| SECURITIES AND EXCHANGE COMMISSION |

| Washington, D.C. 20549 |

| |

| SCHEDULE 13D/A |

| |

INFORMATION TO BE INCLUDED IN STATEMENTS FILED PURSUANT

TO RULE 13d-1(a) AND AMENDMENTS THERETO FILED PURSUANT TO

RULE 13d-2(a) |

| |

| Under the Securities Exchange Act of 1934 |

| (Amendment No. 1)* |

| |

|

AMAG Pharmaceuticals,

Inc. |

| (Name of Issuer) |

| |

|

Common Stock,

par value $0.01 per share |

| (Title of Class of Securities) |

| |

|

00163U106 |

| (CUSIP Number) |

| |

| David Johnson |

| Samuel J. Merksamer |

| Caligan Partners LP |

| 520 Madison Avenue |

| New York, NY 10022 |

| (646) 859-8204 |

| |

| Eleazer Klein, Esq. |

| Schulte Roth & Zabel LLP |

| 919 Third Avenue |

| New York, NY 10022 |

|

(212) 756-2000 |

| (Name, Address and Telephone Number of Person |

| Authorized to Receive Notices and Communications) |

| |

|

September

4, 2019 |

| (Date of Event Which Requires Filing of This Statement) |

If the filing person has previously filed a statement on Schedule

13G to report the acquisition that is the subject of this Schedule 13D, and is filing this schedule because of Rule 13d-1(e), Rule

13d-1(f) or Rule 13d-1(g), check the following box. [ ]

(Page 1 of 10 Pages)

______________________________

* The remainder of this cover page shall be filled out for a reporting

person’s initial filing on this form with respect to the subject class of securities, and for any subsequent amendment containing

information which would alter disclosures provided in a prior cover page.

The information required on the remainder of this cover page shall

not be deemed to be "filed" for the purpose of Section 18 of the Securities Exchange Act of 1934 ("Act")

or otherwise subject to the liabilities of that section of the Act but shall be subject to all other provisions of the Act (however,

see the Notes).

| CUSIP No. 00163U106 | SCHEDULE 13D/A | Page 2 of 10 Pages |

|

1

|

NAME OF REPORTING PERSON

Caligan Partners LP

|

|

2

|

CHECK THE APPROPRIATE BOX IF A MEMBER OF A GROUP |

(a) ¨

(b) x |

|

3

|

SEC USE ONLY |

|

4

|

SOURCE OF FUNDS

AF

|

|

5

|

CHECK BOX IF DISCLOSURE OF LEGAL PROCEEDING IS REQUIRED PURSUANT

TO ITEMS 2(d) or 2(e)

|

¨ |

|

6

|

CITIZENSHIP OR PLACE OF ORGANIZATION

Delaware

|

|

NUMBER OF

SHARES

BENEFICIALLY

OWNED BY

EACH

REPORTING

PERSON WITH: |

7

|

SOLE VOTING POWER

-0-

|

|

8

|

SHARED VOTING POWER

3,499,428 shares of Common Stock

|

|

9

|

SOLE DISPOSITIVE POWER

-0-

|

|

10

|

SHARED DISPOSITIVE POWER

3,499,428 shares of Common Stock

|

|

11

|

AGGREGATE AMOUNT BENEFICIALLY OWNED BY EACH PERSON

3,499,428 shares of Common Stock

|

|

12

|

CHECK IF THE AGGREGATE AMOUNT IN ROW (11) EXCLUDES CERTAIN

SHARES |

¨ |

|

13

|

PERCENT OF CLASS REPRESENTED BY AMOUNT IN ROW (11)

10.3%

|

|

14

|

TYPE OF REPORTING PERSON

IA, PN

|

| |

|

|

|

|

| CUSIP No. 00163U106 | SCHEDULE 13D/A | Page 3 of 10 Pages |

|

1

|

NAME OF REPORTING PERSON

David Johnson

|

|

2

|

CHECK THE APPROPRIATE BOX IF A MEMBER OF A GROUP |

(a) ¨

(b) x |

|

3

|

SEC USE ONLY |

|

4

|

SOURCE OF FUNDS

AF

|

|

5

|

CHECK BOX IF DISCLOSURE OF LEGAL PROCEEDING IS REQUIRED PURSUANT

TO ITEMS 2(d) or 2(e)

|

¨ |

|

6

|

CITIZENSHIP OR PLACE OF ORGANIZATION

United States

|

|

NUMBER OF

SHARES

BENEFICIALLY

OWNED BY

EACH

REPORTING

PERSON WITH: |

7

|

SOLE VOTING POWER

-0-

|

|

8

|

SHARED VOTING POWER

3,499,428 shares of Common Stock

|

|

9

|

SOLE DISPOSITIVE POWER

-0-

|

|

10

|

SHARED DISPOSITIVE POWER

3,499,428 shares of Common Stock

|

|

11

|

AGGREGATE AMOUNT BENEFICIALLY OWNED BY EACH PERSON

3,499,428 shares of Common Stock

|

|

12

|

CHECK IF THE AGGREGATE AMOUNT IN ROW (11) EXCLUDES CERTAIN

SHARES |

¨ |

|

13

|

PERCENT OF CLASS REPRESENTED BY AMOUNT IN ROW (11)

10.3%

|

|

14

|

TYPE OF REPORTING PERSON

IN

|

| |

|

|

|

|

| CUSIP No. 00163U106 | SCHEDULE 13D/A | Page 4 of 10 Pages |

|

1

|

NAME OF REPORTING PERSON

Samuel J. Merksamer

|

|

2

|

CHECK THE APPROPRIATE BOX IF A MEMBER OF A GROUP |

(a) ¨

(b) x |

|

3

|

SEC USE ONLY |

|

4

|

SOURCE OF FUNDS

AF

|

|

5

|

CHECK BOX IF DISCLOSURE OF LEGAL PROCEEDING IS REQUIRED PURSUANT

TO ITEMS 2(d) or 2(e)

|

¨ |

|

6

|

CITIZENSHIP OR PLACE OF ORGANIZATION

United States

|

|

NUMBER OF

SHARES

BENEFICIALLY

OWNED BY

EACH

REPORTING

PERSON WITH: |

7

|

SOLE VOTING POWER

-0-

|

|

8

|

SHARED VOTING POWER

3,499,428 shares of Common Stock

|

|

9

|

SOLE DISPOSITIVE POWER

-0-

|

|

10

|

SHARED DISPOSITIVE POWER

3,499,428 shares of Common Stock

|

|

11

|

AGGREGATE AMOUNT BENEFICIALLY OWNED BY EACH PERSON

3,499,428 shares of Common Stock

|

|

12

|

CHECK IF THE AGGREGATE AMOUNT IN ROW (11) EXCLUDES CERTAIN

SHARES |

¨ |

|

13

|

PERCENT OF CLASS REPRESENTED BY AMOUNT IN ROW (11)

10.3%

|

|

14

|

TYPE OF REPORTING PERSON

IN

|

| |

|

|

|

|

| CUSIP No. 00163U106 | SCHEDULE 13D/A | Page 5 of 10 Pages |

|

1

|

NAME OF REPORTING PERSON

Kenneth Shea

|

|

2

|

CHECK THE APPROPRIATE BOX IF A MEMBER OF A GROUP |

(a) ¨

(b) x |

|

3

|

SEC USE ONLY |

|

4

|

SOURCE OF FUNDS

AF

|

|

5

|

CHECK BOX IF DISCLOSURE OF LEGAL PROCEEDING IS REQUIRED PURSUANT

TO ITEMS 2(d) or 2(e)

|

¨ |

|

6

|

CITIZENSHIP OR PLACE OF ORGANIZATION

United States

|

|

NUMBER OF

SHARES

BENEFICIALLY

OWNED BY

EACH

REPORTING

PERSON WITH: |

7

|

SOLE VOTING POWER

5,000 shares of Common Stock

|

|

8

|

SHARED VOTING POWER

-0-

|

|

9

|

SOLE DISPOSITIVE POWER

5,000 shares of Common Stock

|

|

10

|

SHARED DISPOSITIVE POWER

-0-

|

|

11

|

AGGREGATE AMOUNT BENEFICIALLY OWNED BY EACH PERSON

5,000 shares of Common Stock

|

|

12

|

CHECK IF THE AGGREGATE AMOUNT IN ROW (11) EXCLUDES CERTAIN

SHARES |

¨ |

|

13

|

PERCENT OF CLASS REPRESENTED BY AMOUNT IN ROW (11)

Less than 0.1%

|

|

14

|

TYPE OF REPORTING PERSON

IN

|

| |

|

|

|

|

| CUSIP No. 00163U106 | SCHEDULE 13D/A | Page 6 of 10 Pages |

| The following

constitutes Amendment No. 1 to the Schedule 13D filed by the undersigned (the "Amendment No. 1"). This

Amendment No. 1 amends the Original Schedule 13D, filed with the Securities and Exchange Commission on August 15, 2019 (the

"Original Schedule 13D") as specifically set forth herein. |

| |

| Item 2. |

IDENTITY AND BACKGROUND |

| |

|

| Items 2(a) - (f) of the Schedule 13D are hereby amended and restated as follows: |

| |

|

| (a) |

This statement is filed by:

(i) Caligan Partners LP, a Delaware limited

partnership ("Caligan"), the investment manager of an affiliated fund (the "Caligan Fund") and

managed account (the "Caligan Account"), with respect to the shares of Common Stock held by the Caligan Fund and

the Caligan Account;

(ii) David Johnson, a Partner of Caligan and

a Managing Member of Caligan Partners GP LLC, the general partner of Caligan ("Mr. Johnson"), with respect to

the shares of Common Stock held by the Caligan Fund and the Caligan Account;

(iii) Samuel J. Merksamer, a Partner of Caligan

and a Managing Member of Caligan Partners GP LLC, the general partner of Caligan ("Mr. Merksamer," and together

with Caligan, Caligan Partners GP LLC and Mr. Johnson, the "Caligan Parties") with respect to the shares of Common

