VAALCO Energy, Inc.

Third Quarter 2015 Earnings Results Conference Call

TRANSCRIPT

Moderator:

Ladies and Gentlemen, good morning. Thank you for standing by and welcome to the VAALCO Energy Third Quarter 2015 Earnings Report. At this time, all lines are in a listen-only mode. Later there will be an opportunity for your questions and instructions will be given at that time.

If you should require any assistance today, please press * followed by the 0 and an AT&T operator will assist you. As a reminder, this conference is being recorded. I’d now like to turn the conference over to our host, Investor Relations Coordinator, Mr. Al Petrie. Please go ahead.

Al Petrie, VAALCO Investor Relation Coordinator:

Thanks, Tom, and on behalf of the management team, I welcome all of you to today’s conference call to review VAALCO’s Third Quarter 2015 Operating and Financial performance.

After I cover the Forward Looking Statements narrative, Steve Guidry, VAALCO’s Chairman and CEO, will review key highlights of the third quarter. Following Steve’s comments, Greg Hullinger will provide a more in-depth financial review and an update to our 2015 guidance. Cary Bounds, our COO will then review operational results in more detail and our plans for the balance of 2015. Steve will then return for some closing comments before we take your questions.

On November 6th, the Company issued a statement in response to Group 42 and Bradley Radoff’s filing of consent solicitation materials. VAALCO will respond to the matters discussed in the filing and the Board will be providing its recommendations to our shareholders in due course. We appreciate your limiting any questions in today’s call to those regarding third quarter financial and operational matters and not regarding the consent solicitation. Please note that our earnings call today does not constitute the solicitation of consents or proxies.

During our question session, we ask you to limit your questions to one and a follow up.

With that, let me proceed with our Forward Looking Statement guidance.

During the course of this conference call, the Company will be making forward-looking statements. We caution you that any statement that is not a statement of historical fact is a forward-looking statement. Forward-looking statements are those concerning VAALCO's plans, expectations, future drilling and completion activities, expected capital expenditures, prospect evaluations, negotiations with governments and third parties, reserve growth and other operations.

Statements made during this conference call that address activities, events or developments that VAALCO expects, believes or anticipates will or may occur in the future are forward-looking statements. These statements are based on assumptions made by VAALCO based on its experience, perception of historical trends, current conditions, expected future developments and other factors it believes are appropriate in the circumstances. Such statements are subject to a number of assumptions, risks and uncertainties, many of which are beyond VAALCO's control.

Investors are cautioned that forward-looking statements are not guarantees of future performance and those actual results or developments may differ materially from those projected in the forward-looking statements. VAALCO disclaims any intention or obligation to update or revise any forward-looking statements, whether as a result of new information, future events, or otherwise. Accordingly, you should not place undue reliance on forward-looking statements.

These and other risks are described in yesterday’s press release and in the reports we file with the Securities and Exchange Commission, notably the 2014 Form 10-K filed with the Commission on March 16th, 2015, and Form 10-Q’s filed with the Commission on May 7th and August 6th, and yesterday afternoon.

Please note that this conference call is being recorded. Let me turn the call over to Steve.

Steve Guidry, VAALCO Chief Financial Officer:

Thank you Al, good morning everyone, and welcome to our third quarter 2015 earnings conference call.

Before I get into the quarterly results, let me begin by welcoming Don McCormack to our executive team as our CFO. Don has an extensive financial background in the energy industry having served in key financial leadership positions with other publicly traded E&P companies. He has significant international and domestic experience in accounting, treasury, M&A and corporate finance. His overall financial and public market experience will serve VAALCO well in the future. Let me also thank Greg Hullinger for his financial leadership here at VAALCO over the past 7 years. Greg was actively involved in all facets of our business and was a trusted financial advisor to senior management and the Board and was our primary investor relations contact. We wish him the best in his upcoming retirement.

On the call this morning we will reference an updated supplemental information slide deck, located on our website, which builds on the improvements that we made last quarter of enhancing the information we provide to our shareholders.

As you already know, 2015 has been a volatile year for the energy industry with continued weakness and uncertainty in commodity prices. Because of this volatility, our strategy is directed toward lowering costs, investing in projects that yield good economic returns in the current price environment, while remaining focused on shareholder value.

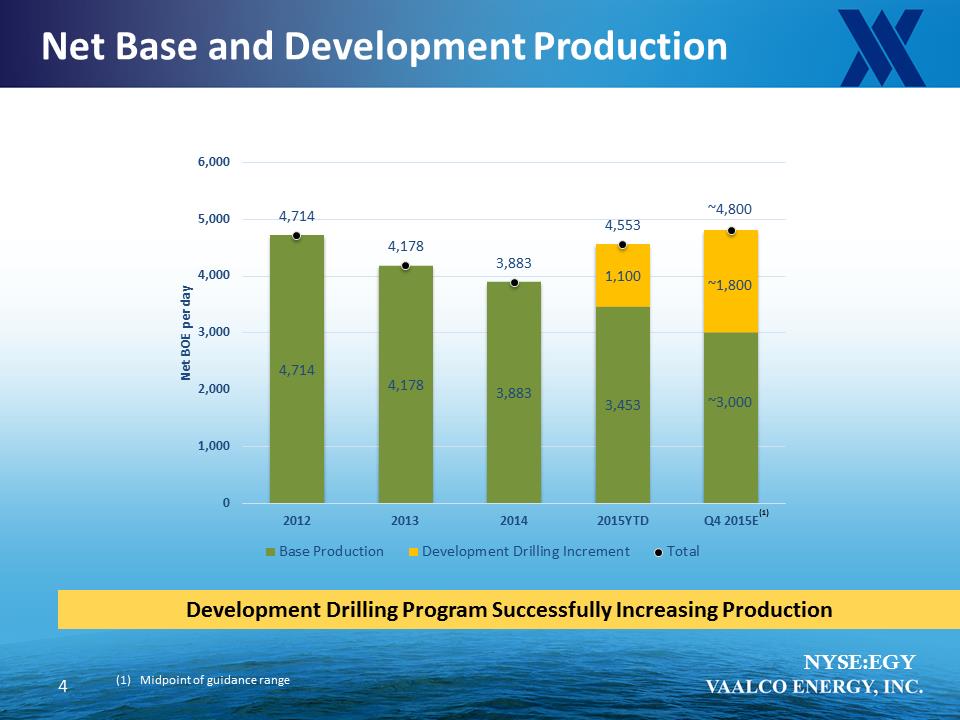

Our development drilling success in our multi-well, offshore Gabon program resulted in continued production growth in the third quarter. Contributing to that increase in volumes was strong production from our Southeast Etame 2-H well completed in July and the incremental production from the North Tchibala 1-H well completed in mid-September. Combined with the two successful wells drilled earlier this year on the Etame platform, our 2015 drilling program has added about 1,100 net barrels of oil per day to our year to date volumes.

This success allowed us to average production of about 4,800 BOE per day for the third quarter, slightly above the upper end of our guidance range. You can see the growth in production that this program has contributed to VAALCO on slide 4 of the supplemental information. Notice that the impact to the fourth quarter volumes from our development program will be about net 1,800 BOPD, this accounts for over 33% of our fourth quarter 2015 volumes.

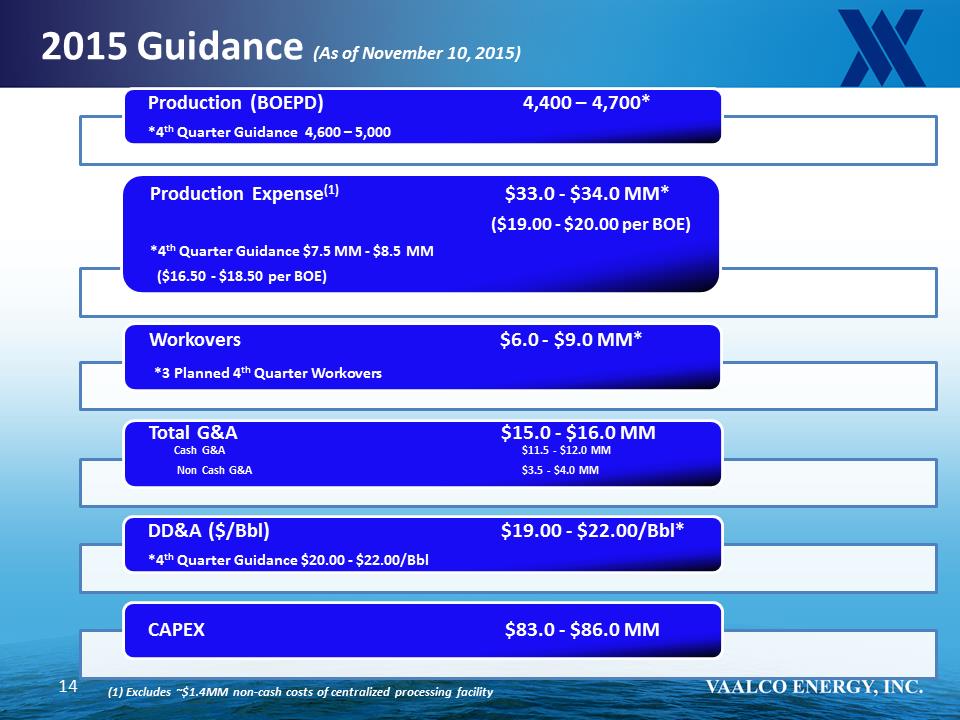

Based on these successes and the anticipated volumes from our North Tchibala 2-H well currently drilling and some limited late-year production benefit from the planned Avouma platform workovers, we expect our fourth quarter production to be in the range of 4,600 to 5,000 BOE per day. Taking all of this into account, we are raising the range of our full year 2015 production guidance to be between 4,400 to 4,700 BOE per day. Cary will discuss the results of our drilling program and plans for the rest of the year in more detail shortly. Because

of the re-sequencing of the North Tchibala 2-H well and the workovers, along with increased costs associated with the partial well redrills, we have revised our full-year 2015 capital program to $83 to $86 million.

