UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d) of the

Securities Exchange Act of 1934

Date of Report (Date of earliest event reported):

November 10, 2015

Wabash National Corporation

(Exact name of registrant

as specified in its charter)

| Delaware |

1-10883 |

52-1375208 |

| (State or other jurisdiction of incorporation) |

(Commission File No.) |

(IRS Employer Identification No.) |

| 1000 Sagamore Parkway South, Lafayette, Indiana 47905 |

| (Address of principal executive offices) (Zip Code) |

Registrant’s telephone number, including

area code:

(765) 771-5310

__________________

Not applicable

(Former name or former

address, if changed since last report)

Check the appropriate box below if the Form 8-K filing is intended

to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

| ¨ | Written communications pursuant to Rule 425 under the

Securities Act (17 CFR 230.425) |

| ¨ | Soliciting material pursuant to Rule 14a-12 under the

Exchange Act (17 CFR 240.14a-12) |

| ¨ | Pre-commencement communications pursuant to Rule 14d-2(b)

under the Exchange Act (17 CFR 240.14d-2(b)) |

| ¨ | Pre-commencement communications pursuant to Rule 13e-4(c)

under the Exchange Act (17 CFR 240.13e-4(c)) |

INFORMATION TO BE INCLUDED IN THE REPORT

Section 7 – Regulation FD

Item 7.01 Regulation FD Disclosure.

Wabash National Corporation

has prepared updated slides for use in connection with investor presentations. A copy of the slides is furnished as an exhibit

hereto and is incorporated herein by reference. This information shall not be deemed “filed” for purposes of Section

18 of the Securities Exchange Act of 1934, as amended, or otherwise subject to the liabilities of that section, and is not incorporated

by reference into any filing of Wabash National Corporation, whether made before or after the date of this report, regardless of

any general incorporation language in the filing.

Section 9 – Financial Statements and Exhibits

Item 9.01 Financial Statements and Exhibits.

| 99.1 | Wabash National Corporation slide presentation. |

SIGNATURES

Pursuant to the requirements of the Securities

Exchange Act of 1934, as amended, the registrant has duly caused this report to be signed on its behalf by the undersigned thereunto

duly authorized.

| |

|

WABASH NATIONAL CORPORATION |

| |

|

|

|

| |

|

|

|

| Date: November 10, 2015 |

|

By: |

/s/ Jeffery L. Taylor

Jeffery L. Taylor

Senior Vice President and Chief Financial Officer |

EXHIBIT INDEX

| Exhibit No. |

|

Description |

| |

|

|

|

|

| 99.1 |

|

Wabash National Corporation slide presentation |

Exhibit 99.1

WABASH NATIONAL CORPORATION Investor Update November 2015

2 This presentation contains certain forward - looking statements, as defined by the Private Securities Litigation Reform Act of 1995. All statements other than historical facts are forward - looking statements, including without limit, those regarding shipment outlook, Operating EBITDA, backlog, demand level expectations, profitability and earnings capacity, margin opportunities, and potential benefits of any recent acquisitions. Any forward - looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from those implied by the forward - looking statements. Without limit, these risks and uncertainties include economic conditions, increased competition, dependence on new management, reliance on certain customers and corporate partnerships, shortages and costs of raw materials, manufacturing capacity and cost containment risks, dependence on industry trends, access to capital, acceptance of products, and government regulation. You should review and consider the various disclosures made by the Company in this presentation and in its reports to its stockholders and periodic reports on Forms 10 - K and 10 - Q. We cannot give assurance that the expectations reflected in our forward - looking statements will prove to be correct. Our actual results could differ materially from those anticipated in these forward - looking statements. All written and oral forward - looking statements attributable to us are expressly qualified in their entirety by the factors we disclose that could cause our actual results to differ materially from our expectations. S AFE H ARBOR S TATEMENT © 2015 Wabash National, L.P. All rights reserved. Wabash®, Wabash National®, DuraPlate®, DuraPlate AeroSkirt®, Walker, Brenner® and Beall® are marks owned by Wabash National, L. P. Transcraft® and Benson® are marks owned by Transcraft Corporation.

3 S TRATEGIC S EGMENTS Wabash National Corporation Commercial Trailer Products 2014 Sales: $ 1.3B • Dry & Refrigerated Vans • Platform Trailers • Dry & Refrigerated Truck Bodies • Fleet Used Trailers Diversified Products 2014 Sales: $466M • Tank Trailers • Truck - Mounted Tanks • Aircraft Refueling Equipment • Composite Panels & Products • Aseptic Containment Systems • Dairy, Food and Beverage Equipment New Markets. New Innovation. New Growth. Retail 2014 Sales: $ 190M • 15 Retail Locations in U.S. • New & Used Trailer Sales • Parts & Service Segment Revenue is prior to the elimination of intersegment sales.

4 2014 S EGMENT R EVENUE AND P RODUCT M IX New Markets. New Innovation. New Growth. 2014 Consolidated Revenue: $1.86B

5 L EADING M ARKET P OSITIONS DPG End Markets CTP End Markets DPG Market Positions #1 All liquid transportation systems in North America #1 Stainless steel liquid tank trailers in North America (chemical and food markets) #1 Aircraft refuelers worldwide* #1 Isolators and downflow booths worldwide * #2 Stationary silos in the U.S. * * Based on industry estimates Note: All information based on 2014 revenues Sources for market positions: TTMA, ACT, Polk, Trailer Body Builders 2014 CTP Market Positions #1 Dry van trailers in North America #3 Refrigerated van trailers in North America #2 Platform trailers in North America* New Markets. New Innovation. New Growth.