Stock held by the Caligan Fund and the Caligan Account; and

(iv) Kenneth Shea ("Mr. Shea"). |

| |

|

| |

Each of the foregoing is referred to as a "Reporting Person" and collectively as the "Reporting Persons." |

| |

|

| (b) |

The principal business address of each of the Caligan Parties is 520 Madison Avenue, New York, New York 10022. The principal business address of Mr. Shea is c/o Caligan Partners, 520 Madison Ave, New York, NY 10022. |

| |

|

| (c) |

The principal business of each of the Caligan Parties is investment management. The principal business of Mr. Shea is investment banking. |

| |

|

| (d) |

During the last five years, none of the Reporting Persons have been convicted in a criminal proceeding (excluding traffic violations or similar misdemeanors). |

| |

|

| (e) |

During the last five years, none of the Reporting Persons have been a party to a civil proceeding of a judicial or administrative body of competent jurisdiction and, as a result of such proceeding, was, or is subject to, a judgment, decree or final order enjoining future violations of, or prohibiting or mandating activities subject to, Federal or State securities laws or finding any violation with respect to such laws. |

| |

|

| CUSIP No. 00163U106 | SCHEDULE 13D/A | Page 7 of 10 Pages |

| (f) |

Caligan is a Delaware limited partnership. Messrs. Johnson, Merksamer and Shea are each United States citizens. Caligan Partners GP LLC is a Delaware limited liability company. |

| Item 3. |

SOURCE AND AMOUNT OF FUNDS OR OTHER CONSIDERATION |

| |

|

| Item 3 of the Schedule 13D is hereby amended and restated by the addition of the following: |

| |

|

| |

The Caligan Parties used a total of approximately

$29,535,114 (including brokerage commissions) to acquire the Common Stock beneficially owned by them. The source of the funds used

to acquire the Common Stock beneficially owned by the Caligan Parties was the working capital of the Caligan Fund and the Caligan

Account.

Mr. Shea used a total of approximately $57,005

(including brokerage commissions) to acquire the Common Stock beneficially owned by him. The source of the funds used to acquire

the Common Stock beneficially owned by Mr. Shea was his personal funds. |

| Item 4. |

PURPOSE OF TRANSACTION |

| |

|

| Item 4 of the Schedule 13D is hereby amended and supplemented by the addition of the following: |

| |

|

| |

On September 4, 2019, the Reporting

Persons filed a preliminary consent statement (the "Preliminary Consent Statement") in connection with

its solicitation of written consents of the Issuer’s stockholders stating, among other things, their intention to

solicit stockholders to (i) remove four members of the Board of the Issuer; (ii) elect the following four individuals—Paul

Fonteyne, Lisa Gersh, David Johnson and Kenneth Shea (collectively, the "Nominees")—to fill the

resulting vacancies; (iii) repeal any provision of the Amended and Restated Bylaws of the Company (the "Bylaws")

currently in effect that was not included in the Bylaws filed with the SEC on December 17, 2015; (iv) amend Article 2,

Sections 2.2 and 2.3 of the Bylaws to fix the size of the Board at no more than nine members; and (v) amend Article 7,

Section 7.1 of the Bylaws to require unanimous Board approval in order for directors to amend the Bylaws.

|

| |

Additionally,

the Reporting Persons issued a press release (the "Press Release"), announcing, among other things, their

intention to solicit consents to remove and replace members of the Board due to operational, strategic and capital

allocation missteps made by the incumbent Board and management of the Issuer. This description of the Press

Release is qualified in its entirety by reference to the full text of the Press Release, which is attached hereto as Exhibit

B and is incorporated by reference herein. The Reporting Persons have also made available a public

presentation to stockholders (the "AMAG Presentation"), stating, among other things, the Reporting

Persons’ belief that (i) the Issuer’s Board is in need of immediate refreshment with the Nominees, (ii)

post-Board refreshment, the Issuer should initiate a comprehensive strategic review around its asset portfolio, (iii) the

Issuer should engage an international distribution partner for Feraheme and (iv) the Issuer should immediately rationalize its

commercial spending and explore non-traditional efforts and partnerships to market certain products. The foregoing

summary of the AMAG Presentation is qualified in its entirety by reference to the full text of the AMAG Presentation, which

is attached hereto as Exhibit C and is incorporated by reference herein. |

| CUSIP No. 00163U106 | SCHEDULE 13D/A | Page 8 of 10 Pages |

| Item 5. |

INTEREST IN SECURITIES OF THE ISSUER

|

| |

|

|

Items 5 (a) – (c) of the Schedule 13D are hereby

amended and restated as follows:

|

|

|

| (a) |

See rows (11) and (13) of the cover pages to

this Schedule 13D for the aggregate number of and percentages of the shares of Common Stock beneficially owned by each Reporting

Person. The percentages set forth in this Schedule 13D are based upon 33,900,681 shares of Common Stock outstanding as of August

1, 2019, as reported in the Issuer's Quarterly Report on Form 10-Q for the quarterly period ended June 30, 2019, filed with the

Securities and Exchange Commission on August 7, 2019.

By reason of Caligan's intention

to solicit consents of stockholders in favor of appointing Mr. Shea to the Board, the Caligan Parties and Mr. Shea may be

deemed members of a "group" within the meaning of Section 13(d)(3) of the Act and the "group" may be

deemed to beneficially own an aggregate of 3,504,428 shares of Common Stock, or

approximately 10.3% of the outstanding Common Stock. The Caligan Parties expressly

disclaim beneficial ownership of any shares of Common Stock beneficially owned by

Mr. Shea and Mr. Shea expressly disclaims beneficial ownership of any

shares of Common Stock beneficially owned by the Caligan Parties. |

| |

|

| (b) |

See rows (7) through (10) of the cover pages

to this Schedule 13D for the number of shares of Common Stock as to which each Reporting Person has the sole or shared power to

vote or direct the vote and sole or shared power to dispose or to direct the disposition.

|

| |

|

| (c) |

The Caligan Parties have not transacted in any securities of the Issuer since the filing of the Original Schedule 13D. Information concerning transactions in the shares of Common Stock reported herein effected during the past sixty (60) days by Mr. Shea is set forth in Annex A, which is attached hereto and is incorporated herein by reference. All of the transactions in the shares of Common Stock listed therein were effected in the open market through various brokerage entities. |

| |

|

| CUSIP No. 00163U106 | SCHEDULE 13D/A | Page 9 of 10 Pages |

| Item 6. |

CONTRACTS, ARRANGEMENTS, UNDERSTANDINGS OR RELATIONSHIPS WITH RESPECT TO SECURITIES OF THE ISSUER |

| |

|

| Item 6 of the Schedule 13D is hereby amended and supplemented by the addition of the following: |

| |

| |

The Reporting Persons entered into

an agreement with each of the Nominees (except Mr. Johnson) (the "Nomination Agreement") whereby, among other

things, each Nominee party to a Nomination Agreement agreed to consult with the Reporting Persons regarding any purchase of securities

of the Issuer and to not dispose of any such securities prior to the termination of the Nomination Agreement without the prior

consent of Caligan. This description of the Nomination Agreement is qualified in its entirety by reference to the full text of

the Nomination Agreement, the form of which is attached hereto as Exhibit D and is incorporated by reference herein.

On

September 4, 2019, Caligan and Mr. Shea entered into a Joint Filing Agreement in which, among other things, the parties agreed

to the joint filing on behalf of each of them of statements on Schedule 13D, and any amendments thereto, with respect to the securities

of the Issuer to the extent required by applicable law. The Joint Filing Agreement is filed as Exhibit E to this Schedule

13D and is incorporated by reference into this Item 6. |

| Item 7. |

MATERIAL TO BE FILED AS EXHIBITS |

| |

|

| Item 7 of the Schedule 13D is hereby amended and supplemented by the addition of the following: |

| |

|

| Exhibit B: |

Press Release |

|

|

| Exhibit

C: |

AMAG Presentation |

| |

|

| Exhibit

D: |

Form of Nomination Agreement |

| |

|

| Exhibit E: |

Joint Filing Agreement |

| |

|

|

| CUSIP No. 00163U106 | SCHEDULE 13D/A | Page 10 of 10 Pages |

SIGNATURES

After reasonable inquiry and to the best

of his or its knowledge and belief, the undersigned certifies that the information set forth in this statement is true, complete

and correct.

Dated:

September 4, 2019

| |

CALIGAN PARTNERS LP |

| |

|

|

| |

|

|

| |

By: |

/s/ David Johnson |

| |

Name: |

David Johnson |

| |

Title: |

Partner |

| |

|

| |

|

| |

/s/ David Johnson |

| |

DAVID JOHNSON |

| |

|

| |

|

| |

/s/ Samuel J. Merksamer |

| |

SAMUEL J. MERKSAMER |

| |

|

| |

|

| |

/s/

Kenneth Shea |

| |

KENNETH SHEA |

| |

|

| |

|

Annex A

Transactions in the Shares of Common Stock

of the Issuer in the Past Sixty Days

The following table sets

forth all transactions in the Common Stock effected by Mr. Shea in the past sixty (60) days. Except as noted below, all such transactions

were effectuated by Mr. Shea in the open market through brokers and the price per share excludes commissions.

Mr. Shea

| Trade Date |

Shares Purchased (Sold) |

Price Per Share ($) |

| |

|

|

| 8/19/2019 |

5,000 |

11.40 |

| |

|

|

EXHIBIT B

CALIGAN PARTNERS FILES PRELIMINARY

CONSENT STATEMENT TO REPLACE FOUR DIRECTORS OF AMAG PHARMACEUTICALS, INC.

CALIGAN RELEASES PRESENTATION

AT WWW.SAVEAMAG.COM DETAILING URGENT NEED FOR CHANGE

NEW YORK, September 4, 2019—

Caligan Partners LP (“Caligan”), one of the largest shareholders of AMAG Pharmaceuticals, Inc. (“AMAG”

or the “Company”), announced today that it has filed a preliminary consent statement with the U.S. Securities and Exchange

Commission (the “SEC”) for shareholders to act by written consent to effect the replacement of four directors of AMAG

and to, among other things, amend the Company's bylaws to help prevent against entrenchment by incumbent directors.