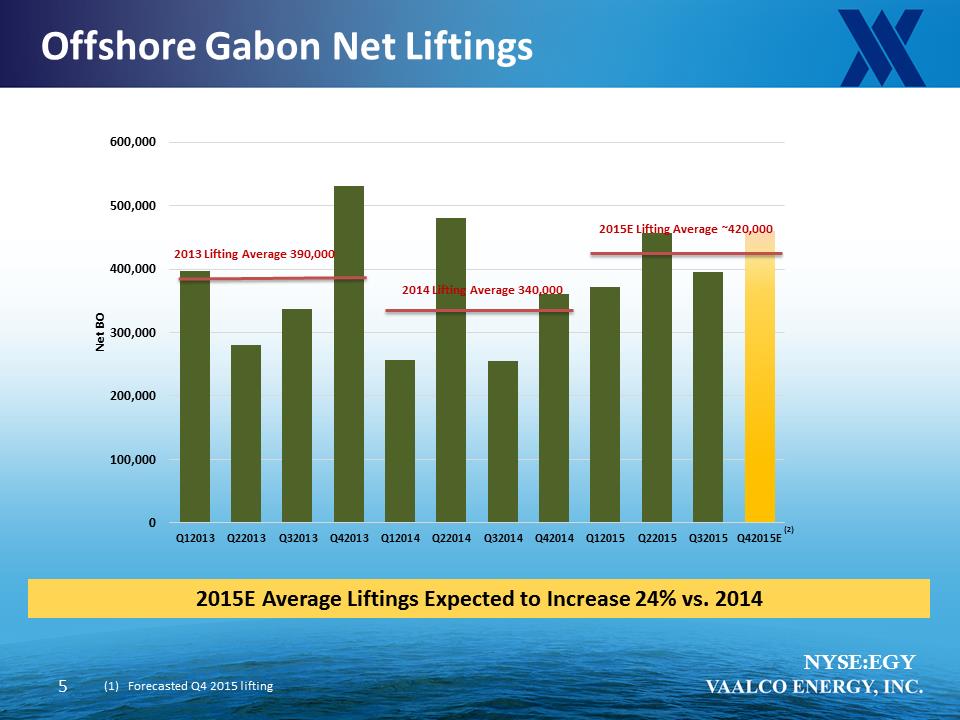

In the third quarter of 2015, we were not able to fully benefit financially from higher production, largely due to a 26% decline in oil price realizations and lower liftings compared to the second quarter of 2015. If you look at slide 5 of the supplemental information, you will see that liftings fluctuate from quarter to quarter due to a variety of factors including the timing and volume of each offloading. Our net average monthly liftings totaled 390,000 barrels in 2013, then declined to 340,000 barrels in 2014, and are averaging about 420,000 barrels for the first nine months of 2015. We are anticipating a further increase in fourth quarter liftings, evidenced by the strong October lifting that we recently disclosed on our web site. Hopefully prices will be higher as well, but we can’t control pricing and we must continue to focus on what we can control, which are the costs associated with this production.

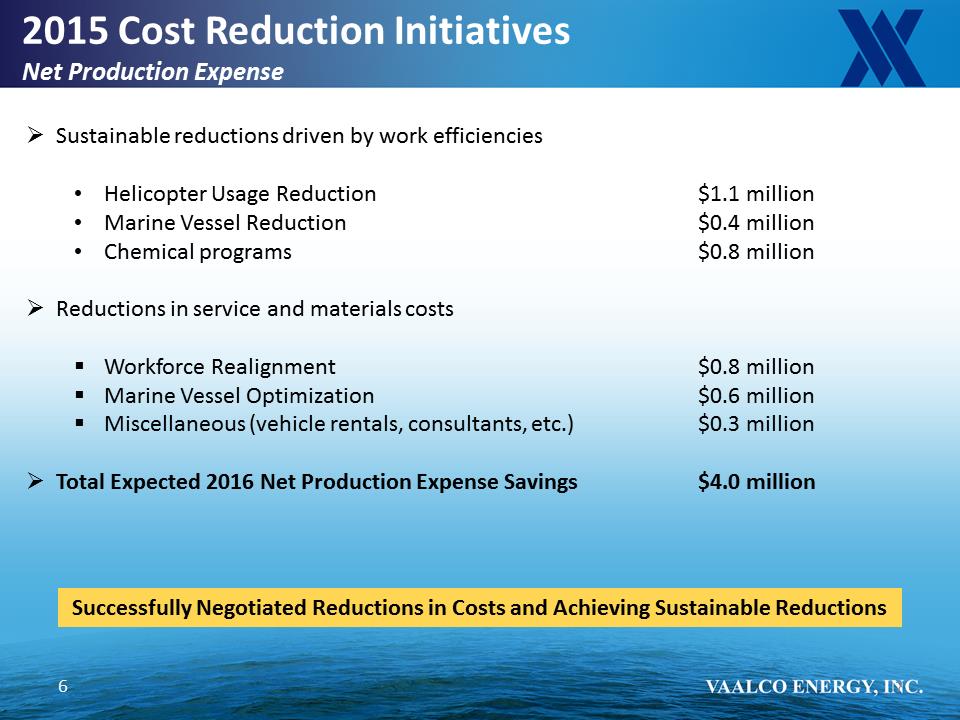

VAALCO began reducing costs even before the decline in oil prices as we began taking steps in 2014 to reduce executive cash compensation. In 2015, we have reorganized and reduced our corporate staff and have further reduced costs at the field level. The benefit from these actions results in the downward trend of our production expenses in 2015, while corporate G&A cost reductions will be more evident in 2016.

Regarding production expenses, we are making more efficient use of helicopters and marine vessels. We have also reduced our manpower costs through a 20% across the board reduction in dayrate for all rotating expatriates and cut other related benefits, as well as took actions to lower travel costs. We are achieving 10-15% production cost reductions since the beginning of the year. We have additional plans to further reduce costs in early 2016 as our development projects begin to wind down.

Additional detail on our production expense reductions can be seen on slide 7 of the supplemental information. I would like to point out that we have reduced production expenses on a per BOE basis over the past year from $27.43 per BOE in Q4 2014 to $19.36 per BOE in Q3 2015. We also expect Q4 2015 to be even lower and have shown the range between $16.50 and $18.50 per BOE.

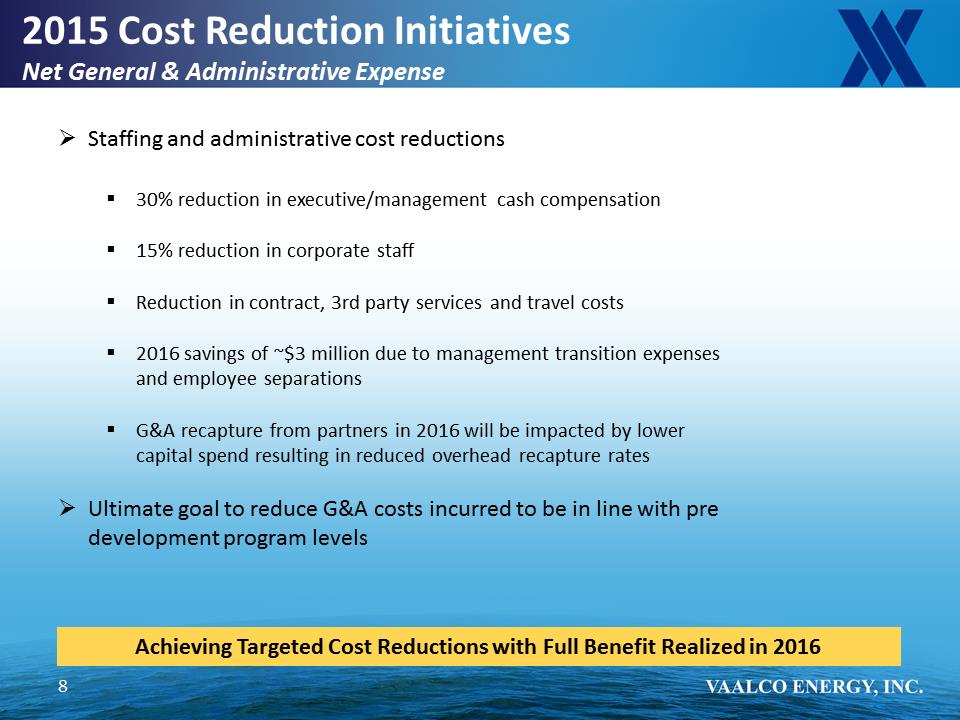

On the G&A front, let me remind you that in early 2014, we increased our staffing levels when we undertook the two-platform design, fabrication and installation projects and the subsequent six-well drilling program, and have already made changes to meaningfully reduce future G&A costs. We are cutting our aggregate future executive and management cash compensation 30% compared with 2013. We have also reduced our corporate staff in Houston by approximately 15%, as well as reduced our contract services and other third party costs. We will continue to make the difficult decisions to ensure we are delivering on our 2015 cost reduction initiatives. Moving into 2016, we will seek out additional opportunities where we can reduce expenses to ensure we are competitive and are in a position to weather a “lower for longer” oil price environment.

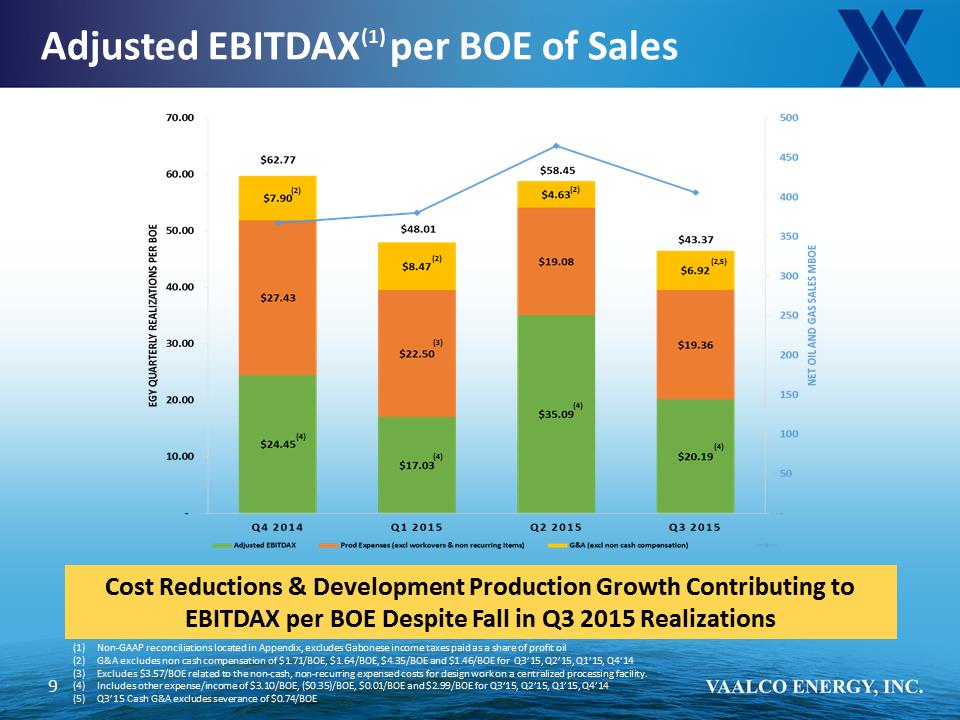

We generated positive adjusted EBITDAX of $8.2 million in the third quarter despite the 26% decline in oil prices and the 13% decline in liftings between the second and third quarters. On a BOE basis as shown on slide 9, cash production expenses remained low at $19.36 per BOE and cash G&A was $6.92 per BOE after severance expenses, resulting in positive Adjusted EBITDAX per BOE of $20.19 despite lower prices and liftings.

