Exchange Offer; |

| |

• |

|

applicable presence conditions being fulfilled on the Expiration Date; and |

9

| |

• |

|

holders of accelerated Performance Shares authorizing the Performance Share Plan administrator to sell on the market all the resulting Alcatel Lucent Shares on

their behalf no later than two French trading days before the last day of the subsequent offering period. |

In respect of beneficiaries

who elect not to accept the acceleration and except as set forth in the following sentence, the terms and conditions of the Performance Shares, including the performance conditions and the presence conditions, will remain unchanged. Nokia and

Alcatel Lucent have agreed that Alcatel Lucent would amend the terms and conditions of any Performance Shares that remain outstanding in order to, in case of Reduced Liquidity (as defined below), use the stock market price of Nokia Shares instead of

the stock market price of Alcatel Lucent Shares as the reference stock market price and to adjust the representative reference panel. Certain beneficiaries of Performance Shares will be offered the Lock-Up Liquidity Agreement, as further described

in the section entitled “—Liquidity Agreements Offered to Holders of Alcatel Lucent Stock Options and Beneficiaries of Performance Shares Granted Before 2015 and Subject to a Lock-Up Period” below.

In certain jurisdictions, these mechanisms may be adapted to comply with possible applicable statutory, regulatory or other type of constraints.

The foregoing summary of the Performance Shares does not purport to be complete and is qualified in its entirety by reference to the form of Performance Shares

Acceleration Agreement, a copy of which is included as Exhibit (e)(8) hereto and is incorporated herein by reference, and the Performance Share Plans, copies of which are included as Exhibits (e)(13) and (e)(22) to (e)(24) to this Schedule 14D-9 and

are incorporated herein by reference.

On July 29, 2015, Alcatel Lucent’s board of directors, on the recommendation of the compensation

committee, resolved to adopt an additional Performance Share Plan (the “2015 Performance Share Plan”) pursuant to which Alcatel Lucent expects, as of October 31, 2015, to issue a maximum amount of 9 970 550

Performance Shares to Alcatel Lucent employees. The Performance Shares issued pursuant to the 2015 Performance Share Plan will be subject to customary presence and performance conditions over a four-year vesting period, and will not be accelerated

in connection with the Exchange Offer. The beneficiaries of Performance Shares issued pursuant to the 2015 Performance Share Plan will be required to enter into a 2015 Performance Share Plan Liquidity Agreement, as further described in the section

entitled “—Liquidity Agreement Offered to Beneficiaries of Performance Shares granted pursuant to the 2015 Performance Share Plan” below.

In certain jurisdictions, these mechanisms may be adapted to comply with possible applicable statutory, regulatory or other type of constraints.

The foregoing summary of the Performance Shares to be issued pursuant to the 2015 Performance Share Plan does not purport to be complete and is qualified in its entirety by reference to the 2015 Performance Share

Plan, a copy of which is included as Exhibit (e)(10) to this Schedule 14D-9 and is incorporated herein by reference.

As of April 13, 2015, Alcatel

Lucent’s executive officers and directors (and their respective affiliates and affiliated investment entities) were beneficiaries of 417 651 Performance Shares (including unvested Performance Shares which may be accelerated as for any

employee under the conditions described above. If Alcatel Lucent’s executive officers and directors (and affiliates and affiliated investment entities) as of April 13, 2015, had exchanged all Performance Shares (including unvested

Performance Shares which may be accelerated as for any employee under the conditions described above) held as of that date for Alcatel Lucent Shares and had validly tendered all of the resulting Alcatel Lucent Shares pursuant to the Exchange Offer,

Alcatel Lucent’s executive officers and directors (and their

10

respective affiliates and affiliated investment entities) as of that date would have received Nokia Shares having an aggregate value of approximately EUR 1 783 370, based on the closing

price of the Nokia Shares as of April 13, 2015 of EUR 7.77.