Caligan’s nominees for change

include:

| · | Paul Fonteyne, former CEO of Boehringer Ingelheim USA |

| · | Lisa Gersh, former CEO of Alexander Wang, Goop, and Martha Stewart Living Omnimedia |

| · | David Johnson, Managing Partner of Caligan Partners LP |

| · | Kenneth Shea, Senior Advisor, Guggenheim Securities, LLC |

Additional information on each

of the nominees is available at www.saveamag.com. Caligan has released presentation materials highlighting the operational, strategic,

and capital allocation missteps that have resulted in over $1.3 billion of value destruction overseen by AMAG’s incumbent

board and management. The materials note that while Caligan believes AMAG has unique, durable assets that could be worth at least

$30 per share, AMAG’s current leadership will be unable to achieve that outcome for shareholders. The presentation can be

accessed here.

David Johnson, Managing Partner

of Caligan, issued the following statement: “We believe urgent change is needed at AMAG to reverse the sharp share price

decline caused by the Company’s misguided strategic priorities. Caligan’s highly qualified nominees will conduct a

comprehensive review of AMAG’s product portfolio, research and development priorities, and SG&A spending.”

Once Caligan files a definitive

consent statement, Caligan will begin soliciting the consents of stockholders.

Caligan strongly recommends

that if AMAG stockholders have loaned, pledged or hypothecated any of their Common Stock, they consult with their bank or broker

in order to have these shares returned to their accounts before the forthcoming record date. Doing so will allow AMAG stockholders

to express consent on all of their shares of Common Stock in favor of Caligan’s nominees and proposals.

Investor Contact

Edward McCarthy/ Geoffrey Weinberg

DF King & Co., Inc.

+1 (212) 269-5550

AMAG@dfking.com

Media Contact

Robert Laman

Caligan Partners

+1 (646) 859-8205

rl@caliganpartners.com

For Additional Information

IR@caliganpartners.com

LEGEND

Caligan, Caligan CV II LP, David

Johnson, Samuel Merksamer, Paul Fonteyne, Lisa Gersh, and Kenneth Shea (collectively, the “Participants”) intend to

file with the SEC a definitive consent statement and accompanying form of consent card to be used in connection with the solicitation

of consents from the stockholders of AMAG Pharmaceuticals, Inc. (the “Company”). All stockholders of the Company are

advised to read the definitive consent statement and other documents related to the solicitation of consents by the Participants

when they become available, as they will contain important information, including additional information related to the Participants.

The definitive consent statement and an accompanying consent card will be furnished to some or all of the Company’s stockholders

and will be, along with other relevant documents, available at no charge on the SEC website at http://www.sec.gov/ and at Caligan’s

website www.saveamag.com and from the Participants’ consent solicitor, D.F. King & Co., Inc. by requesting a copy via

email to AMAG@dfking.com. Information about the Participants and a description of their direct or indirect interests by security

holdings is contained in the Schedule 14A filed by Caligan with the SEC on September 4, 2019. This document is available free of

charge from the sources indicated above.

About Caligan Partners LP

Caligan Partners LP is an investment

firm headquartered in New York, NY that pursues a deep value-oriented strategy through investments in activist equities and distressed

debt.

EXHIBIT C

SAVING AMAG: URGENT CHANGE NEEDED TO UNLOCK VALUE SEPTEMBER 2019 WWW.SAVEAMAG.COM

Additional Information 2 • THIS PRESENTATION AND THE VIEWS EXPRESSED HEREIN ARE ONLY TO BE USED TO PROVIDE GENERAL INFORMATION FROM CALIGAN PARTNERS LP AND ITS AFFILIATES (COLLECTIVELY, “CALIGAN”) REGARDING AMAG PHARMACEUTICALS, INC . (“AMAG” OR THE “COMPANY”) . THIS PRESENTATION AND THE VIEWS EXPRESSED HEREIN DO NOT HAVE REGARD TO THE SPECIFIC INVESTMENT OBJECTIVE, FINANCIAL SITUATION, SUITABILITY, OR THE PARTICULAR NEED OF ANY SPECIFIC PERSON WHO MAY RECEIVE THIS PRESENTATION, AND SHOULD NOT BE TAKEN AS ADVICE ON THE MERITS OF ANY INVESTMENT DECISION . THE VIEWS EXPRESSED HEREIN REPRESENT THE CURRENT OPINIONS AS OF THE DATE HEREOF OF CALIGAN AND ARE DERIVED FROM PUBLICLY AVAILABLE INFORMATION AND THE ANALYSIS OF CALIGAN REGARDING THE COMPANY . CERTAIN FINANCIAL INFORMATION AND DATA USED HEREIN HAVE BEEN DERIVED OR OBTAINED FROM, WITHOUT INDEPENDENT VERIFICATION, PUBLIC FILINGS, INCLUDING FILINGS MADE BY THE COMPANY WITH THE SECURITIES AND EXCHANGE COMMISSION (“SEC”), AND OTHER SOURCES . • THIS PRESENTATION DOES NOT CONSTITUTE AN OFFER TO SELL OR A SOLICITATION OF AN OFFER TO BUY ANY SECURITY DESCRIBED HEREIN IN ANY JURISDICTION TO ANY PERSON, NOR DOES IT CONSTITUTE A FINANCIAL PROMOTION, INVESTMENT ADVICE OR AN INDUCEMENT OR AN INCITEMENT TO PARTICIPATE IN ANY PRODUCT, OFFERING OR INVESTMENT . THIS PRESENTATION IS INFORMATIONAL ONLY AND SHOULD NOT BE USED AS THE BASIS FOR ANY INVESTMENT DECISION, NOR SHOULD IT BE RELIED UPON FOR LEGAL, ACCOUNTING OR TAX ADVICE OR INVESTMENT RECOMMENDATIONS OR FOR ANY OTHER PURPOSE . NO REPRESENTATION OR WARRANTY IS MADE THAT CALIGAN’S INVESTMENT PROCESSES OR INVESTMENT OBJECTIVES WILL OR ARE LIKELY TO BE ACHIEVED OR SUCCESSFUL OR THAT CALIGAN’S INVESTMENT WILL MAKE ANY PROFIT OR WILL NOT SUSTAIN LOSSES . PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS . • CALIGAN HAS NOT SOUGHT OR OBTAINED CONSENT FROM ANY THIRD PARTY TO USE ANY STATEMENTS OR INFORMATION INDICATED HEREIN AS HAVING BEEN OBTAINED OR DERIVED FROM STATEMENTS MADE OR PUBLISHED BY THIRD PARTIES . ANY SUCH STATEMENTS OR INFORMATION SHOULD NOT BE VIEWED AS INDICATING THE SUPPORT OF SUCH THIRD PARTY FOR THE VIEWS EXPRESSED HEREIN . NO WARRANTY IS MADE THAT DATA OR INFORMATION, WHETHER DERIVED OR OBTAINED FROM FILINGS MADE WITH THE SEC OR FROM ANY THIRD PARTY, ARE ACCURATE . • EXCEPT FOR THE HISTORICAL INFORMATION CONTAINED HEREIN, THE MATTERS ADDRESSED IN THIS PRESENTATION, INCLUDING PROJECTIONS, MARKET OUTLOOKS, ASSUMPTIONS AND ESTIMATES, ARE FORWARD - LOOKING STATEMENTS THAT ARE BASED ON CERTAIN ASSUMPTIONS, AND INVOLVE CERTAIN RISKS AND UNCERTAINTIES, INCLUDING RISKS AND CHANGES AFFECTING INDUSTRIES GENERALLY AND THE COMPANY SPECIFICALLY . YOU SHOULD BE AWARE THAT PROJECTIONS AND OTHER FORWARD - LOOKING STATEMENTS ARE INHERENTLY UNCERTAIN, AND ACTUAL RESULTS MAY DIFFER FROM THE PROJECTIONS AND OTHER FORWARD LOOKING STATEMENTS CONTAINED HEREIN DUE TO REASONS THAT MAY OR MAY NOT BE FORESEEABLE . NO REPRESENTATION, WARRANTY OR UNDERTAKING, EXPRESS OR IMPLIED, IS MADE AS TO THE ACCURACY OR REASONABLENESS OF THE ASSUMPTIONS UNDERLYING THE PROJECTIONS AND OTHER FORWARD LOOKING STATEMENTS CONTAINED HEREIN OR TO THE ACCURACY OR COMPLETENESS OF THE INFORMATION OR VIEWS CONTAINED HEREIN . • CALIGAN SHALL NOT BE RESPONSIBLE OR HAVE ANY LIABILITY FOR ANY MISINFORMATION CONTAINED IN ANY SEC FILING, ANY THIRD PARTY REPORT OR THIS PRESENTATION . ALL AMOUNTS, MARKET VALUE INFORMATION AND ESTIMATES INCLUDED IN THIS PRESENTATION HAVE BEEN OBTAINED FROM OUTSIDE SOURCES THAT CALIGAN BELIEVES TO BE RELIABLE OR REPRESENT THE BEST JUDGMENT OF CALIGAN AS OF THE DATE OF THIS PRESENTATION . • CALIGAN RESERVES THE RIGHT TO CHANGE OR MODIFY ANY OF ITS OPINIONS EXPRESSED HEREIN AT ANY TIME AS IT DEEMS APPROPRIATE . CALIGAN DISCLAIMS ANY OBLIGATION TO UPDATE THE INFORMATION CONTAINED HEREIN .