Now let me now turn the call over to Greg for a more detailed review of our financials.

Greg Hullinger, VAALCO Chief Financial Officer:

Thank you, Steve. I will be reviewing key financial information pertaining to the third quarter of 2015 that we reported yesterday in our earnings press release and the SEC Form 10-Q. I will also be providing guidance information pertaining to remainder of the year.

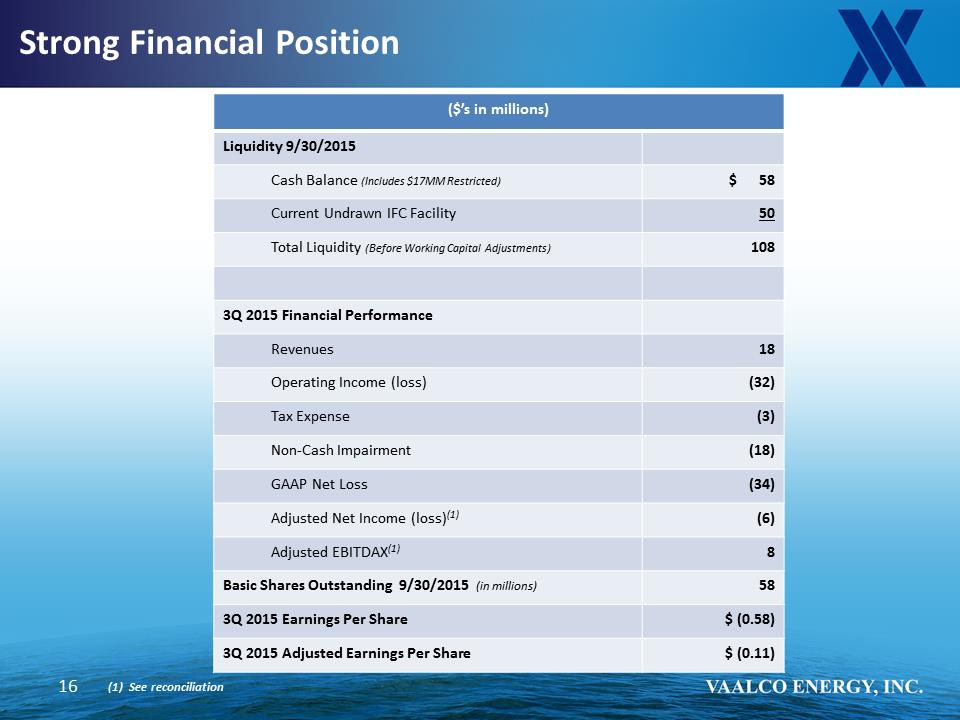

We reported an adjusted net loss of $6.5 million dollars, or eleven cents per diluted share for the third quarter of 2015. Adjusted EBITDAX was $8.2 million dollars in the third quarter of 2015. The third quarter adjusted net loss number is before an $18.0 million dollar non-cash impairment charge related to the Etame Marin block offshore Gabon. Also excluded was a $9.2 million dollar non-cash charge to exploration expense for a well drilled in 2012 onshore Gabon in the Mutamba Iroru block. I will be talking more about these items in a couple of minutes. For comparison, adjusted net income for the second quarter of 2015 was $0.6 million dollars or one cent per diluted share.

Including the impairment and well write-off, GAAP net loss for the third quarter was $33.7 million dollars or fifty-eight cents per share. This compared to a net loss of $5.2 million or nine cents per diluted share in the second quarter of 2015.

The impact of lower oil prices continue to be clearly seen in our quarterly revenue number. Revenues of $17.5 million dollars reported for the third quarter of 2015 were lower than the $27.1 million of revenues for the second quarter of 2015. The average oil price we received in the third quarter of 2015 was $43.97 per barrel, compared to $59.16 per barrel in the second quarter of 2015, a 26% decrease. Going back a year ago to the third quarter of 2014, the oil price averaged $94.67 per barrel, a decrease of 54% compared to the third quarter 2015 oil price received.

Barrels lifted during the third quarter of 2015 in Gabon of approximately 396,000 barrels were lower than the 455,000 lifted in the second quarter of 2015. The higher Q2 lifting amount resulted from a large opening inventory balance that was lifted during that period.

Revenue is a function of both price and the amount of barrels sold via the crude liftings that occur in Gabon on approximately a monthly basis. VAALCO’s net production from Gabon in the third quarter of 2015 was approximately 431,000 net BOE or 4,700 net BOE per day compared to approximately 404,000 or 4,400 net BOE per day produced during the second quarter of 2015, a 7% increase. Production in the third quarter of 2015 was approximately 21% higher than the third quarter of 2014 at 358,000 net BOE or 3,900 net BOE per day.

Production increases are attributable to new producing development wells that were drilled post-third quarter 2014, including two wells brought online in the third quarter of 2015. Cary will be providing more information on this topic shortly.

VAALCO’s working interest in the inventory aboard the FPSO vessel at September 30, 2015 was approximately 55,000 barrels versus approximately 27,000 barrels at June 30, 2015.

Now let me move to the other key financial components for the third quarter of 2015.

Operating loss was $32.1 million dollars in the third quarter of 2015 compared to an operating loss of $1.0 million dollars in the second quarter of 2015. The operating loss in the third quarter was significantly impacted by the impairment charge of $18.0 million dollars to adjust to fair value certain fields in the Etame Marin block and the $9.2 million dollars for the onshore Gabon well write-off as it no longer met the criteria for capital treatment as suspended exploration well cost.

In connection with its assessment of impairment for the three months ended September 30, 2015, the Company identified an immaterial error. This immaterial error was present in the calculation of the impairment for the December 31, 2014, March 31, 2015 and June 30, 2015 periods. As a result of this error, the impairment charge of $98.3 million dollars recorded for the year ended December 31, 2014 was understated by $7.0 million dollars or 7.2%. The impact of the error resulted in an overstatement of the impairment charge of $3.1 million for the

three months ended March 31, 2015 and an understatement of the charge of $0.5 million dollars for the three months ended June 30, 2015. In accordance with Staff Accounting Bulletin (“SAB”) No. 99, titled Materiality, and SAB No. 108, titled Considering the Effects of Prior Year Misstatements when Quantifying Misstatements in Current Year Financial Statements, we evaluated these errors, including both qualitative and quantitative considerations, and concluded that the errors did not, individually or in the aggregate, result in a material misstatement of our previously issued consolidated financial statements. For more information, please refer to our 10-Q filed yesterday.

Additionally, we incurred a $13.5 million dollar impairment charge based on our third quarter assessment of impairment for the North Tchibala field. Lower projected oil prices and higher well costs that were considered in the fair value evaluation of the field were the factors that brought about the current period impairment charge.

Production expenses for the 2015 third quarter were $7.9 million dollars or $19.36 per BOE, compared to $8.9 million dollars, or $19.08 per BOE for the second quarter of 2015. The decrease in the expense amount is attributable to cost reductions in contract services, materials and operational efficiencies. We are slightly increasing our production expense guidance on an absolute basis to $33 - $34 million for full year 2015. While we are slightly raising the absolute production expenses, our per unit costs are expected to decline. Cary will talk about this in more detail shortly.

As we have previously disclosed, we anticipate we will have up to three workovers performed in the Avouma and South Tchibala fields in the fourth quarter to replace electrical submersible pumps at an approximate combined net cost to VAALCO of between $6 and $9 million dollars. Our plan is to begin the workovers following the completion of the North Tchibala 2-H development well.

Exploration expense for the third quarter of 2015 was $9.0 million dollars, compared to $1.1 million dollars recorded in the second quarter of 2015. Exploration expense during the third quarter of 2015 includes a $9.2 million dollar non-cash charge for suspended exploratory well costs related to the Mutamba Iroru onshore Gabon block. We drilled a successful exploration well, the N’Gongui #2, in 2012 and have had it recorded as an asset on our books as suspended well cost since that time. We conduct quarterly evaluations to determine whether sufficient progress is being made towards development as well as the economic and operational viability of the project. We determined the investment in the well did not continue to meet the criteria for suspended well costs primarily based on lower projected oil price data and updated development cost scenarios. Accordingly, the costs were recorded as exploration expense in the third quarter of 2015. Exploration expense for the fourth quarter of 2015 is expected to be minimal.

DD&A for the third quarter of 2015 was $8.3 million dollars compared to $9.3 million in the second quarter of 2015. The third quarter DD&A rate was $20.34 per barrel. Guidance for the fourth quarter is a range of $20 to $22 dollars per barrel and we expect to be in the range of $19 to $22 dollars per barrel for full year 2015.

General and Administrative expenses for the third quarter of 2015 totaled $3.8 million dollars comparable to the $2.8 million dollars recorded last quarter. $0.3 million of the increase is due to severance costs. Guidance for net G&A expense is expected to be in the range of $15 to $16 million dollars in 2015.

Other Costs and Expenses of $2.8 million dollars represents a further bad debt allowance taken on the Value Added Taxes receivable we have from the Government of Gabon. We recorded bad debt expense in the third quarter of 2014 of $1.8 million for the same reason. These bad debt allowances against the accounts receivable balance were taken to reflect slow repayment by the Republic of Gabon to reimburse the Company for its VAT payments. Across the industry in Gabon, the Republic has not been repaying these amounts as timely as they had in the past. Repayments by the government have a history of being non-timely, but it appears that repayments are falling further behind. No reimbursements were received in the third quarter of 2015. We recorded the bad debt expense to reflect the further slowdown and uncertainty in receiving payments dating

back as far as August of 2012. We will be able to recognize the allowances taken as income if we ultimately receive these monies that are owed to us. The full amount owing the Company at September 30, 2015 was $8.9 million dollars. In addition, the unreserved VAT receivable balance has been re-classified from the current asset section to the noncurrent asset section on the balance sheet beginning this reporting period.

Income tax expenses for the third quarter of 2015 were $2.7 million dollars compared to $4.3 million dollars in the second quarter of 2015. The decrease in income taxes reflects the impact of the lower sales price received for oil sales during Q3 2015.