As of October 27, 2015, Alcatel Lucent’s executive officers and directors

(and their respective affiliates and affiliated investment entities) were beneficiaries of 311 975 Performance Shares (including unvested Performance Shares which may be accelerated as for any employee under the conditions described above, but

excluding those Performance Shares granted pursuant to the 2015 Performance Share Plan, which will not be accelerated in connection with the Exchange Offer and will remain subject to presence and performance conditions). If Alcatel Lucent’s

executive officers and directors (and affiliates and affiliated investment entities) as of October 27, 2015, were to exchange all Performance Shares (including unvested Performance Shares which may be accelerated as for any employee under the

conditions described above, but excluding those Performance Shares granted pursuant to the 2015 Performance Share Plan, which will not be accelerated in connection with the Exchange Offer and will remain subject to presence and performance

conditions) held as of that date for Shares and validly tender all of the resulting Shares pursuant to the Exchange Offer, Alcatel Lucent’s executive officers and directors (and their respective affiliates and affiliated investment entities) as

of that date would receive Nokia Shares having an aggregate value of approximately EUR 1 020 158, based on the closing price of the Nokia Shares as of October 27, 2015 of EUR 5.95.

Acceleration of the Performance Units

In connection with

its long-term incentive compensation arrangements, Alcatel Lucent grants performance units (“Performance Units”) exclusively to executive officers and directors. Performance Units are conditional rights which grant the beneficiary

the right to receive compensation in cash. Performance Units are subject to the satisfaction of performance and presence conditions at the end of the vesting period. Performance conditions, presence conditions, and vesting periods for Performance

Units vary and are set by Alcatel Lucent’s board of directors when the Performance Units are granted.

Performance Units granted to the leadership

team (other than Alcatel Lucent’s president and chief executive officer) would be accelerated upon a change of control of Alcatel Lucent, pursuant to a decision of Alcatel Lucent’s board of directors in 2013, as for any employee in

connection with his or her Performance Shares as described above. For further information on arrangements with respect to Performance Units granted to Mr. Combes and the reduction in Performance Units agreed between Alcatel Lucent and

Mr. Combes, see the section entitled “—Employment Arrangements—Employment Arrangements with Mr. Michel Combes (Former Chief Executive Officer and Former Director)” below. The Performance Units granted to

Mr. Philippe Camus, Alcatel Lucent’s chairman and interim chief executive officer, will not be accelerated in connection with the Exchange Offer. Performance Units granted to all beneficiaries are payable in cash upon the date of

acceleration.

The foregoing summary of the grant of Performance Units does not purport to be complete.

As of April 13, 2015, Alcatel Lucent’s executive officers and directors (and their respective affiliates and affiliated investment entities) were

beneficiaries of 5 890 000 Performance Units (including unvested Performance Units which may be accelerated as described above). If Alcatel Lucent’s executive officers and directors (and affiliates and affiliated investment entities)

as of April 13, 2015, had exchanged all Performance Units (including unvested Performance Units which may be accelerated as for any employee under the conditions described above) held as of that date for cash compensation, Alcatel Lucent’s

executive officers and directors (and their respective affiliates and affiliated investment entities) as of that date would have received cash compensation having an aggregate value of

11

approximately EUR 23 836 250, based on the closing price of Alcatel Lucent Shares as of April 13, 2015 of EUR 3.86, except for the Performance Units granted to Mr. Combes,

which would have been payable in Alcatel Lucent Shares (or Nokia Shares, following completion of the squeeze-out of Alcatel Lucent Shares, if any) at their respective maturity dates in 2016, 2017 and 2018 (one Alcatel Lucent Share (or 0.5500 Nokia

Shares) per Performance Unit) and for which the estimated value is calculated based on the closing price of the Nokia Shares as of April 13, 2015 of EUR 7.77 and the exchange ratio of 0.5500, resulting in an implied value of EUR 4.27 per

Performance Unit.

As of October 27, 2015, Alcatel Lucent’s executive officers and directors (and their respective affiliates and affiliated

investment entities) were beneficiaries of 3 205 000 Performance Units (including unvested Performance Units which may be accelerated in connection with the Exchange Offer). If Alcatel Lucent’s executive officers and directors (and

affiliates and affiliated investment entities) as of October 27, 2015, were to exchange all Performance Units (including unvested Performance Units which may be accelerated under the conditions described above) held as of that date for cash

compensation, Alcatel Lucent’s executive officers and directors (and their respective affiliates and affiliated investment entities) as of that date would receive cash compensation having an aggregate value of approximately EUR

10 448 300, based on the closing price of the Alcatel Lucent Shares as of October 27, 2015 of EUR 3.26.