Executive Summary 3 • Caligan Partners, LP is one of the largest shareholders of AMAG Pharmaceuticals, owning over 10 % of AMAG’s outstanding shares • Caligan is seeking removal of four incumbent AMAG directors who have seen an average total shareholder return of NEGATIVE 63 . 9 % 2 over their tenures • Caligan’s has nominated four individuals (the “Nominees”) who will bring the experience, financial discipline, and accountability necessary to rebuild shareholder value • Caligan believes that AMAG could be worth more than $ 30 per share 1 , 170 % higher than its current trading levels 1 See slide 6 for additional details. Based on AMAG’s closing share price of $11.24 as of September 3, 2019 2 See slide 12 for additional details

Caligan’s Message to AMAG Shareholders • Caligan is seeking your support to : • Remove four AMAG directors who have overseen significant value destruction • Elect our four highly qualified Nominees to the Board • To prevent Board entrenchment, Caligan is asking your consent to : • Repeal any provision in the bylaws that would seek to circumvent our attempts to act by written consent • Amend the bylaws to fix the size of the Board at nine members and require unanimous approval in order for the Board to amend the bylaws • To ensure you have the right to consent : • If you have loaned, pledged, or hypothecated your common stock, please consult with your bank or broker in order to have those shares returned to your account before the record date (which we expect to be set by AMAG) 4

Caligan Nominees For Change 5 Nominees Education Relevant Experience Paul Fonteyne MBA, Carnegie Mellon University MS, Chemical Engineering, University of Brussels • President and CEO of Boehringer Ingelheim USA Corporation • Commercial Leadership Roles, Boehringer Ingelheim, Merck and Co., Inc. and Abbott Laboratories • Current Director of resTORbio , Inc. (TORC) and Ypsomed Holding AG (SWX: YPSN) Lisa Gersh JD, Rutgers Law School BA, SUNY Binghamton • Former CEO, Alexander Wang, Former CEO, Goop Inc. • President & CEO, Martha Stewart Living Omnimedia • Current Director of Hasbro, Inc. (HAS) and Establishment Labs Holdings, Inc. (ESTA) David Johnson SM, Harvard College AB, Harvard College • Co - Founder, Managing Partner, Caligan Partners LP • Former Managing Director, The Carlyle Group • Former Vice President, Morgan Stanley Kenneth Shea MBA, University of Virginia BA, Boston College • Senior Advisor, Guggenheim Securities, LLC • Former Senior Managing Director, Guggenheim Securities • Former Senior Managing Director, Bear, Stearns & Co. Inc. • Current Director of Equity Commonwealth (EQC)

What Could AMAG Be Worth? 6 1 S&P Capital IQ For Consensus Revenue estimates and highest analyst revenue estimates 2 Caligan estimates . High end of the EV/Revenue range consistent with Vifor Pharma EV/Revenue multiple as detailed on slide 17 . For Feraheme International Rights, 26 % global market share on $ 413 MM of ex - US Ferinject sales equals $ 119 MM of ex - US Feraheme revenue . At a 33 . 33 % royalty rate, AMAG would receive $ 39 . 7 MM annually . 3 - 7 x capitalization rate . 3 Caligan calculation based on AMAG 2018 10 - K which disclosed $ 46 . 9 MM of tax - effected net operating losses, $ 24 . 3 MM of tax credit carryforwards, $ 20 . 9 MM of tax - effected capital loss carryforwards, and Caligan’s estimate of $ 165 MM of 2019 pre - tax operating losses multiplied by a 21 % effective tax rate 4 Value of AMAG’s pipeline assets is based on AMAG capital invested to date, including $ 68 . 2 MM for the acquisition of Perosphere , $ 22 . 5 MM for the acquisition of Velo Bio LLC, and $ 100 MM of investment in R&D in 2019 5 Caligan fully - diluted share calculation based on RSUs outstanding, options outstanding, and conversion of the 2022 convertible notes 6 Based on AMAG’s closing price of $ 11 . 24 on September 3 , 2019 • Caligan believes the individual pieces of AMAG’s portfolio are worth substantially more than AMAG’s current enterprise value • A strategic review could maximize value for AMAG shareholders by unlocking its significant sum of the parts discount • Caligan believes that, assuming conservative EV/revenue multiples and ascribing no value to AMAG’s pipeline, AMAG is worth at least ~ $ 30 per share, a 170 % premium to current trading levels Base High 2020E Feraheme Revenues 1 186.1 210.0 EV/Revenue 2 3.0x 7.0x Feraheme EV 558.2 1,470.0 Feraheme International Rights 2 119.1 277.9 2020E Makena Revenues 1 111.5 156.9 EV/Revenue 2 2.0x 3.0x Makena EV 223.0 470.7 Other Products 1 54.9 75.4 EV/Revenue 2 1.0x 2.0x Other Products EV 54.9 150.8 Tax Assets 3 126.7 126.7 Pipeline Assets 4 190.7 190.7 Total AMAG EV 1,272.6 2,686.8 YE2019 Net (Debt)/Cash 1 200.0 200.0 Total Equity Value 1,472.6 2,886.8 Fully Diluted Shares Outstanding 5 48.6 49.4 AMAG Value Per Share 30.31$ 58.42$ Upside 6 170% 420%

AMAG Has a Collection of Valuable Assets 7 • Feraheme is a one of two approved high molecular weight IV irons in the US ; 2019 E net sales of $ 170 MM 1 • Feraheme has competitive advantages (substantially lower rates of hypophosphatemia, lower cost per dose) versus its primary competitor, Injectafer • AMAG owns the worldwide rights to Feraheme but has no international distribution partner currently • Makena is the only FDA approved therapy indicated to reduce the risk of recurrent pre - term birth ; 2019 E net sales of ~ $ 145 MM 1 1 Consensus estimates from S&P Capital IQ.

Feraheme Is A Durable, Growing Product 8 • Feraheme is one of six marketed intravenous (IV) iron products in the US and one of two high molecular weight IV irons • Feraheme received a label expansion in February 2018 , based on a non - inferiority study versus Injectafer, which allowed it to expand into iron deficiency anemia (IDA) in non - chronic kidney disease (non - CKD) patients, resulting in revenue growth of 27 % in 2018 and consensus revenue growth of 26 % in 2019 . The non - inferiority study highlighted Feraheme’s (i) comparable safety profile and (ii) hypophosphatemia benefits versus Injectafer • IV irons are non - biologic complex drugs (“NBCD”) ; Venofer’s patents expired in November 2003 and it has not had a generic competitor introduced to date Marketed US IV Iron Revenue Per Product ($MM) 1 1 Consensus estimates for revenue and revenue growth from S&P Capital IQ 0 50 100 150 200 250 300 350 400 450 500 Ferrlecit InFed Nulecit Feraheme Venofer Injectafer 2019E Growth 1 : 0% 0% 0% 26% - 3% 18% Patent Expiry: Expired Expired N/A 2023 Expired 2003 2027 Approved: 1999 1974 2011 2009 2000 2013

Feraheme & Makena Auto - Injector Continue To Grow Market Share 9 • Post label expansion in February 2018 , Feraheme has continued to increase its share of the IDA market . Caligan believes that, given the hypophosphatemia and cost benefits versus Injectafer , Feraheme has a significant opportunity to grow its presence in gastroenterology, oncology, and iron deficiency in pregnancy • Makena, the only FDA approved treatment option to lower the risk of recurrent preterm birth, has had generic competition since July 2018 . AMAG launched its patent - protected auto - injector in 2 Q 2018 and has continued to take share from the generic intramuscular injection due to physician, nurse and patient preference for the auto - injector • Caligan believes Feraheme and Makena are durable, growing products which serve serious medical needs and could make AMAG worth ~ $ 30 /share 3 . AMAG’s Board and management have chosen to invest the cash flows from Feraheme and Makena in value destructive business development Feraheme IDA Market Share 1 Makena Auto - Injector Market Share 2 1 AMAG Quarterly Investor Presentations 2 AMAG Quarterly Investor Presentations. Share of FDA - approved hydroxyprogesterone caproate 3 See slide 6 for additional details 10% 11% 12% 13% 14% 15% 16% 17% 18% 1Q2018 2Q2018 3Q2018 4Q2018 1Q2019 2Q2019 Post IDA non - CKD label expansion 10% 20% 30% 40% 50% 60% 70% 4Q2018 1Q2019 2Q2019

Fundamental Problems At AMAG 10 AMAG’s Board & Management Have Abysmal TSR AMAG Commercial Spending Needs To Be Rationalized Business Development Has Destroyed Shareholder Value AMAG Management Lacks Credibility No Commercial Synergies Across Portfolio Caligan Action Plan

Underperformance Of Total Shareholder Return Over Any Time Period Against Any Relevant Benchmark 11 • AMAG has materially underperformed all of its relevant benchmarks over the last 1 , 2 , 3 , 5 and 10 - year periods • Specifically, AMAG has underperformed the NASDAQ Biotech Index by : • - 393 % over the last 10 years • - 84 % over the last 5 years 1 Through July 31, 2019, the day before Caligan began substantial purchases of AMAG shares. All TSR data from S&P Capital IQ 2 Proxy peers include ACOR, ASRT, EGRX, EBS, HZNP, IRWD, NKTR, PCRX, SPPI, SUPN, MDCO, TXMD, and VNDA 10-Yr 1 5-Year 1 3-Year 1 2-Year 1 1-Year 1 AMAG Pharmaceuticals -81.8% -56.7% -68.9% -57.9% -62.5% Nasdaq Biotech Index 310.9% 27.4% 10.2% -1.1% -9.2% Relative Performance -392.7% -84.1% -79.1% -56.7% -53.3% Proxy Peer Average 2 112.3% 61.1% 0.4% -8.0% -32.7% Relative Performance -194.1% -117.9% -69.3% -49.9% -29.9% Proxy Peer Median 2 14.7% -3.8% 10.3% -6.7% -37.0% Relative Performance -96.5% -52.9% -79.2% -51.2% -25.6% Russell 2000 224.5% 50.7% 34.4% 13.0% -4.5% Relative Performance -306.3% -107.4% -103.2% -70.9% -58.1%

Significant Underperformance Over The Course Of Every Director’s Tenure 1 12 • AMAG’s total shareholder return has significantly underperformed both the Nasdaq Biotech Index and the S&P 500 over the tenure of every director • Every AMAG director has overseen a significant absolute decline in AMAG shares over their tenure 1 Through July 31, 2019, the day before Caligan began substantial purchases of AMAG shares. All TSR data from S&P Capital IQ Directors for which Caligan is seeking their removal Director Director Since AMAG Performance Nasdaq Biotech Index AMAG Relative Performance S&P 500 AMAG Relative Performance Davey Scoon 12/1/2006 -86.0% 307.3% -393.3% 175.4% -261.4% Gino Santini 2/7/2012 -51.1% 165.7% -216.8% 156.4% -207.6% Bill Heiden 5/9/2012 -48.4% 160.3% -208.8% 153.5% -202.0% Barbara Deptula 9/9/2013 -66.9% 55.6% -122.4% 99.8% -166.6% James Sulat 4/16/2014 -53.5% 43.7% -97.1% 77.3% -130.8% Dr. John Fallon 9/5/2014 -64.8% 18.1% -82.9% 63.3% -128.1% Rob Perez 7/1/2015 -88.3% -13.7% -74.7% 55.2% -143.5% Kathrine O'Brien 4/12/2019 -33.9% -4.8% -29.1% 3.0% -36.9% Anne Phillips 4/12/2019 -33.9% -4.8% -29.1% 3.0% -36.9%