Cash and cash equivalents including restricted cash totaled $57.6 million dollars at the end of the third quarter of 2015. This compares to $78.1 million dollars at the end of the second quarter of 2015 and $91.5 million dollars at the end of 2014. We also have $50 million of undrawn capacity on our $65 million IFC credit facility. Capital expenditures spent totaled $72.2 million dollars through the first three quarters of 2015.

As Steve discussed, our guidance regarding capital expenditures in 2015 is expected to be in the range of $83 to $86 million dollars.

Cary will now provide you with an operational update.

Cary Bounds, VAALCO Chief Operating Officer:

Thank you Greg.

And I am excited to provide more details on the positive operational developments that we had this past quarter and then take a look ahead for the balance of 2015. Let me start with a few comments on production performance. The wells drilled and completed so far in 2015 have made a substantial contribution to our production rates. As Steve mentioned, third quarter production exceeded the high end of our guidance range.

The primary driver behind exceeding third quarter production expectations was better than expected performance from the new wells that came on line in the quarter, which were the SE Etame 2H and the North Tchibala 1H. However, the production uplift from our new wells was partially offset by the natural decline we see in the underlying base production from wells drilled prior to 2015. In addition, strong production from the new wells also helped us overcome lost production as a result of shutting in the South Tchibala 2H well due to an Electric Submersible Pump failure.

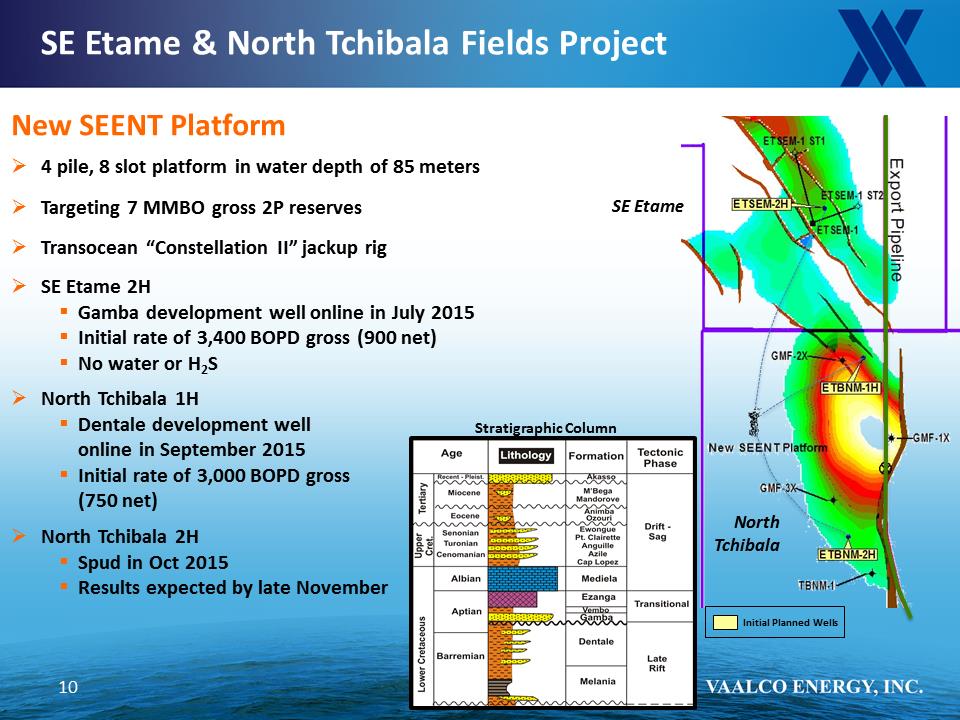

Now I will turn to our drilling campaign and talk about our development well results. All of our third quarter drilling was conducted from the SEENT platform, which was installed in late 2014. The SEENT platform came on line, trouble free, in July with first oil from the SE Etame 2H well. As I mentioned earlier, production performance from the SE Etame 2H well exceeded expectations and the well continues to produce at strong rates.

Upon completion of the SE Etame 2H, we successfully drilled and completed the North Tchibala 1H, which is a development well in the Dentale D-9 formation, which was discovered in 1977 prior to VAALCO having an interest in the block. The Dentale formation already produces from onshore Gabon fields, but has never produced offshore

We are very proud that the North Tchibala 1H established the first Dentale production for the industry in the offshore waters of Gabon.

As Steve noted earlier, the North Tchibala 1-H well was drilled to approximately 11,200 feet measured depth and came on production on September 15th at about 3,000 gross barrels of oil per day with no H2S and no water production. The 1H well exceeded our expectations and produced at a sustained rate of 3,000 barrels of

oil per day for six weeks with minimal pressure depletion. We are continuously monitoring the well’s performance and we recently observed a decline in bottom hole pressure accompanied by an increase in gas production rates. In response to the drop in pressure, we have choked the well back to stabilize bottom hole pressure and rates have decreased by 1,000 to 1,500 barrels of oil per day. Even with the reduction in rate, production from the well is still slightly higher than our initial expectations. I want to emphasize that it is too early to determine the extent of the impact this recently observed pressure depletion may have on the well’s long-term performance and we will continue to monitor and optimize the well.

Turning to the North Tchibala 2-H where we are currently drilling, this well is targeting the deeper Dentale D-18/19 formation at about 16,000 feet measured depth and we believe the North Tchibala 2H will be the longest well ever drilled in Gabon. We ran and cemented intermediate casing at approximately 14,600 feet measured depth without encountering any problems while drilling. We are currently in the process of re-drilling the last 1,800 feet of lateral section in the wellbore after encountering hole stability issues with the open hole portion of the well. The initial lateral encountered good quality reservoir and we believe we will have the same, or possibly better quality reservoir in the replacement lateral. We still expect to have results from the well by late November.

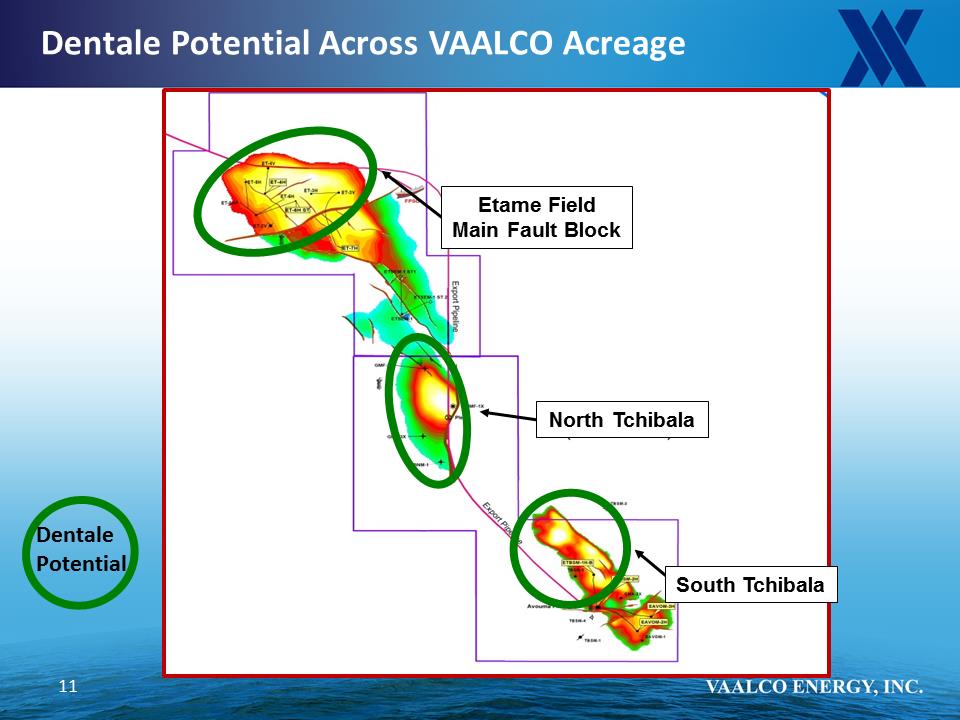

So far, the reservoir results from both the North Tchibala 1H and North Tchibala 2H are encouraging and we are looking for other areas on the Etame Marin block to develop the Dentale. If you take a look at slide #11 in the supplemental information, you will see several other areas on the block where we think there is Dentale potential and we are looking at these areas closely. However, it will take additional drilling along with long-term monitoring of the first two wells before we have a clear understanding of what that ultimate potential might be. Future drilling may include another Gamba development well on the Etame platform, and this well could also test the Dentale formation in the main Etame fault block.

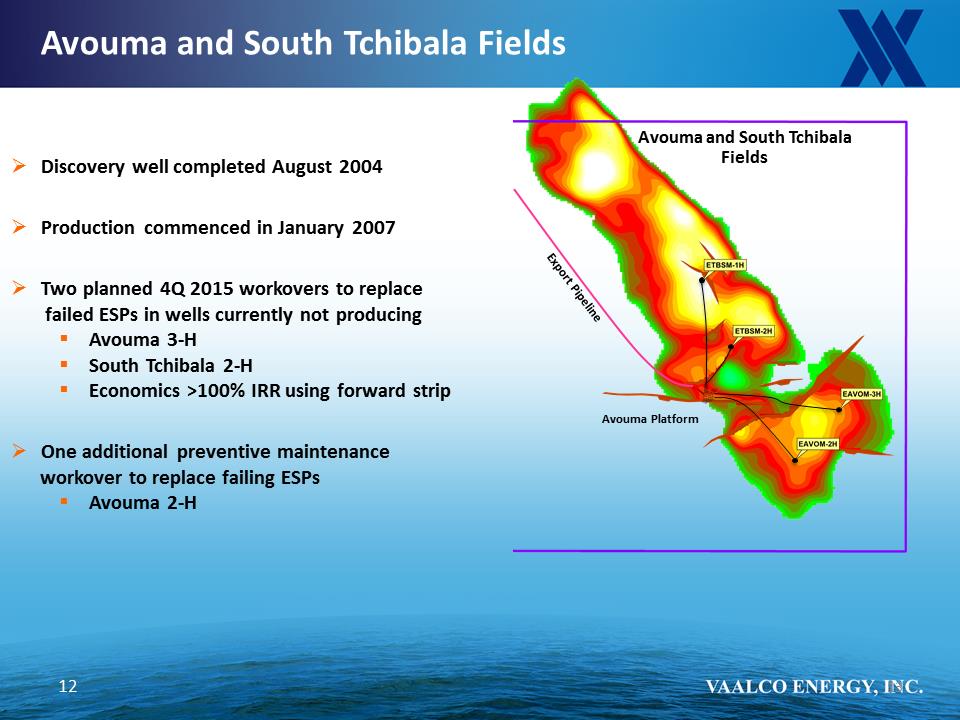

Now, I will spend a few minutes on the rig schedule for the remainder of the year. Given favorable sea state conditions, our contract jack up rig, the Transocean Constellation II, will move to the Avouma platform after completing the North Tchibala 2-H well. On the Avouma platform, the rig will perform workovers to replace electrical submersible pumps, or ESPs, in three existing wells, two of which are currently off line. The production uplift from the two off-line wells is expected to generate returns greater than 100% using current strip pricing. The third workover is for preventive maintenance to minimize the risk of an ESP failure in the future

The production impact from the workovers will be minimal for fourth quarter 2015 volumes, but we do expect to see a robust production boost by early 2016. Moving from drilling to operations, the 2015 planned shutdown for annual maintenance on the Etame block has been rescheduled to January 2016. The planned shutdown is expected to last approximately six days during which period all producing wells will be shut-in.