Liquidity Agreements Offered

to Holders of Alcatel Lucent Stock Options and Beneficiaries of Performance Shares Granted Before 2015 and Subject to a Lock-Up Period

Pursuant to

the Memorandum of Understanding, Nokia will offer liquidity agreements (the “Lock-Up Liquidity Agreements”) to the French tax residents who are beneficiaries of the following plans, as a result of tax constraints to which they are

subject:

| |

• |

|

Performance Share Plans n°A0914RUROW and n°A0914RPROW dated September 15, 2014, namely, a maximum number of 1 796 429 Alcatel Lucent

Shares as of October 31, 2015; |

| |

• |

|

Alcatel Lucent Stock Options Plan n°A0812NHFR2 dated August 13, 2012, namely, a maximum number of 26 420 Alcatel Lucent Shares as of

October 31, 2015; |

| |

• |

|

Alcatel Lucent Stock Options Plans n°A0312COFR2, n°A0312CPFR2 and n°A0312NHFR2 dated March 14, 2012, namely, a maximum number of

1 474 681 Alcatel Lucent Shares as of October 31, 2015. |

The Lock-Up Liquidity Agreements will also be offered to

Belgian tax residents who are beneficiaries of the following plan, provided that they opted for the taxation at the grant on a reduced basis of these Alcatel Lucent Stock Options and that they committed to hold these Alcatel Lucent Stock Options:

| |

• |

|

Alcatel Lucent Stock Options Plan n°A0713COBE2 dated July 12, 2013, namely, a maximum number of 170 637 Alcatel Lucent Shares as of

October 31, 2015. |

Pursuant to the Lock-Up Liquidity Agreements, in case of (i) delisting of the Alcatel Lucent Shares,

(ii) holding by Nokia of more than 85% of the Alcatel Lucent Shares or (iii) average daily trading volume of Alcatel Lucent Shares on Euronext Paris falling below 5 000 000 Alcatel Lucent Shares for 20 consecutive French trading days (any

such event, “Reduced Liquidity”), the Alcatel Lucent Shares received by holders of Alcatel Lucent Stock Options will automatically be exchanged for either Nokia Shares or for cash consideration equal to the market value of such

Nokia Shares, upon exercise of these Alcatel Lucent Stock Options after expiration of the applicable lock-up period. The Lock-Up Liquidity Agreement also provides that the relevant Performance Shares would be automatically exchanged by Nokia for

either Nokia Shares or for cash consideration equal to the market value of such Nokia Shares, shortly after the end of the applicable lock-up period.

12

The exchange ratio to be offered pursuant to the Lock-Up Liquidity Agreements would be consistent with the exchange

ratio of the Exchange Offer, subject to certain adjustments, in case of certain financial transactions of Nokia or Alcatel Lucent, in order for the holders of Alcatel Lucent Stock Options and beneficiaries of Performance Shares to be able to obtain

the same value in either Nokia Shares or cash consideration that they would have obtained if such a transaction had not taken place.

In certain

jurisdictions, the mechanism described above may be adjusted to comply with possible applicable legal, regulatory or other local constraints.

The

foregoing summary of the Lock-Up Liquidity Agreements does not purport to be complete and is qualified in its entirety by reference to the Forms of Lock-Up Liquidity Agreement, copies of which are included as Exhibits (e)(3) and (e)(4) to this

Schedule 14D-9 and are incorporated herein by reference.