-100% -50% 0% 50% 100% 150% 200% 250% 300% 350% 400% Underperformance Versus Peer Set 1 13 • Relative to its 2013 and 2018 proxy peer sets, AMAG is the third and second worst performing company in the peer group, respectively • To note, 7 of the 18 companies in the 2013 proxy peer set have sold themselves • From May 9 , 2012 to July 31 , 2019 , AMAG has underperformed : • The 2013 Peer Group by - 186 % • The 2018 Peer Group by - 150 % 1 Total shareholder return performance from May 9, 2012, the day of the appointment of Bill Heiden as CEO, through July 31, 2019, the day before Caligan began substantial purchases of AMAG shares. Peer Group’s from AMAG Proxy Statements. 2012 Proxy Peer Group not disclosed. AMAG has underperformed every proxy peer set over every year from 2013 – 2018. All TSR data from S&P Capital IQ TSR (2013 Proxy Peer Group) 1 TSR (2018 Proxy Peer Group) 2 -100% 200% 500% 800% 1100% 1400% 1700% 2000% 2300% 2600% DYAX RGEN ARRY LGND ALNY NPSP CADX IMMU SCMP ENZN DUSA OPTR ASRT PGNX AMAG INFI AFFY

Fundamental Problems At AMAG 14 AMAG’s Board & Management Have Abysmal TSR AMAG Commercial Spending Needs To Be Rationalized Business Development Has Destroyed Shareholder Value AMAG Management Lacks Credibility No Commercial Synergies Across Portfolio Caligan Action Plan

Over $1.3 Billion Of Non - Feraheme Capital Invested Since 2013 Has Resulted In Negative Value To AMAG Shareholders 15 • $ 1 . 38 Bn of shareholder capital has been spent on non - Feraheme related R&D, acquisitions (net of divestitures), and milestone payments from Jan 2012 – June 2019 . The cumulative change in AMAG’s market cap since May 2012 is negative $ 13 MM . 1 All information from AMAG SEC filings. Non - Feraheme R&D is R&D enumerated in AMAG SEC filings to products other than Feraheme. Acquisitions are netted with the proceeds of the CBR sale. Milestone payments includes the $60MM payment to Palatin that was paid in July 2019. Change in AMAG market capitaliza tio n from S&P Capital IQ. Capital Invested vs Change in Market Cap (May 2012 – July 2019) 1 (50) 100 250 400 550 700 850 1,000 1,150 1,300 1,450 2012 - 2019 Capital Invested Change in Mkt Cap (Since May 2012) Non-Feraheme R&D Acquisitions (Net) Milestone Payments Total

Despite 27% CAGR For Feraheme Sales, AMAG’s Market Cap Has Declined At A 1% CAGR 16 • Despite AMAG’s only commercial product in 2012 , Feraheme, growing its US revenues at a 27 % CAGR from 2012 – 2019 E, AMAG’s market capitalization has declined at a 1 % CAGR since May 2012 • Additionally, due to the dilution from value destructive stock issuances, AMAG shareholders who held AMAG stock in 2012 only own 63 % of Feraheme today • Based on our analysis, if, beginning in 2012 , AMAG had done no business development and AMAG traded at the same multiple of forward revenues that it did in 2012 , AMAG’s market cap would be at least 52 % higher than where it is trading today 3 1 All market capitalization data from S&P Capital IQ 2 SEC Filings 3 AMAG traded at 1.57x forward revenues in March 2012. Using 1.57x EV/Revenues multiplied by $170MM of 2019E Revenues for Fera he me, excluding the 37% share dilution would imply a market capitalization of $423MM, a 52% premium to AMAG’s $278MM market capitalization as of July 31, 2019 AMAG Market Cap 1 Feraheme US Net Revenues 2 275 277 279 281 283 285 287 289 291 293 AMAG Mkt Cap - May 2012 AMAG Mkt Cap - July 2019 - 1% CAGR 50 70 90 110 130 150 170 190 2012 2019E 27% CAGR

- 2,000 4,000 6,000 8,000 10,000 12,000 Vifor IV Iron 2019E Rev Vifor EV - July 2019 - 50 100 150 200 250 300 350 Feraheme 2019E Rev AMAG EV - July 2019 Comparison With Vifor Highlights Undervalued IV Iron Franchise 17 • Feraheme, despite having no international distribution partner, and giving a four year head start to Injectafer to penetrate IDA in non - CKD patients in the US, is on pace to generate $ 170 MM of revenue in 2019 . As physician awareness of Feraheme’s benefits increases, Caligan believes Feraheme will continue to grow its share of the IDA market • Despite a growing, durable, IV iron franchise, AMAG trades at a fraction of the multiple of Vifor Pharma, the dominant IV iron competitor • We believe that separating Feraheme from the rest of AMAG should deliver significant value to AMAG shareholders that is multiples higher than its current trading price 1 Consensus Feraheme estimates from S&P Capital IQ. EV from S&P Capital IQ 2 Consensus IV iron estimates from S&P Capital IQ. EV from S&P Capital IQ. Vifor IV Iron revenue incorporates the full amount o f Regent’s US sales. Vifor reports 33.3% of the total revenue for Regent’s sales and bears no costs. AMAG ( Feraheme ) ($MM) 1 Vifor Pharma ($MM) 2 1.7x EV/Revenue 7.5x EV/Revenue

• For public companies focused on women’s health, despite having the highest 2020 E consensus revenue, AMAG has (i) a lower enterprise value than both TherapeuticsMD and Obseva and (ii) the worst TSR of the three companies under the tenure of AMAG’s current Board and management • Caligan believes this disconnect between commercial success and market value results from (i) a lack of management credibility with the investment community ; (ii) poor capital allocation ; and (iii) the market’s view of AMAG’s pipeline Comparison With Other Women’s Health Companies Demonstrates Market’s Opinion of AMAG Board, Management, & Pipeline 18 1 S&P Capital IQ consensus estimates 2 S&P Capital IQ as of 7 / 31 / 19 , , the day before Caligan began substantial purchases of AMAG shares 3 All TSR data from S&P Capital IQ . Obseva TSR from IPO as of January 25 , 2017 2020 Consensus Revenue ($MM) 1 Current Enterprise Value 2 TSR Since May 2012 3 - 50 100 150 200 250 300 350 400 AMAG TXMD OBSV - 50 100 150 200 250 300 350 400 450 500 TXMD OBSV AMAG -50% -45% -40% -35% -30% -25% -20% -15% -10% -5% 0% TXMD OBSV AMAG

Fundamental Problems At AMAG 19 AMAG’s Board & Management Have Abysmal TSR AMAG Commercial Spending Needs To Be Rationalized Business Development Has Destroyed Shareholder Value AMAG Management Lacks Credibility No Commercial Synergies Across Portfolio Caligan Action Plan

• As a percentage of revenues, AMAG’s cash SG&A spending is 30 percentage points higher than its next closest peer and 50 percentage points higher than pharmaceutical companies with similar product revenues • AMAG spends more than 90 % of its market capitalization on its commercial infrastructure and launch costs . The next closest peer is 50 percentage points lower and AMAG is 80 percentage points higher than the average of pharmaceutical companies with similar product revenues • This spending, associated with Intrarosa and Vyleesi launches and commercialization, is a significant overhang on AMAG shares with the investment community AMAG’s Commercial Infrastructure And Launch Costs Are Exorbitant Relative To Peers 3 20 1 SG&A is last quarter SG&A reported in respective SEC filings, less stock - based compensation expense, annualized . 2020 E revenues are consensus estimates from S&P Capital IQ . Comparison set is chosen as US public pharmaceutical and biotech companies that are expected to generate between $ 300 MM and $ 600 MM of product revenue in 2020 . 2 SG&A is last quarter SG&A reported in respective SEC filings, less stock - based compensation expense, annualized . Market Capitalization calculated by S&P Capital IQ . Comparison set is chosen as US public pharmaceutical and biotech companies that are expected to generate between $ 300 MM and $ 600 MM of consensus product revenue in 2020 . 3 Comparison set is chosen as US public pharmaceutical and biotech companies that are expected to generate between $ 300 MM and $ 600 MM of consensus product revenue in 2020 . SG&A Run - Rate (% of 2020E Revenues) 1 SG&A Run - Rate (% of Market Cap) 2 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

• The synergies that AMAG highlighted when pursuing the Lumara and CBR acquisitions have never materialized : • When announcing the Lumara acquisition in September 2014 , AMAG highlighted revenues of $ 180 MM and EBITDA of $ 110 MM and synergies of $ 20 MM . Combined with Feraheme this would imply an operating expense run - rate of $ 101 MM . Actual 2015 operating expense of $ 131 MM missed by over $ 30 MM • Then, in 2015 , in announcing the purchase of CBR, AMAG highlighted $ 60 MM of EBITDA from CBR, which included $ 15 MM of synergies . Combined with Feraheme and Makena, this implied an operating expense run - rate of $ 145 MM . Actual 2016 operating expense of $ 193 MM missed by over $ 47 MM Announced Merger Synergies Never Materialized 21 1 Feraheme 2014 SG&A is from AMAG”s 10 - Q annualized . Makena operating expenses are calculated as $ 180 MM of revenue at an assumed 95 % gross margin less $ 110 MM of EBITDA . Synergies are from AMAG’s investor presentation announcing the acquisition . 2015 Actual is from AMAG’s 2018 10 - K 2 Feraheme 2014 SG&A is from AMAG”s 10 - Q annualized . Makena operating expenses are calculated as $ 180 MM of revenue at an assumed 95 % gross margin less $ 110 MM of EBITDA . Synergies are from AMAG’s investor presentation announcing the acquisition . CBR operating expenses are using AMAG”s projections from the CBR acquisition announcement which assumed $ 120 MM of revenue, at a 95 % gross margin, less $ 60 MM of EBITDA . 2016 Actual operating expenses are from AMAG’s 2016 10 - K Feraheme + Makena Opex ($MM) 1 Feraheme, Makena + CBR Opex ($MM) 2 $30MM Miss $47MM Miss