Moving on to the crude sweetening project, our engineering team continues to focus on evaluating the most cost effective crude sweetening option for the removal of H2S from the affected wells at Ebouri and Etame. The outcome of the team’s evaluation is expected to be reviewed by the Etame partners in the fourth quarter of 2015. Moving to onshore Gabon and our Mutamba project where, since mid-2014, we have been working to finalize a revised or new PSC with the government of Gabon to allow for development of the discovery and to maintain exploration rights on the block.

We received a letter last month from the Gabon government expressing their view that the initial PSC has expired. The letter also encouraged us to quickly negotiate to enter into a new PSC, thereby preserving our rights to the 2012 discovery and the current cost account. VAALCO and our joint venture partner are in agreement that the initial PSC has not expired. Further meetings were held in October of this year with the government and our joint venture partner to discuss possible new PSC terms that take into account the recent substantial decrease in oil price. We plan to continue meeting with the joint venture partner and the government

in an effort to negotiate and enter into a new PSC that will give us the opportunity to develop discovered resources on the block

Turning our attention to Angola, the Company recently opened a data room in London to seek to farm out a portion of our working interest in Block 5 offshore Angola. We previously mentioned that our interpretation of the reprocessed 3-D seismic data on the block has identified four top prospects with an estimated total gross unrisked mean recoverable resource potential of over 800 million barrels of oil. A number of large independent exploration and production companies as well as major oil companies have expressed interest and signed confidentiality agreements and will be reviewing the data over the coming months. We are excited about the potential in Angola, but would like to mitigate some of the exploration risk through this farm out process.

The current concession extends through November 2017 with no additional exploratory drilling in Angola expected before early 2017. As Steve has mentioned in the past, our remaining three commitment wells in Angola each have termination costs of $5 million net to VAALCO. While there are no current plans to drill additional wells on Block 5 until early 2017, any future actions in Angola will depend on our cash position, the forecast of oil price at the time of the rig commitment, the revised estimated cost to drill the wells, the success of our farm out efforts, as well as the size and quality of the targeted prospects.

In Equatorial Guinea, we continue to work with the Ministry of Mines, Industry and Energy as well as GEPetrol, the current block operator, on a revised joint operating agreement which we expect will name VAALCO as operator. We’ve had good dialogue in recent months with our partners and we are working on timing and budgeting for the project, including the approval of a development and production plan. Development project economics are being re-evaluated, considering continued low oil prices and the expected decrease in development costs associated with the fall in oil prices.

Finally, I would like to wrap up the operations update by talking about the operational cost reductions that we have put in place and how those have contributed to the significant reduction in unit operating expense. This past year, we implemented sustainable cost reductions through work efficiencies, reducing contract services, reducing material costs and right sizing our operations organization in an effort to maximize margins. None of these cost reductions have impacted our focus on asset integrity, safety and environmental performance. As you can see on slide 6, the cost reductions are coming from a number of areas and the most notable reductions are associated with changing the way we do our business in terms of logistics, manpower and chemicals.

As you can see on slide 7 of the supplemental information, we have been successful in our efforts to reduce costs on a unit basis from $27.43 per BOE in the fourth quarter of 2014 to a forecast of approximately $18 per BOE in the fourth quarter of 2015. We are capturing these savings and efficiencies and believe that we have approximately $4 million net in cost reductions heading into 2016.

To close out, I want to emphasize that we are focused on conducting our operations in a cost effective manner without compromising safety, the environment or the integrity of our assets. The growing production profile at Etame has really helped improve our financial performance as we have brought high margin barrels into our existing operating infrastructure. We are generating positive results as we deliver on the strategy that Steve laid out earlier to reduce costs, economically develop production and add shareholder value as we continue to look for more efficient ways to run our operations.

With that, let me now turn the call back over to Steve.

Steve Guidry, VAALCO Chief Executive Officer:

Thanks, Cary.

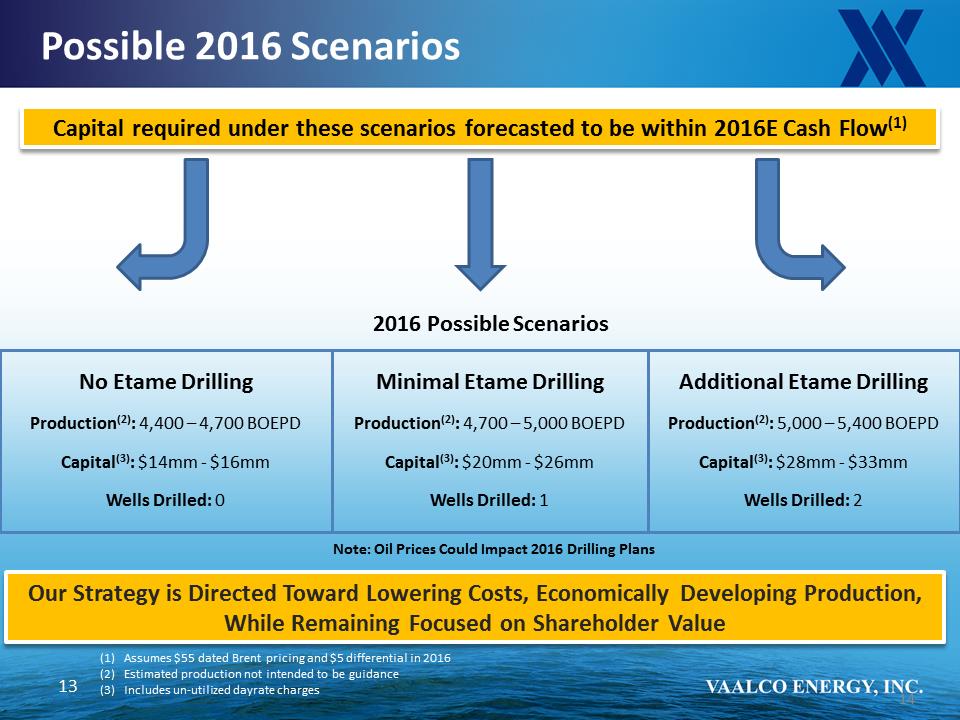

As we look ahead past the North Tchibala 2H development well currently drilling and the upcoming three-well Avouma/South Tchibala workover program, we will consider any further drilling beyond that point in 2016 on a well-by-well basis. As previously discussed, in early 2014, VAALCO and its partners contracted with Transocean for the use of the Constellation II jack up rig through July 5, 2016. We have a portfolio of additional Etame development wells in both the Gamba and Dentale formations as options for continuing the drilling program beyond this year’s commitment. Additionally, to provide us with maximum flexibility next year. We have hired a broker to actively market the rig to other operators.

Should VAALCO and its partners elect to not fully utilize the rig for the entire contract duration, and if sub-lease options are not available, a day-rate charge for the unused portion of the contract would be incurred. We are currently discussing our 2016 budget with our partners and as you can see on slide 13 of the supplemental information, we have several scenarios that we are evaluating.

The first possible scenario is to release the rig after the workovers, which will cost us approximately $9 million in un-utilized day-rate charges net to VAALCO. Keep in mind that we have benefited from a lower day rate than we otherwise would’ve had with a shorter term rig contract. In this scenario, our total net capital expenditure for 2016 is estimated in the $14-$16 MM range. The second scenario is to drill one additional development well, likely an Etame platform well with a Dentale pilot test that Cary mentioned. This would result in approximately $20-26 million in total net capital and reduce the un-utilized day-rate charges to approximately $6 million net to VAALCO. The third scenario involves the drilling of 2 additional wells, with approximately $4 million of un-utilized day-rate charges and a total net capex spend of approximately $28-33 million. As you can see, all three of these possible scenarios are significantly lower than our 2015 capex spend of $83 to $86 million. We are currently forecasting that cash flow from operations will exceed the cash required for any of these three possible capital investment scenarios assuming $55 per barrel Dated Brent pricing.

We are working closely with our partners to identify the appropriate course of action for all parties involved that will allow us to maximize the value of every dollar spent. And, obviously oil prices will have a significant impact on our future drilling plans. With that said, we continue to have a very strong balance sheet, and in the current price environment we want to protect our liquidity, while remaining opportunistic in our investment decisions allowing us to stay focused on shareholder value.

In summary, I would like to re-emphasize the fact that our strategy is directed toward lowering costs and investing in projects that yield good economic returns in the current pricing environment. We have done a good job of achieving strong production results from our drilling program, unit operating costs have been reduced and we are maximizing the margins that we make on every barrel that we sell. We are in a strong position financially to be opportunistic in the current macro pricing environment. We will strive to improve our operating performance even further and continue to deliver free cash flow with the consistent goal of enhancing shareholder value.

Thank you and with that Al, we are ready to take questions.

Al Petrie, VAALCO Investor Relations Coordinator:

We are ready to open up the queue for questions.

Moderator:

Thank you. Ladies and Gentlemen, if you wish to ask a question please press * followed by the 1. You will hear a tone indicating that you have been placed in queue and you may remove yourself from queue at any time by pressing the pound key. Once again, for questions, please press * followed by the 1 key at this time. One moment for our first question.

Our first question today comes from the line of Leo Mariani with RBC Capital. Please go ahead.

Leo Mariani, RBC Capital:

Hey guys, I appreciate the update. I was hoping to get a little bit more color on how that first well at Southeast Etame is currently holding up in terms of what it is producing and then what is the overall current production at VAALCO right now?