6 2007 Higher Growth and Margin Profile, Less Cyclicality 2014 D IVERSIFICATION E FFORTS D RIVING R ESULTS Revenue Manufacturing Retail 14% 86% 24% Commercial Trailer Products Diversified Products Retail 66% 10% Operating Income Manufacturing Retail Diversified Products Commercial Trailer Products 39% 3 % 58% Gross Margin 0% 5% 10% 15% 20% 25% 8.1% 22.2% 10.9% 12.5% CTP Retail Consol. DPG 0% 5% 10% 15% 20% 25% 8.7% 6.3% 8.3% Mfg Retail Consol. $1.1B $1.9B $92M $233M 100% $26M $122M Growth > 69% > 153% > 362%

7 L ONG - T ERM G ROWTH D RIVERS ▪ Pricing discipline ▪ Operational efficiency / lean manufacturing ▪ Supply chain optimization Margin Expansion ▪ New end markets and geographies ▪ Product innovations / portfolio expansion ▪ Aftermarket p arts and s ervice capabilities Organic Growth ▪ Proven ability to acquire and integrate ▪ Enhance business stability and reduce cyclicality ▪ Operational synergies ▪ Strategic but selective Mergers & Acquisitions New Markets. New Innovation. New Growth.

8 S EGMENT G ROWTH I NITIATIVES New Markets. New Innovation. New Growth. CTP DPG Retail ▪ Bonded Technology ▪ DuraPlate ® Nose ▪ Integrated Logistics ▪ Roof and Sidewall ▪ High Strength Steel Coupler ▪ MaxClearance ™ Door System ▪ Heavy Duty Truck Bodies ▪ First Mile/Last Mile Focus ▪ Cold Chain Development ▪ Weight Reduction and Corrosion Resistance Through Advanced Materials ▪ Indirect Channel Development ▪ Transportation Related Aftermarket Parts ▪ International Market Development Innovation/Product Portfolio Growth Key Strategic Initiatives ▪ Lean Duplex Steel ▪ FRP Tank Trailers ▪ Mobile Clean Rooms ▪ Aerodynamic Solutions Portfolio ▪ Mobile Shelters/Portable Storage Units ▪ Freight Decking Systems ▪ LTL TruckBox ▪ Aluminum Trailer Growth Nationally ▪ Semiconductor Market Opportunities ▪ Commercial Cargo Trailer Market (towables) ▪ Silo Manufacturing Expansion ▪ Next Generation Composite Panels ▪ Mobile Service — Roadside ▪ Mobile Service — Customer Terminal ▪ Customer Site Service (asset lite) ▪ Product O ffering Expansion — Non - Wabash Equipment ▪ Tank Trailer Parts and Service Expansion ▪ Targeted N. American Expansion ▪ Local Market Competitiveness ▪ Expand Customer Site Service Offering

9 T RANSPORTATION S ECTOR O UTLOOK Strong demand above replacement levels ▪ Truck Tonnage at or near record levels ▪ Truck Loadings continue to rise ▪ Trucking Conditions outlook remains strong Positive Freight Trend and Trucking Conditions Trucking Indicators

10 ACT Forecast by Segment 2013 2014 2015 2016 2017 2018 2019 Dry Van 134,586 155,909 180,800 177,500 162,000 148,000 153,800 Refrigerated 35,879 38,616 45,600 41,000 37,500 38,000 40,000 Platform 22,122 25,749 31,700 27,500 28,200 24,000 23,000 Liquid Tanks 8,301 8,656 7,600 7,200 6,700 6,700 7,200 Dry Bulk Tanks 1,403 3,227 2,900 1,500 1,800 2,100 2,100 Other 32,071 36,589 38,900 36,400 38,500 39,200 37,900 Total 234,362 268,746 307,500 291,100 274,700 258,000 264,000 T RAILER S ECTOR O UTLOOK Strong demand above replacement levels Strong Demand Projected Throughout Forecast Period ▪ Strong demand above replacement levels forecast for next 5 years ▪ Fleet equipment dynamics and regulations key drivers of trailer demand ▪ ACT forecasts for 2016 – 2018 include anticipated federal regulations for 33' pups Trailer Forecasts

11 T RAILER D EMAND D RIVERS Strong demand above replacement levels Fleet Age and Regulations Driving Trailer D emand Fleet Equipment Dynamics ▪ Average age of equipment remains near record high ▪ 3 + years of significant underbuy (2008 - 2010) ▪ Improved access to financing ▪ Trailer population expected to return to 2007 levels mid - 2017; GDP up 20 % in same time period ▪ Hours of Service (HOS) ▪ Compliance, Safety, Accountability (CSA ) ▪ California Air Resources Board (CARB) ▪ Highway Trust Fund Bill Regulatory

12 T RAILER D EMAND D RIVERS Fleets Benefitting from Tight Capacity, Freight Volumes ▪ Active truck utilization expected to stay high for several years due to regulatory impact ▪ Truckload rates elevated ▪ Fleet profitability near record levels Carrier Operating Environment