AMAG SG&A Productivity Lowest Of Peers With >$300MM Product Revenue 22 1 Gross Profit and SG&A from 2014 – 2018 from SEC Filings (S&P Capital IQ). AMAG Gross Profit excludes intangible amortization. Peer group selected as companies with >$300MM of product revenue in 2015 and consensus estimates of >$300MM of product revenue in 2019E 5 - Year Gross Profit/SG&A Ratio 1 • Of all North American biotech and pharmaceutical companies that generated more than $ 300 MM of revenue in 2015 and have consensus revenue estimates of more than $ 300 MM of revenue for 2019 , AMAG has the lowest SG&A productivity with a ratio that’s half of the peer average • Caligan believes this poor productivity results from disparate commercial infrastructure for its women’s health and nephrology portfolio and sub - scale product offerings 0x 1x 2x 3x 4x 5x 6x 7x 5-Year GP/SG&A Avg

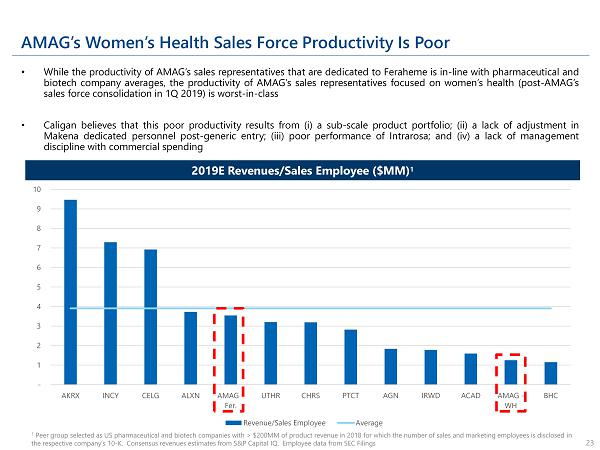

AMAG’s Women’s Health Sales Force Productivity Is Poor • While the productivity of AMAG’s sales representatives that are dedicated to Feraheme is in - line with pharmaceutical and biotech company averages, the productivity of AMAG’s sales representatives focused on women’s health (post - AMAG’s sales force consolidation in 1 Q 2019 ) is worst - in - class • Caligan believes that this poor productivity results from (i) a sub - scale product portfolio ; (ii) a lack of adjustment in Makena dedicated personnel post - generic entry ; (iii) poor performance of Intrarosa ; and (iv) a lack of management discipline with commercial spending 1 Peer group selected as US pharmaceutical and biotech companies with > $200MM of product revenue in 2018 for which the number of sales and marketing employees is disclosed in the respective company’s 10 - K. Consensus revenues estimates from S&P Capital IQ. Employee data from SEC Filings 23 2019E Revenues/Sales Employee ($MM) 1 - 1 2 3 4 5 6 7 8 9 10 AKRX INCY CELG ALXN AMAG - Fer. UTHR CHRS PTCT AGN IRWD ACAD AMAG - WH BHC Revenue/Sales Employee Average

Pipeline & Spending Remain Overhang With Investment Community 24 Analyst Date Jefferies May 7 , 2019 “It is hard to be encouraged by the potential of the pipeline when AMAG narratives have repeatedly failed to pan out . Currently trading at ~ 1 x 2019 revenue, its valuation largely reflects the Street's disappointment/concerns . ” JP Morgan May 8 , 2019 “Heading into a period of increased R&D spend and continued investment in Intrarosa coupled with anticipated launch spend for Vyleesi for which we and the market have significant market questions , we think investors will need to see demonstrated traction in driving revenues from these assets (and/or surprises from the pipeline) for the stock to outperform . ” Piper Jaffray May 22 , 2019 “We don’t doubt that AMAG’s recent delevering was the right move but continue to question if FY 19 's ~ $ 150 M+ y/y negative EBITDA swing to support Intrarosa and Vyleesi is wise . ” – May 22 , 2019 Leerink June 23 , 2019 “We believe that commercial potential of Vylessi remains an outstanding debate given its route of administration via injection and risks around market creation . ” Piper Jaffray June 24 , 2019 “We still think the drug’s profile ( SubQ injection at least 45 minutes prior to anticipated sexual activity, with a 40 % nausea rate and ~ 5 % vomiting rate) makes for a difficult sell . Combining this with a history of disappointing launches ( MuGard , Intrarosa to name two), we think a wait and see approach is warranted here . ” HC Wainwright August 1 , 2019 “AMAG shares have declined consistently since peaking in July 2015 , with shares down 89 % versus the healthcare XLV up 20 % .... The CBR business failed to live up to management’s expectations . Likewise, the company’s acquisition of Intrarosa has been another disappointment . ” Cowen August 7 , 2019 “ As for our broader thesis – and as we have indicated in the past and above – we simply do not believe in the current new commercial portfolio (Intrarosa and Vyleesi) , and with Makena stalled, this leaves Faraheme as the lone growth driver . At this valuation that is simply not enough . Although management is indicating that the company should be EBITDA neutral next year, given our likely lower total sales expectations for the company, we believe the losses will persist into 2021 . And again, given our view of high development risk for AMAG - 423 and ciraparantag, we believe investors should seek better options . ” Source: Analyst reports. Permission to use quotations neither sought nor obtained.

Fundamental Problems At AMAG 25 AMAG’s Board & Management Have Abysmal TSR AMAG Commercial Spending Needs To Be Rationalized Business Development Has Destroyed Shareholder Value AMAG Management Lacks Credibility No Commercial Synergies Across Portfolio Caligan Action Plan

AMAG Management Has Consistently Missed Expectations 26 Product Public Statement 2019E Revenues 1 MuGard “In terms of product potential, there are estimated to be around 400 , 000 patients each year who’re at risk of developing oral mucositis, so it's a fairly significant market and using numbers like a 5 % share of that market opportunity would bring in revenues of excess of $ 20 million . ” – William Heiden, Morgan Stanley Conference, September 9 , 2017 N/M Makena “ So here we are in 2017 with forecasted sales of Makena of approximately $ 425 million at the middle of our range . Now we have a range of cases in our scenario planning for 2020 . Our base case assumptions include the sub - q auto - injector is approved in the fourth quarter of 2017 and generics to the intramuscular product arrive to the market in February 2018 . You can see here that our Makena sales by 2020 in that base or middle case scenario ( $ 250 MM) , which include an authorized generic and some net price decline on the branded Makena business due to generic entries may be lower in 2020 than in 2017 . So that's the base case . ” – William Heiden, 2017 Analyst Day, May 24 , 2017 “So no, that isn't changed . Remember that wasn't guidance . That was sort of directional discussion . ” – Edward Myles, 3 Q 2017 Earnings Call, November 2 , 2017 $145MM Cord Blood Registry “We believe our purchase price represents an attractive valuation for this profitable business at approximately 11 x expected 2015 adjusted EBITDA, including cost synergies . And with some of the revenue synergy opportunities for the future, we like the valuation even more . ” – Frank Thomas, M&A Call, June 29 , 2015 Divested for $170MM Loss in June 2018 (56% of AMAG EV) Intrarosa “ As you move down the income statement to adjusted EBITDA, you'll see that we are planning to invest significantly in Intrarosa in 2017 . As Nik mentioned, we believe this product is a significant revenue opportunity, potentially exceeding $ 500 million per year . ” – Edward Myles, 1 Q 2017 Earnings Call, May 2 , 2017 $20MM Source: S&P Capital IQ transcripts 1 Consensus Expectations

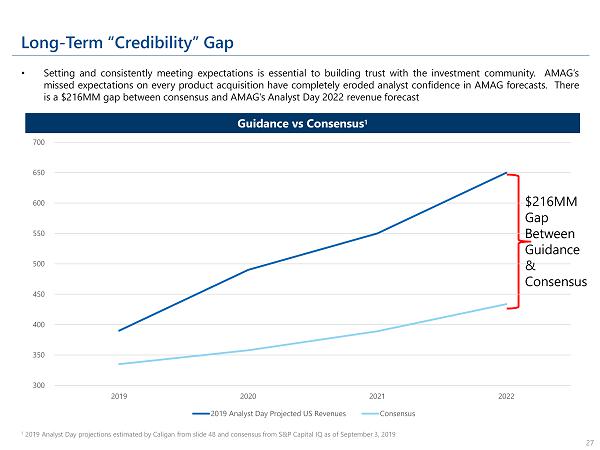

Long - Term “Credibility” Gap • Setting and consistently meeting expectations is essential to building trust with the investment community . AMAG’s missed expectations on every product acquisition have completely eroded analyst confidence in AMAG forecasts . There is a $ 216 MM gap between consensus and AMAG’s Analyst Day 2022 revenue forecast 1 2019 Analyst Day projections estimated by Caligan from slide 48 and consensus from S&P Capital IQ as of September 3, 2019 27 Guidance vs Consensus 1 300 350 400 450 500 550 600 650 700 2019 2020 2021 2022 2019 Analyst Day Projected US Revenues Consensus $216MM Gap Between Guidance & Consensus

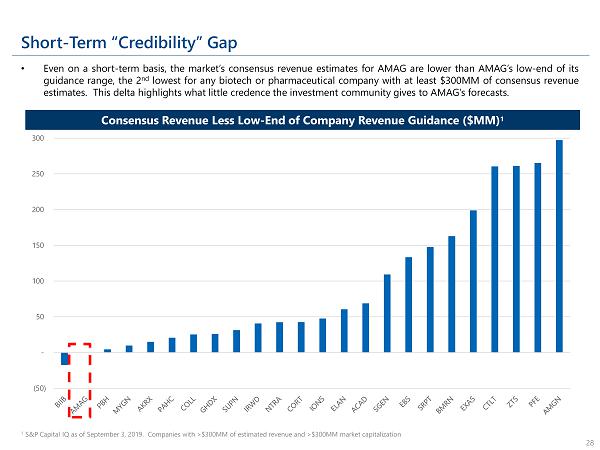

Short - Term “Credibility” Gap • Even on a short - term basis, the market’s consensus revenue estimates for AMAG are lower than AMAG’s low - end of its guidance range, the 2 nd lowest for any biotech or pharmaceutical company with at least $ 300 MM of consensus revenue estimates . This delta highlights what little credence the investment community gives to AMAG’s forecasts . 1 S&P Capital IQ as of September 3, 2019. Companies with >$300MM of estimated revenue and >$300MM market capitalization 28 Consensus Revenue Less Low - End of Company Revenue Guidance ($MM) 1 (50) - 50 100 150 200 250 300