Steve Guidry, VAALCO Chief Executive Officer:

Thanks Leo. The well is doing very well. The Southeast Etame well continues to perform very well, in fact as we said in our prepared remarks---we’re very happy with the last four wells that we have drilled in 2015. Southeast Etame, just as a reminder, it was drilled to an area of the field that---it’s a Gamba producer so it’s continuing to exhibit the kind of performance that we’ve come to expect from the Gamba. For more details, let me just ask Cary to give us an update on that well in particular. I can you that our current production is right now circa 20,000 barrels a day gross

Cary Bounds, VAALCE Chief Operating Officer:

That’s right Steve, our gross production is around 20,000 barrels a day gross and a bid contributor is the Southeast Etame 2-H well and Leo, we have not really seen any material decline in the well’s rate or pressure---it is a very strong well.

Leo Mariani, RBC Capital:

So, it came on a 3,000 barrels a day---so it’s still at 3,000 barrels a day? Is that what you’re saying?

Cary Bounds, VAALCE Chief Operating Officer:

Yes, it’s very close to 3,000 barrels a day.

Leo Mariani, RBC Capital:

Okay. In terms of your oil price realizations in the third quarter, I guess they were roughly $6.00 below Brent. I want to get a sense of where those are going to be going forward. I know you guys were able to get a new contract to sell your production.

Steve Guidry, VAALCO Chief Executive Officer:

Yes Leo, let me take that one. We have experienced a widening of the differentials in West Africa. The last time oil prices dipped to this level, we saw a widening of the differentials. That improved a bit when we saw the bump this summer when oil prices went back above $60, but now that prices are back down again the differential is beginning to widen, so I think it’s a sign that West Africa crude oil right now in this environment has to travel further and is just less sought after. But we are using an estimate of about $5.00 a barrel differential going forward.

Leo Mariani, RBC Capital:

Okay, that’s helpful. In terms of the Dentale reservoir, obviously the good first well result there---I’m trying to get a sense, do you have any reserves booked in the Dentale in terms of the either 1P or 2P at year end 2014?

Steve Guidry, VAALCO Chief Executive Officer:

Yes, we do. I’ll say this, that the majority of those reserves are booked in probable, not in proven developed. Let me ask Cary to give you some more information on that.

Cary Bounds, VAALCE Chief Operating Officer:

If I recall correctly, Leo, it’s a very nominal amount that’s booked in proven---maybe 0.2 million barrels and I think 0.3 million barrels are booked in probable and that’s for, like I said, the Dentale development off SEENT.

Steve Guidry, VAALCO Chief Executive Officer:

And those numbers are net to VAALCO.

Leo Mariani, RBC Capital:

Okay, thanks guys.

Moderator:

Our next question comes from Matt Dhane, with Tieton Capital. Please go ahead.

Matt Dhane, Tieton Capital:

Great, thank you. I was curious, the guidance for Q4, does it include any costs for the activist investor situation that you are facing here today?

Steve Guidry, VAALCO Chief Executive Officer:

No, we were looking to limit our comments to Q3, but you’re right, in Q4 we are anticipating additional costs---those costs are not included in any guidance that we have given. They would be extraneous to that current guidance and so you should look for us to report on that as kind of a separate item in Q4.

Matt Dhane, Tieton Capital:

Okay. I also wanted to ask about Angola. The pre-salt timeline. As you sit here today, what’s your expectation with current pricing? I know you have the data room open. Discuss your expectation around Angola today.

Steve Guidry, VAALCO Chief Executive Officer:

Okay, well we’re very excited about the uptake that we’ve seen in companies interested in our data room in London. The number continues to climb, but I want to say we have twelve companies currently that have indicated an interest, four of those have been through the data room, the rest are in the queue to go through the data room. So, a lot of interest in the project. What we have done is for 2016, we’ve included money in our budget for long-lead materials to put us in a position to be able to execute on a drilling program in 2017. It’s too early right now for us to say exactly how the farm-out will turn out, but we’re hopeful that we will be successful in getting a carry on those wells and we’ll be able to move forward according to the plan.

Matt Dhane, Tieton Capital:

Great, thank you.

Moderator:

There are no other questions queuing up at this time.

Steve Guidry, Chief Executive Officer:

Okay, well let me thank everyone for your attention and your participation in this morning’s call. We look forward to visiting with you at the end of 2015 where we can give you a full year view of how our performance stacked up.

Al Petrie, Investor Relations Coordinator:

Tom, it looks like we picked up one more question that has come up…

Moderator:

Okay, we will go to Leo Mariani’s line with RBC. Please go ahead.

Leo Mariani, RBC Capital:

Hey guys, a quick follow-up question here. Obviously, your capex is trending upwards in 2015---you know, a kind of chunky number here on the 3rd quarter---just over $30 million. I’m trying to get a sense, you guys referenced some higher drilling costs. Are you guys actually seeing some kind of higher per well costs or has this been more a result of some mechanical issues where you had to re-drill some wells this year in terms of your well costs?

Steve Guidry, Chief Executive Officer:

Good question Leo. Let me tee this up here, then I’ll ask Cary to give you some additional details. In drilling off the SEENT platform, we are drilling wells that are really cutting edge for Gabon. These wells we’re drilling---they really are the first wells that have ever been drilled---deviated wells---that have been drilled through the formations that we’re drilling. Primarily the Dentale, which is a stacked, sand-shale sequence. We have had some hole stability and mechanical issues with the wells we have drilled off of SEENT. I am happy to say that our team has reassessed our approach to these wells. We’ve had an outside party come in and look at all of our drilling plans and drilling parameters. We’ve made adjustments to the drilling plan and, with time, we’ve been able to really get our hands around the drilling costs and we’ve had fewer and fewer drilling problems on the SEENT platform as we’ve gone from the first Southeast Etame well, we had fewer on the North Tchibala 1-H well and we’ve had minimal problems now on the North Tchibala 2-H well. So, they’ve done a great job. Let me ask Cary to tell you a bit about it…

Cary Bounds, VAALCE Chief Operating Officer:

That’s a good summary Steve. I’ll just add that, like Steve mentioned, we have incorporated lessons learned from our early well in the drilling campaign and we have found that we needed to change, say, the well design to account for H2S---so we’ve added metallurgy to the new wells that is compatible to H2S. Based on some of the hole stability issues we saw early in the campaign, we switched from drilling with water-based mud to oil-based mud---that increased the cost a little bit. And then, unfortunately, early in the campaign we did leave bottom-hole assemblies behind in two wells and that cost us some money. But like Steve said, we’ve seen some dramatic improvements and we don’t envision that will happen again.

Leo Mariani, RBC Capital:

Okay, so what do you see as a kind of run-rate number to drill one of these wells in the Etame Marin concession with a jack-up going forward here in terms of gross, and then net?

Steve Guidry, Chief Executive Officer:

You know, it depends if you’re drilling Gamba or Dentale. Our Gamba wells, I think, we are currently estimating to be in the range of $32 million gross. So just over $10 million our net share. The Dentale wells we are estimating to be gross $37 to $39 million.

Leo Mariani, RBC Capital:

Okay, thank guys.

Steve Guidry, Chief Executive Officer:

Thank you, Leo.

Moderator:

We did have one other question, would you like to take that?

Al Petrie, Investor Relations Coordinator:

Yes, that will be fine.

Moderator:

Okay, we will go to the line of John Kornizter with Kornitzer Capital Management. Please go ahead.

John Kornizter, Kornitzer Capital Management:

Can you hear me okay?

Steve Guidry, Chief Executive Officer:

Yes, we can. Thank John, good morning.

John Kornizter, Kornitzer Capital Management:

Good morning. On these wells, what do you need for gross production to make them profitable at $45 a barrel? Or $50?

Steve Guidry, Chief Executive Officer:

I don’t have that number in front of us right now, but we were estimating that these wells were---I’ll tell you, at $55 oil, I think we were estimating these wells to be rates of returns in the 30-40% range.

John Kornizter, Kornitzer Capital Management:

Okay.

Steve Guidry, Chief Executive Officer:

To your point, John, we think a 1,500 barrel a day gross initial rate is what is necessary for us to earn an acceptable rate of return on a Gamba well.

John Kornizter, Kornitzer Capital Management:

Okay, and all your wells have been coming in at over 1,500 barrels a day.

Steve Guidry, Chief Executive Officer:

They have been, yes.

John Kornizter, Kornitzer Capital Management:

Okay. You know, I think you’ve done an excellent job with this company. You’ve had bad luck this past year in drilling some of these wells where the costs were extremely high. But, you know when I think about the number of oil companies that are near bankruptcy that have lost a tremendous amount of their value because oil dropped down to forty-some dollars a barrel---you guys are in excellent shape financially. We’re not talking about you going bankrupt, we’re not talking about restructuring any debt, we’re not talking about anything that’s life threatening to the company except the price of oil is down and that’s just going to be a matter of patience for it to go back up.

What I don’t understand is---you know, I am extremely happy with the company, okay. And I think you guys have done an excellent job, okay. Nobody can predict a well when you drill it. Your cost overruns, because what rigs were the past couple of years, because oil was over $100, was very acceptable. Getting a rig was very tough. You had timelines you had to drill.

Monday morning quarterbacking is a great deal. In football, and basketball and baseball and everything else. But Monday morning quarterbacking is easy. But being there and making the tough decisions is tough. And I want to congratulate you on the excellent job you guys have done over the years. Especially with the new team, you’re doing a great job. The Board has been with you all the way. And it’s very hard to change things within the company within ten days and people not up to speed can make a big blunder going forward. So I congratulate you and keep up the good work.

Steve Guidry, Chief Executive Officer:

John, thanks for those comments. We’ve done everything we can to make the best of a bad situation. I think it was fortunate for our company that as oil prices fell we did have the cash balance necessary to continue to fund the development. That was a luxury that most other E&P companies did not have. And I think it’s put us in a very favorable position now with production at near-peak levels. The way we see it, we will be able to weather this storm going forward. Thank you for the comments.

John Kornizter, Kornitzer Capital Management:

You’re welcome, they are well deserved.

Moderator:

There are no other questions queued up at this time.

Steve Guidry, Chief Executive Officer:

Again, thanks everyone for your time this morning and thanks for your interest and your questions and your investments. We appreciate it, thank you very much.

Moderator:

Ladies and Gentlemen, this conference will be available for replay starting at 10:00 AM this morning and run through December 10th at midnight. You may access the AT&T executive playback service at any time by dialing 1-800-475-6701 and entering the access code of 369429. International participants may dial 320-365-3844. Those numbers again are 800-475-6701 and International Participants dial 320-365-3844. Please enter the access code of 369429. That does conclude our conference for today. We thank you for your participation.

