Additional Proxy Soliciting Materials (definitive) (defa14a)

February 10 2016 - 9:18AM

Edgar (US Regulatory)

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of the Securities

Exchange Act of 1934 (Amendment No.

)

| Filed by the Registrant [X] |

| Filed by a Party other than the Registrant [ ] |

| |

| Check the appropriate box: |

| |

| [ ] |

|

Preliminary Proxy Statement |

| [ ] |

|

Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| [ ] |

|

Definitive Proxy Statement |

| [X] |

|

Definitive Additional Materials |

| [ ] |

|

Soliciting Material Pursuant to §240.14a-12 |

| |

DEERE

& COMPANY |

|

| |

(Name of Registrant as Specified In Its Charter) |

|

| |

|

|

| |

|

|

| |

(Name of Person(s) Filing Proxy Statement, if other than the Registrant) |

|

| Payment of Filing Fee (Check the appropriate box): |

| [X] |

|

No fee required. |

| [ ] |

|

Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. |

| |

|

|

|

|

| |

|

1) |

|

Title of each class of securities to which transaction applies: |

| |

|

|

|

|

| |

|

2) |

|

Aggregate number of securities to which transaction applies: |

| |

|

|

|

|

| |

|

3) |

|

Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): |

| |

|

|

|

|

| |

|

4) |

|

Proposed maximum aggregate value of transaction: |

| |

|

|

|

|

| |

|

5) |

|

Total fee paid: |

| |

|

|

|

|

| [ ] |

|

Fee paid previously with preliminary materials. |

| |

|

|

| [ ] |

|

Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. |

| |

|

|

|

|

| |

|

1) |

|

Amount Previously Paid: |

| |

|

|

|

|

| |

|

2) |

|

Form, Schedule or Registration Statement No.: |

| |

|

|

|

|

| |

|

3) |

|

Filing Party: |

| |

|

|

|

|

| |

|

4) |

|

Date Filed: |

| |

|

|

|

|

Dear Stockholders:

Within the past few weeks you should

have received the Proxy Statement and related materials for the Deere & Company Annual Meeting of Stockholders to be held on

Wednesday, February 24, 2016. In the Proxy Statement, Deere’s Board of Directors recommends that you vote “FOR”

Item 2, the advisory resolution to approve Deere’s executive compensation (“say-on-pay”), and “AGAINST”

Item 4a, the stockholder proposal requesting adoption of a “proxy access” bylaw amendment.

We have carefully designed our executive

compensation programs and corporate governance structure to drive superior business results and maintain strong alignment with

and accountability to our stockholders. Accordingly, our stockholders have in the past overwhelmingly supported our Board’s

recommendations on annual meeting matters, for example by providing our say-on-pay resolution with at least 93% support each year

since Deere first adopted say-on-pay at our 2011 annual meeting.

Given this history, we were surprised by ISS’s recommendation that stockholders vote against our say-on-pay

proposal this year, particularly after we learned that Glass Lewis has recommended that stockholders vote “for” this

same proposal. We were also disappointed that both ISS and Glass Lewis recommended

votes in favor of the proxy access stockholder proposal. We fundamentally disagree with ISS’s conclusions (and those of Glass

Lewis with respect to proxy access), and want to take this opportunity to share the reasons we believe a vote “FOR”

the Company’s say-on-pay proposal and “AGAINST” the proxy access stockholder proposal are in the best interests

of our stockholders.

Capitalized terms used in this letter

have the same meanings as in the Proxy Statement.

Say-on-Pay:

We are firm in our belief that Deere’s

compensation programs drive the right behaviors for Deere employees at all levels, which in turn benefits our stockholders by driving

solid results throughout the business cycle. Even though these results may not always align with TSR in the short run, we believe

our stockholders’ interests are best served over time by a balanced compensation program that takes a long-term, holistic

view of the Company’s business strategy and recognizes the cyclicality of the industries in which we operate.