0x 1x 2x 3x 4x 5x 6x 7x 8x PTCT NTRA HARV IRWD CHRS SUPN PCRX CORT TSX:ADVZ AMPH PAHC LCI AKRX OPK AMAG AMAG Trades At Lowest EV/Revenue Multiple Of Biotech and Pharmaceutical Companies With Greater Than $300MM of Revenue 29 1 TEV < $2.5Bn; Estimated Forward Product Revenues > $300MM as of July 31, 2019 the day before Caligan began substantial purcha se s of AMAG shares EV/2019 Revenue 1

Fundamental Problems At AMAG 30 AMAG’s Board & Management Have Abysmal TSR AMAG Commercial Spending Needs To Be Rationalized Business Development Has Destroyed Shareholder Value AMAG Management Lacks Credibility No Commercial Synergies Across Portfolio Caligan Action Plan

AMAG’s Public Statements Confirm No Portfolio Synergies 31 Product Public Statement Makena “And so, large sales force, about 110 reps out there , calling on the OB/GYNs . Very good, sort of stickiness within the supply chain and reimbursement channel . Good connections to the payers . ” – Ed Myles, BAML Leveraged Finance Conference, November 29 , 2016 Intrarosa “As we look at the 150 approximately sales folks bearing down, this is a competitive marketplace . There are other folks out there who will have sales forces . And making sure that we're getting the appropriate share of voice across all of the target physicians is going to be important, not just OB/GYNs but also looking at high - prescribing primary care physicians in some cases, who are also prescribing in this field . ” – Nicholas Grund, 4 Q 2016 Earnings Call, February 14 , 2017 Vyleesi “Frankly, it's a little bit too early to tell, right? So as we go through the final budget planning and go - to - market strategy, a lot of it is around where do women present . As you know, this condition is -- struggles with low awareness at the physician level on diagnosis pathways . So some women with the condition are ending up at OB/GYNs, where we're very very, strong in both maternal health and Intrarosa sales forces, but also some end up in sexual health experts as well as psychiatrists or psychologists . So making sure that we know exactly where patients are presenting is an important part of how we go to market . ” - Nicholas Grund, 3 Q 2018 Earnings Call, November 1 , 2018 Feraheme “ On the Feraheme side, again, I think we're looking for profitable growth on Feraheme . So we took a responsible approach at expanding into additional segments, primarily GIs . We also have an effort in OB/GYN, that's not going away, but this expansion was primarily about getting some broader reach into the GI marketplace . It's a modest increase . We went from roughly 42 to roughly 48 , but we also have a very talented team out there, and strategic account managers, they're almost solely dedicated to hematology, oncology space, doing some contracting with those groups and then also in the hospital setting . ” - Anthony Casciano, 1 Q 2019 Earnings Call, May 7 , 2019 Source: S&P Capital IQ transcripts • Despite consolidation of the Makena and Intrarosa sales forces announced on 4 Q 2018 earnings call, AMAG has publicly communicated that they expect SG&A to increase in 2019 with increased investment in direct - to - consumer campaign spending ; further highlighting the lack of commercial synergies across their portfolio

- 100 200 300 400 500 600 - 50 100 150 200 250 300 350 2015 2016 2017 2018 2019E Revenues ($MM) Cash SG&A ($MM) Compensation & Benefits Professional, Consulting, Other Outside Revenues AMAG’s Disparate Therapeutic Portfolio Provides No Leverage On Existing Commercial Infrastructure • To launch Intrarosa and Vyleesi, AMAG has increased its SG&A by $ 165 MM from 2016 to 2019 during a period when revenues declined ~ $ 100 MM overall . Caligan believes it is unlikely that AMAG shareholders will see any return on this spending 32 AMAG Cash SG&A vs Revenues 1 1 AMAG SEC Filings. 2015 SG&A breakdown between professional and consulting and compensation and benefits is a Caligan estimat e, though the aggregate number is from AMAG’s 2019 10 - K $165MM More SG&A In 2019 vs 2016

Fundamental Problems At AMAG 33 AMAG’s Board & Management Have Abysmal TSR AMAG Commercial Spending Needs To Be Rationalized Business Development Has Destroyed Shareholder Value AMAG Management Lacks Credibility No Commercial Synergies Across Portfolio Caligan Action Plan

34 Action Rationale Significant Board Refreshment • Given AMAG’s absolute and relative underperformance, AMAG would benefit from the fresh perspective of a new set of independent directors that includes both (i) directors with significant pharmaceutical expertise and public company experience and (ii) direct representation for AMAG shareholders • Caligan is proposing 4 new directors, 3 independent of Caligan Comprehensive Review of Strategic Alternatives • Post board refreshment, AMAG should conduct a comprehensive review of strategic alternatives of its asset portfolio • The nephrology, women’s health, and hematology assets cannot leverage a single commercial infrastructure (or require additional direct - to - consumer marketing spending that questions the need for a sales force) questioning the logic of having multiple subscale therapeutic focuses Immediate Rationalization of Commercial Footprint to Achieve Positive EBITDA • Given the spending and pipeline overhang with the investment community, the quickest way to re - build trust is to immediately get the company to profitability • Positive steps include exploring non - traditional ways and partnerships to monetize Intrarosa and Vyleesi and establishing risk - sharing development partnerships on ciraparantag and AMAG - 423 that alleviate the R&D burden on AMAG Monetize Feraheme International Rights • Given the hypophosphatemia benefits vs . Injectafer that the non - inferiority study demonstrated, this would seem like an opportune time to explore a new partnership (Vifor/Daiichi provides a template) • A low - risk business development initiative could provide substantial upside to AMAG shareholders Caligan Action Plan

AMAG Directors Have Purchased an Immaterial Number of Shares 1 35 • AMAG’s directors own an immaterial amount of shares (< 0 . 50 % ) and, over the last 7 years, only one director has purchased shares worth ~ $ 100 k . Caligan owns over 10 % of AMAG’s shares . • As AMAG shareholders have lost ~ 50 % of their share value under current leadership, annual director compensation (retainer, RSUs, and options) has increased at a 28 % CAGR 1 SEC Form 3 & 4 Filings as of May 20, 2019 for Independent Directors. John Fallon purchased 3,230 shares on November 10, 2015 f or $31.20 per share. 2 As disclosed in AMAG annual proxy statements Director Ownership Of AMAG (% O/S) 1 Annual Director Compensation 2 0% 2% 4% 6% 8% 10% 12% Director Shares Purchased Director Shares Owned Caligan - 50,000 100,000 150,000 200,000 250,000 2012 2013 2014 2015 2016 2017 2018 Cash RSU Options 28% CAGR

AMAG Board Should Explore Whether Separating Assets Will Create Value 36 1 Consensus estimates 2 Caligan estimates 3 1Q2019 Earnings Call 4 2Q2018 Earnings Call; pre - sales force consolidation Nephrology/Hematology Women’s Health Feraheme Pipeline 2019E Revenues 1 $170MM N/A 2019E EBITDA 2 $100MM $(50)MM Worldwide Rights Yes Yes Sales Reps 3 48 N/A Sales Points Hematologists Oncologists GPOs Gastroenterologists Hospitals Hematologists Hospitals Potential Indications Patient Blood Management Heart Failure Iron Deficiency Anticoagulant reversal Makena Intrarosa / Vyleesi Pipeline 2019E Revenues 1 $145MM $20MM N/A 2019E EBITDA 2 $50MM $(130)MM $(50)MM Worldwide Rights Yes No Yes Sales Reps 4 105 137 N/A Sales Points OB/GYNs OB/GYNs SH Experts Psychiatrists Psychologists OB/GYNs Hospitals Potential Indications N/A Intrarosa for HSDD Severe preeclampsia Separating AMAG assets could create shareholder value

SG&A Should Be Reduced Immediately 37 1 Consensus revenue estimates. SG&A is last quarter annualized. Best - In - Class is Amphastar Pharmaceuticals. Peer Average is US public pharmaceutical and biotech companies that are expected to generate between $300MM and $600MM of product revenue in 2020 2 Excluding CBR. SG&A from AMAG 2016 10 - K SG&A Run - Rate (% of 2020E Revenues) 1 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% AMAG (Current) AMAG (2016) Peer Average "Best-In-Class" • In 2016 , when AMAG’s only commercial products were Feraheme and Makena, AMAG spent $ 128 MM on SG&A ( 30 % of revenue) 2 • In 2019 , AMAG is on pace to spend more than 85 % of revenues on SG&A : • Peer Average = 34 . 2 % • Best - In - Class = 12 . 8 % • Applying average SG&A % of sales generates $ 172 MM of cost savings • Applying best - in - class SG&A % of sales generates $ 248 MM of cost savings • AMAG is spending $ 165 MM in SG&A to generate an incremental $ 20 MM in revenue from Intrarosa and Vylessi . This needs to be stopped immediately