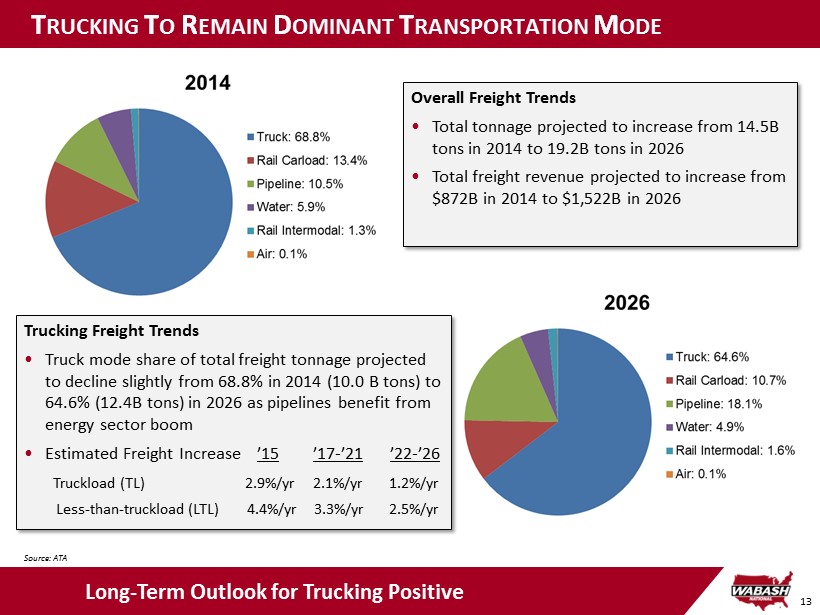

13 C OMMERCIAL T RAILER P RODUCTS T RUCKING T O R EMAIN D OMINANT T RANSPORTATION M ODE Long - Term Outlook for Trucking Positive Overall Freight Trends • Total tonnage projected to increase from 14.5B tons in 2014 to 19.2B tons in 2026 • Total freight revenue projected to increase from $872B in 2014 to $ 1,522B in 2026 Trucking Freight Trends • Truck mode share of total freight tonnage projected to decline slightly from 68.8% in 2014 (10.0 B tons) to 64.6% (12.4B tons) in 2026 as pipelines benefit from energy sector boom • Estimated Freight Increase ’15 ’17 - ’21 ’22 - ’26 Truckload (TL) 2.9%/yr 2.1%/yr 1.2%/yr Less - than - truckload ( LTL) 4.4%/yr 3.3%/yr 2.5%/yr Source: ATA

14 I NDUSTRY - W IDE T RAILER O RDER - TO - S HIPMENT C YCLE Order - to - Shipment Cycle Trends Show Distinct Seasonality Reflects Order - to - Shipment Cycles: 2010 - 2014 Source: ACT

15 M ARKET D EMAND D RIVERS ▪ Projected growth in Truck Body market drives DuraPlate® panel sales growth ▪ CARB compliance requirements continue to drive demand for aerodynamic products ▪ Housing starts support potential moving and storage growth and need for portable storage containers

16 S EGMENT O UTLOOK : D IVERSIFIED P RODUCTS ▪ Growing milk production supports demand for dairy silos, mixers and food - grade tank trailers ▪ Pharmaceutical R&D is expected to increase through 2018 ▪ Lower cost access to natural gas driving increased capital spending and output in the domestic chemical industry

17 S EGMENT O UTLOOK : D IVERSIFIED P RODUCTS ▪ World air passenger traffic is projected to steadily increase over the next 20 years ▪ World air cargo traffic is projected to more than double over the next 20 years RTK: Revenue Ton Kilometers (a single ton of goods that is transported for one kilometer) Source : Boeing, World Air Cargo Forecast 2014 - 2015

18 V ALUE P ROPOSITION New Markets. New Innovation. New Growth. Superior Product ▪ Leading producer of semi - trailers and liquid transportation systems for 14 of the past 21 years* ▪ Long history of innovation with over 200 patents ▪ Customer - focused solutions ▪ Products that revolutionize the trucking industry ▪ Designing for safety, efficiency and performance ▪ Lower total cost of ownership Operational Excellence ▪ Lean manufacturing expertise for more than 12 years ▪ Focus on continuous improvement ▪ Manufacturing optimization/velocity Customer Relationships ▪ Best - in - class quality and durability ▪ Proven reliability ▪ Dependable service and delivery ▪ Personal sales and service support ▪ Serve nearly half of the top 50 U.S. fleets Investment Thesis Strong Brands ▪ Blue Chip Customer Base Industry Leadership ▪ #1 in total trailer production ▪ #1 in dry van production ▪ #1 in tank trailer production Growth & Diversification ▪ Less risk of cyclicality ▪ More balanced across segments ▪ Leveraging synergies between businesses ▪ Diverse and expanded customer profile ▪ Margins expanding Solid Long - Term Forecast ▪ Trailer demand cycle remains strong Financial Discipline ▪ Record revenue, gross profit, operating income and operating EBITDA in 2014 ▪ Good stewards of capital ▪ Strong cash flow and liquidity ▪ Strong balance sheet * Source: Trailer Body Builders Magazine

19 2013 I NVESTOR D AY S TATED G OALS 2012 2013 2014 Stated Goals (3, 4) Revenue $1.5B $1.6B $1.9B > $ 2.0B Diversified Products Revenue (1) $321M (2) $459M (2) $466M (2) > $600M Consolidated Gross Margins 11.2% 13.2% 12.5% > 13% CTP Gross Margins 7.1% 7.8% 8.1% > 10% Operating EBITDA Margins 8.1% 9.2% 9.1% > 10% Net Leverage 3.1x 1.9x 1.2x < 2.0x Executing Against Our Strategic Plan x x x x x Notes: (1) Diversified Products segment revenues prior to eliminations (2) Adjusted for segment restructuring effective 2/27/15 (3) As established in May 2013 (4) Revenue goal is forecasted to be completed by 2015 YE