As illustrated further by the attached

materials:

| · | Realizable CEO compensation over the past

three years was equal to just 63% of Summary Compensation Table compensation over the same period, demonstrating that our executive

compensation program as a whole is aligned with performance and is sensitive to financial and TSR results. |

| · | The metrics used in Deere’s cash

incentive plans (STI and MTI) are tied directly to our business strategy and have been integral in driving the success of the Company

since 2004. |

| · | Since the implementation of the STI and

MTI plans, Deere’s asset efficiency performance, as measured by OROA and return on invested capital, has consistently exceeded

the 75th percentile relative to our peers. |

| · | This focus on asset efficiency has enabled

Deere’s businesses to become far more durable in the face of the cyclicality of the industries in which we operate. For example,

in fiscal 2015, Deere achieved net income in excess of $1.9 billion and positive SVA of $774 million despite a decline in worldwide

net sales and revenues of 20%. In many previous down-cycles, we experienced negative net income, SVA, or both. |

| · | To further align pay with performance,

the Compensation Committee has raised the goals for the STI program effective with our current 2016 fiscal year and added a relative

TSR modifier for executive officers under the MTI program effective with the 2015-2017 performance period. These changes illustrate

the Compensation Committee’s continuing commitment to aligning pay with performance. |

Proxy Access:

| · | In discussions with our stockholders, we

have learned that their views on proxy access vary widely and in many cases are not aligned with the stockholder proposal in the

Proxy Statement. |

| · | Our existing corporate governance practices

give stockholders meaningful input into the director nomination process. Stockholder nominees are evaluated in the same manner

as all other nominees. In addition, stockholders are invited to communicate directly both with the Company and the Board of Directors

on director nominations and other matters. |

| · | We believe that the Corporate Governance

Committee and Board of Directors are in the best position to review and recommend director nominees to ensure that the highest

quality candidates, whose experiences and skillsets best align with overall Company strategy and needs, are nominated for election. |

| · | We are deeply troubled by the risk that

proxy access could allow stockholders with special interests to use the proxy process to promote positions that are not in the

best interests of all stockholders and would make it easier for directors whose primary focus is to promote those narrow positions

to get elected. |

| · | Stockholder-nominated directors, particularly

those with special interests, could cause the Board to become dysfunctional, reducing its ability to oversee the Company’s

strategy and operations. |

| · | It is also our view that implementation

of proxy access would create a greater risk of proxy contests, which could result in significant expense to the Company and distraction

to Company management and directors. |

we

encourage you to read the Proxy Statement for more information regarding the reasons for the Board’s recommendationS ON THESe

PROPOSALS, and urge you to vote “FOR” Item 2, THE Advisory Vote on Executive Compensation, AND “AGAINST”

ITEM 4a, the proxy access stockholder proposal.

| $4,431 $4,431 $17,623 $17,623 $8,778 $2,214 $18,459 $6,963 $49,291 $31,231 10/31/12; $78.53 10/31/15; $77.40 $77 $78 $79 0 10,000 20,000 30,000 40,000 50,000 60,000 Summary Compensation Table Total Realizable Pay Adj. Close Price w/ Dividend Impact Total CEO Pay ($ thousands) Deere & Company 3 - Year CEO Total Pay vs. 3 - Year Total Shareholder Return FY2013 - FY2015 Salary STI/MTI Option Awards Stock Awards Adjusted Close Price Pay for Performance a lignment February 2016 1 • Relative performance results, and the sensitivity of our compensation programs to financial and shareholder return performance, led to realizable CEO pay equal to only 63 % of summary compensation table pay over the past 3 fiscal years, exclusive of retirement and non - direct remuneration • The graph below shows the relative alignment between CEO total r ealizable p ay and our TSR over this period Source: Pearl Meyer, LLC

| STI OROA p erformance m etric Directly tied to the business strategy S ee Proxy Statement pages 30 - 33 February 2016 2 • Adopted as primary STI metric in 2004 with target goal set at peer median • Focuses on making Deere’s asset - intensive business leaner • Enables more rapid response to changing business conditions • Incents employees to optimize asset efficiency throughout the business cycle • Result: OROA has risen dramatically and been sustained at above - upper quartile levels , leading to high payouts even in challenging market conditions OROA Deere vs. Peers 1997 – 2015* *Peer group data for 2015 is not yet available OROA metric adoption