AMAG Needs An International Distribution Partner For Feraheme 38 1 S&P Capital IQ For Consensus Estimates 2 26% global market share on $413MM of ex - US Ferinject sales equals $119MM of ex - US Feraheme revenue. At a 33.33% royalty rate, AMAG would receive $39.7MM annually. At a 3x – 7x capitalization rate, AMAG’s market capitalization would increase by $119MM – $278MM, 33 - 77% higher than its closing market capit alization of $362MM on September 3, 2019. Ferinject vs. Feraheme ex - US Revenues 1 - 50 100 150 200 250 300 350 400 450 500 Ferinject ROW 2019E Revenues Feraheme ROW 2019E Revenues • Ferinject (the ex - US brand name for Injectafer ) consensus estimates are for over $ 450 MM of international revenue in 2019 • Ferinject is launching in Japan this year . On its 1 H 2019 earnings call, Vifor estimated ~ 5 million patients in Japan are suffering from iron deficiency anemia with more than 50 % of them not being treated at all and less than 10 % are currently being treated with intravenous iron • Caligan (and Vifor ) believes there is a huge unmet medical need in treating iron deficiency and iron deficiency anemia worldwide . Vifor has observed 25 % + volume growth in underpenetrated therapy areas, such as cardiology and patient blood management in Europe and oncology and gastroenterology in the U . S . • Regent (a subsidiary of Daiichi) pays Vifor a 33 . 33 % revenue royalty on its sales of Venofer and Injectafer in the US and bears all of the costs of marketing • If Feraheme achieved similar market share penetration in the rest of the world as it did in the US, Feraheme could achieve over $ 100 MM of international revenues . At a 33 % royalty rate and a 5 x capitalization multiple, getting an international distribution partner for Feraheme could increase AMAG’s share price by 33 % - 77 % 2

Caligan’s Research on AMAG Pharmaceuticals • Caligan has conducted exhaustive research over the past 18 months to better understand AMAG’s products and strategy, including working with respected former pharmaceutical executives to diligence each of AMAG’s products • Caligan has worked with leading nephrologists, chemists, and academics to understand the potential of Feraheme in the US and internationally and its competitive advantages versus other IV irons • Caligan has spoken to OB/GYNs, lead investigators, and consultants to evaluate AMAG’s women’s health assets and its current commercial strategy • Our conclusion from this analysis is that AMAG’s assets are valuable/durable and that the business possesses several fundamental upside drivers but that its future will be increasingly difficult if AMAG continues with its existing strategy • Caligan believes that AMAG needs ( i ) board refreshment to reestablish credibility with the investment community and (ii) to implement some low - risk, high reward value creation initiatives 39

About Caligan Partners 40 Caligan Partners, LP was founded by David Johnson and Sam Merksamer in 2017 to pursue a deep value - oriented investment strategy Caligan’s principals have extensive experience working closely with management teams on strategic and operating initiatives, and working through industry transitions to create value Caligan matches its investment horizon to the opportunity, with a singular focus on creating value for its investors and shareholders

Contacts & Additional Information 41 Investors Edward McCarthy/ Geoffrey Weinberg D . F . King & Co . , Inc . + 1 ( 212 ) 269 - 5550 AMAG@dfking . com Press Robert Laman Caligan Partners + 1 ( 646 ) 859 - 8205 rl@caliganpartners . com F or Additional Information IR@caliganpartners . com LEGEND Caligan, Caligan CV II LP, David Johnson, Samuel Merksamer, Paul Fonteyne, Lisa Gersh , and Kenneth Shea (collectively, the “Participants”) intend to file with the SEC a definitive consent statement and accompanying form of consent card to be used in connection with the solicitation of consents from the stockholders of AMAG Pharmaceuticals, Inc . (the “Company”) . All stockholders of the Company are advised to read the definitive consent statement and other documents related to the solicitation of consents by the Participants when they become available, as they will contain important information, including additional information related to the Participants . The definitive consent statement and an accompanying consent card will be furnished to some or all of the Company’s stockholders and will be, along with other relevant documents, available at no charge on the SEC website at http : //www . sec . gov/ and at Caligan’s website www . saveamag . com and from the Participants’ consent solicitor, D . F . King & Co . , Inc . by requesting a copy via email to AMAG@dfking . com . Information about the Participants and a description of their direct or indirect interests by security holdings is contained in the Schedule 14 A filed by Caligan with the SEC on September 4 , 2019 . This document is available free of charge from the sources indicated above .

EXHIBIT D

FORM OF NOMINATION AGREEMENT

| 1. | This Nomination Agreement (the “Agreement”) is by and between Caligan Partners LP (“Caligan,”

“we” or “us”) and [ ] (“you”). |

| 2. | You agree that you are willing, should we so elect, to become a member of a slate of nominees (the

“Slate”) of Caligan or an affiliate thereof (the “Nominating Party”), which nominees shall be nominated

for election as directors of AMAG Pharmaceuticals, Inc. (the “Corporation”) in connection with a consent solicitation

(the “Consent Solicitation”) to be conducted by Caligan and certain other parties, or appointment or election by other

means. You further agree to serve as a director of the Corporation if so elected or appointed. Caligan agrees to pay the costs

of the Consent Solicitation and agrees to reimburse you for any documented and reasonable out-of-pocket expenses you incur in connection

with the Consent Solicitation that are approved in writing in advance by Caligan, including reasonable expenses for travel requested

by Caligan in connection therewith. |

| 3. | Caligan agrees on behalf of the Nominating Party that, so long as you actually serve on the Slate,

Caligan will defend, indemnify and hold you harmless from and against any direct, out-of-pocket losses, claims, damages, penalties,

judgments, awards, settlements, liabilities, costs, expenses and disbursements (including, without limitation, reasonable, reasonably

documented attorneys’ fees and related costs, expenses and disbursements) incurred by you in the event that you become a

party, or are threatened to be made a party, to any civil, criminal, administrative or arbitrative action, suit or proceeding brought

by a third party, and any appeal thereof, (i) relating to your role as a nominee for director of the Corporation on the Slate,

or (ii) otherwise directly arising from or in connection with or relating to the Consent Solicitation in connection with your role

as a nominee for director of the Corporation on the Slate. Your right of indemnification hereunder shall continue after the Consent

Solicitation has taken place but only for events that occurred prior to the conclusion of the Consent Solicitation and subsequent

to the date hereof. Anything to the contrary herein notwithstanding, Caligan is not indemnifying you for any action taken by you

or on your behalf that occurs prior to the date hereof or subsequent to the conclusion of the Consent Solicitation or such earlier

time as you are no longer a nominee on the Slate or for any actions taken by you as a director of the Corporation, if you are elected.

Nothing herein shall be construed to provide you with indemnification (i) if you are found to have engaged in a violation of any

provision of state or federal law in connection with the Consent Solicitation, unless you demonstrate that your action was taken

in good faith and in a manner you reasonably believed to be in or not opposed to the best interests of electing the Slate; (ii)

if you acted in a manner that constitutes gross negligence or willful misconduct; or (iii) if you provided false or misleading

information, or omitted material information, in the Questionnaires (as defined below) or otherwise in connection with the Consent

Solicitation. You shall promptly notify Caligan in writing in the event of any third-party claims actually made against you or

known by you to be threatened if you intend to seek indemnification hereunder in respect of such claims. In addition, upon your |

delivery of notice with respect to

any such claim, Caligan shall promptly assume control of the defense of such claim with counsel chosen by Caligan. From

and after such determination by Caligan to assume the defense of such claim, Caligan will not be liable to you under this Agreement

for any expenses subsequently incurred by you in connection with the defense thereof other than reasonable costs of investigation

and preparation therefor (including, without limitation, appearing as a witness and reasonable fees and expenses of legal counsel

in connection therewith). Caligan shall not be responsible for any settlement of any claim against you covered by this indemnity

without its prior written consent. However, Caligan may not enter into any settlement of any such claim without your consent unless

such settlement includes (i) no admission of liability or guilt by you, and (ii) an unconditional release of you from any and all

liability or obligation in respect of such claim. If you are required to enforce the obligations of Caligan in this agreement in

a court of competent jurisdiction, or to recover damages for breach of this agreement, Caligan will pay on your behalf, in advance,

any and all reasonably documented out-of-pocket expenses (including, without limitation, reasonable, reasonably documented attorneys’

fees and related costs, expenses and disbursements) actually and reasonably incurred by you in such action, provided,

however, that all amounts advanced in respect of such expenses shall be promptly repaid to Caligan by you to the extent it shall

ultimately be determined in a final judgment by a court of competent jurisdiction that you are not entitled to be indemnified for

or advanced such expenses.

| 4. | You understand that it may be difficult, if not impossible, to replace a nominee who, such as yourself,

has agreed to serve on the Slate and, if elected or appointed, as a director of the Corporation if such nominee later changes his

mind and determines not to serve on the Slate or, if elected or appointed, as a director of the Corporation. Accordingly, Caligan

is relying upon your agreement to serve on the Slate and, if elected, as a director of the Corporation. In that regard, you will

be supplied with a questionnaire (the “Caligan Questionnaire”) in which you will provide Caligan with information necessary

for the Nominating Party to make appropriate disclosure to the Corporation and to use in creating the consent solicitation materials

to be sent to stockholders of the Corporation and filed with the Securities and Exchange Commission in connection with the Consent

Solicitation, and may in the future be supplied with a questionnaire from the Corporation for similar purposes (together with the

Caligan Questionnaire, the “Questionnaires”). |

| 5. | You agree that (i) upon request you will promptly complete, sign and return the Questionnaires,

(ii) your responses in the Questionnaires will be true, complete and correct in all respects, and (iii) you will provide any additional

information related to the Consent Solicitation as may be reasonably requested by Caligan, with information including, but not

limited to, any other matters as is required or customary to be disclosed regarding a nominee and his or her nomination to the

board of directors under the Corporation’s Certificate of Incorporation or bylaws or pursuant to the rules and regulations

contained in the Securities Exchange Act of 1934, as amended, or the rules and regulations promulgated thereunder. You commit that

such information will be true and correct in all material respects and will not omit any material information necessary in order

to make the information provided not misleading and that you will promptly notify Caligan of any material changes or updates to

any information provided by you to Caligan. In addition, |

you agree that you will execute and

return a separate instrument confirming that you consent to being nominated for election as a director of the Corporation and,

if elected or otherwise appointed, consent to serving as a director of the Corporation. Upon being notified that you have been

chosen, we and the Nominating Party may forward your consent and completed Questionnaires (or summaries thereof), to the Corporation,

and we and the Nominating Party may at any time, in our and their discretion, disclose the information contained therein, as well

as the existence and contents of this Agreement and any information this Agreement requires you to provide. Furthermore, you understand

that we may elect, at our expense, to conduct a background and reference check on you and you agree to complete and execute any

necessary authorization forms or other documents required in connection therewith.