20 2020 G OALS 2014 2015 Consensus Consolidated Revenue $1.9B $2.0B Consolidated Operating Margin 6.6% 8.7% EPS Growth $0.89 $1.39 ROIC (1) 12.5% Notes: (1) ROIC = Net Operating Profit After Tax/Invested Capital Promises Delivered – Accelerating Diversification Strategy 2020 Goals > $3.0B > 10% > 20% > $2.50

WABASH NATIONAL CORPORATION Financial Overview

22 $338 $640 $1,187 $1,462 $1,636 $1,863 $2,011 $0 $300 $600 $900 $1,200 $1,500 $1,800 $2,100 12/09 12/10 12/11 12/12 12/13 12/14 9/15 ($ millions) F INANCIAL P ERFORMANCE Trailing Twelve Month (TTM) Revenue FY 2014 Revenue and Operating Income Set New Records ($ millions) Significantly improved financial results: ▪ TTM revenue exceeds $2.0B , up more than $ 1.6B since year end 2009 ▪ TTM Operating Income increases $ 226M since year end 2009 ▪ WNC Gross Margin levels approach 14% on TTM basis ▪ 2014 Financial Results – Record performance in Revenue, Gross Profit and Operating Income ▪ 2015 expected to be fourth consecutive record year TTM Operating Income and Gross Margin $(66) $(15) $20 $70 $103 $122 $160 - 6.8% 4.4% 5.6% 11.2% 13.2% 12.5% 13.8% -10.0% -5.0% 0.0% 5.0% 10.0% 15.0% $(100) $(50) $- $50 $100 $150 $200 12/09 12/10 12/11 12/12 12/13 12/14 9/15 Operating Income Gross Margin

23 F INANCIAL P ERFORMANCE TTM Operating EBITDA at $207M and Net Leverage of 0.7x Net Leverage Ratio Improved top - line and margins lead to: ▪ Record FY Operating EBITDA and year end liquidity in 2014 ▪ Cash generation leading to lower net debt leverage ($43) $5 $39 $119 $150 $169 $207 ($100) ($50) $0 $50 $100 $150 $200 $250 12/09 12/10 12/11 12/12 12/13 12/14 9/15 ($millions) (1) See Appendix for reconciliation of non - GAAP financial information TTM Operating EBITDA (1) Target Liquidity (2) (2) Defined as cash on hand plus available borrowing capacity on our revolving credit facility $21 $60 $126 $224 $254 $290 $366 $- $50 $100 $150 $200 $250 $300 $350 $400 12/09 12/10 12/11 12/12 12/13 12/14 9/15 ($ millions) 3.1 2.7 2.3 1.9 2.1 1.9 1.7 1.2 1.3 0.7 0 0.5 1 1.5 2 2.5 3 3.5 4 Q1 13 Q2 13 Q3 13 Q4 13 Q1 14 Q2 14 Q3 14 Q4 14 Q1 15 Q3 15 Leverage

24 • Share repurchases: $41M repurchased in 2015 YTD • $380M of acquisitions with Walker and Beall • Debt Profile: >$100M of debt reduction over past 3 years • Total Capital Expenditures: Approx. $75M Organic Growth Investment/ CapEX Debt Reduction Strategic Investment/ Acquisitions Liquidity C APITAL A LLOCATION : 2012 – 2015F Shareholder Return of Capital Share Repurchase/ Dividends

25 S TRATEGIC A CQUISITIONS 1. Value - added, engineered products and services, where we can provide value - added customer solutions 2. Operating Margins > 10% 3. Strong management teams that are a cultural fit 4. Aligned with core competencies in purchasing, operations, distribution and product development 5. Diversified growth markets ( end markets or geographies) and less cyclical industries » Tank Trailers » Process Systems » Aviation & Truck Equipment Transformative Acquisition Platform Expanding Acquisition » Aluminum 406 » Dry Bulk Tanks 2012 & 2013 Future Investment Criteria Growth Through Acquisition Remains a Strategic Component

26 F INANCIAL P ERFORMANCE – A DJUSTED EPS G ROWTH 2011 – 2015 Adjusted EPS CAGR is 78% a) 2011 Reported Non - GAAP EPS was $0.23 per diluted share Adjusted EPS as shown of $ 0.14 per diluted share has been tax effected @40% as the tax rate for 2011 was impacted by full valuation allowances on our NOLS. Adjustment made to enable comparisons to 2013 - 2015. b) 2012 Reported Non - GAAP EPS $0.95 per diluted share. Adjusted EPS as shown of $0.57 per diluted share has been tax effected @ 40% as WNC did not accrue for income tax expense in 2012. Adjustment made to enable comparisons to 2013 - 2015. c) 2015 represents the mid - point of WNC Non - GAAP EPS guidance as of 10/27/2015 ($1.38 - 1.43 per diluted share). ▪ 2015 is projected to be the fifth straight year of EPS growth ▪ 2011 - 2015 Adjusted EPS CAGR is 78% $0.14 $0.57 $0.70 $0.89 $1.41 22.8% 27.1% 58.4% 0% 10% 20% 30% 40% 50% 60% 70% $- $0.20 $0.40 $0.60 $0.80 $1.00 $1.20 $1.40 $1.60 2011ᵃ 2012ᵇ 2013 2014 2015F ᶜ Tax Impact Adjusted EPS (Left) YoY EPS Growth (Right) $0.95 $0.23