-------------------------------------------

Important Additional Information

In connection with the consent solicitation initiated by the Group 42−BLR Group, the Company may file a consent revocation statement and other documents regarding the proposals of the Group 42−BLR Group with the SEC and may mail a consent revocation statement and a consent revocation card to each stockholder of record entitled to deliver a written consent with respect to the proposals of the Group 42−BLR Group. STOCKHOLDERS ARE ENCOURAGED TO READ ANY CONSENT REVOCATION STATEMENT AND ANY OTHER RELEVANT DOCUMENTS FILED WITH THE SEC WHEN THEY BECOME AVAILABLE, BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION.

The Company, its directors and executive officers may be deemed to be participants in the solicitation of consent revocations in connection with the proposals of the Group 42−BLR Group. Information regarding the names of the Company’s participants and their respective interests in the Company by security holdings or otherwise is set forth in the proxy statement for the Company’s 2015 Annual Meeting of Stockholders as filed with the SEC on Schedule 14A on April 16, 2015. To the extent names of the Company’s directors and executive officers and their holdings in the Company’s securities have changed since the 2015 proxy statement, such changes have been reflected on Initial Statements of Beneficial Ownership on Form 3 or Statements of Change in Ownership on Form 4 filed with the SEC. Additional information can also be found in the Company’s Annual Report on Form 10-K for the year ended December 31, 2014, filed with the SEC on March 16, 2015 and in the Company’s Quarterly Reports on Form 10-Q for the first three quarters of the fiscal year ending December 31, 2015 filed with the SEC on May 7, 2015, August 6, 2015, and November 9, 2015, respectively. Additional information regarding the interests of the Company’s participants in any solicitation of consent revocations in connection with the proposals of the Group 42−BLR Group and other relevant materials, if any, will be filed with the SEC when they become available.

These documents, including any consent revocation statement (and amendments or supplements thereto) and other documents filed by the Company with the SEC, are or will be available for no charge at the SEC’s website at www.sec.gov and at the Company’s investor relations website at vaalco.investorroom.com. Copies may also be obtained by contacting the Company by mail at 9800 Richmond, Suite 700, Houston, Texas 77042, Attention: Corporate Secretary or by telephone at (713) 623-0801.

NYSE:EGY

VAALCO ENERGY, INC

Third Quarter 2015

Supplemental Information

2

Safe Harbor Statement

VAALCO ENERGY, INC

This document includes "forward-looking statements" within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking statements are those concerning VAALCO's plans, expectations, and objectives for future drilling, completion and other operations and activities. All statements included in this document that address activities, events or developments that VAALCO expects, believes or anticipates will or may occur in the future are forward-looking statements. These statements include expected capital expenditures, future drilling plans, prospect evaluations, availability of capital, negotiations with governments and third parties, expectations regarding processing facilities, and reserve growth. These statements are based on assumptions made by VAALCO based on its experience and perception of historical trends, current conditions, expected future developments and other factors it believes are appropriate in the circumstances. Such statements are subject to a number of assumptions, risks and uncertainties, many of which are beyond VAALCO's control. These risks include, but are not limited to, oil and gas price volatility, inflation, general economic conditions, the Company's success in discovering, developing and producing reserves, lack of availability of goods, services and capital, environmental risks, drilling risks, foreign operational risks, and regulatory changes. These and other risks are further described in VAALCO's quarterly reports on Form 10-Q for the three months ended March 31, 2015, June 30, 2015 and September 30, 2015, annual report on Form 10-K for the years ended December 31, 2014, and other reports filed with the SEC which can be reviewed at http://www.sec.gov, or which can be received by contacting VAALCO at 9800 Richmond Avenue, Suite 700, Houston, Texas 77042, (713) 623-0801. Investors are cautioned that forward-looking statements are not guarantees of future performance and that actual results or developments may differ materially from those projected in the forward-looking statements. VAALCO disclaims any intention or obligation to update or revise any forward-looking statements, whether as a result of new information, future events, or otherwise. .The SEC generally permits oil and natural gas companies, in filings made with the SEC, to disclose proved reserves, which are reserve estimates that geological and engineering data demonstrate with reasonable certainty to be recoverable in future years from known reservoirs under existing economic and operating conditions and certain probable and possible reserves that meet the SEC’s definitions for such terms. In this press release and the conference call, the Company may use the terms “resource potential” and “oil in place”, which the SEC guidelines restrict from being included in filings with the SEC without strict compliance with SEC definitions. These terms refer to the Company’s internal estimates of unbooked hydrocarbon quantities that may be potentially added to proved reserves. Unbooked resource potential and oil in place do not constitute reserves within the meaning of the Society of Petroleum Engineer’s Petroleum Resource Management System or SEC rules and do not include any proved reserves. Actual quantities of reserves that may be ultimately recovered from the

Company’s interests may differ substantially from those presented herein. Factors affecting ultimate recovery include the scope of the Company’s ongoing drilling program, which will be directly affected by the availability of capital, decreases in oil and natural gas prices, drilling and production costs, availability of drilling services and equipment, drilling results, lease expirations, transportation constraints, processing costs, regulatory approvals, negative revisions to reserve estimates and other factors as well as actual drilling results, including geological and mechanical factors affecting recovery rates. Estimates of unproved reserves may change significantly as development of the Company’s assets provides additional data. In addition, our production forecasts and expectations for future periods are dependent upon many assumptions, including estimates of production decline rates from existing wells and the undertaking and outcome of future drilling activity, which may be affected by significant commodity price declines or drilling cost increases.

Investor Contacts

Gregory R. Hullinger Chief Financial Officer 713-623-0801

Al Petrie Investor Relations Coordinator 713-543-3422

Important Additional Information.In connection with the consent solicitation initiated by the Group 42-BLR Group, the Company may file a consent revocation statement and other documents regarding the proposals of the Group 42-BLR Group with the SEC and may mail a consent revocation statement and a consent revocation card to each stockholder of record entitled to deliver a written consent with respect to the proposals of the Group 42-BLR Group. STOCKHOLDERS ARE ENCOURAGED TO READ ANY CONSENT REVOCATION STATEMENT AND ANY OTHER RELEVANT DOCUMENTS FILED WITH THE SEC WHEN THEY BECOME AVAILABLE, BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. .The Company, its directors and executive officers may be deemed to be participants in the solicitation of consent revocations in connection with the proposals of the Group 42-BLR Group. Information regarding the names of the Company’s participants and their respective interests in the Company by security holdings or otherwise is set forth in the proxy statement for the Company’s 2015 Annual Meeting of Stockholders as filed with the SEC on Schedule 14A on April 16, 2015. To the extent names of the Company’s directors and executive officers and their holdings in the Company’s securities have changed since the 2015 proxy statement, such changes have been reflected on Initial Statements of Beneficial Ownership on Form 3 or Statements of Change in Ownership on Form 4 filed with the SEC. Additional information can also be found in the Company’s Annual Report on Form 10-K for the year ended December 31, 2014, filed with the SEC on March 16, 2015 and in the Company’s Quarterly Reports on Form 10-Q for the first two quarters of the fiscal year ending December 31, 2015 filed with the SEC on May 7, 2015 and August 6, 2015, respectively. Additional information regarding the interests of the Company’s participants in any solicitation of consent revocations in connection with the proposals of the Group 42-BLR Group and other relevant materials, if any, will be filed with the SEC when they become available. .These documents, including any consent revocation statement (and amendments or supplements thereto) and other documents filed by the Company with the SEC, are or will be available for no charge at the SEC’s website at www.sec.gov and at the Company’s investor relations website at vaalco.investorroom.com. Copies may also be obtained by contacting the Company by mail at 9800 Richmond, Suite 700, Houston, Texas 77042, Attention: Corporate Secretary or by telephone at (713) 623-0801.

Third Quarter and Recent Highlights.Grew total production 6% from 2Q 2015 to approximately 4,800 BOE per day, above the high end of 3Q 2015 guidance of 4,400 – 4,700 BOE per day .Successfully drilled and completed the North Tchibala 1-H well at a rate of 3,000 BOPD (750 Net), representing the first offshore Gabon production from the Dentale formation .Reduced production expense to $7.9 million, or $19.36 per BOE, in 3Q 2015 down significantly over the past year from $10.1 million, or $27.43 per BOE, in 4Q 2014, primarily due to cost reduction initiatives .Reported GAAP net loss of $33.7 million, or $0.58 loss per diluted share; Adjusted Net Loss(1) of $6.5 million, or $0.11 per diluted share .Reported 3Q 2015 Adjusted EBITDAX(1) of $8.2 million .Reported total liquidity of $108 million, before working capital adjustments .$58 million cash balance ($17 million in restricted cash included) .$50 million undrawn IFC facility 3

(1)Non-GAAP reconciliations located in Appendix

NYSE:EGY Net Base and Development Production 4,714 4,178 3,883 3,453 1,100 4,714 4,178 3,883 4,553 0 1,000 2,000 3,000 4,000 5,000 6,000 2012 2013 2014 2015YTD Q4 2015E Net BOE per day Base Production Development Drilling Increment

Total

4 (1)Midpoint of guidance range

(1)

~4,800

~1,800

~3,000

Development Drilling Program Successfully Increasing Production

NYSE:EGY

Offshore Gabon Net Liftings

0

100,000

200,000

300,000

400,000

500,000

600,000

Q12013

Q22013

Q32013

Q42013

Q12014

Q22014

Q32014

Q42014

Q12015

Q22015

Q32015

Q42015E

Net BO

2013 Lifting Average 390,000

2014 Lifting Average 340,000

2015E Lifting Average ~420,000

5

(2)

(1)Forecasted Q4 2015 lifting

2013 Lifting Average 390,000

2014 Lifting Average 340,000

2015E Lifting Average ~420,000

2015E Average Liftings Expected to Increase 24% vs. 2014

2015 Cost Reduction Initiatives

Net Production Expense

.Sustainable reductions driven by work efficiencies

•Helicopter Usage Reduction $1.1 million

•Marine Vessel Reduction $0.4 million

•Chemical programs $0.8 million

.Reductions in service and materials costs

.Workforce Realignment $0.8 million

.Marine Vessel Optimization $0.6 million

.Miscellaneous (vehicle rentals, consultants, etc.) $0.3 million

.Total Expected 2016 Net Production Expense Savings $4.0 million

Successfully Negotiated Reductions in Costs and Achieving Sustainable Reductions 6

Net Production Expenses

7

10.1

8.5 8.9

7.9

$27.43

$22.50

$19.08 $19.36

$-

$5.00

$10.00

$15.00

$20.00

$25.00

$30.00

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Q4 2014

Q1 2015

Q2 2015

Q3 2015

Q4 2015E

$/BOE of sales

$MM Production Expense

$/BOE

(2)

(1)

$16.50

$18.50

7.5- 8.5

Cost Reduction Initiatives Contributing to Decline in Production Expense per BOE (1)Q1 2015 excludes $1.4MM or $3.57/BOE related to the non-cash, non-recurring expensed costs for design work on a centralized processing facility.