Liquidity Agreement Offered to Holders of Underwater Stock Options

Pursuant to the Memorandum of Understanding, Nokia has agreed to offer a liquidity agreement (the “Underwater Stock Options Liquidity Agreement”)

to holders of Alcatel Lucent Stock Options with respect to (i) the vested Alcatel Lucent Stock Options not covered by the undertaking to sell described in the section entitled “—Acceleration of Alcatel Lucent Stock

Options” above where the sum of the exercise price and the costs and expenses relating to the exercise and sale of the resulting Alcatel Lucent Shares will represent more than 90% of the Alcatel Lucent Share price as of the closing

of the last day of the subsequent offering period on Euronext Paris and (ii) the unvested and vested Alcatel Lucent Stock Options to be subject to a liquidity agreement as described in the section entitled “—Acceleration of Alcatel

Lucent Stock Options” above. The Underwater Stock Options Liquidity Agreement would provide for Alcatel Lucent Shares received to be automatically exchanged by Nokia for either Nokia Shares or for cash consideration equal to the market

value of such Nokia Shares.

The exchange ratio to be offered pursuant to the Underwater Stock Options Liquidity Agreement would be consistent with the

exchange ratio of the Exchange Offer, subject to certain adjustments, in case of certain financial transactions of Nokia or Alcatel Lucent, in order for holders of Alcatel Lucent Stock Options to be able to obtain the same value in either Nokia

Shares or cash consideration that they would have obtained if such a transaction had not taken place.

In certain jurisdictions, the mechanism described

above may be adjusted to comply with possible applicable legal, regulatory or other local constraints.

The foregoing summary of the Underwater Stock

Option Liquidity Agreement does not purport to be complete and is qualified in its entirety by reference to the Form of Underwater Stock Option Liquidity Agreement, a copy of which is included as Exhibit (e)(6) to this Schedule 14D-9 and is

incorporated herein by reference.

Liquidity Agreement Offered to Beneficiaries of Performance Shares granted pursuant to the 2015 Performance Share

Plan

Pursuant to the Memorandum of Understanding, Nokia and Alcatel Lucent have agreed to enter into a liquidity agreement (the “2015

Performance Share Plan Liquidity Agreement”) with all beneficiaries of Performance Shares granted pursuant to the 2015 Performance Share Plan, pursuant to which, in case of Reduced Liquidity at the date of expiration of the applicable

vesting period, all Performance Shares granted pursuant to the 2015 Performance Share Plan, representing a maximum amount of 9 970 550 Alcatel Lucent Shares as of October 31, 2015, would be automatically exchanged by Nokia for either

Nokia Shares or for cash consideration equal to the market value of such Nokia Shares shortly after the end of the vesting period.

13

The exchange ratio to be offered pursuant to the 2015 Performance Share Plan Liquidity Agreement would be consistent

with the exchange ratio of the Exchange Offer, subject to certain adjustments, in case of certain financial transactions of Nokia or Alcatel Lucent, in order for the beneficiaries of Performance Shares granted pursuant to the 2015 Performance Share

Plan to be able to obtain the same value in either Nokia Shares or cash consideration that they would have obtained if such a transaction had not taken place.

In certain jurisdictions, the mechanism described above may be adjusted to comply with possible applicable legal, regulatory or other local constraints.

The foregoing summary of the 2015 Performance Share Plan Liquidity Agreements does not purport to be complete and is qualified in its entirety by reference to the Form of 2015 Performance Share Plan Liquidity

Agreement, a copy of which is included as Exhibit (e)(5) to this Schedule 14D-9 and is incorporated herein by reference.

14

Table of Consideration Related to the Exchange Offer as of Immediately Prior to the Memorandum of Understanding

The following table sets forth as of April 13, 2015 the approximate aggregate amount of consideration that Alcatel Lucent’s executive

officers and directors as of that date would have been entitled to receive in connection with the completion of the Exchange Offer, assuming that such executive officers and directors (1) validly tendered all Alcatel Lucent Shares and Alcatel

Lucent ADSs held by them pursuant to the Exchange Offer, (2) exercised all Alcatel Lucent Stock Options held by them for Alcatel Lucent Shares and validly tendered such Alcatel Lucent Shares into the Exchange Offer, (3) exchanged all