WABASH NATIONAL CORPORATION Appendix

28 Best - in - Class , Technologically Innovative Products Financial Performance ▪ 2014 New Trailer Shipments: 53,550 ▪ Comprehensive portfolio: dry vans, refrigerated vans, platform trailers, truck bodies ▪ Leading brands and long - standing customer relationships ▪ Industry leader in van and platform trailer manufacturing ▪ Mature practitioner of lean manufacturing methodology ▪ Long history of innovative solutions for customers S EGMENT P ROFILE : C OMMERCIAL T RAILER P RODUCTS Segment Revenue and OI are prior to the elimination of intersegment sales. Key Brands & Models -25 0 25 50 75 100 125 - 250 500 750 1,000 1,250 1,500 2010 2011 2012 2013 2014 Operating Income ($M) Revenue ($M) Revenue ($M) Op Income ($M)

29 CTP O RGANIC G ROWTH I NITIATIVES New Markets. New Innovation. New Growth. 2015 2016 2017 2018 2019 2020 ▪ Aftermarket Parts Distribution ▪ LTL Growth, Double Drops ▪ Reefer Truck Body ▪ Indirect Channel Growth ▪ Dry Truck Body ▪ 33’ Stretch ▪ Advanced Materials

30 L ONG - T ERM G ROWTH D RIVERS New Markets. New Innovation. New Growth. ▪ Align to serve “Final Mile” needs for Today and Beyond ▪ Configure Manufacturing for Efficiency and Capability ▪ Align Supply Chain for Further Optimization & New Market Needs ▪ Capture New Customers through New Channels Position for the Future ▪ Indirect Channel Growth & Development ▪ Aftermarket Part Manufacturing ▪ Trailer and Adjacent Markets Organic Growth ▪ Bringing the Next Wave of Change in Advanced Materials ▪ Redefine the Design and Manufacture of Equipment through Industry - Leading Bonding and Assembly Methods Leading Through Innovation

31 Diverse Products and End Markets Financial Performance Key Brands ▪ Divisions: Tank Trailers, Aviation & Truck Equipment, Process Systems, and Composites ▪ Diverse portfolio of products serving a variety of customers and attractive end markets ▪ Leading brands and long - standing relationships with blue - chip customer base ▪ Higher growth and higher margin businesses ▪ Stable, strong cash flow profile S EGMENT P ROFILE : D IVERSIFIED P RODUCTS Segment Revenue and OI are prior to the elimination of intersegment sales. 0 15 30 45 60 75 90 - 100 200 300 400 500 600 2010 2011 2012 2013 2014 Operating Income ($M) Revenue ($M) Revenue ($M) Op Income ($M)

32 2015 O RGANIZATIONAL S TRUCTURE AND BRANDS Composites Tank Trailer Aviation & Truck Equip. Process Systems Wabash National Corporation Commercial Trailer Products Diversified Products Retail Strategically Focused & Rationalized Brands

33 Strong Platforms for Growth DPG – B USINESS P ROFILES Diversified Products Group Tank Trailers 53% of Total • Chemical • Sanitary • Refined Fuel • Crude Oil • Corrosive Materials • Asphalt • Agriculture • Dry Bulk • Used Trailers • Parts Aviation & Truck Equip. Process Systems Composites 12% of Total • Aircraft Refuelers • Hydrant Servicers • Hydrant Carts • Above Ground Storage Systems • Refined Fuel Trucks • Vacuum Trucks • Propane Trucks • Refurbished Equip. • Parts & Service 15% of Total • Composite Panels • Aerodynamic Devices • Portable Storage Containers • Custom Solutions • Parts 20% of Total • Silos • Stationary Tanks • Processors & Mixers • Isolators • Downflow Booths • Mobile Clean Rooms • Tank Heads • Custom Equipment • Field Service • Parts Business Revenues as a % of DPG Total based on 2014 Revenue

34 Sanitary Trailer Refined Fuel Truck Processor Downflow Booth Isolator Aircraft Refueler Dry Bulk Sand Trailer Vertical Silos Above Ground Storage Tanks Mobile Clean Room Hydrant Cart FRP Corrosives Trailer Lift & Hoist Vacuum Truck Refined Fuel Truck & Pull Chemical Trailer Truck Body Panels AeroSkirt ® Truckbox Deck Systems Portable Storage Container DPG – P RODUCT O VERVIEW Tank Trailers Process Systems Aviation & Truck Equip. Composites

35 DPG O RGANIC G ROWTH I NITIATIVES New Markets. New Innovation. New Growth. 2015 2016 2017 2018 2019 2020 ▪ Aluminum Trailer Growth Nationally ▪ MCR Product Line Expansion ▪ Aerodynamic Products Portfolio Growth ▪ LTL Truck Boxes ▪ Mexico Silo Growth ▪ Custom Tank Container Solutions ▪ Energy Related Products ▪ Custom Cargo Boxes ▪ Processing Equipment (Food, Dairy, Pharma) ▪ Next Generation Composite Panels

36 Company - Owned Retail Locations Strategic Footprint Providing National Support Financial Performance ▪ Dealership model, selling new and used trailers, aftermarket parts, and maintenance and repair services ▪ Integrated with OEM to deliver best practices and innovation in the aftermarket ▪ Expansion into new markets with mobile service and 3rd party maintenance ▪ Low CapEx and synergistic expansion in higher - margin tank parts and service S EGMENT P ROFILE : R ETAIL Tank Services Segment Revenue and OI are prior to the elimination of intersegment sales. -2 0 2 4 6 - 50 100 150 200 2010 2011 2012 2013 2014 Operating Income ($M) Revenue ($M) Revenue ($M) Op Income ($M)