(2)Q4 2015 guidance ranges

8

2015 Cost Reduction Initiatives

Net General & Administrative Expense

.Staffing and administrative cost reductions

.30% reduction in executive/management cash compensation

.15% reduction in corporate staff

.Reduction in contract, 3rd party services and travel costs

.2016 savings of ~$3 million due to management transition expenses

and employee separations

.G&A recapture from partners in 2016 will be impacted by lower

capital spend resulting in reduced overhead recapture rates

.Ultimate goal to reduce G&A costs incurred to be in line with pre

development program levels

Achieving Targeted Cost Reductions with Full Benefit Realized in 2016

Net General & Administrative Expense

Cost Reductions & Development Production Growth Contributing to

EBITDAX per BOE Despite Fall in Q3 2015 Realizations

Adjusted EBITDAX(1) per BOE of Sales

9

(1)Non-GAAP reconciliations located in Appendix, excludes Gabonese income taxes paid as a share of profit oil

(2)G&A excludes non cash compensation of $1.71/BOE, $1.64/BOE, $4.35/BOE and $1.46/BOE for Q3’15, Q2’15, Q1’15, Q4’14

(3)Excludes $3.57/BOE related to the non-cash, non-recurring expensed costs for design work on a centralized processing facility.

(4)Includes other expense/income of $3.10/BOE, ($0.35)/BOE, $0.01/BOE and $2.99/BOE for Q3’15, Q2’15, Q1’15, Q4’14

(5)Q3’15 Cash G&A excludes severance of $0.74/BOE

10

New SEENT Platform

.4 pile, 8 slot platform in water depth of 85 meters

.Targeting 7 MMBO gross 2P reserves

.Transocean “Constellation II” jackup rig

.SE Etame 2H

.Gamba development well online in July 2015

.Initial rate of 3,400 BOPD gross (900 net)

.No water or H2S

.North Tchibala 1H

.Dentale development well

online in September 2015

.Initial rate of 3,000 BOPD gross

(750 net)

.North Tchibala 2H

.Spud in Oct 2015

.Results expected by late November

11

Dentale Potential Across VAALCO Acreage

Etame Field

Main Fault Block

North Tchibala

South Tchibala

Dentale

Potential

12

Avouma Platform

Avouma and South Tchibala

Fields

Export Pipeline

Avouma and South Tchibala Fields

Discovery well completed August 2004

.Production commenced in January 2007

Two planned 4Q 2015 workovers to replace

failed ESPs in wells currently not producing

.Avouma 3-H

.South Tchibala 2-H

.Economics >100% IRR using forward strip

.One additional preventive maintenance

workover to replace failing ESPs

.Avouma 2-H

13

Additional Etame Drilling

Production(2): 5,000 – 5,400 BOEPD

Capital(3): $28mm - $33mm

Wells Drilled: 2

Minimal Etame Drilling

Production(2): 4,700 – 5,000 BOEPD

Capital(3): $20mm - $26mm

Wells Drilled: 1

No Etame Drilling

Production(2): 4,400 – 4,700 BOEPD

Capital(3): $14mm - $16mm

Wells Drilled: 0

2016 Possible Scenarios

14

Our Strategy is Directed Toward Lowering Costs, Economically Developing Production,

While Remaining Focused on Shareholder Value

Capital required under these scenarios forecasted to be within 2016E Cash Flow(1)

Possible 2016 Scenarios

(1)Assumes $55 dated Brent pricing and $5 differential in 2016

(2)Estimated production not intended to be guidance

(3)Includes un-utilized dayrate charges

14

Production (BOEPD) 4,400 – 4,700*

*4th Quarter Guidance 4,600 – 5,000

Production Expense(1) $33.0 - $34.0 MM*

($19.00 - $20.00 per BOE)

*4th Quarter Guidance $7.5 MM - $8.5 MM

($16.50 - $18.50 per BOE)

Workovers $6.0 - $9.0 MM*

*3 Planned 4th Quarter Workovers

Total G&A $15.0 - $16.0 MM

Cash G&A $11.5 - $12.0 MM

Non Cash G&A $3.5 - $4.0 MM

DD&A ($/Bbl) $19.00 - $22.00/Bbl*

*4th Quarter Guidance $20.00 - $22.00/Bbl

CAPEX $83.0 - $86.0 MM

(1) Excludes ~$1.4MM non-cash costs of centralized processing facility

NYSE:EGY

Appendix

16

Strong Financial Position

($’s in millions)

Liquidity 9/30/2015

Cash Balance (Includes $17MM Restricted) $ 58

Current Undrawn IFC Facility

50

Total Liquidity (Before Working Capital Adjustments)

108

3Q 2015 Financial Performance

Revenues

18

Operating Income (loss)

(32)

Tax Expense

(3)

Non-Cash Impairment

(18)

GAAP Net Loss

(34)

Adjusted Net Income (loss)(1)

6)

8

Basic Shares Outstanding 9/30/2015 (in millions)

58

3Q 2015 Earnings Per Share

$ (0.58)

3Q 2015 Adjusted Earnings Per Share

$ (0.11)

(1) See reconciliation

17

Non-GAAP Measures

Adjusted EBITDAX is a supplemental non-GAAP financial measure used by VAALCO’s management and by external users of the Company’s financial statements, such as industry analysts, lenders, rating agencies, investors and others who follow the industry as an indicator of the Company’s ability to internally fund exploration and development activities and to service or incur additional debt. Adjusted EBITDAX is a non-GAAP financial measure and as used herein represents net income before interest income (expense) net, income tax expense, depletion, depreciation and amortization, impairment of proved properties, exploration expense and our other non-cash or unusual items of stock compensation expense and allowance for bad debts. Adjusted EBITDAX has significant limitations, including that it does not reflect the Company’s cash requirements for capital expenditures, contractual commitments, working capital or debt service. Adjusted EBITDAX should not be considered as a substitute for net income (loss), operating income (loss), cash flows from operating activities or any other measure of financial performance or liquidity presented in accordance with GAAP. Adjusted EBITDAX excludes some, but not all, items that affect net income (loss) and operating income (loss) and these measures may vary among other companies. Therefore, the Company’s Adjusted EBITDAX may not be comparable to similarly titled measures used by other companies.

Adjusted Net Loss excludes impairments of proved properties, non-operational adjustments, including impairment of proved properties and exploration expense on the onshore Gabon Mutamba Iroru discovery. Management uses this financial measure as an indicator of the Company’s operational trends and performance relative to other oil and natural gas companies and believes it is more comparable to earnings estimates provided by securities analysts. Adjusted Net Income is not a measure of financial performance under GAAP and should not be considered a substitute for loss applicable to common stockholders. The tables below reconcile the most directly comparable GAAP financial measures to Adjusted EBITDAX and Adjusted Net Income.

18

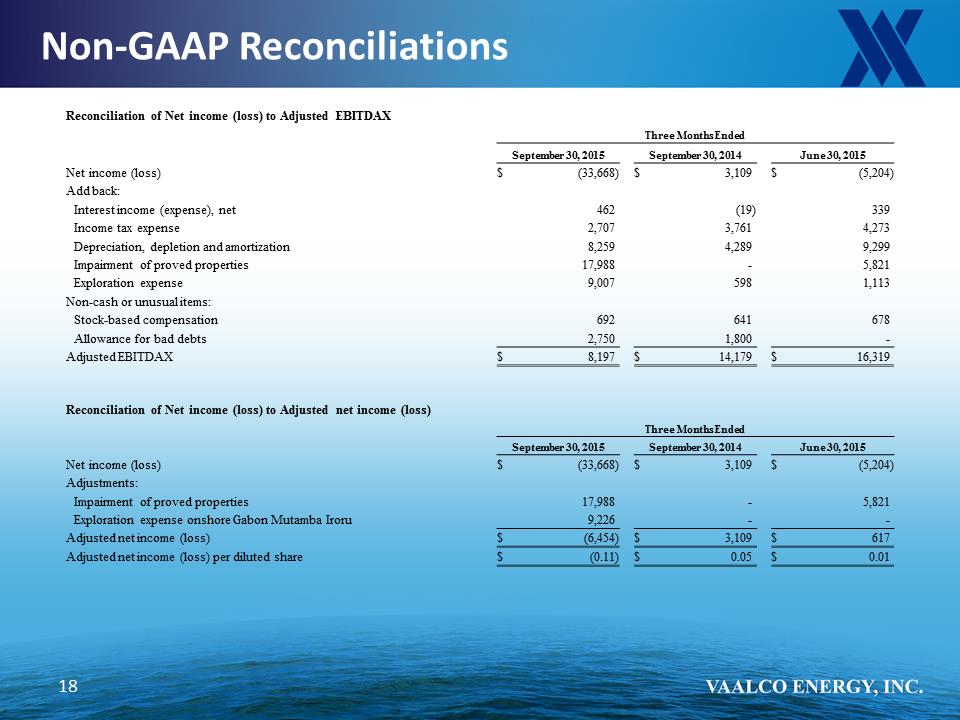

Non-GAAP Reconciliations

Three Months Ended September 30, 2015 September 30, 2014 June 30, 2015

Net income (loss)

$ (33,668)

5,204)

Add back:

Interest income (expense), net

462

(19)

339

Income tax expense

2,707

3,761

4,273

Depreciation, depletion and amortization

8,259

4,289

9,299

Impairment of proved properties

17,988

5,821

Exploration expense

9,007

598

1,113

Non-cash or unusual items:

Stock-based compensation

692

641

678

Allowance for bad debts

2,750

1,800

-

Adjusted EBITDAX

$ 8,197

$ 14,179

$ 16,319

Reconciliation of Net income (loss) to Adjusted net income (loss)

Three Months Ended

September 30, 2015

September 30, 2014

June 30, 2015

Net income (loss)

$ (33,668)

$ 3,109

$ (5,204)

Adjustments:

Impairment of proved properties

17,988

-

5,821

Exploration expense onshore Gabon Mutamba Iroru

9,226

-

-

Adjusted net income (loss)

$ (6,454)

$ 3,109

$ 617

Adjusted net income (loss) per diluted share

$ (0.11)

$ 0.05

$ 0.01