Performance Shares held by them for Alcatel Lucent Shares and validly tendered such Alcatel Lucent Shares into the Exchange Offer and (4) received cash compensation in respect of all Performance Units granted to them. Unless otherwise

indicated, estimated values are calculated based on the closing price of the Nokia Shares as of April 13, 2015 of EUR 7.77 and the exchange ratio of 0.5500, resulting in an implied value of EUR 4.27 per Alcatel Lucent Share.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Name and Title |

|

Number of

Alcatel

Lucent

Shares and

Alcatel

Lucent

ADSs(1) |

|

|

Estimated

Value Alcatel

Lucent

Shares and

Alcatel

Lucent ADSs |

|

|

Number

of Alcatel

Lucent

Stock

Options(2) |

|

|

Estimated

Value of

Alcatel

Lucent

Stock

Options(3) |

|

|

Number

of

Performance

Shares(4) |

|

|

Estimated

Value of

Performance

Shares |

|

|

Number

of

Performance

Units(5) |

|

|

Estimated

Value

of

Performance

Units(6) |

|

|

Estimated

Total Value of

Consideration |

|

| Philippe Camus (Chairman) |

|

|

1 131 352 |

|

|

€ |

4 830 873 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

400 000 |

|

|

€ |

1 544 000 |

|

|

€ |

6 374 873 |

|

| Jean C. Monty (Vice Chairman) |

|

|

5 030 001 |

|

|

€ |

21 478 104 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

€ |

21 478 104 |

|

| Michel Combes (CEO and Director)(7) |

|

|

— |

(8) |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

2 685 000 |

|

|

€ |

11 464 950 |

|

|

€ |

11 464 950 |

|

| Francesco Caio (Director) |

|

|

2 100 |

|

|

€ |

8 967 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

€ |

8 967 |

|

| Carla Cico (Director) |

|

|

29 359 |

|

|

€ |

125 363 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

€ |

125 363 |

|

| Stuart E. Eizenstat (Director) |

|

|

29 963 |

|

|

€ |

127 942 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

€ |

127 942 |

|

| Kim Crawford Goodman (Director) |

|

|

6 348 |

|

|

€ |

27 106 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

€ |

27 106 |

|

| Louis R. Hughes (Director) |

|

|

33 926 |

|

|

€ |

144 864 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

€ |

144 864 |

|

| Véronique Morali (Director) |

|

|

500 |

|

|

€ |

2 135 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

€ |

2 135 |

|

| Olivier Piou (Director) |

|

|

88 955 |

|

|

€ |

379 838 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

€ |

379 838 |

|

| Jean-Cyril Spinetta (Director) |

|

|

29 791 |

|

|

€ |

127 208 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

€ |

127 208 |

|

| Total Other Executive Officers(9) |

|

|

403 278 |

|

|

€ |

1 721 997 |

|

|

|

841 777 |

|

|

€ |

1 690 289 |

|

|

|

417 651 |

|

|

€ |

1 783 370 |

|

|

|

2 805 000 |

|

|

€ |

10 827 300 |

|

|

€ |

16 022 956 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total |

|

|

6 785 573 |

|

|

€ |

28 974 397 |

|

|

|

841 777 |

|

|

€ |

1 690 288 |

|

|

|

417 651 |

|

|

€ |

1 783 370 |

|

|

|

5 890 000 |

|

|

€ |

23 836 250 |

|

|

€ |

56 284 305 |

|

| (1) |

Includes certain Alcatel Lucent Shares held by directors that are subject to restrictions and may not be tendered into the Exchange Offer. In particular:

|

| |

(a) |

Article 12 of Alcatel Lucent’s By-Laws requires each director to hold at least 500 Alcatel Lucent Shares. As a result, Alcatel Lucent expects that no director will tender

the 500 Alcatel Lucent Shares he or she holds in compliance with this requirement. |

| |

(b) |

The 2010 annual shareholders meeting of Alcatel Lucent authorized the payment of additional attendance fees (jetons de présence) to directors,

subject to each director (i) using the |

15

| |

additional attendance fees received (after taxes) to purchase Alcatel Lucent Shares and (ii) holding the acquired Alcatel Lucent Shares for the duration of his or her term of office.

|

| |

(c) |

The terms of Alcatel Lucent’s Performance Shares Plans and related decisions of Alcatel Lucent’s board of directors require that Mr. Philippe Camus continues to

hold the Alcatel Lucent Shares granted in connection therewith and the Alcatel Lucent Shares purchased in connection therewith for so long as he remains the Chairman of Alcatel Lucent’s board of directors. Mr. Camus is also required to

continue to hold any Alcatel Lucent Shares acquired during his term for so long as he remains in office. |

| (2) |

Includes Alcatel Lucent Stock Options granted prior to the date of the Memorandum of Understanding which Alcatel Lucent’s board of directors has resolved to accelerate.