37 R ETAIL G ROWTH I NITIATIVES New Markets. New Innovation. New Growth. ▪ Build Initial Customer Site Service Footprint ▪ Leverage Tank & Trailer Combined Footprint ▪ Expand Mobile Service Fleet ▪ Accelerate Tank Parts & Service Sales Growth ▪ Expand Customer Site Service Offering 2015 2016 2017 2018 2019 2020

38 K EY C USTOMERS Large and Diverse Customer Profile Commercial Trailer Products Diversified Products Group

39 C ONSOLIDATED E ND M ARKETS Note: All information based on 2014 revenues New Markets. New Innovation. New Growth.

40 C ONSOLIDATED I NCOME S TATEMENT New Markets. New Innovation. New Growth. ($ in thousands, except per share amounts) 2009 2010 2011 2012 2013 2014 YTD Q3 2015 Net sales 337,840$ 640,372$ 1,187,244$ 1,461,854$ 1,635,686$ 1,863,315$ 1,483,778$ Cost of sales 360,750 612,289 1,120,524 1,298,031 1,420,563 1,630,681 1,268,153 Gross profit (22,910)$ 28,083$ 66,720$ 163,823$ 215,123$ 232,634$ 215,625$ % of sales -6.8% 4.4% 5.6% 11.2% 13.2% 12.5% 14.5% General and administrative expenses 29,033 29,876 30,994 44,751 58,666 61,694 53,758 % of sales 8.6% 4.7% 2.6% 3.1% 3.6% 3.3% 3.6% Selling expenses 11,176 10,669 12,981 23,589 30,597 26,676 20,216 % of sales 3.3% 1.7% 1.1% 1.6% 1.9% 1.4% 1.4% Amortization of intangibles 2,955 2,955 2,955 10,590 21,786 21,878 15,945 % of sales 0.9% 0.5% 0.2% 0.7% 1.3% 1.2% 1.1% Acquisition expenses - - - 14,409 883 - - % of sales 0.0% 0.0% 0.0% 1.0% 0.1% 0.0% 0.0% - - - - - - (Loss) Income from operations (66,074)$ (15,417)$ 19,790$ 70,484$ 103,191$ 122,386$ 125,706$ % of sales -19.6% -2.4% 1.7% 4.8% 6.3% 6.6% 8.5% Other income (expense) Increase in fair value of warrant (33,447) (121,587) - - - - - Interest expense (4,379) (4,140) (4,136) (21,724) (26,308) (22,165) (14,759) Other, net (866) (667) (441) (97) 740 (1,759) 2,500 (Loss) Income before income taxes (104,766)$ (141,811)$ 15,213$ 48,663$ 77,623$ 98,462$ 113,447$ Income tax (benefit) expense (3,001) (51) 171 (56,968) 31,094 37,532 42,445 Net (loss) income (101,765)$ (141,760)$ 15,042$ 105,631$ 46,529$ 60,930$ 71,002$ Preferred stock dividends and early extinguishment 3,320$ 25,454$ -$ -$ -$ -$ -$ Net (loss) income applicable to common stockholders (105,085)$ (167,214)$ 15,042$ 105,631$ 46,529$ 60,930$ 71,002$ Diluted net (loss) income per share (3.48)$ (3.36)$ 0.22$ 1.53$ 0.67$ 0.85$ 1.01$