| -1,600 -1,200 -800 -400 0 400 800 1,200 1,600 2,000 2,400 2,800 3,200 3,600 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 ($ millions) Adoption of MTI program MTI SVA performance metric Directly tied to the business strategy s ee Proxy Statement pages 34 - 36 February 2016 3 • The adoption of the MTI program in 2003 has been a consistent driver of SVA performance • P romotes long - term, sustainable growth accomplished through a combination of revenue growth and high returns on invested capital • Encourages teamwork across all units of our business for multi - year periods • Reinforces a culture of ownership and alignment with stockholders, critical to Deere’s long - term success • Three - year performance periods emphasize and reward consistent, sustained operating performance Record 2013 SVA results of $3.4 billion contributed to maximum MTI payouts for the last three performance periods SVA 1993 – 2015

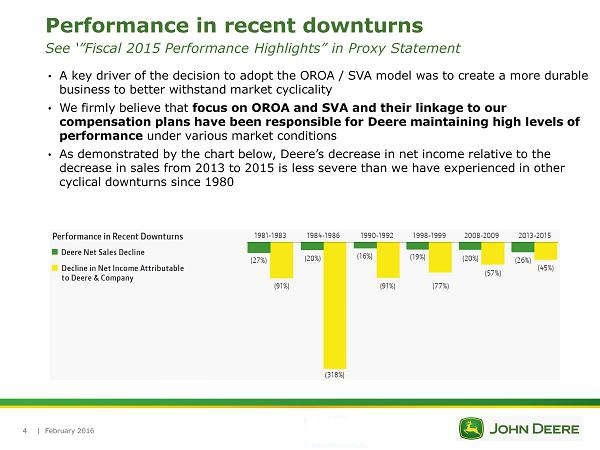

| Performance in recent d ownturns S ee ‘”Fiscal 2015 Performance Highlights” in Proxy Statement February 2016 4 • A key driver of the decision to adopt the OROA / SVA model was to create a more durable business to better withstand market cyclicality • We firmly believe that focus on OROA and SVA and their linkage to our compensation plans have been responsible for Deere maintaining high levels of performance under various market conditions • As demonstrated by the chart below, Deere’s decrease in net income relative to the decrease in sales from 2013 to 2015 is less severe than we have experienced in other cyclical downturns since 1980

| OROA goals increase for STI in 2016 S ee Proxy Statement pages 31 - 32 February 2016 5 • OROA performance resulted in high STI payouts in recent fiscal years • Peer group OROA performance has remained essentially unchanged • Deere has proven its ability to deliver OROA performance under varying business conditions • The Committee approved significant increases to OROA goals starting in 2016 • The degree of increase balances short - term performance with longer - term growth goals; if set too high, OROA goals can discourage investment and impede long - term growth by over - incentivizing short - term results

| SVA goals increase for MTI for 2016 and 2017 See Proxy Statement page 34 • SVA goals are increasing significantly for the performance periods ending in 2016 and 2017 to ensure that we keep setting goals aligned with shareholder expectations • Strong agricultural equipment sales in recent years have driven an increase in our calculation of mid - volume sales February 2016 6 * TSR modifier for MTI payout applies starting in fiscal 2017 – see slide 7 - 2,000 4,000 6,000 8,000 10,000 2013 2014 2015 2016 2017* $ millions SVA Goals for Maximum Payout +31% +25% Three - year performance periods ending

| • For the 2015 - 2017 performance period, the Committee approved the addition of a relative TSR modifier to MTI payouts • The TSR modifier is triggered if Deere’s relative TSR is below median of the S&P Industrials, further aligning compensation with stockholder interests • For TSR at or below the 25th percentile, the final MTI payout will be reduced 25 % • For TSR between the 25th and 50th percentiles, the final MTI payout will be reduced between 0 - 25% on a linear basis. TSR m odifier added to MTI S ee Proxy Statement page 35 February 2016 7

Deere (NYSE:DE)

Historical Stock Chart

From Mar 2024 to Apr 2024

Deere (NYSE:DE)

Historical Stock Chart

From Apr 2023 to Apr 2024