|

| (3) |

Calculated using a weighted average exercise price for the Alcatel Lucent Stock Options of EUR 2.262. |

| (4) |

Includes Performance Shares granted prior to the date of the Memorandum of Understanding which Alcatel Lucent’s board of directors has resolved to accelerate.

|

| (5) |

Includes Performance Units granted prior to the date of the Memorandum of Understanding which Alcatel Lucent’s board of directors has resolved to accelerate, but excludes

those Performance Units with performance conditions relating to periods prior to the date of the Memorandum of Understanding for which the relevant conditions were not satisfied. |

| (6) |

Calculated based on the right to receive cash compensation in cash in respect of each Performance Unit equal to the value of one Alcatel Lucent Share, and based on the closing

price of Alcatel Lucent Shares as of April 13, 2015 of EUR 3.86, except for the Performance Units granted to Mr. Combes, which would have been payable in Alcatel Lucent Shares (or Nokia Shares, following completion of the squeeze-out of

Alcatel Lucent Shares, if any) at their respective maturity dates in 2016, 2017 and 2018 (one Alcatel Lucent Share (or 0.5500 Nokia Shares) per Performance Unit) and for which the estimated value is calculated based on the closing price of the Nokia

Shares as of April 13, 2015 of EUR 7.77 and the exchange ratio of 0.5500, resulting in an implied value of EUR 4.27 per Performance Unit. |

| (7) |

Reflects amounts attributable to Mr. Combes as of April 13, 2015, which Alcatel Lucent’s board of directors subsequently resolved, with the agreement of and upon

the request of Mr. Combes, to reduce to a payment in cash of EUR 3 251 307 in respect of Performance Units for the years ended December 31, 2013 and 2014 a maximum amount in cash of EUR 1 408 887 in respect of

Performance Units for the year ended December 31, 2015, as further described in the section entitled “—Employment Arrangements—Employment Arrangements with Mr. Michel Combes (Former Chief Executive Officer and Former

Director)” below. |

| (8) |

Excludes 500 Alcatel Lucent Shares held by Mr. Combes that have been lent by Florelec, a subsidiary of Alcatel Lucent, to Mr. Combes for the duration of his term as a

director of Alcatel Lucent, in order to satisfy Article 12 of Alcatel Lucent’s By-Laws, which requires each director to hold at least 500 Alcatel Lucent Shares, and which will be returned to Florelec for no consideration at the end of such

term. |

| (9) |

The other executive officers of Alcatel Lucent as of April 13, 2015, were Mr. Jean Raby, Mr. Philippe Keryer, Ms. Nicole Gionet, Mr. Tim Krause and

Mr. Philippe Guillemot who, together with Mr. Combes, comprised the Management Committee of Alcatel Lucent. |

Table of

Consideration Related to the Exchange Offer as of Immediately Prior to Alcatel Lucent’s Recommendation

Between April 13, 2015 and the date

of this Schedule 14D-9, Ms. Sylvia Summers was appointed a director by the meeting of Alcatel Lucent’s shareholders on May 26, 2015, Ms. Véronique Morali’s term as a director ended on July 15, 2015,

Mr. Michel Combes resigned as a director and chief executive officer effective as of September 1, 2015, and Mr. Philippe Camus was appointed interim chief executive officer effective as of September 1, 2015.