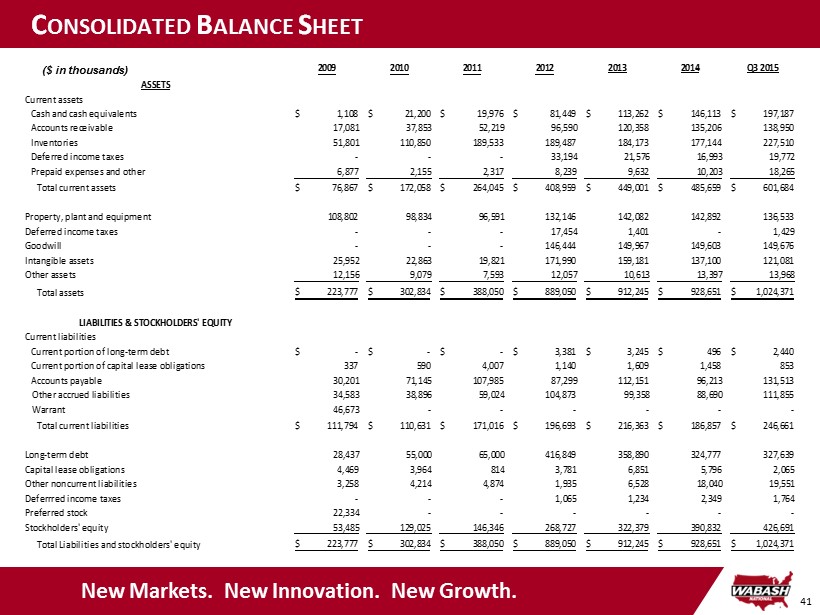

41 C ONSOLIDATED B ALANCE S HEET New Markets. New Innovation. New Growth. ($ in thousands) 2009 2010 2011 2012 2013 2014 Q3 2015 ASSETS Current assets Cash and cash equivalents 1,108$ 21,200$ 19,976$ 81,449$ 113,262$ 146,113$ 197,187$ Accounts receivable 17,081 37,853 52,219 96,590 120,358 135,206 138,950 Inventories 51,801 110,850 189,533 189,487 184,173 177,144 227,510 Deferred income taxes - - - 33,194 21,576 16,993 19,772 Prepaid expenses and other 6,877 2,155 2,317 8,239 9,632 10,203 18,265 Total current assets 76,867$ 172,058$ 264,045$ 408,959$ 449,001$ 485,659$ 601,684$ Property, plant and equipment 108,802 98,834 96,591 132,146 142,082 142,892 136,533 Deferred income taxes - - - 17,454 1,401 - 1,429 Goodwill - - - 146,444 149,967 149,603 149,676 Intangible assets 25,952 22,863 19,821 171,990 159,181 137,100 121,081 Other assets 12,156 9,079 7,593 12,057 10,613 13,397 13,968 Total assets 223,777$ 302,834$ 388,050$ 889,050$ 912,245$ 928,651$ 1,024,371$ LIABILITIES & STOCKHOLDERS' EQUITY Current liabilities Current portion of long-term debt -$ -$ -$ 3,381$ 3,245$ 496$ 2,440$ Current portion of capital lease obligations 337 590 4,007 1,140 1,609 1,458 853 Accounts payable 30,201 71,145 107,985 87,299 112,151 96,213 131,513 Other accrued liabilities 34,583 38,896 59,024 104,873 99,358 88,690 111,855 Warrant 46,673 - - - - - - Total current liabilities 111,794$ 110,631$ 171,016$ 196,693$ 216,363$ 186,857$ 246,661$ Long-term debt 28,437 55,000 65,000 416,849 358,890 324,777 327,639 Capital lease obligations 4,469 3,964 814 3,781 6,851 5,796 2,065 Other noncurrent liabilities 3,258 4,214 4,874 1,935 6,528 18,040 19,551 Deferrred income taxes - - - 1,065 1,234 2,349 1,764 Preferred stock 22,334 - - - - - - Stockholders' equity 53,485 129,025 146,346 268,727 322,379 390,832 426,691 Total Liabilities and stockholders' equity 223,777$ 302,834$ 388,050$ 889,050$ 912,245$ 928,651$ 1,024,371$

42 C ONSOLIDATED C ASH F LOWS New Markets. New Innovation. New Growth. ($ in thousands) 2009 2010 2011 2012 2013 2014 YTD Q3 2015 Cash flows from operating activities Net (loss) income (101,765)$ (141,760)$ 15,042$ 105,631$ 46,529$ 60,930$ 71,002$ Adjustments to reconcile net (loss) income to net cash (used in) provided by operating activities Depreciation 16,630 13,900 12,636 14,975 16,550 16,951 12,514 Amortization of intangibles 2,955 2,955 2,955 10,590 21,786 21,878 15,945 Net (gain) loss on the sale of assets (55) 431 (9) 203 140 13 (8,315) Loss on debt extinguishment 303 - 668 - 1,889 1,042 5,620 Deferred income taxes - - - (55,292) 30,089 16,573 (4,772) Increase in fair value of warrant 33,447 121,587 - - - - - Stock-based compensation 3,382 3,489 3,398 5,149 7,480 7,833 6,655 Accretion of debt discount - - - 2,972 4,643 4,840 3,366 Changes in operating assets and liabilities Accounts receivable 20,845 (20,772) (14,366) 1,180 (23,691) (14,848) (3,744) Inventories 41,095 (59,062) (78,683) 41,696 6,260 3,116 (50,366) Prepaid expenses and other (1,570) 3,024 (162) 736 (3,893) (571) (2,704) Accounts payable and accrued liabilities (22,666) 45,251 56,968 (48,777) 18,082 (26,787) 58,465 Other, net 420 650 386 (3,046) 2,805 1,665 1,025 Net cash (used in) provided by operating activities (6,979)$ (30,307)$ (1,167)$ 76,017$ 128,669$ 92,635$ 104,691$ Cash flows from investing activities Capital expenditures (981) (1,782) (7,264) (14,916) (18,352) (19,957) (12,554) Acquisition, net of cash acquired - - - (364,012) (15,985) - - Proceeds from the sale of property, plant and equipment 300 1,813 17 607 305 87 13,180 Other - - - (2,500) 2,500 4,113 (5,358) Net cash (used in) provided by investing activities (681)$ 31$ (7,247)$ (380,821)$ (31,532)$ (15,757)$ (4,732)$ Cash flows from financing activities Proceeds from issuance of common stock, net of expenses - 71,948 (155) - - - - Proceeds from exercise of stock options - 504 538 354 600 1,921 1,959 Borrowings under revolving credit facilities 276,853 712,491 848,705 206,015 1,166 806 665 Payments under revolving credit facilities (328,424) (685,928) (838,705) (271,015) (1,166) (806) (613) Principal payments under capital lease obligations (334) (352) (671) (1,629) (1,700) (1,898) (3,964) Principal payments under term loan credit facility - - - (2,250) (62,827) (42,078) (193,809) Principal payments under industrial revenue bond - - - - (381) (475) (370) Stock repurchase (35) (384) (533) (564) (35) (1,497) (43,017) Proceeds from issuance of convertible senior notes - - - 145,500 - - - Proceeds from issuance of term loan credit facility, net of issuance costs - - - 292,500 - - 192,845 Proceeds from issuance of preferred stock and warrant 35,000 - - - - - - Payments under redemption of preferred stock - (47,791) - - - - - (1,420) - (1,989) (5,134) (981) - (2,581) - - - 2,500 - - - (2,638) (120) - - - - - Net cash (used in) provided by financing activities (20,998)$ 50,368$ 7,190$ 366,277$ (65,324)$ (44,027)$ (48,885)$ Net (decrease) increase in cash and cash equivalents (28,658)$ 20,092$ (1,224)$ 61,473$ 31,813$ 32,851$ 51,074$ Cash and cash equivalents at beginning of period 29,766 1,108 21,200 19,976 81,449 113,262 146,113 Cash and cash equivalents at end of period 1,108$ 21,200$ 19,976$ 81,449$ 113,262$ 146,113$ 197,187$ Preferred stock issuance costs paid Debt amendment and issuance costs paid Proceeds from issuance of industrial revenue bond