16

The following table sets forth as of October 27, 2015, the approximate aggregate amount of consideration that

Alcatel Lucent’s executive officers and directors as of that date would be entitled to receive in connection with the completion of the Exchange Offer, assuming that such executive officers and directors (1) validly tender all Shares and

ADSs held by them pursuant to the Exchange Offer, (2) exercise all Stock Alcatel Lucent Stock Options held by them for Alcatel Lucent Shares and validly tender such Alcatel Lucent Shares into the Exchange Offer, (3) exchange all

Performance Shares held by them (other than Performance Shares granted pursuant to the 2015 Performance Share Plan, which will not be accelerated in connection with the Exchange Offer and will remain subject to presence and performance conditions)

for Alcatel Lucent Shares and validly tender such Alcatel Lucent Shares into the Exchange Offer and (4) receive cash compensation in respect of all Performance Units granted to them. Unless otherwise indicated, estimated values are calculated

based on the closing price of the Nokia Shares as of October 27, 2015 of EUR 5.95 and the exchange ratio of 0.5500, resulting in an implied value of EUR 3.27 per Share.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Name and Title |

|

Number of

Alcatel

Lucent

Shares and

Alcatel

Lucent

ADSs(1) |

|

|

Estimated

Value Alcatel

Lucent

Shares and

Alcatel

Lucent ADSs |

|

|

Number

of Alcatel

Lucent

Stock

Options(2) |

|

|

Estimated

Value of

Alcatel

Lucent

Stock

Options(3) |

|

|

Number

of

Performance

Shares(4) |

|

|

Estimated

Value of

Performance

Shares |

|

|

Number

of

Performance

Units(5) |

|

|

Estimated

Value

of

Performance

Units(6) |

|

|

Estimated

Total Value of

Consideration |

|

| Philippe Camus (Chairman & Interim CEO) |

|

|

1 131 352 |

|

|

€ |

3 699 521 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

400 000 |

|

|

€ |

1 304 000 |

|

|

€ |

5 003 521 |

|

| Jean C. Monty (Vice Chairman) |

|

|

5 033 706 |

|

|

€ |

16 460 219 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

€ |

16 460 219 |

|

| Francesco Caio (Director) |

|

|

5 803 |

|

|

€ |

18 976 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

€ |

18 976 |

|

| Carla Cico (Director) |

|

|

33 062 |

|

|

€ |

108 113 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

€ |

108 113 |

|

| Stuart E. Eizenstat (Director) |

|

|

33 668 |

|

|

€ |

110 094 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

€ |

110 094 |

|

| Kim Crawford Goodman (Director) |

|

|

10 053 |

|

|

€ |

32 873 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

€ |

32 873 |

|

| Louis R. Hughes (Director) |

|

|

37 631 |

|

|

€ |

123 053 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

€ |

123 053 |

|

| Olivier Piou (Director) |

|

|

92 658 |

|

|

€ |

302 992 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

€ |

302 992 |

|

| Jean-Cyril Spinetta (Director) |

|

|

33 494 |

|

|

€ |

109 525 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

€ |

109 525 |

|

| Sylvia Summers (Director) |

|

|

500 |

|

|

€ |

1 635 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

€ |

1 635 |

|

| Total Other Executive Officers(7) |

|

|

403 078 |

|

|

€ |

1 318 065 |

|

|

|

849 100 |

|

|

€ |

733 622 |

|

|

|

311 975 |

|

|

€ |

1 020 158 |

|

|

|

2 805 000 |

|

|

€ |

9 144 300 |

|

|

€ |

12 216 146 |

|

| Total |

|

|

6 815 005 |

|

|

€ |

22 285 066 |

|

|

|

849 100 |

|

|

€ |

733 622 |

|

|

|

311 975 |

|

|

€ |

1 020 158 |

|

|

|

3 205 000 |

|

|

€ |

10 448 300 |

|

|

€ |

34 487 147 |

|

| (1) |

Includes certain Alcatel Lucent Shares held by directors that are subject to restrictions and may not be tendered into the Exchange Offer. In particular:

|

| |

(a) |

Article 12 of Alcatel Lucent’s By-Laws requires each director to hold at least 500 Alcatel Lucent Shares. As a result, Alcatel Lucent expects that no director will tender

the 500 Alcatel Lucent Shares he or she holds in compliance with this requirement. |

| |

(b) |

The 2010 annual shareholders meeting of Alcatel Lucent authorized the payment of additional attendance fees (jetons de présence) to directors, subject to each

director (i) using the additional fees received (after taxes) to purchase Alcatel Lucent Shares and (ii) holding the acquired Alcatel Lucent Shares for the duration of his or her term of office. |

17

| |

(c) |