43 R ECONCILIATION OF N ON - GAAP M EASURES New Markets. New Innovation. New Growth. ($ in millions) Note: This table reconciles annual net income (loss) for the periods presented to the non - GAAP measure of Operating EBITDA. Di fferences may exist in the calculation of Operating EBITDA due to rounding. 2009 2010 2011 2012 2013 2014 TTM Q3 2015 Net (loss) income (101.8)$ (141.8)$ 15.0$ 105.6$ 46.5$ 60.9$ 90.1$ Income tax (benefit) expense (3.0) (0.1) 0.2 (57.1) 31.1 37.5 52.1 Increase in fair value of warrant 33.4 121.6 - - - - - Interest expense 4.4 4.1 4.1 21.7 26.3 22.2 20.0 Depreciation and amortization 19.6 16.9 15.6 25.6 38.3 38.8 38.1 Stock-based compensation 3.4 3.5 3.4 5.2 7.5 7.8 9.0 Acquisition expenses - - - 17.3 0.9 - - Other non-operating expense (income) 0.9 0.7 0.5 0.2 (0.7) 1.8 (2.4) Operating EBITDA (43.1)$ 4.9$ 38.8$ 118.5$ 149.9$ 169.0$ 207.0$ % of sales -12.8% 0.8% 3.3% 8.1% 9.2% 9.1% 10.8%

44 R ECONCILIATION OF N ON - GAAP M EASURES Note: This table reconciles annual net income for the periods presented to the non - GAAP measure of adjusted earnings and adjust ed earnings per share. Differences may exist in the calculation of adjusted earnings per share due to rounding. $ Per Share $ Per Share $ Per Share $ Per Share Net income 15,042$ 0.22$ 105,631$ 1.54$ 46,529$ 0.67$ 60,930$ 0.86$ Income tax benefit, net - - (58,991) (0.86) - - - - Loss on debt extinguishment, net of taxes 668 0.01 - - 1,132 0.02 645 0.01 Impact of acquired profit in inventories and short term intangible amortization - - 3,800 0.06 - - - - Revaluation of net deferred income tax assets due to changes in statutory tax rates - - - - - - 1,041 0.01 Acquisition expenses, net of taxes - - 14,409 0.21 529 0.01 - - Loss on transitioning Retail branch locations, net of tax - - - - - - 376 0.01 Adjusted Earnings and Adjusted Earnings Per Share 15,710$ 0.23$ 64,849$ 0.95$ 48,190$ 0.70$ 62,992$ 0.89$ WA shares outstanding 68,418 68,564 69,081 71,063 2011 2012 2013 2014 Twelve Months Ended December 31,

45 Hypothetical Quarterly Average Share Price (NYSE: WNC) (1) Potential Incremental Shares for Diluted EPS (in 000s shares) (2) 11.50$ - 12.00$ 316 12.50$ 816 13.00$ 1,277 13.50$ 1,704 14.00$ 2,101 14.50$ 2,471 15.00$ 2,816 15.50$ 3,138 16.00$ 3,441 16.50$ 3,725 17.00$ 3,992 17.50$ 4,244 18.00$ 4,482 18.50$ 4,707 19.00$ 4,921 19.50$ 5,123 20.00$ 5,316 20.50$ 5,499 21.00$ 5,673 21.50$ 5,839 22.00$ 5,997 22.50$ 6,149 23.00$ 6,294 23.50$ 6,433 24.00$ 6,566 P OTENTIAL D ILUTIVE I MPACT OF S ENIOR C ONVERTIBLE N OTES (UNAUDITED) Table below illustrates the potential dilutive shares that would be included in the calculation of the Company’s reported earnings per share in a future period assuming various hypothetical quarterly average market prices for the Company’s stock (NYSE: WNC). The table should only be considered for illustrative purposes and does not represent the Company’s estimates for future stock performances. Notes: (1) The share prices listed in this table are for illustrative purposes only. Dilution will continue beyond $24.00 per share. (2) This represents the number of shares to be used for calculating diluted earnings per share in accordance with generally accepted accounting principals. Background Information: » In April 2012, the Company issued Convertible Senior Notes due 2018 with a principal amount of $150 million principal and bear interest at a rate of 3.375% annually » Initial conversion rate of 85.4372 shares of common stock per $1,000 in principal amount which is equal to a conversion price of approximately $11.70 per share » The Senior Notes will have a dilutive effect on earnings per share to extent average quarterly share price exceeds the conversion price » The Company’s intent is to settle conversions through a net share settlement which involves repayment of cash for the principal amount and delivery of shares of common stock for any excess of conversion value over principal amount

Wabash National (NYSE:WNC)

Historical Stock Chart

From Mar 2024 to Apr 2024

Wabash National (NYSE:WNC)

Historical Stock Chart

From Apr 2023 to Apr 2024